Can Instability Be an Asset Class?Aerospace and Defense (A&D) ETFs have shown remarkable performance in 2025, with funds like XAR achieving a 49.11% year-to-date return. This surge follows President Trump's October 2025 directive to resume U.S. nuclear weapons testing after a 33-year moratorium, a decisive policy shift responding to recent Russian weapons demonstrations. The move signals the formalization of Great Power Competition into a sustained, technology-intensive arms race, transforming A&D spending from discretionary to structurally mandatory. Investors now view defense appropriations as a guaranteed source of funding, creating what analysts call a permanent "instability premium" on sector valuations.

The financial fundamentals supporting this outlook are substantial. The FY2026 defense budget allocates $87 billion for nuclear modernization alone, a 26% increase in funding for critical programs like the B-21 bomber, Sentinel ICBM, and Columbia-class submarines. Major contractors are reporting exceptional results: Lockheed Martin established a record $179 billion backlog while raising its 2025 outlook, effectively creating multi-year revenue certainty that functions like a long-duration bond. In 2023, global military spending reached $2.443 trillion, with NATO allies driving over $170 billion in U.S. foreign military sales, which extended revenue visibility beyond domestic congressional cycles.

Technological competition is accelerating investments in hypersonics, digital engineering, and modernized command-and-control systems. The shift toward AI-driven warfare, resilient space-based architectures, and advanced manufacturing processes (exemplified by Lockheed's digital twin technology for the Precision Strike Missile program) is transforming defense contracting into a hybrid hardware-software model with sustained high-margin revenue streams. The modernization of Nuclear Command, Control, and Communications (NC3) systems and implementation of Joint All-Domain Command and Control (JADC2) strategy require continuous, multi-decade investments in cybersecurity and advanced integration capabilities.

The investment thesis reflects structural certainty: legally mandated nuclear modernization programs are immune to typical budget cuts, contractors hold unprecedented backlogs, and technological superiority demands perpetual high-margin research and development. The resumption of nuclear testing, driven by strategic signaling rather than technical necessity, has created a self-fulfilling cycle that guarantees future expenditures. With geopolitical escalation, macroeconomic certainty through front-loaded appropriations, and rapid technological innovation converging simultaneously, the A&D sector has emerged as an essential component of institutional portfolios, supported by what analysts characterize as "geopolitics guaranteeing profits."

Defensecontractors

Can Defense Giants Print Money During Global Chaos?General Dynamics delivered exceptional Q3 2025 results with revenue reaching $12.9 billion (up 10.6% year-over-year) and diluted EPS soaring to $3.88 (up 15.8%). The company's dual-engine growth strategy continues to drive performance: its defense segments capitalize on mandatory global rearmament driven by escalating geopolitical tensions, while Gulfstream Aerospace leverages resilient demand from high-net-worth individuals. The Aerospace segment alone grew revenue by 30.3% with operating margin expanding 100 basis points, delivering record jet deliveries as supply chains normalized. Operating margin reached 10.3% overall, with operating cash flow hitting $2.1 billion—an extraordinary 199% of net earnings.

The defense portfolio secures decades of revenue visibility through strategic programs, most notably the $130 billion Columbia-class submarine program, which represents the U.S. Navy's top acquisition priority. General Dynamics European Land Systems has secured a €3 billion contract from Germany for next-generation reconnaissance vehicles, capitalizing on record European defense spending that reached €343 billion in 2024 and is projected to reach €381 billion in 2025. The Technology division strengthened its position with $2.75 billion in recent IT modernization contracts, deploying AI, machine learning, and advanced cybersecurity capabilities for critical military infrastructure. The company's 3,340-patent portfolio, with over 45% still active, reinforces its competitive moat in nuclear propulsion, autonomous systems, and signals intelligence.

However, significant operational headwinds persist in the Naval segment. The Columbia-class program faces a 12-to 16-month delay, with the first delivery now anticipated between late 2028 and early 2029, driven by supply chain fragility and specialized workforce shortages. Late delivery of major components forces complex out-of-sequence construction work, while the defense industrial base struggles with critical skill gaps in nuclear-certified welders and specialized engineers. Management emphasizes that the upcoming year will be pivotal for driving productivity improvements and margin recovery in Naval operations.

Despite near-term challenges, General Dynamics' balanced portfolio positions it for sustained outperformance. The combination of non-discretionary defense spending, technological superiority in strategic systems, and robust free cash flow generation provides resilience against volatility. Success in stabilizing the submarine industrial base will determine long-term margin trajectory, but the company's strategic depth and cash generation capability support continued alpha generation in an increasingly uncertain global environment.

Can a $251 Billion Backlog Predict the Future?RTX Corporation has positioned itself at the intersection of escalating global defense imperatives and the recovery of commercial aviation, generating a formidable $251 billion backlog that provides unprecedented revenue visibility. The company reported strong Q3 2025 results with sales of $22.5 billion (up 12% year-over-year) and raised its full-year guidance, driven by double-digit organic growth across all segments. This performance reflects RTX's dual-market advantage: surging defense spending, with global military expenditure reaching $2.7 trillion in 2024 and NATO's new 5% GDP target by 2035, combined with recovering commercial aviation demand projected to exceed 12 billion passengers by 2030.

RTX's technological superiority centers on proprietary Gallium Nitride (GaN) semiconductor innovations that power next-generation radar systems, creating substantial barriers to entry. The company's LTAMDS radar delivers twice the power of legacy Patriot systems while eliminating battlefield blind spots, and the newly launched APG-82(V)X radar enhances fighter aircraft capabilities against advanced threats. Major contracts underscore this dominance, including a $5 billion Army award for the Coyote counter-drone system, which extends through 2033. RTX has committed over $600 million to manufacturing expansion this year alone, with the Redstone Missile Integration Facility expansion specifically targeting increased production of Standard Missile variants and counter-hypersonic solutions.

On the commercial side, Pratt & Whitney's GTF Advantage engine achieved EASA certification in Q4 2025, resolving earlier durability challenges with a design targeting double the time-on-wing compared to prior models. This breakthrough secures RTX's control over the A320neo and A220 fleets, guaranteeing decades of high-margin maintenance, repair, and overhaul revenue. Collins Aerospace's global network of over 70 MRO sites and flexible AssetFlex program capitalizes on supply chain constraints that force airlines to invest more heavily in fleet maintenance rather than new aircraft purchases.

The financial trajectory appears compelling: analysts project free cash flow will surge from $5.5 billion in 2023 to $9.9 billion by 2027, representing 15.5% annualized growth and compressing the price-to-FCF multiple from 31.3x to 17.3x. Wall Street maintains a consensus "Buy" rating across thirteen covering firms with zero sell recommendations. RTX's 60,000-patent portfolio, built on $7.5 billion in annual R&D spending, spans advanced materials, AI, autonomy, and next-generation propulsion, creating a self-reinforcing cycle where investment drives proprietary technology that secures long-term government contracts. With an affirmed BBB+ credit rating and stable outlook, RTX presents a structurally sound investment thesis built on geopolitical necessity, technological moats, and expanding cash generation.

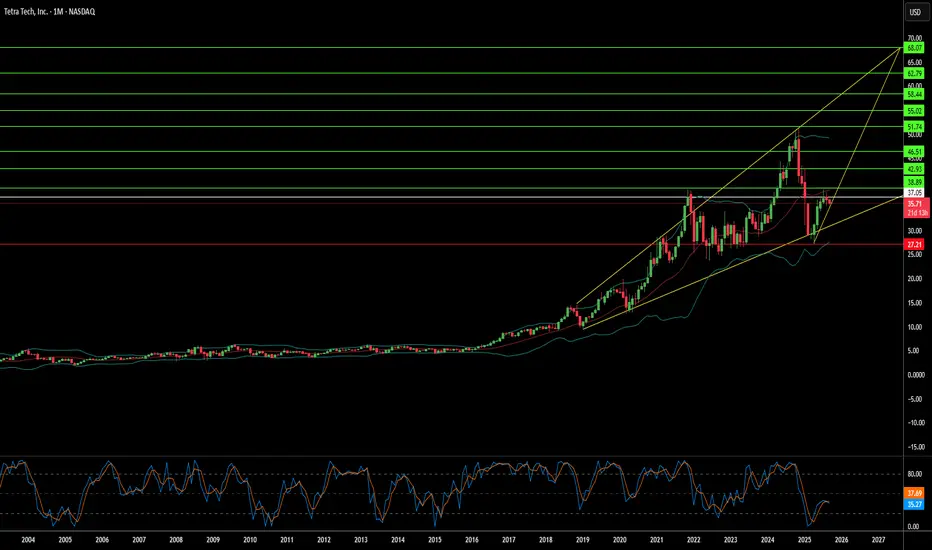

When Does Destruction Create Trillion-Dollar Opportunity?Tetra Tech's remarkable market surge represents a confluence of technological innovation and geopolitical opportunity that positions the Pasadena-based engineering firm at the epicenter of global reconstruction efforts. The company has distinguished itself through substantial intellectual property holdings—over 500 global patents across infrastructure and environmental technologies—and cutting-edge capabilities, including an AI innovation lab focused on robotics, cloud migration, and cognitive systems that automate complex engineering workflows. This technological foundation has translated into impressive financial performance, with the company reporting approximately 11% revenue growth year-over-year in Q3 2025 and maintaining a record backlog of $4.15 billion while earning "Moderate Buy" ratings from analysts with price targets in the low $40s.

The strategic value proposition extends far beyond traditional engineering services into the realm of conflict-zone reconstruction, where Tetra Tech's four decades of experience in war-torn regions uniquely position it for emerging opportunities. The company already maintains USAID contracts in conflict areas, including a $47 million project in the West Bank and Gaza, and has demonstrated critical capabilities in Ukraine through generator deployment, power grid restoration, and explosive ordnance clearance operations. These competencies align precisely with the skill sets required for large-scale reconstruction efforts, from debris removal and pipeline repair to the engineering of essential infrastructure systems, including roads, power plants, and water treatment facilities.

Gaza's reconstruction represents a potentially transformative business opportunity that could fundamentally alter Tetra Tech's trajectory. Conservative estimates place Gaza's infrastructure rebuilding needs at $18-50 billion over approximately 14 years, with immediate priorities including roads, bridges, power generation, water treatment systems, and even airport reconstruction. A major contract in this range—potentially $10-20 billion—would dwarf Tetra Tech's current market capitalization of approximately $9.4 billion and could significantly increase the company's annual revenue. The strategic importance is amplified by broader geopolitical initiatives, including proposed Gaza trade corridors linking Asia and Europe as part of U.S.-led stability plans that envision Gaza as a revived commercial hub.

Institutional investors have recognized this potential, with 93.9% of shares held by institutional owners and recent substantial position increases by firms like Paradoxiom Capital, which acquired 140,955 shares worth $4.1 million in Q1 2025. The convergence of global infrastructure demand—estimated at $64 trillion over the next 25 years—with Tetra Tech's proven expertise in high-stakes reconstruction projects creates a compelling investment thesis. The company's combination of advanced technology capabilities, extensive patent portfolio, and demonstrated success in complex geopolitical environments positions it as a primary beneficiary of the intersection between global instability and the massive capital deployment required for post-conflict reconstruction.

Can AI Weather the Storm of Volatility?BigBear.ai has captured the market's attention with its dramatic stock performance, navigating through a sea of volatility with recent gains fueled by significant contract wins and positive AI sector developments. The company's journey reflects a broader narrative in the tech industry: the high stakes of betting on AI innovation. With its stock soaring over 378% in the last year, BigBear.ai demonstrates the potential for rapid growth in an era where AI is increasingly central to strategic sectors like defense, security, and space exploration.

However, the narrative isn't without its twists. Analyst warnings about cyclical business patterns and valuation concerns introduce a layer of complexity to the investment thesis. BigBear.ai's ability to secure pivotal contracts with the U.S. Department of Defense showcases its technological prowess, yet the challenge lies in converting this into sustainable profitability. This scenario invites investors to ponder the delicate balance between innovation, market sentiment, and financial stability in the AI landscape.

The strategic acquisition of Pangiam and partnerships like the one with Virgin Orbit illustrate BigBear.ai's ambition to not only ride the wave of AI hype but also to steer it into new territories. These moves are about expanding market presence and redefining what AI can achieve in practical, real-world applications. As BigBear.ai continues to evolve, it challenges us to consider how far AI can go in reshaping industries and whether the market can keep pace with such rapid technological advancements. This saga of BigBear.ai is a microcosm of the broader AI investment landscape, urging us to look beyond immediate gains to the long-term vision and viability of AI-driven companies.

LMT a defense large cap dips for buyers LONGLMT has been flat sideways since a good earnings beat 5 weeks ago. Lockheed Martin as a

defense contractor is in a growth environment with the US supplying arms to Ukraine as well

a Isreal. Domestic stockpiles and those of NATO are somewhat depleted. The contraacts will not

catch up for years. Gone are the days of making face masks and gowns during COVID to keep

revenues flowing in. I see this 2% dip as a change to get a small discount on what should

be a stock with upside for some years to come. This is a long swing trade not expectant of

a 3-4% profit in a week. I expect to hold this at least until the next earnings if not through

the presidential elections where the defense and national security perspectives of the

incoming or returning president may be a factor in the fundamentals of defense contractors.

Technical Analysis of RTX (Raytheon Technologies) Weekly ChartSubscribe & Follow For:

➞ Quick Chart Summary Breakdown

➞ Pertinent Supply Demand Zones and Considerations

➞ US Stocks / Crypto Only

➞ Before / After Analysis

🙏 Like & Subscribe

💬 Drop a line and let me know what you think

🍯 Coin donations always appreciated

🚀 Boost this post to share value

NYSE:RTX is currently exhibiting a double megaphone pattern on the weekly chart, indicating a period of increased volatility and potential uncertainty in the market sentiment. This pattern typically suggests conflicting forces at play, with widening price swings signaling indecision among traders.

Key Pattern: Double Megaphone

A megaphone pattern, also known as a broadening formation, consists of two expanding trendlines that diverge away from each other. This pattern reflects growing volatility and uncertainty, with higher highs and lower lows being established over time. In this scenario with RTX we are showing two long term trends one inside of another.

Explanation:

Textbook Answer: This double megaphone pattern often signifies a struggle between bulls and bears, with neither side gaining a clear advantage. It also represents volatility & opportunity. It's up to us to determine price point where we can capitalize on positioning for profitability!

Real World Answer: Manipulation & Perfect Timing

As the price oscillates between the expanding trendlines, traders should exercise caution and closely monitor key support and resistance levels for potential trading opportunities. I got a feeling this one is going to be a mover!

RSI Breakout with Hidden Divergence:

In addition to the double megaphone pattern, RTX is exhibiting a notable breakout on the Relative Strength Index (RSI) with hidden bullish divergence and the highs are currently compromised with clear and visible hidden bearish divergence leading me to believe that we will revisit the 5th swing level (or in the vicinity of) one more time and see how well prices hold.

Current Situation:

At present, NYSE:RTX is approaching a critical juncture within the double megaphone pattern. Traders must evaluate whether the price will push through the upper trendline or revisit the lower trendline, known as the 5th swing in Elliott Wave Theory.

Potential Scenarios:

Managing Breakout:

If RTX manages to break above the upper trendline of the double megaphone pattern, it could signal a bullish continuation, with the potential for further upside momentum. Traders may consider initiating long positions with appropriate risk management strategies in place.

Revisit of 5th Swing (Lower Trendline)

Conversely, if RTX fails to sustain upward momentum and revisits the lower trendline, it could indicate a bearish reversal or consolidation phase. Traders should be prepared for increased volatility and monitor key support levels for potential downside targets.

Key Levels to Watch:

Resistance: Upper trendline of both of the megaphone patterns.

Support: Lower trendline (5th swing) and previous swing lows within the pattern.

Conclusion:

In conclusion, the presence of a double megaphone pattern on the RTX weekly chart suggests heightened volatility and uncertainty in the market. Traders should remain vigilant and adapt their strategies based on the price action relative to the pattern's trendlines. Granted the series of unfortunate events occurring on the global stage I could almost anticipate what is going to happen here in the long term

As always, it's essential to incorporate risk management techniques and exercise caution when navigating such volatile market conditions.

Note: Ensure to identify your price levels accordingly. This analysis is for educational purposes only and should not be construed as financial advice. Traders should conduct their own research and consult with a financial advisor before making any investment decisions.

Huntington Ingalls: Cup with Handle with 89% Upside PotentialHII is a Shipbuilder US Defense Contractor that has formed a Cup with Handle Pattern with MACD Hidden Bullish Divergence, and it is currently breaking free from the handle and will soon challenge the Cup's Horizontal Resistance. If it breaks out, HII could nearly double up in value all the way to $480 as it goes for the measured move.

Boeing BA - A Dark HarbourI have never looked at Boeing until today, when I saw some guy posting ideas about it while I was having lunch and I didn't even recognize the ticker, and so I took a look at it, and was surprised to see what I found.

In considering this company, I completely understand that they've had problems with their planes, and big ones. But I have also said that I do not put much weight in the ostensible correlation between fundamentals of a company and price.

So long as the equity is still being maintained by Wall Street's behemoths, price action will remain orderly made and constitute a fractal that is rationally written and contains the combined intelligence of all market participants.

Boeing is really notable on the monthly charts:

Frankly, its bullish price action looked even better than what stuff like AAPL and TSLA printed during this unsustainable Federal Reserve money printer-backed tractor pull to SPX 4,800, and it occurred before COVID, and was accompanied by heavy distribution.

It only finally corrected when COVID hit, and yet it only swept out the '16 low, which led to the original impulse to $450.

Even more taste bud-piquing is the weekly chart:

BA has not had a shred of bullish impulse since March of 2021. More or less, while the entire market went ape-up in a straight line, Boeing has just grinded downwards.

This is highly indicative of significant smart money accumulation.

When the big 2022 correction started, Boeing lost 30% like everyone else, but formed a 24-month double bottom and protected its pre-COVID low with a generous wick and a healthy bounce.

More importantly, there is a gap that appears both on the daily and weekly candles at $330, which is exceptionally notable considering this mid-term range high, printed 18 months ago, wasn't far away at $~279.

I believe that a significant shakeout in the market will come shortly.

VIX - 9x8 = 72

But based on the price action of Boeing, I can't help but feel this is the definition of oversold and that an expectation from short sellers that this is going to turn around and rip south to new lows is going to be met with only one outcome: liquidation.

For other defense contractors like Lockheed Martin and Raytheon, although they have totally different (and much more bullish) price action compared BA, they share the characteristic of severely lagging the overall market in terms of bull impulse.

And these are arguably the most critical companies underpinning the United States and the globalist empire.

This leads me to believe that what lies ahead is a catalyst that will see defense and aerospace stocks go on a _significant_ bull run, providing an unlikely harbour amid an overall market that sees both equities and commodities revisiting (and breaking) pre-COVID market structure.

SPX / ES - Bull Whips and Bear Saws

For Boeing, it's still too expensive to buy, trading above the equilibrium point of this June-forward dealing range.

However, if this thesis that Boeing will go on a tear and not turn around and die is correct, I would want to see it fall to only a certain point and not flirt with the double bottom or the even the June gap lows.

The best buy signal, hands down, will be a dump into the $135 range, accompanied by market makers reverently supporting this area.

If so, you should definitely expect this whole 18 month range below $280 gets cleaned up, and likely in a highly aggressive fashion.

The question is, what serves as a catalyst for the defense and aerospace industry to moon?

There are no pleasant answers.