Multi-Asset % Performance Table | v2.1 | TCP Multi-Asset % Performance Table | v2.1 | TCP

ESSENTIAL SUMMARY:

Multi-Asset % Performance Table eliminates the need to manually draw and manage individual "Price Range" tools for every asset. It automatically tracks up to 15 tickers independently in a single dashboard, calculating a TOTAL SCORE (Portfolio Average) for you. Unlike manual drawings, it supports a Global Range while allowing Custom Dates for specific assets, ensuring each ticker is calculated based on its own precise entry/exit. The Smart Visuals dynamically draw the correct date lines only for the ticker you are currently viewing, keeping your chart automatic, accurate, and clutter-free.

FUL DESCRIPTION:

📊 What is this tool?

The Multi-Asset % Performance Table is a powerful portfolio dashboard designed to track the percentage performance of up to 15 different assets simultaneously.

Instead of checking tickers one by one or manually drawing price ranges, this indicator aggregates everything into a single, clean table. It allows you to compare the ROI (Return on Investment) of a basket of coins or stocks over a specific time period and calculates an aggregate TOTAL SCORE (Average %) for your selection.

🚀 Key Features

15 Asset Slots: Monitor up to 15 different tickers (Crypto, Stocks, Forex, etc.) in one view.

Global vs. Custom Dates: Set a "Global" start/end date for the whole portfolio, but override specific assets with Custom Dates if they entered the portfolio at a different time.

Smart Visuals: Automatically draws vertical dashed lines on your chart representing the start and end dates of the ticker you are currently viewing.

Total Score Calculation: Calculates the average percentage change of your portfolio. You can dynamically include or exclude specific assets from this average using the settings.

Status Column: A quick visual reference (✔ or ✘) in the table showing which assets are currently included in the Total Score calculation.

⚙️ How it Works

Data Fetching: The script pulls "Close" prices from the Daily timeframe to ensure accuracy across long periods.

Smart Matching: The visual lines automatically detect which asset you are viewing. For example, if you are looking at BTCUSDT and have custom dates set for it, the vertical lines will jump to those specific dates. If you view a ticker not in your list, it defaults to the Global dates.

Visual Protection: The script uses advanced logic to ensure only one set of range lines appears on the chart at a time, keeping your workspace clean.

🛠️ Instructions & Settings

1. Setting up your Assets

Open the Settings (Cogwheel icon).

Under ASSET 1 through ASSET 15, enter the tickers you want to track (e.g., BINANCE:BTCUSDT).

Include in Avg?: Uncheck this if you want to see the asset in the table but exclude it from the "TOTAL SCORE" average.

2. Defining Time Ranges

Global Settings: Set the Global Start and Global End dates at the top. This applies to all assets by default.

Custom Dates: If a specific asset (e.g., Asset 4) was bought on a different day, check the "Custom Dates?" box for that asset and enter its specific Start/End time.

3. Reading the Table

The table appears on the chart (default: Bottom Right) with three columns:

Asset: The name of the ticker.

% Change: The percentage move from Start Date to End Date. (Green = Positive, Red = Negative).

Inc: Shows a ✔ if the asset is included in the Total Score average, or a ✘ if excluded.

4. The Visual Lines

Two vertical dashed lines will appear on your chart.

Note: These lines are visual references only. You cannot drag them to change the dates. To change the dates, you must use the Settings menu.

💡 Tips

Hover for Details: Hover your mouse over the % Change value in the table to see a tooltip showing the exact Start Price and End Price used for the calculation.

Resolution: The script defaults to 1 Day resolution for optimal accuracy on historical data.

v2.1 | TCP - Custom Built for Precision Performance Tracking

Portfolio management

calculator contracts MNQ PIPEGAVTRADESThis is a Risk Management indicator that calculates the exact contracts to trade based on your defined Max Risk ($) and Stop Loss Ticks.

It displays all key Position Sizing metrics (including Account Capital and Risk %) in a fixed table on the chart.

TernTable: Crypto SectorsTernTables:CryptoSecs

This was hung on my Sector ETFs script to see if I could filter some noise from crypto by applying a GICS (Global Industry Classification Standard) style sector model to the crypto markets.

Crypto classification is certainly a little more nuanced so not completely straightforward.

It was designed to filter a researched and organised view of generally recognised cryptocurrency sectors and their confirmed constituent components.

The main purpose was a shot at displaying live crypto market data on my chart with instantaneous visual analysis, using leader laggard colour logic for performance indication, plus bullish bearish colour logic using the header for instant visual sector strength analysis.

This was never going to be an exhaustive tool of course and amazingly only or two of the sector lists wont fit on your laptop screen without zooming but it’s UI versatility both in custom display and custom threshold functionality is very effective. Viewing a coin on your watchlist with its sector overlayed in the chart brings the optional visual alert function into consideration. All basic but all effective and all customisable

Can't ignore the educational value either it’s teaching by osmosis what the sectors do and which coins go where clues to why.

As an after thought - I added a live stock market filter for 20 sector-specific ETFs like SPY, QQQ, XLV, XLF, allowing the comparison of the live performance of traditional financial sectors to live crypto sector data without leaving your chart.

Not certain how often it will need to be updated and any feedback re the legitimacy and accuracy of its components is kindly welcomed it is up to date at date of publishing.

It’s pretty easy to use, here is a list what you're getting with sector classifications with brief descriptions

CMC 20

CoinMarketCap Top 20: the largest cryptos by market cap. Great starting point to see what the overall market is doing

ETFs

All major U.S.-listed Bitcoin & Ethereum ETFs. Lets you compare crypto performance directly with traditional finance

Layer 0

Foundational interoperability protocols (Polkadot, Cosmos, ICP, etc.). These are the “bridges” that allow different blockchains to communicate

Layer 1

Independent base-layer blockchains that run their own consensus and security (Bitcoin, Ethereum, Solana, Cardano, TON, etc.).

Layer 2

Scaling networks built on top of Layer 1s to increase speed and lower fees (Arbitrum, Optimism, Base, Polygon, zk-rollups, etc.)

Layer 3

Application-specific chains or rollups designed for one purpose (gaming chains, DeFi-specific, social, etc.)

Web3

The “ownership internet”: gaming tokens, NFTs, metaverse land, music/streaming platforms, social tokens, and creator-economy projects

DeFi

Decentralised Finance: lending platforms, decentralized exchanges, derivatives, yield aggregators, and insurance protocols

Decentralised Storage

Blockchain-based alternatives to AWS/Google Cloud (Filecoin, Arweave, Storj, etc.)

Oracles

Data providers that feed off-chain information (prices, weather, sports results) into smart contracts

Privacy

Privacy coins and protocols that obfuscate transaction details (Monero, Zcash, Beam, etc.)

Yield & Lending

Protocols focused purely on lending, borrowing, and yield generation

DEX

Pure decentralized exchanges (Uniswap, SushiSwap, Jupiter, GMX, etc.)

DAO

Governance tokens of major decentralized autonomous organizations (Maker, Lido, Aave, ENS, etc.)

Infrastructure / Middleware

The picks-and-shovels layer: node services, RPC providers, indexing, cross-chain bridges, etc

Real World Assets (RWA)

Tokenised traditional assets: treasuries, real estate, private credit, stablecoins backed by real-world collateral

Restaking & Liquid Restaking

EigenLayer ecosystem and liquid-restaking tokens (eigen, ether.fi, Pendle, etc.). Currently the fastest-growing narrative

Traditional Sector ETFs

Classic U.S. sector ETFs (SPY, QQQ, XLF, XLE, XLV, XLY, etc.). Extra layer of analysis by comparing live stock market conditions with livecrypto market conditions

A list of the UI Toggles

* Sector Dropdown

• Select Sector: Choose the sector to display (e.g., CMC 20, Layer 1, DeFi, etc.)

* Custom Tickers

• Enter Tickers: Input custom coin tickers (e.g., BTCUSD, ETHUSD) to track specific assets

* Show % Change Row

• Toggle On/Off: Display the % change row for each sector/coin

* Show Current Price Row

• Toggle On/Off: Display the current price for each sector/coin

* Show Price-Diff Row

• Toggle On/Off: Display the price difference (current price - previous day's price)

* Show Spacer Row

• Toggle On/Off: Add a spacer row between data rows for clarity

* Table Position

• Select Position: Choose the position of the data table on your chart (Top Left, Top Right, etc.)

Visual Options:

* Show Sector Name

• Toggle On/Off: Display the sector name pane label on chart

* Custom Bull/Bear Threshold

• Toggle On/Off: Set a custom threshold for bullish/bearish sector performance

• Threshold (%): Set the percentage threshold (e.g., 50%) for bullish/bearish classification

* Show Live % in Header

• Toggle On/Off: Display the live percentage change in the table header

* Dynamic Decimal Formatting

• Toggle On/Off: Enable dynamic formatting for numbers display.

* Sort by % Change

• Toggle On/Off: Sort sectors by % change in performance

* Enable Alerts

• Toggle On/Off: Enable alerts based on performance thresholds

* Alert Threshold (%)

• Set Threshold: Define the percentage threshold (e.g.,70%) for triggering alerts

* Cooldown (bars)

• Toggle On/Off: Enable cooldown to prevent alerts from triggering too quickly

• Cooldown Duration: Set the cooldown period in bars (e.g., 10 bars)

* % Threshold Mode

• Toggle On/Off: Enable % Threshold Mode to filter sectors based on a percentage change threshold

• Threshold %: Set the percentage for filtering sectors (e.g., only show sectors with > 5% change)

A lot of toggles probably left once favourites are set but this UI interface does allow experimentation with the utility of channelling raw live data through custom designed filters. Just saying !

I need to include this of course

This indicator provides sector-based organisation and real-time performance visualisation for cryptocurrencies. It is not intended to predict price movements or guarantee outcomes. Crypto assets carry significant risk, including loss of capital. Past performance does not guarantee future results. All data and sector classifications are best-effort and may be incomplete, inaccurate, or outdated. Nothing in this script should be interpreted as financial advice. You are solely responsible for your own trading decisions.

That’s it really, I am currently pleased with how this indicator turned out, if you have a crypto trading toolkit put this in it.

ICT/SMC DOL Detector PRO (Final)This indicator is designed to operate only on the 1-hour timeframe.

The ICT/SMC DOL Detector PRO is an educational indicator designed to identify and visualize Draw on Liquidity (DOL) levels across multiple time-frames. It tracks unmitigated daily highs and lows, clusters them into zones, and calculates confidence scores based on multiple factors including time decay, cluster size, and time-frame alignment.

This indicator is based on ICT (Inner Circle Trader) concepts and liquidity theory, which suggests that price tends to seek out areas of concentrated unfilled orders before reversing or continuing its trend.

What is a DOL (Draw on Liquidity)?

A Draw on Liquidity represents a daily high or low that has not been revisited (mitigated) by price. These levels act as "magnets" that draw price toward them because:

1. They represent untapped liquidity pools where unfilled orders exist

2. Market makers and institutions often target these levels to fill large orders

3. Price is drawn to these zones to clear pending orders

4. They can serve as potential reversal or continuation zones once liquidity is taken

Methodology

1. Level Tracking

The indicator monitors daily session highs and lows on the 1-hour time-frame, tracking:

- Session high price and time of formation

- Session low price and time of formation

- Whether each level has been breached (mitigated)

- Time elapsed since level formation

2. Clustering Algorithm

Unmitigated levels within a defined tolerance (default 0.5% of price) are grouped together to identify zones where multiple DOLs cluster. Larger clusters indicate stronger liquidity pools.

3. Confidence Scoring (The "AI" Logic)

Each DOL receives a confidence score (0-100%) based on three weighted factors. This is the core "AI" intelligence of the indicator:

**Factor 1: Cluster Size (50% weight)**

- Counts how many unmitigated levels exist within 0.5% of the price zone

- Formula: (levels_in_cluster / total_unmitigated_levels) × 50

- Logic: More unfilled orders clustered together = stronger liquidity pool = higher confidence

- Example: If 5 out of 10 total unmitigated levels cluster at 27,500, cluster score = (5/10) × 50 = 25%

**Factor 2: Time Decay (25% weight)**

- Calculates age of the level since formation

- Fresh levels (< 1 week old): Full 25% score

- Aging penalty: Loses 5% per week of age

- Maximum penalty: 25% (very old levels = 0% time score)

- Formula: max(0, 25 - (weeks_old × 5))

- Logic: Recent liquidity is more relevant than old liquidity that price has ignored for months

**Factor 3: Timeframe Alignment (25% weight)**

- Checks how many timeframes (1H, 4H, D1, W1) point in the same direction

- If multiple timeframes identify DOLs on the same side (all bullish or all bearish): Higher score

- If mixed signals: Lower score

- Formula: (aligned_timeframes / total_timeframes) × 25

- Logic: When multiple timeframes agree, the liquidity zone is validated across different time perspectives

**Total Confidence Score:**

```

Confidence = Cluster_Score + Time_Score + Alignment_Score

= (0-50%) + (0-25%) + (0-25%)

= 0-100%

```

**Example Calculation:**

```

DOL at 27,500:

- 6 out of 12 unmitigated levels cluster here → (6/12) × 50 = 25%

- Level is 2 weeks old → 25 - (2 × 5) = 15%

- 3 out of 4 timeframes bullish toward this level → (3/4) × 25 = 18.75%

- Total Confidence = 25% + 15% + 18.75% = 58.75% ≈ 59%

```

This mathematical approach removes subjectivity and provides objective, data-driven confidence scoring.

4. Multi-Timeframe Analysis

The indicator analyzes DOLs across four timeframes:

- **1H:** Intraday levels (fastest reaction)

- **4H:** Short-term swing levels

- **Daily:** Intermediate-term levels

- **Weekly:** Long-term structural levels

For each timeframe, it identifies:

- Highest confidence unmitigated high

- Highest confidence unmitigated low

- Directional bias (bullish if high > low confidence, bearish if low > high confidence)

5. Primary DOL Selection (AI Auto-Selection Logic)

When "Show AI DOL" is enabled, the indicator uses an automated selection algorithm to identify the most important targets:

**Step 1: Collect All Candidates**

The algorithm gathers all identified DOLs from all timeframes (1H, 4H, D1, W1) that meet minimum criteria:

- Must be unmitigated (not yet swept)

- Must have confidence score > 0%

- Must have at least 1 level in cluster

**Step 2: Calculate Confidence for Each**

Each candidate DOL receives its confidence score using the three-factor formula described above (Cluster + Time + Alignment).

**Step 3: Sort by Confidence**

All candidates are ranked from highest to lowest confidence score.

**Step 4: Select Primary and Secondary**

- **P1 (Primary DOL):** The DOL with the absolute highest confidence score

- **P2 (Secondary DOL):** The DOL with the second highest confidence score

**Why This Matters:**

Instead of manually scanning multiple timeframes and guessing which level is most important, the AI objectively identifies the two highest-probability liquidity targets based on quantifiable data.

**Example AI Selection:**

```

Available DOLs:

- 1H High: 27,400

- 4H High: 27,500

- D1 High: 27,500 ← P1 (Highest)

- W1 High: 27,650 ← P2 (Second Highest)

- 1H Low: 26,800

- D1 Low: 26,500

AI Selection:

P1 = 27,500 (Daily High with 92% confidence)

P2 = 27,650 (Weekly High with 88% confidence)

```

This provides a data-driven target selection rather than subjective manual interpretation. The AI removes emotion and bias, selecting targets based purely on mathematical probability.

Features

Why "AI" DOL?

The term "AI" in this indicator refers to the automated algorithmic selection process, not machine learning or neural networks. Specifically:

**What the AI Does:**

- Automatically evaluates all available DOLs across all timeframes

- Applies a weighted scoring algorithm (Cluster 50%, Time 25%, Alignment 25%)

- Objectively ranks DOLs by probability

- Selects the top 2 highest-confidence targets (P1 and P2)

- Removes human bias and emotion from target selection

**What the AI Does NOT Do:**

- It does not use machine learning or train on historical data

- It does not predict future price movements

- It does not adapt or "learn" over time

- It does not guarantee accuracy

The "AI" is simply an automated decision-making algorithm that applies consistent mathematical rules to identify the most statistically significant liquidity zones. Think of it as a "smart filter" rather than artificial intelligence in the traditional sense.

Visual Components

**Daily Level Lines:**

- Green lines: Unmitigated (not yet breached) levels

- Red lines: Mitigated (already breached) levels

- Dots at origin point showing where level was formed

- X marker when level gets breached

- Lines extend forward to show projection

**DOL Labels:**

- Display timeframe (1H, 4H, D1, W1) or "DOL" for AI selection

- Show confidence percentage in brackets

- Color-coded by timeframe:

- Lime: AI DOL (Smart selection)

- Aqua: 1-hour timeframe

- Blue: 4-hour timeframe

- Purple: Daily timeframe

- Orange: Weekly timeframe

**Info Box (Top Right):**

Displays comprehensive liquidity metrics:

- Total levels tracked

- Active (unmitigated) levels count

- Cleared (mitigated) levels count

- Flow direction (BID PRESSURE / OFFER PRESSURE)

- Most recent sweep

- Primary and Secondary DOL targets

- Multi-timeframe bias analysis

- Overall directional bias

Settings Explained

**Daily Levels Group:**

- Show Daily Highs/Lows: Toggle visibility of all daily level tracking

- Unbreached Color: Color for levels not yet hit

- Breached Color: Color for levels that have been swept

- Show X on Breach: Display marker when level is breached

- Show Dot at Origin: Display marker at level formation point

- Line Width: Thickness of level lines (1-5)

- Line Extension: How many bars forward to project (1-24)

- Max Days to Track: Historical lookback period (5-200 days)

**DOL Settings Group:**

- Cluster Tolerance %: Price range to group DOLs (0.1-2.0%)

- Show Price on Labels: Display actual price value on labels

- Backtest Mode: Only show recent labels for clean historical analysis

- Labels Lookback: Number of bars to show labels when backtesting (10-500)

**Info Box Group:**

- Show Info Box: Toggle info panel visibility

**DOL Toggles Group:**

- Show AI DOL: Display smart auto-selected primary target

- Show 1HR DOL: Display 1-hour timeframe DOLs

- Show 4HR DOL: Display 4-hour timeframe DOLs

- Show Daily DOL: Display daily timeframe DOLs

- Show Weekly DOL: Display weekly timeframe DOLs

**Advanced Group:**

- Manual Mode: Simplified display showing only daily high/low clusters

How to Use This Indicator

Educational Application

This indicator is intended for educational purposes to help traders:

1. **Understand Liquidity Concepts:** Visualize where unfilled orders may exist

2. **Identify Key Levels:** See where price may be drawn to

3. **Analyze Market Structure:** Understand how price interacts with liquidity

4. **Study Multi-Timeframe Alignment:** Observe when multiple timeframes agree

5. **Learn ICT Concepts:** Apply liquidity theory in practice

Interpretation Guidelines

**BID PRESSURE (Flow):**

When lows are being swept more than highs, it suggests:

- Sell-side liquidity being taken

- Potential for upward move to unfilled buy-side liquidity

- Market may be clearing the way for a bullish move

**OFFER PRESSURE (Flow):**

When highs are being swept more than lows, it suggests:

- Buy-side liquidity being taken

- Potential for downward move to unfilled sell-side liquidity

- Market may be clearing the way for a bearish move

**Confidence Scores:**

- 90-100%: Very high probability zone (strong cluster, recent, aligned)

- 80-89%: High probability zone (good cluster, relatively recent)

- 70-79%: Moderate probability zone (decent cluster or older)

- 60-69%: Lower probability zone (small cluster or very old)

- Below 60%: Weak zone (minimal confluence)

**Timeframe Analysis:**

- All timeframes LONG: Strong bullish alignment

- All timeframes SHORT: Strong bearish alignment

- Mixed: Conflicting signals, exercise caution

- Higher timeframes (D1, W1) carry more weight than lower (1H, 4H)

**DIRECTIONAL Indicator:**

- BULLISH: Overall bias suggests upward movement toward buy-side DOLs

- BEARISH: Overall bias suggests downward movement toward sell-side DOLs

- NEUTRAL: No clear directional bias, conflicting signals

Practical Application Examples

**Example 1: Bullish Setup**

```

Flow: BID PRESSURE (lows being swept)

P1: 27,500 (price above current market)

D1: LONG 27,500

W1: LONG 27,650

DIRECTIONAL: BULLISH

```

Interpretation: Price has cleared sell-side liquidity. High confidence buy-side DOL at 27,500. Daily and Weekly timeframes aligned bullish. Watch for move toward 27,500 target.

**Example 2: Bearish Setup**

```

Flow: OFFER PRESSURE (highs being swept)

P1: 26,200 (price below current market)

D1: SHORT 26,200

W1: SHORT 26,100

DIRECTIONAL: BEARISH

```

Interpretation: Price has cleared buy-side liquidity. High confidence sell-side DOL at 26,200. Daily and Weekly timeframes aligned bearish. Watch for move toward 26,200 target.

**Example 3: Mixed Signals - Wait**

```

Flow: BID PRESSURE

P1: 26,800

D1: LONG 27,000

W1: SHORT 26,200

DIRECTIONAL: NEUTRAL

```

Interpretation: Conflicting signals. Flow suggests up, but Weekly bias is down. Confidence scores moderate. Better to wait for clarity.

Important Considerations

This Indicator Does NOT:

- Predict the future

- Guarantee profitable trades

- Provide buy/sell signals

- Replace proper risk management

- Work in isolation without other analysis

This Indicator DOES:

- Visualize liquidity concepts

- Identify potential target zones

- Show timeframe alignment

- Calculate objective confidence scores

- Help understand market structure

Proper Usage:

1. Use as one component of a complete trading strategy

2. Combine with price action analysis

3. Confirm with other technical indicators

4. Consider fundamental factors

5. Always use proper risk management

6. Backtest any strategy before live trading

Risk Disclaimer

**FOR EDUCATIONAL PURPOSES ONLY**

This indicator is for educational purposes only. Trading financial markets involves substantial risk of loss. Past performance does not guarantee future results. Always conduct your own research and consult with a financial advisor before making trading decisions.

**Important Limitations:**

- No indicator is 100% accurate, including the AI selection

- The "AI" is an automated algorithm, not predictive artificial intelligence

- DOL levels can be swept and price can continue in the same direction

- Confidence scores are mathematical calculations, not predictions or probabilities of success

- High confidence does not mean guaranteed profit

- Markets can remain irrational longer than you can remain solvent

- Always use stop losses and proper position sizing

**Understanding the AI Component:**

The AI auto-selection feature uses a fixed mathematical formula to rank DOLs. It does not:

- Predict where price will go

- Learn from past performance

- Adapt to market conditions

- Guarantee any level of accuracy

The confidence score represents the mathematical strength of a liquidity cluster based on objective factors (cluster size, recency, timeframe alignment), NOT a probability of the trade succeeding.

**Risk Warning:**

Trading is risky. Most traders lose money. This indicator cannot change that fundamental reality. Use it as an educational tool to understand market structure, not as a trading signal or system.

Technical Requirements

- **Timeframe:** Best used on 1-hour charts (required for accurate daily level tracking)

- **Markets:** Works on any market (forex, crypto, stocks, futures, indices)

- **Updates:** Real-time calculation on each bar close

- **Resources:** Uses max 500 lines and 500 labels (TradingView limits)

Backtesting Features

The indicator includes "Backtest Mode" to keep historical charts clean:

- When enabled, only shows labels from recent bars

- Adjustable lookback period (10-500 bars)

- All lines remain visible

- Helps review past setups without clutter

To use:

1. Enable "Backtest Mode" in settings

2. Adjust "Labels Lookback" to desired period

3. Review historical price action

4. Disable for live trading

Credits and Methodology

This indicator implements concepts from:

- ICT (Inner Circle Trader) liquidity theory

- Smart Money Concepts (SMC)

- Order flow analysis

- Multi-timeframe analysis principles

The clustering algorithm, confidence scoring, and timeframe synthesis are original implementations designed to quantify and visualize these concepts.

Version History

**v1.0 - Initial Release**

- Multi-timeframe DOL detection

- Confidence scoring system

- Info box with liquidity metrics

- Backtest mode for clean charts

- Black/white professional theme

Support and Updates

For questions, feedback, or suggestions, please use the TradingView comments section. Updates and improvements will be released as needed based on user feedback and market evolution.

**Remember:** This is an educational tool. Successful trading requires knowledge, discipline, risk management, and continuous learning. Use this indicator to enhance your understanding of market structure and liquidity, not as a standalone trading system.

Golden Cross 50/200 EMATrend-following systems are characterized by having a low win rate, yet in the right circumstances (trending markets and higher timeframes) they can deliver returns that even surpass those of systems with a high win rate.

Below, I show you a simple bullish trend-following system with clear execution rules:

System Rules

-Long entries when the 50-period EMA crosses above the 200-period EMA.

-Stop Loss (SL) placed at the lowest low of the 15 candles prior to the entry candle.

-Take Profit (TP) triggered when the 50-period EMA crosses below the 200-period EMA.

Risk Management

-Initial capital: $10,000

-Position size: 10% of capital per trade

-Commissions: 0.1% per trade

Important Note:

In the code, the stop loss is defined using the swing low (15 candles), but the position size is not adjusted based on the distance to the stop loss. In other words, 10% of the equity is risked on each trade, but the actual loss on the trade is not controlled by a maximum fixed percentage of the account — it depends entirely on the stop loss level. This means the loss on a single trade could be significantly higher or lower than 10% of the account equity, depending on volatility.

Implementing leverage or reducing position size based on volatility is something I haven’t been able to include in the code, but it would dramatically improve the system’s performance. It would fix a consistent percentage loss per trade, preventing losses from fluctuating wildly with changes in volatility.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to stop loss

And when volatility is high and would exceed the fixed percentage we want to expose per trade (if the SL is hit), we could reduce the position size accordingly.

Practical example:

Imagine we only want to risk 15% of the position value if the stop loss is triggered on Tesla (which has high volatility), but the distance to the SL represents a potential 23.57% drop. In this case, we subtract the desired risk (15%) from the actual volatility-based loss (23.57%):

23.57% − 15% = 8.57%

Now suppose we normally use $200 per trade.

To calculate 8.57% of $200:

200 × (8.57 / 100) = $17.14

Then subtract that amount from the original position size:

$200 − $17.14 = $182.86

In summary:

If we reduce the position size to $182.86 (instead of the usual $200), even if Tesla moves 23.57% against us and hits the stop loss, we would still only lose approximately 15% of the original $200 position — exactly the risk level we defined. This way, we strictly respect our risk management rules regardless of volatility swings.

I hope this clearly explains the importance of capping losses at a fixed percentage per trade. This keeps risk under control while maintaining a consistent percentage of capital invested per trade — preventing both statistical distortion of the system and the potential destruction of the account.

About the code:

Strategy declaration:

The strategy is named 'Golden Cross 50/200 EMA'.

overlay=true means it will be drawn directly on the price chart.

initial_capital=10000 sets the initial capital to $10,000.

default_qty_type=strategy.percent_of_equity and default_qty_value=10 means each trade uses 10% of available equity.

margin_long=0 indicates no margin is used for long positions (this is likely for simulation purposes only; in real trading, margin would be required).

commission_type=strategy.commission.percent and commission_value=0.1 sets a 0.1% commission per trade.

Indicators:

Calculates two EMAs: a 50-period EMA (ema50) and a 200-period EMA (ema200).

Crossover detection:

bullCross is triggered when the 50-period EMA crosses above the 200-period EMA (Golden Cross).

bearCross is triggered when the 50-period EMA crosses below the 200-period EMA (Death Cross).

Recent swing:

swingLow calculates the lowest low of the previous 15 periods.

Stop Loss:

entryStopLoss is a variable initialized as na (not available) and is updated to the current swingLow value whenever a bullCross occurs.

Entry and exit conditions:

Entry: When a bullCross occurs, the initial stop loss is set to the current swingLow and a long position is opened.

Exit on opposite signal: When a bearCross occurs, the long position is closed.

Exit on stop loss: If the price falls below entryStopLoss while a position is open, the position is closed.

Visualization:

Both EMAs are plotted (50-period in blue, 200-period in red).

Green triangles are plotted below the bar on a bullCross, and red triangles above the bar on a bearCross.

A horizontal orange line is drawn that shows the stop loss level whenever a position is open.

Alerts:

Alerts are created for:Long entry

Exit on bearish crossover (Death Cross)

Exit triggered by stop loss

Favorable Conditions:

Tesla (45-minute timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $12,458.73 or +124.59%

Maximum drawdown: $1,210.40 or 8.29%

Total trades: 107

Winning trades: 27.10% (29/107)

Profit factor: 3.141

Tesla (1-hour timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $7,681.83 or +76.82%

Maximum drawdown: $993.36 or 7.30%

Total trades: 75

Winning trades: 29.33% (22/75)

Profit factor: 3.157

Netflix (45-minute timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,380.73 or +113.81%

Maximum drawdown: $699.45 or 5.98%

Total trades: 134

Winning trades: 36.57% (49/134)

Profit factor: 2.885

Netflix (1-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,689.05 or +116.89%

Maximum drawdown: $844.55 or 7.24%

Total trades: 107

Winning trades: 37.38% (40/107)

Profit factor: 2.915

Netflix (2-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $12,807.71 or +128.10%

Maximum drawdown: $866.52 or 6.03%

Total trades: 56

Winning trades: 41.07% (23/56)

Profit factor: 3.891

Meta (45-minute timeframe)

May 18, 2012 – November 17, 2025

Total net profit: $2,370.02 or +23.70%

Maximum drawdown: $365.27 or 3.50%

Total trades: 83

Winning trades: 31.33% (26/83)

Profit factor: 2.419

Apple (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,232.55 or +80.59%

Maximum drawdown: $581.11 or 3.16%

Total trades: 140

Winning trades: 34.29% (48/140)

Profit factor: 3.009

Apple (1-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $9,685.89 or +94.93%

Maximum drawdown: $374.69 or 2.26%

Total trades: 118

Winning trades: 35.59% (42/118)

Profit factor: 3.463

Apple (2-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,001.28 or +77.99%

Maximum drawdown: $755.84 or 7.56%

Total trades: 67

Winning trades: 41.79% (28/67)

Profit factor: 3.825

NVDA (15-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $11,828.56 or +118.29%

Maximum drawdown: $1,275.43 or 8.06%

Total trades: 466

Winning trades: 28.11% (131/466)

Profit factor: 2.033

NVDA (30-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $12,203.21 or +122.03%

Maximum drawdown: $1,661.86 or 10.35%

Total trades: 245

Winning trades: 28.98% (71/245)

Profit factor: 2.291

NVDA (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $16,793.48 or +167.93%

Maximum drawdown: $1,458.81 or 8.40%

Total trades: 172

Winning trades: 33.14% (57/172)

Profit factor: 2.927

Major Crypto Relative Strength Portfolio System Majors RSPS - Relative Strength Portfolio System for Major Cryptocurrencies

Overview

Majors RSPS (Relative Strength Portfolio System) is an advanced portfolio allocation indicator that combines relative strength analysis, trend consensus, and macro risk factors to dynamically allocate capital across major cryptocurrency assets. The system leverages the NormalizedIndicators Library to evaluate both absolute trends and relative performance, creating an adaptive portfolio that automatically adjusts exposure based on market conditions.

This indicator is designed for portfolio managers, asset allocators, and systematic traders who want a data-driven approach to cryptocurrency portfolio construction with automatic rebalancing signals.

🎯 Core Concept

What is RSPS?

RSPS (Relative Strength Portfolio System) evaluates each asset on two key dimensions:

Relative Strength: How is the asset performing compared to other major cryptocurrencies?

Absolute Trend: Is the asset itself in a bullish trend?

Assets that show both strong relative performance AND positive absolute trends receive higher allocations. Weak performers are automatically filtered out, with capital reallocated to cash or stronger assets.

Dual-Layer Architecture

Layer 1: Majors Portfolio (Orange Zone)

Evaluates 14 major cryptocurrency assets

Calculates relative strength against all other majors

Applies trend filters to ensure absolute momentum

Dynamically allocates capital based on comparative strength

Layer 2: Cash/Risk Position (Navy Zone)

Evaluates macro risk factors and market conditions

Determines optimal cash allocation

Acts as a risk-off mechanism during adverse conditions

Provides downside protection through dynamic cash holdings

📊 Tracked Assets

Major Cryptocurrencies (14 Assets)

BTC - Bitcoin (Benchmark L1)

ETH - Ethereum (Smart Contract L1)

SOL - Solana (High-Performance L1)

SUI - Sui (Move-Based L1)

TRX - Tron (Payment-Focused L1)

BNB - Binance Coin (Exchange L1)

XRP - Ripple (Payment Network)

FTM - Fantom (DeFi L1)

CELO - Celo (Mobile-First L1)

TAO - Bittensor (AI Network)

HYPE - Hyperliquid (DeFi Exchange)

HBAR - Hedera (Enterprise L1)

ADA - Cardano (Research-Driven L1)

THETA - Theta (Video Network)

🔧 How It Works

Step 1: Relative Strength Calculation

For each asset, the system calculates relative strength by:

RSPS Score = Average of:

- Asset/BTC trend consensus

- Asset/ETH trend consensus

- Asset/SOL trend consensus

- Asset/SUI trend consensus

- ... (all 14 pairs)

- Asset's absolute trend consensus

Key Logic:

Each pair is evaluated using the eth_4d_cal() calibration from NormalizedIndicators

If an asset's absolute trend is extremely weak (≤ 0.1), it receives a penalty score (-0.5)

Otherwise, it gets the average of all its relative strength comparisons

Step 2: Trend Filtering

Assets must pass a trend filter to receive allocation:

Trend Score = Average of:

- Asset/BTC trend (filtered for positivity)

- Asset/ETH trend (filtered for positivity)

- Asset's absolute trend (filtered for positivity)

Only positive values contribute to the trend score, ensuring bearish assets don't receive allocation.

Step 3: Portfolio Allocation

Capital is allocated proportionally based on filtered RSPS scores:

Asset Allocation % = (Asset's Filtered RSPS Score / Sum of All Filtered Scores) × Main Portfolio %

Example:

SOL filtered score: 0.6

BTC filtered score: 0.4

All others: 0

Total: 1.0

SOL receives: (0.6 / 1.0) × Main% = 60% of main portfolio

BTC receives: (0.4 / 1.0) × Main% = 40% of main portfolio

Step 4: Cash/Risk Allocation

The system evaluates macro conditions across 6 factors:

Inverse Major Crypto Trends (40% weight)

When BTC, ETH, SOL, SUI, DOGE, etc. trend down → Cash allocation increases

Evaluates total market cap trends (TOTAL, TOTAL2, OTHERS)

Stablecoin Dominance (10% weight)

USDC dominance vs. major crypto dominances

Higher stablecoin dominance → Higher cash allocation

MVRV Ratios (10% weight)

BTC and ETH Market Value to Realized Value

High MVRV (overvaluation) → Higher cash allocation

BTC/ETH Ratio (15% weight)

Relative performance between two market leaders

Indicates market phase (BTC dominance vs. alt season)

Active Address Ratios (5% weight)

USDC active addresses vs. BTC/ETH active addresses

Network activity comparison

Macro Indicators (15% weight)

Global currency circulation (USD, EUR, CNY, JPY)

Treasury yield curve (10Y-2Y)

High yield spreads

Central bank balance sheets and money supply

Cash Allocation Formula:

Cash % = (Sum of Risk Factors × 0.5) / (Risk Factors + Majors TPI)

When risk factors are elevated, cash allocation increases, reducing exposure to volatile assets.

📈 Visual Components

Orange Zone (Majors Portfolio)

Fill: Light orange area showing aggregate portfolio strength

Line: Average trend power index (TPI) of allocated assets

Baseline: 0 level (neutral)

Interpretation:

Above 0: Bullish allocation environment

Rising: Strengthening portfolio momentum

Falling: Weakening portfolio momentum

Below 0: No allocation (100% cash)

Navy Zone (Cash Position)

Fill: Navy blue area showing cash allocation strength

Line: Risk-adjusted cash allocation signal

Baseline: 0 level

Interpretation:

Higher navy zone: Elevated risk-off signal → More cash

Lower navy zone: Risk-on environment → Less cash

Zero: No cash allocation (100% invested)

Performance Line (Orange/Blue)

Orange: Main portfolio allocation dominant (risk-on mode)

Blue: Cash allocation dominant (risk-off mode)

Tracks: Cumulative portfolio returns with dynamic rebalancing

Allocation Table (Bottom Left)

Shows real-time portfolio composition:

ColumnDescriptionAssetCryptocurrency nameRSPS ValuePercentage allocation (of main portfolio)CashDollar amount (if enabled)

Color Coding:

Orange: Active allocation

Gray: Weak signal (borderline)

Blue: Cash position

Missing: No allocation (filtered out)

⚙️ Settings & Configuration

Required Setup

Chart Symbol

MUST USE: INDEX:BTCUSD or similar major crypto index

Recommended Timeframe: 1D (Daily) or 4D (4-Day)

Why: System needs price data for all 14 majors, BTC provides stable reference

Hide Chart Candles

For clean visualization:

Right-click on chart

Select "Hide Symbol" or set candle opacity to 0

This allows the indicator fills and table to be clearly visible

User Inputs

plot_table (Default: true)

Enable/disable the allocation table

Set to false if you only want the visual zones

use_cash (Default: false)

Enable portfolio dollar value calculations

Shows actual dollar allocations per asset

cash (Default: 100)

Total portfolio size in dollars/currency units

Used when use_cash is enabled

Example: Set to 10000 for a $10,000 portfolio

💡 Interpretation Guide

Entry Signals

Strong Allocation Signal:

✓ Orange zone elevated (> 0.3)

✓ Navy zone low (< 0.2)

✓ Performance line orange

✓ Multiple assets in allocation table

→ Action: Deploy capital to allocated assets per table percentages

Risk-Off Signal:

✓ Orange zone near zero

✓ Navy zone elevated (> 0.4)

✓ Performance line blue

✓ Few or no assets in table (high cash %)

→ Action: Reduce exposure, increase cash holdings

Rebalancing Triggers

Monitor the allocation table for changes:

New assets appearing: Add to portfolio

Assets disappearing: Remove from portfolio

Percentage changes: Rebalance existing positions

Cash % changes: Adjust overall exposure

Market Regime Detection

Risk-On (Bull Market):

Orange zone high and rising

Navy zone minimal

Many assets allocated (8-12)

High individual allocations (15-30% each)

Risk-Off (Bear Market):

Orange zone near zero or negative

Navy zone elevated

Few assets allocated (0-3)

Cash allocation dominant (70-100%)

Transition Phase:

Both zones moderate

Medium number of assets (4-7)

Balanced cash/asset allocation (40-60%)

🎯 Trading Strategies

Strategy 1: Pure RSPS Following

1. Check allocation table daily

2. Rebalance portfolio to match percentages

3. Follow cash allocation strictly

4. Review weekly, act on significant changes (>5%)

Best For: Systematic portfolio managers, passive allocators

Strategy 2: Threshold-Based

Entry Rules:

- Orange zone > 0.4 AND Navy zone < 0.3

- At least 5 assets in allocation table

- Total non-cash allocation > 60%

Exit Rules:

- Orange zone < 0.1 OR Navy zone > 0.5

- Fewer than 3 assets allocated

- Cash allocation > 70%

Best For: Active traders wanting clear rules

Strategy 3: Relative Strength Overlay

1. Use RSPS for broad allocation framework

2. Within allocated assets, overweight top 3 performers

3. Scale position sizes by RSPS score

4. Use individual asset charts for entry/exit timing

Best For: Discretionary traders with portfolio focus

Strategy 4: Risk-Adjusted Position Sizing

For each allocated asset:

Position Size = Base Position × (Asset's RSPS Score / Max RSPS Score) × (1 - Cash Allocation)

Example:

- $10,000 portfolio

- SOL RSPS: 0.6 (highest)

- BTC RSPS: 0.4

- Cash allocation: 30%

SOL Size = $10,000 × (0.6/0.6) × (1-0.30) = $7,000

BTC Size = $10,000 × (0.4/0.6) × (1-0.30) = $4,667

Cash = $10,000 × 0.30 = $3,000

Best For: Risk-conscious allocators

📊 Advanced Usage

Multi-Timeframe Confirmation

Use on multiple timeframes for robust signals:

1D Chart: Tactical allocation (daily rebalancing)

4D Chart: Strategic allocation (weekly review)

Strong Confirmation:

- Both timeframes show same top 3 assets

- Both show similar cash allocation levels

- Orange zones aligned on both

Weak/Conflicting:

- Different top performers

- Diverging cash allocations

→ Wait for alignment or use shorter timeframe

Sector Rotation Analysis

Group assets by type and watch rotation:

L1 Dominance: BTC, ETH, SOL, SUI, ADA high → Layer 1 season

Alt L1s: TRX, FTM, CELO rising → Alternative platform season

Specialized: TAO, THETA, HYPE strong → Niche narrative season

Payment/Stable: XRP, BNB allocation → Risk reduction phase

Divergence Trading

Bullish Divergence:

Navy zone declining (less risk-off)

Orange zone flat or slightly rising

Few assets still allocated but strengthening

→ Early accumulation signal

Bearish Divergence:

Orange zone declining

Navy zone rising

Asset count decreasing in table

→ Distribution/exit signal

Performance Tracking

The performance line (overlay) shows cumulative strategy returns:

Compare to BTC/ETH: Is RSPS outperforming?

Drawdown analysis: How deep are pullbacks?

Correlation: Does it track market or provide diversification?

🔬 Technical Details

Data Sources

Price Data:

COINEX: Primary exchange for alt data

CRYPTO: Alternative price feeds

INDEX: Aggregated index prices (recommended for BTC)

Macro Data:

Dominance metrics (SUI.D, BTC.D, etc.)

MVRV ratios (on-chain valuation)

Active addresses (network activity)

Global money supply and macro indicators

Calculation Methodology

RSPS Scoring:

For each asset, calculate 14 relative trends (vs. all others)

Calculate asset's absolute trend

Average all 15 values

Apply penalty filter for extremely weak trends (≤ 0.1)

Trend Consensus:

Uses eth_4d_cal() from NormalizedIndicators library

Combines 8 normalized indicators per measurement

Returns value from -1 (bearish) to +1 (bullish)

Performance Calculation:

Daily Return = Σ(Asset ROC × Asset Allocation)

Cumulative Performance = Previous Perf × (1 + Daily Return / 100)

Assumes perfect rebalancing and no slippage (theoretical performance).

Filtering Logic

filter() function:

pinescriptfilter(input) => input >= 0 ? input : 0

This zero-floor filter ensures:

Only positive trend values contribute to allocation

Bearish assets receive 0 weight

No short positions or inverse allocations

Anti-Manipulation Safeguards

Null Handling:

All values wrapped in nz() to handle missing data

Prevents calculation errors from data gaps

Normalization:

Allocations always sum to 100%

Prevents over/under-allocation

Conditional Logic:

Assets need positive values on multiple metrics

Single metric cannot drive allocation alone

⚠️ Important Considerations

Required Timeframes

1D (Daily): Recommended for most users

4D (4-Day): More stable, fewer rebalances

Other timeframes: Use at your own discretion, may require recalibration

Data Requirements

Needs INDEX:BTCUSD or equivalent major crypto symbol

All 14 tracked assets must have available data

Macro indicators require specific TradingView data feeds

Rebalancing Frequency

System provides daily allocation updates

Practical rebalancing: Weekly or on significant changes (>10%)

Consider transaction costs and tax implications

Performance Notes

Theoretical returns: No slippage, fees, or execution delays

Backtest carefully: Validate on your specific market conditions

Past performance: Does not guarantee future results

Risk Warnings

⚠️ High Concentration Risk: May allocate heavily to 1-3 assets

⚠️ Volatility: Crypto markets are inherently volatile

⚠️ Liquidity: Some allocated assets may have lower liquidity

⚠️ Correlation: All assets correlated to BTC/ETH to some degree

⚠️ System Risk: Relies on continued availability of data feeds

Not Financial Advice

This indicator is a tool for analysis and research. It does not constitute:

Investment advice

Portfolio management services

Trading recommendations

Guaranteed returns

Always perform your own due diligence and risk assessment.

🎓 Use Cases

For Portfolio Managers

Systematic allocation framework

Objective rebalancing signals

Risk-adjusted exposure management

Performance tracking vs. benchmarks

For Active Traders

Identify strongest assets to focus trading on

Gauge overall market regime (risk-on/off)

Time entry/exit for portfolio shifts

Complement technical analysis with allocation data

For Institutional Allocators

Quantitative portfolio construction

Multi-asset exposure optimization

Drawdown management through cash allocation

Compliance-friendly systematic approach

For Researchers

Study relative strength dynamics in crypto markets

Analyze correlation between majors

Test macro factor impact on crypto allocations

Develop derived strategies and signals

🔧 Setup Checklist

✅ Chart Configuration

Set chart to INDEX:BTCUSD

Set timeframe to 1D or 4D

Hide chart candles for clean visualization

Add indicator from library

✅ Indicator Settings

Enable plot_table (see allocation table)

Set use_cash if tracking dollar amounts

Input your portfolio size in cash parameter

✅ Monitoring Setup

Bookmark chart for daily review

Set alerts for major allocation changes (optional)

Create spreadsheet to track allocations (optional)

Establish rebalancing schedule (weekly recommended)

✅ Validation

Verify all 14 assets appear in table (when allocated)

Check that percentages sum to ~100%

Confirm performance line is tracking

Test cash allocation calculation if enabled

📋 Quick Reference

Signal Interpretation

ConditionOrange ZoneNavy ZoneActionStrong BullHigh (>0.4)Low (<0.2)Full allocationModerate BullMid (0.2-0.4)Low-MidStandard allocationNeutralLow (0.1-0.2)Mid (0.3-0.4)Balanced allocationModerate BearVery Low (<0.1)Mid-HighReduce exposureStrong BearZero/NegativeHigh (>0.5)High cash/exit

Rebalancing Thresholds

Change TypeThresholdActionIndividual asset±5%Consider rebalanceIndividual asset±10%Strongly rebalanceCash allocation±10%Adjust exposureAsset entry/exitAnyAdd/remove position

Color Legend

Orange: Main portfolio strength/allocation

Navy: Cash/risk-off allocation

Blue text: Cash position in table

Orange text: Active asset allocation

Gray text: Weak/borderline allocation

White: Headers and labels

🚀 Getting Started

Beginner Path

Add indicator to INDEX:BTCUSD daily chart

Hide candles for clarity

Enable plot_table to see allocations

Check table daily, note top 3-5 assets

Start with small allocation, observe behavior

Gradually increase allocation as you gain confidence

Intermediate Path

Set up on both 1D and 4D charts

Enable use_cash with your portfolio size

Create tracking spreadsheet

Implement weekly rebalancing schedule

Monitor divergences between timeframes

Compare performance to buy-and-hold BTC

Advanced Path

Modify code to add/remove tracked assets

Adjust relative strength calculation methodology

Customize cash allocation factors and weights

Integrate with portfolio management platform

Develop algorithmic rebalancing system

Create alerts for specific allocation conditions

📖 Additional Resources

Related Indicators

NormalizedIndicators Library: Core calculation engine

Individual asset trend indicators for deeper analysis

Macro indicator dashboards for cash allocation factors

Complementary Analysis

On-chain metrics (MVRV, active addresses, etc.)

Order book liquidity for execution planning

Correlation matrices for diversification analysis

Volatility indicators for position sizing

Learning Materials

Study relative strength portfolio theory

Research tactical asset allocation strategies

Understand crypto market cycles and phases

Learn about risk management in volatile assets

🎯 Key Takeaways

✅ Systematic allocation across 14 major cryptocurrencies

✅ Dual-layer approach: Asset selection + Cash management

✅ Relative strength focused: Invests in comparatively strong assets

✅ Trend filtering: Only allocates to assets in positive trends

✅ Dynamic rebalancing: Automatically adjusts to market conditions

✅ Risk-managed: Increases cash during adverse conditions

✅ Transparent methodology: Clear calculation logic

✅ Practical visualization: Easy-to-read table and zones

✅ Performance tracking: See cumulative strategy returns

✅ Highly customizable: Adjust assets, weights, and factors

📋 License

This code is subject to the Mozilla Public License 2.0 at mozilla.org

Majors RSPS transforms complex multi-asset portfolio management into a systematic, data-driven process. By combining relative strength analysis with trend consensus and macro risk factors, it provides traders and portfolio managers with a robust framework for navigating cryptocurrency markets with discipline and objectivity.WiederholenClaude kann Fehler machen. Bitte überprüfen Sie die Antworten. Sonnet 4.5

Price Drop CounterThe Price Drop Counter is a very basic statistical indicator.

See it as an analytical tool that tracks how many times an asset's price has dropped by a specified percentage from its recent peak within a defined date range.

The indicator monitors the highest price reached and counts each occurrence when the price falls by your chosen threshold, then resets its peak tracking point after each drop is registered.

Uses

Volatility Assessment: Measure how frequently significant price corrections occur during specific periods

Market Behavior Analysis: Compare drop frequency across different timeframes or market conditions

Risk Evaluation: Identify assets or periods with higher downside volatility

Historical Pattern Recognition: Study how often major pullbacks happened during bull or bear markets

Backtesting Support: Analyze how your strategy would perform based on the frequency of drawdowns

How to use it

Add the indicator to your TradingView chart

Configure the Percent Drop (%) to define your threshold (default: 10%). The indicator will count each time price falls by this percentage from the most recent high

IMPORTANT Set your Start Date and End Date to analyze a specific period of interest

The blue step-line plot shows the cumulative count of drops within your date range

Adjust the percentage threshold based on your analysis needs - use smaller values (2-5%) for more frequent signals or larger values (15-20%) for major corrections only

The counter resets its high-water mark after each qualifying drop, allowing it to track multiple sequential drops within the same period.

Rendement périodes (finary compass)Rendement sur une période donnée,

Outil de décision pour stratégie Momentum

Net Liquidity (WALCL - TGA - ON RRP)//@version=5

indicator("Net Liquidity (WALCL - TGA - ON RRP)", overlay=false, timeframe="W")

a = request.security("FRED:WALCL", "W", close) // Fed total assets (millions)

b = request.security("FRED:WTREGEN", "W", close) // TGA (millions)

c = request.security("FRED:RRPONTSYD","W", close) // ON RRP (millions)

netliq = (a - b - c) / 1000.0 // billions

plot(netliq, color=color.new(color.blue, 0), linewidth=2)

Expsoure Guide by Tradewith_GaryDaily Guide for exposure building. Use this Indicator to improve your profitability by avoiding over-trading and picking the best days to initiate new trades. Valid only for swing trading format.

ATR Risk Display - Multi FuturesWhat This Does

I got tired of manually calculating my ATR stops and risk for different futures contracts, especially when switching between ES, NQ, and their micro versions. This indicator automatically detects what futures symbol you're trading and shows you the exact tick count and dollar risk for your stop loss.

The Problem It Solves

If you trade futures with ATR-based stops, you know the hassle:

Different contracts have different tick values

You need to calculate position risk in dollars

Switching between symbols means redoing all the math

Renko charts make it even more confusing since ATR needs to come from regular candles

This handles all of that automatically.

Key Features

Auto-detects futures symbols - ES, NQ, YM, RTY, GC, CL, and all the micros (MES, MNQ, etc.)

Shows everything you need in one line: ATR(timeframe) × multiplier = X ticks ($XXX)

Works on Renko charts - pulls ATR from regular timeframe charts (super important if you use Renko)

Adjustable position sizing - set your contract count and see total risk instantly

Clean, minimal display - just the info you need, no clutter

How to Use

Add it to any futures chart

Set your preferred ATR timeframe (I use 5-minute)

Set your ATR multiplier (I use 1.5x for my stops)

Set your contract size

That's it - the indicator handles the rest

The display will show something like: "ES ATR(5) × 1.5 = 12 ticks ($150)"

Settings Explained

ATR Timeframe: What timeframe to calculate ATR from (always uses regular candles, even on Renko)

ATR Multiplier: How many ATRs for your stop (1.5 is common, 2.0 for wider stops)

Number of Contracts: Your position size for risk calculation

Auto-Detect Symbol: Leave on unless you want to manually override

Supported Futures

Full size: ES, NQ, YM, RTY, GC, CL, ZB, ZN, 6E, 6J

Micros: MES, MNQ, MYM, M2K, MGC, MCL

Notes

Made this primarily for my own ES trading but figured others might find it useful

The tick values are based on standard CME specs

If you trade other futures, you can modify the code to add them

Works great alongside level indicators for risk management

Why This Exists

I use ATR trailing stops on all my trades and got tired of doing mental math every time I switched between charts or contracts. Especially useful if you trade both full-size and micro contracts - the risk difference is huge and easy to mess up.

Hope this helps your trading! Feel free to suggest improvements.

BEMFUNDING MAX LOT CALCULATION (Sakince)You can use this indicator to ensure you don't exceed the "Maximum Lot" limit. Because the required data varies from pair to pair, you should obtain the latest information from the BEM Funding platform.

Top 20 Screener📘 Indicator Description: I Top 20 Screener

Name:

Top 20 Screener

✅ 1. Features

This screener is designed to monitor and evaluate up to 20 selected IDX (Indonesia Stock Exchange) stocks using technical indicators. It offers a compact and visual table on your chart.

🔧 2. How to Use

Apply the Indicator

Add the indicator to your TradingView chart.

Make sure the timeframe and chart symbol are set correctly (usually apply it to any chart, as it requests data from the 20 symbols independently).

Choose Stocks to Screen

Under the “Symbols” section, check the stocks you want to include (default includes all 20).

Use the Filter Panel (Optional)

Turn on "Filter Enabled".

Choose a Filter Column (e.g., MACD > 0).

Set the "From" and "To" values to filter conditions (e.g., From = 1, To = 1 to show only MACD-positive stocks).

Interpret the Table

Each row shows one stock and its current technical status based on the selected indicators.

Green backgrounds mean bullish signals.

Red or gray indicate bearish or neutral.

📝 3. Remarks

This script uses request.security() to fetch external symbol data — it may lag slightly or be restricted in real-time depending on your plan.

Customizable Symbol List: You can edit the list to monitor any other stocks (IDX or non-IDX).

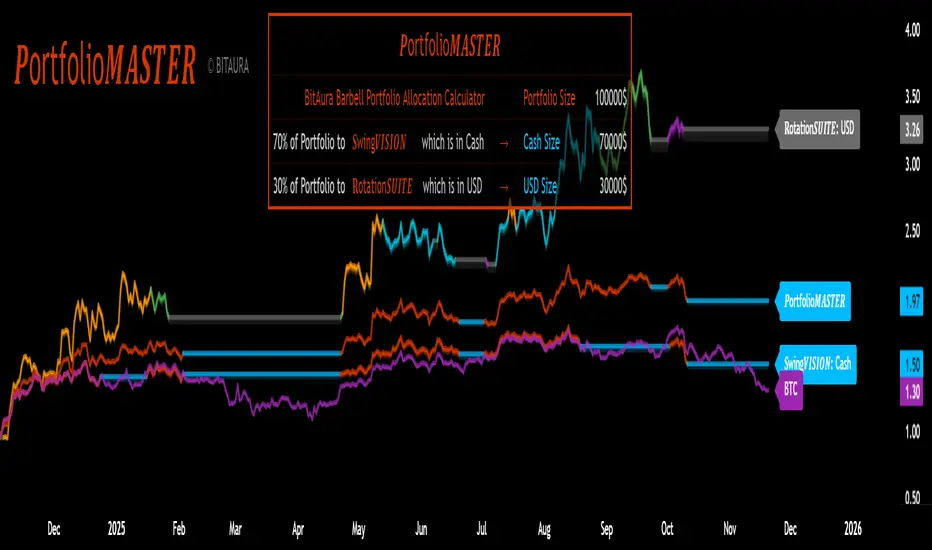

𝑷ortfolio𝑴𝑨𝑺𝑻𝑬𝑹 [BitAura]𝑷ortfolio𝑴𝑨𝑺𝑻𝑬𝑹

This Pine Script® indicator is meant to be used to manage a Barbell Portfolio composed of BitAura's various strategies in order to create a risk-reward balance for the investor's needs. The Portfolio is divided in two main parts, one being a lower-risk Bitcoin-only strategy while the other being the higher-risk, higher-reward 𝐑otation𝑺𝑼𝑰𝑻𝑬 V3 system. The user can choose the percentage splits between these two systems and then also configure them based on their risk profile.

Logic and Core Concepts

The 𝑷ortfolio𝑴𝑨𝑺𝑻𝑬𝑹 System uses the Barbell Portfolio theory to create a portfolio taylored for the final user and automatically calculates dollar allocation based on inputted settings.

Features

𝐑otation𝑺𝑼𝑰𝑻𝑬 : our advanced Strategy which allocates to the strongest asset amongst a pool of 4 Major Crypto Tokens, or de-risk to USD when these lack momentum.

BItcoin-only Strategy : This is theoretically a lower-risk system compared to 𝐑otation𝑺𝑼𝑰𝑻𝑬 and is made out of Universal Trend Following strategies. There are two variants, one being a Long-Term strategy (𝐂ycle𝑽𝑰𝑺𝑰𝑶𝑵) while the other one being of Medium-Term speed (𝐒wing𝑽𝑰𝑺𝑰𝑶𝑵).

Customizable Inputs : Allows users to adjust table settings, backtest date ranges, portfolio splits and portfolio dollar allocations.

Visual Outputs :

Allocation Table : Displays calculated allocation to each system based on user settings.

Equity Plots : Plots the Barbell Portfolio performance along with the two individual systems equities and allow comparisons between them and to Bitcoin Buy & Hold.

Color Presets : Offers five color themes (e.g., Arctic Blast, Fire vs. Ice) or custom color options for long/cash signals.

Pine Script v6 : Leverages matrices, tables, and gradient coloring for enhanced usability.

How to Use

Add to Chart : Apply the indicator to any chart on the 1D timeframe. The ticker doesn't matter as it doesn't affect the calculations, just make sure the ticker start date is earlier than the Backtest Start date applied in the script settings.

Input Portfolio size : Adjust the Dollar Portfolio size in the script settings in order to obtain accurate Portfolio Allocations in the respective table. Note that BitAura can't and won't be able to access your portfolio size.

Choose Barbell Split : Adjust based on your risk-profile how much to allocate to your preferred Bitcoin Strategy (default 70%) and how much to allocate to 𝐑otation𝑺𝑼𝑰𝑻𝑬 (default 30%).

Configure Systems : Select your preferred allocation type for 𝐑otation𝑺𝑼𝑰𝑻𝑬. Aggressive allocates 100% to the dominant asset, Moderate allocates 80% to the dominant asset and 20% to the second strongest one while Conservative does a 60/40 split between the first two assets.

Configure Settings : Adjust backtest start date (default: 31 Oct 2024) to properly track the Portfolio's performance.

Select Color Theme : Choose a preset color mode (e.g., Arctic Blast) or enable custom colors in the Colors group.

Monitor Outputs : Check the Table for Allocations and system signals, and view the equity curves to view the portfolio's performance.

Notes

The script is closed-source.

The script avoids lookahead bias by using barmerge.lookahead_off in request.security() calls.

The BitAura watermark can be toggled in the Script Settings .

Disclaimer : This script is for educational and analytical purposes only and does not constitute financial advice. Investing involves significant risk, and past performance is not indicative of future results. Always conduct your own research and apply proper risk management.

Kalkulator Pozycji — Auto Pip Point kalkulator wyznacza pozycje na podstawie ryzyka podanego w procentach

Checklist (D1 / H4 / M15/30 BoS / VP / Fibo / S/R) This is a simple, visual checklist indicator that allows you to quickly assess how many of your strategy conditions are met, without affecting the chart itself. It is ideal for multi-timeframe strategies and point-by-point setup monitoring.

Tactical Holding [SwissAlgo]Tactical Holding

A visual framework for managing long-term positions across market cycles

--------------------------------------------------------------

Purpose

Instead of holding a fixed position through all market conditions , you can use this framework to adjust your exposure tactically . By reducing positions during distribution phases and accumulating during favorable accumulation zones, you may end up holding more units of the asset over complete market cycles - even if you temporarily exit or reduce exposure during unfavorable periods. This approach aims to help you compound your holdings by taking advantage of market volatility rather than simply enduring it.

--------------------------------------------------------------

Recommended Settings

Timeframe : Weekly (1W) chart

Chart Type : Standard candlesticks (select 'Bar' type Candles)

This indicator is designed for higher timeframe analysis. While it can be applied to other timeframes, the logic and signal generation are optimized for weekly charts to filter out short-term noise and focus on major market cycles.

--------------------------------------------------------------

Key Features

♦ Market State Classification

The indicator aims to categorize potential market conditions into five color-coded states based on technical confluences:

* Bull (bright green): Multiple bullish indicators align

* Bull Retrace (teal): Bullish structure with temporary weakness

* Bull ⇆ Bear Reversal (yellow): Transitional phase between trends

* Bear (bright red): Multiple bearish indicators align

* Bear Retrace (Pale Red/Maroon): Bearish structure with temporary strength

♦ Visual Elements

* Candles change color based on the current market state

* A 50-period EMA tracks with the same color coding, providing visual trend context

* Small arrow markers appear when specific pattern conditions are met (zones for potential distribution or accumulation)

* A legend table (toggle on/off) explains the color system

* A label shows the current state name on the chart

♦ Pattern Recognition

The system monitors for two types of potential entry/exit zones:

1. State transition patterns after periods of market regime consistency

2. RSI divergence patterns (when price and momentum move in opposite directions)

♦ Customization

* Toggle the legend table visibility through settings

* All calculations are transparent and use standard technical analysis methods

--------------------------------------------------------------

How It Works

Think of this indicator as a traffic light system for your portfolio:

♦ Green zones suggest the asset might be in an environment where long-term holders historically have remained invested

Bright green (Bull) : Multiple technical indicators align in a potentially strong bullish phase

Pale green (Bull Retrace) : Bullish structure remains intact, but momentum shows temporary weakness - often a pullback within an uptrend

♦ Red zones suggest conditions where long-term holders might consider reducing exposure or waiting for better entry points

Dark red (Bear) : Multiple technical indicators align in a potentially strong bearish phase

Pale red (Bear Retrace) : Bearish structure remains intact but shows temporary strength - often a bounce within a downtrend

♦ Yellow zones indicate the market is in transition between bull and bear regimes - a time for increased attention as the trend direction becomes uncertain

The system doesn't predict future prices. Instead, it helps you understand the current technical environment by doing the heavy lifting of analyzing multiple indicators at once and presenting them in a simple visual format.

Example: During the 2022 crypto bear market, the indicator would have displayed extended red periods, signaling defensive conditions for holders. When accumulation arrows appeared in late 2022-early 2023, it highlighted potential re-entry zones as the technical regime transitioned back toward green, before the 2024 recovery.

--------------------------------------------------------------

Who This Is For

♦ Long-term investors who want to hold assets through cycles but prefer a systematic approach to position sizing and timing rather than buying and never selling .

♦ Portfolio managers looking for a visual tool to help determine when to increase or decrease exposure to specific assets based on technical regime changes.

♦ Swing traders on higher timeframes who want to align their positions with the broader market structure rather than fighting the trend.

This is not designed for:

* Day traders or scalpers

* Those seeking exact entry/exit prices

* Automated trading systems (this is a visual decision-support tool)

--------------------------------------------------------------

Understanding the Visuals

When you apply Tactical Holding to a chart, you'll see:

1. Colored candles - Instantly see what market regime the asset is in

2. Colored EMA line (thick line) - Provides a dynamic support/resistance reference that changes color with market conditions

3. Small arrows (↑ ↓) - Mark bars where specific technical patterns complete

4. State label - Shows current market classification

5. Legend table (top right) - Quick reference guide for the color system

6. Warning banner (top center) - Reminds you to use weekly charts

The visual design prioritizes clarity over complexity. You should be able to glance at a chart and immediately understand the current technical environment.

--------------------------------------------------------------

Important Limitations

This indicator cannot:

* Predict future price movements

* Guarantee profitable trades

* Work equally well on all assets or timeframes

* Replace your own research and risk management

Technical considerations:

* Divergence detection has a 3-bar confirmation lag (by design, to avoid false signals)

* State transitions require multiple technical confirmations, which may cause delayed reactions to rapid market changes

* The system is reactive, not predictive - it responds to price action after it occurs

* Performance varies significantly between trending assets (like Solana) and stable assets (like Apple)

--------------------------------------------------------------

Practical Application

Consider using this indicator as one component of a broader investment framework:

♦ Understanding Position Context:

The color-coded states can help frame your thinking about current holdings:

Bull: Technical conditions that have historically been associated with sustained uptrends

Bull Retrace: Pullbacks within an overall bullish structure- these periods may offer opportunities to evaluate entry points or reassess existing positions

Reversal (Yellow): Transitional phases where the trend direction is unclear - periods that may warrant closer monitoring

Bear Retrace: Temporary strength within an overall bearish structure - rallies that historically have often faded

Bear: Technical conditions that have historically been associated with sustained downtrends

♦ Interpreting Signal Arrows:

Arrow markers indicate when specific technical pattern conditions have been met. These are observation points, not instructions:

A signal appearing doesn't mean immediate action is required

Treat arrows as prompts for further analysis rather than automatic triggers

Consider the broader context: fundamentals, your investment timeline, risk tolerance, and overall market conditions

Signals show when historical technical patterns have formed - not whether those patterns will lead to the same outcomes as in the past

The framework is designed to organize information visually, not to tell you what to do. Your investment decisions should incorporate this technical perspective alongside other factors relevant to your situation.

--------------------------------------------------------------

Technical Methodology

For transparency, the indicator uses:

* RSI (14) with a 14-period SMA to assess momentum direction

* MACD (12,26,9) to confirm trend strength and histogram momentum

* Stochastic RSI with K and D line crossovers for additional confirmation

* 50-period EMA as the primary trend filter

* Linear regression-based slope analysis to detect flat/transitional periods

* Pivot-based divergence detection following standard technical analysis principles

All calculations use publicly available technical analysis formulas. Nothing is hidden or proprietary beyond the specific combination and weighting of these standard tools.

--------------------------------------------------------------

Disclaimer

This indicator is an educational and analytical tool only. It is not financial advice.

* Trading and investing involve substantial risk of loss

* Past performance of any technical system does not indicate future results

* No indicator can predict market movements with certainty

* Always conduct your own research and consult with qualified financial professionals

* Never invest more than you can afford to lose

* The creators of this indicator are not responsible for any trading losses

* This tool is not affiliated with, endorsed by, or connected to TradingView, 3Commas, or any other trading platform

* Use of this indicator is at your own risk

Risk Management: Regardless of what any indicator shows, always use proper position sizing, stop losses, and risk management appropriate to your personal financial situation.

This indicator provides a framework for analysis. Your decisions, research, and risk management determine your results.

Opening Range The OR indicator plots the Opening Range based on the choice of Start Time and End Time (Hour:Minute:Second).

BTC CME Gaps Detector [SwissAlgo]BTC CME Gaps Detector

Track Unfilled Gaps & Identify Price Magnets

------------------------------------------------------

Overview

The BTC CME Gap Detector identifies and tracks unfilled price gaps on any timeframe (1-minute recommended for scalping) to gauge potential trading bias.

Verify Gap Behavior Yourself : Use TradingView's Replay Mode on the 1-Minute chart to observe how the price interacts with gaps. Load the BTC1! ticker (Bitcoin CME Futures), enable Replay Mode, and play forward through time (for example: go back 15 days). You may observe patterns such as price frequently returning to fill gaps, nearest gaps acting as near-term targets, and gaps serving as potential support/resistance zones. Some gaps may fill quickly, while others may remain open for longer periods. This hands-on analysis lets you independently assess how gaps may influence price movement in real market conditions and whether you may use this indicator as a complement to your trading analysis.

------------------------------------------------------

Purpose