COPPER ~ TECHNICAL. 2H.Exiting this current channel may be accompanied by a significant price change...

So, we may have an eye on this after we buy or sell. but strongly.

Tradingidea

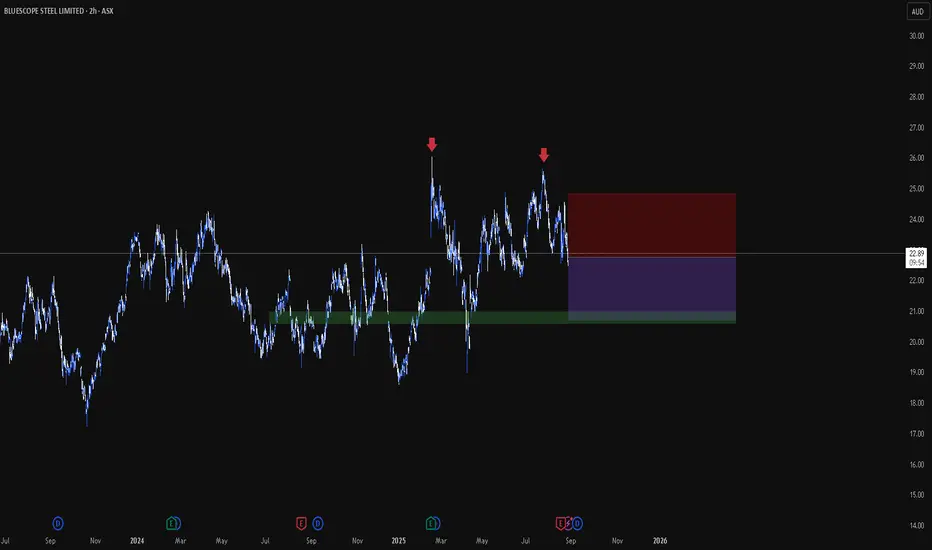

BLS | Tech. Short. The price two time tested most important resistance levels here... So, we may except it will now go down to nearest most strong support level. There where we have our TP.

CRWD | Check for buy? Idk.As we see, the time period of the waves is getting shorter in the time range.

My price prediction in this situation is that the price will go up to check new higher levels...

Rigetti | Technical analysis. 2H.This stock price performance is so crazy...

The price still looks like it's going to reach the previous highest mark first.

Cybersecurity Risks in the Global Trading SystemThreats, Vulnerabilities, and Strategic Defenses

In today’s highly interconnected world, the global trading system relies heavily on digital infrastructure. From stock exchanges and commodity markets to forex platforms and cross-border payment systems, technology is the backbone of modern trade. While digitization has improved speed, efficiency, and accessibility, it has also exposed global markets to significant cybersecurity risks. Cyber threats now pose one of the most critical non-financial risks to the stability, trust, and integrity of global trading systems.

Understanding the Global Trading System’s Digital Dependency

The global trading system includes stock exchanges, clearing corporations, depositories, brokerage firms, banks, commodity exchanges, logistics networks, and regulatory systems. These entities are interconnected through real-time data feeds, cloud services, APIs, and payment networks such as SWIFT. Even a minor cyber incident in one node can trigger a cascading effect across global markets.

High-frequency trading (HFT), algorithmic trading, and automated settlement systems depend on uninterrupted data flow and low latency. This dependency makes the system extremely sensitive to cyber disruptions, where milliseconds of delay or data manipulation can result in massive financial losses.

Major Cybersecurity Risks in Global Trading Systems

1. Data Breaches and Information Theft

One of the most common cybersecurity risks is data breaches. Trading platforms store sensitive information such as client identities, bank details, trade positions, proprietary algorithms, and market strategies. A successful breach can lead to insider trading, front-running, identity theft, and financial fraud.

State-sponsored hackers and cybercriminal groups often target financial institutions to steal market-sensitive data, which can be exploited for unfair trading advantages or sold on the dark web.

2. Market Manipulation Through Cyber Attacks

Cyber attackers can manipulate markets by altering data feeds, hacking trading algorithms, or spreading false information. For example, compromising a price feed can trigger automated buy or sell orders, leading to artificial volatility or flash crashes.

In algorithm-driven markets, even small distortions in data can cause massive ripple effects. Attackers may exploit vulnerabilities to manipulate liquidity, inflate volumes, or disrupt price discovery mechanisms.

3. Distributed Denial of Service (DDoS) Attacks

DDoS attacks flood trading platforms or exchanges with traffic, making systems unavailable to legitimate users. During critical market hours, such attacks can halt trading, delay order execution, or prevent access to risk management systems.

DDoS attacks are often used strategically during geopolitical tensions, economic announcements, or high-volatility events to destabilize markets or undermine confidence in financial institutions.

4. Ransomware Attacks on Financial Infrastructure

Ransomware attacks have become increasingly sophisticated. Hackers encrypt critical trading and settlement systems and demand ransom payments to restore access. If clearing and settlement systems are compromised, it can delay trade confirmations, margin calculations, and fund transfers.

Such attacks not only cause financial losses but also damage reputations and erode investor trust in the reliability of global trading systems.

Systemic Risk and Cascading Failures

Cybersecurity risks in global trading systems are not isolated threats—they represent systemic risk. A successful cyberattack on a major exchange, clearing house, or payment network can disrupt multiple markets simultaneously.

For example:

A compromised clearing corporation can delay settlements across thousands of trades.

A hacked forex trading platform can affect currency stability.

A cyberattack on a major bank can freeze liquidity across regions.

These cascading failures can amplify market panic, trigger margin calls, and even lead to broader financial instability.

Geopolitical and State-Sponsored Cyber Threats

Cybersecurity has become a tool of geopolitical conflict. Nation-states increasingly use cyber warfare to target financial infrastructure of rival economies. Global trading systems are prime targets because disrupting financial markets can weaken economic stability without direct military confrontation.

State-sponsored cyberattacks may aim to:

Undermine confidence in a country’s financial markets

Steal economic intelligence

Disrupt trade during sanctions or conflicts

Manipulate commodity or currency markets

This elevates cybersecurity from an IT issue to a matter of national and global economic security.

Third-Party and Supply Chain Vulnerabilities

Global trading systems rely on third-party vendors for cloud services, data analytics, trading software, and connectivity. A vulnerability in any third-party provider can expose multiple institutions simultaneously.

Supply chain attacks—where hackers infiltrate a trusted vendor to access clients—are particularly dangerous. Since vendors often have privileged system access, attackers can bypass traditional security controls and remain undetected for long periods.

Human Error and Insider Threats

Despite advanced security technologies, human error remains a major risk factor. Weak passwords, phishing emails, poor access controls, and lack of cybersecurity awareness can open doors to attackers.

Insider threats—whether malicious or accidental—are equally dangerous. Disgruntled employees or compromised insiders can leak sensitive data, sabotage systems, or provide access credentials to attackers.

Regulatory and Compliance Challenges

Global trading systems operate across multiple jurisdictions, each with different cybersecurity regulations and standards. Inconsistent regulatory frameworks create gaps that attackers can exploit.

Additionally, rapid technological innovation often outpaces regulation. New trading technologies such as decentralized finance (DeFi), blockchain-based trading, and AI-driven systems introduce fresh cybersecurity risks that regulators may not fully address yet.

Impact on Market Confidence and Trust

Trust is the foundation of global trading. Cyber incidents erode investor confidence, reduce participation, and increase risk premiums. Repeated cybersecurity failures can push investors away from affected markets and lead to long-term reputational damage for exchanges and financial institutions.

In extreme cases, loss of trust can cause liquidity shortages, capital flight, and prolonged market instability.

Strengthening Cybersecurity in Global Trading Systems

To mitigate cybersecurity risks, a multi-layered and proactive approach is essential:

Advanced Threat Detection: Use AI and machine learning to identify abnormal trading behavior and cyber intrusions in real time.

Zero-Trust Architecture: Assume no system or user is automatically trusted; verify every access request.

Regular Stress Testing: Conduct cyber stress tests and simulations to assess resilience against large-scale attacks.

Encryption and Data Protection: Secure data at rest and in transit using strong cryptographic standards.

Employee Training: Build cybersecurity awareness to reduce phishing and social engineering risks.

Global Coordination: Regulators, exchanges, and financial institutions must share threat intelligence and coordinate responses to cyber incidents.

Conclusion

Cybersecurity risks in the global trading system represent one of the most significant challenges to modern financial markets. As trading becomes faster, more automated, and more interconnected, the potential impact of cyber threats grows exponentially. These risks go beyond financial losses, threatening market integrity, systemic stability, and global economic trust.

Addressing cybersecurity is no longer optional—it is a strategic imperative. Only through continuous investment in technology, strong governance, international cooperation, and a culture of cyber resilience can the global trading system remain secure, stable, and trustworthy in an increasingly digital world.

XAUUSD PULLBACK AND PUMP (READ CAPTION)Hi trader's what do you think about gold

Gold (XAUUSD) is currently showing a bullish trade structure, with price respecting key demand zones and buyers maintaining control on pullbacks. The overall market behavior supports further upside continuation as long as price holds above major support areas.

🔹 Support Zone: 4307

This is the primary bullish support zone where buyers are actively defending price.

Holding above 4307 keeps the bullish bias valid.

🔹 Strong Bullish Zone: 4286–4273

This area represents a strong demand and accumulation zone.

Any pullback into 4286–4273 is considered a high-probability buying region, where strong bullish reactions are expected.

🔹 Resistance Zone: 4348

This is the first upside resistance, where price may face temporary rejection or consolidation.

A clean breakout and close above 4348 will confirm bullish continuation.

🔹 Supply Zone: 4373

This is the major upside target and supply area.

If Gold breaks above 4348, price is likely to extend toward the 4373 supply zone, where sellers may attempt to slow the move.

A strong breakout above this zone could signal further upside expansion.

📈 Market Outlook

Holding above 4307 → Bullish continuation expected

Pullback into 4286–4273 → Strong buy reaction zone

Break above 4348 → Opens path toward 4373 supply

Supply zone reaction will define next directional move

don't forget to like comment and follow

BTCUSD BULLISH OR BEARISH (READ CAPTION)Hi trader's what do you think about BTCUSD

BTCUSD is currently showing a bullish market structure, with price holding above key demand areas and buyers actively defending lower levels. The overall price action suggests a potential upside continuation.

🔹 Support Zone: 86,500

This is the primary bullish support zone where buyers have previously stepped in.

As long as price holds above 86,500, bullish momentum remains intact.

🔹 Bounce Support: 85,000

This level represents a strong bounce support and deeper retracement area.

If BTC pulls back toward 85,000, it is expected to attract strong buyer interest and trigger a bullish bounce.

🔹 Supply Zone: 90,200

This is the major upside target and supply area.

If bullish momentum continues, price is likely to move toward 90,200, where sellers may attempt to slow down or reject the move.

📈 Market Outlook

Holding above 86,500 → Bullish continuation expected

Deep pullback toward 85,000 → Strong buy reaction zone

Upside target → 90,200 supply zone

Supply zone reaction will define the next major move

The structure supports a bullish pullback → continuation setup, favoring buyers unless key supports break.

please don't forget to like comment and follow

BRCUUSD BULLISH OR TRAP (READ CAPTION)Hi trader's what do you think about BTCUSD

BTCUSD is currently developing a bullish setup, as the market is holding above key support levels and showing signs of buyer strength. Price is respecting the lower zones, indicating a possible continuation toward higher levels.

🔹 Support: 89,600

This is the primary support level where buyers have reacted previously.

As long as BTC stays above 89,600, bullish sentiment remains intact.

🔹 Strong Support: 89,000

This zone represents strong structural support.

If the market dips into 89,000, it is considered a high-probability demand area for buyers to re-enter.

🔹 Resistance: 92,200

This is the first bullish target, where short-term profit-taking may occur.

A breakout above 92,200 will strengthen bullish momentum.

🔹 Supply Zone: 94,000

This is the major supply zone where sellers may become active.

If BTC breaks above 94,000, the market could shift into a stronger bullish trend.

📈 Market Outlook

Holding above 89,600 / 89,000 → Bullish continuation expected

Break above 92,200 → Opens the way toward 94,000 supply zone

Supply at 94,000 will decide the next major directional move

please like comment and follow thank you

XAUUSD – Clean 1H Demand + 4H Support Reaction

Bias

Bullish short-term after price tapped a strong 1H demand zone that aligns perfectly with 4H support.

Why I Took This Setup

Price returned to a fresh 1H demand zone

Same level is a 4H support, giving stronger confluence

Liquidity was taken below the zone before the rejection

Strong bullish reaction + momentum shift on lower timeframes

Trade Plan

Entry: Inside the refined 1H demand zone

SL: Below the zone

TP: Next major swing high

Reasoning

Market grabbed liquidity, tapped a clean zone, and showed immediate strength. Structure is now pushing upward with clear bullish intention.

WIF/USDT - Fresh meme coin. Trading setup in chanal. Popular fresh meme coin – Dogwifhat

📊 CoinMarketCap Rank: #102

🐦 Twitter (X) : 152K followers

💬 Telegram : 50K members

✅ Highly liquid meme coin – traded on many major exchanges, including Binance.

After the hype phase , the coin is now declining along with the overall crypto market —no exceptions. Essentially, it broke below multiple channel supports , and the price is now sitting at the support of the outer channel.

I also notice a non-textbook Head & Shoulders pattern, which suggests a potential -64% breakdown . The last squeeze happened around this level.

Currently, we are seeing consolidation with increased volume , along with high-wick price action in this zone.

I've marked potential downside support zones as well as upside resistance targets on the chart. Consider this in your trading strategy!

STRK/USDT – Position accumulation in a descending channel.StarkNet - is a permissionless decentralized Validity-Rollup (also known as a “ZK-Rollup”). It operates as an L2 network over Ethereum, enabling any dApp to achieve unlimited scale for its computation – without compromising Ethereum’s composability and security, thanks to StarkNet’s reliance on the safest and most scalable cryptographic proof system – STARK.

StarkNet Contracts and the StarkNet OS are written in Cairo – supporting the deployment and scaling of any use case, whatever the business logic.

CoinMarketCap : #106

Twitter(X) : 346,4k

Currently, STRK is trading within a large descending channel , with the price sitting at the support of the inner channel . After the hype, the price has dropped by -95% ! The Series B & C Round zones are being tested. A -30% drop to the support of the outer channel is not ruled out.

STRK will likely move only when ETH starts growing , as it is an L2 solution.

During the listing phase , this coin was heavily hyped— bloggers were screaming to buy before it "took off" , but they forgot to mention that the rocket was headed downward . Most of them had no real idea what they were doing—it was all just for hype and content .

Now, few still believe in its potential … faith is gone .

But this is exactly why fear is unnecessary . Historically, negative zones often provide some of the best entry points.

I expect STRK to outperform ETH in profitability due to its low liquidity.

I’ve marked everything on the chart—consider this in your trading strategy.

Investors, Traders, and Policy Makers in the World MarketImportance and Difference.

Introduction

The global financial market is an intricate ecosystem where capital flows seamlessly across borders, industries, and sectors. Within this ecosystem, three fundamental participants play distinct yet interconnected roles — investors, traders, and policy makers. Each group contributes to the market’s structure, functioning, and stability in different ways.

Investors provide the long-term capital necessary for growth and innovation; traders ensure market liquidity and efficiency through short-term operations; and policy makers establish the regulatory and economic framework that governs both.

Understanding their importance and differences is essential for comprehending how the world market operates and responds to global financial dynamics.

1. Role and Importance of Investors

1.1 Who are Investors?

Investors are individuals or institutions that allocate capital to assets such as stocks, bonds, mutual funds, real estate, or startups with the expectation of earning long-term returns. Unlike traders, who focus on short-term market fluctuations, investors emphasize fundamental value and sustainability.

Investors can be categorized into:

Retail investors – individual participants investing personal funds.

Institutional investors – entities such as pension funds, insurance companies, mutual funds, and sovereign wealth funds managing large capital pools.

1.2 Importance of Investors in the Global Market

Capital Formation:

Investors are the backbone of economic growth. Their funds are used by corporations for expansion, innovation, and employment generation. When investors purchase shares or bonds, they provide the necessary capital for companies to operate and expand.

Long-term Stability:

Investors bring stability to the market through their long-term orientation. Unlike traders, they are less influenced by daily market volatility, ensuring that companies have a reliable source of capital even during uncertain times.

Corporate Governance:

Institutional investors often influence corporate governance by voting on important issues, promoting transparency, ethical conduct, and accountability. This oversight helps maintain investor confidence in global markets.

Economic Growth and Development:

By channeling savings into productive investments, investors drive infrastructure development, technological advancement, and job creation. Their confidence can determine the economic trajectory of entire nations.

Wealth Creation:

Investors benefit from dividends, interest, and capital appreciation, which enhances individual and institutional wealth. This wealth accumulation fuels consumption and savings, further stimulating the economy.

2. Role and Importance of Traders

2.1 Who are Traders?

Traders are market participants who buy and sell financial instruments — such as equities, commodities, currencies, or derivatives — to profit from short-term price movements. Their approach is usually technical, relying on charts, patterns, and market sentiment rather than long-term fundamentals.

Traders can be classified as:

Day traders: Execute multiple trades within a single day.

Swing traders: Hold positions for days or weeks.

Arbitrage traders: Exploit price differences across markets.

Algorithmic or high-frequency traders: Use computer algorithms to execute rapid trades.

2.2 Importance of Traders in the Global Market

Market Liquidity:

Traders enhance liquidity by constantly buying and selling assets, ensuring that other market participants can enter or exit positions easily. A liquid market reduces transaction costs and improves efficiency.

Price Discovery:

Through continuous trading activity, traders help establish fair market prices. Their collective actions reflect real-time market sentiment, economic data, and investor expectations, making markets more transparent.

Market Efficiency:

Traders exploit inefficiencies and arbitrage opportunities, which helps align prices with intrinsic value. This process of correcting mispriced assets contributes to overall market efficiency.

Risk Management and Hedging:

Traders also play a role in managing financial risks through derivative instruments. For instance, commodity traders help producers hedge against price volatility in oil, metals, or agricultural goods.

Economic Signaling:

The behavior of traders can act as a signal of market health. Sharp price movements or heavy trading volumes often indicate changes in investor sentiment, guiding policy makers and long-term investors in their decisions.

3. Role and Importance of Policy Makers

3.1 Who are Policy Makers?

Policy makers are government officials, central banks, and regulatory authorities responsible for shaping the financial, monetary, and fiscal policies that govern the global market. Their actions influence interest rates, inflation, exchange rates, taxation, and capital flow regulations.

Key examples include:

Central Banks (like the U.S. Federal Reserve, European Central Bank, Reserve Bank of India)

Financial Regulators (like SEBI, SEC, FCA)

Government Ministries and Economic Councils

3.2 Importance of Policy Makers in the Global Market

Economic Stability:

Policy makers ensure macroeconomic stability through monetary and fiscal policies. By adjusting interest rates and money supply, central banks can control inflation, manage unemployment, and stabilize currencies.

Regulation and Oversight:

Regulatory bodies protect investors and maintain market integrity by enforcing laws against fraud, insider trading, and market manipulation. Effective regulation enhances investor confidence and market credibility.

Crisis Management:

During financial crises, policy makers implement interventions such as bailouts, stimulus packages, or liquidity support to prevent systemic collapse. For example, central banks’ coordinated actions during the 2008 crisis prevented a global depression.

Trade and Capital Flow Management:

Policy makers influence global trade through tariffs, exchange rate policies, and cross-border investment regulations. Their decisions can encourage or restrict foreign investment and affect global capital mobility.

Long-term Economic Planning:

Governments design long-term economic strategies to promote sustainable development, technological innovation, and social welfare, ensuring that the market supports inclusive growth.

4. Interrelationship Between the Three Groups

Although their goals and methods differ, investors, traders, and policy makers are interdependent within the world market:

Investors and Traders:

Traders provide liquidity that allows investors to buy or sell assets without major price disruptions. Meanwhile, investors create long-term value that traders can speculate on in the short term.

Traders and Policy Makers:

Traders respond immediately to policy announcements — such as interest rate changes or fiscal packages — influencing market volatility. Policy makers, in turn, observe trader behavior as a barometer for market sentiment.

Investors and Policy Makers:

Investors rely on stable and predictable policies to make long-term decisions. Conversely, governments depend on investor confidence to finance public debt and stimulate economic growth.

This cyclical relationship ensures that each participant supports the other, maintaining balance within the global financial ecosystem.

5. Global Examples and Case Studies

2008 Financial Crisis:

The crisis highlighted how interconnected these three groups are. Excessive risk-taking by traders and institutions led to a collapse in investor confidence, prompting massive interventions by policy makers through quantitative easing and stimulus measures.

COVID-19 Pandemic (2020):

During the pandemic, investors sought safe assets, traders reacted to volatility, and policy makers injected liquidity and cut interest rates to stabilize economies. The coordinated response prevented a deeper global recession.

Inflation Control by Central Banks (2022–2023):

Central banks worldwide raised interest rates to combat inflation. Traders responded with shifts in bond and currency markets, while investors adjusted portfolios toward defensive assets, showing the dynamic interplay between all three.

6. Challenges Faced by Each Group

Investors: Face risks from inflation, policy uncertainty, and geopolitical tensions. Their challenge lies in maintaining returns amid market volatility.

Traders: Confront high competition, algorithmic dominance, and unpredictable market swings. Risk management and speed are critical to survival.

Policy Makers: Must balance economic growth with financial stability while avoiding overregulation or political interference. Global coordination remains a persistent challenge.

7. The Future of Their Roles in the Global Market

The future of the world market will be shaped by technology, globalization, and sustainability.

Investors are increasingly prioritizing ESG (Environmental, Social, Governance) principles.

Traders are adopting AI-driven and algorithmic systems to enhance speed and accuracy.

Policy Makers are developing frameworks for digital currencies, blockchain regulation, and climate finance.

This evolution will demand greater cooperation among all three to ensure inclusive and resilient global markets.

8. Conclusion

The global financial market is a dynamic system where investors, traders, and policy makers each play indispensable roles. Investors provide long-term capital and stability; traders inject liquidity and efficiency; and policy makers maintain order and economic balance.

Their interactions create a complex yet balanced ecosystem that fuels global economic growth, innovation, and development. Recognizing the distinctions and synergies among these three groups helps one appreciate the mechanisms that sustain the world market and the challenges that lie ahead in maintaining its stability and inclusiveness.

Commodity Supercycles and Resource ScarcityIntroduction

Commodities—ranging from energy and metals to agricultural products—are the essential building blocks of the global economy. Their prices fluctuate based on demand and supply dynamics, technological progress, and macroeconomic cycles. However, history reveals that commodity markets often experience prolonged periods of rising and falling prices known as “commodity supercycles.” These cycles, typically lasting decades, reflect fundamental transformations in the world economy—industrial revolutions, rapid urbanization, or structural shifts in demand.

In recent decades, economists and investors have increasingly linked commodity supercycles to resource scarcity, the growing challenge of balancing finite natural resources with the expanding needs of humanity. As population growth, industrialization, and the transition to green technologies intensify, questions about the sustainability of resource use have become central to global economic planning.

This essay explores the concept of commodity supercycles, their historical patterns, causes, and implications, as well as the relationship between these cycles and resource scarcity. It also examines how emerging trends such as renewable energy, recycling technologies, and geopolitical tensions are shaping the next possible supercycle.

Understanding Commodity Supercycles

A commodity supercycle refers to a long-term, broad-based price boom across multiple commodities, driven by structural shifts in global demand. Unlike short-term price fluctuations due to seasonal or cyclical economic activity, supercycles typically last 20 to 40 years. They are usually tied to periods of rapid industrialization or technological transformation that cause sustained increases in commodity consumption.

For example, the post-World War II reconstruction era, the 1970s oil shocks, and the China-led industrialization of the 2000s each corresponded with major supercycles. These booms were followed by extended downturns as supply caught up with demand or economic growth slowed.

Economists identify three key phases of a commodity supercycle:

Expansion Phase – Rising demand, limited supply, and increasing investment in resource extraction.

Peak and Plateau Phase – Supply gradually expands, demand growth stabilizes, and prices reach their highest levels.

Contraction Phase – Oversupply, slowing demand, and technological changes drive prices down over a long period.

Each phase reflects deep economic transformations that go beyond traditional business cycles, often linked to the rise and fall of global powers, demographic shifts, and major infrastructure booms.

Historical Overview of Commodity Supercycles

1. The 19th Century Industrial Revolution Cycle (1850–1914)

The first recognized supercycle was driven by the Industrial Revolution in Europe and North America. Rapid urbanization, rail expansion, and mechanized manufacturing led to soaring demand for coal, iron, steel, and agricultural commodities.

Technological innovation in steam engines, metallurgy, and transportation created a massive pull on global resources. Colonization expanded access to raw materials, but prices still rose sharply due to unprecedented demand. This cycle ended with the onset of World War I and the Great Depression, which collapsed trade and industrial output.

2. The Post-World War II Boom (1945–1973)

The second major supercycle followed World War II, driven by reconstruction in Europe and Japan, the rise of suburbanization, and the U.S. economic boom. Infrastructure projects, automobiles, and consumer goods required steel, copper, oil, and agricultural commodities. The Bretton Woods system, which stabilized exchange rates, and the establishment of multilateral trade institutions like the IMF and World Bank, supported global growth.

The cycle peaked with the 1973 oil crisis, when OPEC’s embargo sent oil prices skyrocketing, causing inflationary pressures and economic slowdown.

3. The China-Driven Supercycle (2000–2014)

The most recent supercycle was fueled by China’s industrialization and urbanization after joining the World Trade Organization (WTO) in 2001. Massive infrastructure spending, steel production, and construction caused an extraordinary demand surge for iron ore, copper, aluminum, coal, and oil.

Prices of most commodities reached historic highs between 2008 and 2011. However, by 2014, a slowdown in China’s growth and global oversupply brought the cycle to an end. The collapse in oil and metal prices marked the beginning of a prolonged downturn.

Causes of Commodity Supercycles

Several structural forces interact to create supercycles. The most significant include:

1. Industrialization and Urbanization

Periods of intense industrial expansion, such as in 19th-century Britain or 21st-century China, lead to sharp increases in commodity demand. Infrastructure development, housing, and manufacturing all require raw materials, creating upward pressure on prices.

2. Demographic Growth

Population booms in emerging economies increase demand for food, energy, and housing. For example, post-war baby booms and the rise of the global middle class have repeatedly expanded resource consumption.

3. Technological Innovation

Technological revolutions both create and destroy demand for commodities. The internal combustion engine increased oil demand; renewable technologies now increase demand for lithium, nickel, and copper. These transitions often reconfigure global trade flows.

4. Supply Constraints

Commodity supply is slow to adjust due to long investment cycles, geological limitations, and political instability. For instance, developing a new copper mine can take over a decade. Limited supply elasticity amplifies the impact of demand shocks.

5. Geopolitical and Policy Factors

Wars, trade restrictions, or resource nationalism can tighten supply and intensify price cycles. The 1970s oil crisis and recent Russia-Ukraine conflict illustrate how geopolitics can trigger commodity surges.

Resource Scarcity: A Growing Challenge

Resource scarcity refers to the limited availability of natural resources relative to human demand. This scarcity is not only physical but also economic—driven by rising extraction costs, environmental degradation, and geopolitical constraints.

1. Physical and Geological Limits

Many commodities, especially fossil fuels and certain metals, exist in finite quantities. As high-quality reserves are depleted, extraction becomes more expensive and energy-intensive. For example, new oil discoveries have declined steadily since the 1980s, raising concerns about “peak oil.”

2. Environmental Constraints

Mining, deforestation, and fossil fuel extraction cause environmental damage and carbon emissions. Climate change policies now restrict resource exploitation, creating a trade-off between economic growth and sustainability.

3. Economic and Political Constraints

Resource access is often limited by political instability, nationalization of assets, and export controls. Countries with critical resources may use them for strategic leverage, increasing global scarcity risk.

4. Water and Food Scarcity

Beyond metals and energy, water and arable land are becoming increasingly scarce. Global warming, desertification, and pollution threaten agricultural productivity, leading to food security challenges and potential social unrest.

The Link Between Supercycles and Resource Scarcity

Supercycles often exacerbate resource scarcity. During expansion phases, intense demand leads to rapid depletion of reserves, environmental damage, and overexploitation. As production costs rise, prices increase, creating feedback loops that sustain the cycle.

Conversely, resource scarcity can trigger new supercycles by increasing extraction costs and limiting supply. For example, the transition to renewable energy requires massive amounts of critical minerals like lithium, cobalt, and rare earth elements—resources that are themselves scarce and geographically concentrated.

This dynamic interplay means that resource scarcity is both a driver and a consequence of commodity supercycles. As one resource becomes scarce, economies adapt by shifting demand to substitutes—sometimes triggering new cycles in different commodities.

Case Studies: Resource Scarcity in Action

1. Oil and Energy Scarcity

Oil remains the world’s most important commodity. Periods of high prices, such as during the 1970s and 2000s, reflected both demand surges and fears of resource exhaustion. While technological innovations like fracking temporarily alleviated scarcity, geopolitical risks and environmental constraints continue to threaten long-term supply stability.

2. The Green Energy Transition and Critical Minerals

The global push toward decarbonization has created massive demand for metals such as lithium, nickel, cobalt, and copper. Electric vehicles (EVs), solar panels, and batteries rely on these inputs. However, these minerals are heavily concentrated in a few countries—such as the Democratic Republic of Congo (cobalt) and Chile (lithium)—raising concerns over future bottlenecks and new forms of resource dependency.

3. Water Scarcity and Agricultural Commodities

Climate change-induced droughts are reducing freshwater availability for irrigation. In regions like South Asia and Africa, this threatens food production and could trigger volatility in agricultural commodity markets such as wheat, rice, and soybeans. As populations grow, the risk of food inflation and social instability rises.

The Emerging 21st-Century Supercycle

Many analysts believe the world may be entering a new commodity supercycle, driven by structural transformations such as green industrialization, digital infrastructure, and geopolitical realignments.

Key Drivers:

Energy Transition – The shift from fossil fuels to renewables increases demand for transition metals and critical minerals.

Geopolitical Fragmentation – Resource nationalism, trade wars, and sanctions are disrupting supply chains, raising production costs.

Reindustrialization in the West – Efforts to “reshore” supply chains and reduce dependency on China are spurring domestic infrastructure investment.

Global Population and Urban Growth – With the world population surpassing 8 billion, resource demand for housing, energy, and food remains robust.

However, this new supercycle differs from past ones—it is shaped by sustainability imperatives, technological advances, and decarbonization policies. While demand for green metals is booming, fossil fuel demand may plateau or decline, making this supercycle more selective and diversified.

Economic and Market Implications

1. Inflationary Pressures

Sustained commodity price increases can fuel inflation, especially in emerging economies reliant on imports. The 2021–2023 period illustrated how energy and food shortages contributed to global inflation spikes.

2. Investment Opportunities

Supercycles create profitable opportunities in mining, energy, and infrastructure sectors. Investors anticipate long-term demand by financing exploration and extraction. However, volatility remains high, requiring risk management strategies.

3. Shifts in Global Power

Resource-rich nations—such as Australia, Chile, and Saudi Arabia—gain geopolitical leverage during supercycles. Conversely, resource-dependent importers face economic vulnerability and trade deficits.

4. Technological Innovation

Scarcity stimulates innovation. Rising commodity prices encourage investment in recycling, substitution, and efficiency technologies. For example, advances in battery chemistry aim to reduce reliance on cobalt.

Managing Resource Scarcity: Sustainable Pathways

To mitigate the risks of resource scarcity and stabilize future supercycles, policymakers and industries must pursue sustainable resource management strategies.

1. Circular Economy

Recycling and reusing materials can reduce pressure on primary extraction. The shift toward a circular economy—where waste becomes input—offers a long-term solution to resource depletion.

2. Technological Substitution

Innovation can replace scarce materials with more abundant ones. For instance, sodium-based batteries may reduce dependence on lithium, and carbon composites may replace steel in some applications.

3. Diversification of Supply

Developing multiple sources for critical materials reduces geopolitical dependency. Collaborative international frameworks can ensure more equitable resource distribution.

4. Resource Efficiency

Improving energy and material efficiency across industries can lower demand growth. Smart grids, energy-efficient buildings, and sustainable farming techniques play key roles.

5. Global Governance and Cooperation

International institutions must coordinate policies for resource management, ensuring fair trade, transparent supply chains, and environmental protection. Initiatives like the Extractive Industries Transparency Initiative (EITI) promote responsible mining and investment.

Conclusion

Commodity supercycles are more than economic phenomena—they are reflections of humanity’s evolving relationship with the planet’s resources. Each cycle marks a phase of industrial transformation, technological progress, and social change. Yet, they also expose the vulnerabilities of a world dependent on finite natural assets.

As we enter a new era defined by climate imperatives, energy transitions, and population growth, resource scarcity is likely to be the defining economic and political challenge of the 21st century. Whether this results in instability or innovation depends on how effectively societies manage the delicate balance between consumption and conservation.

Future supercycles may not be characterized by endless extraction, but by smart utilization, circular economies, and technological breakthroughs. In this sense, the path ahead requires not only economic foresight but also environmental responsibility—because managing resource scarcity wisely will determine the sustainability of global growth itself.

Positional Trading Globally1. Understanding Positional Trading

Positional trading is a strategy where a trader or investor takes a long-term position in an asset with the expectation that its price will move substantially in their favor over time. The trader ignores short-term volatility and focuses on the broader market trend.

Unlike day trading, which relies on short-term price fluctuations, positional trading depends on macro-level factors such as economic cycles, interest rates, corporate earnings, and geopolitical developments. The key objective is to ride a major trend until there are clear signs of reversal.

Key Characteristics of Positional Trading:

Holding period: Several weeks to years

Focus: Long-term trends and fundamentals

Tools used: Technical charts (weekly/monthly), fundamentals, macroeconomic indicators

Risk tolerance: Moderate to high

Goal: Capture large market movements rather than frequent small profits

Positional traders are patient and strategic, often viewing the market through a broad lens. They are less concerned about daily market noise and more focused on trend confirmation and momentum.

2. The Global Perspective on Positional Trading

Positional trading is practiced worldwide, from Wall Street to Dalal Street, and across all asset classes — equities, forex, commodities, and cryptocurrencies. Each global market has its own rhythm and volatility, which influences how positional traders operate.

a. United States

In the U.S., positional trading has deep roots due to the stability and liquidity of markets like the New York Stock Exchange (NYSE) and NASDAQ. Traders often rely on fundamental indicators such as earnings growth, Federal Reserve policies, and GDP trends.

Prominent examples include:

Warren Buffett, who epitomizes long-term positional investing with his buy-and-hold philosophy.

Ray Dalio, whose macro-trading strategies focus on long-term global economic shifts.

b. Europe

European positional traders pay close attention to interest rates, ECB policies, and energy prices, given the region’s sensitivity to commodities and geopolitical issues. The FTSE 100, DAX, and CAC 40 indices are common targets for positional plays.

c. Asia

In Asia, markets like India, Japan, and China have seen a surge in positional trading, especially among retail investors. India’s Nifty 50 and Sensex are popular for medium-to-long-term positions, supported by strong corporate growth and favorable demographics.

d. Middle East & Africa

In emerging economies, positional trading often centers on commodities like oil and gold. Traders focus on global demand-supply trends, OPEC decisions, and currency movements.

e. Global Commodities & Forex

In the forex market, positional traders bet on long-term currency trends based on interest rate differentials, inflation, and trade balances. Similarly, in commodities, traders analyze seasonal cycles, geopolitical tensions, and global demand patterns to hold long-term positions in assets like crude oil, gold, or copper.

3. Core Principles of Positional Trading

1. Trend Following

The foundation of positional trading lies in identifying and following trends. Traders use tools like:

Moving Averages (50-day, 200-day)

MACD (Moving Average Convergence Divergence)

ADX (Average Directional Index)

to determine whether a market is trending upward or downward.

2. Fundamental Analysis

Fundamentals play a critical role. Traders assess:

Earnings reports

Debt levels

Economic growth rates

Inflation and interest rates

Industry trends

A fundamentally strong company or economy provides the confidence to hold a position long-term.

3. Technical Confirmation

Even long-term traders use charts to find ideal entry and exit points. Weekly and monthly charts reveal major trend lines, support/resistance levels, and volume patterns that help refine timing.

4. Patience and Discipline

The hallmark of successful positional trading is patience. Traders must tolerate drawdowns and avoid reacting to short-term volatility. Emotional stability and adherence to a well-defined plan are essential.

5. Risk Management

Despite being long-term in nature, positional trading requires proper stop-loss levels, position sizing, and portfolio diversification to protect against adverse movements.

4. Strategies Used in Positional Trading

Positional traders globally use several strategic approaches depending on their risk appetite and market conditions:

a. Trend Following Strategy

This involves entering positions aligned with the prevailing trend — buying during uptrends and shorting during downtrends. Indicators like moving averages or trendlines confirm direction.

b. Breakout Strategy

Traders enter when the price breaks out of a major resistance or support zone, signaling the start of a strong trend. This is effective in markets with high momentum.

c. Fundamental Positioning

Based on long-term macroeconomic or corporate fundamentals. For example, investing in renewable energy stocks anticipating global energy transition trends.

d. Contrarian Strategy

This involves going against prevailing sentiment, buying undervalued assets when the majority are bearish, and selling overvalued ones during excessive optimism.

e. Global Macro Strategy

Positional traders adopt a macroeconomic approach — investing based on factors like interest rates, inflation, or geopolitical shifts. Hedge funds like Bridgewater Associates employ this strategy.

5. Tools and Indicators for Positional Traders

Successful positional trading depends on combining technical and fundamental tools. Key instruments include:

Moving Averages (SMA & EMA): To identify long-term trends

Relative Strength Index (RSI): To gauge overbought or oversold levels

MACD: To spot trend reversals

Fibonacci Retracement: For long-term entry levels

Volume Analysis: Confirms the strength of price movements

Economic Calendars: To track interest rate decisions, GDP data, inflation, etc.

Earnings Reports: For stock-specific decisions

Globally, platforms like TradingView, MetaTrader, and Bloomberg Terminal help traders analyze data across markets.

6. Global Examples of Successful Positional Trades

Apple Inc. (AAPL):

Long-term investors who held Apple since the early 2000s have seen massive returns as the company evolved into a global tech giant.

Gold (2008–2020):

Investors who entered during the 2008 financial crisis captured a multiyear bull run as central banks pursued monetary easing.

Bitcoin (2015–2021):

Early positional holders witnessed exponential gains as digital assets gained mainstream acceptance.

Indian IT Sector (2020–2023):

Traders who held positions in Infosys, TCS, or HCL Tech benefited from the global digital transformation wave.

These examples highlight how patience, conviction, and timing define the success of positional trading globally.

7. Advantages of Positional Trading

Lower Stress:

Since positions are held long-term, traders avoid the daily pressure of short-term fluctuations.

Time Efficiency:

Positional trading doesn’t require constant market monitoring.

Tax Efficiency:

In many countries, long-term capital gains are taxed at lower rates than short-term profits.

Compounding Growth:

The longer an investor holds a quality asset, the more compounding enhances returns.

Reduced Transaction Costs:

Fewer trades mean lower brokerage and slippage costs.

Ability to Capture Major Trends:

Long-term positioning allows traders to benefit from large, sustained price movements.

8. Challenges and Risks in Global Positional Trading

While rewarding, positional trading isn’t without challenges:

Market Volatility: Unexpected geopolitical events can disrupt long-term trends.

Interest Rate Changes: Central bank policies directly impact valuations.

Psychological Pressure: Holding during drawdowns tests emotional discipline.

Global Uncertainty: Economic downturns, wars, or pandemics can distort fundamentals.

Currency Fluctuations: For cross-border positions, forex risk can erode returns.

Hence, diversification, hedging, and dynamic risk management are crucial for sustainability.

9. Technology’s Role in Modern Positional Trading

Technology has revolutionized global positional trading. AI-driven analytics, big data, and automated alerts now help traders identify long-term opportunities more efficiently.

AI Algorithms: Analyze large datasets to detect emerging macro trends.

Machine Learning Models: Forecast long-term price behavior using pattern recognition.

Robo-Advisors: Assist in portfolio rebalancing based on market shifts.

Blockchain Transparency: Provides secure and traceable data for crypto positional traders.

Digital platforms also allow traders to participate globally, accessing assets across continents with minimal friction.

10. The Psychology of a Positional Trader

A successful positional trader embodies:

Patience: Understanding that wealth grows over time.

Conviction: Confidence in research-backed positions.

Resilience: Ability to withstand market corrections.

Discipline: Avoiding impulsive reactions to short-term volatility.

In essence, positional trading blends the mindset of an investor with the agility of a trader — creating a balanced approach to long-term wealth creation.

11. The Future of Global Positional Trading

As global markets evolve, positional trading is set to become even more strategic. Factors shaping its future include:

AI-based analytics that enhance long-term forecasting

Global capital flow integration allowing cross-border investments

Sustainable investing trends, as ESG factors drive long-term positions

Decentralized finance (DeFi) creating new asset classes for positional exposure

With increasing financial literacy and access to digital platforms, positional trading is becoming more democratized — accessible to both institutional and retail participants worldwide.

Conclusion

Positional trading globally stands at the crossroads of patience, knowledge, and vision. It requires understanding not only technical charts but also the economic heartbeat of nations and industries. In a world of constant volatility and noise, positional traders remain the calm strategists — those who see beyond the day-to-day chaos and focus on the long-term direction of progress.

By combining global market awareness, disciplined strategy, and emotional control, positional traders harness the true potential of markets — turning time into their greatest ally.

Master Correlation StrategiesUnlocking the Power of Inter-Market Relationships in Trading.

1. Understanding Correlation in Trading

Correlation refers to the statistical relationship between two or more financial instruments — how their prices move relative to each other. It is expressed through a correlation coefficient ranging from -1 to +1.

Positive Correlation (+1): When two assets move in the same direction. For example, crude oil and energy sector stocks often rise and fall together.

Negative Correlation (-1): When two assets move in opposite directions. For instance, the U.S. dollar and gold often have an inverse relationship — when one rises, the other tends to fall.

Zero Correlation (0): Indicates no consistent relationship between two assets.

Understanding these relationships helps traders predict how one market might respond based on the movement of another, enhancing decision-making and portfolio design.

2. Why Correlation Matters

In modern financial markets, where globalization links commodities, equities, currencies, and bonds, no asset class operates in isolation. Correlation strategies allow traders to see the “bigger picture” — understanding how shifts in one area of the market ripple across others.

Some key reasons why correlation is vital include:

Risk Management: Diversification is only effective when assets are uncorrelated. If all your holdings move together, your portfolio is not truly diversified.

Predictive Analysis: Monitoring correlated assets helps anticipate price moves. For example, a rally in crude oil might foreshadow gains in oil-dependent currencies like the Canadian Dollar (CAD).

Hedging Opportunities: Traders can offset risks by holding negatively correlated assets. For instance, pairing long stock positions with short positions in an inverse ETF.

Market Confirmation: Correlations can validate or contradict signals. If gold rises while the dollar weakens, the move is more credible than when both rise together, which is rare.

3. Core Types of Correlations in Markets

a. Intermarket Correlation

This examines how different asset classes relate — such as the link between commodities, bonds, currencies, and equities. For example:

Rising interest rates typically strengthen the domestic currency but pressure stock prices.

Falling bond yields often boost equity markets.

b. Intra-market Correlation

This focuses on assets within the same category. For example:

Technology sector stocks often move together based on broader industry trends.

Gold and silver tend to share similar price patterns.

c. Cross-Asset Correlation

This involves analyzing relationships between assets of different types, such as:

Gold vs. U.S. Dollar

Crude Oil vs. Inflation Expectations

Bitcoin vs. NASDAQ Index

d. Temporal Correlation

Certain correlations shift over time. For instance, the correlation between equities and bonds may be positive during economic growth and negative during recessions.

4. Tools and Techniques to Measure Correlation

Correlation is not merely an observation—it’s a quantifiable concept. Several statistical tools help traders measure and monitor it accurately.

a. Pearson Correlation Coefficient

This is the most widely used formula to calculate linear correlation between two data sets. A reading close to +1 or -1 shows a strong relationship, while values near 0 indicate weak correlation.

b. Rolling Correlation

Markets evolve constantly, so rolling correlation (using moving windows) helps identify how relationships shift over time. For example, a 30-day rolling correlation between gold and the USD can show whether their inverse relationship is strengthening or weakening.

c. Correlation Matrices

These are tables showing the correlation coefficients between multiple assets at once. Portfolio managers use them to construct diversified portfolios and reduce overlapping exposures.

d. Software Tools

Platforms like Bloomberg Terminal, TradingView, MetaTrader, and Python-based tools (like pandas and NumPy libraries) allow traders to calculate and visualize correlation efficiently.

5. Applying Correlation Strategies in Trading

a. Pair Trading

Pair trading is a market-neutral strategy that exploits temporary deviations between two historically correlated assets.

Example:

If Coca-Cola and Pepsi usually move together, but Pepsi lags temporarily, traders may go long Pepsi and short Coca-Cola, betting the relationship will revert.

b. Hedging with Negative Correlations

Traders can use negatively correlated instruments to offset risk. For instance:

Long positions in the stock market can be hedged by taking positions in safe-haven assets like gold or the Japanese Yen.

c. Sector Rotation and ETF Strategies

Investors track sector correlations with broader indices to identify leading and lagging sectors.

For example:

If financial stocks start outperforming the S&P 500, this could signal a shift in the economic cycle.

d. Currency and Commodity Correlations

Currencies are deeply linked to commodities:

The Canadian Dollar (CAD) often correlates positively with crude oil prices.

The Australian Dollar (AUD) correlates with gold and iron ore prices.

The Swiss Franc (CHF) is often inversely correlated with global risk sentiment, acting as a safe haven.

Traders can exploit these relationships for cross-market opportunities.

6. Case Studies of Correlation in Action

a. Gold and the U.S. Dollar

Gold is priced in dollars; therefore, when the USD strengthens, gold usually weakens as it becomes more expensive for other currency holders.

During 2020’s pandemic uncertainty, both assets briefly rose together — a rare situation showing correlation can shift temporarily under stress.

b. Oil Prices and Inflation

Oil serves as a barometer for inflation expectations. When crude prices rise, inflation fears grow, prompting central banks to tighten policies.

Traders who monitor this relationship can anticipate policy shifts and market reactions.

c. Bitcoin and Tech Stocks

In recent years, Bitcoin has shown increasing correlation with high-growth technology stocks. This suggests that cryptocurrency markets are influenced by risk sentiment similar to the equity market.

7. Benefits of Mastering Correlation Strategies

Enhanced Market Insight: Understanding inter-market dynamics reveals the underlying forces driving price movements.

Stronger Portfolio Construction: Diversify effectively by choosing assets that truly offset one another.

Smarter Risk Control: Correlation analysis highlights hidden exposures across asset classes.

Improved Trade Timing: Correlation signals help confirm or challenge technical and fundamental setups.

Global Perspective: By studying correlations, traders gain insight into how global events ripple through interconnected markets.

8. Challenges and Limitations

Despite its power, correlation analysis is not foolproof. Traders must be aware of its limitations:

Changing Relationships: Correlations evolve over time due to policy changes, crises, or shifting investor sentiment.

False Correlation: Sometimes two assets appear correlated by coincidence without a fundamental link.

Lag Effect: Correlation may not capture time delays between cause and effect across markets.

Overreliance: Correlation is one tool among many; combining it with technical, fundamental, and sentiment analysis produces more reliable outcomes.

9. Advanced Correlation Techniques

a. Cointegration

While correlation measures relationships at a moment in time, cointegration identifies long-term equilibrium relationships between two non-stationary price series.

For example, even if short-term correlation fluctuates, two assets can remain cointegrated over the long run — useful in statistical arbitrage.

b. Partial Correlation

This method isolates the relationship between two variables while controlling for others. It’s particularly helpful in complex portfolios involving multiple correlated instruments.

c. Dynamic Conditional Correlation (DCC) Models

These advanced econometric models (used in quantitative finance) measure time-varying correlations — essential for modern algorithmic trading systems.

10. Building a Correlation-Based Trading System

A professional correlation strategy can be structured as follows:

Data Collection: Gather historical price data for multiple assets.

Statistical Analysis: Calculate correlations and rolling relationships using software tools.

Strategy Design: Develop pair trades, hedges, or intermarket signals based on correlation thresholds.

Backtesting: Validate the system across different market phases to ensure robustness.

Execution and Monitoring: Continuously update correlation data and adjust positions as relationships evolve.

Risk Control: Implement stop-loss rules and diversification limits to prevent overexposure to correlated positions.

11. The Future of Correlation Strategies

In an era of high-frequency trading, AI-driven analytics, and global macro interconnectedness, correlation strategies are evolving rapidly. Machine learning models now identify non-linear and hidden correlations that traditional statistics might miss.

Furthermore, as markets integrate further — with crypto, ESG assets, and alternative data sources entering the scene — understanding these new correlations will be crucial for maintaining an edge in trading.

12. Final Thoughts

Mastering correlation strategies isn’t just about mathematics — it’s about understanding the language of global markets. Every movement in commodities, currencies, and indices tells a story about how capital flows across the world.

A trader who comprehends these relationships gains not only analytical power but also strategic foresight. By mastering correlation analysis, you move beyond isolated price charts and see the interconnected web that drives the global financial ecosystem.

In essence, correlation strategies are the bridge between micro-level technical trades and macro-level economic understanding. Those who can navigate this bridge with confidence stand at the forefront of modern trading excellence — armed with knowledge, precision, and an unshakable sense of market direction.

Currency Convertibility Issues in the Global MarketIntroduction

Currency convertibility is one of the fundamental pillars of the global financial system. It determines how freely a nation’s currency can be exchanged for foreign currencies, influencing trade, investment, and international economic stability. In a world increasingly interconnected through globalization, the concept of currency convertibility is central to understanding how nations engage in global commerce and finance. However, the issue of currency convertibility is complex and often tied to a country’s monetary policy, balance of payments, capital control measures, and overall economic health.

This essay explores the concept of currency convertibility in the global market, its types, significance, challenges, and the major issues that affect countries’ decisions to make their currencies fully convertible. It also examines case studies of economies that have struggled or succeeded with convertibility and provides an outlook on how currency convertibility impacts the global financial ecosystem.

1. Meaning of Currency Convertibility

Currency convertibility refers to the ease with which a country’s currency can be converted into another currency or gold. It represents the degree of freedom that individuals, businesses, and investors have in exchanging domestic currency for foreign currencies for trade, investment, or travel purposes.

Essentially, convertibility is an indicator of how open an economy is to international financial flows. When a currency is fully convertible, it can be freely exchanged without restrictions for any purpose. When it is partially convertible, certain limitations exist—usually to control capital outflow or to stabilize the domestic economy.

2. Types of Currency Convertibility

Currency convertibility is generally categorized into two main types:

a. Current Account Convertibility

This allows the exchange of domestic currency for foreign currency for trade in goods and services, interest payments, and remittances. It ensures smooth international trade and reflects a country’s openness to global commerce.

Most nations, including India, have achieved current account convertibility. This means residents can pay for imports or receive export payments in foreign currencies freely.

b. Capital Account Convertibility

This involves the freedom to convert domestic financial assets into foreign assets and vice versa. It allows unrestricted movement of capital across borders—such as investment in foreign stocks, bonds, real estate, or repatriation of profits.

While this form of convertibility attracts foreign direct investment (FDI) and portfolio flows, it can also expose the domestic economy to external shocks and speculative capital movements.

3. Importance of Currency Convertibility in the Global Market

Currency convertibility plays a vital role in integrating national economies into the global system. Its importance can be highlighted through several key dimensions:

Facilitating International Trade:

Convertibility enables smooth cross-border transactions, reducing transaction costs and delays. Exporters and importers can easily settle payments in international currencies like the US dollar or euro.

Encouraging Foreign Investment:

Foreign investors prefer investing in economies where they can easily convert their earnings into other currencies. Full convertibility signals economic openness and financial maturity.

Enhancing Market Confidence:

A convertible currency reflects the stability and credibility of a nation’s monetary policy. It builds confidence among traders, investors, and international partners.

Improving Resource Allocation:

When funds can flow freely across borders, resources are allocated more efficiently, and economies can tap into global capital pools.

Promoting Globalization:

Convertibility supports global integration, allowing citizens and companies to participate more actively in the international economy.

4. Challenges and Risks of Currency Convertibility

While currency convertibility brings several advantages, it also presents significant challenges and risks, especially for developing economies.

a. Exchange Rate Volatility

Full convertibility can expose a nation’s currency to global market fluctuations. Speculative attacks and sudden changes in capital flows can destabilize the exchange rate, leading to inflationary pressures or currency depreciation.

b. Capital Flight

When investors lose confidence in a country’s economy, unrestricted capital convertibility can lead to massive capital outflows. This can drain foreign exchange reserves and weaken the domestic currency.

c. Loss of Monetary Control

With full capital account convertibility, central banks may find it difficult to manage monetary policy effectively, as large inflows and outflows can disrupt domestic liquidity and interest rates.

d. External Shocks

Global crises, such as the 2008 financial meltdown, highlight how interconnected financial markets can transmit risks rapidly. Countries with fully convertible currencies may face contagion effects more severely.

e. Inflation and Economic Instability

Sudden currency depreciation due to speculative pressures can raise import costs, leading to inflation and economic instability, particularly in countries dependent on imports for essential goods.

5. Case Studies: Global Experiences with Currency Convertibility

a. India

India has achieved current account convertibility since 1994 but still maintains partial capital account convertibility. The Reserve Bank of India (RBI) exercises control over capital flows to prevent volatility and speculative attacks. The cautious approach helped India withstand crises such as the Asian Financial Crisis (1997) and the Global Financial Crisis (2008).

b. China

China’s yuan (CNY) has been gradually moving toward greater convertibility. While trade-related transactions are largely convertible, capital account restrictions remain. China maintains tight control over capital flows to manage its exchange rate and protect economic stability.

c. Argentina

Argentina’s experience serves as a cautionary tale. In the 1990s, it adopted full convertibility by pegging its currency to the US dollar. While initially stabilizing inflation, it later led to economic collapse due to inflexible policies, capital flight, and loss of competitiveness.

d. Developed Economies (U.S., U.K., Eurozone)

Fully convertible currencies like the US Dollar, Euro, and British Pound dominate global trade and finance. Their stable economies, robust institutions, and deep financial markets enable them to sustain full convertibility with minimal disruption.

6. The Role of International Institutions

International organizations like the International Monetary Fund (IMF) and the World Bank play crucial roles in guiding countries toward managed currency convertibility.

The IMF’s Article VIII encourages member nations to remove restrictions on current account transactions but advises caution regarding capital account liberalization. It promotes gradual, sequenced reforms to avoid destabilizing the economy.

7. Factors Influencing a Country’s Currency Convertibility Decision

A nation’s decision to move toward full convertibility depends on several economic and political factors:

Macroeconomic Stability:

Low inflation, sustainable fiscal deficits, and stable growth are prerequisites for safe convertibility.

Foreign Exchange Reserves:

Adequate reserves ensure that the country can handle fluctuations in capital flows.

Financial Market Depth:

Developed financial markets can absorb capital movements efficiently without destabilizing the economy.

Exchange Rate Regime:

Flexible exchange rate systems are generally better suited for managing convertibility risks.

Institutional Strength and Governance:

Transparent regulatory systems and strong institutions reduce corruption and speculative behavior.

8. The Debate: Full vs. Partial Convertibility

Economists often debate whether developing nations should pursue full convertibility.

Proponents argue that it boosts foreign investment, promotes efficiency, and integrates the economy globally.

Critics warn that premature convertibility can expose the economy to crises, as seen in Latin America and Southeast Asia during the late 20th century.

The consensus among policymakers today is that gradual liberalization, backed by strong macroeconomic fundamentals, is the safest path.

9. The Future of Currency Convertibility in the Global Market

As the world moves toward digital currencies, blockchain, and fintech innovations, the landscape of currency convertibility is rapidly evolving. Central Bank Digital Currencies (CBDCs), for instance, could simplify cross-border transactions and make convertibility more efficient and transparent.

Moreover, the rise of the Chinese yuan and the decline of dollar dominance could reshape how currencies are exchanged globally. Emerging markets are also exploring regional payment systems and currency swap agreements to reduce dependency on traditional reserve currencies.

However, the fundamental challenge remains the same: balancing openness with stability. Policymakers must ensure that liberalization does not come at the cost of economic security.

10. Conclusion

Currency convertibility is a cornerstone of international economic integration, enabling trade, investment, and global cooperation. Yet, it remains a double-edged sword. While full convertibility symbolizes economic maturity and confidence, it also requires strong institutions, sound fiscal management, and robust financial systems.

For developing economies, the path toward full convertibility must be gradual, strategic, and supported by macroeconomic stability. India, China, and several other emerging markets demonstrate that measured liberalization, rather than abrupt openness, provides the best results.

In the evolving global financial landscape—marked by digital transformation, shifting geopolitical alliances, and economic uncertainty—understanding and managing the issues surrounding currency convertibility will continue to be a defining factor in shaping the world’s economic future.

U.S. Federal Reserve Policy and Interest RatesThe Backbone of Global Economic Stability.

Introduction

The United States Federal Reserve (commonly known as the Fed) stands as one of the most influential institutions in the global financial system. Its policies, particularly regarding interest rates, have far-reaching consequences — not only for the U.S. economy but also for financial markets, currencies, trade flows, and economic stability across the world. The Fed’s ability to adjust interest rates and implement monetary policies allows it to control inflation, influence employment levels, and stabilize economic growth.

In this essay, we will explore in detail the evolution, mechanisms, tools, and impacts of the Federal Reserve’s policy decisions, with a special focus on interest rates — their role, rationale, and implications for both domestic and international economies.

1. The Role and Structure of the U.S. Federal Reserve

The Federal Reserve System was established in 1913 through the Federal Reserve Act, in response to recurring financial panics and instability in the U.S. banking system. Its primary mission is to promote a stable monetary and financial environment.

The Fed operates through three key entities:

The Board of Governors – Located in Washington, D.C., consisting of seven members appointed by the President and confirmed by the Senate.

Twelve Regional Federal Reserve Banks – These regional banks represent different districts and carry out the Fed’s policies locally.

The Federal Open Market Committee (FOMC) – Comprising the Board of Governors and five Reserve Bank presidents, this committee is the primary decision-making body for setting interest rates and implementing monetary policy.

The Fed’s dual mandate is to achieve:

Maximum employment, and

Stable prices (low and predictable inflation).

In addition, the Fed seeks to moderate long-term interest rates and maintain the stability of the financial system.

2. The Tools of Federal Reserve Monetary Policy

To achieve its goals, the Federal Reserve uses several key tools:

a. Open Market Operations (OMO)

This is the primary tool for controlling short-term interest rates. The Fed buys or sells government securities (like U.S. Treasury bonds) in the open market.

Buying securities increases money supply, lowers interest rates, and stimulates economic activity.

Selling securities decreases money supply, raises interest rates, and curbs inflationary pressure.

b. The Discount Rate

This is the interest rate the Fed charges commercial banks for short-term loans through its discount window. Lowering this rate encourages banks to borrow more and lend to businesses and consumers, while increasing it discourages lending and cools the economy.

c. Reserve Requirements

This refers to the percentage of deposits that banks must hold as reserves. Lowering reserve requirements increases available funds for lending, boosting liquidity and credit growth. Raising them does the opposite, restricting credit.

d. Interest on Reserve Balances (IORB)

The Fed pays interest on reserves that banks hold at the central bank. Adjusting this rate influences how much banks lend versus how much they keep in reserves, indirectly impacting money supply.

e. Quantitative Easing (QE) and Tightening (QT)

In extraordinary circumstances, such as the 2008 financial crisis or the 2020 pandemic, the Fed uses QE to purchase long-term securities, injecting liquidity into the economy. Conversely, Quantitative Tightening (QT) involves selling assets or allowing them to mature to reduce liquidity and combat inflation.

3. Interest Rate Policy: The Core of Monetary Control

Interest rates lie at the heart of the Federal Reserve’s monetary policy. The Federal Funds Rate — the rate at which banks lend reserves to each other overnight — is the most critical benchmark.

When the Fed changes the target range for this rate, it indirectly affects:

Consumer borrowing costs (credit cards, mortgages, auto loans),

Business investment decisions,

Government borrowing costs, and

The valuation of financial assets globally.

a. When the Fed Raises Interest Rates

Inflation Control: Higher rates make borrowing more expensive, slowing spending and investment, thereby cooling inflation.

Currency Appreciation: The U.S. dollar strengthens as higher rates attract foreign investors seeking better returns.

Stock Market Impact: Equity prices often fall due to higher discount rates and reduced profit expectations.

Global Ripples: Emerging markets may face capital outflows as investors shift to U.S. assets.

b. When the Fed Lowers Interest Rates

Stimulating Growth: Cheaper credit encourages consumption, business expansion, and investment.

Weakening of Dollar: A lower yield reduces demand for the U.S. dollar, making exports more competitive.

Boost to Financial Markets: Lower discount rates increase asset valuations, benefiting equity and bond markets.

Support During Crises: Rate cuts are often used during recessions to stimulate economic recovery.

4. Historical Perspective: Major Fed Rate Cycles

a. The Volcker Era (Late 1970s–1980s)

Inflation had surged due to oil shocks and loose monetary policy. Chairman Paul Volcker implemented drastic rate hikes, pushing the federal funds rate above 20% in 1981. This aggressive stance broke the back of inflation but triggered a short-term recession.

b. The Greenspan Era (1987–2006)