Rolls-Royce Holdings: Wave Count AdjustedAfter Rolls-Royce shares recently surged and broke through resistance at €14.10, we have revisited our wave count and made some adjustments. We now primarily believe that the low of wave (4) in magenta was likely set at the end of November, forming a turquoise A-B-C three-wave move. In any case, the ongoing wave (5) in magenta should still have some upside potential before completing the larger cyclical wave I in beige.

Aerospace

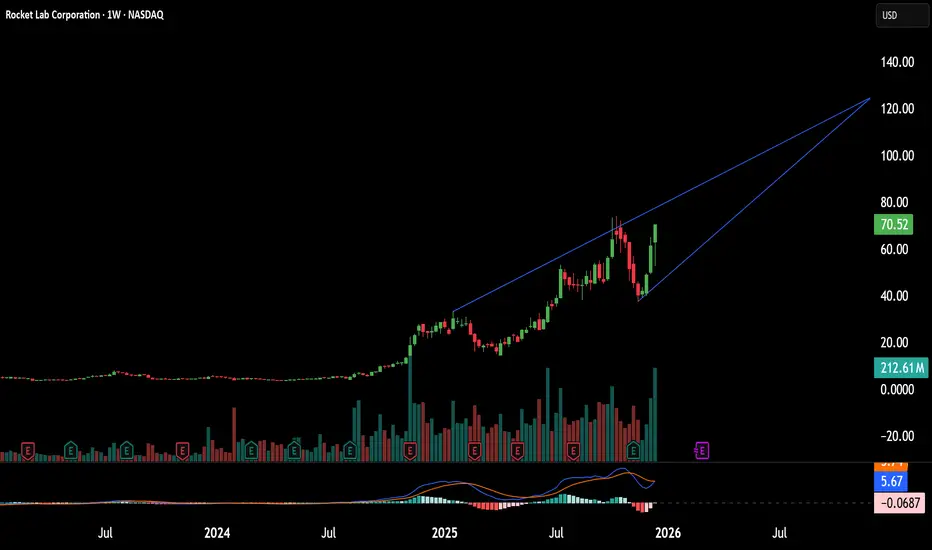

Can a Small-Sat Pioneer Become a Defense Superpower?Rocket Lab has transformed from a niche small-satellite launch provider into a strategic national security asset, closing 2025 with 21 successful Electron launches and a remarkable 175% stock surge. The company's evolution culminated in an $816 million Space Development Agency contract to build 18 satellites for hypersonic missile threat detection, signaling its emergence as a primary defense contractor. This vertical integration strategy positions Rocket Lab as a critical player in an era where supply chain sovereignty has become paramount for military readiness.

The technological centerpiece of Rocket Lab's 2026 ambitions is the Neutron rocket, a medium-lift vehicle capable of carrying 13,000 kilograms to low Earth orbit. Set for its maiden test flight in mid-2026, Neutron features the innovative "Hungry Hippo" fairing design and 3D-printed Archimedes engines, targeting the lucrative mega-constellation market currently dominated by SpaceX's Falcon 9. This technological leap, combined with over 550 global patents covering critical propulsion and structural innovations, creates a formidable intellectual property moat that competitors cannot easily replicate.

The financial trajectory underscores this transformation: analysts project 52.2% EPS growth for 2026, reaching $0.27 per share and dramatically outpacing traditional aerospace giants like Lockheed Martin (0.6%) and Northrop Grumman (-7.6%). A potential SpaceX IPO at $1.5 trillion valuation could trigger sector-wide revaluation, with Rocket Lab standing as the only publicly traded, vertically integrated alternative. Wall Street has responded accordingly, raising price targets to $90 as the company bridges the gap between startup agility and aerospace titan scale, with defense contracts poised to dominate its revenue mix.

AST SpaceMobile: The High-Stakes Race for Global CoverageAST SpaceMobile ( NASDAQ:ASTS ) is currently redefining the orbital telecommunications landscape. On December 24, 2025, the company achieved a historic milestone with the successful launch of BlueBird 6. This satellite represents the largest commercial communications array ever deployed in Low Earth orbit (LEO). Despite this technical triumph, investors are closely monitoring recent volatility. A significant share sale by American Tower Corporation ( NYSE:AMT ) has introduced a complex narrative to the stock’s 250% year-to-date rally.

Geostrategy: The US-India Aerospace Alliance

The launch of BlueBird 6 via India’s LVM3-M6 rocket underscores a strategic shift in aerospace logistics. By leveraging Indian launch capabilities, AST SpaceMobile reduces its dependence on domestic providers like SpaceX. This diversification strengthens the company's supply chain resilience. It also aligns with broader US geostrategy to deepen technological ties with India. This move secures reliable access to space amid a global shortage of heavy-lift launch windows.

Technology: The Patent Moat and AST5000 ASIC

AST SpaceMobile holds a formidable intellectual property portfolio with over 3,800 patents and pending claims. At the core of their technical advantage is the AST5000 ASIC. This proprietary chip enables peak speeds of 120 Mbps per coverage cell. Such capacity allows standard, unmodified smartphones to connect directly to broadband from space. This innovation effectively bypasses the need for specialized hardware, creating a massive competitive moat against traditional satellite providers.

Macroeconomics: Navigating Strategic Divestments

The mid-December sell-off by American Tower ( NYSE:AMT ) caught the market's attention. American Tower reduced its position by approximately 49%, generating nearly $160 million in proceeds. While some analysts view this as routine profit-taking after a massive run, others see a cautionary signal. However, AST SpaceMobile maintains a robust cash position of $3.2 billion as of late 2025. This liquidity supports the planned ramp-up to producing six satellites per month by early 2026.

Industry Trends: The MNO Integration Model

The company's business model relies on 50/50 revenue-sharing agreements with Mobile Network Operators (MNOs). Strategic partnerships with AT&T and Verizon have solidified AST SpaceMobile’s lead in the US market. These carriers provide the licensed spectrum necessary for space-based cellular service. As the "Direct-to-Device" (D2D) trend accelerates, AST SpaceMobile is positioned as a wholesale provider. This model allows for rapid scaling without the high cost of customer acquisition.

Management & Leadership: Executing the Scaled Vision

Founder and CEO Abel Avellan has transitioned the company from a visionary R&D firm to a manufacturing powerhouse. The Midland, Texas, facility now operates at nearly 500,000 square feet across five sites. This vertical integration allows for 95% of satellite components to be produced in-house. Management's ability to hit launch milestones in late 2025 has restored confidence following earlier delays. The leadership's focus remains on achieving continuous US coverage by the end of 2026.

---

Impact Summary for Traders

The successful BlueBird 6 launch validates the technology, but institutional selling suggests a near-term valuation peak.

* Bullish Factors: Successful orbital deployment of 2,400 sq ft array, $3.2B liquidity, and proprietary ASIC technology.

* Bearish Factors: High price-to-book ratio and significant discretionary selling by a strategic partner (American Tower).

* Key Watch: Launch frequency in Q1 2026 and the commencement of commercial beta testing in the US.

FJET - From Private Skies to Public Markets!!Most retail investors never had access to the biggest space winners.🌌

SpaceX went from a private valuation near $46B to over $800B without ever giving the public a chance to participate.

This time, the door is open❗️

Starfighters Space, Inc. AMEX:FJET has officially entered the public markets, giving everyday investors exposure to a real aerospace company… Not a concept, not a slide deck; but one already flying missions out of NASA’s Kennedy Space Center.

📊 Technical Analysis

Following its public debut, FJET delivered a strong impulsive move 📈, confirming aggressive buyer interest.

After a healthy correction into demand, buyers stepped in again, keeping the structure intact.

Price has now broken and held above the $10 area , confirming bullish continuation and validating the higher-timeframe structure.

🔁 From here, the expectation is a shallow pullback / consolidation , followed by continuation in line with the scenario marked in purple.

🏹 The $20 zone represents the first target , and upon reaching it, I will be watching for further upside , at which point I’ll post an updated outlook.

💡 Bigger Picture

This isn’t a speculative space idea, it’s an operating aerospace company 💼with rare credentials:

- World’s only commercial Mach 2-capable fleet of Lockheed F-104 Starfighters.

- Operating directly out of NASA’s Kennedy Space Center.

- Strategic validation from NASA, Lockheed Martin, GE, and the U.S. Air Force.🛩

- Pioneering a hypersonic air-launch platform designed to dramatically reduce the cost and timeline of microsatellite deployment.

- Successfully completed a $40M Regulation A+ raise , transitioning from private capital into the public markets.

Recent history shows that real aerospace IPOs tend to move early:

Voyager, Firefly, Karman, and AIRO all saw sharp post-listing expansions.

In this sector, the first phase after going public often matters the most.

📘 Bottom line

FJET offers something rare:

💎Early exposure to a credible aerospace company right after it entered the public markets, before full institutional positioning and before the story became widely crowded.

📡Whether you approach it as a technical setup, a newly public aerospace play, or a longer-term space infrastructure narrative, this is a name worth keeping on the radar.

⚠️ Always do your own research and speak with your financial advisor before investing.

📚 Stick to your trading plan, entry, risk management, and execution.

All strategies are good; if managed properly.

~ Richard Nasr

Disclaimer: I have been paid $800 by CDMG, funded by Starfighters Space, to disseminate this message.

Rocket Lab’s Strategic Ascent: Beyond the NumbersRocket Lab (NASDAQ: RKLB) has solidified its status as a cornerstone of the modern space economy. Following a turbulent period that saw shares retrace nearly 50%, the stock has staged a commanding recovery, rallying roughly 111% year-to-date. This resurgence is not merely a product of market speculation; it reflects a convergence of geopolitical necessity, operational maturity, and favorable macroeconomic shifts.

Geostrategy and Defense Dynamics

The company’s recent momentum is deeply rooted in shifting geopolitical realities. The successful STP-S30 mission for the U.S. Space Force, launched five months ahead of schedule, underscores Rocket Lab’s critical role in national security. In an era where orbital assets are vulnerable to kinetic and cyber threats, the ability to rapidly replace satellites is a strategic deterrent. Rocket Lab provides the "responsive space" capability that Western defense planners demand.

Furthermore, the dedicated launch for the Japan Aerospace Exploration Agency (JAXA) highlights a strengthening of allied aerospace integration. As nations like Japan seek to diversify launch providers away from domestic bottlenecks, Rocket Lab has emerged as the preferred neutral partner. This expands its total addressable market beyond U.S. borders, insulating it from single-market risks.

Industry Trends and Valuation Benchmarks

A massive sector-wide repricing is underway, catalyzed by reports of a potential SpaceX IPO in 2026 at a $1.5 trillion valuation. This news has fundamentally altered how investors assess the space industry’s long-term economics. SpaceX’s valuation serves as a powerful anchor, validating the orbital economy’s scale.

As the only other publicly traded, vertically integrated launch provider with a proven track record, Rocket Lab is the primary beneficiary of this sentiment shift. Capital that once flowed into speculative pre-revenue SPACs is consolidating into proven operators. Rocket Lab’s business model, which combines launch services with high-margin space systems, offers investors a tangible hedge against the capital-intensive nature of pure launch plays.

Operational Excellence and Culture

Corporate culture remains Rocket Lab’s hidden alpha. While the broader aerospace sector struggles with chronic delays, Rocket Lab’s delivery of the STP-S30 mission ahead of schedule speaks to a unique internal ethos. This "execution-first" culture sharply contrasts with competitors who rely on PowerPoint engineering.

Management’s ability to navigate high-tech manufacturing challenges while maintaining launch cadence has built a reservoir of institutional trust. This reliability is a defensive moat. In the launch business, reputation is currency; Rocket Lab’s consistency allows it to command pricing power and secure long-term government contracts that competitors cannot access.

Technology and the Neutron Horizon

The upcoming Neutron rocket represents a technological inflection point. Scheduled for its maiden flight in the first half of 2026, Neutron moves the company from a small-lift niche to medium-lift dominance. This vehicle targets the lucrative constellation deployment market, currently a SpaceX monopoly.

From a patent and science perspective, Neutron’s design—featuring unique carbon composite structures and reusable fairings—signals a leap in material science application. These proprietary engineering solutions create high barriers to entry. By securing intellectual property around rapid reusability and automated manufacturing, Rocket Lab protects its margins against commoditization.

Conclusion

Rocket Lab’s recovery is structural, not accidental. It is driven by a unique intersection of defense utility, superior execution, and a repricing of the space sector’s potential. As the company prepares for the Neutron era, it is shedding its label as a "small launch" provider and emerging as a diversified aerospace prime.

PL: room to follow-through Price continues to follow the macro bullish trend structure outlined in the September updates. Watching for further follow-through into the next 24–30 resistance zone.

The earnings gap may offer a delayed-reaction setup if we see a constructive, low-volume pullback in the coming days - ideally with price holding above the 15 local support.

Chart:

Macro view (Weekly):

Previously:

• On macro bullish-trend structure (Sep 14):

www.tradingview.com

• On resistance zone and pullback (Sep 26):

www.tradingview.com

Is Boeing's Defense Bet America's New Arsenal?Boeing's recent stock appreciation stems from a fundamental strategic pivot toward defense contracts, driven by intensifying global security tensions. The company has secured major wins, including the F-47 Next Generation Air Dominance (NGAD) fighter contract worth over $20 billion and a $4.7 billion deal to supply AH-64E Apache helicopters to Poland, Egypt, and Kuwait. These contracts position Boeing as central to U.S. military modernization efforts aimed at countering China's rapid expansion of stealth fighters like the J-20, which now rivals American fifth-generation aircraft production rates.

The F-47 program represents Boeing's redemption after losing the Joint Strike Fighter competition two decades ago. Through its Phantom Works division, Boeing developed and flight-tested full-scale prototypes in secret, validating designs through digital engineering methods that dramatically accelerated development timelines. The aircraft features advanced broadband stealth technology and will serve as a command node controlling autonomous drones in combat, fundamentally changing air warfare doctrine. Meanwhile, the modernized Apache helicopter has found renewed relevance in NATO's Eastern flank defense strategy and counter-drone operations, securing production lines through 2032.

However, risks remain in execution. The KC-46 tanker program continues facing technical challenges with its Remote Vision System, now delayed until 2027. The F-47's advanced variable-cycle engines are two years behind schedule due to supply chain constraints. Industrial espionage, including cases where secrets were sold to China, threatens technological advantages. Despite these challenges, Boeing's defense portfolio provides counter-cyclical revenue streams that hedge against commercial aviation volatility, creating long-term financial stability as global rearmament enters what analysts describe as a sustained "super-cycle" driven by great power competition.

Can Instability Be an Asset Class?Aerospace and Defense (A&D) ETFs have shown remarkable performance in 2025, with funds like XAR achieving a 49.11% year-to-date return. This surge follows President Trump's October 2025 directive to resume U.S. nuclear weapons testing after a 33-year moratorium, a decisive policy shift responding to recent Russian weapons demonstrations. The move signals the formalization of Great Power Competition into a sustained, technology-intensive arms race, transforming A&D spending from discretionary to structurally mandatory. Investors now view defense appropriations as a guaranteed source of funding, creating what analysts call a permanent "instability premium" on sector valuations.

The financial fundamentals supporting this outlook are substantial. The FY2026 defense budget allocates $87 billion for nuclear modernization alone, a 26% increase in funding for critical programs like the B-21 bomber, Sentinel ICBM, and Columbia-class submarines. Major contractors are reporting exceptional results: Lockheed Martin established a record $179 billion backlog while raising its 2025 outlook, effectively creating multi-year revenue certainty that functions like a long-duration bond. In 2023, global military spending reached $2.443 trillion, with NATO allies driving over $170 billion in U.S. foreign military sales, which extended revenue visibility beyond domestic congressional cycles.

Technological competition is accelerating investments in hypersonics, digital engineering, and modernized command-and-control systems. The shift toward AI-driven warfare, resilient space-based architectures, and advanced manufacturing processes (exemplified by Lockheed's digital twin technology for the Precision Strike Missile program) is transforming defense contracting into a hybrid hardware-software model with sustained high-margin revenue streams. The modernization of Nuclear Command, Control, and Communications (NC3) systems and implementation of Joint All-Domain Command and Control (JADC2) strategy require continuous, multi-decade investments in cybersecurity and advanced integration capabilities.

The investment thesis reflects structural certainty: legally mandated nuclear modernization programs are immune to typical budget cuts, contractors hold unprecedented backlogs, and technological superiority demands perpetual high-margin research and development. The resumption of nuclear testing, driven by strategic signaling rather than technical necessity, has created a self-fulfilling cycle that guarantees future expenditures. With geopolitical escalation, macroeconomic certainty through front-loaded appropriations, and rapid technological innovation converging simultaneously, the A&D sector has emerged as an essential component of institutional portfolios, supported by what analysts characterize as "geopolitics guaranteeing profits."

Can a $251 Billion Backlog Predict the Future?RTX Corporation has positioned itself at the intersection of escalating global defense imperatives and the recovery of commercial aviation, generating a formidable $251 billion backlog that provides unprecedented revenue visibility. The company reported strong Q3 2025 results with sales of $22.5 billion (up 12% year-over-year) and raised its full-year guidance, driven by double-digit organic growth across all segments. This performance reflects RTX's dual-market advantage: surging defense spending, with global military expenditure reaching $2.7 trillion in 2024 and NATO's new 5% GDP target by 2035, combined with recovering commercial aviation demand projected to exceed 12 billion passengers by 2030.

RTX's technological superiority centers on proprietary Gallium Nitride (GaN) semiconductor innovations that power next-generation radar systems, creating substantial barriers to entry. The company's LTAMDS radar delivers twice the power of legacy Patriot systems while eliminating battlefield blind spots, and the newly launched APG-82(V)X radar enhances fighter aircraft capabilities against advanced threats. Major contracts underscore this dominance, including a $5 billion Army award for the Coyote counter-drone system, which extends through 2033. RTX has committed over $600 million to manufacturing expansion this year alone, with the Redstone Missile Integration Facility expansion specifically targeting increased production of Standard Missile variants and counter-hypersonic solutions.

On the commercial side, Pratt & Whitney's GTF Advantage engine achieved EASA certification in Q4 2025, resolving earlier durability challenges with a design targeting double the time-on-wing compared to prior models. This breakthrough secures RTX's control over the A320neo and A220 fleets, guaranteeing decades of high-margin maintenance, repair, and overhaul revenue. Collins Aerospace's global network of over 70 MRO sites and flexible AssetFlex program capitalizes on supply chain constraints that force airlines to invest more heavily in fleet maintenance rather than new aircraft purchases.

The financial trajectory appears compelling: analysts project free cash flow will surge from $5.5 billion in 2023 to $9.9 billion by 2027, representing 15.5% annualized growth and compressing the price-to-FCF multiple from 31.3x to 17.3x. Wall Street maintains a consensus "Buy" rating across thirteen covering firms with zero sell recommendations. RTX's 60,000-patent portfolio, built on $7.5 billion in annual R&D spending, spans advanced materials, AI, autonomy, and next-generation propulsion, creating a self-reinforcing cycle where investment drives proprietary technology that secures long-term government contracts. With an affirmed BBB+ credit rating and stable outlook, RTX presents a structurally sound investment thesis built on geopolitical necessity, technological moats, and expanding cash generation.

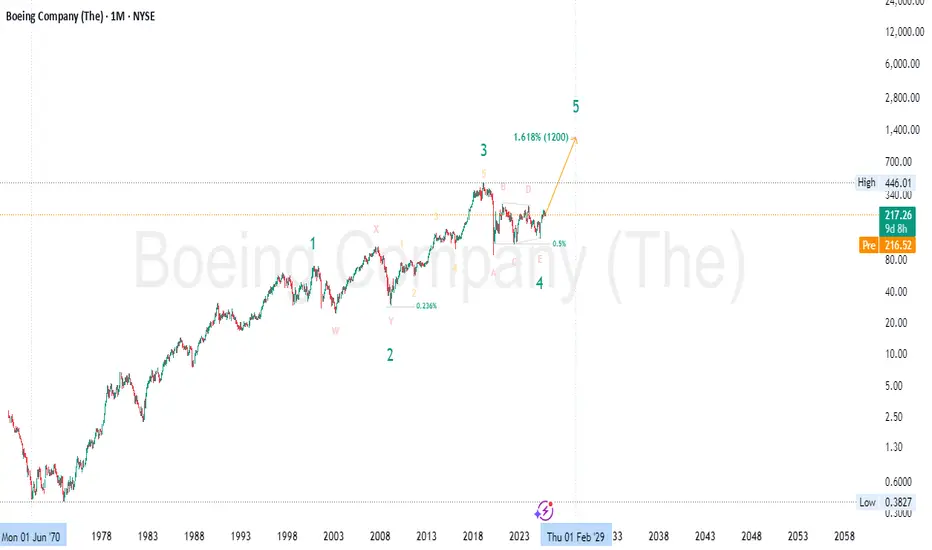

Boeing (BA) – Final Leg of Macro Bull Run✈️ Boeing (BA) – Final Leg of Macro Bull Run | Wave 5 to 1.618 Extension ($1200) 🚀

📅 Timeframe: Monthly (Macro Cycle Outlook)

📍 Current Price: $217

🎯 Wave 5 Target : ~$1200 (1.618 Extension)

🌀 Wave Theory Structure

Boeing appears to be entering Wave 5 of a long-term Elliott Wave cycle:

✅ Wave 1: Multi-decade rise until the early 2000s

✅ Wave 2: Complex correction (W–X–Y) into 2009 lows

✅ Wave 3: Powerful rally through 2019, completed with an extended 5-wave subdivision

✅ Wave 4: A large-scale triangle correction (ABCDE) — now completed, as price has broken structure upward

🚀 Wave 5: Projected move toward the 1.618 Fibonacci extension (~$1200) from the 1–3 wave distance

This is a textbook impulsive wave structure playing out on the monthly macro scale — with a final bullish leg now unfolding.

📐 Fibonacci Confluence

Wave 2 retraced ~0.236 of Wave 1 (shallow, bullish corrective behavior)

Wave 4 retraced ~0.5 of Wave 3 — typical for triangle patterns and expanded flats

Wave 5 target at 1.618 Fib extension measured from Wave 1–3 aligns around $1200 , completing the 5-wave macro cycle 🔺

🧠 Smart Money Concepts (SMC)

🔹 Accumulation Phase (2020–2024): After COVID crash and multi-year consolidation, price has shown strong accumulation characteristics

🔹 Final Sweep of Lows (E leg) flushed out late longs and retail stops before institutional re-entry

🔹 Break of Structure (BOS) confirms transition from reaccumulation to markup phase 📈

🔹 Price is now in a reprice phase — a classic SMC trait where value is rapidly adjusted after institutional positioning completes

📊 Price Action Analysis

Bullish breakout from triangle structure

Monthly higher low established at E-wave base

Strong bullish candle from demand zone — early confirmation of trend continuation

Break above $260 would open clean skies toward the next major resistance at ATH ($446) and beyond 🧭

💼 Fundamental Outlook

Boeing is regaining strength after multiple challenging years:

✈️ Rebound in global aviation demand

📦 Growing defense & aerospace contracts amid rising geopolitical tensions

💰 Expected recovery in cash flows, backlog, and profitability

🌐 Expansion in space and unmanned systems (future growth verticals)

Although regulatory and delivery risks remain, Boeing’s turnaround story is gathering steam — aligning with the technical forecast of Wave 5 acceleration.

🔍 Summary

Boeing is entering what could be the final and most explosive leg (Wave 5) of its macro Elliott Wave cycle. Key confluences include:

✅ Elliott Wave triangle completion

✅ Fibonacci 1.618 extension to ~$1200

✅ Institutional accumulation confirmed

✅ Price Action breakout from multi-year structure

✅ Improving long-term fundamentals

This setup favors long-term swing positions , with pullbacks offering buying opportunities until the final cycle target is approached. 🧠📈

⚠️ Disclaimer: This is not financial advice. For educational purposes only. Always do your own due diligence and manage risk responsibly. 🛡️

#Boeing #BA #ElliottWave #SmartMoney #PriceAction #Fibonacci #Wave5 #TriangleBreakout #TechnicalAnalysis #LongTermInvestment #MacroTrading #StockMarket #BullishOutlook #Aerospace #WaveTheory #SwingTrading #AviationRecovery #FibonacciTargets #TradingStrategy

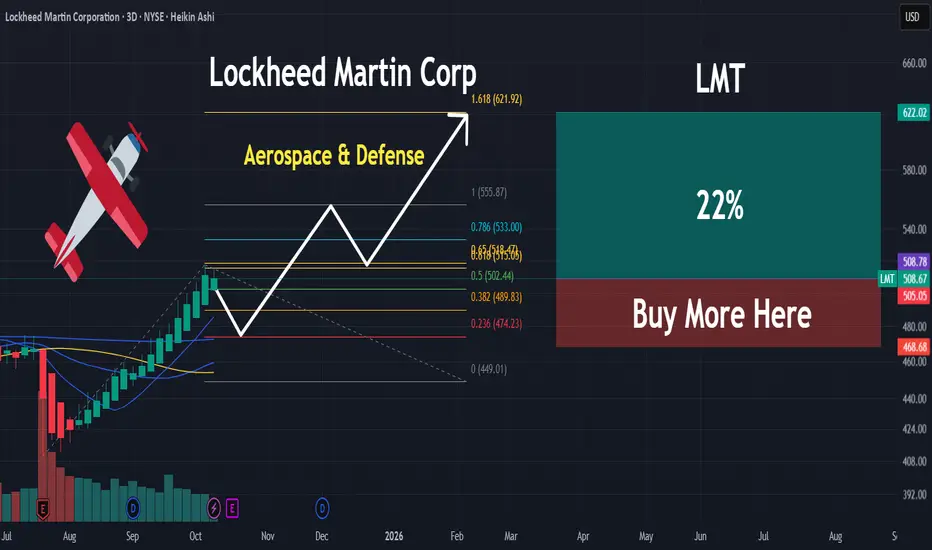

LMT | Lockheed Martin Could Rise Higher | LONGLockheed Martin Corp. is a global security and aerospace company, which engages in the research, design, development, manufacture, integration, and sustainment of technology systems, products, and services. It operates through the following business segments: Aeronautics, Missiles and Fire Control (MFC), Rotary and Mission Systems (RMS), and Space. The Aeronautics segment researches, designs, develops, manufactures, integrates, sustains, supports, and upgrades advanced military aircraft, including combat and air mobility aircraft, unmanned air vehicles, and related technologies. The MFC segment is involved in air and missile defense systems, tactical missiles and air-to-ground precision strike weapon systems, logistics, fire control systems, mission operations support, readiness, engineering support and integration services, manned and unmanned ground vehicles, and energy management solutions. The RMS segment designs, manufactures, services, and supports various military and commercial helicopters, surface ships, sea and land-based missile defense systems, radar systems, sea and air-based mission and combat systems, command and control mission solutions, cyber solutions, and simulation and training solutions. The Space segment includes the production of satellites, space transportation systems, and strategic, advanced strike, and defensive systems. The company was founded in 1995 and is headquartered in Bethesda, MD.

War is a Racket | DFEN | Long at $28.00The war machine keeps turning. Profits will reign. Direxion Aerospace and Defense 3x AMEX:DFEN never fully recovered from pandemic lows, but world peace is (unfortunately) far from reach. The uptrend in the chart has commenced. Personal entry point at $28.00.

Target #1 = $37.00

Target #2 = $50.00

Target #3 = $64.00

How Does a Silent Giant Dominate Critical Technologies?Teledyne Technologies has quietly established itself as a formidable force across defense, aerospace, marine, and space markets through a disciplined strategy of strategic positioning and technological integration. The company recently reported record Q2 2025 results with net sales of $1.51 billion (10.2% increase) and demonstrated exceptional organic growth across all business segments. This performance reflects not market timing but the culmination of deliberate long-term positioning at the intersection of mission-critical, high-barrier-to-entry markets where geopolitical factors create natural competitive advantages.

The company's strategic acumen is exemplified by products like the Black Hornet Nano micro-UAV, which has proven its tactical value in conflicts from Afghanistan to Ukraine, and the emerging Black Recon autonomous drone system for armored vehicles. Teledyne has strengthened its market position through geopolitically aligned partnerships, such as its collaboration with Japan's ACSL for NDAA-compliant drone solutions, effectively turning regulatory compliance into a competitive moat against non-allied competitors. The 2021 acquisition of FLIR Systems for $8.2 billion demonstrated horizontal integration mastery, with thermal imaging technology now deployed across multiple product lines and market segments.

Teledyne's competitive advantage extends beyond products to intellectual property dominance, holding 5,131 patents globally with an exceptional 85.6% USPTO grant rate. These patents span imaging and photonics (38%), defense and aerospace electronics (33%), and scientific instrumentation (29%), with frequent citations by industry giants like Boeing and Samsung indicating their foundational nature. The company's $474 million annual R&D investment, supported by 4,700 engineers with advanced degrees, ensures continuous innovation while building legal barriers against competitors.

The company has proactively positioned itself to meet emerging regulatory requirements, particularly the Department of Defense's new Cybersecurity Maturity Model Certification (CMMC) mandate, which takes effect in October 2025. Teledyne's existing cybersecurity infrastructure and certifications provide a crucial advantage in meeting these standards, creating an additional "compliance moat" that will likely enable the company to capture increased defense contract opportunities as competitors struggle with new requirements.

Aeva Technologies (AEVA) – Pioneering Next-Gen LiDAR Company Snapshot:

Aeva NASDAQ:AEVA is revolutionizing perception systems with 4D FMCW LiDAR—offering instant velocity detection, high precision, and long-range sensing, setting a new standard for autonomous systems.

Key Catalysts:

Breakthrough Technology

AEVA’s proprietary 4D Frequency Modulated Continuous Wave (FMCW) LiDAR provides real-time velocity and depth data, outperforming traditional Time-of-Flight systems in accuracy and safety.

Automotive OEM Traction 🚗

Strategic collaborations are translating into production-stage contracts, marking a key inflection from R&D to scalable revenue generation.

Multi-Sector Expansion 🌐

AEVA’s sensing tech is penetrating robotics, aerospace, and industrial automation, significantly broadening its TAM and diversifying revenue streams.

Government & Aerospace Validation

Recent contract wins with defense and aerospace clients underscore AEVA’s technological credibility and commercial viability.

Investment Outlook:

Bullish Entry Zone: Above $22.50–$23.00

Upside Target: $39.00–$40.00, supported by production scaling, cross-sector adoption, and deep-tech differentiation.

⚙️ AEVA stands at the forefront of smart sensing innovation with strong momentum into high-growth verticals.

#AEVA #LiDAR #AutonomousVehicles #Robotics #Aerospace #IndustrialTech #SensorRevolution #4DPerception #FMCW #TechStocks #Innovation #SmartMobility

Red Cat Holdings (RCAT) – Soaring with Defense & Global DemandCompany Snapshot:

Red Cat NASDAQ:RCAT is an emerging UAV (drone) technology leader, rapidly scaling through defense-grade contracts, global expansion, and vertical integration.

Key Catalysts:

Defense Sector Traction 🎯

Recent U.S. DoD contract wins underscore RCAT’s credibility as a mission-critical UAV supplier.

Sequential revenue growth in earnings signals accelerating adoption in defense and commercial markets.

Global Expansion Strategy 🌐

RCAT is diversifying via allied procurement programs, reducing dependence on U.S. defense budgets and broadening international exposure.

Tech Stack Integration ⚙️

Strategic acquisitions are bolstering RCAT’s in-house capabilities—driving vertical integration, improving margins, and fueling innovation velocity.

Investment Outlook:

Bullish Entry Zone: Above $8.50–$9.00

Upside Target: $15.00–$16.00, supported by defense contract momentum, global reach, and a strengthened tech edge.

🛡️ RCAT is becoming a high-leverage play on modern defense tech with scalable, global upside.

#RCAT #DefenseStocks #UAV #DroneTechnology #MilitaryContracts #Innovation #DoD #Aerospace #Geopolitics #GrowthStocks #VerticalIntegration

Is Red Cat Holdings a Drone Industry Maverick?Red Cat Holdings (NASDAQ: RCAT) navigates a high-stakes segment of the burgeoning drone market. Its subsidiary, Teal Drones, specializes in rugged, military-grade uncrewed aerial systems (UAS). This niche positioning has attracted significant attention, evidenced by contracts with the U.S. Army and U.S. Customs and Border Protection. Geopolitical tensions, particularly the escalating demand for advanced military drone capabilities, create a favorable backdrop for companies like Red Cat, which offer NDAA-compliant and Blue UAS-certified solutions. These certifications are critical, ensuring drones meet stringent U.S. defense and security standards, differentiating Red Cat from foreign competitors.

Despite its strategic positioning and significant contract wins, Red Cat faces considerable financial and operational challenges. The company currently operates at a loss, with a net loss of $23.1 million in Q1 2025 against modest revenues of $1.6 million. Its revenue projections of $80-$120 million for 2025 underscore the lumpy nature of government contracts. To bolster its capital, Red Cat completed a $30 million equity offering in April 2025. This financial volatility is compounded by an ongoing class action lawsuit. This lawsuit alleges misleading statements regarding the production capacity of its Salt Lake City facility and the value of its U.S. Army Short Range Reconnaissance (SRR) program contract.

The SRR contract, which could involve up to 5,880 Teal 2 systems over five years, represents a substantial opportunity. However, the lawsuit highlights a significant discrepancy, with allegations from short-seller Kerrisdale Capital suggesting a much lower annual budget allocation for the program compared to Red Cat's initially intimated "hundreds of millions to over a billion dollars." This legal challenge and the inherent risks of government funding cycles contribute to the stock's high volatility and elevated short interest, which recently exceeded 18%. For risk-tolerant investors, Red Cat presents a "moonshot" opportunity, contingent on its ability to convert contract wins into sustainable, scalable revenue and successfully navigate its legal and financial hurdles.

Is Rocket Lab the Future of Space Commerce?Rocket Lab (RKLB) is rapidly ascending as a pivotal force in the burgeoning commercial space industry. The company's vertically integrated model, spanning launch services, spacecraft manufacturing, and component production, distinguishes it as a comprehensive solutions provider. With key operations and launch sites in both the U.S. and New Zealand, Rocket Lab leverages a strategic geographic presence, particularly its strong U.S. footprint. This dual-nation capability is crucial for securing sensitive U.S. government and national security contracts, aligning perfectly with the U.S. imperative for resilient, domestic space supply chains in an era of heightened geopolitical competition. This positions Rocket Lab as a trusted partner for Western allies, mitigating supply chain risks for critical missions and bolstering its competitive edge.

The company's growth is inextricably linked to significant global shifts. The space economy is projected to surge from $630 billion in 2023 to $1.8 trillion by 2035, driven by decreasing launch costs and increasing demand for satellite data. Space is now a critical domain for national security, compelling governments to rely on commercial entities for responsive and reliable access to orbit. Rocket Lab's Electron rocket, with over 40 launches and a 91% success rate, is ideally suited for the burgeoning small satellite market, vital for Earth observation and global communications. Its ongoing development of Neutron, a reusable medium-lift rocket, promises to further reduce costs and increase launch cadence, targeting the expansive market for mega-constellations and human spaceflight.

Rocket Lab's strategic acquisitions, such as SolAero and Sinclair Interplanetary, enhance its in-house manufacturing capabilities, allowing greater control over the entire space value chain. This vertical integration not only streamlines operations and reduces lead times but also establishes a significant barrier to entry for competitors. While facing stiff competition from industry giants like SpaceX and emerging players, Rocket Lab's diversified approach into higher-margin space systems and its proven reliability position it strongly. Its strategic partnerships further validate its technological prowess and operational excellence, ensuring a robust position in an increasingly competitive landscape. As the company explores new frontiers like on-orbit servicing and in-space manufacturing, Rocket Lab continues to demonstrate the strategic foresight necessary to thrive in the dynamic new space race.

Soaring High: What Fuels GE Aerospace's Ascent?GE Aerospace's remarkable rise reflects a confluence of strategic maneuvers and favorable market dynamics. The company maintains a dominant position in the commercial and military aircraft engine markets, powering over 60% of the global narrowbody fleet through its CFM International joint venture and proprietary platforms. This market leadership, coupled with formidable barriers to entry and significant switching costs in the aircraft engine industry, secures a robust competitive advantage. Furthermore, a highly profitable aftermarket business, driven by long-term maintenance contracts and an expanding installed engine base, provides a resilient, recurring revenue stream. This lucrative segment buffers the company against cyclicality and ensures consistent earnings visibility.

Macroeconomic tailwinds also play a crucial role in GE Aerospace's sustained growth. Global air travel is steadily increasing, driving higher aircraft utilization rates. This directly translates to greater demand for new engines and, more importantly, consistent aftermarket servicing, which is a core profit driver for GE Aerospace. Management, under CEO Larry Culp, has also strategically navigated external challenges. They localized supply chains, secured alternate component sources, and optimized logistics costs. These actions proved critical in mitigating the impact of new tariff regimes and broader trade war tensions.

Geopolitical developments have significantly shaped GE Aerospace's trajectory. Notably, the U.S. government's decision to lift restrictions on exporting aircraft engines, including LEAP-1C and GE CF34 engines, to China's Commercial Aircraft Corporation of China (COMAC) reopened a vital market channel. This move, occurring amidst a complex U.S.-China trade environment, underscores the strategic importance of GE Aerospace's technology on the global stage. The company's robust financial performance further solidifies its position, with strong earnings beats, a healthy return on equity, and positive outlooks from a majority of Wall Street analysts. Institutional investors are actively increasing their stakes, signaling strong market confidence in GE Aerospace's continued growth potential.

Howmet Aerospace: Navigating Geopolitics to New Heights?Howmet Aerospace (HWM) has emerged as a formidable player in the aerospace sector, demonstrating exceptional resilience and growth amidst global uncertainties. The company's robust performance, marked by record revenues and significant earnings per share increases, stems from dual tailwinds: surging demand in commercial aerospace and heightened global defense spending. Howmet's diversified portfolio, which includes advanced engine components, fasteners, and forged wheels, positions it uniquely to capitalize on these trends. Its strategic focus on lightweight, high-performance parts for fuel-efficient aircraft like the Boeing 787 and Airbus A320neo, alongside critical components for defense programs such as the F-35 fighter jet, underpins its premium market valuation and investor confidence.

The company's trajectory is deeply intertwined with the prevailing geopolitical landscape. Escalating international rivalries, particularly between the U.S. and China, coupled with regional conflicts, are driving an unprecedented surge in global military expenditures. European defense budgets are expanding significantly, fueled by the conflict in Ukraine and broader security concerns, leading to increased demand for advanced military hardware incorporating Howmet’s specialized components. Simultaneously, while commercial aviation navigates challenges like airspace restrictions and volatile fuel costs, the imperative for fuel-efficient aircraft, driven by both environmental regulations and economic realities, solidifies Howmet’s role in the industry’s strategic evolution.

Howmet's success also reflects its adept navigation of complex geostrategic challenges, including trade protectionism. The company has proactively addressed potential tariff impacts, demonstrating a capacity to mitigate risks through strategic clauses and renegotiation, thereby protecting its supply chain and operational efficiency. Despite its premium valuation, Howmet’s strong fundamentals, disciplined capital allocation, and commitment to shareholder returns highlight its financial health. The company's innovative solutions, crucial for enhancing the performance and cost-effectiveness of next-generation aircraft, solidify its integral position within the global aerospace and defense ecosystem, making it a compelling consideration for discerning investors.

Embraer–Soaring on Regional Jet Demand &Global Defense ExpansionCompany Overview:

Embraer NYSE:ERJ is a top-tier aerospace manufacturer, delivering commercial jets, executive aircraft, and cutting-edge defense platforms. With a dominant position in the sub-150-seat market, it's primed to benefit from structural aviation tailwinds.

Key Catalysts:

$680B Market Opportunity 📈

Global demand forecast for 10,500 regional jets/turboprops over the next 20 years.

Embraer, with its E-Jet family, is positioned to capture meaningful share amid rising demand for regional connectivity and fleet efficiency.

Defense Momentum 🛡️

C-390 Millennium sales to Portugal and the Netherlands enhance NATO exposure.

Recent A-29N Super Tucano contracts expand Embraer’s tactical footprint, with follow-on order potential from NATO allies.

Resilience to Tariffs + Margin Protection ⚙️

Q1 results unaffected by new U.S. tariffs, thanks to global supply chain integration and high U.S.-sourced content.

Ongoing cost-cutting and trade advocacy expected to preserve margins.

Investment Outlook:

Bullish Case: We remain bullish on ERJ above $44.00–$45.00.

Upside Target: $72.00–$74.00, supported by commercial demand tailwinds, defense diversification, and cost discipline.

✈️ Embraer is flying high—with commercial orders climbing and global defense contracts in formation.

#Embraer #ERJ #Aerospace #RegionalJets #DefenseContracts #NATO #AviationMarket #IndustrialStocks #TariffResilience #C390 #SuperTucano #Bullish

GE AERO WHERE WILL THE PRICE GOTRENDS and Price targets marked.

Price appears to be in "danger zone" or high side with not many price targets left.

There are both support and rejection trends trading down in the short term.

These both lead to a support trend.

Good luck.

Follow for more charts like this.

These 2 Signals Made Members 80% Profit!NYSE:GE has had a massive rejection off of Monthly chart rejection.

We issued an alert to members om June 6th 2025. We entered a 245 Put (July 3) $5 con

We closed out our contracts today at $9 and roughly 80% gain.

This chart demonstrates the power of multiyear monthly chart resistance. Trades like these don't come around often but when they do you have to execute and forget about the noise!

This chart proves that technical trendlines do have power!

GE Aerospace: How to go to the moon!GE's stock is soaring due to strong earnings and optimistic future guidance from its aerospace division.

1. Blowout Earnings: GE Aerospace reported earnings per share of $1.75, far exceeding analysts' expectations of $1.10.

2. Surging Orders: The company saw a 46% increase in orders last quarter, signaling strong demand for its products.

3. Revenue Growth: GE generated $10.8 billion in revenue, beating forecasts of $10 billion.

4. Wall Street Optimism: Analysts are raising price targets, with some predicting the stock could climb even higher.

5. Industry Momentum: The aerospace sector is experiencing a boom, with GE positioned as a key player.

I'm betting we are close to a pullback and then catapult to New ATH!