Failure data from ADP, ECB decision & BoA warnings Primarily the data on the US labor market from ADP was remembered yesterday. The number of jobs in private companies in the US in May increased by 27K (the forecast was + 180K). The figures are frankly failing and extremely alarming, given that official statistics from the US Department of Labor will be published on Friday.

The dollar was one of the first victims of such data. Such a negative reaction is due to two main factors. Firstly, the US economy clearly signals problems, and secondly, such data is a reason for the Fed to establish itself in the expediency of reducing rates. Naturally, both of these factors are extremely negative for the dollar.

Well, at the end of the day, the dollar managed to recover. One of the reasons was the publication of pretty good data on business activity indices. Secondly, there is, of course, a chance that Friday's labor market data will not disappoint. Nevertheless, we continue to recommend looking for points for dollar sales.

The key event will be the announcement of the ECB meeting decision. Monetary policy parameters are likely to remain unchanged, but forecasts for economic growth will be revised downwards. In addition, weak Eurozone inflation data, published this week, led to the fact that the markets no longer expected to tighten monetary policy in the foreseeable future, and now they are waiting for its further softening. In particular, traders assume a 0.1% reduction in the rate by July of next year.

This is definitely a bearish signal for the euro, so today we will refrain from recommending to buy euros. Well, or at least make it from very attractive points.

Meanwhile, analysts are continuing to analyze the of a trade war possible consequence. The Bank of America experts named a number of possible scenarios for the situation development (between the USA and China). In particular, China’s exit from US public debt, delisting of Chinese ADRs, the exodus of American investors from the Chinese market, which is fraught with stock and bond sales on the markets, Chinese IPOs could lose access to the American financial market, and finally, countries could start a full-fledged currency war. So to the question “Could the situation become worse?” The answer is unequivocal “could.”

Our position for today: we will continue to look for points for selling of the US dollar, sales of oil and the Russian ruble, as well as buying of gold and the Japanese yen. In addition, we will sell the Australian dollar against the US dollar.

ADP

The Bank of England, the problems of the ruble & NFPThe Bank of England left the monetary policy parameters unchanged as we expected. Since this decision was included in the price, all the attention of traders was focused on the comments of the Central Bank and its head. The Bank of England raised its economic growth forecast (up to 1.5% of GDP growth) but warned that the situation with Brexit “darkens” the future for monetary policy. At the same time, the Members of the Monetary Policy Committee of the Bank of England support the view that the Central Bank will require a more stringent policy. However, the markets were not that impressed with such rhetoric of the Central Bank and the pound for the day suffered losses.

Today, all the attention of the markets will be focused on data on the US labor market. In view of the pause in the Fed's actions, it is the figures of the NFP that will shape the market expectations for the future actions of the Central Bank.

Recall, last month the data turned out to be quite good + 196K and the dollar buyers could breathe out with relief after the devastating February data (the NFP was only + 30K). Good numbers are also expected this time - + 180K. This figure fully coincides with the average value of the NFP over the past two years. This means that data will almost certainly differ from forecasts. The question is this number will be worse than predicted or better.

In our opinion, there are reasons to expect an excess with a “+” sign. These thoughts are pushed by numbers from ADP (on Wednesday, the data showed an increase of 275K with a forecast of 180K). The level of correlation between these indicators is low, but they still characterize, by and large, the same thing. In addition, the US GDP figures for the first quarter, albeit with some assumptions, “insist” in a positive way.

So today we will buy a dollar. Another motivation for this is the results of research by analysts JPMorgan Chase, who conducted a retrospective analysis of the dollar behavior over the past 10 years. So, in May, the dollar index grew 8 times. For the American currency, this is the strongest month of the year.

The Russian ruble showed the worst results in the foreign exchange market yesterday. So those of our readers who listen to our recommendations should have earned good money. The reasons for the current sales of the ruble on the surface - the decline in oil prices and fears of new sanctions from the US. As for the deeper, fundamental foundations, we wrote about them earlier in our previous reviews.

About the oil market. Here our readers could earn even more. Russia published data on oil production in April. The country has again failed to meet the conditions of OPEC +. And this is despite the fact that Alexander Novak. Minister of Energy of the Russian Federation, swore an oath that the country would fulfill the terms of the deal. The problem is not in additional volumes of oil that Russia releases to the market (they are insignificant, about 40-50K b / d). But that Russia is not fulfilling the agreement.

If other members of OPEC + start following a similar strategy, then in June the agreement may well not be extended. And this could potentially lead to the appearance on the market of 1.2 million b / d of additional oil supply. That, naturally, will be the strongest blow to the oil quotes. So the current decline is far from the limit. We continue to monitor the situation on the oil market. In the light of such events and market sentiments, today we will also look for points for asset sales.

FOMC results, what to expect from the Bank of England & ADPThe announcement of the Federal Open Market Committee (FOMC) Fed meeting results was the main event. As we expected parameters of monetary policy were left unchanged. As for the comments, the Fed has been extremely positive about what is happening in the US economy recently. At the same time, the Central Bank noted weak inflation indicators, which were perceived by the markets as a “pigeon” position. Recall that the Fed simply does not have any reason to raise the rate with weak inflation. And that means that the pause in the rate increase will be delayed or the rate might be lowered, to intensify the inflation processes in the country. Nevertheless, the lack of any mention of the fall on the part of the Fed possibility perceived the markets as a signal for buying the dollar, which, by the end of the day, somehow compensated previous losses. Our position is still unchanged - we continue to look for the dollar selling points today.

About the dollar news. Publication of statistics on US employment from ADP was another important news. The data came out surprisingly good: + 275K jobs (forecast was + 180K). Recall that this Friday we are waiting for official statistics on the US labor market. If the figures for the NFP are somewhere in this area, it can greatly help the dollar, which is experiencing serious problems this week. But in more details, we will talk about this tomorrow.

The meeting of the Bank of England is on focus today. To begin with, as in the case of the Fed, we do not expect any changes in the Great Britain monetary policy parameters. In addition to the factors that put pressure on both the Fed and the Bank of England (the threat of a slowdown in global economic growth and a possible transition to the recession stage), the Central Bank of England has one more even greater problem - Brexit. While there is no clarity on this issue, the risks of the chaotic exit of Britain from the EU are great, and this promises a very serious level of uncertainty and potential damage to the economy. To loosen the boat in such conditions, the Central Bank simply has no right. So today we do not expect surprises from the Bank of England. As for buying the pound, after the strong growth in the last couple of days, the results of the Bank of England meeting may well be perceived as a reason for the local correction. So today we are more likely to sell pounds than to buy it.

According to the Ministry of Energy report, oil production in the United States increased by 100 thousand to 12.3 million barrels per day, which is a new absolute record. At the same time, oil reserves in the US unexpectedly rose sharply (by +9.93 million, with a forecast +1.47 million). These are pretty strong bearish signals. So today we will look for points for oil sales.

Our positions for today are as follows: we will continue to look for points for selling the dollar against the euro, as well as the Australian and Canadian dollars. In addition, we will buy gold, as well as sell oil and the Russian ruble on the intraday basis.

ADP: CD leg commencing downside target $128, -12%Market is turning bearish again and ADP looks like it has completed a counter-trend rally to the 78.6% retracement level. ABCD downside projection of $128, -c.12% with stops placed within 3% of current price; 4:1 risk reward ratio.

How should we interpret yesterday's ADP data?We continue to prepare our followers to the most important event of the week or probably even of a month - labor market statistics of the USA.

Yesterday, traditionally, a couple of days before official statistics, data from the ADP Research Institute on the level of employment in the private sector were published. Recall, analysts had expected growth rate at 187K. We noted that considering the current form of the US economy, we should expect the fact to exceed the forecast. Actually, the way it turned out - the data came out much better than analysts' expectations and amounted to +227K. This is a great indicator that confirms the fact that the US labor market is in the best form over the last 10 years.

Is it worth it to extrapolate these figures on Friday data on NFP? In yesterday's review, we noted that the level of correlation between data on ADP and NFP is about 25%. So the chances that the coincidence will be intense are not so high (about ¼).

We provide some statistical data (see table below).

Date ADP NFP delta

7.2017 158 222 64

8.2017 178 209 31

9.2017 237 156 -81

10.202 135 -33 -168

11.202 235 261 26

12.202 190 228 38

1.2018 250 148 -102

2.2018 234 200 -34

3.2018 235 313 78

4.2018 241 103 -138

5.2018 204 164 -40

6.2018 178 223 45

7.2018 177 213 36

8.2018 219 157 -62

9.2018 163 201 38

10.202 230 134 -96

As we can see, data on ADP and NFP usually differ significantly. On average, ADP comes out 30K better than NFP data. Tellingly, periods of the excess of ADP over NFP are replaced by an excess of NFP over ADP. That is, it is a high probability that this time (this Friday), the ADP numbers will be worse than the NFP (last month they were much better).

This means that we may fully expect the NFP growth not at 190K, as analysts expect, but at 250-260K. And although the forecast seems quite optimistic, we consider it is realistic, especially given that after the end of the hurricane season, the demand for labor usually increases sharply.

Our recommendations on the dollar are unchanged in this light - looking the points for the dollar purchases.

ADP data and dollar responseThe dollar is exclusively strong in the foreign exchange market so far. Consistent with an old rule “trend is your friend”, core strategy in current conditions should be purchases of the dollar. But, as we know, fundamental factors may break trends. Therefore, it is necessary to monitor the fundamental background for threatening the dollar. The nearest on the horizon - statistics on the US labor market.

On Friday we will get the most important block of macroeconomic statistics from the USA. Referring to the data on the number of new jobs created outside of agricultural (so-called NFP - Non-farm Payrolls), unemployment rate, as well as the average hourly wage. We will discuss Friday’s data in more detail tomorrow and the day after tomorrow. Today let’s just leave on the ADP report on the level of employment in the private sector. If Friday's statistics are official data from the US Department of Labor, then unofficial data from the ADP Research Institute will be published today.

Let’s start with that even though ADP and NFP formally display similar statistics, their value rarely coincides even at the level of basic trends. Actually, the level of correlation between them in the last 3 years is about 25%. That is, only in 1 case out of four, the trends in these indicators coincide.

In this light, making any final conclusions based on data from the ADP would be clearly premature. Nevertheless, data may well influence the traders' sentiments.

Analysts' forecasts for data from ADP are very optimistic. About 190K. And although this is slightly lower than the value in the past period, the figure itself is excellent and is quite close to the average value of 204K over the last couple of years. Since the hurricane season is over, and the US economy, according to the latest figures for GDP, continues to be in excellent shape, we see no reason for failure. Rather, on the contrary, average analyst forecasts give space for a positive surprise.

Overall, our expectations from today's and Friday statistics are generally positive, so we recommend buying the dollar. The motivation for this recommendation: the total positive position of the dollar in the foreign exchange market, as well as the excellent shape of the US labor market (according to some indicators, this is a record value since the 60s of the XXth century).

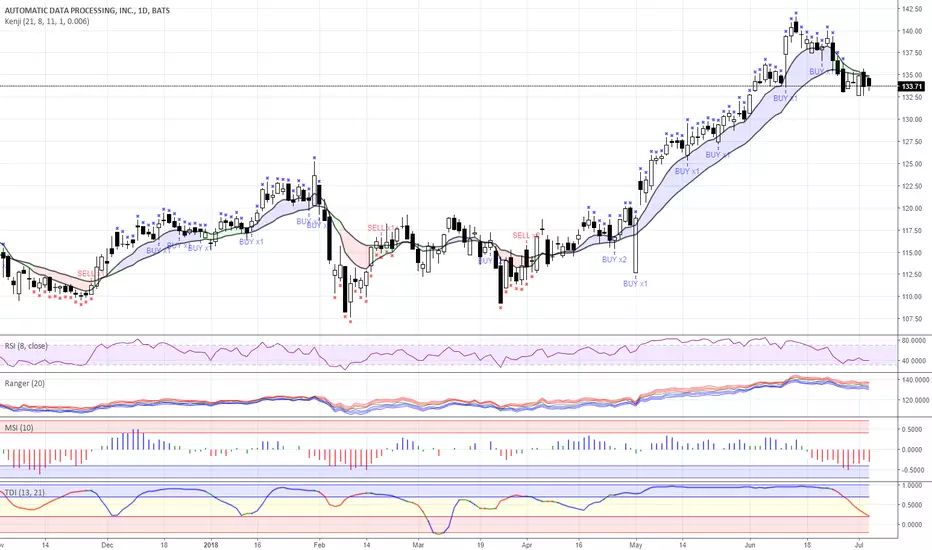

[ADP] Starting to phase 3?If the price bounces to $ 141.44, it'll continue in phase 2, but I think it's starting phase 3 because the RSI is down and the force of sale takes more than 2 years.

ADP: Expanding triangle formation I don't have a price target for ADP but it is interesting to see the resistance at $140 and the lower lows with a negatively diverging MACD. This is ultimately a bearish pattern.

Statistic from ADP:reason to be worried for buyers of the dollarToday's statistics on the US labor market may well disappoint. At least, this is indicated by data on the level of employment in the private sector from ADP. With an average forecast of experts in +190K, in fact the figure was +177K. Overall, there is nothing terrible in this figure. By itself, it is very, very good. The problem is that the States have become a hostage of excellent data. Markets have become too accustomed to numbers of + 200K and above. Accordingly, any negative deviation from the forecasts may be interpreted by participants of financial markets as the beginning of problems in the US economy, with all the ensuing consequences: a decrease in GDP growth rates, an end to the Fed's rate increase phase, and so on.

Just in case, let's remind you that today is published a whole block of data that includes not only the number of new jobs created outside agriculture, but also the rate of unemployment, and, which is no less important, in the conditions of the active phase of the FED interest rate increase - the average hourly earnings:

Pre-Forecast

15:30 USA 3 NFP (June) 223K 190K

15:30 USA 3 Average hourly earnings (m / m) (June) 0.3% 0.3%

15:30 USA 3 Unemployment rate (June) 3.8% 3.8%

As can be seen, the forecasts are rather optimistic and, in some cases, even aggressive, and therefore the chances that they will not come true fully or partially are high.

Thus, we see on the horizon a potential fundamental threat to the dollar.

In addition, purely technically, if you look at the graph of the Dollar Index, you can see its inability to overcome the key resistance 95 and can see signs of a possible correction: consolidation at the top, the formation of reversal graphical patterns, candlestick signals, trend indicators enter into a neutral negative state (see KenJi and TDI indications), etc.

Total, dollar sales continue to look more promising than its purchases.

Data from ADP send negative signals to the dollarTraditionally, on the eve of the release of official statistics on the labor market in the United States, unofficial data on the number of new jobs created in the US by ADP are published (note that data from ADP cover only the private sector, state enterprises are not included in it).

The ADP report reflects the level of employment Data are received from approximately 500,000 US legal entities. And although the level of correlation between ADP and NFP data is not very significant (about 30-40%), nevertheless, ADP data are an important indicator, especially on the eve of the main data block.

The data published today turned out to be worse than the forecasted values and much lower than the indications of the previous period. The growth rate was 178 K (forecast 190 K, the previous 204 K). In general, the figure is excellent, but the fact of its lagging behind the market expectations sends a negative signal to the dollar and adjusts to a negative mood on Friday, when the NFP figures will be published. Another alarming signal for the dollar was a significant negative revision of the April values from 204K to 163K.

It is also worth noting that the data on US GDP, also published on Wednesday, was below forecasts.

In total, we consider today's data as a reason for the start of dollar sales. Recall also that for two months in a row the data on the NFP are worse than forecasts, which is quite an alarming signal for dollar buyers.

Stronger ADP...EURUSD for a short retraceVolatility ahead. In addition to the uncertainty on the USD arising from the trade war (increased tariffs), and change of personnel in the White house, from today till Friday, we see several economic data release and policy decisions which could surprise the market and also bring about higher volatility.

Tonight, we have the USD ADP NFP, which is released 2 days ahead of the Govt NFP release on Friday evening.

This is data is likely to bring some short term volatility to the USD, with anticipation that data released to be better than forecasted, close to previous month.

If EURUSD breaks below 1.2400 a quick sell towards 1.2350 could be viable.

EURUSD - Broke supportThe price of EURUSD broke support after the ADP release, Next local support found at 1.1175. Breaking below it could send the price down to the trend line (blue one on the char).

Dollar Data Dependant The USD sell off as traders set a chain of profit taking after 2 weeks rally due to various factors:

- Greece uncertainty of exiting the EZ make holding USD worthwhile

- US Economic data has been promising with CPI much higher

- Hawkish comment from Yellen

- That view is changing with 5th of June looming for a potential deal and no Grexit

A lower USD potentially because:

- Euro rally with Bund unable to find support and Grexit averted

- Unwinding of USD/JPY longs

- Commodities currencies caught bids

- A worse than expected US economic data

A higher USD potentially because:

- Grexit so USD safe haven currency

- Better than expected US economic data that imply a September rate hike

- Hawkish comment from Fed members

Technically:

- Heavy band of resistance between 96.63 and 97.73

- Heavily biased for more downside with a possible AB - CD playing out

Consolidation next on US dollar indexExpect some consolidation

Forming a potential H & S?

Will wait for confirmation

Daily RSI has rooms to fall

Data Dependant on ADP & Non Farm Payroll

Previous yellow box was a bullish wedge

Forecast next yellow box is a bearish wedge?