Mystic Pulse V2.0 [CHE] Mystic Pulse V2.0 — Adaptive DI streaks with gradient intensity for clearer trend persistence

Summary

Mystic Pulse V2.0 measures directional persistence by counting how often the positive or negative directional index strengthens and dominates. These counts drive gradient colors for bars, wicks, and helper plots, so intensity reflects local momentum rather than absolute values. A windowed normalization and gamma control adapt the visuals to recent conditions, preventing one regime from overpowering the next. The result is an immediate, at-a-glance read of trend direction and stamina without relying on crossovers alone.

Motivation: Why this design?

Classical DI and ADX signals can flip during choppy phases or feel sluggish in calm regimes. This script focuses on persistence: it increments a positive or negative streak only when the corresponding directional pressure both strengthens compared with the prior bar and dominates the other side. Simple OHLC pre-smoothing reduces micro-noise, and local normalization keeps the scale relevant to the last segment of data, not a distant past.

What’s different vs. standard approaches?

Reference baseline: Traditional DI and ADX lines with crossovers and fixed-scale thresholds.

Architecture differences:

Wilder-style recursive smoothing on true range and directional movement.

Streak counters for positive and negative pressure that advance only on strengthening and dominance.

Windowed normalization and gamma shaping for visual intensity.

Wick coloring via `plotcandle` with forced overlay from a pane indicator.

Practical effect: Bars and wicks grow more vivid during sustained pressure and fade during indecision. The column plots show streak depth directly, which helps filter one-bar flips.

How it works (technical)

1. Pre-smoothing: Open, high, low, and close are averaged over a short simple moving window to dampen micro-ticks.

2. Directional inputs: True range and directional movement are formed from the smoothed prices, then recursively smoothed using a Wilder-style update that carries prior state forward.

3. DI comparison: The script derives positive and negative directional ratios relative to smoothed range. A side advances its streak when it increases compared with the previous bar and exceeds the opposite side. The other streak resets.

4. Trend score and color base: The difference between positive and negative streaks defines the active side.

5. Normalization and gamma: The absolute streak magnitude and each side’s streak are normalized within a rolling window. Gamma parameters reshape intensity so mid-range values are either compressed or emphasized.

6. Rendering:

Two column plots show positive and negative streak counts in the pane with gradient colors.

A square marker at the bottom uses the global gradient as a compact heat cue.

Bar colors on the main chart use either the gradient, neutral trend colors, or no paint depending on toggles.

Wick, border, and candle overlays are colored via `plotcandle` with forced overlay.

7. State handling: Smoothed values and counters persist across bars; initialization uses first available values without lookahead. No higher-timeframe requests are used, so repaint risk is limited to normal live-bar evolution.

Parameter Guide

Show neutral candles (fallback) — Paints main-chart bars in plain up or down colors when gradients are disabled — Default false — Use when you prefer simple up/down coloring.

Show last N shapes — Limits bottom square markers — Default 333 — Reduce if your chart gets cluttered.

ADX smoothing length — Controls the Wilder smoothing window for range and directional movement — Default 9 — Larger values increase stability but respond later.

OHLC SMA length — Pre-smoothing for inputs — Default 1 — Increase slightly on noisy assets to reduce flip risk.

Gradient barcolor — Enables gradient bar paint on the main chart — Default true — Turn off to use wicks only or neutral bars.

Wick coloring — Colors wicks, borders, and bodies via overlay — Default true — Disable if it conflicts with other overlays.

Gradient window — Lookback for local normalization — Default 100 — Shorter windows adapt faster; longer windows provide steadier intensity.

Gradient transparency — Overall transparency for gradient paints — Default 0 — Increase to make gradients subtler.

Gamma bars/shapes — Contrast for bar and shape intensity — Default 0.70 — Lower values brighten mid-tones; higher values compress them.

Gamma plots — Contrast for the column plots — Default 0.80 — Tune separately from bar intensity.

Wick transparency — Transparency for wick coloring — Default 0 — Raise to let price action show through.

Up/Down colors (dark and neon) — Base and accent colors for both directions — Defaults as provided — Adjust to match your chart theme.

Reading & Interpretation

Pane columns: The green column represents the positive streak count; the red column represents the negative streak count. Taller columns signal stronger persistence.

Gradient marker: The bottom square indicates the active side and persistence strength at a glance.

Main-chart bars and wicks: Color direction shows the dominant side; intensity reflects the normalized and gamma-shaped streak magnitude. Faded tones suggest weak or fading pressure.

Practical Workflows & Combinations

Trend following: Enter in the direction of the active side when the corresponding column expands over several bars. Confirm with structure such as higher highs and higher lows or lower highs and lower lows.

Exits and stops: Consider scaling out when intensity fades toward mid-range while structure stalls. Tighten stops after extended streaks or when wicks lose intensity.

Multi-asset/Multi-TF: Use defaults for liquid assets on intraday to swing timeframes. For highly volatile instruments, raise smoothing and the normalization window. For calm markets, lower them to regain sensitivity.

Behavior, Constraints & Performance

Repaint/confirmation: Values update during the live bar and stabilize after bar close. No historical repaint beyond normal live-bar updates.

security()/HTF: Not used; cross-timeframe repaint paths do not apply.

Resources: Declared `max_bars_back` two thousand; no explicit loops or arrays; plot and label limits are generous.

Known limits: Streak counters can remain elevated during slow reversals. Very short normalization windows can cause rapid intensity swings. Gaps or extreme spikes may temporarily distort intensity until the window adapts.

Sensible Defaults & Quick Tuning

Start with: ADX smoothing nine, OHLC SMA one, normalization window one hundred, gradient and wick coloring enabled, gamma around zero point seven to zero point eight.

Too many flips: Increase ADX smoothing and the normalization window; consider a small bump in OHLC SMA.

Too sluggish: Decrease ADX smoothing and the normalization window.

Colors overpower chart: Increase gradient and wick transparency or raise gamma to compress mid-tones.

What this indicator is—and isn’t

This is a visualization and signal layer that represents directional persistence and intensity. It does not issue trade entries or exits on its own and is not predictive. Use it alongside market structure, volume, and risk controls.

Disclaimer

The content, including any code, is for educational and informational purposes only and does not constitute financial advice or a recommendation to buy or sell any instrument. Trading involves substantial risk, including the possible loss of principal. Past performance is not indicative of future results. Always do your own research and consider consulting a qualified professional.

Search in scripts for "gaps"

Adaptive Heikin Ashi [CHE]Adaptive Heikin Ashi — volatility-aware HA with fewer fake flips

Summary

Adaptive Heikin Ashi is a volatility-aware reinterpretation of classic Heikin Ashi that continuously adjusts its internal smoothing based on the current ATR regime, which means that in quiet markets the indicator reacts more quickly to genuine directional changes, while in turbulent phases it deliberately increases its smoothing to suppress jitter and color whipsaws, thereby reducing “noise” and cutting down on fake flips without resorting to heavy fixed smoothing that would lag everywhere.

Motivation: why adapt at all?

Classic Heikin Ashi replaces raw OHLC candles with a smoothed construction that averages price and blends each new candle with the previous HA state, which typically cleans up trends and improves visual coherence, yet its fixed smoothing amount treats calm and violent markets the same, leading to the usual dilemma where a setting that looks crisp in a narrow range becomes too nervous in a spike, and a setting that tames high volatility feels unnecessarily sluggish as soon as conditions normalize; by allowing the smoothing weight to expand and contract with volatility, Adaptive HA aims to keep candles readable across shifting regimes without constant manual retuning.

What is different from normal Heikin Ashi?

Fixed vs. adaptive blend:

Classic HA implicitly uses a fixed 50/50 blend for the open update (`HA_open_t = 0.5 HA_open_{t-1} + 0.5 HA_close_{t-1}`), while this script replaces the constant 0.5 with a dynamic weight `w_t` that oscillates around 0.5 as a function of observed volatility, which turns the open update into an EMA-like filter whose “alpha” automatically changes with market conditions.

Volatility as the steering signal:

The script measures volatility via ATR and compares it to a rolling baseline (SMA of ATR over the same length), producing a normalized deviation that is scaled by sensitivity, clamped to ±1 for stability, and then mapped to a bounded weight interval ` `, so the adaptation is strong enough to matter but never runs away.

Outcome that matters to traders:

In high volatility, the weight shifts upward toward the prior HA open, which strengthens smoothing exactly where classic HA tends to “chatter,” while in low volatility the weight shifts downward toward the most recent HA close, which speeds up reaction so quiet trends do not feel artificially delayed; this is the practical mechanism by which noise and fake signals are reduced without accepting blanket lag.

How it works

1. HA close matches classic HA:

`HA_close_t = (Open_t + High_t + Low_t + Close_t) / 4`

2. Volatility normalization:

`ATR_t` is computed over `atr_length`, its baseline is `ATR_SMA_t = SMA(ATR, atr_length)`, and the raw deviation is `(ATR_t / ATR_SMA_t − 1)`, which is then scaled by `adapt_sensitivity` and clamped to ` ` to obtain `v_t`, ensuring that pathological spikes cannot destabilize the weighting.

3. Adaptive weight around 0.5:

`w_t = 0.5 + oscillation_range v_t`, giving `w_t ∈ `, so with a default `range = 0.20` the weight stays between 0.30 and 0.70, which is wide enough to matter but narrow enough to preserve HA identity.

4. EMA-like open update:

On the very first bar the open is seeded from a stable combination of the raw open and close, and thereafter the update is

`HA_open_t = w_t HA_open_{t−1} + (1 − w_t) HA_close_{t−1}`,

which is equivalent to an EMA where higher `w_t` means heavier inertia (more smoothing) and lower `w_t` means stronger pull to the latest price information (more responsiveness).

5. High and low follow classic HA composition:

`HA_high_t = max(High_t, max(HA_open_t, HA_close_t))`,

`HA_low_t = min(Low_t, min(HA_open_t, HA_close_t))`,

thereby keeping visual semantics consistent with standard HA so that your existing reading of bodies, wicks, and transitions still applies.

Why this reduces noise and fake signals in practice

Fake flips in HA typically occur when a fixed blending rule is forced to process candles during a volatility surge, producing rapid alternations around pivots or within wide intrabar ranges; by increasing smoothing exactly when ATR jumps relative to its baseline, the adaptive open stabilizes the candle body progression and suppresses transient color changes, while in the opposite scenario of compressed ranges, the reduced smoothing allows small but persistent directional pressure to reflect in candle color earlier, which reduces the tendency to enter late after multiple slow transitions.

Parameter guide (what each input really does)

ATR Length (default 14): controls both the ATR and its baseline window, where longer values dampen the adaptation by making the baseline slower and the deviation smaller, which is helpful for noisy lower timeframes, while shorter values make the regime detector more reactive.

Oscillation Range (default 0.20): sets the maximum distance from 0.5 that the weight may travel, so increasing it towards 0.25–0.30 yields stronger smoothing in turbulence and faster response in calm periods, whereas decreasing it to 0.10–0.15 keeps the behavior closer to classical HA and is useful if your strategy already includes heavy downstream smoothing.

Adapt Sensitivity (default 6.0): multiplies the normalized ATR deviation before clamping, such that higher sensitivity accelerates adaptation to regime shifts, while lower sensitivity produces gradual transitions; negative values intentionally invert the mapping (higher vol → less smoothing) and are generally not recommended unless you are testing a counter-intuitive hypothesis.

Reading the candles and the optional diagnostic

You interpret colors and bodies just like with normal HA, but you can additionally enable the Adaptive Weight diagnostic plot to see the regime in real time, where values drifting up toward the upper bound indicate a turbulent context that is being deliberately smoothed, and values gliding down toward the lower bound indicate a calm environment in which the indicator chooses to move faster, which can be valuable for discretionary confirmation when deciding whether a fresh color shift is likely to stick.

Practical workflows and combinations

Trend-following entries: use color continuity and body expansion as usual, but expect fewer spurious alternations around news spikes or into liquidity gaps; pairing with structure (swing highs/lows, breaks of internal ranges) keeps entries disciplined.

Exit management: when the diagnostic weight remains elevated for an extended period, you can be stricter with exit triggers because flips are less likely to be accidental noise; conversely, when the weight is depressed, consider earlier partials since the indicator is intentionally more nimble.

Multi-asset, multi-TF: the adaptation is especially helpful if you rotate instruments with very different vol profiles or hop across timeframes, since you will not need to retune a fixed smoothing parameter every time conditions change.

Behavior, constraints, and performance

The script does not repaint historical bars and uses only past information on closed candles, yet just like any candle-based visualization the current live bar will update until it closes, so you should avoid acting on mid-bar flips without a rule that accounts for bar close; there are no `security()` calls or higher-timeframe lookups, which keeps performance light and execution deterministic, and the clamping of the volatility signal ensures numerical stability even during extreme ATR spikes.

Sensible defaults and quick tuning

Start with the defaults (`ATR 14`, `Range 0.20`, `Sensitivity 6.0`) and observe the weight plot across a few volatile events; if you still see too many flips in turbulence, either raise `Range` to 0.25 or trim `Sensitivity` to 4–5 so that the weight can move high but does not overreact, and if the indicator feels too slow in quiet markets, lower `Range` toward 0.15 or raise `Sensitivity` to 7–8 to bias the weight a bit more aggressively downward when conditions compress.

What this indicator is—and is not

Adaptive Heikin Ashi is a context-aware visualization layer that improves the signal-to-noise ratio and reduces fake flips by modulating smoothing with volatility, but it is not a complete trading system, it does not predict the future, and it should be combined with structure, risk controls, and position management that fit your market and timeframe; always forward-test on your instruments, and remember that even adaptive smoothing can delay recognition at sharp turning points when volatility remains elevated.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

BOCS AdaptiveBOCS Adaptive Strategy - Automated Volatility Breakout System

WHAT THIS STRATEGY DOES:

This is an automated trading strategy that detects consolidation patterns through volatility analysis and executes trades when price breaks out of these channels. Take-profit and stop-loss levels are calculated dynamically using Average True Range (ATR) to adapt to current market volatility. The strategy closes positions partially at the first profit target and exits the remainder at the second target or stop loss.

TECHNICAL METHODOLOGY:

Price Normalization Process:

The strategy begins by normalizing price to create a consistent measurement scale. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). The current close price is then normalized using the formula: (close - lowest_low) / (highest_high - lowest_low). This produces values between 0 and 1, allowing volatility analysis to work consistently across different instruments and price levels.

Volatility Detection:

A 14-period standard deviation is applied to the normalized price series. Standard deviation measures how much prices deviate from their average - higher values indicate volatility expansion, lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() functions to track when volatility reaches peaks and troughs over the detection length period (default 14 bars).

Channel Formation Logic:

When volatility crosses from a high level to a low level, this signals the beginning of a consolidation phase. The strategy records this moment using ta.crossover(upper, lower) and begins tracking the highest and lowest prices during the consolidation. These become the channel boundaries. The duration between the crossover and current bar must exceed 10 bars minimum to avoid false channels from brief volatility spikes. Channels are drawn using box objects with the recorded high/low boundaries.

Breakout Signal Generation:

Two detection modes are available:

Strong Closes Mode (default): Breakout occurs when the candle body midpoint math.avg(close, open) exceeds the channel boundary. This filters out wick-only breaks.

Any Touch Mode: Breakout occurs when the close price exceeds the boundary.

When price closes above the upper channel boundary, a bullish breakout signal generates. When price closes below the lower boundary, a bearish breakout signal generates. The channel is then removed from the chart.

ATR-Based Risk Management:

The strategy uses request.security() to fetch ATR values from a specified timeframe, which can differ from the chart timeframe. For example, on a 5-minute chart, you can use 1-minute ATR for more responsive calculations. The ATR is calculated using ta.atr(length) with a user-defined period (default 14).

Exit levels are calculated at the moment of breakout:

Long Entry Price = Upper channel boundary

Long TP1 = Entry + (ATR × TP1 Multiplier)

Long TP2 = Entry + (ATR × TP2 Multiplier)

Long SL = Entry - (ATR × SL Multiplier)

For short trades, the calculation inverts:

Short Entry Price = Lower channel boundary

Short TP1 = Entry - (ATR × TP1 Multiplier)

Short TP2 = Entry - (ATR × TP2 Multiplier)

Short SL = Entry + (ATR × SL Multiplier)

Trade Execution Logic:

When a breakout occurs, the strategy checks if trading hours filter is satisfied (if enabled) and if position size equals zero (no existing position). If volume confirmation is enabled, it also verifies that current volume exceeds 1.2 times the 20-period simple moving average.

If all conditions are met:

strategy.entry() opens a position using the user-defined number of contracts

strategy.exit() immediately places a stop loss order

The code monitors price against TP1 and TP2 levels on each bar

When price reaches TP1, strategy.close() closes the specified number of contracts (e.g., if you enter with 3 contracts and set TP1 close to 1, it closes 1 contract). When price reaches TP2, it closes all remaining contracts. If stop loss is hit first, the entire position exits via the strategy.exit() order.

Volume Analysis System:

The strategy uses ta.requestUpAndDownVolume(timeframe) to fetch up volume, down volume, and volume delta from a specified timeframe. Three display modes are available:

Volume Mode: Shows total volume as bars scaled relative to the 20-period average

Comparison Mode: Shows up volume and down volume as separate bars above/below the channel midline

Delta Mode: Shows net volume delta (up volume - down volume) as bars, positive values above midline, negative below

The volume confirmation logic compares breakout bar volume to the 20-period SMA. If volume ÷ average > 1.2, the breakout is classified as "confirmed." When volume confirmation is enabled in settings, only confirmed breakouts generate trades.

INPUT PARAMETERS:

Strategy Settings:

Number of Contracts: Fixed quantity to trade per signal (1-1000)

Require Volume Confirmation: Toggle to only trade signals with volume >120% of average

TP1 Close Contracts: Exact number of contracts to close at first target (1-1000)

Use Trading Hours Filter: Toggle to restrict trading to specified session

Trading Hours: Session input in HHMM-HHMM format (e.g., "0930-1600")

Main Settings:

Normalization Length: Lookback bars for high/low calculation (1-500, default 100)

Box Detection Length: Period for volatility peak/trough detection (1-100, default 14)

Strong Closes Only: Toggle between body midpoint vs close price for breakout detection

Nested Channels: Allow multiple overlapping channels vs single channel at a time

ATR TP/SL Settings:

ATR Timeframe: Source timeframe for ATR calculation (1, 5, 15, 60, etc.)

ATR Length: Smoothing period for ATR (1-100, default 14)

Take Profit 1 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 2.0)

Take Profit 2 Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 3.0)

Stop Loss Multiplier: Distance from entry as multiple of ATR (0.1-10.0, default 1.0)

Enable Take Profit 2: Toggle second profit target on/off

VISUAL INDICATORS:

Channel boxes with semi-transparent fill showing consolidation zones

Green/red colored zones at channel boundaries indicating breakout areas

Volume bars displayed within channels using selected mode

TP/SL lines with labels showing both price level and distance in points

Entry signals marked with up/down triangles at breakout price

Strategy status table showing position, contracts, P&L, ATR values, and volume confirmation status

HOW TO USE:

For 2-Minute Scalping:

Set ATR Timeframe to "1" (1-minute), ATR Length to 12, TP1 Multiplier to 2.0, TP2 Multiplier to 3.0, SL Multiplier to 1.5. Enable volume confirmation and strong closes only. Use trading hours filter to avoid low-volume periods.

For 5-15 Minute Day Trading:

Set ATR Timeframe to match chart or use 5-minute, ATR Length to 14, TP1 Multiplier to 2.0, TP2 Multiplier to 3.5, SL Multiplier to 1.2. Volume confirmation recommended but optional.

For Hourly+ Swing Trading:

Set ATR Timeframe to 15-30 minute, ATR Length to 14-21, TP1 Multiplier to 2.5, TP2 Multiplier to 4.0, SL Multiplier to 1.5. Volume confirmation optional, nested channels can be enabled for multiple setups.

BACKTEST CONSIDERATIONS:

Strategy performs best during trending or volatility expansion phases

Consolidation-heavy or choppy markets produce more false signals

Shorter timeframes require wider stop loss multipliers due to noise

Commission and slippage significantly impact performance on sub-5-minute charts

Volume confirmation generally improves win rate but reduces trade frequency

ATR multipliers should be optimized for specific instrument characteristics

COMPATIBLE MARKETS:

Works on any instrument with price and volume data including forex pairs, stock indices, individual stocks, cryptocurrency, commodities, and futures contracts. Requires TradingView data feed that includes volume for volume confirmation features to function.

KNOWN LIMITATIONS:

Stop losses execute via strategy.exit() and may not fill at exact levels during gaps or extreme volatility

request.security() on lower timeframes requires higher-tier TradingView subscription

False breakouts inherent to breakout strategies cannot be completely eliminated

Performance varies significantly based on market regime (trending vs ranging)

Partial closing logic requires sufficient position size relative to TP1 close contracts setting

RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance of this or any strategy does not guarantee future results. This strategy is provided for educational purposes and automated backtesting. Thoroughly test on historical data and paper trade before risking real capital. Market conditions change and strategies that worked historically may fail in the future. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions.

ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by AlgoAlpha in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns and sharing this innovative technique with the TradingView community. The enhancements added to the original concept include automated trade execution, multi-timeframe ATR-based risk management, partial position closing by contract count, volume confirmation filtering, and real-time position monitoring.

X VIBVolume Imbalance Zones

X VIB highlights price-levels where buying or selling pressure overwhelmed the opposing side within a single bar transition, leaving a void that the market often revisits. The script paints those voids as boxes so you can quickly see where liquidity may rest, where price may pause or react, and which imbalances persist across sessions.

What it plots

For each completed calculation bar (your chart’s timeframe or a higher timeframe you choose), the indicator draws a box that spans the prior bar’s close to the current bar’s open—only when that bar-to-bar transition exhibits a valid volume imbalance (VIB) by the selected rules. Boxes are time-anchored from the previous bar’s time to the current bar’s time close, and they are capped to a configurable count so the chart remains readable.

Two ways to define “Volume Imbalance”

X VIB calculates imbalances in two complementary ways. Both techniques isolate bar-to-bar displacement that reflects one-sided pressure, but they differ in strictness and how much confirmation they require.

Continuity VIB (Bar-to-Bar Displacement)

A strict definition that requires aligned progress and overlap between consecutive bars. In practical terms, a bullish continuity VIB demands that the new bar advances beyond the prior bar’s close, opens above it, and maintains upward progress without erasing the displacement; the bearish case mirrors this to the downside.

Use when: you want the cleanest, most structurally reliable voids that reflect decisive initiative flow.

Effect on boxes: typically fewer, higher-quality zones that mark locations of strong one-sided intent.

Gap-Qualified VIB (Displacement with Gap Confirmation)

A confirmatory definition that treats the bar-to-bar displacement as an imbalance only if the transition also observes a protective “gap-like” relationship with surrounding prices. This extra condition filters out many borderline transitions and emphasizes voids that were less likely to be traded through on their formation.

Use when: you want additional confirmation that the void had genuine follow-through pressure at birth.

Effect on boxes: often slightly fewer but “stickier” zones that can attract price on retests.

Both modes are drawn identically on the chart (as boxes spanning the displacement). Their difference is purely in the qualification of what counts as a VIB. You can display either set independently or together to compare how each mode surfaces structure.

Multi-Timeframe (MTF) logic

You can compute imbalances on a higher timeframe (e.g., 15-minute) while viewing a lower timeframe chart. When MTF is active, X VIB:

Samples open, high, low, close, time, and time_close from the selected HTF in a single, synchronized request (no gaps, no lookahead).

Only evaluates and draws boxes once per HTF bar close, ensuring clean, stable zones that don’t repaint intra-bar.

How traders use these zones

Reversion into voids: Price often returns to “fill” part of a void before deciding on continuation or reversal.

Context for entries/exits: VIB boxes provide precise, mechanically derived levels for limit entries, scale-outs, and invalidation points.

Confluence: Combine with session opens, HTF levels, or volatility bands to grade setups. Continuity VIBs can mark impulse anchors; Gap-Qualified VIBs often mark stickier pockets.

Inputs & controls

Calculate on higher timeframe? Toggle MTF computation; choose your Calc timeframe (e.g., 15).

Show VIBs: Master toggle for drawing imbalance boxes.

Color & Opacity: Pick the box fill and border intensity that suits your theme.

# Instances: Cap how many historical boxes remain on the chart to avoid clutter.

Notes & best practices

Signal density: Continuity VIBs tend to be more frequent on fast charts; Gap-Qualified VIBs are more selective. Try both and keep what aligns with your trade plan.

MTF discipline: When using a higher calc timeframe, analyze reactions primarily at that timeframe’s pace to avoid over-fitting to noise.

Lifecycle awareness: Not all voids fill. Track which boxes persist; durable voids often define the map of the session.

Foresight Cone (HoltxF1xVWAP) [KedArc Quant]Description:

This is a time-series forecasting indicator that estimates the next bar (F1) and projects a path a few bars ahead. It also draws a confidence cone based on how accurate the recent forecasts have been. You can optionally color the projection only when price agrees with VWAP.

Why it’s different

* One clear model: Everything comes from Holt’s trend-aware forecasting method—no mix of unrelated indicators.

* Transparent visuals: You see the next-bar estimate (F1), the forward projection, and a cone that widens or narrows based on recent forecast error.

* Context, not signals: The VWAP option only changes colors. It doesn’t add trade rules.

* No look-ahead: Accuracy is measured using the forecast made on the previous bar versus the current bar.

Inputs (what they mean)

* Source: Price series to forecast (default: Close).

* Preset: Quick profiles for fast, smooth, or momentum markets (see below).

* Alpha (Level): How fast the model reacts to new prices. Higher = faster, twitchier.

* Beta (Trend): How fast the model updates the slope. Higher = faster pivots, more flips in chop.

* Horizon: How many bars ahead to project. Bigger = wider cone.

* Residual Window: How many bars to judge recent accuracy. Bigger = steadier cone.

* Confidence Z: How wide the cone should be (typical setting ≈ “95% style” width).

* Show Bands / Draw Forward Path: Turn the cone and forward lines on/off.

* Color only when aligned with VWAP: Highlights projections only when price agrees with the trend side of VWAP.

* Colors / Show Panel: Styling plus a small panel with RMSE, MAPE, and trend slope.

Presets (when to pick which)

* Scalp / Fast (1-min): Very responsive; best for quick moves. More twitch in chop.

* Smooth Intraday (1–5 min): Calmer and steadier; a good default most days.

* Momentum / Breakout: Quicker slope tracking during strong pushes; may over-react in ranges.

* Custom: Set your own values if you know exactly what you want.

What is F1 here?

F1 is the model’s next-bar fair value. Crosses of price versus F1 can hint at short-term momentum shifts or mean-reversion, especially when viewed with VWAP or the cone.

How this helps

* Gives a baseline path of where price may drift and a cone that shows normal wiggle room.

* Helps you tell routine noise (inside cone) from information (edges or breaks outside the cone).

* Keeps you aware of short-term bias via the trend slope and F1.

How to use (step by step)

1. Add to chart → choose a Preset (start with Smooth Intraday).

2. Set Horizon around 8–15 bars for intraday.

3. (Optional) Turn on VWAP alignment to color only when price agrees with the trend side of VWAP.

4. Watch where price sits relative to the cone and F1:

* Inside = normal noise.

* At edges = stretched.

* Outside = possible regime change.

5. Check the panel: if RMSE/MAPE spike, expect a wider cone; consider a smoother preset or a higher timeframe.

6. Tweak Alpha/Beta only if needed: faster for momentum, slower for chop.

7. Combine with your own plan for entries, exits, and risk.

Accuracy Panel — what it tells you

Preset & Horizon: Shows which preset you’re using and how many bars ahead the projection goes. Longer horizons mean more uncertainty.

RMSE (error in price units): A “typical miss” measured in the chart’s currency (e.g., ₹).

Lower = tighter fit and a usually narrower cone. Rising = conditions getting noisier; the cone will widen.

MAPE (error in %): The same idea as RMSE but in percent.

Good for comparing different symbols or timeframes. Sudden spikes often hint at a regime change.

Slope T: The model’s short-term trend reading.

Positive = gentle up-bias; negative = gentle down-bias; near zero = mostly flat/drifty.

How to read it at a glance

Calm & directional: RMSE/MAPE steady or falling + Slope T positive (or negative) → trends tend to respect the cone’s mid/upper (or mid/lower) area.

Choppy/uncertain: RMSE/MAPE climbing or jumping → expect more whipsaw; rely more on the cone edges and higher-TF context.

Flat tape: Slope T near zero → mean-revert behavior is common; treat cone edges as stretch zones rather than breakout zones.

Warm-up & tweaks

Warm-up: Right after adding the indicator, the panel may be blank for a short time while it gathers enough bars.

Too twitchy? Switch to Smooth Intraday or increase the Residual Window.

Too slow? Use Scalp/Fast or Momentum/Breakout to react quicker.

Timeframe tips

* 1–3 min: Scalp/Fast or Momentum/Breakout; horizon \~8–12.

* 5–15 min: Smooth Intraday; horizon \~12–15.

* 30–60 min+: Consider a larger residual window for a steadier cone.

FAQ

Q: Is this a strategy or an indicator?

A: It’s an indicator only. It does not place orders, TP/SL, or run backtests.

Q: Does it repaint?

A: The next-bar estimate (F1) and the cone are calculated using only information available at that time. The forward path is a projection drawn on the last bar and will naturally update as new bars arrive. Historical bars aren’t revised with future data.

Q: What is F1?

A: F1 is the indicator’s best guess for the next bar.

Price crossing above/below F1 can hint at short-term momentum shifts or mean-reversion.

Q: What do “Alpha” and “Beta” do?

A: Alpha controls how fast the indicator reacts to new prices

(higher = faster, twitchier). Beta controls how fast the slope updates (higher = quicker pivots, more flips in chop).

Q: Why does the cone width change?

A: It reflects recent forecast accuracy. When the market gets noisy, the cone widens. When the tape is calm, it narrows.

Q: What does the Accuracy Panel tell me?

A:

* Preset & Horizon you’re using.

* RMSE: typical forecast miss in price units.

* MAPE: typical forecast miss in percent.

* Slope T: short-term trend reading (up, down, or flat).

If RMSE/MAPE rise, expect a wider cone and more whipsaw.

Q: The panel shows “…” or looks empty. Why?

A: It needs a short warm-up to gather enough bars. This is normal after you add the indicator or change settings/timeframes.

Q: Which timeframe is best?

A:

* 1–3 min: Scalp/Fast or Momentum/Breakout, horizon \~8–12.

* 5–15 min: Smooth Intraday, horizon \~12–15.

Higher timeframes work too; consider a larger residual window for steadier cones.

Q: Which preset should I start with?

A: Start with Smooth Intraday. If the market is trending hard, try Momentum/Breakout.

For very quick tapes, use Scalp/Fast. Switch back if things get choppy.

Q: What does the VWAP option do?

A: It only changes colors (highlights when price agrees with the trend side of VWAP).

It does not add or remove signals.

Q: Are there alerts?

A: Yes—alerts for price crossing F1 (up/down). Use “Once per bar close” to reduce noise on fast charts.

Q: Can I use this on stocks, futures, crypto, or FX?

A: Yes. It works on any symbol/timeframe. You may want to adjust Horizon and the Residual Window based on volatility.

Q: Can I use it with Heikin Ashi or other non-standard bars?

A: You can, but remember you’re forecasting the synthetic series of those bars. For pure price behavior, use regular candles.

Q: The cone feels too wide/too narrow. What do I change?

A:

* Too wide: lower Alpha/Beta a bit or increase the Residual Window.

* Too narrow (misses moves): raise Alpha/Beta slightly or try Momentum/Breakout.

Q: Why do results change when I switch timeframe or symbol?

A: Different noise levels and trends. The accuracy stats reset per chart, so the cone adapts to each context.

Q: Any limits or gotchas?

A: Extremely large Horizon may hit TradingView’s line-object limits; reduce Horizon or turn

off extra visuals if needed. Big gaps or news spikes will widen errors—expect the cone to react.

Q: Can this predict exact future prices?

A: No. It provides a baseline path and context. Always combine with your own rules and risk management.

Glossary

* TS (Time Series): Data over time (prices).

* Holt’s Method: A forecasting approach that tracks a current level and a trend to predict the next bars.

* F1: The indicator’s best guess for the next bar.

* F(h): The projected value h bars ahead.

* VWAP: Volume-Weighted Average Price—used here for optional color alignment.

* RMSE: Typical forecast miss in price units (how far off, on average).

* MAPE: Typical forecast miss in percent (scale-free, easy to compare).

Notes & limitations

* The panel needs a short warm-up; stats may be blank at first.

* The cone reflects recent conditions; sudden volatility changes will widen it.

* This is a tool for context. It does not place trades and does not promise results.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

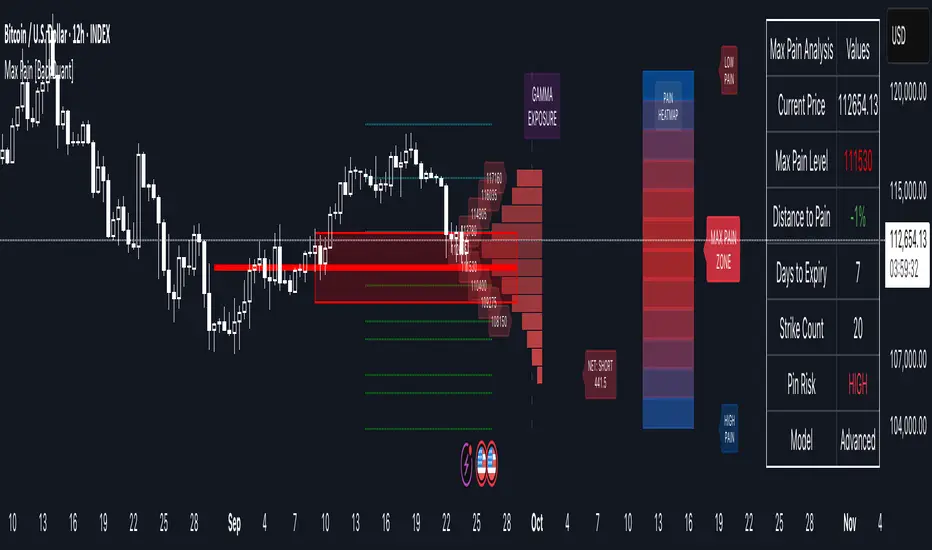

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

Price Level Highlighter [ldlwtrades]This indicator is a minimalist and highly effective tool designed for traders who incorporate institutional concepts into their analysis. It automates the identification of key psychological price levels and adds a unique, dynamic layer of information to help you focus on the most relevant area of the market. Inspired by core principles of market structure and liquidity, it serves as a powerful visual guide for anticipating potential support and resistance.

The core idea is simple: specific price points, particularly those ending in round numbers or common increments, often act as magnets or barriers for price. While many indicators simply plot static lines, this tool goes further by intelligently highlighting the single most significant level in real-time. This dynamic feature allows you to quickly pinpoint where the market is currently engaged, offering a clear reference point for your trading decisions. It reduces chart clutter and enhances your focus on the immediate price action.

Features

Customizable Price Range: Easily define a specific Start Price and End Price to focus the indicator on the most relevant area of your chart, preventing unnecessary clutter.

Adjustable Increment: Change the interval of the lines to suit your trading style, from high-frequency increments (e.g., 10 points) for scalping to wider intervals (e.g., 50 or 100 points) for swing trading.

Intelligent Highlighting: A key feature that automatically identifies and highlights the single horizontal line closest to the current market price with a distinct color and thickness. This gives you an immediate visual cue for the most relevant price level.

Highly Customizabile: Adjust the line color, style, and width for both the main lines and the highlighted line to fit your personal chart aesthetic.

Usage

Apply the indicator to your chart.

In the settings, input your desired price range (Start Price and End Price) to match the market you are trading.

Set the Price Increment to your preferred density.

Monitor the chart for the highlighted line. This is your active price level and a key area of interest.

Combine this tool with other confirmation signals (e.g., order blocks, fair value gaps, liquidity pools) to build higher-probability trade setups.

Best Practices

Pairing: This tool is effective across all markets, including stocks, forex, indices, and crypto. It is particularly useful for volatile markets where price moves rapidly between psychological levels.

Mindful Analysis: Use the highlighted level as a reference point for your analysis, not as a standalone signal. A break above or below this level can signify a shift in market control.

Backtesting: Always backtest the indicator on your preferred market and timeframe to understand how it performs under different conditions.

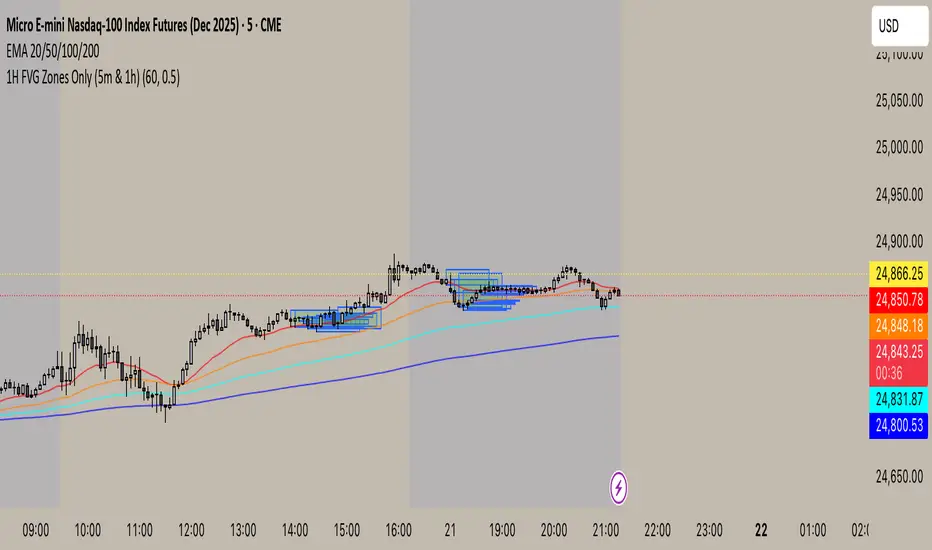

1H FVG Zones Only (5m & 1h)new uses trend anaylosis. takes 15 min chart and breaks into 1hr chart fvg gaps

Harmonic Super GuppyHarmonic Super Guppy – Harmonic & Golden Ratio Trend Analysis Framework

Overview

Harmonic Super Guppy is a comprehensive trend analysis and visualization tool that evolves the classic Guppy Multiple Moving Average (GMMA) methodology, pioneered by Daryl Guppy to visualize the interaction between short-term trader behavior and long-term investor trends. into a harmonic and phase-based market framework. By combining harmonic weighting, golden ratio phasing, and multiple moving averages, it provides traders with a deep understanding of market structure, momentum, and trend alignment. Fast and slow line groups visually differentiate short-term trader activity from longer-term investor positioning, while adaptive fills and dynamic coloring clearly illustrate trend coherence, expansion, and contraction in real time.

Traditional GMMA focuses primarily on moving average convergence and divergence. Harmonic Super Guppy extends this concept, integrating frequency-aware harmonic analysis and golden ratio modulation, allowing traders to detect subtle cyclical forces and early trend shifts before conventional moving averages would react. This is particularly valuable for traders seeking to identify early trend continuation setups, preemptive breakout entries, and potential trend exhaustion zones. The indicator provides a multi-dimensional view, making it suitable for scalping, intraday trading, swing setups, and even longer-term position strategies.

The visual structure of Harmonic Super Guppy is intentionally designed to convey trend clarity without oversimplification. Fast lines reflect short-term trader sentiment, slow lines capture longer-term investor alignment, and fills highlight compression or expansion. The adaptive color coding emphasizes trend alignment: strong green for bullish alignment, strong red for bearish, and subtle gray tones for indecision. This allows traders to quickly gauge market conditions while preserving the granularity necessary for sophisticated analysis.

How It Works

Harmonic Super Guppy uses a combination of harmonic averaging, golden ratio phasing, and adaptive weighting to generate its signals.

Harmonic Weighting : Each moving average integrates three layers of harmonics:

Primary harmonic captures the dominant cyclical structure of the market.

Secondary harmonic introduces a complementary frequency for oscillatory nuance.

Tertiary harmonic smooths higher-frequency noise while retaining meaningful trend signals.

Golden Ratio Phase : Phases of each harmonic contribution are adjusted using the golden ratio (default φ = 1.618), ensuring alignment with natural market rhythms. This reduces lag and allows traders to detect trend shifts earlier than conventional moving averages.

Adaptive Trend Detection : Fast SMAs are compared against slow SMAs to identify structural trends:

UpTrend : Fast SMA exceeds slow SMA.

DownTrend : Fast SMA falls below slow SMA.

Frequency Scaling : The wave frequency setting allows traders to modulate responsiveness versus smoothing. Higher frequency emphasizes short-term moves, while lower frequency highlights structural trends. This enables adaptation across asset classes with different volatility characteristics.

Through this combination, Harmonic Super Guppy captures micro and macro market cycles, helping traders distinguish between transient noise and genuine trend development. The multi-harmonic approach amplifies meaningful price action while reducing false signals inherent in standard moving averages.

Interpretation

Harmonic Super Guppy provides a multi-dimensional perspective on market dynamics:

Trend Analysis : Alignment of fast and slow lines reveals trend direction and strength. Expanding harmonics indicate momentum building, while contraction signals weakening conditions or potential reversals.

Momentum & Volatility : Rapid expansion of fast lines versus slow lines reflects short-term bullish or bearish pressure. Compression often precedes breakout scenarios or volatility expansion. Traders can quickly gauge trend vigor and potential turning points.

Market Context : The indicator overlays harmonic and structural insights without dictating entry or exit points. It complements order blocks, liquidity zones, oscillators, and other technical frameworks, providing context for informed decision-making.

Phase Divergence Detection : Subtle divergence between harmonic layers (primary, secondary, tertiary) often signals early exhaustion in trends or hidden strength, offering preemptive insight into potential reversals or sustained continuation.

By observing both structural alignment and harmonic expansion/contraction, traders gain a clear sense of when markets are trending with conviction versus when conditions are consolidating or becoming unpredictable. This allows for proactive trade management, rather than reactive responses to lagging indicators.

Strategy Integration

Harmonic Super Guppy adapts to various trading methodologies with clear, actionable guidance.

Trend Following : Enter positions when fast and slow lines are aligned and harmonics are expanding. The broader the alignment, the stronger the confirmation of trend persistence. For example:

A fast line crossover above slow lines with expanding fills confirms momentum-driven continuation.

Traders can use harmonic amplitude as a filter to reduce entries against prevailing trends.

Breakout Trading : Periods of line compression indicate potential volatility expansion. When fast lines diverge from slow lines after compression, this often precedes breakouts. Traders can combine this visual cue with structural supports/resistances or order flow analysis to improve timing and precision.

Exhaustion and Reversals : Divergences between harmonic components, or contraction of fast lines relative to slow lines, highlight weakening trends. This can indicate liquidity exhaustion, trend fatigue, or corrective phases. For example:

A flattening fast line group above a rising slow line can hint at short-term overextension.

Traders may use these signals to tighten stops, take partial profits, or prepare for contrarian setups.

Multi-Timeframe Analysis : Overlay slow lines from higher timeframes on lower timeframe charts to filter noise and trade in alignment with larger market structures. For example:

A daily bullish alignment combined with a 15-minute breakout pattern increases probability of a successful intraday trade.

Conversely, a higher timeframe divergence can warn against taking counter-trend trades in lower timeframes.

Adaptive Trade Management : Harmonic expansion/contraction can guide dynamic risk management:

Stops may be adjusted according to slow line support/resistance or harmonic contraction zones.

Position sizing can be modulated based on harmonic amplitude and compression levels, optimizing risk-reward without rigid rules.

Technical Implementation Details

Harmonic Super Guppy is powered by a multi-layered harmonic and phase calculation engine:

Harmonic Processing : Primary, secondary, and tertiary harmonics are calculated per period to capture multiple market cycles simultaneously. This reduces noise and amplifies meaningful signals.

Golden Ratio Modulation : Phase adjustments based on φ = 1.618 align harmonic contributions with natural market rhythms, smoothing lag and improving predictive value.

Adaptive Trend Scaling : Fast line expansion reflects short-term momentum; slow lines provide structural trend context. Fills adapt dynamically based on alignment intensity and harmonic amplitude.

Multi-Factor Trend Analysis : Trend strength is determined by alignment of fast and slow lines over multiple bars, expansion/contraction of harmonic amplitudes, divergences between primary, secondary, and tertiary harmonics and phase synchronization with golden ratio cycles.

These computations allow the indicator to be highly responsive yet smooth, providing traders with actionable insights in real time without overloading visual complexity.

Optimal Application Parameters

Asset-Specific Guidance:

Forex Majors : Wave frequency 1.0–2.0, φ = 1.618–1.8

Large-Cap Equities : Wave frequency 0.8–1.5, φ = 1.5–1.618

Cryptocurrency : Wave frequency 1.2–3.0, φ = 1.618–2.0

Index Futures : Wave frequency 0.5–1.5, φ = 1.618

Timeframe Optimization:

Scalping (1–5min) : Emphasize fast lines, higher frequency for micro-move capture.

Day Trading (15min–1hr) : Balance fast/slow interactions for trend confirmation.

Swing Trading (4hr–Daily) : Focus on slow lines for structural guidance, fast lines for entry timing.

Position Trading (Daily–Weekly) : Slow lines dominate; harmonics highlight long-term cycles.

Performance Characteristics

High Effectiveness Conditions:

Clear separation between short-term and long-term trends.

Moderate-to-high volatility environments.

Assets with consistent volume and price rhythm.

Reduced Effectiveness:

Flat or extremely low volatility markets.

Erratic assets with frequent gaps or algorithmic dominance.

Ultra-short timeframes (<1min), where noise dominates.

Integration Guidelines

Signal Confirmation : Confirm alignment of fast and slow lines over multiple bars. Expansion of harmonic amplitude signals trend persistence.

Risk Management : Place stops beyond slow line support/resistance. Adjust sizing based on compression/expansion zones.

Advanced Feature Settings :

Frequency tuning for different volatility environments.

Phase analysis to track divergences across harmonics.

Use fills and amplitude patterns as a guide for dynamic trade management.

Multi-timeframe confirmation to filter noise and align with structural trends.

Disclaimer

Harmonic Super Guppy is a trend analysis and visualization tool, not a guaranteed profit system. Optimal performance requires proper wave frequency, golden ratio phase, and line visibility settings per asset and timeframe. Traders should combine the indicator with other technical frameworks and maintain disciplined risk management practices.

NX - ICT PD ArraysThis Pine Script indicator identifies and visualizes Fair Value Gaps (FVGs) and Order Blocks (OBs) based on refined price action logic.

FVGs are highlighted when price leaves an imbalance between candles, while Order Blocks are detected using ICT methodology—marking the last opposing candle before a displacement move.

The script dynamically tracks and updates these zones, halting box extension once price interacts with them. Customizable colors and lookback settings allow traders to tailor the display to their strategy.

Adaptive Gap Bands - DolphinTradeBot1️⃣ Overview

Adaptive Gap Bands is a momentum indicator that measures the percentage difference between fast and slow moving averages. This helps identify potential overbought or oversold zones.

The goal is to analyze “gap” behaviors within a trend and generate clearer entry–exit signals.

Since the bands are anchored to the slow moving average, they are more sensitive to the trend direction, making signals stronger in line with the prevailing trend.

📌 Signals do not repaint — once confirmed, they remain fixed on the chart.

2️⃣ How It Works ?

The indicator tracks the distance between fast and slow MAs.

The indicator measures the percentage gap between the fast and slow moving averages, relative to the slow MA.

Each time the gap reaches a new extreme during a swing, that value is stored.

When the averages cross, the stored values from the last N swings (defined by Swing Count) are collected.

These gap values are then averaged to create a smoother and more adaptive reference.

The bands are built by multiplying this average gap with the % Multiplier and projecting it around the slow MA.

3️⃣ How to Use It ?

Add the script to your chart.

Green label → potential Long signal.

Red label → potential Short signal.

Signals often appear when price moves outside the adaptive bands, showing extreme momentum.

Can also be used as a reference tool in manual trades to set profit/loss expectations.

By comparing upward vs. downward gaps, it can help analyze and confirm the dominant trend direction.

4️⃣⚙️ Settings

Swing Count → Number of past swings considered.

% Multiplier → Adjusts band width (narrower or wider).

MA Lengths & Types → Choose fast and slow moving averages (EMA, SMA, RMA, etc.).

TPO Levels [VAH/POC/VAL] with Poor H/L, Single Prints & NPOCs### 🎯 Advanced Market Profile & Key Level Analysis

This script is a unique and comprehensive technical analysis tool designed to help traders understand market structure, value, and key liquidity levels using the principles of **Auction Market Theory** and **Market Profile**.

This script is unique (and shouldn't be censored) because :

It allows large history of levels to be displayed

Accurate as possible tick size

Doesn't draw a profile but only the actual levels

Supports multi-timeframe levels even on the daily mode giving macro context

There is no indicator out there that does it

While these concepts are universal, this indicator was built primarily for the dynamic, 24/7 nature of the **cryptocurrency market**. It helps you move beyond simple price action to understand *why* the market is moving, which is especially crucial in the volatile crypto space.

### ## 📊 The Concepts Behind the Calculations

To use this script effectively, it's important to understand the core concepts it is built upon. The entire script is self-contained and does not require other indicators.

* **What is Market Profile?**

Market Profile is a unique charting technique that organizes price and time data to reveal market structure. It's built from **Time Price Opportunities (TPOs)**, which are 30-minute periods of market activity. By stacking these TPOs, the script builds a distribution, showing which price levels were most accepted (heavily traded) and which were rejected (lightly traded) during a session.

* **What is the Value Area (VA)?**

The Value Area is the heart of the profile. It represents the price range where **70%** of the session's trading volume occurred. This is considered the "fair value" zone where both buyers and sellers were in general agreement.

* **Point of Control (POC):** The single price level with the most TPOs. This was the most accepted or "fairest" price of the session and acts as a gravitational line for price.

* **Value Area High (VAH):** The upper boundary of the 70% value zone.

* **Value Area Low (VAL):** The lower boundary of the 70% value zone.

VAH and VAL are dynamic support and resistance levels. Trading outside the previous session's value area can signal the start of a new trend.

***

### ## 📈 Key Features Explained

This script automatically calculates and displays the following critical market-generated information:

* **Multi-Timeframe Market Profile**

Automatically draws Daily, Weekly, and Monthly profiles, allowing you to analyze market structure across different time horizons. The script preserves up to 20 historical sessions to provide deep market context.

* **Naked Point of Control (nPOC)**

A "Naked" POC is a Point of Control from a previous session that has **not** been revisited by price. These levels often act as powerful magnets for price, representing areas of unfinished business that the market may seek to retest. The script tracks and displays Daily, Weekly, and Monthly nPOCs until they are touched.

* **Single Prints (Imbalance Zones)**

A Single Print is a price level where only one TPO traded during the session's development. This signifies a rapid, aggressive price move and an imbalanced market. These areas, like gaps in a traditional chart, are frequently revisited as the market seeks to "fill in" these thin parts of the profile.

* **Poor Structure (Unfinished Auctions)**

A **Poor High** or **Poor Low** occurs when the top or bottom of a profile is flat, with two or more TPOs at the extreme price. This suggests that the auction in that direction was weak and inconclusive. These weak structures often signal a high probability that price will eventually break that high or low.

***

### ## 💡 How to Use This Indicator

This tool is not a signal generator but an analytical framework to improve your trading decisions.

1. **Determine Market Context:** Start by asking: Is the current price trading *inside* or *outside* the previous session's Value Area?

* **Inside VA:** The market is in a state of balance or range-bound. Look for trades between the VAH and VAL.

* **Outside VA:** The market is in a state of imbalance and may be starting a trend. Look for continuation or acceptance of prices outside the prior value.

2. **Identify Key Levels:**

* Use historical **nPOCs** as potential profit targets or areas to watch for a price reaction.

* Treat historical **VAH** and **VAL** levels as significant support and resistance zones.

* Note where **Single Prints** are. These are often price magnets that may get "filled" in the future.

3. **Spot Weakness:**

* A **Poor High** suggests weak resistance that may be easily broken.

* A **Poor Low** suggests weak support, signaling a potential for a continued move lower if broken.

***

### ## ⚙️ Customization & Crypto Presets

The indicator is highly customizable, allowing you to change colors, transparency, the number of historical sessions, and more.

To help traders get started quickly, the indicator includes **built-in layout presets** specifically calibrated for major cryptocurrencies: ** BINANCE:BTCUSDT.P , BINANCE:ETHUSDT.P , and BINANCE:SOLUSDT.P **. These presets automatically adjust key visual parameters to better suit the unique price characteristics and volatility of each asset, providing an optimized view right out of the box.

***

### ## ⚠️ Disclaimer

This indicator is a tool for market analysis and should not be interpreted as direct buy or sell signals. It provides information based on historical price action, which does not guarantee future results. Trading involves significant risk, and you should always use proper risk management. This script is designed for use on standard chart types (e.g., Candlesticks, Bar) and may produce misleading information on non-standard charts.

Chimera [theUltimator5]In myth, the chimera is an “impossible” hybrid—lion, goat, and serpent fused into one—striking to look at and formidable in presence. The word has come to mean a beautiful, improbable union of parts that shouldn’t work together, yet do.

Chimera is a dual-mode market context tool that blends a multi-input oscillator with classic ADX/DI trend strength, plus optional multi-timeframe “gap-line” tracking. Use it to visualize regime (trend vs. range), momentum swings around an adaptive midline, and higher timeframe (HTF) reference levels that auto-terminate on touch/cross.

Modes

1) Oscillator view

A smoothed composite of five common inputs—RSI, MACD (oscillator), Bollinger position, Stochastic, and an ATR/DI-weighted bias. Each is normalized to a comparable 0–100 style scale, averaged, and plotted as a candle-style oscillator (short vs. long smoothing, wickless for clarity). A dynamic midline with standard-deviation bands frames neutral → bearish/bullish zones. Colors ramp from neutral to your chosen Oversold/Overbought endpoints; consolidation can override to white.

Here is a description of the (5) signals used to calculate the sentiment oscillator:

RSI (14): Measures recent momentum by comparing average gains vs. losses. High = strength after advances; low = weakness after declines. (Z-score normalized to 0–100.)

MACD oscillator (12/26/9): Uses the difference between MACD and its signal (histogram) to gauge momentum shifts. Positive = bullish tilt; negative = bearish. (Z-score normalized.)

Bollinger Bands position (20, 2): Locates price within the bands (0–100 from lower → upper). Near upper suggests strength/expansion; near lower suggests weakness/contraction. (Then normalized.)

Stochastic (14, 3, 3): Shows where the close sits within the recent high-low range, smoothed via %D. Higher values = closes near highs; lower = near lows. (Scaled 0–100.)

ATR/DI composite (14): Volatility-weighted directional bias: (+DI − −DI) amplified by ATR as a % of price and its relative average. Positive = bullish pressure with volatility; negative = bearish. (Rank/scale normalized.)

All five are normalized and averaged into one composite, then smoothed (short/long) and compared to an adaptive midline with bands.

2) ADX view

Shows ADX, +DI, –DI with user-defined High Threshold. Transparency and color shift with regime. When ADX is strong, a directional “fire/ice” gradient fills the area between ADX and the high threshold, biased toward the dominant DI; when ADX is weak, a soft white fade highlights low-trend conditions.

HTF gap-line tracking (optional; both modes)

Detects “gap-like” reference levels after weak-trend consolidation flips into a sudden DI jump.

Anchors a line at the event bar’s open and auto-terminates upon first touch/cross (tick-size tolerance).

Auto-selects up to three higher timeframes suited to your chart resolution and prints non-overlapping lines with labels like 1H / 4H / 1D. Lower-priority duplicates are suppressed to reduce clutter.

Confirmation / repaint notes

Signals and lines finalize on bar close of the relevant timeframe.

HTF elements update only on the HTF bar close. During a forming bar they may appear transiently.

Line removal finalizes after the bar that produced the touch/cross closes.

Visual cues & effects

Oscillator candles: Open/High = long smoothing; Low/Close = short smoothing (no wicks).

Adaptive bands: Midline ± StdDev Multiplier × stdev of the blended series.

Consolidation tint: Optional white backdrop/candles when the consolidation condition is true (balance + low ADX).

Breakout VFX (optional): With strong DI/ADX and Bollinger breaks, renders a subtle “fire” flare above upper-band thrusts or “ice” shelf below lower-band thrusts.

Inputs (high-level)

Visual Style: Oscillator or ADX.

General (Oscillator): Lookback Period, Short/Long Smoothing, Standard Deviation Multiplier.

Color (Oscillator): Oversold/Overbought colors for gradient endpoints.

Plot (Oscillator): Show Candles, Show Slow MA Line, Show Individual Component (RSI/MACD/BB/Stoch/ATR).

Table (Oscillator): Show Information Table & position (compact dashboard of component values + status).

ADX / Gaps / VFX (both modes): ADX High Threshold, Highlight Backgrounds, Show Gap Labels, Visual Overlay Effects, and color choices for current-TF & HTF lines.

HTF selection: Automatic ladder (3 tiers) based on your chart timeframe.

Alerts (built-in)

Buy Signal – Primary: Oscillator exits oversold.

Sell Signal – Primary: Oscillator exits overbought.

Gap Fill Line Created (Any TF)

Gap Fill Line Terminated (Any TF)

ADX Crossed ABOVE/BELOW Low Threshold

ADX Crossed ABOVE/BELOW High Threshold

Consolidation Started

Alerts evaluate on the close of the relevant timeframe.

How to read it (quick guide)

Pick your lens: Oscillator for blended momentum around an adaptive midline; ADX for trend strength and DI skew.

Watch extremes & mean re-entries (Oscillator): Approaches to the top/bottom band show persistent momentum; returns toward the midline show normalization.

Check regime (ADX): Below Low = low-trend; above High = strong trend, with “fire/ice” bias toward +DI/–DI.

Track gap lines: Fresh labels mark new reference levels; lines auto-remove on first interaction. HTF lines add context but finalize only on HTF close.

The uniqueness from this indicator comes from multiple areas:

1. A unique multi-timeframe algorithm detects gap fill zones and plots them on the chart.

2. Visual effects for both visual modes were hand crafted to provide a visually stunning and intuitive interface.

3. The algorithm to determine sentiment uses a unique blend of weight and sensitivity adjustment to create a plot with elastic upper and lower bounds based off historical volatility and price action.

ATR Future Movement Range Projection

The "ATR Future Movement Range Projection" is a custom TradingView Pine Script indicator designed to forecast potential price ranges for a stock (or any asset) over short-term (1-month) and medium-term (3-month) horizons. It leverages the Average True Range (ATR) as a measure of volatility to estimate how far the price might move, while incorporating recent momentum bias based on the proportion of bullish (green) vs. bearish (red) candles. This creates asymmetric projections: in bullish periods, the upside range is larger than the downside, and vice versa.

The indicator is overlaid on the chart, plotting horizontal lines for the projected high and low prices for both timeframes. Additionally, it displays a small table in the top-right corner summarizing the projected prices and the percentage change required from the current close to reach them. This makes it useful for traders assessing potential targets, risk-reward ratios, or option strategies, as it combines volatility forecasting with directional sentiment.

Key features:

- **Volatility Basis**: Uses weekly ATR to derive a stable daily volatility estimate, avoiding noise from shorter timeframes.

- **Momentum Adjustment**: Analyzes recent candle colors to tilt projections toward the prevailing trend (e.g., more upside if more green candles).

- **Time Horizons**: Fixed at 1 month (21 trading days) and 3 months (63 trading days), assuming ~21 trading days per month (excluding weekends/holidays).

- **User Adjustable**: The ATR length/lookback (default 50) can be tweaked via inputs.

- **Visuals**: Green/lime lines for highs, red/orange for lows; a semi-transparent table for quick reference.

- **Limitations**: This is a probabilistic projection based on historical volatility and momentum—it doesn't predict direction with certainty and assumes volatility persists. It ignores external factors like news, earnings, or market regimes. Best used on daily charts for stocks/ETFs.

The indicator doesn't generate buy/sell signals but helps visualize "expected" ranges, similar to how implied volatility informs option pricing.

### How It Works Step-by-Step

The script executes on each bar update (typically daily timeframe) and follows this logic:

1. **Input Configuration**:

- ATR Length (Lookback): Default 50 bars. This controls both the ATR calculation period and the candle count window. You can adjust it in the indicator settings.

2. **Calculate Weekly ATR**:

- Fetches the ATR from the weekly timeframe using `request.security` with a length of 50 weeks.

- ATR measures average price range (high-low, adjusted for gaps), representing volatility.

3. **Derive Daily ATR**:

- Divides the weekly ATR by 5 (approximating 5 trading days per week) to get an equivalent daily volatility estimate.

- Example: If weekly ATR is $5, daily ATR ≈ $1.

4. **Define Projection Periods**:

- 1 Month: 21 trading days.

- 3 Months: 63 trading days (21 × 3).