Can a Small-Sat Pioneer Become a Defense Superpower?Rocket Lab has transformed from a niche small-satellite launch provider into a strategic national security asset, closing 2025 with 21 successful Electron launches and a remarkable 175% stock surge. The company's evolution culminated in an $816 million Space Development Agency contract to build 18 satellites for hypersonic missile threat detection, signaling its emergence as a primary defense contractor. This vertical integration strategy positions Rocket Lab as a critical player in an era where supply chain sovereignty has become paramount for military readiness.

The technological centerpiece of Rocket Lab's 2026 ambitions is the Neutron rocket, a medium-lift vehicle capable of carrying 13,000 kilograms to low Earth orbit. Set for its maiden test flight in mid-2026, Neutron features the innovative "Hungry Hippo" fairing design and 3D-printed Archimedes engines, targeting the lucrative mega-constellation market currently dominated by SpaceX's Falcon 9. This technological leap, combined with over 550 global patents covering critical propulsion and structural innovations, creates a formidable intellectual property moat that competitors cannot easily replicate.

The financial trajectory underscores this transformation: analysts project 52.2% EPS growth for 2026, reaching $0.27 per share and dramatically outpacing traditional aerospace giants like Lockheed Martin (0.6%) and Northrop Grumman (-7.6%). A potential SpaceX IPO at $1.5 trillion valuation could trigger sector-wide revaluation, with Rocket Lab standing as the only publicly traded, vertically integrated alternative. Wall Street has responded accordingly, raising price targets to $90 as the company bridges the gap between startup agility and aerospace titan scale, with defense contracts poised to dominate its revenue mix.

Nationalsecurity

Can a $89M Company Execute on a $151B Defense Contract?Sidus Space (NASDAQ: SIDU) experienced a dramatic 97% stock surge following its selection for the Missile Defense Agency's SHIELD program, an Indefinite-Delivery/Indefinite-Quantity (IDIQ) contract with a staggering $151 billion ceiling. This represents an extraordinary valuation asymmetry—the contract ceiling is 1,696 times the company's current market capitalization of approximately $89 million. The SHIELD award validates Sidus's AI-enabled satellite technology as critical to America's "Golden Dome" missile defense strategy, positioning the micro-cap company alongside defense giants like Parsons Corporation to compete for task orders over the next decade.

The company's LizzieSat platform and FeatherEdge AI system address urgent national security needs, particularly the hypersonic missile threat from near-peer adversaries. By processing data at the edge in orbit rather than relaying it to ground stations, Sidus reduces the "kill chain" latency from minutes to milliseconds—a capability essential for tracking maneuvering hypersonic glide vehicles. The company's 3D-printed satellite manufacturing approach enables rapid 45-day production cycles, supporting the Pentagon's "Tactically Responsive Space" doctrine for quickly reconstituting destroyed assets in contested environments.

However, significant execution risks remain. Sidus currently generates under $5 million in annual revenue while burning approximately $6 million per quarter, with only $12.7 million in cash reserves as of Q3 2025. The company operates at negative gross margins and survives through dilutive equity raises. The SHIELD contract is not guaranteed revenue but rather a "hunting license" requiring successful competitive bidding on individual task orders. The path to profitability depends on winning sufficient task orders to achieve the scale needed to cover high fixed costs and transition to the high-margin Data-as-a-Service model. For investors, this represents a high-risk, asymmetric bet on whether a micro-cap can successfully navigate the "Valley of Death" to become a defense prime contractor.

Will Quantum Computing Rewrite the Rules of Global Power?D-Wave Quantum Inc. (QBTS) stands at the intersection of three transformative forces reshaping the investment landscape: the intensifying U.S.-China technology race, the shift toward energy-efficient computing, and the militarization of optimization technology. The company has achieved what few quantum computing firms can claim: actual commercial revenue with over 200% year-over-year growth and software-like gross margins approaching 78%. With a fortified balance sheet of $836 million in cash, D-Wave has eliminated the existential funding risk that plagues most deep-tech ventures, providing a multi-year runway to execute its dual-track strategy of commercializing quantum annealing while developing next-generation gate-model systems.

The strategic deployment of D-Wave's Advantage2 quantum computer at Davidson Technologies in Huntsville, Alabama, the heart of U.S. missile defense, marks a watershed moment. This isn't cloud access; it's physical hardware embedded in secure defense infrastructure, optimizing interceptor assignments and radar scheduling for national security applications. As the U.S.-China Economic and Security Review Commission warns of "Q-Day" threats and recommends $2.5 billion in quantum funding through 2030, D-Wave's transition from research curiosity to critical defense asset positions it to capture significant government procurement contracts. The company's quantum annealing technology solves combinatorial optimization problems that classical supercomputers struggle with, issues that underpin modern warfare logistics, supply chain resilience, and industrial competitiveness.

Beyond defense, D-Wave addresses a critical bottleneck in the AI revolution: energy consumption. As data centers strain against power grid limits, D-Wave's quantum annealers offer energy-efficient solutions for optimization problems, from pharmaceutical drug discovery to financial portfolio management. The company's "Proof of Quantum Work" blockchain mechanism demonstrates potential applications in secure financial infrastructure, while partnerships with Fortune 500 companies, such as BASF and Ford, show immediate operational value. Scientific validation has proven D-Wave's annealers vastly outperform both gate-model quantum competitors and classical supercomputers on specific problem sets. With institutional investors like Citadel increasing their stakes and macroeconomic conditions favoring a 2026 rotation toward high-growth tech as interest rates decline, D-Wave represents an asymmetric opportunity, a company priced for skepticism but delivering results that demand conviction.

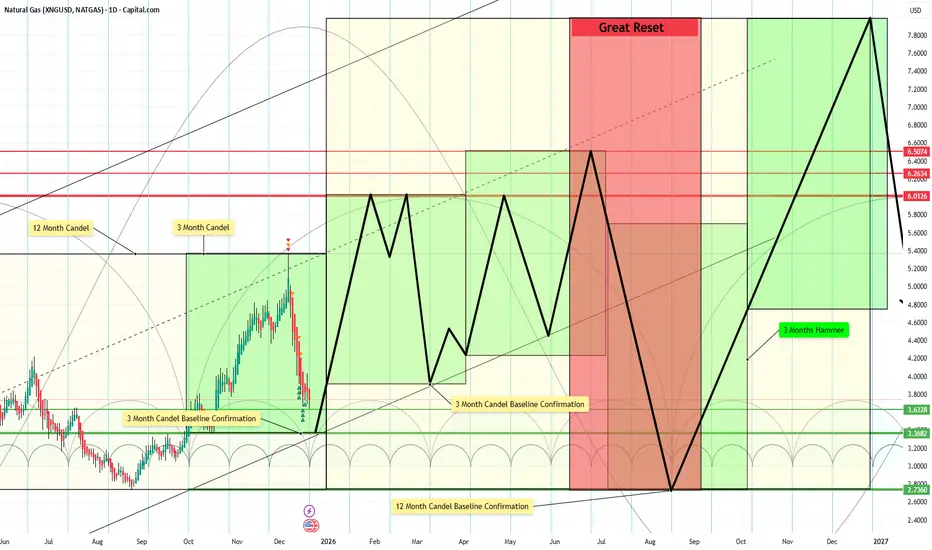

3Month and 12 Month Candels retest and RetrecmentThe 3-month and 12-month candle retest and retracement concept is a higher-timeframe market analysis approach that focuses on how price reacts after forming major quarterly and yearly candles. The high, low, open, and midpoint of these candles function as critical structural levels that often act as magnets for price.

After a candle closes, price frequently retests these levels in subsequent periods before continuing in the prevailing trend, reflecting institutional participation and liquidity rebalancing. Retracements toward these higher-timeframe levels are considered a natural and necessary process within trending markets.

At the end of major sell cycles, a strong retracement is expected, as selling pressure becomes exhausted and liquidity conditions shift. These deeper retracements often target the candle open or midpoint and may mark the transition from distribution to accumulation, preceding trend stabilization or reversal. This behavior provides valuable context for identifying high-probability zones for long-term positioning and risk control.

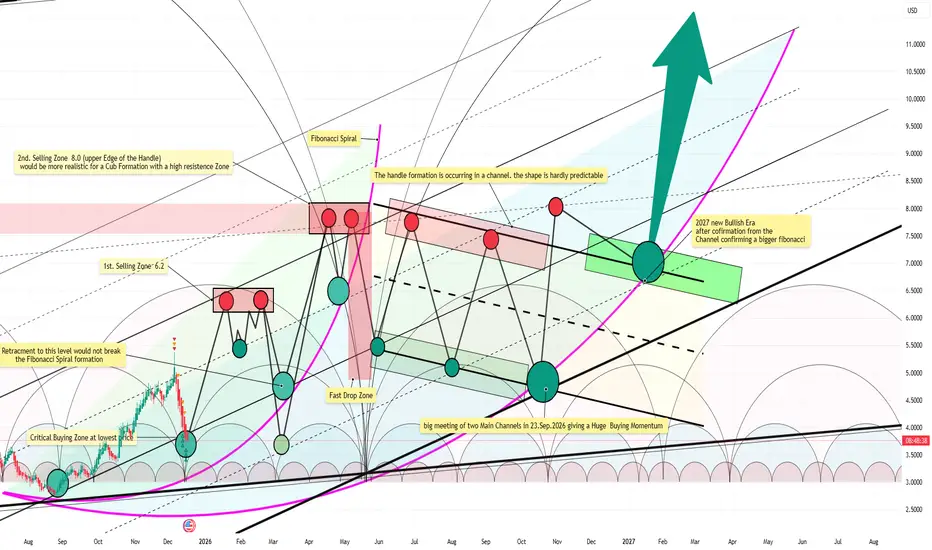

THE SETUP: 2026 CUP and Handel Formation (most realistic)This observation has crossed a threshold.

It is no longer merely "trading ideas" or speculative commentary.

We are witnessing the most structurally significant formation of the cycle a multi-stage Handle and Channel Convergence setting the stage for a historic move.

The alignment of a historic Cup & Handle replication, within a 10-year Fibonacci framework, at the meeting point of macro channels, creates a scenario that demands a higher level of consideration. It presents a probability that is now too significant to ignore.

Phase 1: The Final Exhaustion Drop

Price is rejected from the massive 8.0 resistance wall. This isn't just a normal pullback.

Why it drops fast: This sell-off represents the final liquidation wave of the previous bear cycle. Weak hands capitulate, and late sellers scramble for the exit, creating a sharp, high-volume descent into the formation. This rapid drop is necessary to flush out the last remnants of selling pressure.

Phase 2: The Energy Channel (The "No-Return" Zone)

The price enters the Handle channel, a defined equilibrium zone where the final sell orders are absorbed.

This is where the major trend channels converge. Once price consolidates here and breaks north, there is no logical support left to retest—it becomes a one-way trajectory. The "no-return point."

Phase 3: The Launchpad

This entire structure acts as a rocket launch base, compressing energy for the next macro leg up confirming a bogger Fibonacci. The completion of this base targets a powerful ignition in January 2027.

This is not trading advice or signal at all

This is the identification of a mathematical and structural precedent that now stands, clear and present, on the chart. The responsibility for any action taken—or not taken—rests solely with the individual.

The market is a mechanism.

This is how its gears are aligning.

The Great Channel: The Great Reset from 9.5A Once-in-a-Decade Market Opportunity

The Great Channel thesis presents a compelling long-term market structure that is becoming increasingly difficult to ignore. From a macro-technical perspective, current price action suggests we may be trading at, or extremely close to, the lowest valuation level we are likely to witness over the next decade. Even the next cyclical low, should it occur, may still print at levels higher than today’s price.

This outcome is not guaranteed, but it represents one of the most probable scenarios on the table and one that now carries more conviction than ever before. The concept of the Great Channel first emerged in 2024 as a theoretical framework; however, evolving market behavior indicates that it may now be transitioning from hypothesis into structural reality. If confirmed, this channel has the potential to reprice the market into entirely new regimes.

Importantly, this structure does not conflict with the broader cup-and-handle formation that many long-term participants are tracking. On the contrary, the two patterns may be complementary, with the cup-and-handle reaching full maturity only after a potential Great Reset event. Such a reset could occur near the extreme boundaries of the Great Channel, precisely where asymmetric risk-to-reward conditions are most favorable.

From this vantage point, current levels may represent the most attractive strategic accumulation zone we are likely to see for many years to come. For patient, long-term traders and investors, this region offers a rare alignment of macro structure, technical positioning, and cyclical timing—an opportunity that may not present itself again for a very long time.

Natural Gas (NG): The Freestyle Framework Natural Gas: The Freestyle Landscape

This is not a forecast. It is a dynamic structural map.

Designed for the discretionary trader, this "Freestyle" framework deconstructs Natural Gas into its core technical components: cyclical rhythms, evolving Elliott Wave structures, adaptive price channels, and multi-layered zones of confluence.

We provide the architecture; you dictate the strategy.

Within This Framework, You Will Identify:

- Cyclical Turning Nodes: Time-based projections where trend exhaustion or acceleration is statistically heightened.

- Price Channel Evolution: Visualizing the market's breathing pattern through expanding and contracting volatility corridors.

- Confluence Zones: High-Probability regions where support/resistance, Fibonacci projections, and channel boundaries cluster, defining the market's true decision points.

- Momentum & Risk Gradients: Areas shaded for potential trend acceleration or reversal, framing asymmetric risk/reward opportunities.

The Core Philosophy: Trade Context, Not Clarity.

This map eliminates the noise of directional bias. Instead, it provides a professional-grade canvas to:

Plan high-probability setups within predefined zones.

Anticipate volatility shifts before they occur.

Objectively manage risk by highlighting invalidation levels.

Align your unique strategy (swing, position) with the market's inherent structure.

Disclaimer: This analysis is for informational and educational purposes only. It is a framework for context, not a substitute for independent analysis. All trading decisions and risk management are solely the responsibility of the individual. Past performance is not indicative of future results.

Trade The Reaction. Navigate The Structure.

Extended Scinario to Fall Zone from 8.5This scenario appears more plausible to me personally, and confirmation of it should emerge in March 2026 if the critical buying zone is reached. The period from March to April could represent a very strong buying opportunity, potentially serving as the final upward move toward the 8.5 area.

This reflects a personal opinion and general market perspective only. It is not investment, trading, or financial advice, and should not be interpreted as a recommendation to buy or sell any asset.

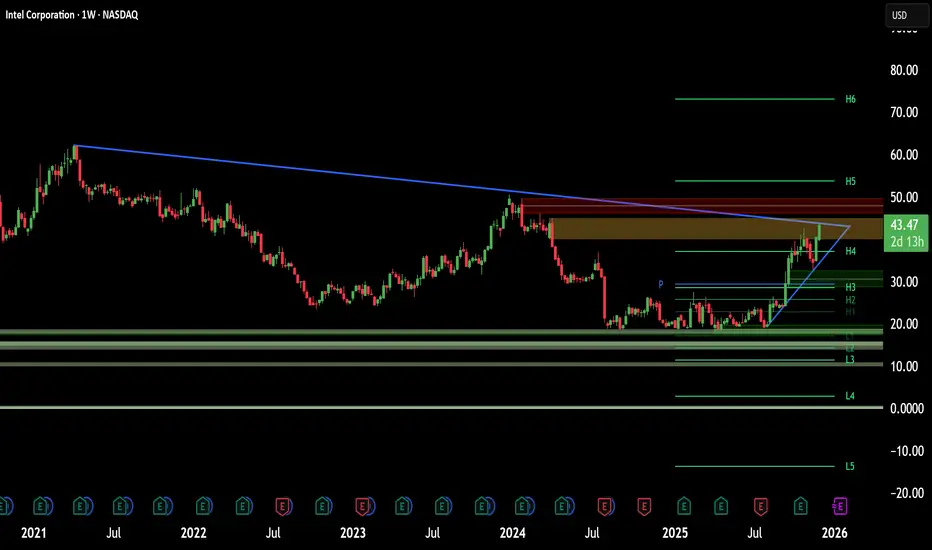

Is Intel’s Apple Deal the Ultimate Pivot?Intel (NASDAQ: INTC) stock soared over 116% this year. Reports suggest Apple may use Intel’s foundry by 2027. We analyze the drivers behind this potential resurrection.

Geopolitics & Geostrategy: The Stability Premium

In a volatile world, Intel offers a "stability premium." TSMC’s concentration in Taiwan risks Western supply chains. The US government now holds a ~10% stake in Intel. This actively incentivizes domestic production to secure the grid. Apple chooses Intel to hedge against geopolitical friction. This move aligns with US strategic interests, treating Intel as a sovereign asset.

Management & Leadership: The Tan Effect

CEO Lip-Bu Tan drives a massive cultural shift. He replaced Pat Gelsinger’s engineering vision with operational discipline. Tan prioritizes customer listening, an area where Intel historically struggled. This pivot is paying off. Securing Apple proves Intel is shedding its "arrogant" legacy. It is becoming a true service-oriented foundry.

Technology & Innovation: The 18A-P Advantage

The deal relies on Intel’s **18A-P process technology**. Apple aims to use this for entry-level M-series chips. This validates Intel's aggressive manufacturing roadmap. Additionally, the Trump administration invested $150 million in xLight. This startup develops next-gen lithography lasers to aid chipmaking. It reinforces the ecosystem surrounding Intel’s manufacturing capabilities.

Business Models: The Foundry Pivot

Intel is transforming from a product company to a hybrid foundry. Analysts estimate the Apple deal could generate ~$1 billion annually. However, the "Apple Seal of Approval" is worth far more. It signals to giants like Qualcomm that Intel is ready. It also creates leverage against TSMC’s pricing power.

Final Verdict: The Apple rumors convert Intel into a legitimate turnaround play. US geopolitical interests align with the new leadership. Validated technology suggests Intel’s worst days are likely over.

D-Wave: Quantum Leap or Valuation Bubble?D-Wave Quantum (QBTS) has outperformed peers in 2025, but a divergence between practical defense contracts and insider selling signals a critical pivot point for 2026.

D-Wave Quantum has emerged as the surprise breakout of the year, decoupling from competitors like IonQ and Rigetti to deliver triple-digit gains before a recent correction. While the stock has pulled back from its October highs, the fundamental thesis has shifted from speculative "science projects" to deployable national security assets. The question for 2026 is whether revenue execution can catch up to an $8 billion market cap that currently trades at a premium to reality.

Geostrategy & Geopolitics: The Huntsville Stronghold

The most significant development for D-Wave is not in Silicon Valley, but in Huntsville, Alabama. The installation of the Advantage2™ system at Davidson Technologies places D-Wave at the heart of the US missile defense ecosystem. In a geostrategic landscape defined by US-China technological decoupling, D-Wave has effectively become a "dual-use" asset. The system is now operational for Department of Defense (DoD) applications, specifically targeting contested logistics and radar resource deployment—problems where seconds determine survival.

Technology & Science: The Annealing Advantage

While competitors chase the "gate-model" holy grail, D-Wave’s dominance in quantum annealing offers immediate utility. The sixth-generation Advantage2 system is not theoretical; it is solving energy-minimization problems today. This scientific pragmatism was validated when Fast Company recognized D-Wave in its "Next Big Things in Tech" awards. The technology's ability to handle 20-way connectivity allows for higher-fidelity modeling of real-world chaos, distinguishing it from peers still stuck in error-correction limbo.

Business Models & Innovation: Quantum-as-a-Service (QaaS)

D-Wave is successfully transitioning from hardware sales to a high-margin recurring revenue model via its Leap™ cloud service . By offering "Quantum-as-a-Service," the company allows clients like NTT DOCOMO to access solvers remotely, reducing paging signal traffic by 15% without capital-intensive hardware purchases. This business model innovation mirrors the early SaaS evolution, creating sticky ecosystems where customers build proprietary hybrid applications on top of D-Wave’s architecture, increasing switching costs and lifetime value.

Macroeconomics & Economics: The Valuation Disconnect

Despite the bullish narrative, the economic fundamentals demand caution. D-Wave trades at a price-to-sales ratio exceeding 300x, a valuation that assumes flawless execution. While third-quarter revenue doubled to $3.7 million, the company reported a $27.7 million operating loss. However, the balance sheet is a fortress: with **$836.2 million in cash**, D-Wave is insulated from the high-interest-rate environment that crushes capital-poor tech firms. This capital buffer allows them to burn cash on R&D through 2027 without immediate dilution risks.

Management & Leadership: Vision vs. Execution

Leadership signals are currently mixed. CEO Alan Baratz has been a vocal defender of the company's "commercial-first" strategy, effectively countering skeptics in *The Wall Street Journal*. However, insider activity paints a complex picture. Baratz sold approximately $3.9 million in stock in mid-November, a move that often rattles retail sentiment. Investors must weigh this liquidity event against the strategic clarity the governing council has provided regarding the company's roadmap toward profitability.

Industry Trends & Cyber: The Real-World ROI

The industry is moving from "quantum supremacy" experiments to ROI-driven case studies. D-Wave is leading this trend across multiple verticals:

* Public Safety: A joint project with **North Wales Police** reduced incident response planning from months to minutes.

* Cyber-Logistics: The US Army utilizes the tech to optimize fuel breaks for wildfire management, a critical infrastructure protection capability.

These applications prove that D-Wave is solving "NP-hard" optimization problems that classical supercomputers struggle to process efficiently.

Patent Analysis & Intellectual Property

D-Wave has constructed a formidable defensive moat with over 250 U.S. patents . Their IP strategy focuses heavily on the hybridization of quantum and classical processing, ensuring they own the interface where business problems meet quantum solvers. This patent portfolio makes them a potential acquisition target for hyperscalers seeking to bypass years of R&D in the annealing space.

Strategic Outlook

D-Wave is no longer a penny stock gamble; it is a capitalized institutional play with backing from the Swiss National Bank . However, the current valuation prices are based on years of growth upfront. The stock is a "Hold" for conservative portfolios but a strategic "Buy" on dips for those betting on the US defense sector’s rapid adoption of quantum logistics.

Is Cisco Building the Internet of Tomorrow or Something Else?Cisco Systems has undergone a dramatic transformation in 2025, evolving from a traditional hardware vendor into what the company positions as the architect of secure, AI-driven global infrastructure. With fiscal year 2025 revenue reaching $56.7 billion and a remarkable 30% surge in operating cash flow, Cisco's financial performance tells only part of the story. The company has strategically positioned itself at the intersection of three critical technological timelines: the immediate AI infrastructure boom, the ongoing geopolitical supply chain realignment, and the long-term quantum computing development.

The company's geopolitical strategy has been particularly aggressive. In response to escalating US-China trade tensions and tariffs reaching up to 145% on certain components, Cisco has pivoted its manufacturing operations to India, establishing it as a new global export hub. Simultaneously, the company launched its Sovereign Critical Infrastructure portfolio in Europe, offering air-gapped solutions that address European concerns about digital sovereignty and US extraterritorial reach. These moves position Cisco as the "trusted vendor" for Western alliance infrastructure while monetizing the fragmentation of the global internet.

On the technology front, Cisco has made bold bets on the future. A landmark partnership with IBM aims to build the world's first large-scale quantum network by the early 2030s, with Cisco developing the optical infrastructure to connect quantum processors. The company has also integrated SpaceX's Starlink into its SD-WAN portfolio and participated in NASA's Artemis program. Meanwhile, its AI-native Hypershield security platform, protected by the company's 25,000th patent, and the integration of the Splunk acquisition demonstrate Cisco's push into AI-era cybersecurity.

The convergence of these initiatives reveals a company no longer simply selling networking equipment, but rather positioning itself as essential infrastructure for Western technological sovereignty. With explosive demand from hyperscaler customers generating over $2 billion in AI infrastructure orders and analysts raising price targets amid a 25% stock rally, Cisco appears to have successfully weaponized the geopolitical moment to reinforce its market position for the next generation of computing.

Is Boeing's Defense Bet America's New Arsenal?Boeing's recent stock appreciation stems from a fundamental strategic pivot toward defense contracts, driven by intensifying global security tensions. The company has secured major wins, including the F-47 Next Generation Air Dominance (NGAD) fighter contract worth over $20 billion and a $4.7 billion deal to supply AH-64E Apache helicopters to Poland, Egypt, and Kuwait. These contracts position Boeing as central to U.S. military modernization efforts aimed at countering China's rapid expansion of stealth fighters like the J-20, which now rivals American fifth-generation aircraft production rates.

The F-47 program represents Boeing's redemption after losing the Joint Strike Fighter competition two decades ago. Through its Phantom Works division, Boeing developed and flight-tested full-scale prototypes in secret, validating designs through digital engineering methods that dramatically accelerated development timelines. The aircraft features advanced broadband stealth technology and will serve as a command node controlling autonomous drones in combat, fundamentally changing air warfare doctrine. Meanwhile, the modernized Apache helicopter has found renewed relevance in NATO's Eastern flank defense strategy and counter-drone operations, securing production lines through 2032.

However, risks remain in execution. The KC-46 tanker program continues facing technical challenges with its Remote Vision System, now delayed until 2027. The F-47's advanced variable-cycle engines are two years behind schedule due to supply chain constraints. Industrial espionage, including cases where secrets were sold to China, threatens technological advantages. Despite these challenges, Boeing's defense portfolio provides counter-cyclical revenue streams that hedge against commercial aviation volatility, creating long-term financial stability as global rearmament enters what analysts describe as a sustained "super-cycle" driven by great power competition.

Can One Company Power America's Nuclear Future?BWX Technologies (BWXT) has positioned itself at the critical intersection of national security and energy infrastructure, establishing dominance in the advanced nuclear sector through strategic contracts and technological leadership. The company's Q3 2025 results reveal remarkable momentum, with revenue reaching $866 million (a 29% year-over-year increase) and total backlog surging to $7.4 billion, a 119% increase. With a book-to-bill ratio of 2.6 times, BWXT demonstrates demand substantially exceeding current capacity, driven by converging forces of decarbonization, electrification, and the explosive growth of AI power requirements.

BWXT's competitive moat extends across multiple dimensions. The company secured pivotal defense contracts worth $1.5 billion for domestic uranium enrichment and $1.6 billion for high-purity depleted uranium production, directly addressing America's strategic vulnerability to foreign fuel dependence. Leading Project Pele, the Department of Defense's first transportable microreactor prototype delivering 1-5 MW, BWXT is manufacturing the reactor core for 2027 delivery, aligned with Executive Order 14299's mandate to accelerate advanced nuclear deployment for national security and AI infrastructure. This first-mover advantage positions the company strongly for follow-on programs like Project JANUS, which aims to deploy a military installation reactor by September 2028.

The company's technical superiority centers on mastery of TRISO fuel manufacturing tristructural isotropic particles that cannot melt under reactor conditions and serve as self-contained safety systems. BWXT controls proprietary patents for specialized HALEU fuel element designs and maintains strategic partnerships with Northrop Grumman (control systems) and Rolls-Royce LibertyWorks (power conversion), ensuring compliance with stringent DoD cybersecurity standards. This integrated approach spanning fuel enrichment authorization, patented component design, validated manufacturing capabilities, and defense-grade partnerships creates formidable barriers to competition while capturing the multi-decade tailwind of institutional nuclear adoption mandated by federal policy and geopolitical necessity.

Can One Company Control Computing's Future?Google has executed a strategic transformation from a digital advertising platform to a full-stack technology infrastructure provider, positioning itself to dominate the next era of computation through proprietary hardware and breakthrough scientific discoveries. The company's vertical integration strategy centers on three pillars: custom Tensor Processing Units (TPUs) for AI workloads, quantum computing breakthroughs with verifiable advantages, and Nobel Prize-winning drug discovery capabilities through AlphaFold. This approach creates formidable competitive barriers by controlling foundational computational infrastructure rather than relying on commodity hardware.

The TPU strategy exemplifies Google's infrastructure lock-in model. By designing specialized chips optimized for machine learning tasks, Google achieved superior energy efficiency and performance scaling compared to general-purpose processors. The company's multibillion-dollar deal with Anthropic, deploying up to one million TPUs, transforms a potential cost center into a profit generator while locking competitors into Google's ecosystem. This technical dependence makes migration to rival platforms financially prohibitive, ensuring Google monetizes a significant portion of the generative AI market through its cloud services regardless of which AI models succeed.

Google's quantum computing achievement represents a paradigm shift from theoretical benchmarks to practical utility. The Willow chip's "Verifiable Quantum Advantage" demonstrates a 13,000-times speedup over classical supercomputers in physics simulations, with immediate applications in molecular structure mapping for drug discovery and materials science. Meanwhile, AlphaFold delivers quantifiable economic impact, reducing Phase I drug development costs by approximately 30% from over $100 million to $70 million per candidate. Isomorphic Labs has secured nearly $3 billion in pharmaceutical partnerships, validating this high-margin revenue stream independent of advertising.

The geopolitical implications are profound. Google holds the second-highest number of quantum technology patents globally, with strategic IP covering essential scaling technologies like chip tiling and error correction. This intellectual property portfolio creates a technical chokepoint, positioning Google as a mandatory licensing partner for nations seeking to deploy quantum technology. Combined with the dual-use nature of quantum computing for both commercial and military applications, Google's dominance extends beyond market competition to national security infrastructure. This convergence of proprietary hardware, scientific breakthroughs, and IP control justifies premium valuations as Google transitions from cyclical advertising dependence to an indispensable deep-tech infrastructure provider.

Can Software Win Wars and Transform Commerce?Palantir Technologies has emerged as a dominant force in artificial intelligence, achieving explosive growth through its unique positioning at the intersection of national security and enterprise transformation. The company reported its first billion-dollar quarter with 48% year-over-year sales growth, driven by an unprecedented 93% surge in U.S. commercial revenue. This performance stems from Palantir's proprietary Ontology architecture, which solves the critical challenge of unifying disparate data sources across organizations, and its Artificial Intelligence Platform (AIP) that accelerates deployment through intensive bootcamp sessions. The company's technological moat is reinforced by strategic patent protections and a remarkable 94% Rule of 40 score, signaling exceptional operational efficiency.

Palantir's defense entrenchment provides a formidable competitive advantage and guaranteed revenue streams. The company secured a $618.9 million Army Vantage contract and deployed the Maven Smart System for the Marine Corps, positioning itself as essential infrastructure for the Pentagon's Combined Joint All-Domain Command and Control strategy. These systems enhance battlefield decision-making, with targeting officers processing 80 targets per hour versus 30 without the platform. Beyond U.S. forces, Palantir supports NATO operations, assists Ukraine, and partners with the UK Ministry of Defence, creating a global network of high-margin, long-term government contracts across democratic allies.

Despite achieving profitability with 26.8% operating margins and maintaining $6 billion in cash with virtually no debt, Palantir trades at extreme valuations of 100 times revenue and 224 times forward earnings. With 84% of analysts recommending Hold or Sell ratings, the market remains divided on whether the premium is justified. Bulls argue the valuation reflects Palantir's transformation from niche government contractor to critical AI infrastructure provider, with analysts projecting potential revenue growth from $4.2 billion to $21 billion. The company's success across nine strategic domains—from military modernization to healthcare analytics—suggests it has built an "institutionally required platform" that could justify sustained premium pricing.

The investment thesis ultimately hinges on whether Palantir's structural advantages—its proprietary data integration technology, defense entrenchment, and accelerating commercial adoption—can sustain the growth trajectory demanded by its valuation. While the platform's complexity requires heavy customization and limits immediate scalability compared to simpler competitors, the 93% commercial growth rate validates enterprise demand. Investors must balance the company's undeniable technological and strategic positioning against valuation risk, with any growth deceleration likely triggering significant multiple compression. For long-term investors willing to weather volatility, Palantir represents a bet on AI infrastructure dominance across both military and commercial domains.

BigBear (BBAI) — Expanding AI Leadership in Defense IntelligenceCompany Overview:

BigBear.ai Holdings, Inc. NYSE:BBAI is a leading provider of AI-powered decision intelligence for defense, supply chain, and digital identity markets—offering investors exposure to the rapidly growing AI and analytics sector focused on mission-critical applications.

Key Catalysts:

Defense expansion: New U.S. Navy partnership for UNITAS 2025 and strategic alliance with Tsecond strengthen BigBear.ai’s role in real-time, edge-based AI processing via ConductorOS and BRYCK platforms.

Long-term contracts: Over $178 million in multi-year defense deals provide strong revenue visibility and recurring income stability.

Strategic momentum: Growing adoption across national security agencies underscores BigBear.ai’s position in U.S. defense modernization efforts.

Investment Outlook:

Bullish above: $6.80–$7.00

Upside target: $17.00–$18.00, supported by defense partnerships, scalable AI deployment, and national security demand.

#BigBearAI #ArtificialIntelligence #DefenseTech #NationalSecurity #EdgeComputing #AIAnalytics #Investing #BBAI

Can Memory Chips Become Geopolitical Weapons?Micron Technology has executed a strategic transformation from commodity memory producer to critical infrastructure provider, positioning itself at the intersection of AI computing demands and U.S. national security interests. The company's fiscal 2025 performance demonstrates this pivot's success, with data center revenue surging 137% year-over-year to comprise 56% of total sales. Gross margins expanded to 45.7% as the company captured pricing power across both its advanced High-Bandwidth Memory (HBM) portfolio and traditional DRAM products. This dual-margin expansion stems from an unusual market dynamic: capacity reallocation toward specialized AI chips has created artificial supply constraints in legacy memory, driving price increases exceeding 30% in some segments. In contrast, HBM3E capacity through 2026 is already sold out.

Micron's technological leadership centers on power efficiency and manufacturing innovation that translate directly into customer economics. The company's HBM3E solutions deliver bandwidth exceeding 1.2 TB/s while consuming 30% less power than competing 8-high configurations—a critical advantage for hyperscale operators managing electricity costs across massive data center footprints. This efficiency edge is reinforced by scientific advances in manufacturing, particularly the mass production deployment of 1γ DRAM using Extreme Ultraviolet lithography. This node transition delivers over 30% more bits per wafer than previous generations while reducing power consumption by 20%, creating structural cost advantages that competitors must match through heavy R&D investment.

The company's unique position as America's sole HBM manufacturer has transformed it from a component supplier to a strategic national asset. Micron's $200 billion U.S. expansion plan, supported by $6.1 billion in CHIPS Act funding, aims to produce 40% of its DRAM capacity domestically within a decade. This geostrategic positioning grants preferential access to U.S. hyperscalers and government projects requiring secure, domestically sourced components, a competitive moat independent of immediate technological specifications. Combined with a robust intellectual property portfolio covering 3D memory stacking and secure boot architectures, Micron has established multiple defensive layers that transcend typical semiconductor industry cycles, validating an investment thesis for sustained high-margin growth through structural rather than cyclical drivers.

Could One Alaskan Mine Reshape Global Power?Nova Minerals Limited has emerged as a strategically critical asset in the escalating U.S.-China resource competition, with its stock surging over 100% to reach a 52-week high. The catalyst is a $43.4 million U.S. Department of War funding award under the Defense Production Act to develop domestic military-grade antimony production in Alaska. Antimony, a Tier 1 critical mineral essential for defense munitions, armor, and advanced electronics, is currently imported by the U.S. in its entirety, with China and Russia controlling the global market. This acute dependency, coupled with China's recent export restrictions on rare earths and antimony, has elevated Nova from mining explorer to national security priority.

The company's dual-asset strategy offers investors exposure to both sovereign-critical antimony and high-grade gold reserves at its Estelle Project. With gold prices exceeding $4,000 per ounce amid geopolitical uncertainty, Nova's fast-payback RPM gold deposit (projected sub-one-year payback) provides crucial cash flow to self-fund the capital-intensive antimony development. The company has secured government backing for a fully integrated Alaskan supply chain from mine to military-grade refinery, bypassing foreign-controlled processing nodes. This vertical integration directly addresses supply chain vulnerabilities that policymakers now treat as wartime-level threats, evidenced by the Department of Defense's renaming to the Department of War.

Nova's operational advantage stems from implementing advanced X-Ray Transmission ore sorting technology, achieving a 4.33x grade upgrade while rejecting 88.7% of waste material. This innovation reduces capital requirements by 20-40% for water and energy, cuts tailings volume up to 60%, and strengthens environmental compliance critical for navigating Alaska's regulatory framework. The company has already secured land use permits for its Port MacKenzie refinery and is on track for initial production by 2027-2028. However, long-term scalability depends on the proposed $450 million West Susitna Access Road, with environmental approval expected in Winter 2025.

Despite receiving equivalent Department of War validation as peers like Perpetua Resources (market cap ~$2.4 billion) and MP Materials, Nova's current enterprise value of $222 million suggests significant undervaluation. The company has been invited to brief the Australian Government ahead of the October 20 Albanese-Trump summit, where critical minerals supply chain security tops the agenda. This diplomatic elevation, combined with JPMorgan's $1.5 trillion Security and Resiliency Initiative, which targets critical minerals, positions Nova as a cornerstone investment in Western supply chain independence. Success hinges on disciplined execution of technical milestones and securing major strategic partnerships to fund the estimated A$200-300 million full-scale development.

Can China Weaponize the Elements We Need Most?China's dominance over rare earth element (REE) processing has transformed these strategic materials into a geopolitical weapon. While China controls approximately 69% of global mining, its true leverage lies in processing, where it commands over 90% of Global capacity and 92% of permanent magnet manufacturing. Beijing's 2025 export controls exploit this chokehold, requiring licenses for REE technologies used even outside China, effectively extending regulatory control over global supply chains. This "long-arm jurisdiction" threatens critical industries from semiconductor manufacturing to defense systems, with immediate impacts on companies like ASML facing shipment delays and US chipmakers scrambling to audit their supply chains.

The strategic vulnerability runs deep through Western industrial capacity. A single F-35 fighter jet requires over 900 pounds of REEs, while Virginia-class submarines need 9,200 pounds. The discovery of Chinese-made components in US defense systems illustrates the security risk. Simultaneously, the electric vehicle revolution guarantees exponential demand growth. EV motor demand alone is projected to reach 43 kilotons in 2025, driven by the prevalence of permanent magnet synchronous motors that lock the global economy into persistent REE dependency.

Western responses through the EU Critical Raw Materials Act and US strategic financing establish ambitious diversification targets, yet industry analysis reveals a harsh reality: concentration risk will persist through 2035. The EU aims for 40% domestic processing by 2030, but projections show the top three suppliers will maintain their stranglehold, effectively returning to 2020 concentration levels. This gap between political ambition and physical execution stems from formidable barriers environmental permitting challenges, massive capital requirements, and China's strategic shift from exporting raw materials to manufacturing high-value downstream products that capture maximum economic value.

For investors, the VanEck Rare Earth/Strategic Metals ETF (REMX) operates as a direct proxy for geopolitical risk rather than traditional commodity exposure. Neodymium oxide prices, which plummeted from $209.30 per kilogram in January 2023 to $113.20 in January 2024, are projected to surge to $150.10 by October 2025 volatility driven not by physical scarcity but by regulatory announcements and supply chain weaponization. The investment thesis hinges on three pillars: China's processing monopoly converted into political leverage, exponential green technology demand establishing a robust price floor, and Western industrial policy guaranteeing long-term financing for diversification. Success will favor companies establishing verifiable, resilient supply chains in downstream processing and magnet manufacturing outside China, though the high costs of secure supply, including mandatory cybersecurity auditing and environmental compliance, ensure elevated prices for the foreseeable future.

Why Did Cheap Lumber Become a National Security Issue?Lumber prices have entered a structurally elevated regime, driven by the convergence of trade policy, industrial capacity constraints, and emerging technological demand. The U.S. administration's imposition of Section 232 tariffs - 10% on softwood lumber and up to 25% on wood products like cabinets - reframes timber as critical infrastructure essential for defense systems, power grids, and transportation networks. This national security designation provides legal durability, preventing a quick reversal through trade negotiations and establishing a permanent price floor. Meanwhile, Canadian producers facing combined duties exceeding 35% are pivoting exports toward Asian and European markets, permanently reducing North American supply by over 3.2 billion board feet annually that domestic mills cannot quickly replace.

The domestic industry faces compounding structural deficits that prevent rapid capacity expansion. U.S. sawmill utilization languishes at 64.4% despite demand, constrained not by timber availability but by severe labor shortages—the average logging contractor age exceeds 57, with one-third planning retirement within five years. This workforce crisis forces expensive automation investments while climate-driven wildfires introduce recurring supply shocks. Simultaneously, cybersecurity vulnerabilities in digitized mill operations pose quantifiable risks, with manufacturing ransomware attacks causing an estimated $17 billion in downtime since 2018. These operational constraints compound tariff costs, with new home prices increasing $7,500 to $22,000 before builder markups and financing costs amplify the final impact by nearly 15%.

Technological innovation is fundamentally reshaping demand patterns beyond traditional housing cycles. Cross-laminated timber (CLT) markets are growing at 13-15% annually as mass timber products displace steel and concrete in commercial construction, while wood-based nanomaterials enter high-tech applications from transparent glass substitutes to biodegradable electronics. This creates resilient demand for premium-grade wood fiber across diversified industrial sectors. Combined with precision forestry technologies - drones, LiDAR, and advanced logistics software—these innovations both support higher price points and require substantial capital investment that further elevates the cost baseline.

The financialization of lumber through CME futures markets amplifies these fundamental pressures, with prices reaching $1,711 per thousand board feet in 2021 and attracting speculative capital that magnifies volatility. Investors must recognize this convergence of geopolitical mandates, chronic supply deficits, cyber-physical risks, and technology-driven demand shifts as establishing a permanently elevated price regime. The era of cheap lumber has definitively come to an end, replaced by a high-cost, high-volatility environment that requires sophisticated supply chain resilience and financial hedging strategies.

Can Silicon Nanowires Redefine America's Battery Future?Amprius Technologies has positioned itself at the convergence of breakthrough materials science and national security imperatives, developing the world's highest energy density lithium-ion batteries through proprietary silicon nanowire technology. The company's batteries deliver up to 450 Wh/kg with targets exceeding 500 Wh/kg - nearly double the performance of conventional graphite-based cells - by solving silicon's historical expansion problems through a unique rooted nanowire architecture that allows internal expansion without structural degradation.

The strategic value extends beyond pure technology metrics. Amprius has secured $50 million in federal funding under Biden's Bipartisan Infrastructure Law and maintains critical defense contracts, including repeat orders totaling over $50 million from unmanned aerial systems manufacturers. This government backing reflects the company's role in domestic supply chain security, as its 100% silicon anode technology reduces reliance on graphite imports while establishing gigawatt-hour manufacturing capacity in Colorado. The Department of Energy's investment essentially validates Amprius as a strategic national asset in the race for advanced battery independence.

Financially, the company has demonstrated rapid acceleration with H1 2025 revenue of $26.4 million already surpassing all of 2024, while achieving a crucial 9% positive gross margin that signals viable unit economics. However, the path to mass market viability remains challenging, with estimated capital expenditures of $120-150 million per GWh of capacity highlighting the complexity of scaling nanowire manufacturing. Wall Street maintains unanimous "Strong Buy" ratings with price targets above $11.67, though recent insider selling following the stock's 1,100% surge raises questions about current valuation versus near-term execution risks.

The company's hybrid manufacturing strategy - leveraging over 1.8 GWh of international contract capacity while building domestic production - reflects a calculated approach to managing capital requirements while capturing immediate high-margin defense and aerospace opportunities. Success hinges on the operational launch of their Colorado facility in H1 2025 and the ability to translate their performance advantages into cost-competitive production for broader electric vehicle markets.

Can a Failed Star Rise from Space Ashes to Rule Earth's NetworksIridium Communications has engineered a remarkable strategic transformation from its predecessor's bankruptcy to become an indispensable global provider of connectivity. The company operates a resilient Low-Earth Orbit (LEO) constellation of 66 cross-linked satellites positioned 780 kilometers above Earth, delivering unprecedented 100% global coverage through L-band frequency transmission. This unique architecture provides superior weather resilience, low latency, and automatic signal re-routing capabilities that distinguish it from both traditional geostationary satellites and emerging broadband competitors like Starlink.

The company's ascendance is fundamentally driven by its critical role in national security operations. Iridium maintains multi-year, fixed-price contracts with the U.S. Department of Defense, providing Enhanced Mobile Satellite Services for mission-critical applications including secure communications, battlefield mapping, precise targeting, and real-time situational awareness. Unlike mass-market LEO providers focused on consumer broadband, Iridium deliberately targets high-value, specialized segments requiring uncompromising security and reliability. The company employs advanced encryption standards, including NSA Type 1 protocols, and has developed a comprehensive, multi-layered cybersecurity framework featuring quantum-resilient encryption and AI-driven threat detection.

Iridium's technological leadership extends beyond core communications through its hosted payload capabilities, supporting specialized applications like Aireon's global aircraft surveillance and exactEarth's ship tracking systems. The company's strategic differentiation lies in its focus on mission-critical applications rather than consumer services, creating a sustainable competitive moat protected by significant intellectual property and specialized technical capabilities. This positioning has enabled stable, high-margin revenue streams from government contracts while minimizing direct competition with volume-oriented providers.

The company's current trajectory represents not merely recovery but strategic re-emergence, capitalizing on mature market conditions where global IoT solutions, remote operations, and critical government communications align perfectly with Iridium's unique capabilities. With its robust financial foundation, expanding hosted payload services, and growing demand for resilient non-terrestrial connectivity, Iridium is positioned for sustained growth in an increasingly connected yet volatile global landscape, transforming from a cautionary tale of premature innovation into a compelling investment in critical infrastructure.

Can One Idaho Mine Break China's Grip on America's Defense?Perpetua Resources Corp. (NASDAQ: PPTA) has emerged as a critical player in America's quest for mineral independence through its Stibnite Gold Project in Idaho. The company has secured substantial backing with $474 million in recent financing, including investments from Paulson & Co. and BlackRock, plus over $80 million in Department of Defense funding. This support reflects the strategic importance of the project, which aims to produce both gold and antimony while restoring legacy mine sites and creating over 550 jobs in rural Idaho.

The geopolitical landscape has dramatically shifted in Perpetua's favor following China's export restrictions on antimony imposed in September 2024. With China controlling 48% of global antimony production and 63% of U.S. imports, Beijing's ban on sales to America has exposed critical supply chain vulnerabilities. The Stibnite Project represents America's only domestic antimony source, positioning Perpetua to potentially supply 35% of U.S. antimony needs and reduce dependence on China, Russia, and Tajikistan, which collectively control 90% of global supply.

Antimony's strategic significance extends far beyond its typical use as a mining commodity, serving as an essential component in defense technologies, including missiles, night vision equipment, and ammunition. The U.S. currently maintains stockpiles of just 1,100 tons against annual consumption of 23,000 tons, highlighting the critical supply shortage. Global antimony prices surged 228% in 2024 due to these shortages, while conflicts in Ukraine and the Middle East have amplified demand for defense-related materials.

The project combines economic development with environmental restoration, employing advanced technologies for low-carbon operations and partnering with companies like Ambri to develop liquid metal battery storage systems. Analysts have set an average price target of $21.51 for PPTA stock, with recent performance showing a 219% surge reflecting market confidence in the company's strategic positioning. As clean energy transitions drive demand for critical minerals and U.S. policies prioritize domestic production, Perpetua Resources stands at the intersection of national security, economic development, and technological innovation.