Those must be one of the best times to buy Cardano tokens [ADA]It very rarely happens that a coin similar to both BTC (UTXO model/limited supply) and ETH (programmable/smart contracts) has its bearish low lower than the last cycle's highest top.

Tech stocks are somehow related to Crypto tech tokens, Therefore BTC likes to correlate to other Alts, but for the longer-term BTC on itself is closer to Gold from the Store of value standpoint and medium of exchange (the lightning network has been developing rapidly recently).

The bottom line is sometimes BTC and crypto will correlate to gold and sometimes it will correlate to stocks, it's not one or the other only. The statistics are very clear that crypto is the most uncorrelated asset.

Keep in mind the global situation with Russia and Ukraine is somehow dragging the US stock market that was already long overdue to pop bubble sooner than later.

The situation with Canadian truckers only confirmed that storing BTC and any crypto on custodian exchange is a bad idea and breaks the purpose of decentralization, do keep your crypto off those central points of failure, and remember, those news are not negative for BTC and other cryptos, they are positive. Truly decentralized ledger blockchain technology cannot be stopped, govs can only block fiat on/off ramps, and even there people are getting smarter and more creative.

For the longer timeframes in my opinion any buy below 0.95 cents for ADA is a good buy, make sure not to wait too long, this thought has 5-year time horizon. Do not trade daily, it's a waste of time and money.

Value

Full Reset before Full SendWhy March 2025 Could See New Highs

What's Happening Right Now?

Everyone is freaking out right now, but this is actually creating one of the best buying opportunities we've seen. Bitcoin is trading around $95,600 after dropping about 24% from its peak of $126,000 in October.

The Fear & Greed Index is at 10 (Extreme Fear) – and you know what they say? Be greedy when others are fearful. But, also, be patient and set limits.

The thing is, most people don't understand the economics behind Bitcoin or how liquidity actually works in crypto markets. We're playing a completely different game than stocks here.

The Real Cost to Mine Bitcoin (And Why It Matters)

Here's where it gets interesting. The big mining operations are producing Bitcoin for around $26,000-$28,000 per coin, while less efficient miners saw costs spike to $114,842 in October 2025... That's a massive range, and it tells you everything about where the floor is.

After the April 2024 halving, it now takes 854,400 kilowatt-hours to mine just one Bitcoin – that's about 81 years of electricity for an average home, just for one coin. That's a fun fact.

No smart miner is going to sell at a loss when they're paying that much for electricity and equipment (GPUs, etc). They'll just hold and wait. This creates natural supply constraints.

The Liquidity Trap

Right now, the market is in what I call a liquidity trap. As Bitcoin crashed from $126K down to where we are now, all the leveraged traders got wiped out. We saw $870 million in Bitcoin ETF outflows in a single day – that's both panic selling and intelligent, planned shorting, not fundamental weakness.

Here's what most people are missing: if Bitcoin drops to around $75K, it's going to unlock massive amounts of liquidity – I'm talking hundreds of millions, possibly billions of dollars that's currently locked up in long positions (Futures).

When those long get liquidated, the shorts will likely reverse their positions, that money floods back into the market and creates a supply shock. Basic economics: limited supply + sudden demand increase = price explosion.

Price Targets & When to Buy

I think we'll see $89K very soon – possibly this week between Monday and Wednesday (November 17-19, 2025). But here's my recommended strategy instead of trying to catch the exact bottom:

First Buy: $89K

Put in about 30% of what you're planning to invest. This is still a good entry even though it's not the absolute bottom.

Second Buy: $80K

Another 35% here. This is where things get really interesting from a risk/reward perspective.

Third Buy: $75K

The final 35%. This is the sweet spot where all that trapped liquidity gets released. Remember, demand increases as the price drops, and miners won't sell below cost. That's your supply shock waiting to happen.

What About MicroStrategy?

MSTR has crashed about 40% and is now trading at only 1.06 times its Bitcoin holdings, down from 2.7 times. The stock is around $200-$237 now, way down from its November 2024 high of $543.

My prediction: MSTR will probably hit the $140-$150 range, maybe even drop to $100-$120 (which is where it found strong support from March to September 2024). If we do see those lower prices, I'm going all-in on

MSTX

shares, not

MSTR

– the 2x leverage structure is better.

The Macro Picture

Fed rate cut expectations dropped from 90% to about 40%, which is why everything's selling off. But this is temporary sentiment, not permanent damage. The infrastructure is still being built, institutions are still coming in, and the fundamentals haven't changed.

Bottom Line

Be patient. Wait for the dips. Bitcoin will likely hit $89K this week, and from there we could see further drops to $80K and $75K. Each level is a buying opportunity. By March 2025, I expect we'll be making new all-time highs.

The key is understanding that crypto operates on different rules than stocks. Liquidity and supply dynamics matter more than anything else right now.

Good luck,

Terrapins

Even The Most Accomplished Make Mistakes $Goog [Berkshire]Berkshire Hathaway made an entrance into the Mag 7 (Excluding Apple) with its purchase of Alphabet / Google I believe that this was a mistake solely based on the fact that the majority of the tech industry is extremely overvalued. While Googles Valuation at least in my opinion is justified considering how strong Its business model is with its High Margin Reoccurring Subscription models (Google Cloud),(YouTube Premium),(Google Workshop),(Google Play) to name a few and how Dominate it is in Ads with YouTube / Chrome. It also Dominates Web Search let alone the majority of people saying they will "Google something" it sounds stupid but its a good mental metric on how people think of search. Google has built Search / web ecosystem to complement each other and force you to use there services in one way or another you are using there web ecosystem everyday from Google maps, to Google Docs or Gmail, they made you dependent on there services, Especially the younger generation (GenZ) is growing very dependent on Google Maps which may be free but shows you the grip they have on peoples web use. The Primary issue I have with Berkshire Hathaway entering at these prices is generally the markets are indiscriminate if the mag 7 or tech industry has a red day no matter how strong Google may be that will bring them down too.

-----------------------

My Personal Thesis on Google:

I am very bullish on several areas of Alphabet Including but not limited to Google Cloud, YouTube, Its subscription Services, Its high Margin software business model. Most Importantly to me is There Robotics Section Deepmind and Gemini Robotics. Robotics is underappreciated and my personal belief is that it is the Next AI like boom but we are very early to this. Robotics has use cases in every industry from Solving lack of labor issues and an aging workforce / population especially in western countries Robots can easily pick up this slack and they will greatly benefit from Artificial intelligence Google / Alphabet has the money and cashflow to heavily invest in this area maybe not creating the physical humanoid robots but they can definitely excel in the software section of it. Segments like Waymo are also interesting and bullish. Google is also massively profitable has very little debt, and an extremely solid balance sheet.

-----------------------

Risks:

I Believe the biggest Risk for Alphabet once again is that The American Tech Sector is extremely Overvalued, I Also See moderate amount of risk being that Google is such a monopoly that leaves it open for Antitrust Suits.

-----------------------

Business Model:

Google Is Vertically Integrated its Business was closely tied to the AI Boom being one of the Big 3 with its AI spending. People Disregard its extremely impressive moat it possesses having one of the strongest moats in tech let alone in the history of business.

-----------------------

Fundamentals:

Cash: US$98.50b

Debt: US$26.60b

Equity: US$386.87b

Total Liabilities: US$149.60b

Total assets: US$536.47b

Net Margins: 32.23%

-----------------------

Metrics:

Return On Equity: 32.1%

Return On Assets: 22.5%

Return On Capital Employed: 28.8%

-----------------------

Valuation:

Price to Sales: 8.9x

Price To Earnings: 27.7x

Price To Book: 8.9x

-----------------------

Disclaimer: I am not Initiating buy, Sell or Hold Opinions. I Only make these posts for Conversation. I am not a financial Expert or an Analyst.

Fear & Greed Index — Rebuilt as a Macro Oscillator for CryptoThe Fear & Greed Index is everywhere — a popular way to gauge market sentiment.

But it's usually just a mix of volatility, momentum, and social buzz...

📉 Not exactly macro.

This script is a technical reinterpretation of the Fear & Greed concept — but grounded in real, measurable economic behavior .

🧠 The Core Idea

This indicator is powered by the Copper/Gold ratio , a time-tested signal used by economists and institutional traders to track macroeconomic cycles:

- 🟢 When Copper outperforms → the economy is likely expanding → risk-on → Greed

- 🔴 When Gold outperforms → the economy may be contracting → risk-off → Fear

Copper represents industrial growth , while Gold signals defensive capital flows .

We track this ratio over time using a Z-Score oscillator to identify when sentiment is statistically stretched in either direction — highlighting moments of macro-level greed or fear.

📊 Why It Matters for Crypto

Crypto doesn’t live in a vacuum.

It's highly sensitive to the broader risk environment.

This oscillator gives you a macro lens to help:

- Anticipate bullish or bearish shifts in crypto markets

- Avoid common emotional traps at sentiment extremes

- Build entries or exits around macro confluence zones

It doesn’t tell you when to buy or sell — it tells you when the market context is shifting .

🔧 How to Use It

- Watch for the Z-Score entering > +2 (Greed) or < -2 (Fear)

- Use it to confirm broader risk-on/off behavior

- Combine with BTC or ETH price for potential lead/lag relationships

- Customize the tickers to test other macro pairs (e.g. SPX/VIX, BTC/DXY)

📈 Built with Pine Script v6

🔍 Default Tickers: CAPITALCOM:COPPER vs TVC:GOLD

📦 Fully customizable inputs, clean visual design, alert-ready

💡 Use this to trade with context — not emotion.

If you found this useful, give it a like and drop your feedback or improvements below 👇

Privacy is Pricy Again — How Zcash Got Back in the GameA significant shift is recently observed in the cryptocurrency space, indicating a resurgence of interest in privacy. The sharp rise of Zcash (ZEC) — over 46% in the week following Galaxy Research's analysis — is a clear example of this trend, reflecting the market's demand for untraceable funds.

Zcash, after years on the sidelines, has returned to the forefront, confirming that the fundamental cypherpunk ideals of privacy hold high value in the modern financial system.

1. Technological Breakthroughs and Zcash’s Fundamental Growth

The Zcash rally is driven not only by speculation but also by major improvements that have made privacy both more accessible and more effective:

Removing Barriers (Zashi & NEAR Intents): The use of zk-SNARKs (zero-knowledge proofs) has become more user-friendly. Enhanced user experience (UX) in new wallets (like Zashi) and integration with cross-chain mechanisms like NEAR Intents have removed the technical friction associated with "shielding" transactions.

Strengthening Anonymity: The most crucial network metric for Zcash is the increase of shielded coins in the Orchard pool to over 30% of the total supply. The more coins are "hidden," the larger the anonymity set becomes, which mathematically increases the difficulty of tracing transactions.

Technological Edge: Zcash, unlike some competitors, offers quantum-resistant cryptography and a stronger privacy mechanism via zk-SNARKs, which allows transaction validation without revealing the amount, sender, or receiver.

2. Zcash as a Counter-Trend to Transparency

The sharp price increase of ZEC after years of stagnation reflects a broader market narrative:

Reaction to Institutionalization: Against the backdrop of Bitcoin's growing transparency and institutionalization (ETFs, centralized custodians), Zcash is positioning itself as “encrypted Bitcoin”—an asset that refocuses attention on the decentralized and private nature of crypto assets.

Regulatory Balance: Zcash utilizes optional privacy, which, according to analysts, may provide the project with greater regulatory resilience compared to coins where privacy is mandatory by default.

Repricing Privacy: The market has demonstrated that the demand for confidentiality has not disappeared. The Zcash rally has forced investors to re-evaluate all privacy-focused projects, proving that, amid increasing online surveillance, the ability to transact privately has once again become a highly valuable feature.

Summary: Zcash is back in the game, bolstered by strong technological improvements that have made its privacy accessible and effective. The sustained nature of this growth will depend on whether the project can convert this speculative momentum into stable growth in user and network activity.

GPUS: Range Bound & Undervalued!AMEX:GPUS is quietly stacking value while trading in a range. At $0.35–$0.37, it's 61% below the estimated NAV of $1.02/share backed by $122M in cash + BTC vs. just $118M market cap (Nov 6 update).

Do your own research and trade at your own risk.

ASTS 4H: space internet or orbital dream?AST SpaceMobile (ASTS) is consolidating above the $61–69 zone, right near the 0.618 Fibonacci level of its last major rally. On the 4H chart, momentum shows early reversal signs: falling volume on pullbacks, stochastic turning up, and buyers defending local lows. The bullish setup holds as long as price stays above $61, with upside targets at $100 and $135 where the extension projection aligns.

Fundamentally , as of November 2025, ASTS stands out as one of the most promising yet capital-intensive players in the satellite telecom industry. The company completed deployment of its BlueWalker test constellation and is preparing for commercial rollout of direct-to-cell satellite connectivity. Successful phone-to-satellite calls using standard smartphones - validated with AT&T and Vodafone - mark a true technological milestone, positioning ASTS as a potential first-mover in global space-based mobile internet.

Revenue for the first nine months of 2025 reached roughly $55M, almost double last year’s level, but operating losses still exceed $300M due to high manufacturing and launch costs. The company holds about $180M in cash versus ~$260M in debt, continuing to rely on strategic partnerships and funding programs to maintain liquidity. The key upcoming catalyst is the commercial network activation in 2026 in cooperation with AT&T, Vodafone, and Rakuten, which could dramatically change valuation if successful.

With investor attention shifting back to space communications, competition with Starlink and Lynk Global is heating up, but ASTS’s advantage lies in using standard smartphones without extra hardware. Risks remain - high capital needs, launch delays, and dependency on partner timelines - yet the reward potential is extraordinary if execution holds.

Tactically, staying above $61 keeps the bullish structure alive with $100 and $135 as primary targets. A breakdown below $60 would negate the setup.

They’ve already connected phones to space - now let’s see if they can connect revenue to profit.

NOVAGRATZLOADED shares at $29.45 Friday. This is MSTR on steroids with actual revenue + AI data centers.

Just printed their best quarter ever ($505M net income, ~$29B rev) thanks to a $9B BTC whale trade 80k+ BTC sold OTC with minimal slippage + exploding trading volumes. But the real rocket fuel is HELIOS AI/HPC pivot: 800MW live, 2.7GW pipeline, NASDAQ:CRWV locked in for $435M+ annual EBITDA potential. Morgan Stanley calls it $30B terminal value. $1.15B convertible notes at 0.50%? Dirt-cheap capital to fund growth — not dilution yet. Catalysts: BTC >$120K (Galaxy amplifies 2-3x)

Helios revenue ramp H1 2026 On track for initial energization/power-up in December 2025

Technicals: Broke out of multi-month base

RSI cooling after dip (oversold bounce incoming)

Volume shelf at $29 = strong support $25 floor

Golden cross forming on weekly

This dip was the last shakeout post-notes FUD.

Add on dips around $30

Trail stops or take partials above $45

Full send to $60+ this year if BTC rips

Helios power-up = moonshot. Estimates backward-looking; if Helios hits + crypto cooperates, Q4 crushes again (revenue normalizes but margins fatten). $60+ YE

Zulu PrincipleJim Slater beat the market for decades by systematizing quality + reasonable price + momentum—first via a 1960s “earning situations” turnaround playbook, then (1992+) via the Zulu Principle: small/mid caps with fast EPS growth, efficient capital use, cheap vs growth (low PEG), and RS strength, managed by strict quarterly rebalances.

The two playbooks

1) “Capitalist” (1960s turnaround)

Yield ≥ 4%, EPS up in ≥4 of 5 years, EPS ≥ 2× in 4 years

Optimistic chairman’s statement, sound liquidity, no exceptional vulnerabilities

Reasonable asset value, not family-controlled, voting shares

Spirit: early GARP before it had a name—cash-generative, improving earners with robust balance sheets.

2) Zulu Principle (1990s, refined & timeless)

PEG < 0.75 (value vs growth in one metric)

P/E < 20

EPS growth > 15%

12-mo Relative Strength > 0% (price momentum)

ROCE > 12% (quality/efficiency)

Market cap £20M–£1B (small–mid where “elephants don’t gallop”)

Quarterly full rebalance: buy all qualifiers; sell anything that drops off; no in-between adds.

Why it still works

Aligns with the three empirically robust factors: Quality, Value (vs growth), Momentum.

Captures post-earnings-announcement drift by favoring positive EPS surprises and upgrades.

Rules ≫ opinions: removes emotion, enforces discipline via scheduled rebalances.

When few names qualify (tight markets)

Relax one notch (e.g., PEG < 1.0, P/E < 25, ROCE > 10%).

Widen geography (apply the same screen across EU/US/ROW).

Layer news filters (earnings beats, trading updates) on top of the screen.

Ready-to-run screen: www.tradingview.com

Universe: your domestic market + optional global small/mid

PEG (1y forward EPS growth) < 0.75

P/E (TTM or forward) < 20

EPS growth (TTM or forward) > 15%

Relative Strength (12m vs market) > 0%

ROCE > 12%

Market Cap , 1.1x USD

Liquidity guardrails: £5k ~ £20k Daily Volume

Sanity Check: Golden Cross, Price above 50/200 DMA

Portfolio construction & rules

Quarterly rebalance (strict): equal-weight all qualifiers; sell anything that no longer qualifies.

Max names: 20–40 (equal weight); if >40, rank by lowest PEG → highest RS → highest ROCE.

Risk: position size so any single name ≤ 5% weight; optional 15–25% stop from entry if you want overlays.

Costs/slippage: use liquid names (ADV filter) and quarterly cadence to keep friction low.

Upgrades you can test

Replace RS>0% with 6-Month RS > 5% or 12-Month RS > 10%.

Add Net debt/EBITDA < 10× (quality balance sheet).

Require positive estimate revisions in the last 3 months.

Momentum overlay: require price above 50/200-DMA to avoid value traps.

Value to Price Contraction PatternVPC Overview

What to Watch During Corrections

Stay engaged. Corrections are when future leaders reveal themselves.

Breadth divergence = danger. If indexes rise while the percentage of stocks above the 200-DMA is less than 50% (especially in the 30s), expect a pullback; rallies are narrow and fragile.

Look beyond cap-weighted indexes. Check equal-weight S&P, S&P 400 (midcaps), and Russell 2000; if they lag, leadership is thin.

Distribution vs. accumulation. Clusters of distribution days with few/brief accumulation days = risk-off regime.

How Leaders Reveal Themselves (3 Phases)

Predictive (during the correction):

Stocks hold up the best, often within ~25% of 52-week highs while the market is weak.

The RS line makes new highs even if the price is flat/down. Keep them on the A-list.

Right off the lows (post-FTD):

Explosive moves straight from lows, first into new high ground.

These often become the cycle’s monsters; wait for the first tight add-on/base if the initial thrust is extended.

Confirming (after the turn):

Breadth broadens; more proper bases are complete; opportunities are more obvious but still fruitful.

Entry Playbook

Require a Confirmed Uptrend: A follow-through day (FTD) + real setups. FTD alone is not a buy signal.

Focus on VCP bases (Volatility Contraction Pattern): successively tighter swings, drier volume, and right-side strength; buy as it clears the pivot with power.

RS Line New Highs into/at Breakout = Green Light.

Recent IPOs: prime “magnitude plays”; catch early primary bases coming out of corrections.

Progressive Exposure (when trades work)

Start with ~25% exposure (e.g., 4–5 x 5% “pilot” positions or one 20–25%).

If pilots gain traction, move quickly to ~50%, concentrating on the best names (add to winners).

If strength persists, scale to 75–100%.

Do not scale up if pilots aren’t working; reduce instead.

Selling & Timeframe

Define intent up front: trade (harvest faster, lower drawdown) vs campaign (accept drawdowns for bigger targets).

Sell into strength when the extension vs. key MAs is wide and the downside is greater than the upside.

For developing skill: take partials at 2–3× your initial risk (R) to “free-roll” the position; trail the rest.

Never raise cash just because the index is red; raise cash when your stocks show deterioration or hit stops.

Risk & Stops

Enter with a tight risk (Minervini style: often 3–5% below a well-defined pivot/low).

Position size so a stop hit costs ~1–2% of equity per idea.

Don’t average down. Cut quickly; the strategy is better than you—your job is to execute it.

Five Fast Filters for New Leaders

Shallow corrections from highs (ideally ≤25%) and quick recoveries.

Bases forming within long-term uptrends; VCP tightenings.

Fastest back to new highs after the market low; frequent up-days > down-days (“ants”: ≥12 up in 15).

The RS line is making new highs before/at breakout.

Recent IPOs with real growth.

Mindset

Commit to one sound strategy and master it; discipline is greater than prediction.

Trust the stocks, not the headlines. When the market confirms and the leaders set up, act.

Scanner:

www.tradingview.com

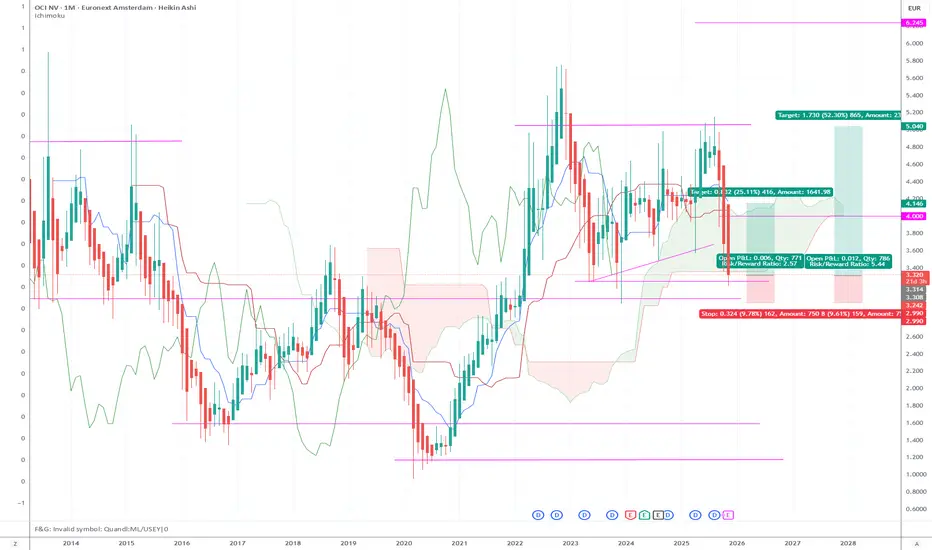

Risk / Reward optimal levelUpcoming merger with Orascom Construction PLC caused unnecessary fear and uncertanity. During such mergers in 75% of cases there is 20% premium paid. Intrinsic value is higher than current value on the market. Analyts recommended prices:

Average price target: Approximately €5.87 to €6.98.

High-end forecast: Around €8.86 to €10.50.

Low-end forecast: Around €4.30 to €4.36.

So calculate intrinsic value yourself for example if its €6 then add 20% premium and Value after merger will be €7,2. In other words you will get so much in value in Orascom Construction PLC stocks.

CAC 40: Poised for a Major UpsideThe French CAC 40 index — often overshadowed by Wall Street giants — may be standing at the edge of a powerful long-term rally. Beneath the surface, the forces driving this potential upside are not just economic cycles, but structural realities of modern finance.

Over the past decade, the global economy has entered an era of permanent liquidity. Central banks have normalized money printing as a policy tool — from the Federal Reserve to the European Central Bank. Every market slowdown or banking tremor now meets the same response: more stimulus, more debt, and more liquidity injections.

This infinite expansion of money supply inevitably pushes asset prices higher. Stocks, real estate, and even commodities have become the escape route from currency debasement. And the CAC 40, with its deep exposure to global blue-chip companies like LVMH, TotalEnergies, and Airbus, stands as one of Europe’s most direct beneficiaries.

Another quiet but powerful driver is demographics. Europe’s aging population means trillions of euros are tied up in pension funds — all of which must be parked in productive assets to sustain retirements. With bond yields historically low and inflation eroding purchasing power, the logical destination for this capital is equities.

Add it all up:

Endless government debt expansion

Central banks addicted to printing

Institutional demand from retirement funds

In such an environment, nominally, the CAC 40 almost has no choice but to rise. Whether measured in euros or in real purchasing power, the next leg up could surprise even the optimists.

SKYX: Breakout to $1.58 and Potential Triple on Small-Cap Surge

SKYX Platforms Corp. (NASDAQ: SKYX) is primed for a run to $1.58 and could triple to $3.30 by year-end, driven by small-cap strength, e-commerce demand, and strong fundamentals. Here’s why SKYX is a must-watch.

Technicals: Clear Shot to $1.58

Trading at $1.10 , SKYX is coiling for a breakout. Resistance at $1.25 (psychological) and $1.40 (prior high) should fall easily with rising volume and a bullish MACD crossover. $1.58 is achievable by August, with $3.30 (200%+ gain) in sight if momentum holds.

Fundamentals: Smart Home Leader

With 97 patents and 60+ e-commerce websites, SKYX’s plug-and-play smart home platform is gaining traction. Their $3B Miami smart city deal (500,000+ units) and Profab Electronics partnership signal scalability . E-commerce sales, projected to hit $8T globally by 2027 , fuel SKYX’s growth.

Market Tailwind

The Russell 2000, which SKYX joined in June 2025, is breaking out, up 10% YTD . TNA’s 30% spikes amplify this . With a $138.61M market cap and 38 institutions adding shares (e.g., Susquehanna, 478,024 shares) , SKYX is set to ride this wave.

Risks

SKYX isn’t cash flow positive until H2 2025, and Q1 revenue missed ($20.1M vs. $21.15M). Small-cap volatility is a factor, but 12.4% YOY growth and the Russell breakout mitigate risks.The Play

SKYX hits $1.58 soon, clearing $1.25 and $1.40, then triples to $3.30+ by December on e-commerce, smart city deals, and small-cap momentum. I’m buying—thoughts, board?

Summary: Targets: $1.58 near-term, $3.30+ year-end.

Resistances: $1.25, $1.40.

Catalysts: Russell 2000/TNA breakout, e-commerce, smart city deal.

Risks: Cash flow, revenue misses, volatility.

Disclaimer: Not financial advice. Do your own DD. Stocks are volatile.

~Sherwood Coast's Group

Webull Chart - Robinhood Competitor?Calling all matadors, we got a bull to corral.

I've charted some levels of interest for a speculative hold. Many view webull as a potential competitor for robinhood, although fundamentally, bull is in no-where near in the financial position that hood is in terms of free cash flow and expenses (or innovation as far as I've seen).

This could make a great swing trade on pure technicals. If the brokerage industry sees a period of exuberance(like we've seen in the quantum space), bull could catch a bid. This could also occur if we see a rotation out of hood.

I would love to pick up some shares or calls if the name completes a look below and fail of the anchored volume profile's value area low(around $12.28). or a LBAF of the box bottom @ $10.20.

So far webull has been consolidating. I believe a hold above the VPOC (volume point of control @ $15.43), a breakout of the lower boxes and reclaim of the larger upper box around $18.33-$18.87, could see a push to the mid 20s and 30s at least.

If we are following box rules for that potential trade, then I would not be surprised if bull goes to the box midpoint @ $48.97.

If this thing holds above the VPOC around $15.43 or does a LBAF of either $12.28 or $10.20 it's ripe for picking imo.

Now this is pure speculation, and my analysis could be a shack of shit, who knows, BUT if these set ups present themselves, I would like to roll the dice.

~ The Villain

Strategically Investing in Berkshire HathawayI'm going to write about what makes Berkshire a good company, and why I am buying it. Since it is such a huge company I might not be able to define every single detail but I will do my best to cover the most important aspects of the company for you. I hope you enjoy my idea, I am using my time to write this for your benefit and entertainment. If your deciding whether or not you want to buy Berkshire shares maybe this idea can help you to be more informed without having to do a ton of research.

One of the most appealing things to me right now about the shares, is that they are significantly undervalued. The best way to determine the intrinsic value for this company would be to use the discounted cash flow calculation. Projecting 5 years into the future, based on how much money the company will be expected to generate over this period of time, it is reasonable to assume the intrinsic value of the shares to be approximately $560. I think it could take some time to get there so I'm estimating about one or two years from now Berkshire will be worth $560 or more.

Looking at how the company actually uses its capital is important. When the market is at all time highs, investors typically rebalance their portfolios into undervalued, less risky, more stable companies. Berkshire fits the narrative here, and I'm going to explain why.

-Berkshire reallocates capital to its diverse portfolio of businesses, including railroad, energy, manufacturing, and service and retail companies. This can involve funding growth and "bolt-on" acquisitions for subsidiary companies.

-A significant portion of capital is used to purchase equity securities, such as stocks in companies like Apple, American Express, and Coca-Cola, either for a full stake or a "part interest".

-The company holds a large amount of cash and short-term investments to be prepared for market opportunities, which can include waiting for the right time to make large acquisitions or investments.

-Berkshire's core insurance operations generate "float"—money taken in as premiums before claims are paid—which is then invested in other businesses and securities.

-Berkshire uses debt very sparingly and prioritizes equity and its insurance float as its primary sources of capital.

-While individual businesses manage their daily operations, top management, led by Warren Buffett, makes the major capital allocation decisions to ensure capital is deployed where it can generate the highest returns. However as many of you know, Warren Buffett will step down as CEO and leave Greg Abel in charge, I don't think this will change much in the core operations of the business.

All of these factors contribute to this being a low risk, undervalued investment opportunity despite unfavorable market conditions with the US500 being at all time highs. I have rotated some capital in Berkshire class B shares as a way to reduce my risk but also stay exposed to the market. Berkshire is a great defensive stock that can be added to a diversified portfolio to grow and protect it.

Reasons why Coca-Cola is a Great CompanyI'm going to do a deep dive into why I think Coca Cola is a great stock to buy and hold, or trade whatever really you want to do with it is up to you. I hope you enjoy my idea, I always start off my ideas discussing the intrinsic value of the stock in question as that is a very fundamentally important aspect of buying stocks! I prefer the dividend discount model because it assumes a 28% upside! However I did account for the discounted cash flow as well which represents an upside of 12% which I think is more reasonable to expect this year. Overall I would like to think this company will be worth at least $77 sometime this year or next.

Coca Cola has made significant capital investments in their business over the last few years. These investments support growth by funding projects like expanding its bottling operations and placing more cold-drink equipment in outlets worldwide to drive sales. Historically, Coca-Cola has acquired other beverage companies to diversify its portfolio, although it also focuses on inorganic growth through other opportunities. In 2024, the company made progress toward refranchising some of its company-owned bottling operations to shift towards a more asset-light model.

The company has a great track record of returning capital to its shareholders. Coca-Cola has a long history of paying and growing dividends, having increased its dividend for 62 consecutive years. In 2024, it paid out $8.4 billion in dividends. The company repurchases its own shares to return capital to shareholders, with net share repurchases of $1.1 billion in 2024.

Coca-Cola manages a mix of debt and equity to finance its operations, with debt representing approximately 37.5% and cash and equivalents making up about 15.0% of its total capital in a recent analysis. This balanced approach is used to support growth while managing financial risk and optimizing overall performance. Coca-Cola focuses on producing and marketing high-margin beverage concentrates, while largely outsourcing the capital-intensive bottling and distribution processes to partners. This efficient model helps maintain high profit margins and financial resilience.

In essence, Coca-Cola acts as an anchor in a diversified portfolio, providing stability and downside protection when other growth-oriented investments may be struggling.

My Waste Management Investment StrategyAfter the last earnings report causing one of my favorite stocks to fall, it presents a valuable opportunity in my opinion. I am going to write what I like about the company and why I feel like it is a good idea to have Waste Management in your portfolio. I will write about all the reasons I think this is a good investment. Enjoy!

The very first thing I do when I am looking at a company for the first time, is calculate the intrinsic value of the stock to determine if it is undervalued or not. According to the numbers I ran through the equation Waste Management is undervalued by approximately 40% at this time of writing. I reasonably believe the stock could be worth as much as $280 in the next couple years.

Waste collection and disposal are critical for public health and safety, making them essential services that society cannot function without. Demand for these services is stable and generally not affected by economic downturns or price increases because customers, whether residential or commercial, will continue to generate waste that needs managing.

Establishing waste management infrastructure, such as landfills and processing facilities, requires significant capital investment, technical expertise, and complex permitting processes, making it difficult for new competitors to enter the market. The industry is often fragmented, allowing large publicly traded companies to acquire smaller, regional firms, leading to economies of scale and increased market share.

Companies are increasingly investing in recycling facilities, converting landfill gas into renewable natural gas (RNG), and offering other environmental services. These initiatives align with global sustainability goals and create new revenue streams and growth opportunities, attracting ESG-focused investors.

Many established companies in this sector have a history of consistent dividend payments and share repurchase programs, appealing to investors seeking reliable income and long-term value. The low volatility of the waste sector can help diversify an investor's portfolio and provide some protection during volatile market cycles.

The cost of waste removal is typically a very small fraction of a customer's total expenses (e.g., well below 1% for commercial customers). This low relative cost makes customers less likely to scrutinize price increases or switch providers over small differences, making it easier for companies to raise prices.

In summary, garbage companies have significant pricing power primarily due to high barriers to entry, the essential nature of their services, and the localized, regional-monopoly characteristics of the industry.

DIS Falling WedgeDis rallied from April '25 until July '25 and then consolidated around $120, forming a bullish falling wedge. The red line is the 200-day moving average which is acting as support at $110. It has been bounced off twice. The seasonals look bullish going into the last 2 months of the year when considering 2023 and 2024 price movement. The P/E ratio is 17.66 which is almost a 3rd of its 2-year moving average which is 47.43, indicating a low valuation with lots of room for upside. The aqua line is the 50-day sma which needs to be closed beyond along with the top side of the rising wedge before this thing can really take off. Fundamentals look bullish as well, with an uptrend in annual revenue growth and downtrend in debt/equity.

Purchasing Power vs Gold, Stocks, Real Estate, BTC (1971 = 100)Since the U.S. left the gold standard in 1971, the dollar has lost more than 85% of its purchasing power. This chart compares the dollar’s decline to major assets including gold, stocks, real estate, and Bitcoin, all normalized to 1971 = 100. It shows how value preservation and growth have shifted across different asset classes over time.

Source: FRED (CPIAUCSL, SP500, MSPUS) • OANDA (XAUUSD) • TradingView (INDEX:BTCUSD/BLX)

Visualization by 3xplain

All Priced In - Selling to CommenceFundamentals all baked in with price to sales ratio at previous 2021 post-covid highs will push to profit locking and selling pressure.

NASDAQ:GOOGL price target in the ~$230 range.

RSI weekly divergence and upper log line hit confluence with top fundamental ratios.

Fair Value Gaps: The Market Secret You Shouldn’t IgnoreEver scrolled through a chart and spotted a weird empty space in the candles — like the market just skipped a beat? That’s a Fair Value Gap (FVG). It’s one of those subtle price imbalances smart traders love to hunt for. Understanding how these gaps form and how price reacts around them can seriously level up your chart-reading game.

What Is a Fair Value Gap in Trading?

A Fair Value Gap happens when there’s a sudden surge in buying or selling pressure that causes price to move so fast, it doesn’t fully balance out between buyers and sellers. In simple terms, it’s an imbalance — a zone where the market skipped over potential orders.

When you hear traders talking about FVG in trading, they’re referring to those little pockets of unfilled liquidity left behind during strong moves.

So, what is FVG in trading, and why does it matter? Because price often comes back to those areas later to “rebalance” — filling the gap before continuing in the original direction. That’s the core logic behind Fair Value Gap trading.

Bullish and Bearish FVGs

There are two main types of Fair Value Gaps — bullish and bearish:

Bullish Fair Value Gap (bullish FVG): Forms during a strong upward move, when aggressive buyers push price higher, leaving a void below. Price might later dip back into that zone before continuing upward.

Bearish Fair Value Gap (bearish FVG): Forms in a sell-off, when sellers dominate and the market drops quickly, skipping over potential buy orders. Later, price often retraces upward to “fill” that gap.

Both can act as magnets for liquidity — areas where smart money likes to re-enter the market.

Fair Value Gap Example

Let’s say Bitcoin jumps from $110,000 to $120,000 in a single bullish candle, with almost no trading in between. That sudden move leaves a Fair Value Gap — the zone between the candle’s high and low where little to no trading took place.

If the market later pulls back to that range and finds support before bouncing, you’ve just witnessed a textbook Fair Value Gap example in action.

Using a Fair Value Gap Indicator

You can spot these zones manually by looking for three-candle structures — one candle that “leaves the gap” and two surrounding it that don’t overlap. But if you prefer automation, you can use a Fair Value Gap indicators:

Fair Value Gap Trading Strategies

Fair Value Gap trading isn’t about chasing price — it’s about waiting for the market to come back to you. Within Smart Money Concepts, traders often combine FVGs with CHoCH (Change of Character) to confirm a potential shift in structure before entering.

A common approach is to mark recent FVGs, identify the broader trend, and wait for price to revisit a gap in line with that trend.

In a bullish trend , traders look for bullish FVGs below current price as potential demand zones — ideally after a CHoCH confirms that buyers are stepping back in.

In a bearish trend , they watch for bearish FVGs above current price as potential supply zones, again validated by a CHoCH showing a shift in control.

Still, it’s important to remember — these setups are not guarantees. The market doesn’t owe you a fill. Use FVGs and CHoCH as part of the Smart Money framework, not as standalone signals. Always manage risk and make your own trading decisions based on your personal strategy and comfort level.

Final Thoughts

So, what is a Fair Value Gap really? It’s not magic — just the market showing where it moved too fast. Learning to read Fair Value Gaps gives you insight into liquidity, momentum, and potential reversals. Whether you use a Fair Value Gap indicator or mark them by hand, mastering FVG in trading can give you a serious edge in spotting high-probability zones.

Just keep in mind — no indicator or setup replaces good judgment.

Observe, adapt, and let the charts speak for themselves.

Writing about Canadian National RailwaySome one asked me to write why I like CNI, also I don't like the other idea I wrote about the company, I felt like I could do a lot better. I am in the mood to write tonight and feel like this is a great time for me to explain why I like CNI. First and foremost, I like undervalued companies on a technical and fundamental level CNI is significantly undervalued at the time of this writing. As you can see by the technical analysis we are sitting at an area of support characterized by the trendline, and to reinforce the technical analysis I have measured a move using the Fibonacci retracement tool.

Talking about the fundamentals, I have calculated both the discounted cash flow, and the dividend discount models of intrinsic value. According to my calculations the price of the stock right now at $93 is undervalued based on the future revenues the company will be expected to generate. The dividend discount model also suggests undervaluation based on the expected dividend payments over the next 5 years. I always calculate a minimum of 5 years into the future. According to my calculations it is reasonable to assume the intrinsic value for CNI to be somewhere near the $115 mark. This leaves me a substantial margin of safety to buy shares at these levels.

Some more reasons I like the company goes beyond the actual price of the stock. One reason I like the company is because it is a very capital intensive business model with a wide economic moat. The massive investment for building tracks, bridges and tunnels creates an almost impossible barrier for new competitors to overcome. These high costs mean there are very few major railroads, often leaving each with a monopoly or duopoly in certain regions, which gives them pricing power.

When I was building my portfolio at first, I didn't really care about the environmental impact companies had on our planet, but eventually as I learned more it started to become important to me to invest in companies I think were good for the planet. Railroads are significantly more fuel-efficient than trucking, especially when hauling heavy goods long distances. This efficiency leads to lower greenhouse gas emissions, which benefits society as a whole.

The company is the largest rail network in Canada and the only North American railway connecting the Atlantic, Pacific, and Gulf Coasts, giving it a dominant position on the continent. Finally, Canadian National has consistently increased its dividend for 20 consecutive years and currently yields nearly 2.7%. Its relatively low payout ratio of 48% suggests its track record of payout increases will likely continue. I think CNI is a great company and I have been using the stock as a defensive/safe haven type of position in my portfolio.