3d world war is coming!;(Bit on oil and Bitcoin to pass the war it will be to hard future is darrrk!

Brent

USOILIs there some value in oil longs here, we can see we are trading just below the fair value range highlighted by the VP, price has contracted and broken the fixed VP, we could look to take some longs back to a fairer price here.

Brent: You Can Do It!On its way down, Brent got stuck at the support line at $97.56. However, we expect it to struggle through and to make it into the blue zone between $94.50 and $89.73, where it should finish wave 5 in blue and wave a in turquoise. Then, Brent should move upwards, crossing even the resistance at $107.64, above which it should complete wave b in turquoise. Afterwards, Brent should resume the downwards movement and drop back below $107.64 as well as below $97.56.

Possible Movements on Crude Oil + Short Setup Explained. The price of crude oil has been moving sideways between 95 and 125.

As a general rule, 90% of the time, I only trade once the price reaches key levels. In this case, the price is in the support zone. Therefore, I have looked for all the scenarios where the price was behaving similar to what it is now (we can define it as a triple bottom). Of course, in some of them, the price bounces, and in the other half, the price breaks it starting a new bearish trend.

The idea of today's post is to explain the scenario I'm considering trading . (Short scenario).

Let's start with the general context . In February 2022, the price reached the weekly resistance zone after Ukraine's invasion, and we observed clear reactions there.

I can define two zones that may work as potential bullish and bearish targets.

Bearish Target: 80.00

Bullish Target: 120.00

Now, let's look at the current situation. It's important to say that no one knows the direction the price may take; the following description is about a setup that I will only take if the price moves as expected.

I'm working on a short setup that looks as follows. Why? Because I have tested this situation in the past, and it's consistent in its resolution. The distance between the current support level and the weekly bearish target provides great bearish potential.

The main concept of this entry is waiting for the price to go below the support zone and then observing a pullback. IF that happens, I will set pending orders on a new low and stop loss at the end of the pullback. The target is defined in the next weekly support zone.

I will not be developing bullish setups yet because the filters I should be waiting for do not provide an acceptable Risk to reward ratio towards the next resistance zone.

Of course, this situation requires patience, and it's important to have clear filters to say, "Now I will set my orders." The risk I will be using on this setup is 3% of my capital on my stop loss; if everything goes as expected, this position should take between 20 to 45 days.

I hope this content was helpful; let me know your view in the comments!

Brent Crude Oil - Elliott wave theoryHave we just completed Elliott wave 1 of a crude oil bull market which I would argue started in November 2021 with Pfizer vaccine news?? Others may say it started from June 2020 after the May 2020 crash low touching zero or below briefly.

I have a question for viewers if Elliott waves up to 5 does indeed play out again for oil (and commodities in general) how can one have any clue how much time this will take?

Please refer to March 1999 (just before dot com crash) through to June 2008 (onset of GFC) Brent crude oil price chart to see how Elliott waves 1, 3 & 5 up-moves happened with waves 2 & 4 corrections.

India tricks the West, Strong dollar & China imports russian oilOil top might be in for this year.

Reasons:

1. Market adjustment mechanisms are underway on the commodity markets, ensuring that Russian oil, which is spurned by the West, once again finds its buyers (india, china). This in turn causes these countries to demand less Brent or WTI oil, which again depresses prices. India and China are buying significantly more crude oil from Russia, Europe less, which means there is a balancing out taking place on the world markets with the new tanker routes and transportation routes.

2. India recently bought more oil from Russia than ever before, according to a recent report by the Finnish Energy and Clean Air Research Center. "A significant portion of the crude is re-exported as refined oil products, including to the U.S. and Europe, an important loophole to close," the Finnish analysts warned. Since new sanctions measures are very unlikely, the alignment process between Russian oil and Brent and WTI crudes is likely to continue.

3. Dollar price, interest hikes & recession fears by FED. The strong dollar is also acting as an additional burden on the oil market. This is because commodities such as oil are traded in dollars. If you read between the lines of the FED, they're doing their best to crush commodity and oil prices to crush long-speculators on comm and oil.

4. Fear of new lockdowns in China. Chinese head of state Xi Jinping nevertheless only recently announced that he would stick to the strict zero-covid strategy. This is fueling fears of new lockdowns in China = downside risk for oil demand in China, probably a small impact, since the gov in China is trying its best to avoid a greater corona outbreak in large cities to stabilise eco. situation.

5. bitcoin/tradional markets are sometimes seen as counterparts to oil. Bitcoin, despite very bad news (CPI increased) and being a risk asset, has not moved much further down in price, showing that risky assets have more or less found their bottom while oil bulls have an empty tank.

Opinion: I see the price cooling down slowly rather than continuing to climb, probably going towards 70-60$ in the next 6-10 months.

! This is not an investment advise! Do your own research! This is NOT a recommendation to buy or sell oil shares and this is NOT a recommendation to short or to long oil!

CRUDE OIL (WTI) Important Update 🛢

As I predicted, WTI Oil dropped nicely yesterday.

The price formed a head and shoulders pattern.

To catch a bearish continuation, watch 100.3 - 102.0 horizontal neckline.

We need a 4H candle close below that to confirm the breakout.

Then, shorting on a retest, a bearish continuation will be expected to 97.2 level.

If the price sets a new high, the setup will be invalid, though.

❤️If you have any questions, please, ask me in the comment section.

Please, support my work with like, thank you!❤️

High chances of a WTI bullish reversalAfter a major 7%+ drop yesterday WTI is starting to show signs of a possible reversal.

To be a successful day trader, or any kind of trader/investor for that matter, you need to have an arsenal of patters which have worked for you in the past and have a high probability rate of success. To us this is one of those patterns, and below is the criteria:

- Price at strong lows

- Price action starts forming higher lows

- Straight line resistance

Thats all there is to it, this pattern is NOT completed yet, but it is starting to show signs of it hence why I added "high chances" in the subject of this post.

I am watching it like a hawk and will be ready to execute long positions if the pattern is completed.

This pattern has worked for me more times that it has not hence why I am super focused on taking advantage of it if it works up and start buying WTI, while if it fails I'll be ready to sell, but only if there is strong enough momentum.

What patterns work best for you?

*See the related post for higher time frame analysis

West Texas Oil to remain underpressure?WTI - Intraday - We look to Sell at 96.74 (stop at 100.41)

The medium term bias remains bearish. A sequence of daily lower lows and highs has been posted. We can see no technical reason for a change of trend. There is scope for mild buying at the open but gains should be limited. Further downside is expected although we prefer to sell into rallies close to the 97.00 level.

Our profit targets will be 88.17 and 86.00

Resistance: 97.00 / 112.73 / 126.60

Support: 88.00 / 76.50 / 60.00

Risk Disclaimer

The trade ideas beyond this page are for informational purposes only and do not constitute investment advice or a solicitation to trade. This information is provided by Signal Centre, a third-party unaffiliated with OANDA, and is intended for general circulation only. OANDA does not guarantee the accuracy of this information and assumes no responsibilities for the information provided by the third party. The information does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

You accept that you assume all risks in independently viewing the contents and selecting a chosen strategy.

Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, Oanda Asia Pacific Pte Ltd (“OAP“) accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore customers should contact OAP at 6579 8289 for matters arising from, or in connection with, the information/research distributed.'

CRUDE OIL (WTI) Very Bearish Outlook 🛢

WTI Crude Oil retraced to a peculiar zone of confluence on 4H:

we see a perfect match between a horizontal structure and 618 retracement of the last bearish impulse.

Reaching that structure, the price broke a support line of a rising wedge pattern on 1H.

I expect a bearish continuation now.

Goals: 101.93 / 100.0

❤️If you have any questions, please, ask me in the comment section.

Please, support my work with like, thank you!❤️

Today’s Notable Sentiment ShiftsCAD – The Canadian dollar weakened on Tuesday as oil prices tumbled. Still, losses for the currency were limited by growing expectations for an oversized interest rate hike this week by the Bank of Canada.

Commenting on CAD, Adam Button – chief currency analyst at ForexLive, stated: “There’s a reluctance to sell the loonie ahead of a Bank of Canada decision. A three-quarter-point hike is widely priced in but that could also be coupled with hints at further large hikes.”

Growth of Brent crude oil, ceased?! HEY traders, what's going on today?!

Oil is down ahead of Biden's trip to Middle East , and it seems that want to be decreased more

Prices of crude oil futures decreased by over 2% on Tuesday as market participants assessed United States President Joe Biden's chances of negotiating an increase in oil production from OPEC countries during his trip to the Middle East later this week. so it seems the geopolitical situation shows the declining of the price of oil it the future.

Also the another coronavirus wave in Asia and global economic downturn concerns could threaten demand for crude.

and as we can BRN1! has been going all the way up from 16$ to 139$ , So now I thing it can correct now on the lower support zone in the mid-term , or according to bars pattern can follow the the rest candles .

news sources :teletrader.com

✌️ Good luck with your trading and investing and remember: Trade smart…OR JUST DON’T TRADE!

--------------------------------------------------------------------------------------------------------------------

👉This analysis is my personal opinion ,not a financial advice ,so do your own research.

💜 if you're fan of my analyses please follow me , give a big thumbs 👍 OR drop a comment 🗯

Brent Outlook (12 July 2022)Following the OPEC+ decision to increase production levels, expectation was for energy prices to trade in a horizontal range, with downside limited by the 100 price level.

However the new wave of covid infections in China has triggered fears of intensified lockdowns and further economic slowdowns.

With lower demand expected, this has led to Brent trading lower at the 100 level, with a high likelihood to test lower, with next support level at 95.00 and 84.00

WTI oil - The backwardation points to the lower price of oilIn the past three months, we warned investors about the imminent trend reversal in the oil market. Accordingly, we set price targets for USOIL at 100 USD, 95 USD, and 90 USD. Yesterday, our short-term price target of 100 USD was taken out. Due to that, we would like to update our thoughts on USOIL. We continue to be bearish on the asset and expect the volatility to stay persistent throughout the third quarter of 2022. Additionally, we expect the prospect of a global recession and production hikes to impact the price negatively. Our views are also supported by bearish technical developments across daily, weekly, and monthly time frames. Because of that, we would like to update our medium-term price target of 95 USD to the short-term price target; additionally, we would also like to update our long-term price target of 90 USD to the medium-term.

Illustration 1.01

WTI oil dropped approximately 25% from its 2022 high to yesterday's low, entering the bear market territory.

Technical analysis - daily time frame

RSI, MACD, and Stochastic are all bearish. The same applies to DM+ and DM-. The ADX hints at growing bearish momentum. Overall, the daily time frame is bearish.

Illustration 1.02

The picture above shows crude oil futures for September 2022. The market backwardation hints at lower prices for oil in the future.

Technical analysis - weekly time frame

RSI, MACD, Stochastic, DM+, DM- are all bearish. Overall, the weekly time frame is bearish.

Illustration 1.03

Illustration 1.03 shows another oil futures contract, but for January 2023. These contracts trade at far less, near the 87 USD price tag.

Please feel free to express your ideas and thoughts in the comment section.

DISCLAIMER: This analysis is not intended to encourage any buying or selling of any particular securities. Furthermore, it should not be a basis for taking any trade action by an individual investor. Therefore, your own due diligence is highly advised before entering a trade.

A complete review of Brent oil with Elliott styleConsidering that oil left its long-term correction process on April 20, 2022; It started an increasing and powerful process and increasing tensions and war made this process more powerful.

By carefully examining this trend, it can be said that this trend ended in 5 waves; And now, with the situation balancing a little, the stagnation, the increase in oil production, and at the same time the permission of Venezuela to enter the oil market; The price has entered price correction. It should be expected that this price correction will be in the form of a wave (ABC).

Considering the price movement in the lower time frame, it can be expected that wave A will be formed in the form of 5 waves.

I believe; Currently, wave 1 is being completed, so we have to wait for wave 2 to be created.

If the end of wave 2 is 115; This analysis is complete and you can make the most of the other waves shown.

It should be considered that with the price reaching the range of 36-39.5 in the consolidation of the higher time frame, this whole movement can be considered as wave 1 and 2.

Tip: We have to see how the trend will be formed along the downward path; It is possible that this entire decline in price can be shown in the higher consolidation of an A wave.

In any case, upon reaching the price range of 36 to 39.5, the trend should be re-examined and a new analysis should be presented.

This analysis is prepared with an economic perspective; But from a human point of view, I am very sorry for the war and I sincerely sympathize with Ukraine.

what is your opinion ?

(be profitable)

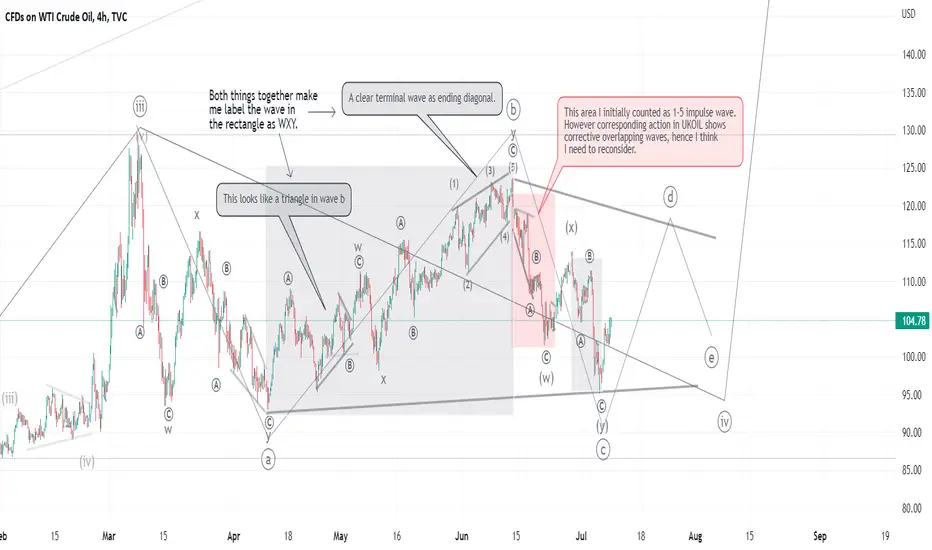

USOIL UpdateMy best count on USOIL . I am also working on the bearish alternative to make sure I covered all scenarios, but I must admit I struggle with it. I hold RIG and therefore biased on oil .

USoil for new week according to new HH since last week , it’s possibly to get more higher prices with lots of pullback. i think 106, 108 and 110 will happen for WTI ( (USOIL) in the new week.

CRUDE Bounced off & rehash...As previously expected, Crude bounced off 95 (95.10 to be exact) and it bounced off with gusto, to reclaim 100 support. The bounce was a fast intraday check-in at 95, and the following day clocked a bullish engulfing of sorts. This was then followed by another bullish day to end the week with a long lower tail, indicative that between 95 to 100, likes a lot of demand.

The daily technical indicators are starting to crossover.

This recovery bounce is also awesome as it broke down and out of the triangle and then returned back in. For technical analysts, we do know that when this happens, there is a higher probability that there will be an exit on the other side... ie. a breakout is imminent.

Note that the triangle was updated by readjustment from previously.

In the weekly chart, while the technical indicators are still trudging lower, the candlestick shows a temporary spike out of the triangle only to make it back in. This is a bullish indication IMHO.

Taken together, expect the bullish run to meet some resistance about 112-114 in the following days of the incoming week. There needs to be a higher low, that bounces off the triangle support... and then we just might get a bull run breakout in early August 2022.

Watch this one!

ps. Target breakout (dotted green arrow) and upside target of 165 updated. Pennant pattern (fibonacci) projection also added (dashed green arrow)

USOILCould have imbalance in the market as oil rises above this area of fair value, seems to be rejecting this area so we have to aim for an area where previously the market has balanced, we have this on the VP at around $108.