SMC Pro+ ICT v4 Enhanced - FINAL🎯 SMC Pro+ ICT v4 Enhanced - Complete Smart Money Trading System📊 Professional All-in-One Indicator for Smart Money Concepts & ICT MethodologyThe SMC Pro+ ICT v4 Enhanced is a comprehensive trading system that combines Smart Money Concepts (SMC) with Inner Circle Trader (ICT) methodology. This indicator provides institutional-grade market structure analysis, liquidity mapping, and volume profiling in one powerful package.✨ CORE FEATURES🏗️ Advanced Market Structure Detection

MSS (Market Structure Shift) - Identifies major trend reversals with precision

BOS (Break of Structure) - Confirms trend continuation moves

CHoCH (Change of Character) - Detects internal structure shifts

Modern LuxAlgo-Style Lines - Clean, professional visualization

Dual Sensitivity System - External structure (major swings) + Internal structure (minor swings)

Customizable Labels - Tiny, Small, or Normal sizes

Structure Break Visualization - Clear break point markers

💎 Supply & Demand Zones (POI - Point of Interest)

Institutional Order Blocks - Where smart money enters/exits

ATR-Based Zone Sizing - Dynamically adjusted to market volatility

Smart Overlap Detection - Prevents cluttered charts

Historical Zone Tracking - Maintains up to 50 zones

POI Central Lines - Pinpoint entry/exit levels

Auto-Extension - Zones extend to current price

Auto-Cleanup - Removes broken zones automatically

📦 Fair Value Gap (FVG) Detection

Bullish & Bearish FVGs - Institutional inefficiencies

Consequent Encroachment (CE) - 50% fill levels

Auto-Delete Filled Gaps - Keeps charts clean

Customizable Lookback - 1-30 days of history

Color-Coded Zones - Easy visual identification

CE Line Styles - Dotted, Dashed, or Solid

🚀 Enhanced PVSRA Volume Analysis

This is one of the most powerful features:

200% Volume Candles - Extreme institutional activity (Lime/Red)

150% Volume Candles - High institutional interest (Blue/Fuchsia)

Volume Climax Detection - Major reversal signals with 2.5x+ volume

Exhaustion Signals - Identifies buying/selling exhaustion with high accuracy

Enhanced Volume Divergence - NEW! High-quality reversal detection

Price makes lower low, Volume makes higher low = Bullish Divergence

Price makes higher high, Volume makes lower high = Bearish Divergence

Strict trend context filtering for accuracy

Rising/Falling Volume Patterns - Momentum confirmation (allows 1 exception in 3 bars)

Volume Spread Analysis - Price range × Volume for true strength

Body/Wick Ratio Analysis - Candle structure quality

ATR Normalization - Adjusts for different market volatility

Volume Profile Indicators - 🔥 EXTREME, ⚡ VERY HIGH, 📈 HIGH, ✅ ABOVE AVG

💧 Advanced Liquidity System

Smart money targets these levels:

Weekly High/Low Liquidity - Major institutional targets

Daily High/Low Liquidity - Intraday key levels

4H Session Liquidity - Short-term targets

Distance Indicators - Shows % distance from current price

Strength Indicators - Identifies high-probability sweeps

Swept Level Detection - Tracks executed liquidity grabs

Customizable Line Styles - Width, length, offset controls

Color-Coded Levels - Easy visual hierarchy

🎯 Master Bias System

Data-driven directional bias with 9-factor scoring:

Bull/Bear Bias Calculation - 0-100% scoring system

Multi-Timeframe Analysis - Daily, 4H, 1H trend alignment

Kill Zone Integration - London (2-5 AM) & NY (8-11 AM) sessions

EMA Alignment Factor - Trend confirmation

Volume Confirmation - Adds 5% when volume supports direction

Range Filter Integration - Adds 10% for trending markets

Session Context - Above/below session midpoint scoring

Bias Strength Rating - STRONG (>75%), MODERATE (60-75%), WEAK (<60%)

Real-Time Updates - Dynamic recalculation

📈 Premium & Discount Zones

Fibonacci-based institutional pricing:

Extreme Premium - Above 78.6% (Overvalued)

Premium Zone - 61.8% - 78.6% (Expensive)

Equilibrium - 38.2% - 61.8% (Fair Value)

Discount Zone - 21.4% - 38.2% (Cheap)

Extreme Discount - Below 21.4% (Undervalued)

Visual Zone Boxes - Color-coded for instant recognition

200-500 Bar Lookback - Customizable range calculation

🔄 Range Filter

Advanced trend detection:

Smoothed Range Calculation - Eliminates noise

Dynamic Support/Resistance - Auto-adjusting levels

Upward/Downward Counters - Measures trend strength

Color-Coded Line - Green (uptrend), Red (downtrend), Orange (ranging)

Adjustable Period - 1-200 bars

Multiplier Control - Fine-tune sensitivity (0.1-10.0)

🌊 Liquidity Zones (Vector Zones)

PVSRA-based horizontal liquidity:

Above Price Zones - Resistance clusters

Below Price Zones - Support clusters

Maximum 500 Zones - Professional-grade capacity

Body/Wick Definition - Choose zone boundaries

Auto-Cleanup - Removes cleared zones

Color Override - Custom styling options

Transparency Control - 0-100% opacity

📊 EMA System

Triple EMA trend confirmation:

Fast EMA (9) - Green line - Immediate trend

Medium EMA (21) - Blue line - Short-term trend

Slow EMA (50) - Red line - Major trend

EMA Alignment Detection - Bull/Bear stack confirmation

Dashboard Integration - Status: 📈 BULL ALIGN, 📉 BEAR ALIGN, 🔀 MIXED

Adjustable Lengths - Customize all three EMAs (5-200)

🎯 IDM (Institutional Decision Maker) Levels

Key institutional price levels:

Latest IDM Detection - 20-bar pivot lookback

Extended Lines - Projects 50 bars into future

Customizable Styles - Solid, Dashed, or Dotted

Line Width Control - 1-5 pixels

Color Selection - Match your chart theme

Price Label - Shows exact level with tick precision

📱 Professional Dashboard

Real-time market intelligence panel:

🎯 SIGNAL - 🟢 LONG, 🔴 SHORT, ⏳ WAIT, 🛑 NO TRADE

🎲 BIAS - Bull/Bear with STRONG/MODERATE/WEAK rating

📊 BULL/BEAR Scores - 0-100% percentage display

💎 ZONE - Current premium/discount location

🕐 KZ - Kill Zone status (🇬🇧 LONDON/🇺🇸 NY/⏸️ OFF)

🏗️ STRUCT - Market structure status (BULLISH/BEARISH/NEUTRAL)

⚡ EVENT - Last structure event (MSS/BOS)

⚡ INT - Internal structure trend

🎯 IDM - Latest institutional level

📊 EMA - EMA alignment status

🔄 RF - Range Filter direction

📊 PVSRA - Volume status (🚀 CLIMAX/📈 RISING/📉 FALLING)

📅 MTF - Multi-timeframe alignment (✅ FULL/⚠️ PARTIAL/❌ CONFLICT)

💪 CONF - Confidence score (0-100%)

📊 VOL - Volume ratio (e.g., 1.8x average)

Advanced Metrics (Toggle On/Off):

📏 RSI - Value + Status (OVERBOUGHT/STRONG/NEUTRAL/WEAK/OVERSOLD)

📈 MACD - Value + Direction (BULL/BEAR)

🌪️ VOL - Volatility state (⚠️ EXTREME/🔥 HIGH/📊 NORMAL/😴 LOW)

🔊 VOL PROF - Volume profile ratio

⏱️ TF - Current timeframe

Dashboard Customization:

4 Positions - Top Left, Top Right, Bottom Left, Bottom Right

3 Sizes - Small, Normal, Large

2 Modes - Compact (MTF combined) or Full (separate rows)

Professional Design - Dark theme with color-coded cells

🎮 TRADING SIGNALS & SETUP SCORING🟢 LONG Setup Requirements (9-Factor Confidence Score)

MTF Alignment - Daily/4H/1H/Structure all bullish (+2 points for full, +1 for partial)

Volume Confirmation - Above 1.2x average (+1 point)

Structure Event - MSS or BOS bullish (+2 points)

EMA Alignment - 9 > 21 > 50 (+1 point)

Kill Zone Active - London/NY + Bull bias >75% (+2 points)

Bias Match - Master bias matches structure trend (+1 point)

Confidence Threshold - >60% minimum for signal

🔴 SHORT Setup Requirements

Same 9-factor system but inverted for bearish conditions.💪 Confidence Levels

75-100% - ⭐ HIGH CONFIDENCE (Strong setup, all factors aligned)

50-74% - ⚠️ MODERATE (Good setup, partial alignment)

0-49% - ❌ LOW CONFIDENCE (Wait for better setup)

🎯 Signal Output

🟢 LONG - Bull bias + Bullish structure + >60% confidence

🔴 SHORT - Bear bias + Bearish structure + >60% confidence

⏳ WAIT LONG - Bull bias but low confidence

⏳ WAIT SHORT - Bear bias but low confidence

🛑 NO TRADE - Neutral bias or conflicting signals

🔔 COMPREHENSIVE ALERT SYSTEM (12 Alerts)Structure Alerts

⚡ MSS Bullish - Major bullish reversal

⚡ MSS Bearish - Major bearish reversal

📈 BOS Bullish - Bullish continuation

📉 BOS Bearish - Bearish continuation

⚠️ CHoCH Bullish - Internal bullish shift

⚠️ CHoCH Bearish - Internal bearish shift

Bias & Confidence Alerts

🟢 Bias Shift Bull - Master bias turns bullish

🔴 Bias Shift Bear - Master bias turns bearish

⭐ High Confidence - Setup reaches 75%+ confidence

Volume Alerts (High Probability)

🚀 Volume Climax Buy - Extreme bullish volume spike

💥 Volume Climax Sell - Extreme bearish volume spike

⚠️ Selling Exhaustion - Potential bullish reversal

⚠️ Buying Exhaustion - Potential bearish reversal

📊 Bullish Volume Divergence - High-quality bullish reversal signal

📊 Bearish Volume Divergence - High-quality bearish reversal signal

🎨 EXTENSIVE CUSTOMIZATIONColors & Styling

✅ All colors customizable for every component

✅ Supply/Demand zone colors + outlines

✅ FVG colors (bullish/bearish)

✅ PVSRA candle colors (6 types)

✅ Liquidity level colors (Weekly/Daily/4H/Swept)

✅ Structure line colors

✅ Premium/Equilibrium/Discount zone colorsDisplay Controls

✅ Toggle each feature on/off independently

✅ Adjustable sensitivities (Structure: 5-30, Internal: 3-15)

✅ Label size controls (Tiny/Small/Normal)

✅ Line width adjustments (1-5 pixels)

✅ Transparency controls (0-100%)

✅ Extension lengths (20-100 bars)

✅ Lookback periods (50-500 bars)Volume Settings

✅ PVSRA symbol override (trade one asset, analyze another)

✅ Climax threshold (2.0-5.0x)

✅ Rising volume bar count (2-5 bars)

✅ Divergence filters (Strict/Lenient)

✅ Divergence minimum bars (10-30)

✅ Volume threshold multiplier (1.0-2.0x)Dashboard Settings

✅ Position (4 corners)

✅ Size (Small/Normal/Large)

✅ Compact/Full mode

✅ Show/Hide advanced metrics

✅ Show/Hide EMA status💡 BEST PRACTICES & USAGE TIPS⏰ Optimal Timeframes

Scalping - 1m, 5m (Use Kill Zones, Volume Climax, FVG)

Day Trading - 5m, 15m, 1H (Use Structure, Liquidity, Bias)

Swing Trading - 4H, Daily (Use MTF, Premium/Discount, Structure)

Position Trading - Daily, Weekly (Use major structure, liquidity)

🎯 Asset Classes

✅ Forex - All pairs (especially majors during Kill Zones)

✅ Crypto - BTC, ETH, altcoins (24/7 liquidity)

✅ Stocks - All stocks and indices (use session times)

✅ Commodities - Gold, Silver, Oil (high volume periods)

✅ Indices - S&P 500, NASDAQ, DAX, etc.🔥 High-Probability Setups

The Perfect Storm

MSS in direction of daily trend

Kill Zone active

Volume climax

Confidence >75%

Price in discount (long) or premium (short)

Volume Divergence Play

Enhanced volume divergence signal

CHoCH confirms direction change

Price near liquidity level

FVG forms for entry

Liquidity Sweep

Price sweeps weekly/daily high/low

Immediate rejection (selling/buying exhaustion)

Structure shift (MSS)

Volume confirmation

Structure Retest

BOS breaks structure

Price returns to POI/FVG

Volume confirms (>1.2x)

Kill Zone active

📊 Multi-Timeframe Analysis

Higher Timeframe - Identify trend & structure (Daily/4H)

Trading Timeframe - Find entries (15m/1H)

Lower Timeframe - Precise entries (1m/5m)

Look for MTF alignment - Dashboard shows ✅ FULL or ⚠️ PARTIAL

⚠️ Risk Management

Always use stop-loss (below/above recent structure)

Position size: 1-2% risk per trade

Target liquidity levels for take profit

Use supply/demand zones for SL placement

Watch for exhaustion signals near targets

Portfolio management

swing indicator Installation & Configuration - swing Indicator

⚙️ Parameter Configuration

"Settings" Group (General Parameters)

Show Moving Average: Show/hide the OI moving average

✅ Recommended: Enabled to visualize the trend

Helps identify if OI is above or below its average

MA Period: Moving average period (default: 20)

📊 Common values:

20: Short/medium term trend (responsive)

50: Medium term trend (balanced)

100: Long term trend (stable)

Compare with Volume: Display normalized volume in background

💡 Useful to compare OI evolution with volume

Helps identify divergences between Open interest (oi) and Volume

OI Significant Change Threshold: Detection threshold for significant changes

Available options: 10%, 15%, 20%, 25%, 30%, 40%

🎯 10-15%: High sensitivity (many signals, possible noise)

🎯 20-25%: Normal sensitivity (moderate signals, recommended)

🎯 30-40%: Low sensitivity (rare but very significant signals)

⚡ This threshold determines when green/red triangles appear

Manual OI Symbol (optional): Manually enter the OI symbol

📝 Leave empty for automatic detection

⚙️ Use only if your symbol is not automatically recognized

Manual example: COMEX:GC1!_OI for gold

"Visual Signals" Group

Show Triangles (Significant Changes): Show/hide triangles

▲ GREEN Triangle = Significant OI increase (> configured threshold)

▼ RED Triangle = Significant OI decrease (< -configured threshold)

✅ Recommended: Enabled to see important changes

💡 Disable if you find the chart too cluttered

Show Circles (MA Crossovers): Show/hide circles

● GREEN Circle = OI crosses MA upward

● RED Circle = OI crosses MA downward

✅ Recommended: Enabled if you use MA crossover strategy

💡 Disable if you focus only on OI variations

"Style" Group (Color Customization)

OI Color: Main Open Interest histogram color

Default: Blue

🎨 Customize according to your visual preferences

OI Rising: Histogram color when OI increases

Default: Transparent green

Subtle display of direction

OI Falling: Histogram color when OI decreases

Default: Transparent red

Subtle display of direction

MA Color: Moving average color

Default: Orange

Should contrast with OI color

Volume Color: Normalized volume background color

Default: Transparent gray

Discreet enough not to hinder reading

📊 Reading the Information Panel

The panel at the top right of the chart displays:

By: Alphaomega18

Indicator creator's signature

⚠️ WARNING: OI symbol not detected

Only appears if OI symbol is not automatically detected

Action: Check symbol or enter manually

Open Interest

Current Open Interest value

Format: number of contracts (e.g., 485.2K = 485,200 contracts)

Change

OI % change from previous bar

🟢 Green = OI increase

🔴 Red = OI decrease

Ex: +2.45% = OI increased by 2.45%

Threshold

Displays configured threshold for alerts

Ex: "25%" = alerts triggered at +25% or -25%

Yellow color for visibility

MA(20)

Current moving average value

Number in parentheses indicates period

Ex: MA(50) if you configured a 50 period

Signal

🟢 Strong Trend: OI > MA → Strong participation, solid trend

🔴 Weak Trend: OI < MA → Weak participation, fragile trend

🎯 Visual Signals on Chart

Triangles (Significant Changes)

▲ GREEN Triangle (bottom of chart)

Meaning: Significant OI increase

Trigger: OI increases more than configured threshold

Example: If threshold = 25%, triangle appears when OI +25% or more

📈 Interpretation: New contracts opened = growing interest

▼ RED Triangle (bottom of chart)

Meaning: Significant OI decrease

Trigger: OI decreases more than configured threshold

Example: If threshold = 25%, triangle appears when OI -25% or less

📉 Interpretation: Massive position closing = disengagement

Circles (Moving Average Crossovers)

🟢 GREEN Circle (bottom of chart)

Meaning: OI just crossed MA upward

Signal: Open interest back above its average

📊 Interpretation: Interest returning, potential trend start

🔴 RED Circle (top of chart)

Meaning: OI just crossed MA downward

Signal: Open interest back below its average

📊 Interpretation: Decreasing interest, potential weakening

🔔 Alert Configuration

Create an alert:

Right-click on chart → "Add Alert" (or ALT + A)

In "Condition", select "Open Interest"

Choose alert type from 4 available

Configure notification options

Click "Create"

Available alert types:

OI Significant Increase

Triggers when OI increases beyond configured threshold

Example: Threshold 25% → Alert if OI +25% or more

Use: Detect massive influx of new contracts

OI Significant Decrease

Triggers when OI decreases beyond configured threshold

Example: Threshold 25% → Alert if OI -25% or less

Use: Detect massive position closing

OI crosses MA up

Triggers when OI crosses its moving average upward

Condition: OI was below MA and crosses above

Use: Identify interest returning

OI crosses MA down

Triggers when OI crosses its moving average downward

Condition: OI was above MA and crosses below

Use: Identify decreasing interest

Notification configuration:

✉️ Email: Receive alert via email

📱 SMS: Receive alert via SMS (subscription required)

🔔 Popup: Notification on TradingView

📲 App: Notification on TradingView mobile app

🔗 Webhook: Send alert to external system

💡 Advanced Interpretation

Combined OI + Price Analysis:

Open InterestPriceInterpretationSuggested Action↑ Rising↑ Rising🟢 STRONG UptrendNew buyers entering, robust trend, consider long positions↑ Rising↓ Falling🔴 STRONG DowntrendNew sellers entering, bearish pressure, consider short positions↓ Falling↑ Rising📊 Short coveringClosing short positions, potentially temporary move↓ Falling↓ Falling📊 Long liquidationClosing long positions, potentially temporary move

OI vs Moving Average:

OI > MA (Signal: Strong Trend)

Open interest above its average

Market participation above normal

Trend supported by growing interest

✅ Increased confidence in market direction

OI < MA (Signal: Weak Trend)

Open interest below its average

Market participation below normal

Potentially fragile trend

⚠️ Caution: trend lacks conviction

OI vs Volume:

Rising OI + Rising Volume

New contracts + high trading activity

💪 Very strong trend signal

Falling OI + Rising Volume

Position closing + high activity

⚡ Potential reversal or massive profit-taking

Stable OI + Rising Volume

Transfer of positions between traders

🔄 Changing hands, no new commitments

🛠️ Troubleshooting

❌ Issue: "⚠️ WARNING - OI symbol not detected"

✅ Solutions:

Check contract symbol

Make sure you're on a continuous futures contract (e.g., GC1!, CL1!)

Not on a specific contract (e.g., GCZ2024)

Enter symbol manually

Go to Settings → Manual OI Symbol

Format: EXCHANGE:SYMBOL_OI

Examples:

Gold: COMEX:GC1!_OI

WTI Crude: NYMEX:CL1!_OI

Natural Gas: NYMEX:NG1!_OI

Check data availability

Not all markets have public OI data

Verify on TradingView if OI data exists

❌ Issue: No data displayed (empty chart)

✅ Solutions:

Change timeframe

OI is generally published daily

Switch to Daily (1D) or Weekly (1W)

Intraday timeframes may not have data

Check data connection

Refresh TradingView page

Check your TradingView subscription (some data requires subscription)

Test on another market

Try with gold (COMEX:GC1!) which always has OI data

If it works, problem comes from initial market

❌ Issue: Too many visual signals (cluttered chart)

✅ Solutions:

Increase detection threshold

Settings → OI Significant Change Threshold

Change from 20% to 30% or 40%

Fewer signals, but more significant

Disable some signals

Visual Signals → Uncheck "Show Triangles" or "Show Circles"

Keep only the most important signals for you

Adjust colors

Style → Reduce color opacity

Make signals more discreet visually

❌ Issue: Not enough signals

✅ Solutions:

Reduce detection threshold

Settings → OI Significant Change Threshold

Change to 10% or 15%

More signals, but beware of noise

Enable all signals

Visual Signals → Check "Show Triangles" AND "Show Circles"

Full display of all events

Reduce MA period

Settings → MA Period → Change from 20 to 10

More responsive MA = more crossovers

📈 Compatible Markets (Auto-detection)

✅ Energy (NYMEX)

CL, CL1!: WTI Crude Oil

BZ, BZ1!: Brent Crude

NG, NG1!: Natural Gas

RB, RB1!: RBOB Gasoline

HO, HO1!: Heating Oil

✅ Precious Metals (COMEX/NYMEX)

GC, GC1!: Gold

SI, SI1!: Silver

PL, PL1!: Platinum

PA, PA1!: Palladium

HG, HG1!: Copper

✅ Industrial Metals (LME)

ALI, ALI1!: Aluminum

ZNC, ZNC1!: Zinc

NI, NI1!: Nickel

✅ Agriculture - Grains (CBOT)

ZC, ZC1!: Corn

ZW, ZW1!: Wheat

ZS, ZS1!: Soybeans

ZM, ZM1!: Soybean Meal

ZL, ZL1!: Soybean Oil

ZO, ZO1!: Oats

ZR, ZR1!: Rice

✅ Agriculture - Softs (ICE)

SB, SB1!: Sugar

KC, KC1!: Coffee

CC, CC1!: Cocoa

CT, CT1!: Cotton

OJ, OJ1!: Orange Juice

✅ Livestock (CME)

LE, LE1!: Live Cattle

GF, GF1!: Feeder Cattle

HE, HE1!: Lean Hogs

✅ Other

LBS, LBS1!: Lumber (CME)

🎓 Usage Tips

For beginners:

Start with default parameters (threshold 25%, MA 20)

Enable all visual signals

Focus on liquid markets (gold, crude oil)

Observe how OI reacts to price movements

For intermediate traders:

Adjust threshold according to market volatility (15-30%)

Combine with other technical indicators

Create alerts for significant changes

Analyze OI/Price divergences

For advanced traders:

Use multiple MA periods (20, 50, 100)

Analyze OI/Volume/Price correlation

Configure alerts on multiple timeframes

Integrate into complete trading strategy

📊 Practical Example

Scenario: Gold Trading (COMEX:GC1!)

Initial setup:

Threshold: 20% (gold volatile)

MA: 20 days

All signals enabled

Timeframe: Daily (1D)

Observation:

Gold price: Uptrend

OI: ▲ Green triangle (increase of +22%)

Signal: 🟢 Strong Trend (OI > MA)

Interpretation:

New buyers massively entering

Uptrend supported by OI

Strong market conviction

Action:

✅ Long position validated by OI

Stop loss below technical support

Monitor if OI continues to increase

✨ Made by Alphaomega18

STS FULL OPTIONAL 2.0 (SURGICAL EDIT)STS TITAN 2.0: The End of Manual Analysis

Stop drawing lines. Stop guessing directions. Start executing trades.

Trading shouldn't be about spending hours analyzing charts. It should be about spotting the opportunity and taking it. STS TITAN 2.0 (Surgical Edit) is not just an indicator—it is an institutional-grade algorithm that does the analysis for you.

It doesn't just show you "data"; it projects actionable, high-probability ENTRY ZONES directly onto your chart.

💎 WHY THIS IS DIFFERENT (The Unfair Advantage)

Most indicators clutter your screen. TITAN gives you clarity. It applies a "Triple Confluence Algorithm" (Market Structure + Volume POC + Fibonacci) to filter out noise and leave you with only the highest quality setups.

🔥 KEY FEATURES:

🎯 Zero Analysis Required: The algorithm automatically identifies Supply & Demand zones. You don't have to draw a single box.

🛡️ The "SAFE STRIP" Technology: Inside every zone, TITAN highlights the inner "Safe Strip" (the optimal 25%). This tells you exactly where to place your limit order for maximum precision and zero drawdown.

⚡ Surgical "Auto-Clean": The code is strict. If a candle wick invalidates a zone, TITAN instantly removes it. No confusion, no old levels. Only fresh, tradable zones.

🧠 Automated Confluence: A zone only turns BLUE (Buy) or RED (Sell) when the Asian Strategy, Fibonacci Golden Zone, and Volume Profile align.

This is the closest you will get to having a professional analyst sitting next to you 24/7.

👉 Unlock your edge. Let TITAN find the trade.

(Alternative: Ultra-Short Version)

🚀 STS TITAN 2.0: Automated Institutional Entries

Tired of manual analysis? Let the algorithm do the work. TITAN 2.0 scans Market Structure, Volume POC, and Fibonacci levels to project High-Probability Entry Zones directly on your chart.

✅ Auto Supply & Demand: No drawing needed.

✅ Surgical Precision: "Safe Strip" technology for sniper entries.

✅ Verified Setups: Zones change color only when fully confirmed.

Stop guessing. Let the code find the entry.

Adaptive Risk Management [sgbpulse]1. Introduction:

Adaptive Risk Management is an advanced indicator designed to provide traders with a comprehensive risk management tool directly on the chart. Instead of relying on complex manual calculations, the indicator automates all critical steps of trade planning. It dynamically calculates the estimated Entry Price , the Stop Loss location, the required Position Size (Quantity) based on your capital and risk limits, and the three Take Profit targets based on your defined Reward/Risk ratios. The indicator displays all these essential data points clearly and visually on the chart, ensuring you always know the potential risk-reward profile of every trade.

ARM : The A daptive R isk M anagement every trader needs to ARM themselves with.

2. The Critical Importance of Risk Management

Proper risk management is the cornerstone of successful trading. Consistent profitability in the market is impossible without rigorously defining risk limits.

Risk Control: This starts by setting the maximum risk amount you are willing to lose in a single trade (Risk per Trade), and limiting the total capital allocated to the position (Max Capital per Trade).

Defining Boundaries (Stop Loss & Take Profit): It is mandatory to define a technical Stop Loss and a Take Profit target. A fundamental rule of risk management is that the Reward/Risk Ratio (R/R) must be a minimum of 1:1.

3. Core Features, Adaptivity, and Customization

The Adaptive Risk Management indicator is engineered for use across all major trading styles, including Swing Trading, Intraday Trading, and Scalping, providing consistent risk control regardless of the chosen timeframe.

Real-Time Dynamic Adaptivity: The indicator calculates all risk management parameters (Entry, Stop Loss, Quantity) dynamically with every new bar, thus adapting instantly to changing market conditions.

Trend Direction Adjustment: Define the analysis direction (Long/Uptrend or Short/Downtrend).

Intraday Session Data Control: Full control over whether lookback calculations will include data from Extended Trading Hours (ETH), or if the daily calculations will start actively only from the first bar of Regular Trading Hours (RTH).

Status Validation: The indicator performs critical status checks and displays clear Warning Messages if risk conditions are not met.

4. Intuitive Visualization and Real-Time Data

Dynamic Tracking Lines: The Entry Price and Stop Loss lines are updated with every new bar. Crucially, the length of these lines dynamically reflects the calculation's lookback range (e.g., the extent of Lookback Bars or the location of the confirmed Pivot Point), providing a visual anchor for the calculated price.

Risk and Reward Zones: The indicator creates a graphical background fill between Entry and Stop Loss (marked with the risk color) and between Entry and the Reward Targets (marked with the reward color).

Essential Information Labels: Labels are placed at the end of each line, providing critical data: Estimated Entry Price, Stock/Contract Quantity (Quantity), Total Entry Amount, Estimated Stop Loss, Risk per Share, Total Financial Risk (Risk Amount), Exit Amount, Estimated Take Profit 1/2/3, Reward/Risk Ratio 1/2/3, Total Reward 1/2/3, TP Exit Amount 1/2/3.

4.1. Data Window Metrics (16 Full Series)

The indicator displays 16 full data series in the TradingView Data Window, allowing precise tracking of every calculation parameter:

Entry Data: Estimated Entry, Quantity, Entry Amount.

Risk Data (Stop Loss): Estimated Stop Loss, Risk per Share, Risk Amount, Exit Amount.

Reward Data (Take Profit): Estimated Take Profit 1/2/3, Reward/Risk Ratio 1/2/3, Total Reward 1/2/3, TP Exit Amount 1/2/3.

4.2. Instant Tracking in the Status Line

The indicator displays 6 critical parameters continuously in the indicator's Status Line: Estimated Entry, Quantity, Estimated Stop Loss, Estimated Take Profit 1/2/3.

5. Detailed Indicator Inputs

5.1 General

Focused Trend: Defines the analysis direction (Uptrend / Downtrend).

Max Capital per Trade: The maximum amount allocated to purchasing stocks/contracts (in account currency).

Risk per Trade: The maximum amount the user is willing to risk in this single trade (in account currency).

ATR Length: The lookback period for the Average True Range (ATR) calculation.

5.2 Intraday Session Data Control

Regular Hours Limitation : If enabled, all daily lookback calculations (for Entry/Stop Loss anchor points) will begin strictly from the first Regular Trading Hours (RTH) bar. This limits the lookback range to the current RTH session, excluding preceding Extended Trading Hours (ETH) data. Only relevant for Intraday charts. Default: False (Off)

5.3 Entry Inputs

Entry Method: Selects the entry price calculation method:

Current Price: Uses the closing price of the current bar as the estimated entry point (Market Entry).

ATR Real Bodies Margin :

- Uptrend: Calculates the Maximum Real Body over the lookback period + the calculated safety margin.

- Downtrend: Calculates the Minimum Real Body over the lookback period - the calculated safety margin.

ATR Bars Margin :

- Uptrend: Calculates the Maximum High price over the lookback period + the calculated safety margin.

- Downtrend: Calculates the Minimum Low price over the lookback period - the calculated safety margin.

Lookback Bars: The number of bars used to calculate the extremes in the ATR-based entry methods (Relevant only for ATR Real Bodies Margin and ATR Bars Margin methods).

ATR Multiplier (Entry): The multiplier applied to the ATR value. The result of the multiplication is the calculated safety margin used to determine the estimated Entry Price.

5.4 Risk Inputs (Stop Loss)

Risk Method: Selects the Stop Loss price calculation method.

ATR Current Price Margin :

- Uptrend: Entry Price - the calculated safety margin.

- Downtrend: Entry Price + the calculated safety margin.

ATR Current Bar Margin :

- Uptrend: Current Bar's Low price - the calculated safety margin.

- Downtrend: Current Bar's High price + the calculated safety margin.

ATR Bars Margin :

- Uptrend: Lowest Low over lookback period - the calculated safety margin.

- Downtrend: Highest High over lookback period + the calculated safety margin.

ATR Pivot Margin :

- Uptrend: The first confirmed Pivot Low point - the calculated safety margin.

- Downtrend: The first confirmed Pivot High point + the calculated safety margin.

Lookback Bars: The lookback period for finding the extreme price used in the 'ATR Bars Margin' calculation.

ATR Multiplier (Risk): The multiplier applied to the ATR value. The result of the multiplication is the calculated safety margin used to place the estimated Stop Loss. Note: If set to 0, the Stop Loss will be placed exactly at the technical anchor point, provided the Minimum Margin Value is also 0.

Minimum Margin Value: The minimum price value (e.g., $0.01) the Stop Loss margin buffer must be.

Pivot (Left / Right): The number of bars required on either side of the pivot bar for confirmation (relevant only for the ATR Pivot Margin method).

5.5 Reward Inputs (Take Profit)

Show Take Profit 1/2/3: ON/OFF switch to control the visibility of each Take Profit target.

Reward/Risk Ratio 1/ 2/ 3: Defines the R/R ratio for the profit target. Must be ≥1.0.

6. Indicator Status/Warning Messages

In situations where the Stop Loss location cannot be calculated logically and validly, often caused by a mismatch between the configured Focused Trend (Uptrend/Downtrend) and the actual price action, the indicator will display a warning message, explaining the reason and suggesting corrective action.

Status Message 1: Pivot reference unavailable

Condition: The Stop Loss is set to the "ATR Pivot Margin" method, but the anchor point (Pivot) is missing or inaccessible.

Message Displayed: "Pivot reference unavailable. Wait for valid price action, or adjust the Regular Hours Limitation setting or Pivot Left/Right inputs."

Status Message 2: Calculated Stop Loss is unsafe

Condition: The calculated Stop Loss is placed illogically or unsafely relative to the trend direction and the Entry price.

Message Displayed: "Calculated Stop Loss is unsafe for current trend. Wait for valid price action or adjust SL Lookback/Multiplier."

7. Summary

The Adaptive Risk Management (ARM) indicator provides a seamless and systematic approach to trade execution and risk control. By dynamically automating all critical trade parameters—from Entry Price and Stop Loss placement to Position Sizing and Take Profit targets—ARM removes emotional bias and ensures every trade adheres strictly to your predefined risk profile.

Key Benefits:

Systematic Risk Control: Strict enforcement of maximum capital allocation and risk per trade limits.

Adaptivity: Dynamic calculation of prices and quantities based on real-time market data (ATR and Lookback).

Clarity and Trust: Clear on-chart visualization, precise data metrics (16 series), and unambiguous Status/Warning Messages ensure transparency and reliability.

ARM allows traders to focus on strategy and analysis, confident that their execution complies with the core principles of professional risk management.

Important Note: Trading Risk

This indicator is intended for educational and informational purposes only and does not constitute investment advice or a recommendation for trading in any form whatsoever.

Trading in financial markets involves significant risk of capital loss. It is important to remember that past performance is not indicative of future results. All trading decisions are your sole responsibility. Never trade with money you cannot afford to lose.

FAIR VALUE CEDEARSFair Value CEDEARS y ETFs

Important: load together with the CEDEARdata library.

Returns the “Fair Value” of CEDEAR and CEDEAR-based ETF prices traded on ByMA, using as a reference the price of the underlying ordinary share or ETF traded on the NYSE or NASDAQ. It multiplies the NYSE/NASDAQ price by the CEDEAR or ETF conversion ratio and converts the currency to ARS or Dólar MEP using the exchange rate implied by the AL30/AL30C ratio for tickers quoted in ARS (e.g., AAPL) and AL30D/AL30C for tickers quoted in Dólar MEP (e.g., AAPLD).

If the CEDEAR or ETF quote is higher than Fair Value, it highlights the difference in red; if it is lower, it highlights it in green. If any of the markets is closed or in an auction period, it notifies the user and changes the background color.

By default, the CEDEAR or ETF quote used is the last price, but the user may choose to use the BID or OFFER instead. This allows CEDEAR and ETF buyers to compare Fair Value against the OFFER, while sellers may prefer to measure Fair Value against the BID of the local instrument.

BCBA:AAPL

BCBA:AAPLD

NASDAQ:AAPL

BCBA:SPY

BCBA:TSLA

BCBA:TSLAD

CEDEARS

ETFs

ByMA

Absorption RatioThe Hidden Connections Between Markets

Financial markets are not isolated islands. When panic spreads, seemingly unrelated assets suddenly begin moving in lockstep. Stocks, bonds, commodities, and currencies that normally provide diversification benefits start falling together. This phenomenon, where correlations spike during crises, has devastated portfolios throughout history. The Absorption Ratio provides a quantitative measure of this hidden fragility.

The concept emerged from research at State Street Associates, where Mark Kritzman, Yuanzhen Li, Sebastien Page, and Roberto Rigobon developed a novel application of principal component analysis to measure systemic risk. Their 2011 paper in the Journal of Portfolio Management demonstrated that when markets become tightly coupled, the variance explained by the first few principal components increases dramatically. This concentration of variance signals elevated systemic risk.

What the Absorption Ratio Measures

Principal component analysis, or PCA, is a statistical technique that identifies the underlying factors driving a set of variables. When applied to asset returns, the first principal component typically captures broad market movements. The second might capture sector rotations or risk-on/risk-off dynamics. Additional components capture increasingly idiosyncratic patterns.

The Absorption Ratio measures the fraction of total variance absorbed or explained by a fixed number of principal components. In the original research, Kritzman and colleagues used the first fifth of the eigenvectors. When this fraction is high, it means a small number of factors are driving most of the market movements. Assets are moving together, and diversification provides less protection than usual.

Consider an analogy: imagine a room full of people having independent conversations. Each person speaks at different times about different topics. The total "variance" of sound in the room comes from many independent sources. Now imagine a fire alarm goes off. Suddenly everyone is talking about the same thing, moving in the same direction. The variance is now dominated by a single factor. The Absorption Ratio captures this transition from diverse, independent behavior to unified, correlated movement.

The Implementation Approach

TradingView does not support matrix algebra required for true principal component analysis. This implementation uses a closely related proxy: the average absolute correlation across a universe of major asset classes. This approach captures the same underlying phenomenon because when assets are highly correlated, the first principal component explains more variance by mathematical necessity.

The asset universe includes eight ETFs representing major investable categories: SPY and QQQ for large cap US equities, IWM for small caps, EFA for developed international markets, EEM for emerging markets, TLT for long-term treasuries, GLD for gold, and USO for oil. This selection provides exposure to equities across geographies and market caps, plus traditional diversifying assets.

From eight assets, there are twenty-eight unique pairwise correlations. The indicator calculates each using a rolling window, takes the absolute value to measure coupling strength regardless of direction, and averages across all pairs. This average correlation is then transformed to match the typical range of published Absorption Ratio values.

The transformation maps zero average correlation to an AR of 0.50 and perfect correlation to an AR of 1.00. This scaling aligns with empirical observations that the AR typically fluctuates between 0.60 and 0.95 in practice.

Interpreting the Regimes

The indicator classifies systemic risk into four regimes based on AR levels.

The Extreme regime occurs when the AR exceeds 0.90. At this level, nearly all asset classes are moving together. Diversification has largely failed. Historically, this regime has coincided with major market dislocations: the 2008 financial crisis, the 2020 COVID crash, and significant correction periods. Portfolios constructed under normal correlation assumptions will experience larger drawdowns than expected.

The High regime, between 0.80 and 0.90, indicates elevated systemic risk. Correlations across asset classes are above normal. This often occurs during the build-up to stress events or during volatile periods where fear is spreading but has not reached panic levels. Risk management should be more conservative.

The Normal regime covers AR values between 0.60 and 0.80. This represents typical market conditions where some correlation exists between assets but diversification still provides meaningful benefits. Standard portfolio construction assumptions are reasonable.

The Low regime, below 0.60, indicates that assets are behaving relatively independently. Diversification is working well. Idiosyncratic factors dominate returns rather than systematic risk. This environment is favorable for active management and security selection strategies.

The Relationship to Portfolio Construction

The implications for portfolio management are significant. Modern portfolio theory assumes correlations are stable and uses historical estimates to construct efficient portfolios. The Absorption Ratio reveals that this assumption is violated precisely when it matters most.

When AR is elevated, the effective number of independent bets in a diversified portfolio shrinks. A portfolio holding stocks, bonds, commodities, and real estate might behave as if it holds only one or two positions during high AR periods. Position sizing based on normal correlation estimates will underestimate portfolio risk.

Conversely, when AR is low, true diversification opportunities expand. The same nominal portfolio provides more independent return streams. Risk can be deployed more aggressively while maintaining the same effective exposure.

Component Analysis

The indicator separately tracks equity correlations and cross-asset correlations. These components tell different stories about market structure.

Equity correlations measure coupling within the stock market. High equity correlation indicates broad risk-on or risk-off behavior where all stocks move together. This is common during both rallies and selloffs driven by macroeconomic factors. Stock pickers face headwinds when equity correlations are elevated because individual company fundamentals matter less than market beta.

Cross-asset correlations measure coupling between different asset classes. When stocks, bonds, and commodities start moving together, traditional hedges fail. The classic 60/40 stock/bond portfolio, for example, assumes negative or low correlation between equities and treasuries. When cross-asset correlation spikes, this assumption breaks down.

During the 2022 market environment, for instance, both stocks and bonds fell significantly as inflation and rate hikes affected all assets simultaneously. High cross-asset correlation warned that the usual defensive allocations would not provide their expected protection.

Mean Reversion Characteristics

Like most risk metrics, the Absorption Ratio tends to mean-revert over time. Extremely high AR readings eventually normalize as panic subsides and assets return to more independent behavior. Extremely low readings tend to rise as some level of systematic risk always reasserts itself.

The indicator tracks AR in statistical terms by calculating its Z-score relative to the trailing distribution. When AR reaches extreme Z-scores, the probability of normalization increases. This creates potential opportunities for strategies that bet on mean reversion in systemic risk.

A buy signal triggers when AR recovers from extremely elevated levels, suggesting the worst of the correlation spike may be over. A sell signal triggers when AR rises from unusually low levels, warning that complacency about diversification benefits may be excessive.

Momentum and Trend

The rate of change in AR carries information beyond the absolute level. Rapidly rising AR suggests correlations are increasing and systemic risk is building. Even if AR has not yet reached the high regime, acceleration in coupling should prompt increased vigilance.

Falling AR momentum indicates normalizing conditions. Correlations are decreasing and assets are returning to more independent behavior. This often occurs in the recovery phase following stress events.

Practical Application

For asset allocators, the AR provides guidance on how much diversification benefit to expect from a given allocation. During high AR periods, reducing overall portfolio risk makes sense because the usual diversifiers provide less protection. During low AR periods, standard or even aggressive allocations are more appropriate.

For risk managers, the AR serves as an early warning indicator. Rising AR often precedes large market moves and volatility spikes. Tightening risk limits before correlations reach extreme levels can protect capital.

For systematic traders, the AR provides a regime filter. Mean reversion strategies may work better during high AR periods when panics create overshooting. Momentum strategies may work better during low AR periods when trends can develop independently across assets.

Limitations and Considerations

The proxy methodology introduces some approximation error relative to true PCA-based AR calculations. The asset universe, while representative, does not include all possible diversifiers. Correlation estimates are inherently backward-looking and can change rapidly.

The transformation from average correlation to AR scale is calibrated to match typical published ranges but is not mathematically equivalent to the eigenvalue ratio. Users should interpret levels directionally rather than as precise measurements.

Correlation regimes can persist longer than expected. Mean reversion signals indicate elevated probability of normalization but do not guarantee timing. High AR can remain elevated throughout extended crisis periods.

References

Kritzman, M., Li, Y., Page, S., and Rigobon, R. (2011). Principal Components as a Measure of Systemic Risk. Journal of Portfolio Management, 37(4), 112-126.

Kritzman, M., and Li, Y. (2010). Skulls, Financial Turbulence, and Risk Management. Financial Analysts Journal, 66(5), 30-41.

Billio, M., Getmansky, M., Lo, A., and Pelizzon, L. (2012). Econometric Measures of Connectedness and Systemic Risk in the Finance and Insurance Sectors. Journal of Financial Economics, 104(3), 535-559.

RiskCraft - Advanced Risk Management SystemRiskCraft – Risk Intelligence Dashboard

Trade like you actually respect risk

"I know the setup looks good… but how much am I actually risking right now?"

RiskCraft is an open-source Pine Script v6 indicator that keeps risk transparent directly on the chart. It is not a signal generator; it is a risk desk that calculates size, frames volatility, and reminds you when your behaviour drifts away from the plan.

Core utilities

Calculates professional-style position sizing in real time.

Reads volatility and market regime before position size is confirmed.

Adjusts risk based on the trader’s emotional state and confidence inputs.

Maps session risk across Asian, London, and New York hours.

Draws exactly one stop line and one target line in the preferred direction.

Provides rotating education tips plus contextual warnings when risk escalates.

It is intentionally conservative and keeps you in the game long enough for any separate entry logic to matter.

---

Chart layout checklist

Use a clean chart on a liquid symbol (e.g., AMEX:SPY or major FX pairs).

Main RiskCraft dashboard placed on the right edge.

Session Risk box on the left with UTC time visible.

Floating risk badge above price.

Stop/target guide lines enabled.

Education panel visible in the bottom-right corner.

---

1. On-chart components

Right-side dashboard : account risk %, position size/value, stop, target, risk/reward, regime, trend strength, emotional state, behavioural score, correlation, and preferred trade direction.

Session Risk box : highlights active session (Asian, London, NY), current UTC time, and risk label (High/Med/Low) per session.

Floating risk badge : keeps actual account risk percent visible with colour-coded wording from Ultra Cautious to Very Aggressive.

Stop/target lines : exactly one dashed stop and one dashed target aligned with the preferred bias.

Education panel : rotates core principles and AI-style warnings tied to volatility, risk %, and behaviour flags.

---

2. Volatility engine – ATR with context 📈

atr = ta.atr(atrLength)

atrPercent = (atr / close) * 100

atrSMA = ta.sma(atr, atrLength)

volatilityRatio = atr / atrSMA

isHighVol = volatilityRatio > volThreshold

ATR vs ATR SMA shows how wild price is relative to recent history.

Volatility ratio above the threshold flips isHighVol , which immediately trims risk.

An ATR percentile rank over the last 100 bars indicates calm versus chaotic regimes.

Daily ATR sampling via request.security() gives higher time-frame context for intraday sessions.

When volatility spikes the script dials position size down automatically instead of cheering for maximum exposure.

---

3. Market regime radar – Danger or Drift 🌊

ema20 = ta.ema(close, 20)

ema50 = ta.ema(close, 50)

ema200 = ta.ema(close, 200)

trendScore = (close > ema20 ? 1 : -1) +

(ema20 > ema50 ? 1 : -1) +

(ema50 > ema200 ? 1 : -1)

= ta.dmi(14, 14)

Regimes covered:

Danger : high volatility with weak trend.

Volatile : volatility elevated but structure still directional.

Choppy : low ADX and noisy action.

Trending : directional flows without extreme volatility.

Mixed : anything between.

Each regime maps to a 1–10 risk score and a multiplier that feeds the final position size. Danger and Choppy clamp size; Trending restores normal risk.

---

4. Behaviour engine – trader inputs matter 🧠

You provide:

Emotional state : Confident, Neutral, FOMO, Revenge, Fearful.

Confidence : slider from 1 to 10.

Toggle for behavioural adjustment on/off.

Behind the scenes:

Each state triggers an emotional multiplier .

Confidence produces a confidence multiplier .

Combined they form behavioralFactor and a 0–100 Behavioural Score .

High-risk emotions or low conviction clamp the final risk. Calm inputs allow normal size. The dashboard prints both fields to keep accountability on-screen.

---

5. Correlation guardrail – avoid stacking identical risk 📊

Optional correlation mode compares the active symbol to a reference (default AMEX:SPY ):

corrClose = request.security(correlationSymbol, timeframe.period, close)

priceReturn = ta.change(close) / close

corrReturn = ta.change(corrClose) / corrClose

correlation = calcCorrelation()

Absolute correlation above the threshold applies a correlation multiplier (< 1) to reduce size.

Dashboard row shows the live correlation and reference ticker.

When disabled, the row simply echoes the current symbol, keeping the table readable.

---

6. Position sizing engine – heart of the script 💰

baseRiskAmount = accountSize * (baseRiskPercent / 100)

adjustedRisk = baseRiskAmount * behavioralFactor *

regimeAdjustment * volAdjustment *

correlationAdjustment

finalRiskAmount = math.min(adjustedRisk,

accountSize * (maxRiskCap / 100))

stopDistance = atr * atrStopMultiplier

takeProfit = atr * atrTargetMultiplier

positionSize = stopDistance > 0 ? finalRiskAmount / stopDistance : 0

positionValue = positionSize * close

Outputs shown on the dashboard:

Position size in units and value in currency.

Actual risk % back on account after adjustments.

Risk/Reward derived from ATR-based stop and target.

---

7. Intelligent trade direction – bias without signals 🎯

Direction score ingredients:

EMA stack alignment.

Price versus EMA20.

RSI momentum relative to 50.

MACD line vs signal.

Directional Movement (DI+/DI–).

The resulting Trade Direction row prints LONG, SHORT, or NEUTRAL. No orders are generated—this is guidance so you only risk capital when the structure supports it.

---

8. Stop/target guide lines – two lines only ✂️

if showStopLines

if preferLong

// long stop below, target above

else if preferShort

// short stop above, target below

Lines refresh each bar to keep clutter low.

When the direction score is neutral, no lines appear.

Use them as visual anchors, not auto-orders.

---

9. Session Risk map – global volatility clock 🌍

Tracks Asian, London, and New York windows via UTC.

Computes average ATR per session versus global ATR SMA.

Labels each session High/Med/Low and colours the cells accordingly.

Top row shows the active session plus current UTC time so you always know the regime you are trading.

One glance tells you whether you are trading quiet drift or the part of the day that hunts stops.

---

10. Floating risk badge – honesty above price 🪪

Text ranges from Ultra Cautious through Very Aggressive.

Colour matches the risk palette inputs (High/Med/Low).

Updates on the last bar only, keeping historical clutter off the chart.

Account risk becomes impossible to ignore while you stare at price.

---

11. Education engine & warnings 📚

Rotates evergreen principles (risk 1–2%, journal trades, respect plan).

Triggers contextual warnings when volatility and risk % conflict.

Flags when emotional state = FOMO or Revenge.

Highlights sub-standard risk/reward setups.

When multiple danger flags stack, an AI-style warning overrides the tip text so you can course-correct before capital is exposed.

---

12. Alerts – hard guard rails 🚨

Excessive Risk Alert : actual risk % crosses custom threshold.

High Volatility Alert : ATR behaviour signals danger regime.

Emotional State Warning : FOMO or Revenge selected.

Poor Risk/Reward Alert : risk/reward drops below your standard.

All alerts reinforce discipline; none suggest entries or exits.

---

13. Multi-market behaviour 🕒

Intraday (1m–1h): session box and badge react quickly; ideal for scalpers needing constant risk context.

Higher time frames (1D–1W): dashboard shifts slowly, supporting swing planning.

Asset classes confirmed in validation: crypto majors, large-cap equities, indices, major FX pairs, and liquid commodities.

Risk logic is price-based, so it adapts across markets without bespoke tuning.

15. Key inputs & recommended defaults

Account Size : 10,000 (modify to match actual account; min 100).

Base Risk % : 1.0 with a Maximum Risk Cap of 2.5%.

ATR Period : 14, Stop Multiplier 2.0, Target Multiplier 3.0.

High Vol Threshold : 1.5 for ATR ratio.

Behavioural Adjustment : enabled by default; disable for fixed risk.

Correlation Check : optional; default symbol AMEX:SPY , threshold 0.7.

Display toggles : main dashboard, risk badge, session map, education panel, and stop lines can be individually disabled to reduce clutter.

16. Usage notes & limits

Indicator mode only; no automated entries or exits.

Trade history panel intentionally disabled (requires strategy context).

Correlation analysis depends on additional data requests and may lag slightly on illiquid symbols.

Session timing uses UTC; adjust expectations if you trade localized instruments.

HTF ATR sampling uses daily data, so bar replay on lower charts may show brief data gaps while HTF loads.

What does everyone think RISK really means?

SmartDCA by TradeAkademiSmartDCA is an advanced position-management strategy built to deliver consistent results even as market conditions shift. Its price-action–driven structure, intelligent DCA scaling model, and multiple entry options provide a powerful automation framework suitable for both beginners and professional traders. With flexible TP/DCA configurations and safety modules such as Smart Take Profit, Risk Reset Exit, and Fail Safe Stop, positions scale more efficiently, risks are managed proactively, and capital remains protected at every stage. SmartDCA is a fully customizable, modern trading engine that offers high adaptability across different assets and timeframes.

The strategy supports five entry methodologies:

ta_default – Opens positions on breakout confirmations based on the selected period’s local highs and lows.

ta_volatility – Uses the same breakout logic while filtering entries that would place the target level outside the system’s defined safety zone.

ta_safety – Extends the volatility model with an additional candle-quality filter, avoiding structurally weak entries and behaving more conservatively.

rsi_based – Generates entries when RSI drops below 30 or rises above 70.

ema_based – Opens positions based on directional shifts in the moving average.

SmartDCA is fully configurable: entry logic, DCA percentage and multiplier, take-profit (TP) settings, maximum DCA steps, order-size mode, and directional preferences can all be tailored to fit any asset, market condition, or timeframe .

Default parameters are optimized for the 30-minute chart.

The strategy also includes three optional protective mechanisms:

Smart Take Profit – Closes profitable trades early when price approaches the target within a configurable proximity, reducing exposure to potential reversal signals.

Risk Reset Exit – After a defined DCA step, the position is closed at breakeven once price returns to the average entry level.

Fail Safe Stop – If the maximum DCA step is reached and recovery fails to occur, the trade is closed at a controlled loss.

All protection modules can be enabled individually and configured to activate only after specific DCA levels, allowing SmartDCA to remain adaptive yet controlled under varying market dynamics.

Universal_Position Size Calculator_by PaulinusFTMO Position Size Calculator - Professional Risk Management Tool

The ultimate position sizing calculator designed specifically for FTMO traders and professional risk managers.

🎯 What Does This Indicator Do?

This powerful calculator automatically determines the exact lot size you should trade based on your account size, risk tolerance, and stop loss distance. No more manual calculations or guesswork - just enter your trade parameters and get instant, accurate position sizing.

✨ Key Features

📈 Two Calculation Methods:

Entry/Stop Price Method: Enter your exact entry and stop loss prices - perfect for planned trades

Stop Loss Pips Method: Simply enter your stop loss distance in pips - ideal for quick calculations

💰 Complete Risk Management:

Calculates precise position size in lots

Shows actual dollar risk amount

Displays potential profit based on your risk:reward ratio

Automatic risk percentage calculation

Real-time updates as you adjust parameters

🌍 Multi-Asset Support:

Cryptocurrencies: BTC, ETH, XRP, LTC, BCH, BNB, ADA

Forex Pairs: All major and cross pairs (EUR/USD, GBP/USD, USD/JPY, etc.)

Commodities: Gold (XAU/USD), Oil (USOIL)

Indices: US30, US100, SPX500

🎨 Professional Interface:

Clean, easy-to-read table display

Customizable position (9 locations on chart)

Adjustable text size (Tiny, Small, Normal, Large)

Toggle detailed breakdown on/off for simplified view

Visual entry, stop loss, and take profit lines on chart

🔧 FTMO-Optimized:

Pre-configured with accurate FTMO contract specifications

Built-in contract sizes for all supported instruments

Minimum lot size requirements automatically applied

Perfect for FTMO Challenge and Verification phases

📋 How To Use

Method 1: Entry/Stop Price

Select your trading pair

Enter your account balance

Set your risk percentage (typically 1-2% for FTMO)

Choose your risk:reward ratio (e.g., 1:2, 1:3)

Enter your planned entry price

Enter your stop loss price

Get instant position size in lots!

Method 2: Stop Loss Pips

Select your trading pair

Enter your account balance

Set your risk percentage

Choose your risk:reward ratio

Enter your stop loss distance in pips

Get instant position size in lots!

📊 What You'll See

Essential Information (Always Visible):

Trading Pair

Account Balance

Risk Percentage

Risk Amount in Dollars

Target Profit Ratio

POSITION SIZE IN LOTS ⬅️ Your main result

Detailed Breakdown (Optional):

Entry Price / Stop Loss / Take Profit

Stop Loss Distance in pips

Contract Size

Actual Risk Amount

Potential Profit in Dollars

🎓 Perfect For:

✅ FTMO Challenge traders

✅ Prop firm traders

✅ Professional risk managers

✅ Swing and day traders

✅ Anyone who wants consistent position sizing

✅ Traders working on passing funded accounts

💡 Why Use This Calculator?

Eliminate Calculation Errors: No more spreadsheets or manual math - get accurate results instantly.

Stay Consistent: Maintain proper risk management on every single trade.

Save Time: Calculate position sizes in seconds, not minutes.

Protect Your Capital: Never risk more than your intended percentage.

Maximize Efficiency: Focus on trading, not calculating.

⚠️ Important Notes

This calculator uses standard FTMO contract specifications

Always verify lot sizes with your broker before placing trades

Recommended risk per trade: 1-2% for FTMO accounts

The calculator rounds to minimum lot sizes automatically

Visual lines only appear when using Entry/Stop Price method

🔒 Professional Tool

This is a protected indicator with clean, optimized code designed for serious traders who value accuracy and efficiency.

📝 Settings Guide

Table Position: Choose where the calculator appears on your chart

Table Text Size: Adjust for your screen and preference

Calculation Method: Switch between price-based or pip-based calculations

Account Balance: Your total account size

Risk Per Trade: Percentage you're willing to risk (0.1% - 5%)

TP Risk:Reward Ratio: Your target profit ratio (e.g., 2 = 1:2 RR)

Show Detailed Breakdown: Toggle extra information on/off

🚀 Start Trading With Confidence

Stop guessing your position sizes. Start using professional risk management today.

⭐ If this indicator helps your trading, please leave a review and share it with fellow traders!

By Paulinus © 2025

SOFR - IORB Spread (pct pts & bps)Tracks short-term funding conditions by measuring the spread between the Secured Overnight Financing Rate (SOFR) and the Fed’s Interest on Reserve Balances (IORB). When SOFR persistently trades above IORB, it signals cash scarcity and stress in overnight funding markets. This indicator is best used as a risk-regime and plumbing health check, not as a directional trading signal. Calm readings allow trends to persist; sustained spikes often precede periods of volatility and forced deleveraging.

Universal Lot Size Calculator (Forex, Index, Metals)Multi-functional lot size calculator with support for various instruments

🎯 MAIN FEATURES:

Universal — works with Forex, indices, metals, and custom instruments

Auto-detect — automatically detects instrument type by ticker

Precise position sizing - considering risk and currency conversions

Currency conversion — automatic conversion between deposit currencies

Advanced visualization — entry, stop-loss, take-profit lines

Smart table — convenient display of all parameters

⚙️ SETTINGS GROUPS:

📈 Instrument Settings

Instrument Type — selection: Auto, Forex, Index, Metals, Custom

Custom Contract Size — manual contract size configuration

Use Manual Exchange Rate — manual rate for currency conversion

💰 Account & Risk Settings

Deposit Currency — account currency (USD, EUR, GBP, CHF, JPY)

Account Size — deposit amount

Risk in % — risk percentage from deposit

🎯 Price Levels

Entry Price — entry price

Stop Price — stop-loss price

Target Price — take-profit price

Color settings for each line

📊 Risk/Reward Settings

Manual Target Price — manual TP setting

Show R Levels — display profit levels in R multiples

Show only last R level — show only the last R level

Number of R Levels — number of R levels (1-10)

🎨 Line Styles & Table Appearance

Line style settings (solid, dashed, dotted)

Line width

Table position and size

Color schemes

📈Supported instrument types:

Forex — standard lot 100,000

Indices — E-mini futures (US100=20, SP500=50, US30=5, DAX=25)

Metals — Gold=100 oz, Silver=5000 oz

Custom — user-defined contract size

📱 KEY FEATURES:

- Auto instrument detection:

Indices: US100, SP500, US30, DAX

Metals: XAUUSD (Gold), XAGUSD (Silver)

Forex: all currency pairs

- Smart table with key parameters:

Instrument type and contract size

Account size and risk

Entry/exit prices

Calculated lot size

- Visual elements:

Dynamic level lines

Labels with profit/loss calculations

R-levels for target prices

- Currency conversion:

Automatic rate fetching

Support for USD, EUR, GBP, CHF, JPY

Manual rate setting when needed

⚠️ IMPORTANT NOTES:

Contract sizes may vary between brokers

For CFD brokers use Custom type with Contract Size = 1

During weekends currency rates may be unavailable — use manual rate

When trading in different currencies verify conversion accuracy

🚀 HOW TO USE:

Select instrument type (Auto for auto-detection)

Set deposit size and account currency

Define risk percentage (1-100%)

Specify prices for entry, stop-loss, and take-profit

Use calculated lot to open positions

⚠️ RESETTING CALCULATIONS:

To reuse the calculator with new price levels, you need to:

Right-click on the indicator's table/chart

Select "Reset Points" from the context menu

OR manually update all three price levels (Entry, Stop Loss, Take Profit) in the settings

MPT Efficient FrontierAMEX:VT

Efficient Frontier: The Tool for Creating a "Superb" Portfolio

The Efficient Frontier is a vital concept in the world of investment that helps investors build a Portfolio—a collection of investment assets—that provides the best possible return for a given level of acceptable risk. This concept stems from the Modern Portfolio Theory (MPT), developed by Nobel laureate in Economics, Harry Markowitz.

What is the Efficient Frontier?

Imagine all the possible investment combinations you can put together. Each portfolio combination has a different level of risk (measured by volatility or Standard Deviation) and a different expected return.

When you plot all these possible portfolios on a graph, with the horizontal axis representing Risk and the vertical axis representing Return, you get a cloud of points (portfolios).

The Efficient Frontier is the curve that sits on the upper-most and left-most boundary of this cloud of points.

"Upper-most" means that the portfolios on this line provide the maximum return for that specific level of risk.

"Left-most" means that the portfolios on this line have the lowest risk for a given return.

Simply put, a portfolio lying on the Efficient Frontier is considered "Efficient" because no other portfolio exists that can offer a higher return at the s ame level of risk, or lower risk at the same level of return.

How to Use the Efficient Frontier

Investors use the Efficient Frontier to help them decide on the optimal portfolio for their needs. The key steps are:

1. Data Collection and Generating Possible Portfolios

Collect Data: Use historical data (or future projections) for the assets you are interested in (e.g., stocks, bonds, funds) to calculate their Expected Return, Risk (Standard Deviation), and, most importantly, the Correlation between the different assets.

Simulate Portfolios: Use computers or mathematical programs to simulate thousands or tens of thousands of different asset mix proportions to find all possible portfolio points.

2. Finding the "Minimum Variance Portfolio" (MVP)

The Minimum Variance Portfolio (MVP) is the point on the frontier with the absolute lowest risk (the far-left point on the curve). Investors with a very low risk tolerance might focus on this portfolio.

3. Finding the "Optimal Portfolio" for You

Once the Efficient Frontier is established, investors must select the point on the line that aligns with their personal Risk Tolerance.

Risk-Averse Investors: Will choose points on the left side of the curve (low risk and moderate return).

Risk-Tolerant Investors: Will choose points on the right side of the curve (high risk and high return).

Visualization Elements:

🔴 Red/Orange/Yellow/Green Dots => Each dot represents 1 portfolio combination. Plotted according to Risk (X-axis) and Return (Y-axis).

Color Coding by Sharpe Ratio => 🟢 Green: Sharpe > 2

🟡 Yellow: Sharpe 1-2

🟠 Orange: Sharpe 0-1

🔴 Red: Sharpe < 0

⬤ Large Yellow DotRepresents the MAX SHARPE RATIO—the Optimal Portfolio! Lying on the Efficient Frontier curve. Labeled with " Efficient Frontier".

❶❷❸❹ Colored Circles => Represents the Individual Assets (e.g., Blue, Red, Green, Purple).

■ Blue Square => Represents the Current Portfolio location.

Four Data Tables

1. Optimal Weights Table => Compares Current vs. Optimal weights for each asset. Weights Comparison: Green = Should increase weight. Red = Should decrease weight.

Max Sharpe (Current and Optimal).

2.Performance Comparison => Return, Risk, Sharpe for Current vs. Optimal portfolios.Improvement Metrics: Return (percent increase), Risk (percent decrease), Sharpe (percent improvement).Recommendation: 🚀 REBALANCE! (Score > 20); Consider (5-20); Maintain (< 5).

3.Correlation Matrix => Displays the Correlation between all assets. Helps assess Diversification.

4.Asset Statistics => Provides detailed statistics for Each Individual Asset.

Daily Dollar Cost Averaging (DCA) Simulator & Yearly PerformanceThis indicator simulates a "Daily Dollar Cost Averaging" strategy directly on your chart. Unlike standard backtesters that trade based on signals, this script calculates the performance of a portfolio where a fixed dollar amount is invested every single day, regardless of price action.

Key Features:

Daily Accumulation: Simulates buying a specific dollar amount (e.g., $10) at the market close every day.

Yearly Breakdown Table: A detailed dashboard displayed on the chart that breaks down performance by year. It tracks total invested, average entry price, total holdings, current value, and PnL percentage for each individual year.

Global Stats: The bottom row of the table summarizes the total performance of the entire strategy since the start date.

Breakeven Line: Plots a yellow line on the chart representing your "Global Average Price." When the current price is above this line, the total strategy is in profit.

How to Use:

Add to chart (Works best on the Daily (D) timeframe).

Open settings to adjust your Daily Investment Amount and Start Year.

The table will automatically update to show how a daily investment strategy would have performed over time.

Position Size Calculator - Fixed Risk Per BarThis indicator calculates the max contracts allowed per bar based on your determined fixed risk.

Dual Account Position Size CalculatorA quick and easy to use position sizing calculator for use on the daily TF only. inputs for two different account sizes and risk %. Calculates risk to low of day (plus a small buffer which can be changed based on ATR). Shows # of shares to buy, stop loss, portfolio %.

Will show on smaller timeframes , but be aware that the stop level will no longer be low of day, so it will not calculate properly. Always use on the daily.

Monthly DCA & Last 10 YearsThis Pine Script indicator simulates a Monthly Dollar Cost Averaging (DCA) strategy to help long-term investors visualize historical performance. Instead of complex timing, the script automatically executes a hypothetical fixed-dollar purchase (e.g., $100) on the first trading day of every month. It visually marks entry points with green "B" labels and plots a dynamic yellow line representing your Global Break-Even Price, allowing you to instantly see if the current price is above or below your average cost basis. To provide deep insight, it generates a detailed performance table in the bottom-right corner that breaks down metrics year-by-year—including total capital invested, shares/coins accumulated, and Profit/Loss percentage—along with a grand total summary of the entire investment period.

Weekly DCA & Yearly TableThis Pine Script indicator simulates a Weekly Dollar Cost Averaging (DCA) strategy directly on your TradingView chart. It automatically calculates a hypothetical portfolio where a fixed dollar amount (default $100) is invested every Friday (or the last trading day of the week) starting from a user-defined year. Visually, it marks every purchase with a green "B" label and plots a yellow line representing your Global Break-Even Price, allowing you to see exactly where your average entry lies relative to current price action. To track performance, it generates a detailed table in the bottom-right corner that breaks down your investment year-by-year, showing total capital invested, "coins" or shares accumulated, average buy price per year, current value, and profit/loss percentage, along with a grand total summary for the entire period.

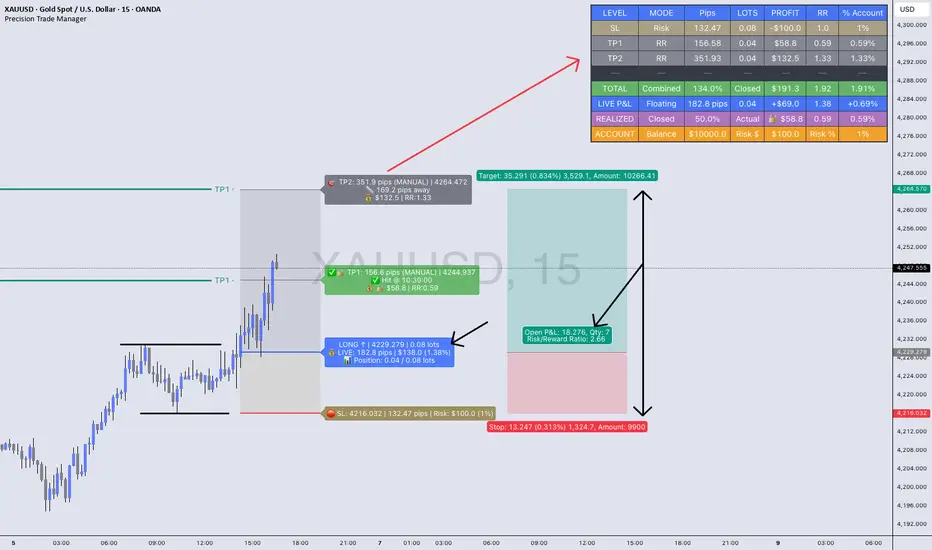

Precision Trade Manager🔥Precision Trade Manager is a complete execution - planning and trade-management system for TradingView.

It gives you full control over entry, stop-loss, position sizing, risk %, multi-TP planning (1–5), live tracking, realized profit, floating P&L, RR, and account % change — all directly on your chart.

Because this tool has many features and workflows, the TradingView description is too short to explain everything properly.

For that reason, please read the two PDF guides below before using the indicator.

They explain exactly how the tool works, how to set it up correctly, and how to avoid mistakes when planning or managing trades.

📘 PDF 1 — Quick Start Guide (Read First)

drive.google.com

This guide explains the core workflow step-by-step:

✔ How to add the tool to the chart

✔ How to configure assets, contract size, account balance, and trading costs

✔ How to set Entry, SL, and your risk %

✔ How to set TP1–TP5 using RR mode or manual mode

✔ How partials work

✔ How LIVE TRACKING mode works

✔ How to reset and prepare your next trade

This PDF teaches you the correct operational flow, so you understand how Precision Trade Manager behaves on the chart and why certain features exist.

Reading this first prevents confusion and ensures you use the tool correctly.

📙 PDF 2 — Feature Overview & Visual Examples

drive.google.com

This PDF gives a full breakdown of everything the tool is capable of:

✔ Real-time dashboard metrics (pips, lots, RR, profit, % account)

✔ Partial TP tracking with green checkmarks and locked profit

✔ Floating vs. locked mode

✔ Pip/point/currency conversions across Gold, Forex, Indices, and Crypto

✔ Example charts for US30, EURUSD, and XAUUSD

✔ A direct comparison against the TradingView Long/Short tool

This document is visual. It shows real examples of the tool in action so you understand what to expect once you’re using it live on your chart.

It is highly recommended to look through this PDF before your first trade. It will help you understand the dashboard, interpret every metric, and recognize the benefits versus the default TradingView tools.

(The tool has many (!) tooltips, hower mouse over each. To get a clear description of what each function/button/box do)

JRien Position Sizer (Real-Time) — ATR / LOD / Manual % $ RiskReal time position sizing based on real time potential entry price and calculations based on max risk. Usable on multi timeframes. You can also input manually your entry and stop based on your own discretion. I usually use a spreadsheet to calculate these things but wanted a way to see this in real time without needing to type out Entry, ATR, Stops, etc - TradingView has all this information already so why not just have it automatically update!

4 Stop Types:

ATR Based Stop

Based on the stocks ATR (mainly used on daily charts but options if you use other timeframe ATR) and uses a multiple of that ATR to base the plot. Many traders use less than 0.6ATR to base your stop as a rule and max entry 60% from LOD as another rule.

Manual Percent Stop

You're able to input your desired % stop and this will dynamically move with the current entry (last) price.

Manual Price Stop