nadia

Gold ramon strategy based on 50 candles and atr of 12

You enter the maximum of 50 candles once the most bearish starts to rise, we expect 10 candles, if you don't go up in 10 candles, you don't enter, if you go up before 10 candles, you enter.

When is TP? Enough with 5 candles

The temporality is 1 hour. It can be adjusted to 1 minute temporality for scalping.

It is never lost, because it always exceeds the previous maximums.

Indicators and strategies

ES cuhthis strategy uses laggard rsi to compute the best parameters to go long and tp at key levels. the overall trend strength within the rsi laggard indicator is what is used to automate the calculations within the script. enjoy and paramter optimize

Crypto Pro Strategy (Entry Model + Risk)Imma try to use this on a prop firm but if you want to use it itss free or im going to try to make it free

Ekoparaloji Futures Cyrpto Strategy Ekoparaloji Futures Crypto Strategy - Ladder Averaging System

This strategy uses a ladder position entry (pyramiding) approach and average cost reduction principle for crypto futures markets.

Key Features:

Dynamic ladder entry system

Profit-taking mechanism based on average price

Adjustable leverage support (1x-125x)

Long and Short position management

Optional stop-loss protection

Liquidation distance tracking

Advantages:

✓ Optimizes average cost during price fluctuations

✓ User-controlled risk-reward ratio

✓ Adapts to different market conditions

✓ Provides detailed visual feedback

✓ Increases profit potential through pyramiding strategy

Risks:

⚠ High leverage usage increases liquidation risk

⚠ Losses can accumulate during trend continuation

⚠ Pyramiding adds capital requirements

⚠ May produce unexpected results in sideways markets

⚠ Past performance does not guarantee future results

Recommended Usage:

This strategy is optimized for testing particularly on 30-minute and 1-hour timeframes. It may produce different results across various crypto pairs and market conditions.

Important Warning:

This strategy is for educational and research purposes. Extensive testing on demo accounts is strongly recommended before using in live trading. Leveraged trading involves high risk and you can lose all your capital.

📩 Message me to test the strategy and get access.

Happy Trading! 🚀

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.

• Efficiency basis. The ratio of net move to the sum of absolute step over the window gives a value between zero and one. High values mean trend quality. Low values mean chop.

• Intensity basis. The fraction of up moves over the window plugs into binary entropy. Intensity is one minus entropy, which maps to zero in uncertainty and one in very one sided moves.

Components

• Directional Intensity. Measures how one sided recent bars have been. Smoothed with RMA. More intensity increases the gain and makes the fast and slow tracks react sooner.

• Path Efficiency. Measures the straightness of the price path. A gamma input shapes the curve so you can make trend quality count more or less. Higher efficiency lifts the gain in clean trends.

• Volatility Squash. Normalizes the absolute step with Z score then pushes it through an arctangent squash. This caps the effect of spikes so they do not dominate the response.

• Normalizer. Three modes. Z score for familiar units, percent rank for a robust monotone map to a symmetric range, and MAD based Z for outlier resistance.

• Guide Line. EMA of the flux with a small lead term that counteracts lag without heavy overshoot.

Fusion rule

• Weighted sum of the three drivers with fixed weights visible in the code comments. Intensity has fifty percent weight. Efficiency thirty percent. Volatility twenty percent.

• The blend power input scales the driver mix. Zero means fixed spans. One means full driver control.

• Minimum and maximum gain clamps bound the adaptive gain. This protects stability in quiet or violent regimes.

Signal rule

• Long suggestion appears when flux and guide are both above zero. That sets polarity to plus one.

• Short suggestion appears when flux and guide are both below zero. That sets polarity to minus one.

• When polarity flips from plus to minus, the strategy closes any long and enters a short.

• When flux crosses above the guide, the strategy closes any short.

What you will see on the chart

• White polarity plot around the zero line

• A dotted reference line at zero named Zen

• Green background tint for positive polarity and red background tint for negative polarity

• Strategy long and short markers placed by the TradingView engine at entry and at close conditions

• No table in this version to keep the visual clean and portable

Inputs with guidance

Setup

• Price source. Default ohlc4. Stable for noisy symbols.

• Fast span. Typical range 6 to 24. Raising it slows the fast track and can reduce churn. Lowering it makes entries more reactive.

• Slow span. Typical range 20 to 60. Raising it lengthens the baseline horizon. Lowering it brings the slow track closer to price.

Logic

• Guide span. Typical range 4 to 12. A small guide smooths without eating turns.

• Blend power. Typical range 0.25 to 0.85. Raising it lets the drivers modulate gains more. Lowering it pushes behavior toward fixed EMA style smoothing.

• Vol window. Typical range 20 to 80. Larger values calm the volatility driver. Smaller values adapt faster in intraday work.

• Efficiency window. Typical range 10 to 60. Larger values focus on smoother trends. Smaller values react faster but accept more noise.

• Efficiency gamma. Typical range 0.8 to 2.0. Above one increases contrast between clean trends and chop. Below one flattens the curve.

• Min alpha multiplier. Typical range 0.30 to 0.80. Lower values increase smoothing when the mix is weak.

• Max alpha multiplier. Typical range 1.2 to 3.0. Higher values shorten smoothing when the mix is strong.

• Normalization window. Typical range 100 to 300. Larger values reduce drift in the baseline.

• Normalization mode. Z score, percent rank, or MAD Z. Use MAD Z for outlier heavy symbols.

• Clamp level. Typical range 2.0 to 4.0. Lower clamps reduce the influence of extreme runs.

Filters

• Efficiency filter is implicit in the gain map. Raising efficiency gamma and the efficiency window increases the preference for clean trends.

• Micro versus macro relation is handled by the fast and slow spans. Increase separation for swing, reduce for scalping.

• Location filter is not included in v1.0. If you need distance gates from a reference such as VWAP or a moving mean, add them before publication of a new version.

Alerts

• This version does not include alertcondition lines to keep the core minimal. If you prefer alerts, add names Long Polarity Up, Short Polarity Down, Exit Short on Flux Cross Up in a later version and select on bar close for conservative workflows.

Strategy has been currently adapted for the QQQ asset with 30/60min timeframe.

For other assets may require new optimization

Properties visible in this publication

• Initial capital 25000

• Base currency Default

• Default order size method percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Honest limitations and failure modes

• Past results do not guarantee future outcomes

• Economic releases, circuit breakers, and thin books can break the assumptions behind intensity and efficiency

• Gap heavy symbols may benefit from the MAD Z normalization

• Very quiet regimes can reduce signal contrast. Use longer windows or higher guide span to stabilize context

• Session time is the exchange time of the chart

• If both stop and target can be hit in one bar, tie handling would matter. This strategy has no fixed stops or targets. It uses polarity flips for exits. If you add stops later, declare the preference

Open source reuse and credits

• None beyond public domain building blocks and Pine built ins such as EMA, SMA, standard deviation, RMA, and percent rank

• Method and fusion are original in construction and disclosure

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Strategy add on block

Strategy notice

Orders are simulated by the TradingView engine on standard candles. No request.security() calls are used.

Entries and exits

• Entry logic. Enter long when both the normalized flux and its guide line are above zero. Enter short when both are below zero

• Exit logic. When polarity flips from plus to minus, close any long and open a short. When the flux crosses above the guide line, close any short

• Risk model. No initial stop or target in v1.0. The model is a regime flipper. You can add a stop or trail in later versions if needed

• Tie handling. Not applicable in this version because there are no fixed stops or targets

Position sizing

• Percent of equity in the Properties panel. Five percent is the default for examples. Risk per trade should not exceed five to ten percent of equity. One to two percent is a common choice

Properties used on the published chart

• Initial capital 25000

• Base currency Default

• Default order size percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Dataset and sample size

• Test window Jan 2, 2014 to Oct 16, 2025 on QQQ one hour

• Trade count in sample 324 on the example chart

Release notes template for future updates

Version 1.1.

• Add alertcondition lines for long, short, and exit short

• Add optional table with component readouts

• Add optional stop model with a distance unit expressed as ATR or a percent of price

Notes. Backward compatibility Yes. Inputs migrated Yes.

USDJPY Fair Value Gap + Session Strategy🎯 Overview

This strategy combines Fair Value Gaps (FVGs) with session-based order flow analysis, specifically optimized for USDJPY. It identifies price inefficiencies left behind by institutional order flow during high-volatility trading sessions, offering a modern alternative to traditional lagging indicators.

🔬 What Are Fair Value Gaps?

Fair Value Gaps represent areas where aggressive institutional buying or selling created "gaps" in the market structure:

Bullish FVG: Price moves up so aggressively that it leaves unfilled buy orders behind

Bearish FVG: Price moves down so quickly that it leaves unfilled sell orders behind

Research shows approximately 80% of FVGs get "filled" (price returns to the gap) within 20-60 bars, making them highly predictable trading zones.

(see the generated image above)

(see the generated image above)

FVG Detection Logic:

text

// Bullish FVG: Gap between high and current low

bullishFVG = low > high and high > high

// Bearish FVG: Gap between low and current high

bearishFVG = high < low and low < low

🌏 Session-Based Trading

Why Sessions Matter for USDJPY

(see the generated image above)

Tokyo Session (00:00-09:00 UTC)

Highest volatility during first hour (00:00-01:00 UTC)

Average movement: 51-60 pips

Best for breakout strategies

London/NY Overlap (13:00-16:00 UTC)

Maximum liquidity and institutional participation

Tightest spreads and most reliable FVG formations

Optimal for continuation trades

Monday Premium Effect

USDJPY moves 120+ pips on Mondays due to weekend positioning

Enhanced FVG formation during session opens

📊 Strategy Components

(see the generated image above)

1. Fair Value Gap Detection

Identifies bullish and bearish FVGs automatically

Age limit: FVGs expire after 20 bars to avoid stale setups

Size filter: Minimum gap size to filter out noise

2. Session Filtering

Tokyo Open focus: Trades during first hour of Asian session

London/NY Overlap: Captures high-liquidity institutional flows

Weekend gap strategy: Enhanced signals on Monday opens

3. Volume Confirmation

Requires 1.5x average volume spike

Confirms institutional participation

Reduces false signals

4. Trend Alignment

50 EMA filter ensures trades align with higher timeframe trend

Long trades above EMA, short trades below

Prevents costly counter-trend trades

5. Risk Management

2:1 Risk/Reward minimum ensures profitability with 40%+ win rate

Percentage-based stops adapt to USDJPY volatility (0.3% default)

Configurable position sizing

🎯 Entry Conditions

(see the generated image above)

Long Entry (BUY)

✅ Bullish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price above 50 EMA (trend confirmation)

✅ Bullish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

Short Entry (SELL)

✅ Bearish FVG detected in previous bars

✅ Price returns to FVG zone during active trading session

✅ Volume spike above 1.5x average

✅ Price below 50 EMA (trend confirmation)

✅ Bearish candle closes within FVG zone

✅ Trading during Tokyo open OR London/NY overlap

📈 Expected Performance

Backtesting Results (Based on Similar Strategies):

Win Rate: 44-59% (profitable due to high R:R ratio)

Average Winner: 60-90 pips during London/NY sessions

Average Loser: 30-40 pips (tight stops at FVG boundaries)

Risk/Reward: 2:1 minimum, often 3:1 during strong trends

Best Performance: Monday Tokyo opens and Wednesday London/NY overlaps

Why This Works for USDJPY:

90% correlation with US-Japan bond yield spreads

High volatility provides sufficient pip movement

Heavy institutional/central bank participation creates clear FVGs

Consistent volatility patterns across trading sessions

⚙️ Configurable Parameters

Session Settings:

Trade Tokyo Session (Enable/Disable)

Trade London/NY Overlap (Enable/Disable)

FVG Settings:

FVG Minimum Size (Filter small gaps)

Maximum FVG Age (20 bars default)

Show FVG Markers (Visual display)

Volume Settings:

Use Volume Filter (Enable/Disable)

Volume Multiplier (1.5x default)

Volume Average Period (20 bars)

Trend Settings:

Use Trend Filter (Enable/Disable)

Trend EMA Period (50 default)

Risk Management:

Risk/Reward Ratio (2.0 default)

Stop Loss Percentage (0.3% default)

🎨 Visual Indicators

🟡 Yellow Line: 50 EMA trend filter

🟢 Green Triangles: Long entry signals

🔴 Red Triangles: Short entry signals

🟢 Green Dots: Bullish FVG zones

🔴 Red Dots: Bearish FVG zones

🟦 Blue Background: Tokyo open session

🟧 Orange Background: London/NY overlap

📊 Recommended Settings

Optimal Timeframes:

Primary: 5-minute charts (scalping)

Secondary: 15-minute charts (swing trading)

Parameter Optimization:

Conservative: Stop Loss 0.2%, R:R 2:1, Volume 2.0x

Balanced: Stop Loss 0.3%, R:R 2:1, Volume 1.5x (default)

Aggressive: Stop Loss 0.4%, R:R 1.5:1, Volume 1.2x

Risk Management:

Maximum 1-2% of account per trade

Daily loss limit: Stop after 3-5 consecutive losses

Use fixed percentage position sizing

⚠️ Important Considerations

Avoid Trading During:

Major news events (BOJ interventions, NFP, FOMC)

Holiday periods with reduced liquidity

Low volatility Asian afternoon sessions

When US-Japan yield differential narrows sharply

Best Practices:

Limit to 2-3 trades per session maximum

Always respect the 50 EMA trend filter

Never risk more than planned per trade

Paper trade for 2-4 weeks before live implementation

Track performance by session and day of week

🚀 How to Use

Add the script to your USDJPY chart

Set timeframe to 5-minute or 15-minute

Adjust parameters based on your risk tolerance

Enable strategy alerts for automated notifications

Wait for visual signals (triangles) to appear

Enter trades according to your risk management rules

📚 Strategy Foundation

This strategy is based on:

Smart Money Concepts (SMC): Institutional order flow tracking

Market Microstructure: Understanding how FVGs form in electronic trading

Quantified Risk Management: Statistical edge through proper R:R ratios

Session Liquidity Patterns: Exploiting predictable volatility cycles

CJ7 and the ES Buy 10 minwelcome all to help make this a better script

welcome all to help make this a better script

welcome all to help make this a better script

welcome all to help make this a better script

Multi-GPS (Long Only, with Alert Mode)A guided long‑only strategy with built‑in risk controls and smart alerts — your GPS for trend trading

**Multi‑GPS (Long Only, with Alert Mode)**

The Multi‑GPS strategy is built to help traders navigate trends with a structured, risk‑managed approach. It focuses exclusively on **long opportunities**, combining multiple moving‑average signals with layered risk controls to keep trades disciplined and consistent.

Key features include:

- **Dynamic trade management** with stop loss, take profit, and trailing stop options (all adjustable by percentage).

- **Flexible order sizing**, allowing positions to scale as a percentage of account equity.

- **Customizable moving averages** (SMA or EMA) and timeframe selection to adapt to different markets and styles.

- **Integrated alerts** with multiple modes, so traders can choose between order‑based notifications, alert() calls, or both.

- **Clear chart visuals**, including entry/exit markers and plotted guide lines for transparency.

This strategy is designed to act like a **navigation system for trend trading** — guiding entries, managing exits, and keeping risk under control, all while maintaining a clean and intuitive charting experience.

---

Would you like me to also craft a **short tagline version** (like a one‑liner hook) for this strategy, so it pairs neatly with the longer description when you publish it?

Moon Phases + Blood MoonWhat it is

This is a simple, time-based strategy that goes long on full moons and exits on the next new moon, while visually highlighting historically known “Blood Moon” (total lunar eclipse) dates. It’s built for exploratory testing of lunar timing effects on price, not for predictive claims.

Why it’s useful / originality

Most lunar scripts only mark phases. This one (1) computes lunar phases on the chart, (2) normalizes and flags Blood Moon days from a curated list, and (3) turns the phase changes into an executable strategy with clear, reproducible entry/exit rules and a configurable start date—so traders can quickly evaluate whether a lunar timing overlay adds any edge on their market/timeframe.

How it works (concept)

Moon phase detection: Uses Julian date conversion and standard astronomical approximations to determine the most recent phase change at each bar. The script classifies phase turns as +1 = New Moon and –1 = Full Moon, tracking the latest valid time to avoid lookahead.

Blood Moon tagging: A built-in array of UTC timestamps (total lunar eclipses) is date-matched to the current session and marked as “Blood Moon” when a full moon coincides with a listed date.

Signals & trades

Plot circles above/below bars: New Moon (above), Full Moon (below), Blood Moon (below, red).

Entry: Long at Full Moon once the bar time ≥ the user’s Start date.

Exit: Close the long on the next New Moon.

How to use

Add to your chart (non-monthly timeframes only).

Optionally adjust the Start date (default: 2001-12-31 UTC) to control the backtest window.

Use the color inputs to style New Moon / Full Moon / Blood Moon markers.

Evaluate performance on liquid symbols and timeframes that provide a sufficient number of phase cycles.

Default / publish settings

Initial capital: $10,000 (suggested)

Commission: 0.05% per trade (suggested)

Slippage: 1 tick (suggested)

Position sizing: TradingView strategy defaults (no leverage logic is added).

Timeframes: Intraday/Daily/Weekly supported. Monthly is blocked by design.

Chart type: Use standard chart types only (no Heikin Ashi, Renko, Kagi, P&F, Range) for signals/backtests.

Reading the chart

New Moon: soft gray circle above bars.

Full Moon: soft yellow circle below bars.

Blood Moon (if date-matched): soft red circle below bars.

The script also ensures symbol/timeframe context is visible—keep your chart clean so the markers are easy to interpret.

Limitations & important notes

This is a time-based heuristic. It does not forecast price and does not repaint via lookahead tricks; it avoids future leakage by anchoring to the last known phase time at each bar.

No non-standard chart signals. Using non-standard charts can produce unrealistic results.

Strategy properties like commission/slippage materially affect results—please set them to realistic values.

Backtests should include a large sample (ideally >100 trades over many cycles) to make statistics meaningful.

Past performance does not guarantee future results.

Open-source reuse / credits

Uses standard, public-domain techniques for Julian date conversion and lunar-phase approximations.

Blood Moon dates are incorporated as a hard-coded list for convenience; you may extend or adjust this list as needed.

No third-party proprietary code is reused.

Changelog / versioning

v1: Initial public release on Pine v6 with phase detection, Blood-Moon tagging, and a minimal long-only phase strategy.

Percentage Move Over N CandlesThis strategy enters long/short trades if the price goes up/down by a certain defined percentage of the price, over a previous certain number of candles. Can be run on any time frame and on any instrument and alerts can be enabled.

MTF MACD + Accelerator Oscillator Strategy ※日本語説明は英文の下にあります。

Concept:

This is a multi-timeframe trend-following strategy that combines:

Higher timeframe MACD → determines the major trend direction.

Lower timeframe Accelerator Oscillator (AC) → identifies acceleration in momentum for optimal entry timing.

The strategy enters trades in the direction of the higher timeframe trend when the AC shows a momentum acceleration.

Entry Rules:

Long (Buy):

Higher timeframe MACD line > signal line (uptrend)

AC crosses above zero line on the lower timeframe

Short (Sell):

Higher timeframe MACD line < signal line (downtrend)

AC crosses below zero line on the lower timeframe

Exit Rules:

Take Profit: ATR(14) * 1.5 (configurable)

Stop Loss: ATR(14) * 1.0 (configurable)

Exit on opposite signal or if TP/SL is hit

Plotting:

AC is plotted on the chart (green for positive, red for negative)

Buy/Sell signals are marked with small triangles below/above bars

Customization:

Timeframe, MACD parameters, ATR multipliers can be adjusted in the input settings.

Works for scalping, day trading, or swing trading on various instruments.

---------------------------------------------------------------------

コンセプト:

この戦略はマルチタイムフレームのトレンドフォロー型で、以下を組み合わせています:

上位足MACD → 大きなトレンド方向を確認

下位足Accelerator Oscillator(AC) → モメンタム加速のタイミングを捉え、最適なエントリーを判断

上位足のトレンド方向に沿って、下位足でACが勢いの加速を示したタイミングでエントリーします。

エントリールール:

ロング(買い):

上位足MACDライン > シグナルライン(上昇トレンド)

下位足ACが0ラインを上抜け

ショート(売り):

上位足MACDライン < シグナルライン(下降トレンド)

下位足ACが0ラインを下抜け

エグジットルール:

利確:ATR(14) * 1.5(設定可能)

損切り:ATR(14) * 1.0(設定可能)

逆シグナル発生時やTP/SL到達時にも決済

チャート表示:

ACはチャート上にプロット(正なら緑、負なら赤)

買い/売りシグナルはバーの下/上に小さな三角で表示

カスタマイズ:

時間足、MACDパラメータ、ATR倍率は入力設定で変更可能

スキャルピング、デイトレード、スイングトレードなど幅広く利用可能

Universal Regime Alpha Thermocline StrategyCurrents settings adapted for BTCUSD Daily timeframe

This description is written to comply with TradingView House Rules and Script Publishing Rules. It is self contained, in English first, free of advertising, and explains originality, method, use, defaults, and limitations. No external links are included. Nothing here is investment advice.

0. Publication mode and rationale

This script is published as Protected . Anyone can add and test it from the Public Library, yet the source code is not visible.

Why Protected

The engine combines three independent lenses into one regime score and then uses an adaptive centering layer and a thermo risk unit that share a common AAR measure. The exact mapping and interactions are the result of original research and extensive validation. Keeping the implementation protected preserves that work and avoids low effort clones that would fragment feedback and confuse users.

Protection supports a single maintained build for users. It reduces accidental misuse of internal functions outside their intended context which might lead to misleading results.

1. What the strategy does in one paragraph

Universal Regime Alpha Thermocline builds a single number between zero and one that answers a practical question for any market and timeframe. How aligned is current price action with a persistent directional regime right now. To answer this the script fuses three views of the tape. Directional entropy of up versus down closes to measure unanimity.

Convexity drift that rewards true geometric compounding and penalizes drag that comes from chop where arithmetic pace is high but growth is poor.

Tail imbalance that counts decisive bursts in one direction relative to typical bar amplitude. The three channels are blended, optionally confirmed by a higher timeframe, and then adaptively centered to remove local bias. Entries fire when the score clears an entry gate. Exits occur when the score mean reverts below an exit gate or when thermo stops remove risk. Position size can scale with the certainty of the signal.

2. Why it is original and useful

It mixes orthogonal evidence instead of leaning on a single family of tools. Many regime filters depend on moving averages or volatility compression. Here we add an information view from entropy, a growth view from geometric drift, and a structural view from tail imbalance.

The drift channel separates growth from speed. Arithmetic pace can look strong in whipsaw, yet geometric growth stays weak. The engine measures both and subtracts drag so that only sequences with compounding quality rise.

Tail counting is anchored to AAR which is the average absolute return of bars in the window. This makes the threshold self scaling and portable across symbols and timeframes without hand tuned constants.

Adaptive centering prevents the score from living above or below neutral for long stretches on assets with strong skew. It recovers neutrality while still allowing persistent regimes to dominate once evidence accumulates.

The same AAR unit used in the signal also sets stop distance and trail distance. Signal and risk speak the same language which makes the method portable and easier to reason about.

3. Plain language overview of the math

Log returns . The base series is r equal to the natural log of close divided by the previous close. Log return allows clean aggregation and makes growth comparisons natural.

Directional entropy . Inside the lookback we compute the proportion p of bars where r is positive. Binary entropy of p is high when the mix of up and down closes is balanced and low when one direction dominates. Intensity is one minus entropy. Directional sign is two times p minus one. The trend channel is zero point five plus one half times sign times intensity. It lives between zero and one and grows stronger as unanimity increases.

Convexity drift with drag . Arithmetic mean of r measures pace. Geometric mean of the price ratio over the window measures compounding. Drag is the positive part of arithmetic minus geometric. Drift raw equals geometric minus drag multiplier times drag. We then map drift through an arctangent normalizer scaled by AAR and a nonlinearity parameter so the result is stable and remains between zero and one.

Tail imbalance . AAR equals the average of the absolute value of r in the window. We count up tails where r is greater than aar_mult times AAR and down tails where r is less than minus aar_mult times AAR. The imbalance is their difference over their total, mapped to zero to one. This detects directional impulse flow.

Fusion and centering . A weighted average of the three channels yields the raw score. If a higher timeframe is requested, the same function is executed on that timeframe with lookahead off and blended with a weight. Finally we subtract a fraction of the rolling mean of the score to recover neutrality. The result is clipped to the zero to one band.

4. Entries, exits, and position sizing

Enter long when score is strictly greater than the entry gate. Enter short when score is strictly less than one minus the entry gate unless direction is restricted in inputs.

Exit a long when score falls below the exit gate. Exit a short when score rises above one minus the exit gate.

Thermo stops are expressed in AAR units. A long uses the maximum of an initial stop sized by the entry price and AAR and a trail stop that references the running high since entry with a separate multiple. Shorts mirror this with the running low. If the trail is disabled the initial stop is active.

Cooldown is a simple bar counter that begins when the position returns to flat. It prevents immediate re entry in churn.

Dynamic position size is optional. When enabled the order percent of equity scales between a floor and a cap as the score rises above the gate for longs or below the symmetric gate for shorts.

5. Inputs quick guide with recommended ranges

Every input has a tooltip in the script. The same guidance appears here for fast reading.

Core window . Shared lookback for entropy, drift, and tails. Start near 80 on daily charts. Try 60 to 120 on intraday and 80 to 200 for swing.

Entry threshold . Typical range 0.55 to 0.65 for trend following. Faster entries 0.50 to 0.55.

Exit threshold . Typical range 0.35 to 0.50. Lower holds longer yet gives back more.

Weight directional entropy . Starting value 0.40. Raise on markets with clean persistence.

Weight convexity drift . Starting value 0.40. Raise when compounding quality is critical.

Weight tail imbalance . Starting value 0.20. Raise on breakout prone markets.

Tail threshold vs AAR . Typical range 1.0 to 1.5 to count decisive bursts.

Drag penalty . Typical range 0.25 to 0.75. Higher punishes chop more.

Nonlinearity scale . Typical range 0.8 to 2.0. Larger compresses extremes.

AAR floor in percent . Typical range 0.0005 to 0.002 for liquid instruments. This stabilizes the math during quiet regimes.

Adaptive centering . Keep on for most symbols. Center strength 0.40 to 0.70.

Confirm timeframe optional . Leave empty to disable. If used, try a multiple between three and five of the chart timeframe with a blend weight near 0.20.

Dynamic position size . Enable if you want size to reflect certainty. Floor and cap define the percent of equity band. A practical band for many accounts is 0.5 to 2.

Cooldown bars after exit . Start at 3 on daily or slightly higher on shorter charts.

Thermo stop multiple . Start between 1.5 and 3.0 on daily. Adjust to your tolerance and symbol behavior.

Thermo trailing stop and Trail multiple . Trail on locks gains earlier. A trail multiple near 1.0 to 2.0 is common. You can keep trail off and let the exit gate handle exits.

Background heat opacity . Cosmetic. Set to taste. Zero disables it.

6. Properties used on the published chart

The example publication uses BTCUSD on the daily timeframe. The following Properties and inputs are used so everyone can reproduce the same results.

Initial capital 100000

Base currency USD

Order size 2 percent of equity coming from our risk management inputs.

Pyramiding 0

Commission 0.05 percent

Slippage 10 ticks in the publication for clarity. Users should introduce slippage in their own research.

Recalculate after order is filled off. On every tick off.

Using bar magnifier on. On bar close on.

Risk inputs on the published chart. Dynamic position size on. Size floor percent 2. Size cap percent 2. Cooldown bars after exit 3. Thermo stop multiple 2.5. Thermo trailing stop off. Trail multiple 1.

7. Visual elements and alerts

The score is painted as a subtle dot rail near the bottom. A background heat map runs from red to green to convey regime strength at a glance. A compact HUD at the top right shows current score, the three component channels, the active AAR, and the remaining cooldown. Four alerts are included. Long Setup and Short Setup on entry gates. Exit Long by Score and Exit Short by Score on exit gates. You can disable trading and use alerts only if you want the score as a risk switch inside a discretionary plan.

8. How to reproduce the example

Open a BTCUSD daily chart with regular candles.

Add the strategy and load the defaults that match the values above.

Set Properties as listed in section 6.(they are set by default) Confirm that bar magnifier is on and process on bar close is on.

Run the Strategy Tester. Confirm that the trade count is reasonable for the sample. If the count is too low, slightly lower the entry threshold or extend history. If the count is excessively high, raise the threshold or add a small cooldown.

9. Practical tuning recipes

Trend following focus . Raise the entry threshold toward 0.60. Raise the trend weight to 0.50 and reduce tail weight to 0.15. Keep drift near 0.35 to retain the growth filter. Consider leaving the trail off and let the exit threshold manage positions.

Breakout focus . Keep entry near 0.55. Raise tail weight to 0.35. Keep aar_mult near 1.3 so only decisive bursts count. A modest cooldown near 5 can reduce immediate false flips after the first burst bar.

Chop defense . Raise drag multiplier to 0.70. Raise exit threshold toward 0.48 to recycle capital earlier. Consider a higher cooldown, for example 8 to 12 on intraday.

Higher timeframe blend . On a daily chart try a weekly confirm with a blend near 0.20. On a five minute chart try a fifteen minute confirm. This moderates transitions.

Sizing discipline . If you want constant position size, set floor equal to cap. If you want certainty scaling, set a band like 0.5 to 2 and monitor drawdown behavior before widening it.

10. Strengths and limitations

Strengths

Self scaling unit through AAR makes the tool portable across markets and timeframes.

Blends evidence that target different failure modes. Unanimity, growth quality, and impulse flow rarely agree by chance which raises confidence when they align.

Adaptive centering reduces structural bias at the score level which helps during regime flips.

Limitations

In very quiet regimes AAR becomes small even with a floor. If your symbol is thin or gap prone, raise the floor a little to keep stops and drift mapping stable.

Adaptive centering can delay early breakout acceptance. If you miss starts, lower center strength or temporarily disable centering while you evaluate.

Tail counting uses a fixed multiple of AAR. If a market alternates between very calm and very violent weeks, a single aar_mult may not capture both extremes. Sweep this parameter in research.

The engine reacts to realized structure. It does not anticipate scheduled news or liquidity shocks. Use event awareness if you trade around releases.

11. Realism and responsible publication

No promises or projections of performance are made. Past results never guarantee future outcomes.

Commission is set to 0.05 percent per round which is realistic for many crypto venues. Adjust to your own broker or exchange.

Slippage is set at 10 in the publication . Introduce slippage in your own tests or use a percent model.

Position size should respect sustainable risk envelopes. Risking more than five to ten percent per trade is rarely viable. The example uses a fixed two percent position size.

Security calls use lookahead off. Standard candles only. Non standard chart types like Heikin Ashi or Renko are not supported for strategies that submit orders.

12. Suggested research workflow

Begin with the balanced defaults. Confirm that the trade count is sensible for your timeframe and symbol. As a rough guide, aim for at least one hundred trades across a wide sample for statistical comfort. If your timeframe cannot produce that count, complement with multiple symbols or run longer history.

Sweep entry and exit thresholds on a small grid and observe stability. Stability across windows matters more than the single best value.

Try one higher timeframe blend with a modest weight. Large weights can drown the signal.

Vary aar_mult and drag_mult together. This tunes the aggression of breakouts versus defense in chop.

Evaluate whether dynamic size improves risk adjusted results for your style. If not, set floor equal to cap for constancy.

Walk forward through disjoint segments and inspect results by regime. Bootstrapping or segmented evaluation can reveal sensitivity to specific periods.

13. How to read the HUD and heat map

The HUD presents a compact view. Score is the current fused value. Trend is the directional entropy channel. Drift is the compounding quality channel. Tail is the burst flow channel. AAR is the current unit that scales stops and the drift map. CD is the cooldown counter. The background heat is a visual aid only. It can be disabled in inputs. Green zones near the upper band show alignment among the channels. Muted colors near the mid band show uncertainty.

14. Frequently asked questions

Can I use this as a pure indicator . Yes. Disable entries by restricting direction to one side you will not trade and use the alerts as a regime switch.

Will it work on intraday charts . Yes. The AAR unit scales with bar size. You will likely reduce the core window and increase cooldown slightly.

Should I enable the adaptive trail . If you wish to lock gains sooner and accept more exits, enable it. If you prefer to let the exit gate do the heavy lifting, keep it off.

Why do I sometimes see a green background without a position . Heat expresses the score. A position also depends on threshold comparisons, direction mode, and cooldown.

Why is Order size set to one hundred percent if dynamic size is on . The script passes an explicit quantity percent on each entry. That explicit quantity overrides the property. The property is kept at one hundred percent to avoid confusion when users later disable dynamic sizing.

Can I combine this with other tools on my chart . You can, yet for publication the chart is kept clean so users and moderators can see the output clearly. In your private workspace feel free to add other context.

15. Concepts glossary

AAR . Average absolute return across the lookback. Serves as a unit for tails, drift scaling, and stops.

Directional entropy . A measure of uncertainty of up versus down closes. Low entropy paired with a directional sign signals unanimity.

Geometric mean growth . Rate that preserves the effect of compounding over many bars.

Drag . The positive difference between arithmetic pace and geometric growth. Larger drag often signals churn that looks active but fails to compound.

Thermo stops . Stops expressed in the same AAR unit as the signal. They adapt with volatility and keep risk and signal on a common scale.

Adaptive centering . A bias correction that recenters the fused score around neutral so the meter does not drift due to persistent skew.

16. Educational notice and risk statement

Markets involve risk. This publication is for education and research. It does not provide financial advice and it is not a recommendation to buy or sell any instrument. Use realistic costs. Validate ideas with out of sample testing and with conservative position sizing. Past performance never guarantees future results.

17. Final notes for readers and moderators

The goal of this strategy is clarity and portability. Clarity comes from a single score that reflects three independent features of the tape. Portability comes from self scaling units that respect structure across assets and timeframes. The publication keeps the chart clean, explains the math plainly, lists defaults and Properties used, and includes warnings where care is required. The code is protected so the implementation remains consistent for the community while the description remains complete enough for users to understand its purpose and for moderators to evaluate originality and usefulness. If you explore variants, keep them self contained, explain exactly what they contribute, publish in English first, and treat others with respect in the comments.

Load the strategy on BTCUSD daily with the defaults listed above and study how the score transitions across regimes. Then adjust one lever at a time. Observe how the trend channel, the drift channel, and the tail channel interact during starts, pauses, and reversals. Use the alerts as a risk switch inside your own process or let the built in entries and exits run if you prefer an automated study. The intent is not to promise outcomes. The intent is to give you a robust meter for regime strength that travels well across markets and helps you structure decisions with more confidence.

Thank you for your time to read all of this

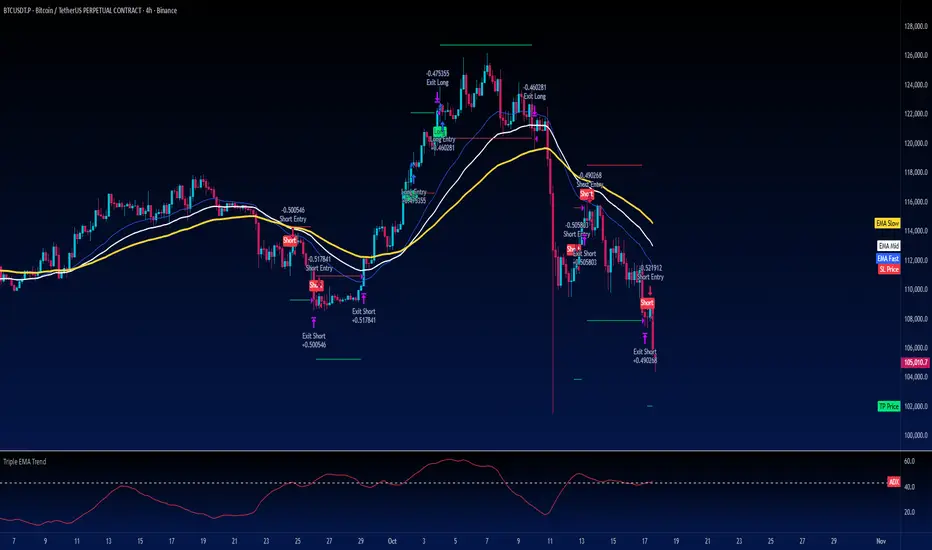

Turtle Strategy - Triple EMA Trend with ADX and ATRDescription

The Triple EMA Trend strategy is a directional momentum system built on the alignment of three exponential moving averages and a strong ADX confirmation filter. It is designed to capture established trends while maintaining disciplined risk management through ATR-based stops and targets.

Core Logic

The system activates only under high-trend conditions, defined by the Average Directional Index (ADX) exceeding a configurable threshold (default: 43).

A bullish setup occurs when the short-term EMA is above the mid-term EMA, which in turn is above the long-term EMA, and price trades above the fastest EMA.

A bearish setup is the mirror condition.

Execution Rules

Entry:

• Long when ADX confirms trend strength and EMA alignment is bullish.

• Short when ADX confirms trend strength and EMA alignment is bearish.

Exit:

• Stop Loss: 1.8 × ATR below (for longs) or above (for shorts) the entry price.

• Take Profit: 3.3 × ATR in the direction of the trade.

Both parameters are configurable.

Additional Features

• Start/end date inputs for controlled backtesting.

• Selective activation of long or short trades.

• Built-in commission and position sizing (percent of equity).

• Full visual representation of EMAs, ADX, stop-loss, and target levels.

This strategy emphasizes clean trend participation, strict entry qualification, and consistent reward-to-risk structure. Ideal for swing or medium-term testing across trending assets.

Fury by Tetrad Fury by Tetrad

What it is:

A rules-based Bollinger+RSI strategy that fades extremes: it looks for price stretching beyond Bollinger Bands while RSI confirms exhaustion, enters countertrend, then exits at predefined profit multipliers or optional stoploss. “Ultra Glow” visuals are purely cosmetic.

How it works — logic at a glance

Framework: Classic Bollinger Bands (SMA basis; configurable length & multiplier) + RSI (configurable length).

Long entries:

Price closes below the lower band and RSI < Long RSI threshold (default 28.3) → open LONG (subject to your “Market Direction” setting).

Short entries:

Price closes above the upper band and RSI > Short RSI threshold (default 88.4) → open SHORT.

Profit exits (price targets):

Uses simple multipliers of the strategy’s average entry price:

Long exit = `entry × Long Exit Multiplier` (default 1.14).

Short exit = `entry × Short Exit Multiplier` (default 0.915).

Risk controls:

Optional pricebased stoploss (disabled by default) via:

Long stop = `entry × Long Stop Factor` (default 0.73).

Short stop = `entry × Short Stop Factor` (default 1.05).

Directional filter:

“Market Direction” input lets you constrain entries to Market Neutral, Long Only, or Short Only.

Visuals:

“Ultra Glow” draws thin layered bands around upper/basis/lower; these do not affect signals.

> Note: Inputs exist for a timebased stop tracker in code, but this version exits via targets and (optional) price stop only.

Why it’s different / original

Explicit extreme + momentum pairing: Entries require simultaneous band breach and RSI exhaustion, aiming to avoid entries on gardenvariety volatility pokes.

Deterministic exits: Multiplier-based targets keep results auditable and reproducible across datasets and assets.

Minimal, unobtrusive visuals: Thin, layered glow preserves chart readability while communicating regime around the Bollinger structure.

Inputs you can tune

Bollinger: Length (default 205), Multiplier (default 2.2).

RSI: Length (default 23), Long/Short thresholds (28.3 / 88.4).

Targets: Long Exit Mult (1.14), Short Exit Mult (0.915).

Stops (optional): Enable/disable; Long/Short Stop Factors (0.73 / 1.05).

Market Direction: Market Neutral / Long Only / Short Only.

Visuals: Ultra Glow on/off, light bar tint, trade labels on/off.

How to use it

1. Timeframe & assets: Works on any symbol/timeframe; start with liquid majors and 60m–1D to establish baseline behavior, then adapt.

2. Calibrate thresholds:

Narrow/meanreverting markets often tolerate tighter RSI thresholds.

Fast/volatile markets may need wider RSI thresholds and stronger stop factors.

3. Pick realistic targets: The default multipliers are illustrative; tune them to reflect typical mean reversion distance for your instrument/timeframe (e.g., ATRinformed profiling).

4. Risk: If enabling stops, size positions so risk per trade ≤ 1–2% of equity (max 5–10% is a commonly cited upper bound).

5. Mode: Use Long Only or Short Only when your discretionary bias or higher timeframe model favors one side; otherwise Market Neutral.

Recommended publication properties (for backtests that don’t mislead)

When you publish, set your strategy’s Properties to realistic values and keep them consistent with this description:

Initial capital: 10,000 (typical retail baseline).

Commission: ≥ 0.05% (adjust for your venue).

Slippage: ≥ 2–3 ticks (or a conservative pertrade value).

Position sizing: Avoid risking > 5–10% equity per trade; fixedfractional sizing ≤ 10% or fixedcash sizing is recommended.

Dataset / sample size: Prefer symbols/timeframes yielding 100+ trades over the tested period for statistical relevance. If you deviate, say why.

> If you choose different defaults (e.g., capital, commission, slippage, sizing), explain and justify them here, and use the same settings in your publication.

Interpreting results & limitations

This is a countertrend approach; it can struggle in strong trends where band breaches compound.

Parameter sensitivity is real: thresholds and multipliers materially change trade frequency and expectancy.

No predictive claims: Past performance is not indicative of future results. The future is unknowable; treat outputs as decision support, not guarantees.

Suggested validation workflow

Try different assets. (TSLA, AAPL, BTC, SOL, XRP)

Run a walkforward across multiple years and market regimes.

Test several timeframes and multiple instruments. (30m Suggested)

Compare different commission/slippage assumptions.

Inspect distribution of returns, max drawdown, win/loss expectancy, and exposure.

Confirm behavior during trend vs. range segments.

Alerts & automation

This release focuses on chart execution and visualization. If you plan to automate, create alerts at your entry/exit conditions and ensure your broker/venue fills reflect your slippage/fees assumptions.

Disclaimer

This script is provided for educational and research purposes. It is not investment advice. Trading involves risk, including the possible loss of principal. © Tetrad Protocol.

Solana 4H RSI->MACD — Counter-Trend By TetradTetrad RSI→RSI Cross→MACD (Sequenced) — Counter-Trend (SL-Only)

Category: Market-neutral, counter-trend, sequenced entries

Timeframe default: Works on any TF; designed around 4H On Solana

Markets: Any (spot, perp, futures); parameterize to your asset

What it does

This strategy hunts reversals using a 3-step sequence on RSI and MACD, then optionally restricts entries by market regime and a price gate. It shows stop-loss lines only when hit (clean chart), and paints a Donchian glow for quick read of backdrop conditions.

Entry logic (sequenced)

1. RSI Extreme:

Long path activates when RSI < Oversold (default 27.5).

Short path activates when RSI > Overbought (default 74).

2. RSI Cross confirmation:

Long path: RSI crosses up back above the oversold level.

Short path: RSI crosses down back below the overbought level.

Each step has a max bar lookback so stale signals time out.

3. MACD Cross trigger:

Long: MACD line crosses above Signal.

Short: MACD line crosses below Signal.

→ When step 3 fires and gates are satisfied, a trade is entered.

Optional gates & filters

Regime Filter (Counter-Trend):

Longs allowed in **Range / Short Trend / Short Parabolic** regimes.

Shorts allowed in **Range / Long Trend / Long Parabolic** regimes.

Based on ADX/DI and ATR% intensity.

* Price Gate (Long Ceiling):

Toggle to **disable new longs above a chosen price (default 209.0 For SOL).

Useful for assets like SOL where you want longs only below a cap.

Exits / Risk

* Stop-Loss (% of entry):** default **14%**, toggleable.

* SL visualization:** plots a **thin dashed red line only on the bar it’s hit**.

* (No take-profit or time-based exit in this version—keep it pure to the sequence and regime. Add TP/time exits if desired.)

Visuals

* Donchian Glow (50): background band only (upper/lower lines hidden).

* Regime HUD: compact table (top-right) highlighting the active regime.

* Minimal marks: no entry/exit “arms” clutter; only SL-hit lines render.

Inputs (key)

* Core: RSI Length, Oversold/Overbought, MACD Fast/Slow/Signal.

* Sequence: Max bars from Extreme→RSI Cross and RSI Cross→MACD Cross.

* Regime: ADX Length, Trend/Parabolic thresholds, ATR length & floor.

* Stops: Enable/disable; SL %.

* Price Gate: Enable; Long ceiling price.

Alerts

Sequenced Long (CT): RSIhigh → RSI cross down → MACD bear cross.

## Notes & Tips

Designed for counter-trend fades that become trend rides. The regime filter helps avoid fading true parabolics and aligns entries with safer contexts.

The sequence is stateful (steps must occur in order). If a step times out, the path resets.

Works on lower TFs, but the 4H baseline reduces noise and over-trading.

Consider pairing with volume or structure filters if you want fewer but higher-conviction entries.

Past performance ≠ future results. **Educational use only. Not financial advice.

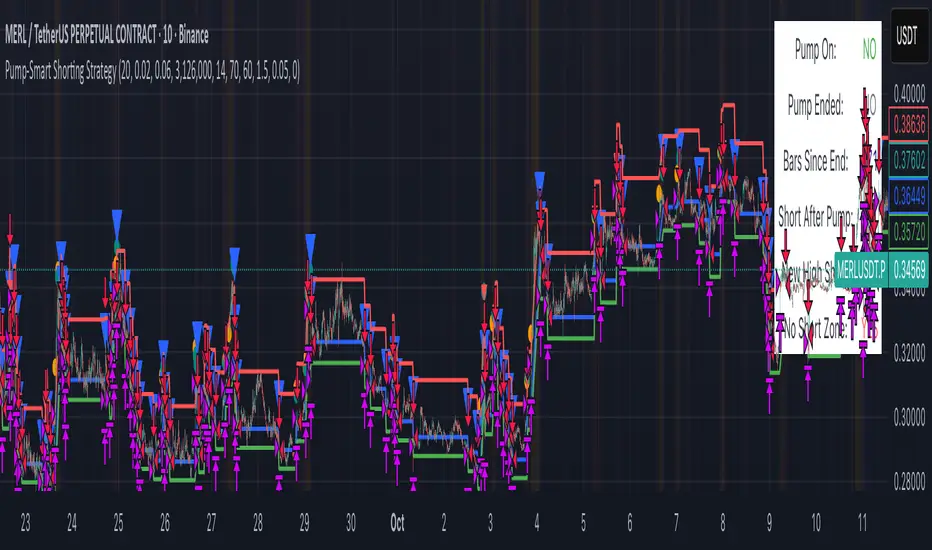

Pump-Smart Shorting StrategyThis strategy is built to keep your portfolio hedged as much as possible while maximizing profitability. Shorts are opened after pumps cool off and on new highs (when safe), and closed quickly during strong upward moves or if stop loss/profit targets are hit. It uses visual overlays to clearly show when hedging is on, off, or blocked due to momentum, ensuring you’re protected in most market conditions but never short against the pump. Fast re-entry keeps the hedge active with minimal downtime.

Pump Detection:

RSI (Relative Strength Index): Calculated over a custom period (default 14 bars). If RSI rises above a threshold (default 70), the strategy considers the market to be in a pump (strong upward momentum).

Volume Spike: The current volume is compared to a 20-bar simple moving average of volume. If it exceeds the average by 1.5× and price increases at least 5% in one bar, pump conditions are triggered.

Price Jump: Measured by (close - close ) / close . A single-bar change > 5% helps confirm rapid momentum.

Pump Zone (No Short): If any of these conditions is true, an orange or red background is shown and shorts are blocked.

Cooldown and Re-Entry:

Cooldown Detection: After the pump ends, RSI must fall below a set value (default ≤ 60), and either volume returns towards average or price momentum is less than half the original spike (oneBarUp <= pctUp/2).

barsWait Parameter: You can specify a waiting period after cooldown before a short is allowed.

Short Entry After Pump/Cooldown: When these cooldown conditions are met, and no short is active, a blue background is shown and a short position is opened at the next signal.

New High Entry:

Lookback New High: If the current high is greater than the highest high in the last N bars (default 20), and pump is NOT active, a short can be opened.

Take Profit (TP) & Stop Loss (SL):

Take Profit: Short is closed if price falls to a threshold below the entry (minProfitPerc, default 2%).

Stop Loss: Short is closed if price rises to a threshold above the entry (stopLossPerc, default 6%).

Preemptive Exit:

Any time a pump is detected while a short position is open, the strategy closes the short immediately to avoid losses.

Visual Feedback:

Orange Background: Market is pumping, do not short.

Red Background: Other conditions block shorts (cooldown or waiting).

Blue Background: Shorts allowed.

Triangles/Circles: Mark entries, pump start/end, for clear trading signals.

ATR + VIX Breakout StrategyChange the symbol to UVXY. Work great for option l long and S short. Take profits before it closes the trade. Pls remember you are using it at your own risk.

DK Fractals (Strategy)Convert to strategy. Introduce the first 2 trading models (Still heavily in development) The reversal and continuation models. More to come.

If you still want to use as an indicator, just disable the two trading models.

Moon Phases Long/Short StrategyThis is an experiment of Moon Phases, likely buy when full moon and sell when new moon with few changes, like it would buy a day ahead or sometimes sell a day post these events, with Stop loss and take profits, 50% profitable so sounds good to me

Long only good for bitcoin gold, both modes(L+S) better for stocks and alt coins

SPY200SMA (+4%/-3%) TQQQ/QQQ STRATEGYSummary of the Improved Strategy: When the price of AMEX:SPY is +4% above the 200SMA BUY NASDAQ:TQQQ and when the price of SPY drops to -3% under the SPY 200SMA SELL everything and slowly DCA into NASDAQ:QQQ over the next 6-12 months or until price returns to +4% above the SPY 200SMA at which point you will go back into 100% TQQQ.

Note: (if the price of QQQ goes 30% above the 200SMA of QQQ deleverage to QQQ or Sell to protect yourself from dot com level event)

More info and stats -https://www.reddit.com/r/LETFs/comments/1nhye66/spy_200sma_43_tqqqqqq_long_term_investment/

超趨勢策略 (中文)-Caelusif ta.change(direction) < 0

strategy.entry("My Long Entry Id", strategy.long)

if ta.change(direction) > 0

strategy.entry("My Short Entry Id", strategy.short)