BTC Risk Metric DCA Adapter (3Commas Webhook Strategy)Risk Metric DCA Adapter (3Commas Webhook Strategy) - WORK IN PROGRESS

This Pine Script strategy, originally inspired by the Risk Metric Indicator, is fundamentally engineered as an Adapter to interface with external trading bots like 3Commas via Webhooks. It calculates a dynamic market risk score and translates that score into specific dollar-cost averaging (DCA) entry levels and tiered profit-taking exits.

Key Features & Logic

Risk Metric Calculation (Credit to The Trading Parrot):

The strategy incorporates a complex, multi-timeframe Risk Metric calculation based on daily and weekly moving averages (SMA) and standard deviation (StDev). This metric aims to quantify the current market overextension or compression relative to long-term historical data. The resulting score dictates the level of conviction for a new trade.

Tiered DCA Entry Sizing:

The strategy defines three distinct Buy Levels (L1, L2, L3) corresponding to increasingly favorable (lower) Risk Metric scores.

L1 (Base): Risk is moderate, initiating the minimum defined trade amount.

L2 (Scaled): Risk is low, initiating L1 amount + L2 amount.

L3 (Aggressive): Risk is very low, initiating L1 + L2 + L3 amounts.

Tiered Profit-Taking Exits:

The strategy implements a staggered, partial profit-taking approach based on the Risk Metric rising:

Sell L1 & L2: Closes a percentage of the current position when the Risk Metric reaches defined high thresholds, locking in partial profits.

Sell L3 (Full Exit): Closes the remaining position when the Risk Metric reaches the highest defined threshold.

The Adapter Function (Webhook Integration)

This script is unique because it uses the Pine Script strategy() function to trigger Order Fills, which are necessary to access powerful placeholders in the TradingView alert system.

Trigger Type: The alert must be set to trigger on Any order fill.

Dynamic Webhook Data: Instead of using fixed alert() commands, the strategy generates dynamic labels (e.g., BUY_ENTRY_L3_USD_1000 or SELL_L1_PCT_25) using the strategy.entry and strategy.close commands.

Data Transfer: The alert message then uses the placeholder {{strategy.order.comment}} to pass these dynamic labels to the 3Commas bot, allowing the bot to execute the precise action (e.g., start_deal_with_volume_in_quote_currency or close_deal_at_market_percentage).

Full Strategy Webhook payload

{

"secret": "YOUR_3COMMAS_SECRET_KEY",

"max_lag": "300",

"timestamp": "{{timenow}}",

"trigger_price": "{{close}}",

"tv_exchange": "{{exchange}}",

"tv_instrument": "{{ticker}}",

"action": "{{strategy.order.action}}",

"bot_uuid": "YOUR_BOT_UUID",

"strategy_info": {

"market_position": "{{strategy.market_position}}",

"market_position_size": "{{strategy.market_position_size}}",

"prev_market_position": "{{strategy.prev_market_position}}",

"prev_market_position_size": "{{strategy.prev_market_position_size}}"

},

"order": {

"amount": "{{strategy.order.contracts}}",

"currency_type": "base",

"comment": "{{strategy.order.comment}}"

}

}

Disclaimer: This script is an adapter tool and does not guarantee profit. Trading requires manual configuration of risk settings, bot parameters, and adherence to platform-specific setup instructions.

Crypto

EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

FluxVector Liquidity Universal Trendline FluxVector Liquidity Trendline FFTL

Summary in one paragraph

FFTL is a single adaptive trendline for stocks ETFs FX crypto and indices on one minute to daily. It fires only when price action pressure and volatility curvature align. It is original because it fuses a directional liquidity pulse from candle geometry and normalized volume with realized volatility curvature and an impact efficiency term to modulate a Kalman like state without ATR VWAP or moving averages. Add it to a clean chart and use the colored line plus alerts. Shapes can move while a bar is open and settle on close. For conservative alerts select on bar close.

Scope and intent

• Markets. Major FX pairs index futures large cap equities liquid crypto top ETFs

• Timeframes. One minute to daily

• Default demo used in the publication. SPY on 30min

• Purpose. Reduce false flips and chop by gating the line reaction to noise and by using a one bar projection

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. Directional Liquidity Pulse plus Volatility Curvature plus Impact Efficiency drives an adaptive gain for a one dimensional state

• Failure mode addressed. One or two shock candles that break ordinary trendlines and saw chop in flat regimes

• Testability. All windows and gains are inputs

• Portable yardstick. Returns use natural log units and range is bar high minus low

• Protected scripts. Not used. Method disclosed plainly here

Method overview in plain language

Base measures

• Return basis. Natural log of close over prior close. Average absolute return over a window is a unit of motion

Components

• Directional Liquidity Pulse DLP. Measures signed participation from body and wick imbalance scaled by normalized volume and variance stabilized

• Volatility Curvature. Second difference of realized volatility from returns highlights expansion or compression

• Impact Efficiency. Price change per unit range and volume boosts gain during efficient moves

• Energy score. Z scores of the above form a single energy that controls the state gain

• One bar projection. Current slope extended by one bar for anticipatory checks

Fusion rule

Weighted sum inside the energy score then logistic mapping to a gain between k min and k max. The state updates toward price plus a small flow push.

Signal rule

• Long suggestion and order when close is below trend and the one bar projection is above the trend

• Short suggestion and flip when close is above trend and the one bar projection is below the trend

• WAIT is implicit when neither condition holds

• In position states end on the opposite condition

What you will see on the chart

• Colored trendline teal for rising red for falling gray for flat

• Optional projection line one bar ahead

• Optional background can be enabled in code

• Alerts on price cross and on slope flips

Inputs with guidance

Setup

• Price source. Close by default

Logic

• Flow window. Typical range 20 to 80. Higher smooths the pulse and reduces flips

• Vol window. Typical range 30 to 120. Higher calms curvature

• Energy window. Typical range 20 to 80. Higher slows regime changes

• Min gain and Max gain. Raise max to react faster. Raise min to keep momentum in chop

UI

• Show 1 bar projection. Colors for up down flat

Properties visible in this publication

• Initial capital 25000

• Base currency USD

• Commission percent 0.03

• Slippage 5

• Default order size method percent of equity value 3%

• Pyramiding 0

• Process orders on close off

• Calc on every tick off

• Recalculate after order is filled off

Realism and responsible publication

• No performance claims

• Intrabar reminder. Shapes can move while a bar forms and settle on close

• Strategy uses standard candles only

Honest limitations and failure modes

• Sudden gaps and thin liquidity can still produce fast flips

• Very quiet regimes reduce contrast. Use larger windows and lower max gain

• Session time uses the exchange time of the chart if you enable any windows later

• Past results never guarantee future outcomes

Open source reuse and credits

• None

Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

Crypto Pro Strategy (Entry Model + Risk)Imma try to use this on a prop firm but if you want to use it itss free or im going to try to make it free

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.

• Efficiency basis. The ratio of net move to the sum of absolute step over the window gives a value between zero and one. High values mean trend quality. Low values mean chop.

• Intensity basis. The fraction of up moves over the window plugs into binary entropy. Intensity is one minus entropy, which maps to zero in uncertainty and one in very one sided moves.

Components

• Directional Intensity. Measures how one sided recent bars have been. Smoothed with RMA. More intensity increases the gain and makes the fast and slow tracks react sooner.

• Path Efficiency. Measures the straightness of the price path. A gamma input shapes the curve so you can make trend quality count more or less. Higher efficiency lifts the gain in clean trends.

• Volatility Squash. Normalizes the absolute step with Z score then pushes it through an arctangent squash. This caps the effect of spikes so they do not dominate the response.

• Normalizer. Three modes. Z score for familiar units, percent rank for a robust monotone map to a symmetric range, and MAD based Z for outlier resistance.

• Guide Line. EMA of the flux with a small lead term that counteracts lag without heavy overshoot.

Fusion rule

• Weighted sum of the three drivers with fixed weights visible in the code comments. Intensity has fifty percent weight. Efficiency thirty percent. Volatility twenty percent.

• The blend power input scales the driver mix. Zero means fixed spans. One means full driver control.

• Minimum and maximum gain clamps bound the adaptive gain. This protects stability in quiet or violent regimes.

Signal rule

• Long suggestion appears when flux and guide are both above zero. That sets polarity to plus one.

• Short suggestion appears when flux and guide are both below zero. That sets polarity to minus one.

• When polarity flips from plus to minus, the strategy closes any long and enters a short.

• When flux crosses above the guide, the strategy closes any short.

What you will see on the chart

• White polarity plot around the zero line

• A dotted reference line at zero named Zen

• Green background tint for positive polarity and red background tint for negative polarity

• Strategy long and short markers placed by the TradingView engine at entry and at close conditions

• No table in this version to keep the visual clean and portable

Inputs with guidance

Setup

• Price source. Default ohlc4. Stable for noisy symbols.

• Fast span. Typical range 6 to 24. Raising it slows the fast track and can reduce churn. Lowering it makes entries more reactive.

• Slow span. Typical range 20 to 60. Raising it lengthens the baseline horizon. Lowering it brings the slow track closer to price.

Logic

• Guide span. Typical range 4 to 12. A small guide smooths without eating turns.

• Blend power. Typical range 0.25 to 0.85. Raising it lets the drivers modulate gains more. Lowering it pushes behavior toward fixed EMA style smoothing.

• Vol window. Typical range 20 to 80. Larger values calm the volatility driver. Smaller values adapt faster in intraday work.

• Efficiency window. Typical range 10 to 60. Larger values focus on smoother trends. Smaller values react faster but accept more noise.

• Efficiency gamma. Typical range 0.8 to 2.0. Above one increases contrast between clean trends and chop. Below one flattens the curve.

• Min alpha multiplier. Typical range 0.30 to 0.80. Lower values increase smoothing when the mix is weak.

• Max alpha multiplier. Typical range 1.2 to 3.0. Higher values shorten smoothing when the mix is strong.

• Normalization window. Typical range 100 to 300. Larger values reduce drift in the baseline.

• Normalization mode. Z score, percent rank, or MAD Z. Use MAD Z for outlier heavy symbols.

• Clamp level. Typical range 2.0 to 4.0. Lower clamps reduce the influence of extreme runs.

Filters

• Efficiency filter is implicit in the gain map. Raising efficiency gamma and the efficiency window increases the preference for clean trends.

• Micro versus macro relation is handled by the fast and slow spans. Increase separation for swing, reduce for scalping.

• Location filter is not included in v1.0. If you need distance gates from a reference such as VWAP or a moving mean, add them before publication of a new version.

Alerts

• This version does not include alertcondition lines to keep the core minimal. If you prefer alerts, add names Long Polarity Up, Short Polarity Down, Exit Short on Flux Cross Up in a later version and select on bar close for conservative workflows.

Strategy has been currently adapted for the QQQ asset with 30/60min timeframe.

For other assets may require new optimization

Properties visible in this publication

• Initial capital 25000

• Base currency Default

• Default order size method percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Honest limitations and failure modes

• Past results do not guarantee future outcomes

• Economic releases, circuit breakers, and thin books can break the assumptions behind intensity and efficiency

• Gap heavy symbols may benefit from the MAD Z normalization

• Very quiet regimes can reduce signal contrast. Use longer windows or higher guide span to stabilize context

• Session time is the exchange time of the chart

• If both stop and target can be hit in one bar, tie handling would matter. This strategy has no fixed stops or targets. It uses polarity flips for exits. If you add stops later, declare the preference

Open source reuse and credits

• None beyond public domain building blocks and Pine built ins such as EMA, SMA, standard deviation, RMA, and percent rank

• Method and fusion are original in construction and disclosure

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Strategy add on block

Strategy notice

Orders are simulated by the TradingView engine on standard candles. No request.security() calls are used.

Entries and exits

• Entry logic. Enter long when both the normalized flux and its guide line are above zero. Enter short when both are below zero

• Exit logic. When polarity flips from plus to minus, close any long and open a short. When the flux crosses above the guide line, close any short

• Risk model. No initial stop or target in v1.0. The model is a regime flipper. You can add a stop or trail in later versions if needed

• Tie handling. Not applicable in this version because there are no fixed stops or targets

Position sizing

• Percent of equity in the Properties panel. Five percent is the default for examples. Risk per trade should not exceed five to ten percent of equity. One to two percent is a common choice

Properties used on the published chart

• Initial capital 25000

• Base currency Default

• Default order size percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Dataset and sample size

• Test window Jan 2, 2014 to Oct 16, 2025 on QQQ one hour

• Trade count in sample 324 on the example chart

Release notes template for future updates

Version 1.1.

• Add alertcondition lines for long, short, and exit short

• Add optional table with component readouts

• Add optional stop model with a distance unit expressed as ATR or a percent of price

Notes. Backward compatibility Yes. Inputs migrated Yes.

Mutanabby_AI | ATR+ | Trend-Following StrategyThis document presents the Mutanabby_AI | ATR+ Pine Script strategy, a systematic approach designed for trend identification and risk-managed position entry in financial markets. The strategy is engineered for long-only positions and integrates volatility-adjusted components to enhance signal robustness and trade management.

Strategic Design and Methodological Basis

The Mutanabby_AI | ATR+ strategy is constructed upon a foundation of established technical analysis principles, with a focus on objective signal generation and realistic trade execution.

Heikin Ashi for Trend Filtering: The core price data is processed via Heikin Ashi (HA) methodology to mitigate transient market noise and accentuate underlying trend direction. The script offers three distinct HA calculation modes, allowing for comparative analysis and validation:

Manual Calculation: Provides a transparent and deterministic computation of HA values.

ticker.heikinashi(): Utilizes TradingView's built-in function, employing confirmed historical bars to prevent repainting artifacts.

Regular Candles: Allows for direct comparison with standard OHLC price action.

This multi-methodological approach to trend smoothing is critical for robust signal generation.

Adaptive ATR Trailing Stop: A key component is the Average True Range (ATR)-based trailing stop. ATR serves as a dynamic measure of market volatility. The strategy incorporates user-defined parameters (

Key Value and ATR Period) to calibrate the sensitivity of this trailing stop, enabling adaptation to varying market volatility regimes. This mechanism is designed to provide a dynamic exit point, preserving capital and locking in gains as a trend progresses.

EMA Crossover for Signal Generation: Entry and exit signals are derived from the interaction between the Heikin Ashi derived price source and an Exponential Moving Average (EMA). A crossover event between these two components is utilized to objectively identify shifts in momentum, signaling potential long entry or exit points.

Rigorous Stop Loss Implementation: A critical feature for risk mitigation, the strategy includes an optional stop loss. This stop loss can be configured as a percentage or fixed point deviation from the entry price. Importantly, stop loss execution is based on real market prices, not the synthetic Heikin Ashi values. This design choice ensures that risk management is grounded in actual market liquidity and price levels, providing a more accurate representation of potential drawdowns during backtesting and live operation.

Backtesting Protocol: The strategy is configured for realistic backtesting, employing fill_orders_on_standard_ohlc=true to simulate order execution at standard OHLC prices. A configurable Date Filter is included to define specific historical periods for performance evaluation.

Data Visualization and Metrics: The script provides on-chart visual overlays for buy/sell signals, the ATR trailing stop, and the stop loss level. An integrated information table displays real-time strategy parameters, current position status, trend direction, and key price levels, facilitating immediate quantitative assessment.

Applicability

The Mutanabby_AI | ATR+ strategy is particularly suited for:

Cryptocurrency Markets: The inherent volatility of assets such as #Bitcoin and #Ethereum makes the ATR-based trailing stop a relevant tool for dynamic risk management.

Systematic Trend Following: Individuals employing systematic methodologies for trend capture will find the objective signal generation and rule-based execution aligned with their approach.

Pine Script Developers and Quants: The transparent code structure and emphasis on realistic backtesting provide a valuable framework for further analysis, modification, and integration into broader quantitative models.

Automated Trading Systems: The clear, deterministic entry and exit conditions facilitate integration into automated trading environments.

Implementation and Evaluation

To evaluate the Mutanabby_AI | ATR+ strategy, apply the script to your chosen chart on TradingView. Adjust the input parameters (Key Value, ATR Period, Heikin Ashi Method, Stop Loss Settings) to observe performance across various asset classes and timeframes. Comprehensive backtesting is recommended to assess the strategy's historical performance characteristics, including profitability, drawdown, and risk-adjusted returns.

I'd love to hear your thoughts, feedback, and any optimizations you discover! Drop a comment below, give it a like if you find it useful, and share your results.

Parabolic RSI Strategy [ChartPrime × PineIndicators]This strategy combines the strengths of the Relative Strength Index (RSI) with a Parabolic SAR logic applied directly to RSI values.

Full credit to ChartPrime for the original concept and indicator, licensed under the MPL 2.0.

It provides clear momentum-based trade signals using an innovative method that tracks RSI trend reversals via a customized Parabolic SAR, enhancing traditional oscillator strategies with dynamic trend confirmation.

How It Works

The system overlays a Parabolic SAR on the RSI, detecting trend shifts in RSI itself rather than on price, offering early reversal insight with visual and algorithmic clarity.

Core Components

1. RSI-Based Trend Detection

Calculates RSI using a customizable length (default: 14).

Uses upper and lower thresholds (default: 70/30) for overbought/oversold zones.

2. Parabolic SAR Applied to RSI

A custom Parabolic SAR function tracks momentum within the RSI, not price.

This allows the system to capture RSI trend reversals more responsively.

Configurable SAR parameters: Start, Increment, and Maximum acceleration.

3. Signal Generation

Long Entry: Triggered when the SAR flips below the RSI line.

Short Entry: Triggered when the SAR flips above the RSI line.

Optional RSI filter ensures that:

Long entries only occur above a minimum RSI (e.g. 50).

Short entries only occur below a maximum RSI.

Built-in logic prevents new positions from being opened against trend without prior exit.

Trade Modes & Controls

Choose from:

Long Only

Short Only

Long & Short

Optional setting to reverse positions on opposite signal (instead of waiting for a flat close).

Visual Features

1. RSI Plotting with Thresholds

RSI is displayed in a dedicated pane with overbought/oversold fill zones.

Custom horizontal lines mark threshold boundaries.

2. Parabolic SAR Overlay on RSI

SAR dots color-coded for trend direction.

Visible only when enabled by user input.

3. Entry & Exit Markers

Diamonds: Mark entry points (above for shorts, below for longs).

Crosses: Mark exit points.

Strategy Strengths

Provides early momentum reversal entries without relying on price candles.

Combines oscillator and trend logic without repainting.

Works well in both trending and mean-reverting markets.

Easy to configure with fine-tuned filter options.

Recommended Use Cases

Intraday or swing traders who want to catch RSI-based reversals early.

Traders seeking smoother signals than price-based Parabolic SAR entries.

Users of RSI looking to reduce false positives via trend tracking.

Customization Options

RSI Length and Thresholds.

SAR Start, Increment, and Maximum values.

Trade Direction Mode (Long, Short, Both).

Optional RSI filter and reverse-on-signal settings.

SAR dot color customization.

Conclusion

The Parabolic RSI Strategy is an innovative, non-repainting momentum strategy that enhances RSI-based systems with trend-confirming logic using Parabolic SAR. By applying SAR logic to RSI values, this strategy offers early, visualized, and filtered entries and exits that adapt to market dynamics.

Credit to ChartPrime for the original methodology, published under MPL-2.0.

Multi-Indicator Swing [TIAMATCRYPTO]v6# Strategy Description:

## Multi-Indicator Swing

This strategy is designed for swing trading across various markets by combining multiple technical indicators to identify high-probability trading opportunities. The system focuses on trend strength confirmation and volume analysis to generate precise entry and exit signals.

### Core Components:

- **Supertrend Indicator**: Acts as the primary trend direction filter with optimized settings (Factor: 3.0, ATR Period: 10) to balance responsiveness and reliability.

- **ADX (Average Directional Index)**: Confirms the strength of the prevailing trend, filtering out sideways or choppy market conditions where the strategy avoids taking positions.

- **Liquidity Delta**: A volume-based indicator that analyzes buying and selling pressure imbalances to validate trend direction and potential reversals.

- **PSAR (Optional)**: Can be enabled to add additional confirmation for trend changes, turned off by default to reduce signal filtering.

### Key Features:

- **Flexible Direction Trading**: Choose between long-only, short-only, or bidirectional trading to adapt to market conditions or account restrictions.

- **Conservative Risk Management**: Implements fixed percentage-based stop losses (default 2%) and take profits (default 4%) for a positive risk-reward ratio.

- **Realistic Backtesting Parameters**: Includes commission (0.1%) and slippage (2 points) to reflect real-world trading conditions.

- **Visual Signals**: Clear buy/sell arrows with customizable sizes for easy identification on the chart.

- **Information Panel**: Dynamic display showing active indicators and current risk settings.

### Best Used On:

Daily timeframes for cryptocurrencies, forex, or stock indices. The strategy performs optimally on assets with clear trending behavior and sufficient volatility.

### Default Settings:

Optimized for conservative position sizing (5% of equity per trade) with an initial capital of $10,000. The backtesting period (2021-2023) provides a statistically significant sample of varied market conditions.

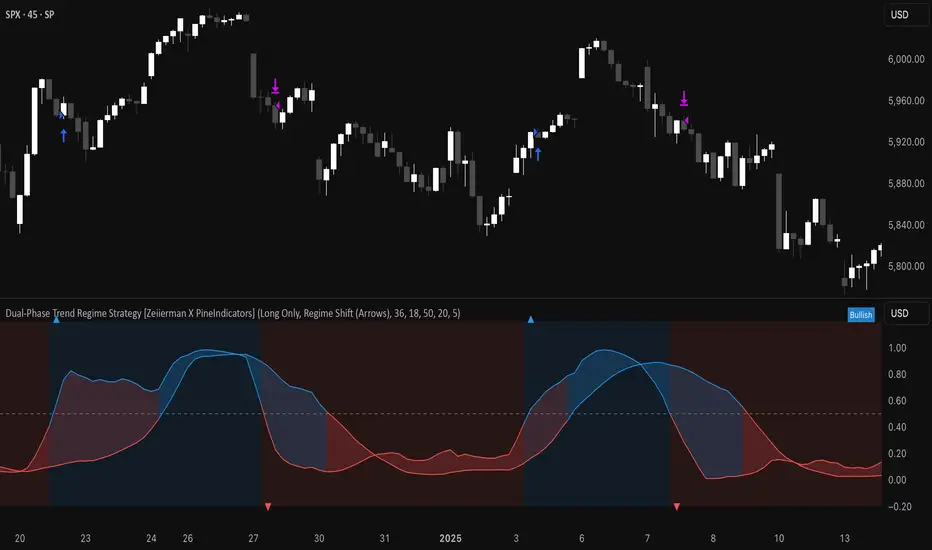

Dual-Phase Trend Regime Strategy [Zeiierman X PineIndicators]This strategy is based on the Dual-Phase Trend Regime Indicator by Zeiierman.

Full credit for the original concept and logic goes to Zeiierman.

This non-repainting strategy dynamically switches between fast and slow oscillators based on market volatility, providing adaptive entries and exits with high clarity and reliability.

Core Concepts

1. Adaptive Dual Oscillator Logic

The system uses two oscillators:

Fast Oscillator: Activated in high-volatility phases for quick reaction.

Slow Oscillator: Used during low-volatility phases to reduce noise.

The system automatically selects the appropriate oscillator depending on the market's volatility regime.

2. Volatility Regime Detection

Volatility is calculated using the standard deviation of returns. A median-split algorithm clusters volatility into:

Low Volatility Cluster

High Volatility Cluster

The current volatility is then compared to these clusters to determine whether the regime is low or high volatility.

3. Trend Regime Identification

Based on the active oscillator:

Bullish Trend: Oscillator > 0.5

Bearish Trend: Oscillator < 0.5

Neutral Trend: Oscillator = 0.5

The strategy reacts to changes in this trend regime.

4. Signal Source Options

You can choose between:

Regime Shift (Arrows): Trade based on oscillator value changes (from bullish to bearish and vice versa).

Oscillator Cross: Trade based on crossovers between the fast and slow oscillators.

Trade Logic

Trade Direction Options

Long Only

Short Only

Long & Short

Entry Conditions

Long Entry: Triggered on bullish regime shift or fast crossing above slow.

Short Entry: Triggered on bearish regime shift or fast crossing below slow.

Exit Conditions

Long Exit: Triggered on bearish shift or fast crossing below slow.

Short Exit: Triggered on bullish shift or fast crossing above slow.

The strategy closes opposing positions before opening new ones.

Visual Features

Oscillator Bands: Plots fast and slow oscillators, colored by trend.

Background Highlight: Indicates current trend regime.

Signal Markers: Triangle shapes show bullish/bearish shifts.

Dashboard Table: Displays live trend status ("Bullish", "Bearish", "Neutral") in the chart’s corner.

Inputs & Customization

Oscillator Periods – Fast and slow lengths.

Refit Interval – How often volatility clusters update.

Volatility Lookback & Smoothing

Color Settings – Choose your own bullish/bearish colors.

Signal Mode – Regime shift or oscillator crossover.

Trade Direction Mode

Use Cases

Swing Trading: Take entries based on adaptive regime shifts.

Trend Following: Follow the active trend using filtered oscillator logic.

Volatility-Responsive Systems: Adjust your trade behavior depending on market volatility.

Clean Exit Management: Automatically closes positions on opposite signal.

Conclusion

The Dual-Phase Trend Regime Strategy is a smart, adaptive, non-repainting system that:

Automatically switches between fast and slow trend logic.

Responds dynamically to changes in volatility.

Provides clean and visual entry/exit signals.

Supports both momentum and reversal trading logic.

This strategy is ideal for traders seeking a volatility-aware, trend-sensitive tool across any market or timeframe.

Full credit to Zeiierman.

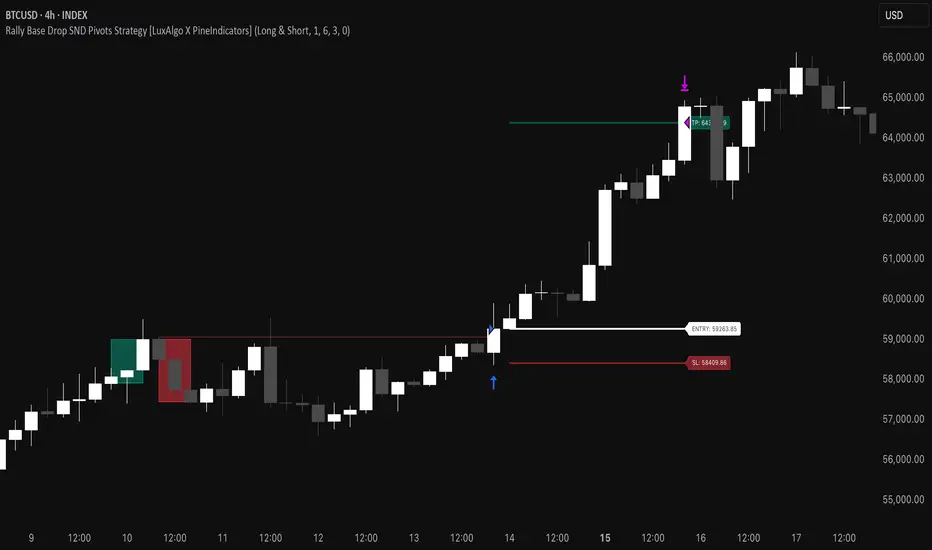

Rally Base Drop SND Pivots Strategy [LuxAlgo X PineIndicators]This strategy is based on the Rally Base Drop (RBD) SND Pivots indicator developed by LuxAlgo. Full credit for the concept and original indicator goes to LuxAlgo.

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand trading system that detects pivot points based on Rally, Base, and Drop (RBD) candles. This strategy automatically identifies key market structure levels, allowing traders to:

Identify pivot-based supply and demand (SND) zones.

Use fixed criteria for trend continuation or reversals.

Filter out market noise by requiring structured price formations.

Enter trades based on breakouts of key SND pivot levels.

How the Rally Base Drop SND Pivots Strategy Works

1. Pivot Point Detection Using RBD Candles

The strategy follows a rigid market structure methodology, where pivots are detected only when:

A Rally (R) consists of multiple consecutive bullish candles.

A Drop (D) consists of multiple consecutive bearish candles.

A Base (B) is identified as a transition between Rallies and Drops, acting as a pivot point.

The pivot level is confirmed when the formation is complete.

Unlike traditional fractal-based pivots, RBD Pivots enforce stricter structural rules, ensuring that each pivot:

Has a well-defined bullish or bearish price movement.

Reduces false signals caused by single-bar fluctuations.

Provides clear supply and demand levels based on structured price movements.

These pivot levels are drawn on the chart using color-coded boxes:

Green zones represent bullish pivot levels (Rally Base formations).

Red zones represent bearish pivot levels (Drop Base formations).

Once a pivot is confirmed, the high or low of the base candle is used as the reference level for future trades.

2. Trade Entry Conditions

The strategy allows traders to select from three trading modes:

Long Only – Only takes long trades when bullish pivot breakouts occur.

Short Only – Only takes short trades when bearish pivot breakouts occur.

Long & Short – Trades in both directions based on pivot breakouts.

Trade entry signals are triggered when price breaks through a confirmed pivot level:

Long Entry:

A bullish pivot level is formed.

Price breaks above the bullish pivot level.

The strategy enters a long position.

Short Entry:

A bearish pivot level is formed.

Price breaks below the bearish pivot level.

The strategy enters a short position.

The strategy includes an optional mode to reverse long and short conditions, allowing traders to experiment with contrarian entries.

3. Exit Conditions Using ATR-Based Risk Management

This strategy uses the Average True Range (ATR) to calculate dynamic stop-loss and take-profit levels:

Stop-Loss (SL): Placed 1 ATR below entry for long trades and 1 ATR above entry for short trades.

Take-Profit (TP): Set using a Risk-Reward Ratio (RR) multiplier (default = 6x ATR).

When a trade is opened:

The entry price is recorded.

ATR is calculated at the time of entry to determine stop-loss and take-profit levels.

Trades exit automatically when either SL or TP is reached.

If reverse conditions mode is enabled, stop-loss and take-profit placements are flipped.

Visualization & Dynamic Support/Resistance Levels

1. Pivot Boxes for Market Structure

Each pivot is marked with a colored box:

Green boxes indicate bullish demand zones.

Red boxes indicate bearish supply zones.

These boxes remain on the chart to act as dynamic support and resistance levels, helping traders identify key price reaction zones.

2. Horizontal Entry, Stop-Loss, and Take-Profit Lines

When a trade is active, the strategy plots:

White line → Entry price.

Red line → Stop-loss level.

Green line → Take-profit level.

Labels display the exact entry, SL, and TP values, updating dynamically as price moves.

Customization Options

This strategy offers multiple adjustable settings to optimize performance for different market conditions:

Trade Mode Selection → Choose between Long Only, Short Only, or Long & Short.

Pivot Length → Defines the number of required Rally & Drop candles for a pivot.

ATR Exit Multiplier → Adjusts stop-loss distance based on ATR.

Risk-Reward Ratio (RR) → Modifies take-profit level relative to risk.

Historical Lookback → Limits how far back pivot zones are displayed.

Color Settings → Customize pivot box colors for bullish and bearish setups.

Considerations & Limitations

Pivot Breakouts Do Not Guarantee Reversals. Some pivot breaks may lead to continuation moves instead of trend reversals.

Not Optimized for Low Volatility Conditions. This strategy works best in trending markets with strong momentum.

ATR-Based Stop-Loss & Take-Profit May Require Optimization. Different assets may require different ATR multipliers and RR settings.

Market Noise May Still Influence Pivots. While this method filters some noise, fake breakouts can still occur.

Conclusion

The Rally Base Drop SND Pivots Strategy is a non-repainting supply and demand system that combines:

Pivot-based market structure analysis (using Rally, Base, and Drop candles).

Breakout-based trade entries at confirmed SND levels.

ATR-based dynamic risk management for stop-loss and take-profit calculation.

This strategy helps traders:

Identify high-probability supply and demand levels.

Trade based on structured market pivots.

Use a systematic approach to price action analysis.

Automatically manage risk with ATR-based exits.

The strict pivot detection rules and built-in breakout validation make this strategy ideal for traders looking to:

Trade based on market structure.

Use defined support & resistance levels.

Reduce noise compared to traditional fractals.

Implement a structured supply & demand trading model.

This strategy is fully customizable, allowing traders to adjust parameters to fit their market and trading style.

Full credit for the original concept and indicator goes to LuxAlgo.

Liquidity Sweep Filter Strategy [AlgoAlpha X PineIndicators]This strategy is based on the Liquidity Sweep Filter developed by AlgoAlpha. Full credit for the concept and original indicator goes to AlgoAlpha.

The Liquidity Sweep Filter Strategy is a non-repainting trading system designed to identify liquidity sweeps, trend shifts, and high-impact price levels. It incorporates volume-based liquidation analysis, trend confirmation, and dynamic support/resistance detection to optimize trade entries and exits.

This strategy helps traders:

Detect liquidity sweeps where major market participants trigger stop losses and liquidations.

Identify trend shifts using a volatility-based moving average system.

Analyze volume distribution with a built-in volume profile visualization.

Filter noise by differentiating between major and minor liquidity sweeps.

How the Liquidity Sweep Filter Strategy Works

1. Trend Detection Using Volatility-Based Filtering

The strategy applies a volatility-adjusted moving average system to determine trend direction:

A central trend line is calculated using an EMA smoothed over a user-defined length.

Upper and lower deviation bands are created based on the average price deviation over multiple periods.

If price closes above the upper band, the strategy signals an uptrend.

If price closes below the lower band, the strategy signals a downtrend.

This approach ensures that trend shifts are confirmed only when price significantly moves beyond normal market fluctuations.

2. Liquidity Sweep Detection

Liquidity sweeps occur when price temporarily breaks key levels, triggering stop-loss liquidations or margin call events. The strategy tracks swing highs and lows, marking potential liquidity grabs:

Bearish Liquidity Sweeps – Price breaks a recent high, then reverses downward.

Bullish Liquidity Sweeps – Price breaks a recent low, then reverses upward.

Volume Integration – The strategy analyzes trading volume at each sweep to differentiate between major and minor sweeps.

Key levels where liquidity sweeps occur are plotted as color-coded horizontal lines:

Red lines indicate bearish liquidity sweeps.

Green lines indicate bullish liquidity sweeps.

Labels are displayed at each sweep, showing the volume of liquidated positions at that level.

3. Volume Profile Analysis

The strategy includes an optional volume profile visualization, displaying how trading volume is distributed across different price levels.

Features of the volume profile:

Point of Control (POC) – The price level with the highest traded volume is marked as a key area of interest.

Bounding Box – The profile is enclosed within a transparent box, helping traders visualize the price range of high trading activity.

Customizable Resolution & Scale – Traders can adjust the granularity of the profile to match their preferred time frame.

The volume profile helps identify zones of strong support and resistance, making it easier to anticipate price reactions at key levels.

Trade Entry & Exit Conditions

The strategy allows traders to configure trade direction:

Long Only – Only takes long trades.

Short Only – Only takes short trades.

Long & Short – Trades in both directions.

Entry Conditions

Long Entry:

A bullish trend shift is confirmed.

A bullish liquidity sweep occurs (price sweeps below a key level and reverses).

The trade direction setting allows long trades.

Short Entry:

A bearish trend shift is confirmed.

A bearish liquidity sweep occurs (price sweeps above a key level and reverses).

The trade direction setting allows short trades.

Exit Conditions

Closing a Long Position:

A bearish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Closing a Short Position:

A bullish trend shift occurs.

The position is liquidated at a predefined liquidity sweep level.

Customization Options

The strategy offers multiple adjustable settings:

Trade Mode: Choose between Long Only, Short Only, or Long & Short.

Trend Calculation Length & Multiplier: Adjust how trend signals are calculated.

Liquidity Sweep Sensitivity: Customize how aggressively the strategy identifies sweeps.

Volume Profile Display: Enable or disable the volume profile visualization.

Bounding Box & Scaling: Control the size and position of the volume profile.

Color Customization: Adjust colors for bullish and bearish signals.

Considerations & Limitations

Liquidity sweeps do not always result in reversals. Some price sweeps may continue in the same direction.

Works best in volatile markets. In low-volatility environments, liquidity sweeps may be less reliable.

Trend confirmation adds a slight delay. The strategy ensures valid signals, but this may result in slightly later entries.

Large volume imbalances may distort the volume profile. Adjusting the scale settings can help improve visualization.

Conclusion

The Liquidity Sweep Filter Strategy is a volume-integrated trading system that combines liquidity sweeps, trend analysis, and volume profile data to optimize trade execution.

By identifying key price levels where liquidations occur, this strategy provides valuable insight into market behavior, helping traders make better-informed trading decisions.

Key use cases for this strategy:

Liquidity-Based Trading – Capturing moves triggered by stop hunts and liquidations.

Volume Analysis – Using volume profile data to confirm high-activity price zones.

Trend Following – Entering trades based on confirmed trend shifts.

Support & Resistance Trading – Using liquidity sweep levels as dynamic price zones.

This strategy is fully customizable, allowing traders to adapt it to different market conditions, timeframes, and risk preferences.

Full credit for the original concept and indicator goes to AlgoAlpha.

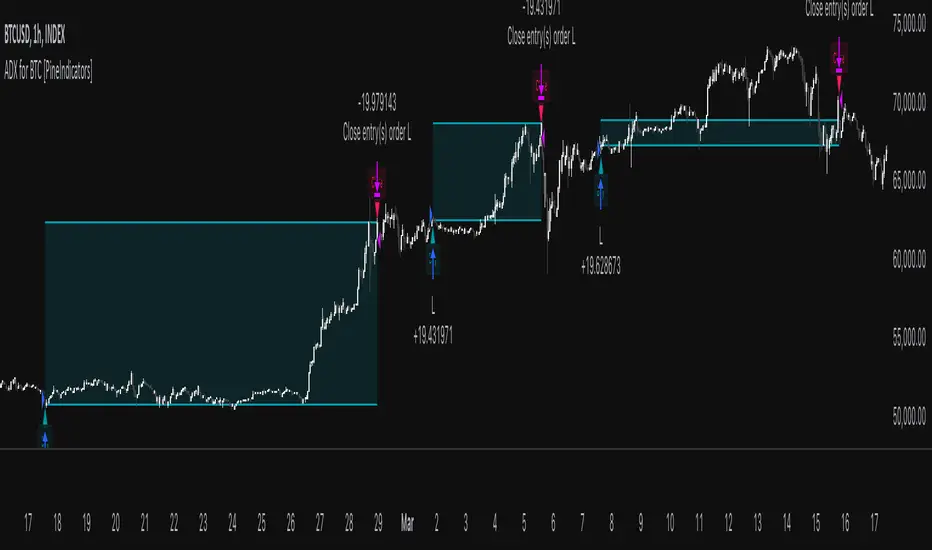

ADX for BTC [PineIndicators]The ADX Strategy for BTC is a trend-following system that uses the Average Directional Index (ADX) to determine market strength and momentum shifts. Designed for Bitcoin trading, this strategy applies a customizable ADX threshold to confirm trend signals and optionally filters entries using a Simple Moving Average (SMA). The system features automated entry and exit conditions, dynamic trade visualization, and built-in trade tracking for historical performance analysis.

⚙️ Core Strategy Components

1️⃣ Average Directional Index (ADX) Calculation

The ADX indicator measures trend strength without indicating direction. It is derived from the Positive Directional Movement (+DI) and Negative Directional Movement (-DI):

+DI (Positive Directional Index): Measures upward price movement.

-DI (Negative Directional Index): Measures downward price movement.

ADX Value: Higher values indicate stronger trends, regardless of direction.

This strategy uses a default ADX length of 14 to smooth out short-term fluctuations while detecting sustainable trends.

2️⃣ SMA Filter (Optional Trend Confirmation)

The strategy includes a 200-period SMA filter to validate trend direction before entering trades. If enabled:

✅ Long Entry is only allowed when price is above a long-term SMA multiplier (5x the standard SMA length).

✅ If disabled, the strategy only considers the ADX crossover threshold for trade entries.

This filter helps reduce entries in sideways or weak-trend conditions, improving signal reliability.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when:

✅ ADX crosses above the threshold (default = 14), indicating a strengthening trend.

✅ (If SMA filter is enabled) Price is above the long-term SMA multiplier.

🔻 Exit Conditions

A position is closed when:

✅ ADX crosses below the stop threshold (default = 45), signaling trend weakening.

By adjusting the entry and exit ADX levels, traders can fine-tune sensitivity to trend changes.

📏 Trade Visualization & Tracking

Trade Markers

"Buy" label (▲) appears when a long position is opened.

"Close" label (▼) appears when a position is exited.

Trade History Boxes

Green if a trade is profitable.

Red if a trade closes at a loss.

Trend Tracking Lines

Horizontal lines mark entry and exit prices.

A filled trade box visually represents trade duration and profitability.

These elements provide clear visual insights into trade execution and performance.

⚡ How to Use This Strategy

1️⃣ Apply the script to a BTC chart in TradingView.

2️⃣ Adjust ADX entry/exit levels based on trend sensitivity.

3️⃣ Enable or disable the SMA filter for trend confirmation.

4️⃣ Backtest performance to analyze historical trade execution.

5️⃣ Monitor trade markers and history boxes for real-time trend insights.

This strategy is designed for trend traders looking to capture high-momentum market conditions while filtering out weak trends.

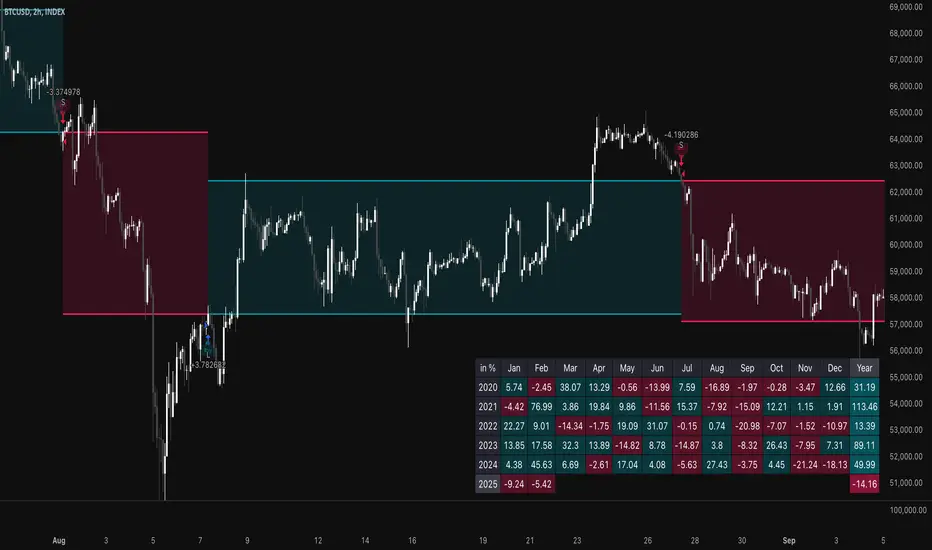

TSI Long/Short for BTC 2HThe TSI Long/Short for BTC 2H strategy is an advanced trend-following system designed specifically for trading Bitcoin (BTC) on a 2-hour timeframe. It leverages the True Strength Index (TSI) to identify momentum shifts and executes both long and short trades in response to dynamic market conditions.

Unlike traditional moving average-based strategies, this script uses a double-smoothed momentum calculation, enhancing signal accuracy and reducing noise. It incorporates automated position sizing, customizable leverage, and real-time performance tracking, ensuring a structured and adaptable trading approach.

🔹 What Makes This Strategy Unique?

Unlike simple crossover strategies or generic trend-following approaches, this system utilizes a customized True Strength Index (TSI) methodology that dynamically adjusts to market conditions.

🔸 True Strength Index (TSI) Filtering – The script refines the TSI by applying double exponential smoothing, filtering out weak signals and capturing high-confidence momentum shifts.

🔸 Adaptive Entry & Exit Logic – Instead of fixed thresholds, it compares the TSI value against a dynamically determined high/low range from the past 100 bars to confirm trade signals.

🔸 Leverage & Risk Optimization – Position sizing is dynamically adjusted based on account equity and leverage settings, ensuring controlled risk exposure.

🔸 Performance Monitoring System – A built-in performance tracking table allows traders to evaluate monthly and yearly results directly on the chart.

📊 Core Strategy Components

1️⃣ Momentum-Based Trade Execution

The strategy generates long and short trade signals based on the following conditions:

✅ Long Entry Condition – A buy signal is triggered when the TSI crosses above its 100-bar highest value (previously set), confirming bullish momentum.

✅ Short Entry Condition – A sell signal is generated when the TSI crosses below its 100-bar lowest value (previously set), indicating bearish pressure.

Each trade execution is fully automated, reducing emotional decision-making and improving trading discipline.

2️⃣ Position Sizing & Leverage Control

Risk management is a key focus of this strategy:

🔹 Dynamic Position Sizing – The script calculates position size based on:

Account Equity – Ensuring trade sizes adjust dynamically with capital fluctuations.

Leverage Multiplier – Allows traders to customize risk exposure via an adjustable leverage setting.

🔹 No Fixed Stop-Loss – The strategy relies on reversals to exit trades, meaning each position is closed when the opposite signal appears.

This design ensures maximum capital efficiency while adapting to market conditions in real time.

3️⃣ Performance Visualization & Tracking

Understanding historical performance is crucial for refining strategies. The script includes:

📌 Real-Time Trade Markers – Buy and sell signals are visually displayed on the chart for easy reference.

📌 Performance Metrics Table – Tracks monthly and yearly returns in percentage form, helping traders assess profitability over time.

📌 Trade History Visualization – Completed trades are displayed with color-coded boxes (green for long trades, red for short trades), visually representing profit/loss dynamics.

📢 Why Use This Strategy?

✔ Advanced Momentum Detection – Uses a double-smoothed TSI for more accurate trend signals.

✔ Fully Automated Trading – Removes emotional bias and enforces discipline.

✔ Customizable Risk Management – Adjust leverage and position sizing to suit your risk profile.

✔ Comprehensive Performance Tracking – Integrated reporting system provides clear insights into past trades.

This strategy is ideal for Bitcoin traders looking for a structured, high-probability system that adapts to both bullish and bearish trends on the 2-hour timeframe.

📌 How to Use: Simply add the script to your 2H BTC chart, configure your leverage settings, and let the system handle trade execution and tracking! 🚀

Ultimate T3 Fibonacci for BTC Scalping. Look at backtest report!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto trading! This strategy is for BITCOIN on the 30 minute chart since I designed it to be a scalping strategy. I calculated for trading fees, and use a small amount of capital in the backtest report. But feel free to modify the capital and how much per order to see how it changes the results:)

It is called the "Ultimate T3 Fibonacci Indicator by NHBprod" that computes and displays two T3-based moving averages derived from price data. The t3_function calculates the Tilson T3 indicator by applying a series of exponential moving averages to a combined price metric and then blending these results with specific coefficients derived from an input factor.

The script accepts several user inputs that toggle the use of the T3 filter, select the buy signal method, and set parameters like lengths and volume factors for two variations of the T3 calculation. Two T3 lines, T3 and T32, are computed with different parameters, and their colors change dynamically (green/red for T3 and blue/purple for T32) based on whether the lines are trending upward or downward. Depending on the selected signal method, the script generates buy signals either when T32 crosses over T3 or when the closing price is above T3, and similarly, sell signals are generated on the respective conditions for crossing under or closing below. Finally, the indicator plots the T3 lines on the chart, adds visual buy/sell markers, and sets alert conditions to notify users when the respective trading signals occur.

The user has the ability to tune the parameters using TP/SL, date timerames for analyses, and the actual parameters of the T3 function including the buy/sell signal! Lastly, the user has the option of trading this long, short, or both!

Let me know your thoughts and check out the backtest report!

Volatility Momentum Breakout StrategyDescription:

Overview:

The Volatility Momentum Breakout Strategy is designed to capture significant price moves by combining a volatility breakout approach with trend and momentum filters. This strategy dynamically calculates breakout levels based on market volatility and uses these levels along with trend and momentum conditions to identify trade opportunities.

How It Works:

1. Volatility Breakout:

• Methodology:

The strategy computes the highest high and lowest low over a defined lookback period (excluding the current bar to avoid look-ahead bias). A multiple of the Average True Range (ATR) is then added to (or subtracted from) these levels to form dynamic breakout thresholds.

• Purpose:

This method helps capture significant price movements (breakouts) while ensuring that only past data is used, thereby maintaining realistic signal generation.

2. Trend Filtering:

• Methodology:

A short-term Exponential Moving Average (EMA) is applied to determine the prevailing trend.

• Purpose:

Long trades are considered only when the current price is above the EMA, indicating an uptrend, while short trades are taken only when the price is below the EMA, indicating a downtrend.

3. Momentum Confirmation:

• Methodology:

The Relative Strength Index (RSI) is used to gauge market momentum.

• Purpose:

For long entries, the RSI must be above a mid-level (e.g., above 50) to confirm upward momentum, and for short entries, it must be below a similar threshold. This helps filter out signals during overextended conditions.

Entry Conditions:

• Long Entry:

A long position is triggered when the current closing price exceeds the calculated long breakout level, the price is above the short-term EMA, and the RSI confirms momentum (e.g., above 50).

• Short Entry:

A short position is triggered when the closing price falls below the calculated short breakout level, the price is below the EMA, and the RSI confirms momentum (e.g., below 50).

Risk Management:

• Position Sizing:

Trades are sized to risk a fixed percentage of account equity (set here to 5% per trade in the code, with each trade’s stop loss defined so that risk is limited to approximately 2% of the entry price).

• Stop Loss & Take Profit:

A stop loss is placed a fixed ATR multiple away from the entry price, and a take profit target is set to achieve a 1:2 risk-reward ratio.

• Realistic Backtesting:

The strategy is backtested using an initial capital of $10,000, with a commission of 0.1% per trade and slippage of 1 tick per bar—parameters chosen to reflect conditions faced by the average trader.

Important Disclaimers:

• No Look-Ahead Bias:

All breakout levels are calculated using only past data (excluding the current bar) to ensure that the strategy does not “peek” into future data.

• Educational Purpose:

This strategy is experimental and provided solely for educational purposes. Past performance is not indicative of future results.

• User Responsibility:

Traders should thoroughly backtest and paper trade the strategy under various market conditions and adjust parameters to fit their own risk tolerance and trading style before live deployment.

Conclusion:

By integrating volatility-based breakout signals with trend and momentum filters, the Volatility Momentum Breakout Strategy offers a unique method to capture significant price moves in a disciplined manner. This publication provides a transparent explanation of the strategy’s components and realistic backtesting parameters, making it a useful tool for educational purposes and further customization by the TradingView community.

Ultimate Stochastics Strategy by NHBprod Use to Day Trade BTCHey All!

Here's a new script I worked on that's super simple but at the same time useful. Check out the backtest results. The backtest results include slippage and fees/commission, and is still quite profitable. Obviously the profitability magnitude depends on how much capital you begin with, and how much the user utilizes per order, but in any event it seems to be profitable according to backtests.

This is different because it allows you full functionality over the stochastics calculations which is designed for random datasets. This script allows you to:

Designate ANY period of time to analyze and study

Choose between Long trading, short trading, and Long & Short trading

It allows you to enter trades based on the stochastics calculations

It allows you to EXIT trades using the stochastics calculations or take profit, or stop loss, Or any combination of those, which is nice because then the user can see how one variable effects the overall performance.

As for the actual stochastics formula, you get control, and get to SEE the plot lines for slow K, slow D, and fast K, which is usually not considered.

You also get the chance to modify the smoothing method, which has not been done with regular stochastics indicators. You get to choose the standard simple moving average (SMA) method, but I also allow you to choose other MA's such as the HMA and WMA.

Lastly, the user gets the option of using a custom trade extender, which essentially allows a buy or sell signal to exist for X amount of candles after the initial signal. For example, you can use "max bars since signal" to 1, and this will allow the indicator to produce an extra sequential buy signal when a buy signal is generated. This can be useful because it is possible that you use a small take profit (TP) and quickly exit a profitable trade. With the max bars since signal variable, you're able to reenter on the next candle and allow for another opportunity.

Let me know if you have any questions! Please take a look at the performance report and let me know your thoughts! :)

RSI Strategy With TP/SL - Lower TFThis Pine Script strategy integrates the Relative Strength Index (RSI) for trade signals with user-defined Take Profit (TP) and Stop Loss (SL) levels. It's designed for flexible application in different market conditions, offering long, short, or dual-direction trading.

Short Description

The strategy uses the RSI to identify overbought and oversold market conditions:

Buy signal: When RSI drops below the specified "Buy Level."

Sell signal: When RSI rises above the "Sell Level."

Additionally, it manages risk and profit targets with:

Take Profit (TP): Exits trades when the price reaches a percentage gain.

Stop Loss (SL): Exits trades to limit losses if the price falls by a certain percentage.

The strategy is versatile and includes options for visualizing performance, monthly profit/loss data, and detailed trade metrics.

How to Use

Set Parameters:

RSI Period: Default is 14. Adjust based on your analysis.

RSI Buy/Sell Levels:

Buy Level: Default is 40. Consider higher levels for conservative entries.

Sell Level: Default is 60. Lower this for earlier exits.

Take Profit (%): Set your profit target (default: 5%).

Stop Loss (%): Set your risk tolerance (default: 2%).

Trade Direction: Choose "Long Only," "Short Only," or "Both."

Interpret Signals:

Buy signals appear when RSI crosses below the buy threshold.

Sell signals appear when RSI crosses above the sell threshold.

Risk Management:

The strategy dynamically calculates TP and SL levels for each trade.

TP/SL is applied using the percentage input based on the entry price.

Monitor Performance:

Review trade statistics in the "Strategy Tester."

Use the monthly performance table to track P/L across months.

Customize Alerts:

Alerts for buy, sell, TP, and SL events can be used to automate notifications.

Key Features

Configurable RSI Settings: Adaptable to various market conditions.

Risk Management: Built-in TP and SL management.

Customizable Trade Direction: Tailored for long-only, short-only, or both directions.

Monthly P/L Table: Visualizes performance trends over time.

Alerts: Notifies when critical trade events occur.

Please do your own research before ase this to your real trading.

Crypto Volatility Bitcoin Correlation Strategy Description:

The Crypto Volatility Bitcoin Correlation Strategy is designed to leverage market volatility specifically in Bitcoin (BTC) using a combination of volatility indicators and trend-following techniques. This strategy utilizes the VIXFix (a volatility indicator adapted for crypto markets) and the BVOL7D (Bitcoin 7-Day Volatility Index from BitMEX) to identify periods of high volatility, while confirming trends with the Exponential Moving Average (EMA). These components work together to offer a comprehensive system that traders can use to enter positions when volatility and trends are aligned in their favor.

Key Features:

VIXFix (Volatility Index for Crypto Markets): This indicator measures the highest price of Bitcoin over a set period and compares it with the current low price to gauge market volatility. A rise in VIXFix indicates increasing market volatility, signaling that large price movements could occur.

BVOL7D (Bitcoin 7-Day Volatility Index): This volatility index, provided by BitMEX, measures the volatility of Bitcoin over the past 7 days. It helps traders monitor the recent volatility trend in the market, particularly useful when making short-term trading decisions.

Exponential Moving Average (EMA): The 50-period EMA acts as a trend indicator. When the price is above the EMA, it suggests the market is in an uptrend, and when the price is below the EMA, it suggests a downtrend.

How It Works:

Long Entry: A long position is triggered when both the VIXFix and BVOL7D indicators are rising, signaling increased volatility, and the price is above the 50-period EMA, confirming that the market is trending upward.

Exit: The strategy exits the position when the price crosses below the 50-period EMA, which signals a potential weakening of the uptrend and a decrease in volatility.

This strategy ensures that traders only enter positions when the volatility aligns with a clear trend, minimizing the risk of entering trades during periods of market uncertainty.

Testing and Timeframe:

This strategy has been tested on Bitcoin using the daily timeframe, which provides a longer-term perspective on market trends and volatility. However, users can adjust the timeframe according to their trading preferences. It is crucial to note that this strategy does not include comprehensive risk management, aside from the exit condition when the price crosses below the EMA. Users are strongly advised to implement their own risk management techniques, such as setting appropriate stop-loss levels, to safeguard their positions during high volatility periods.

Utility:

The Crypto Volatility Bitcoin Correlation Strategy is particularly well-suited for traders who aim to capitalize on the high volatility often seen in the Bitcoin market. By combining volatility measurements (VIXFix and BVOL7D) with a trend-following mechanism (EMA), this strategy helps identify optimal moments for entering and exiting trades. This approach ensures that traders participate in potentially profitable market moves while minimizing exposure during times of uncertainty.

Use Cases:

Volatility-Based Entries: Traders looking to take advantage of market volatility spikes will find this strategy useful for timing entry points during market swings.

Trend Confirmation: By using the EMA as a confirmation tool, traders can avoid entering trades that go against the trend, which can result in significant losses during volatile market conditions.

Risk Management: While the strategy exits when price falls below the EMA, it is important to recognize that this is not a full risk management system. Traders should use caution and integrate additional risk measures, such as stop-losses and position sizing, to better manage potential losses.

How to Use:

Step 1: Monitor the VIXFix and BVOL7D indicators. When both are rising and the Bitcoin price is above the EMA, the strategy will trigger a long entry, indicating that the market is experiencing increased volatility with a confirmed uptrend.

Step 2: Exit the position when the price drops below the 50-period EMA, signaling that the trend may be reversing or weakening, reducing the likelihood of continued upward price movement.

This strategy is open-source and is intended to help traders navigate volatile market conditions, particularly in Bitcoin, using proven indicators for volatility and trend confirmation.

Risk Disclaimer:

This strategy has been tested on the daily timeframe of Bitcoin, but users should be aware that it does not include built-in risk management except for the below-EMA exit condition. Users should be extremely cautious when using this strategy and are encouraged to implement their own risk management, such as using stop-losses, position sizing, and setting appropriate limits. Trading involves significant risk, and this strategy does not guarantee profits or prevent losses. Past performance is not indicative of future results. Always test any strategy in a demo environment before applying it to live markets.

Rsi Long-Term Strategy [15min]Hello, I would like to present to you The "RSI Long-Term Strategy" for 15min tf

The "RSI Long-Term Strategy " is designed for traders who prefer a combination of momentum and trend-following techniques. The strategy focuses on entering long positions during significant market corrections within an overall uptrend, confirmed by both RSI and volume. The use of long-term SMAs ensures that trades are made in line with the broader market trend. The stop-loss feature provides risk management by limiting losses on trades that do not perform as expected. This strategy is particularly well-suited for longer-term traders who monitor 15-minute charts but look for substantial trend reversals or continuations.

Indicators and Parameters: