#CYBER/USDT Forming Bullish Continuation ?#CYBER

The price is moving in a descending channel on the 1-hour timeframe. It has reached the lower boundary and is heading towards a breakout, with a retest of the upper boundary expected.

We are seeing a bearish trend in the Relative Strength Index (RSI), which has reached near the lower boundary, and an upward bounce is expected.

There is a key support zone in green at 0.740, and the price has bounced from this level several times. Another bounce is expected.

We are seeing a trend towards stabilizing above the 100-period moving average, which we are approaching, supporting the upward trend.

Entry Price: 0.760

First Target: 0.778

Second Target: 0.800

Third Target: 0.840

Remember a simple principle: Money Management.

Place your stop-loss order below the green support zone.

For any questions, please leave a comment.

Thank you.

Cybersecurity

Can a Former Penny Stock Become a Defense Tech Powerhouse?Ondas Holdings Inc. (NASDAQ: ONDS) has executed a remarkable 30% surge, climbing from early-year lows of $0.57 to near its 52-week high of $11.70. This dramatic recovery reflects more than market momentum; it signals a fundamental transformation from a collection of disparate assets into a unified defense technology platform. The company's rebranding to "Ondas Inc." in Q1 2026, along with its strategic relocation to West Palm Beach, Florida, underscores management's commitment to establishing a cohesive identity within the aerospace and defense sector.

The company's growth trajectory is anchored by substantial contract wins and an expanding product ecosystem. Ondas secured a landmark government tender to deploy thousands of autonomous drones for border protection, while recording $16.4 million in counter-UAS orders from major European airports. With revenue targets of at least $110 million for 2026, representing 200% growth over 2025's $36 million, the company is positioning itself for a transition from small-cap to mid-cap visibility. This forecast is supported by a record $23.3 million backlog and a strengthened balance sheet featuring $68.6 million in cash reserves.

Ondas has built competitive advantages through strategic acquisitions and proprietary technology. The acquisition of Sentrycs brought advanced "Cyber-over-RF" capabilities that enable non-jamming drone mitigation—critical for operations in dense urban environments. Combined with its FullMAX platform for mission-critical IoT and precision optics IP from SPO, Ondas offers end-to-end multi-domain autonomy solutions. The company's recent AI-powered humanitarian demining pilot in the Middle East, which identified nearly 150 hazardous items across 22 acres, demonstrates the versatility of its technology beyond traditional defense applications. As global demand for autonomous security solutions intensifies, Ondas appears positioned to capture significant market share across border security, infrastructure protection, and humanitarian operations.

Can Japan's Steel Giant Win the Green War?Nippon Steel Corporation stands at a critical crossroads, executing a radical transformation from domestic Japanese producer to global materials powerhouse. The company targets 100 million tons of global crude steel capacity under its "2030 Medium- to Long-term Management Plan," seeking 1 trillion yen in annual underlying business profit. However, this ambition collides with formidable obstacles: the politically contested $14.1 billion U.S. Steel acquisition faces bipartisan opposition despite Japan's allied status, while the strategic withdrawal from China, including dissolving a 20-year joint venture with Baosteel, signals a decisive "de-risking" pivot toward Western security frameworks.

The company's future hinges on its aggressive Indian expansion through the AM/NS India joint venture, which plans to triple capacity to 25-26 million tons by 2030, capturing the subcontinent's infrastructure boom and favorable demographics. Simultaneously, NSC is weaponizing its intellectual property dominance in electrical steel critical for EV motors through unprecedented patent litigation, even suing major customer Toyota to protect proprietary technology. This technological moat, exemplified by brands like "HILITECORE" and "NSafe-AUTOLite," positions NSC as an indispensable supplier in the global automotive lightweighting and electrification revolution.

Yet existential threats loom large. The "NSCarbolex" decarbonization strategy requires massive capital expenditures of 868 billion yen for electric arc furnaces alone, while bridging to unproven hydrogen direct reduction technology by 2050. Europe's Carbon Border Adjustment Mechanism threatens to tax NSC's exports into oblivion, forcing accelerated retirement of coal-based assets. The March 2025 cyberattack on subsidiary NSSOL exposed digital vulnerabilities as operational technology converges with IT systems. The NSC faces a strategic trilemma: balancing growth in protected markets, ensuring security through supply chain decoupling, and making sustainability investments that threaten near-term solvency. Success demands flawless execution across geopolitical, technological, and financial dimensions, simultaneously a precarious bet on reshaping the global steel order.

BlackBerry still encrypts, just not phones anymoreBB closed the week at 4.28. The weekly chart shows a symmetric triangle forming after a fully completed falling wedge. The key point is that price has already reacted from the 0.618 Fibonacci level near 4.00, which aligns with the highest volume area on the Volume Profile and a clear demand zone. A golden cross between MA50 and MA200 on the weekly timeframe adds strong confirmation to the medium term bullish structure. As long as price holds above 4.00, the setup remains constructive with upside potential toward 6.00 and 8.35.

On fundamentals as of December 14, 2025, BlackBerry continues its shift into cybersecurity and software solutions. Fiscal year revenue is around 1.05 billion dollars, with steady growth in IoT and QNX driven by automotive and industrial contracts. Cash reserves exceed 250 million dollars, debt remains limited, and management is focused on margin expansion and strategic partnerships.

BlackBerry is no longer chasing hype, it is quietly building infrastructure.Sometimes the quiet names move first.

Is Cisco Building the Internet of Tomorrow or Something Else?Cisco Systems has undergone a dramatic transformation in 2025, evolving from a traditional hardware vendor into what the company positions as the architect of secure, AI-driven global infrastructure. With fiscal year 2025 revenue reaching $56.7 billion and a remarkable 30% surge in operating cash flow, Cisco's financial performance tells only part of the story. The company has strategically positioned itself at the intersection of three critical technological timelines: the immediate AI infrastructure boom, the ongoing geopolitical supply chain realignment, and the long-term quantum computing development.

The company's geopolitical strategy has been particularly aggressive. In response to escalating US-China trade tensions and tariffs reaching up to 145% on certain components, Cisco has pivoted its manufacturing operations to India, establishing it as a new global export hub. Simultaneously, the company launched its Sovereign Critical Infrastructure portfolio in Europe, offering air-gapped solutions that address European concerns about digital sovereignty and US extraterritorial reach. These moves position Cisco as the "trusted vendor" for Western alliance infrastructure while monetizing the fragmentation of the global internet.

On the technology front, Cisco has made bold bets on the future. A landmark partnership with IBM aims to build the world's first large-scale quantum network by the early 2030s, with Cisco developing the optical infrastructure to connect quantum processors. The company has also integrated SpaceX's Starlink into its SD-WAN portfolio and participated in NASA's Artemis program. Meanwhile, its AI-native Hypershield security platform, protected by the company's 25,000th patent, and the integration of the Splunk acquisition demonstrate Cisco's push into AI-era cybersecurity.

The convergence of these initiatives reveals a company no longer simply selling networking equipment, but rather positioning itself as essential infrastructure for Western technological sovereignty. With explosive demand from hyperscaler customers generating over $2 billion in AI infrastructure orders and analysts raising price targets amid a 25% stock rally, Cisco appears to have successfully weaponized the geopolitical moment to reinforce its market position for the next generation of computing.

A10 Networks (ATEN) — DDoS, ADC, and Edge Security TailwindsCompany Overview

A10 Networks NYSE:ATEN provides advanced cybersecurity and application delivery across cloud, hybrid, and carrier networks—direct exposure to rising demand for DDoS protection, secure networking, and cloud infra security.

Key Catalysts

Threat Landscape & Compliance: Escalating global cyberattacks + stricter regs are accelerating adoption of Thunder ADC and ThreatX—mission-critical for high-performance, distributed environments.

Execution Momentum: Q3’25 revenue $75M (≈+5.6% beat) and EPS $0.17 (≈+9.7% beat) underscore resilient demand and leverage to a recovering IT spend cycle.

5G & AI Infrastructure: A10’s load balancing, DDoS, and edge security sit in the flow of 5G rollouts and AI data center growth, supporting multi-year capacity upgrades.

Platform Differentiation: Carrier-grade performance, automation, and visibility help consolidate point tools while optimizing latency and throughput.

Why It Matters

✅ Direct play on cloud + telco capex (5G/edge)

✅ Beneficiary of AI-era traffic growth and low-latency requirements

✅ Balanced mix of appliance, software, and subscription helps cushion cycles

Investment Outlook

Bullish above: $14.75–$15.00

Target: $22.00–$23.00 — driven by enterprise/telco upgrades, AI/edge security demand, and continued operating discipline.

📌 ATEN — securing next-gen networks with high-performance ADC and DDoS protection.

$CRWD: Secular outperformer in Cybersecurity. CrowdStrike is the bellwether of the cybersecurity sector. I have time and again reiterated my bullish thesis on the $CRWD.

In May I said the near-term target is 500 $.

NASDAQ:CRWD : Exceptional performance. Next stop 500 $. for NASDAQ:CRWD by RabishankarBiswal — TradingView

In June I reiterated my price target of 520 $ and said that the stock is headed to 700 $ in the long term.

NASDAQ:CRWD : Relative outperformance compared to its peers for NASDAQ:CRWD by RabishankarBiswal — TradingView

Since then, we have decisively broken above 520 $ and if the momentum continues then by end of Jan 2026, we might see a 700 $ stock.

In the chart below I have plotted the ratio chart between the cybersecurity ETF AMEX:HACK vs $CRWD. In the last 5 years stock has continually outperformed. I think the outperformance continues into 2026 and 2027.

Trade Set Up : Stay bullish on NASDAQ:CRWD over $HACK. 700 $ in sight and 1500 $ by 2027.

Is IBM Building an Unbreakable Cryptographic Empire?IBM has positioned itself at the strategic intersection of quantum computing and national security, leveraging its dominance in post-quantum cryptography to create a compelling investment thesis. The company led the development of two of the three NIST-standardized post-quantum cryptographic algorithms (ML-KEM and ML-DSA), effectively becoming the architect of global quantum-resistant security. With government mandates like NSM-10 requiring federal systems to migrate by the early 2030s, and the looming threat of "harvest now, decrypt later" attacks, IBM has transformed geopolitical urgency into a guaranteed, high-margin revenue stream. The company's quantum division has already generated nearly $1 billion in cumulative revenue since 2017—more than tenfold that of specialized quantum startups—demonstrating that quantum is a profitable business segment today, not merely an R&D cost center.

IBM's intellectual property moat further reinforces its competitive advantage. The company holds over 2,500 quantum-related patents globally, substantially outpacing Google's approximately 1,500, and secured 191 quantum patents in 2024 alone. This IP dominance ensures future licensing revenue as competitors inevitably require access to foundational quantum technologies. On the hardware front, IBM maintains an aggressive roadmap with clear milestones: the 1,121-qubit Condor processor demonstrated manufacturing scale in 2023, while researchers recently achieved a breakthrough by entangling 120 qubits in a stable "cat state." The company targets deployment of Starling, a fault-tolerant system capable of running 100 million quantum gates on 200 logical qubits, by 2029.

Financial performance validates IBM's strategic pivot. Q3 2025 results showed revenue of $16.33 billion (up 7% year-over-year) with EPS of $2.65, beating forecasts, while adjusted EBITDA margins expanded by 290 basis points. The company generated a record $7.2 billion in year-to-date free cash flow, confirming its successful transition toward high-margin software and consulting services. The strategic partnership with AMD to develop quantum-centric supercomputing architectures further positions IBM to deliver integrated solutions at exascale for government and defense clients. Analysts project IBM's forward P/E ratio may converge with peers like Nvidia and Microsoft by 2026, implying potential share price appreciation to $338-$362, representing a unique dual thesis of proven profitability today combined with validated high-growth quantum optionality tomorrow.

NTSK Netskope: the rocket is on the padNetskope’s shares (ticker NTSK) are trading after a successful IPO, but the chart suggests we’re still in early accumulation phase. The price is hovering in the ~$21-24 zone, and a breakout above near resistance is needed to confirm strength. The first target is $28, with potential extension toward $35–40 if the structure holds. Given IPO volatility, entry requires careful stop-management and confirmation of trend support.

Netskope operates in the rapidly expanding cloud security market (SASE/Zero Trust). With revenue growth exceeding 30% and narrowing losses, the company is well-positioned in the AI-security wave. While the TAM (total addressable market) is large and growth prospects strong, the business still faces profitability and competitive risks.

The rocket may not yet be launched, but the launchpad is set. Stay patient, wait for the “ignition” signal, and let the engine build thrust before liftoff.

Can Defense Giants Print Money During Global Chaos?General Dynamics delivered exceptional Q3 2025 results with revenue reaching $12.9 billion (up 10.6% year-over-year) and diluted EPS soaring to $3.88 (up 15.8%). The company's dual-engine growth strategy continues to drive performance: its defense segments capitalize on mandatory global rearmament driven by escalating geopolitical tensions, while Gulfstream Aerospace leverages resilient demand from high-net-worth individuals. The Aerospace segment alone grew revenue by 30.3% with operating margin expanding 100 basis points, delivering record jet deliveries as supply chains normalized. Operating margin reached 10.3% overall, with operating cash flow hitting $2.1 billion—an extraordinary 199% of net earnings.

The defense portfolio secures decades of revenue visibility through strategic programs, most notably the $130 billion Columbia-class submarine program, which represents the U.S. Navy's top acquisition priority. General Dynamics European Land Systems has secured a €3 billion contract from Germany for next-generation reconnaissance vehicles, capitalizing on record European defense spending that reached €343 billion in 2024 and is projected to reach €381 billion in 2025. The Technology division strengthened its position with $2.75 billion in recent IT modernization contracts, deploying AI, machine learning, and advanced cybersecurity capabilities for critical military infrastructure. The company's 3,340-patent portfolio, with over 45% still active, reinforces its competitive moat in nuclear propulsion, autonomous systems, and signals intelligence.

However, significant operational headwinds persist in the Naval segment. The Columbia-class program faces a 12-to 16-month delay, with the first delivery now anticipated between late 2028 and early 2029, driven by supply chain fragility and specialized workforce shortages. Late delivery of major components forces complex out-of-sequence construction work, while the defense industrial base struggles with critical skill gaps in nuclear-certified welders and specialized engineers. Management emphasizes that the upcoming year will be pivotal for driving productivity improvements and margin recovery in Naval operations.

Despite near-term challenges, General Dynamics' balanced portfolio positions it for sustained outperformance. The combination of non-discretionary defense spending, technological superiority in strategic systems, and robust free cash flow generation provides resilience against volatility. Success in stabilizing the submarine industrial base will determine long-term margin trajectory, but the company's strategic depth and cash generation capability support continued alpha generation in an increasingly uncertain global environment.

From Fallen Giant to Trillion-Dollar Titan — "BlackBerry"From fallen giant to future trillion-dollar titan.

The world forgot BlackBerry… but smart money didn’t. 👀📈

Once the undisputed king of smartphones, BlackBerry (BB) collapsed under the weight of innovation it helped create. But while the world moved on, BlackBerry quietly evolved — transforming from a phone maker into a global cybersecurity, AI, and IoT powerhouse .

Now, the charts and fundamentals whisper the same story: the comeback may already be in motion. 📈🔥

🧠 The New BlackBerry: The Silent Infrastructure of the Digital Age

🔒 Cybersecurity Backbone:

BlackBerry’ s Cylance AI secures over 250M+ endpoints worldwide — protecting enterprises, governments, and critical systems. As AI-driven cyber threats rise, BB’s advanced detection tech is becoming a necessity, not a luxury.

🚗 Automotive Intelligence (QNX):

Over 235M vehicles already run on BlackBerry QNX , trusted by automakers like BMW, Ford, Toyota, and Volkswagen. QNX isn’t just car software — it’s the operating system for the connected vehicle future . With autonomous mobility on the rise, every car is a potential BlackBerry endpoint.

☁️ IoT Expansion with AWS:

Through BlackBerry IVY , co-developed with Amazon Web Services, BB is redefining how vehicles and smart devices share data securely. As the world connects billions of devices, BB could become the security standard behind the Internet of Everything. 🌐

⚡ The Technical Confluence — Smart Money & Wave Theory Alignment

🌀 Elliott Wave 2 correction nearing completion — exhaustion where disbelief reigns.

⚡ Wave 3 ignition potential: historically the most powerful and extended wave.

💰 Smart Money footprints: liquidity sweeps, BOS, and accumulation in key zones hint at institutional accumulation.

📏 Fibonacci 0.786 retracement and 1.618–2.618 extensions align perfectly with historical reversal levels — high-conviction confluence for a generational setup.

This is the phase where patience pays and noise fades .

💎 The Macro Mirror — History Doesn’t Repeat, But It Rhymes

Every great tech story began in disbelief:

NVIDIA (NVDA) was once a $3 stock before AI made it a trillion-dollar icon.

Tesla (TSLA) was ridiculed before redefining transportation.

Palantir (PLTR) quietly built data infrastructure before Wall Street caught up.

Now BlackBerry stands at a similar inflection — undervalued, under-owned, and misunderstood .

It’s no longer about phones — it’s about owning the digital nervous system of the future .

📅 Accumulation: 2024–2028

🚀 Expansion: 2029–2044

🌕 Euphoria: 2045+

"The world once held BlackBerry in its hand. Soon, it might hold the world in its network."🌍✨

Traders!

💬 What do you think — is BlackBerry quietly preparing to shock the world again? — Team FIBCOS

#BlackBerry #ElliottWave #BB #SmartMoney #Fibonacci #IoT #Cybersecurity #AI #LongTermInvesting #TechRebirth #TradingView #ComebackStory

SentinelOne | S | Long at $17.04SentinelOne NYSE:S : a cybersecurity company that uses an autonomous AI-powered platform to performs real-time threat detection, prevention, and remediation across endpoints, cloud, and IoT.

Technical Analysis

Price is consolidating along my historical simple moving average (a regression to the mean). This is after a meteoric rise in 2021 to $78.53 (just after the IPO) and then collapse to $12.43 in 2023. While near-term ups and downs may persist for a bit, usually a price consolidation near the historical simple moving average eventually leads to a major move. The simple moving average band is getting tighter, signaling the potential for a move out of the zone "soon". Given the grow, niche, and need, the future may be bright with this one.

Growth

www.tradingview.com

820% growth expected in earnings per share between 2024 ($0.05) to 2027 ($0.46)

75% revenue growth projected between 2024 ($821 million) to 2027 ($1.4 billion)

Health

Debt-to-equity: 0 (perfection)

Altman's Z Score \ Bankruptcy Risk: 3.3 (extremely low risk)

Quick Ratio: 1.7 (they are able to pay current bills without relying on debt)

Insiders

Warning: Lots of selling and no buying...

openinsider.com

Action

SentinelOne NYSE:S is an extremely healthy company with very high-growth potential. However, the cybersecurity landscape is highly competitive, but NYSE:S is forming a niche with AI-powered tools. While insider selling is a red flag, that is all I can see here besides competition (or the company secretly falling apart behind the scenes). That's the risk we all take as investors. Thus, at $17.04, NYSE:S is in a personal buy zone.

Targets into 2028

$24.00 (+40.8%)

$27.50 (+61.4%)

NET — AI Infrastructure Leader Launches Stablecoin InnovationCompany Overview:

Cloudflare, Inc. NYSE:NET is a global leader in cloud connectivity and cybersecurity, delivering secure, scalable, and high-performance infrastructure for the modern internet. The company is evolving into a key enabler of AI-driven applications, with its Workers platform gaining strong enterprise traction to power large-scale intelligent workloads.

Key Catalysts:

Fintech breakthrough: The launch of the NET Dollar stablecoin bridges AI, cloud, and financial infrastructure, enabling automated machine-to-machine (M2M) payments and introducing new recurring revenue models.

Enterprise growth: Added 219 new large customers in Q2 2025, highlighting accelerating adoption and market leadership.

AI ecosystem expansion: Increasing integration of Cloudflare’s edge computing network within enterprise AI frameworks positions it at the core of the next-generation digital economy.

Investment Outlook:

Bullish above: $188–$190

Upside target: $380–$390, supported by AI infrastructure dominance, fintech innovation, and accelerating enterprise demand.

#Cloudflare #AI #Stablecoin #Cybersecurity #Fintech #DigitalInfrastructure #EdgeComputing #Investing #NET

Can Quantum Annealing Reshape Global Power?D-Wave Quantum Inc. has emerged as a distinctive player in commercial quantum computing by focusing on immediate utility through quantum annealing rather than waiting for fault-tolerant gate systems. The company's Advantage2™ system, featuring over 4,400 qubits, delivers production-grade solutions for complex optimization problems today, generating measurable ROI for clients like Ford Otosan, which reduced vehicle production scheduling from 30 minutes to under five minutes. This hybrid strategy of monetizing mature annealing technology while developing gate-model capabilities positions D-Wave to capture revenue now while hedging technological risk for the future. The quantum computing market's projected growth to $20.20 billion by 2030 (41.8% CAGR) and JPMorgan Chase's $1.5 trillion initiative, which explicitly includes quantum as a critical security technology, validate this sector beyond speculative investment.

D-Wave's recent scientific milestone, demonstrating "beyond-classical computation" on a magnetic materials simulation published in Science, marks a pivotal moment. The Advantage2™ prototype completed in minutes what would have required nearly one million years on classical supercomputers like Frontier, representing the first quantum supremacy claim on a commercially relevant, real-world problem. While classical researchers dispute aspects of the claim, the peer-reviewed validation drives enterprise confidence and accelerates bookings across manufacturing, pharmaceuticals, and energy sectors. Japan Tobacco's proof-of-concept using D-Wave's quantum-AI workflow generated drug candidates with superior properties compared to classical methods, addressing the pharmaceutical industry's 90%+ failure rate crisis.

Geopolitically, D-Wave has strategically embedded itself in European digital sovereignty initiatives, co-founding Italy's Q-Alliance to establish what aims to be the world's most powerful quantum hub. This dual-vendor partnership with IonQ provides Italy and the EU immediate access to D-Wave's production-ready annealing technology while hedging against future gate-model capabilities. Additional strategic deployments include Swiss Quantum Technology's €10 million investment and extended partnerships with Aramco Europe. The company's concentrated portfolio of 208 patent families in superconducting annealing creates defensible IP barriers, though significant risks remain: wider-than-expected losses despite 40% revenue growth, the Advantage2™ system's high cost barrier to adoption, and critical dependence on rare helium-3 supplies subject to geopolitical volatility.

Can Specialized Depth Trump Market Breadth in Cybersecurity?NetScout Systems (NASDAQ: NTCT) has emerged as a compelling investment opportunity at the intersection of escalating global cyber threats and artificial intelligence innovation. With DDoS attacks surging to over 8 million globally in the first half of 2025—including record-breaking attacks reaching 7.3 terabits per second—NetScout's specialized position in network security has garnered analyst attention, including B. Riley's recent "Buy" rating with a $33 price target. The company's unique value proposition lies in its patented Adaptive Service Intelligence (ASI) and Deep Packet Inspection (DPI) technologies, which transform raw network traffic into actionable "smart data" without disrupting operations.

The company's financial performance reflects this strategic positioning, with Q1 FY26 revenue growing 7% year-over-year to $186.75 million, driven by a remarkable 19.3% growth in product revenue. NetScout's enterprise segment has been particularly robust, expanding 17.7% annually and comprising 59% of total revenue, while serving high-value clients across government, healthcare, financial services, and telecommunications sectors. The company's gross profit margins of nearly 79% and strong balance sheet with more cash than debt underscore its operational efficiency and financial stability.

NetScout's competitive advantage stems from its focused specialization rather than broad market dominance. While holding only 2.82% of the Application Performance Monitoring market, the company has been recognized as a "Technology Leader" and "Ace Performer" in DDoS mitigation—a critical niche where depth matters more than breadth. The integration of AI and machine learning into its Arbor DDoS protection suite, combined with the ATLAS Intelligence Feed providing global threat visibility, positions NetScout as a force multiplier for understaffed security teams facing increasingly sophisticated attacks.

The strategic outlook appears promising, with the global DDoS protection market projected to grow from $4.34 billion in 2025 to $13.90 billion by 2034 at a 13.81% CAGR. NetScout's 46% international revenue exposure aligns well with rapid cybersecurity growth in Asia-Pacific, where the market is expected to exceed $146 billion by 2030. Despite facing competitive pressure in some segments, the company's focus on AI-enhanced hybrid solutions for large enterprises, coupled with its patent-protected intellectual property, creates a defensible position in an increasingly complex and high-stakes cybersecurity landscape.

#CYBER/USDT Forming Bullish Continuation ?#CYBER

The price is moving within a descending channel on the 4-hour frame, adhering well to it, and is heading for a strong breakout and retest.

We have a bearish trend on the RSI indicator that is about to be broken and retested, which supports the upward breakout.

There is a major support area in green at 1.77, representing a strong support point.

For inquiries, please leave a comment.

We are in a consolidation trend above the 100 Moving Average.

Entry price: 1.83

First target: 1.86

Second target: 1.88

Third target: 1.924

Don't forget a simple matter: capital management.

When you reach the first target, save some money and then change your stop-loss order to an entry order.

For inquiries, please leave a comment.

Thank you.

Can the World's Most Critical Company Survive Its Own Success?Taiwan Semiconductor Manufacturing Company (TSMC) stands at an unprecedented crossroads, commanding 67.6% of the global foundry market while facing existential threats that could reshape the entire technology ecosystem. The company's financial performance remains robust, with Q2 2025 revenue reaching $30.07 billion and over 60% year-over-year net income growth. Yet, this dominance has paradoxically made it the world's most vulnerable single point of failure. TSMC produces 92% of the world's most advanced chips, creating a concentration risk where any disruption could trigger global economic catastrophe exceeding $1 trillion in losses.

The primary threat comes not from a direct Chinese invasion of Taiwan, but from Beijing's "anaconda strategy" of gradual economic and military coercion. This includes record-breaking military flights into Taiwan's airspace, practice blockades, and approximately 2.4 million daily cyberattacks on Taiwanese systems. Simultaneously, U.S. policies create contradictory pressures—while providing billions in CHIPS Act subsidies to encourage American expansion, the Trump administration has revoked export privileges for TSMC's Chinese operations, forcing costly reorganization and individual licensing requirements that could cripple the company's mainland facilities.

Beyond geopolitical risks, TSMC faces an invisible war in cyberspace, with over 19,000 employee credentials circulating on the dark web and sophisticated state-sponsored attacks targeting its intellectual property. The recent alleged leak of 2nm process technology highlights how China's export control restrictions have shifted the battleground from equipment access to talent and trade secret theft. TSMC's response includes an AI-driven dual-track IP protection system, which manages over 610,000 cataloged technologies and extends security frameworks to global suppliers.

TSMC is actively building resilience through a $165 billion global expansion strategy, establishing advanced fabs in Arizona, Japan, and Germany while maintaining its technological edge with superior yields on cutting-edge nodes. However, this de-risking strategy comes at a significant cost - Arizona operations will increase wafer costs by 10-20% due to higher labor expenses, and the company must navigate the strategic paradox of diversifying production while keeping its most advanced R&D concentrated in Taiwan. The analysis concludes that TSMC's future hinges not on current financial performance, but on successfully executing this complex balancing act between maintaining technological leadership and mitigating unprecedented geopolitical risks in an increasingly fragmented global order.

$ZS: Zscaler – Cloud Security Titan or Overhyped Hype Train?(1/9)

Good afternoon, folks! ☀️ NASDAQ:ZS : Zscaler – Cloud Security Titan or Overhyped Hype Train?

With NASDAQ:ZS soaring after smashing earnings, is this cybersecurity champ locking down profits or just riding a digital wave? Let’s crack the code! 🔍

(2/9) – PRICE PERFORMANCE 📊

• Current Price: Up post-earnings, exact $ TBD 💰

• Recent Results: Q1 2025 earnings beat estimates, per X buzz 📏

• Sector Trend: Cloud security demand surging 🌟

It’s a hot streak in a hotter market! ⚡

(3/9) – MARKET POSITION 📈

• Market Cap: Strong, based on 151.62M shares 🏆

• Operations: Leader in Zero Trust security ⏰

• Trend: posts hail robust growth, per Mar 6 chatter 🎯

Solid, shielding the digital frontier! 🌍

(4/9) – KEY DEVELOPMENTS 🔑

• Earnings Win: Q1 2025 topped forecasts, guidance raised 🔄

• Cloud Security: Demand spikes amid cyber threats 🌐

• Market Reaction: Stock jumped📋

Thriving, as hackers keep the world on edge! 💡

(5/9) – RISKS IN FOCUS ⚠️

• Valuation: High P/E could spook investors 🔍

• Competition: Crowded field with CrowdStrike, Palo Alto 📉

• Macro Shifts: Economic dips might slow spending ❄️

Watch out, risks lurk in the shadows! 🕵️

(6/9) – SWOT: STRENGTHS 💪

• Earnings Beat: Q1 2025 growth shines 🥇

• Market Lead: Zero Trust pioneer 📊

• Demand: Cloud security’s red-hot 🔧

Locked and loaded for the cyber age! 🔒

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES ⚖️

• Weaknesses: High valuation, competition pressures 📉

• Opportunities: Rising cyber threats fuel expansion 📈

Can it secure the bag or get hacked by rivals? 🤔

(8/9) – 📢Zscaler’s riding high post-earnings—your call? 🗳️

• Bullish: $250+ by summer, cyber’s king 🐂

• Neutral: Holding steady, risks loom ⚖️

• Bearish: $180 drop, hype fades 🐻

Vote below! 👇

(9/9) – FINAL TAKEAWAY 🎯

Zscaler’s Q1 2025 earnings pop signals strength 📈, but high stakes mean volatility’s a shadow friend 🌫️. Dips? That’s our DCA jackpot 💰. Buy low, soar high! Treasure or trap?

Can a Failed Star Rise from Space Ashes to Rule Earth's NetworksIridium Communications has engineered a remarkable strategic transformation from its predecessor's bankruptcy to become an indispensable global provider of connectivity. The company operates a resilient Low-Earth Orbit (LEO) constellation of 66 cross-linked satellites positioned 780 kilometers above Earth, delivering unprecedented 100% global coverage through L-band frequency transmission. This unique architecture provides superior weather resilience, low latency, and automatic signal re-routing capabilities that distinguish it from both traditional geostationary satellites and emerging broadband competitors like Starlink.

The company's ascendance is fundamentally driven by its critical role in national security operations. Iridium maintains multi-year, fixed-price contracts with the U.S. Department of Defense, providing Enhanced Mobile Satellite Services for mission-critical applications including secure communications, battlefield mapping, precise targeting, and real-time situational awareness. Unlike mass-market LEO providers focused on consumer broadband, Iridium deliberately targets high-value, specialized segments requiring uncompromising security and reliability. The company employs advanced encryption standards, including NSA Type 1 protocols, and has developed a comprehensive, multi-layered cybersecurity framework featuring quantum-resilient encryption and AI-driven threat detection.

Iridium's technological leadership extends beyond core communications through its hosted payload capabilities, supporting specialized applications like Aireon's global aircraft surveillance and exactEarth's ship tracking systems. The company's strategic differentiation lies in its focus on mission-critical applications rather than consumer services, creating a sustainable competitive moat protected by significant intellectual property and specialized technical capabilities. This positioning has enabled stable, high-margin revenue streams from government contracts while minimizing direct competition with volume-oriented providers.

The company's current trajectory represents not merely recovery but strategic re-emergence, capitalizing on mature market conditions where global IoT solutions, remote operations, and critical government communications align perfectly with Iridium's unique capabilities. With its robust financial foundation, expanding hosted payload services, and growing demand for resilient non-terrestrial connectivity, Iridium is positioned for sustained growth in an increasingly connected yet volatile global landscape, transforming from a cautionary tale of premature innovation into a compelling investment in critical infrastructure.

How Does One Platform Navigate Eight Global Disruptions at Once?GitLab has emerged as a dominant force in the DevSecOps landscape during 2025, achieving a remarkable 29% year-over-year revenue growth to reach $759 million annually in fiscal Q4 2025. The platform's success stems from its ability to address multiple converging global challenges simultaneously, from geopolitical tensions and cybersecurity threats to economic volatility and technological transformation. Key milestones include GitLab Dedicated for Government earning FedRAMP Moderate authorization, enabling accelerated public sector adoption, and strategic partnerships like Sigma Defense's implementation that reduced U.S. Navy software deployment times from months to days.

The convergence of geopolitical and geostrategic factors has created unprecedented demand for GitLab's solutions. Rising data sovereignty requirements and U.S.-China tech rivalries have driven nations to enforce strict data residency laws, making GitLab's single-tenant SaaS architecture particularly attractive for compliance. Defense contractors and government agencies increasingly rely on GitLab's integrated DevSecOps capabilities to strengthen national security positions, with organizations like Sigma Defense achieving 90% cost reductions while dramatically accelerating vulnerability fixes and software deployment cycles.

Economic pressures and technological evolution have further accelerated GitLab's adoption across sectors. The platform delivers a compelling ROI of 483% within three years for large organizations, while the broader DevOps market grows at a 19.1% CAGR. GitLab's integrated approach addresses critical pain points, including toolchain consolidation, embedded security, and AI-powered automation, positioning it as essential infrastructure for cloud-native development. The company's strategic focus on eliminating silos through unified workflows from code to cloud has resonated particularly well with enterprises seeking to reduce complexity and operational costs.

Looking ahead, GitLab's intellectual property strategy and continued innovation in AI integration, exemplified by GitLab Duo's capabilities in code generation and vulnerability detection, suggest sustained competitive advantages. The platform's ability to serve diverse sectors-from federally-funded research centers requiring secure collaboration to high-tech firms demanding cutting-edge automation-demonstrates its versatility in addressing the complex, interconnected challenges defining the modern technology landscape.

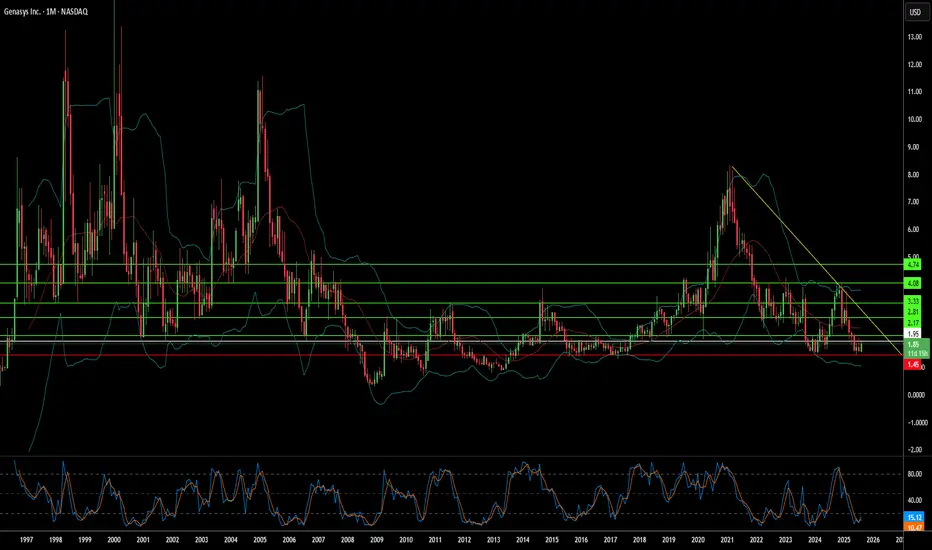

Can Sound Waves Become Tomorrow's Shield Against Global Chaos?Genasys Inc. (NASDAQ: GNSS) operates at the convergence of escalating global instability and technological innovation, positioning itself as a critical player in the protective communications sector. The company's sophisticated portfolio combines its proprietary Long Range Acoustic Device (LRAD) systems with the cloud-first Genasys Protect software platform, serving over 155 million individuals across more than 100 countries. With law enforcement agencies in over 500 U.S. cities utilizing LRAD systems for applications ranging from SWAT operations to crowd control, Genasys has established itself as the global standard in acoustic hailing devices, delivering messages 20-30 decibels louder and with superior intelligibility compared to traditional systems.

The company's growth trajectory aligns with powerful macroeconomic forces driving unprecedented demand for protective communications. Global defense spending surged to $2.718 trillion in 2024—a 9.4% increase representing the steepest rise since 1988—while the critical infrastructure protection market is projected to grow from $148.64 billion in 2024 to $213.94 billion by 2032. Genasys's integrated solutions directly address this expanding market through non-kinetic de-escalation capabilities and cyber-physical threat mitigation, recently securing $1 million in LRAD orders for the Middle East and Africa as geopolitical tensions intensify.

Genasys's competitive advantage rests on a robust foundation of 17 registered patents, particularly in acoustic hailing technology, creating significant barriers to entry while enabling premium pricing. The company's $4.2 million annual R&D investment ensures continued innovation, while strategic partnerships like its collaboration with FloodMapp demonstrate the platform's evolution toward predictive threat mitigation rather than merely reactive response. Despite current profitability challenges—with Q3 2025 net losses of $6.5 million—the company maintains a substantial project backlog exceeding $16 million, plus the transformative $40 million Puerto Rico Early Warning System project expected to generate $15-20 million in fiscal 2025 revenue.

The investment thesis centers on Genasys's unique positioning to capitalize on the global shift toward sophisticated, non-lethal security solutions amid rising geopolitical instability. With percentage-of-completion accounting currently suppressing gross margins to 26.3% but promising significant margin expansion as major projects near completion, the company represents a compelling opportunity for investors seeking exposure to defense, public safety, and critical infrastructure growth markets. The convergence of technological superiority, strategic market positioning, and substantial revenue visibility through confirmed backlog suggests significant long-term potential despite near-term financial complexities.

$ZS - Still room to run - 45% Upside!NASDAQ:ZS - Cybersecurity BEAST right here! 🚀

✅$260 ✅$313

🎯$378 🎯$445

Looking for a small pullback or even a CupnHandle retest then a move back to the upside to our PT's!

Why Is CrowdStrike's Stock Soaring Amidst Cyber Chaos?The digital landscape is increasingly fraught with sophisticated cyber threats, transforming cybersecurity from a mere IT expense into an indispensable business imperative. With global cybercrime costs projected to reach $10.5 trillion annually by 2025, organizations face severe financial penalties, operational disruptions, and reputational damage from data breaches and ransomware attacks. This escalating threat environment has created an urgent and inelastic demand for robust digital defenses, positioning leading cybersecurity firms like CrowdStrike as critical enablers of economic stability and growth.

CrowdStrike's remarkable ascent is directly tied to this surging demand, fueled by pervasive trends such as widespread digital transformation, extensive cloud adoption, and the proliferation of hybrid work models. These shifts have vastly expanded attack surfaces, necessitating comprehensive, cloud-native security solutions that can protect diverse endpoints and cloud workloads. Organizations are increasingly prioritizing cyber resilience, seeking integrated platforms that offer proactive detection and rapid response capabilities. CrowdStrike's Falcon platform, with its AI-native, single-agent architecture, effectively addresses these needs, providing real-time threat intelligence and enabling seamless expansion across various security modules, which drives high customer retention and significant upsell opportunities.

The company's strong financial performance underscores its market leadership and operational efficiency. CrowdStrike consistently reports impressive Annual Recurring Revenue (ARR) growth, healthy non-GAAP operating margins, and robust free cash flow generation, demonstrating a sustainable and profitable business model. This financial strength, combined with its continuous innovation and strategic partnerships, positions CrowdStrike for sustained long-term growth. As enterprises seek to consolidate security vendors and simplify complex operations, CrowdStrike's comprehensive platform is ideally situated to capture a larger share of global cybersecurity spending, solidifying its role as a cornerstone of the digital economy and a compelling investment in a high-stakes environment.