Argentina’s Global Ascent: Decoding the USD/ARS ShiftArgentina is witnessing a historic pivot. Following a landslide midterm victory in late 2025, the administration has consolidated power. The USD/ARS pair now reflects this newfound political stability. This stability signals a departure from years of chronic volatility.

Geopolitical Realignment and the Ecuador Effect

Argentina’s geostrategy has shifted toward a firm Western alliance. The administration’s ties with the United States have unlocked critical financial backing. Recently, Ecuador’s $4 billion bond success served as a regional bellwether. Investors view Ecuador’s market return as a blueprint for Argentina. Both nations share a history of restructuring. However, Argentina's economy is four times larger. This scale attracts institutional appetite for high-yield emerging assets.

Macroeconomics: The Fiscal Anchor

Fiscal discipline is no longer a mere promise. The government achieved a consistent fiscal surplus throughout 2025. Inflation is projected to continue its downward trend throughout 2026. This aggressive disinflation strategy supports the peso’s relative strength. The Central Bank continues to rebuild reserves through strategic dollar purchases. While debt maturities remain high, the recent political mandate empowers the executive to maintain a lean budget.

Tech Frontiers: Infrastructure and Innovation

Technology is driving a structural shift in Argentina’s trade balance. Knowledge-based services (KBS) exports are reaching record highs. Major global tech players are exploring "Stargate" style infrastructure projects in the South. These data centers leverage the region’s cold climate and energy surplus. Such high-tech investments create a steady demand for local currency. Argentina is transitioning from a talent exporter to a global digital infrastructure hub.

Innovation and Patent Analysis

The high-tech sector is maturing beyond simple outsourcing. Patent filings in agritech and biotech have surged annually. Local unicorns now dominate global engineering markets. Patent analysis reveals a focus on AI-driven automation and blockchain-based logistics. These innovations protect intellectual property while diversifying the nation's export portfolio. This scientific progress acts as a long-term hedge against traditional commodity cycles.

Leadership and Corporate Culture

Management styles in Argentina are evolving rapidly. A new era has introduced a culture of radical transparency and efficiency. Business models now prioritize SaaS (Software as a Service) and cloud-native architectures. Leadership teams are adopting "Security-by-Design" to mitigate rising cyber risks. The cybersecurity market is expanding as firms protect digital assets. Companies are investing heavily in Security Operations Centers to ensure operational resilience.

Conclusion: A New Economic Model

Argentina’s path to market normalization is accelerating. New incentive regimes offer long-term stability for major projects. This regulatory certainty attracts energy and mining giants to shale and lithium deposits. The USD/ARS pair is no longer just a measure of crisis. It is now a metric of a nation’s profound structural transformation.

ARGENTINE PESO / U.S. DOLLAR

No trades

What traders are saying

Hyperinflation & DictatorsI cannot make this any simpler.

🚨 I AM ISSUING A WARNING TO EVERYONE!

Should Trump succeed in taking over the FED, the outcome is already known. What is not known is the SEVERITY. FAFO!

Here is how it works:

1️⃣ Political pressure replaces economic reality

When leaders can’t win within the system, they change the system.

Common moves:

Undermine central-bank independence

Fire or sideline technocrats

Declare that “rates are too high” or “money is too tight”

This happened in:

Argentina

Lebanon

Sri Lanka

Pakistan

Turkey

Venezuela

Zimbabwe

Russia.

Different excuses. Same motive.

2️⃣ FED Monetary discipline is framed as “The Enemy”

Raising rates?

Protecting the currency?

Controlling deficits?

Rebranded as:

“Anti-growth”

“Western ideology”

“Sabotage”

“Austerity”

Once price stability becomes political, it’s already over.

3️⃣ Spending continues — funding doesn’t

Here’s the fatal step:

Governments keep spending

Tax capacity doesn’t grow

Borrowing gets harder

So pressure shifts to the currency system

This is where reality kicks in:

You can print currency.

You can’t print trust.

4️⃣ Markets respond instantly (and mercilessly)

Markets don’t argue ideology. They just reprice risk.

What happens next:

Bonds sell off

Currency weakens

Import prices surge

Inflation feeds on itself

At this point, rate hikes don’t “cause” inflation — they’re a late reaction to lost credibility.

5️⃣ Hyperinflation isn’t a surprise — it’s the end stage

Hyperinflation is not:

A policy mistake

Bad luck

“External shocks”

It’s the logical conclusion of:

Political control → monetary submission → currency collapse

Every country on that list followed this arc. No exceptions.

The uncomfortable truth

Countries don’t collapse because they raise rates.

They collapse because they refuse to accept limits.

Markets respond with inflation — not theory.

If you enjoy the work, drop a solid comment

Let’s push it to 6,000 and keep building a community grounded in raw truth, not hype.

Can a Currency Rise While Science Dies?Argentina's peso stands at a historic crossroads in 2026, stabilized by unprecedented fiscal discipline yet undermined by the systematic dismantling of its scientific infrastructure. President Javier Milei's administration has achieved what seemed impossible: a fiscal surplus of 1.8% of GDP and inflation falling from 211% to manageable monthly rates around 2%. The peso's transformation from distressed asset to commodity-backed currency relies on the massive Vaca Muerta energy formation and lithium reserves, supported by a US-aligned trade framework that reduces political risk premiums. The launch of new inflation-linked currency bands in January 2026 signals normalization, while energy exports are projected to generate a cumulative total of $300 billion through 2050.

However, this financial renaissance masks a profound intellectual crisis. CONICET, Argentina's premier research council, suffered a 40% real budget cut, resulting in the loss of 1,000 staff members and triggering a brain drain that saw 10% of researchers abandon the system. Salaries collapsed 30% in real terms, forcing scientists into Uber driving and manual labor. Patent filings plummeted to a multi-decade low of 406 annually, while the country ranks a dismal 92nd globally in innovation inputs despite 64th in outputs. The administration views public science as fiscal waste, creating what critics call "scienticide," the systematic destruction of research capacity that took decades to build.

The peso's future hinges on whether geological wealth can compensate for cognitive atrophy. Energy and mining investments under the RIGI regime (offering 30-year fiscal stability) total billions, fundamentally altering the balance of payments. Yet import tariff eliminations on technology threaten 6,000 jobs in Tierra del Fuego's assembly sector, while the gutting of research labs compromises long-term capacity in biotechnology, nuclear energy, and software development. The geopolitical bet on US alignment provides bridge financing through IMF support, but tensions with China, a vital trade partner for soy and beef exports, create vulnerability. Argentina is transforming into a commodity superpower with a deliberately hollowed-out knowledge economy, raising the question: Can a nation prosper long-term by trading brainpower for barrels?

USD/ARS Outlook: Milei’s Inflation-Linked PivotArgentina has officially changed how it manages the Peso. President Javier Milei’s government introduced a new currency band tied to inflation. This move replaces the old fixed system. The goal is to stop the Peso from becoming too expensive. Markets reacted calmly, with the Peso shifting slightly. This analysis explores why this matters for the USD/ARS pair.

Macroeconomics: The Inflation Link

The Central Bank of Argentina (BCRA) changed its trading rules. Previously, the Peso devalued by a fixed 1% monthly. Now, the trading band adjusts based on official inflation data. This prevents the currency from lagging behind real prices. The bank aims to build $17 billion in reserves. This liquidity is vital for stabilizing the economy. GDP is forecast to grow 3.5% next year, signaling a recovery.

Geopolitics & Strategy: Pleasing the IMF

This monetary shift is a strategic diplomatic move. The International Monetary Fund (IMF) openly urged Argentina to rebuild reserves. By loosening controls, Milei aligns with Western financial standards. This compliance is crucial for regaining access to international debt markets. It signals to global investors that Argentina is serious about paying its debts. This reduces the risk of default and attracts foreign capital.

Management & Leadership: The "Turnaround CEO"

View Milei’s administration as a corporate restructuring team. He acts like a CEO saving a bankrupt company. The "culture" has shifted from spending to austerity. He prohibited the Central Bank from printing money to fund the government. This is a massive leadership change. It forces the public sector to manage budgets strictly. This discipline builds trust in the management of the Argentine economy.

Industry Trends: The Tourism Flip

Currency value dictates tourism flow. A strong Peso made Brazil cheap for Argentines. Record numbers flocked to Brazilian beaches, spending money abroad. Conversely, foreign tourism to Argentina dropped 14% because it became too expensive. The new policy corrects this. A weaker Peso makes Argentina attractive to visitors again. This supports local hotels and restaurants that were losing business to neighbors.

Business Models: Exporters vs. Importers

The previous rigid exchange rate hurt Argentine exporters. Their costs rose with inflation, but their revenue stayed flat due to the currency peg. The new inflation-linked band fixes this broken business model. Farmers and manufacturers can now predict margins accurately. They no longer fear that inflation will eat their profits. This stability encourages them to sell goods abroad, bringing dollars into the country.

Technology & Cyber: Fintech Stability

A predictable currency is essential for the technology sector. Volatile exchange rates force tech companies to focus on financial hedging rather than product innovation. Stability allows fintech startups to plan long-term. It also reduces the need for citizens to use complex crypto-channels to hide wealth. A normalized economy reduces the incentive for digital black markets and cyber-financial crimes.

Science & Patent Analysis

Scientific progress requires long-term investment. Investors tend to avoid funding research in countries with unstable currencies. Milei’s push for a market-based currency helps value intellectual property (IP) correctly. International firms can now assess the value of Argentine patents without currency risk. This clarity could boost foreign direct investment (FDI) into Argentina’s scientific and biotech sectors.

Conclusion

The USD/ARS pair is entering a phase of controlled adjustment. The government will let the Peso weaken, but only to match inflation. This is a smart, calculated decline. It protects reserves and supports local industry. For traders, this means the trend is predictable. The volatility of the past may be replaced by a steady, managed trend.

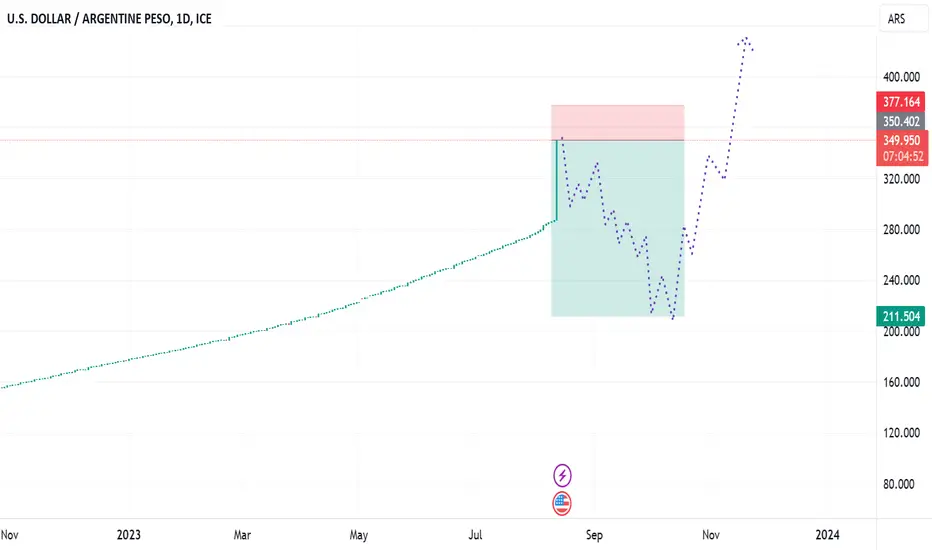

The Argentine peso swung sharply after US Treasury intervention

Treasury Secretary Bessent noted that Argentina faces a severe liquidity crisis, prompting Washington to finalize a USD 20 billion currency swap deal with the Argentine central bank. The rare move to directly purchase pesos appears aimed at preventing the collapse of President Javier Milei’s right-wing government amid mounting economic turmoil and public unrest.

USDARS broke below EMA21 and subsequently retested EMA78. The price broke below the ascending channel's lower boundary, indicating a potential shift toward bearish momentum. If USDARS breaks below EMA78 and the support at 1310, the price may decline further toward 1270. Conversely, if USDARS breaches above the resistance at 1370, the price may gain upward momentum toward the previous high at 1475.

Bad times for Argentina This is not a trade I am making. There's not liquidity for this and even if there was my desire to remain sane would make me very wary of fading this.

With that being said, purely as a TA stress test exercise, I think this is a high.

How much Purchasing Power will Argentina lose in 2023?

Argentina lost 9% of purchasing power in last 31 days

USDARS long this is a perfect trend ,huh? Let profits RUN!Strategy Bullish

Higher Highs Higher Lows

Retracement (10%)

Price above Quartely VWAP

Price above Decade VWAP

Volatility Bullish

Maket Sentiment 98% Bullish

Yearly Trend Bullish

Quartely Trend Bullish

Monthly Bullish

Daily Bullish

4H Bullish

2H Bullish

1H Bullish

30 min. Bullish

Portfolio Strategy:

Volatility/Risk(Per Trade)

Position Sizing

Risk Management 2: Trailing Stop (Donchian/Turtle Trader)/N(Volatility(Per Day) or (Quarter)*(risk per Trade)

William Jackson, chief emerging markets economist at Capital Economics, also noted that shocks from the El Nino weather pattern could prompt inflation in central and south American regions to cool more slowly than previously expected.

"Latin American central banks are unlikely to look through food price shocks given how strong headline inflation and wage growth in the region still are. So, upside inflation surprises could postpone the upcoming monetary easing cycles, or make them more gradual."

The Mexican peso slipped 0.4% and was set to snap a four-day winning streak, after touching its highest level since early December 2015 on Wednesday.

The MSCI gauge for Latam stocks (.MILA00000PUS) gained 1.3%, led by a 1.4% advance in Brazil's Bovespa

IBOV

.

Foreigners funneled over $22 billion net into emerging market portfolios in June, the largest amount since January, according to data from the Institute of International Finance.

A Guatemalan court ordered the suspension of anti-graft presidential candidate Bernardo Arevalo's political party, threatening his place in a run-off vote and prompting U.S. warnings of a challenge to democracy.

Elsewhere, the International Monetary Fund's executive board has approved an immediate $189 million disbursement to Zambia following its first review of a $1.3 billion loan programme.

Latam FX hits 10-year high on weak dollar as US inflation slows

The index for Latin American currencies touched a 10-year high on Wednesday, led by Brazil's real, as the dollar dwindled after a U.S. inflation reading indicated just one more interest rate hike by the Federal Reserve this year.

The MSCI index for Latam currencies (.MILA00000CUS) jumped 1.6%, hitting its highest level since April 2013.

Most currencies hit multi-year highs against a weakening dollar after June U.S. consumer prices rose at their smallest annual pace in over two years.

Although talks of rate cuts have intensified in Latam of late, bets on the U.S. rate-hiking cycle coming to an end will likely lead to a favorable interest rates differential.

The Mexican peso

USDMXN

jumped 1%, breaking below the psychological barrier of 17 pesos per dollar, touching an eight year high.

Higher crude oil prices also boosted the Mexican peso and top exporter Colombia's peso

USDCOP

by 0.8%.

Copper prices hit 2-1/2-week highs, boosting currencies of main exporters. Chile's peso

USDCLP

added 0.7% and Peru's sol

USDPEN

rose 1.3%, to its highest level since November 2020. Peru's central bank is set to decide on policy rates on Thursday.

Chile's Finance Minister Mario Marcel said the government now expects gross domestic product (GDP) to grow 0.2% in 2023, revising its forecast down from a previous estimate of 0.3%.

The Brazilian real (BRBY)

USDBRL

gained 0.8%, touching a one-week high.

The rapporteur for Brazil's tax reform bill in the Senate, Eduardo Braga, on Tuesday said that he expects the proposal to be voted on in October in the House.

Data showed Brazil's services activity grew by much more than expected in May, paring some losses seen in April despite high interest rates.

"Progress on the structural reform agenda and the (Brazil) government decision to maintain the CPI target at 3% have cleared the way for rate cuts; we expect a 50bps cut on August 2," said Lawrence Brainard, chief EM economist at TS Lombard.

Meanwhile, Argentine polling firms warned of difficulties accurately predicting the upcoming presidential primaries' results due to low turnout and the emergence of surprise candidates, leaving the October election also uncertain.

The MSCI index for Latam stocks (.MILA00000PUS) jumped 2.5%, touching a one-week high, led by a 1.4% advance Brazil's Bovespa

IBOV

.

World's largest meat packer JBS SA

JBSS3

jumped 9% after proposing a New York listing.

Separately, the International Monetary Fund (IMF) approved a $3 billion, nine-month bailout programme for Pakistan.

YEN Oil AUD NZD Asian stocks fall on bad chinese data

China Industrial Output Growth Beats Estimates

The Chinese economy advanced 6.3% yoy in Q2 of 2023, faster than a 4.5% growth in Q1 but missing market estimates of 7.3%. The latest figures were distorted by a low base of comparison last year when Shanghai and other big cities were in strict lockdown. During H1, the economy grew by 5.5%. China has set a GDP growth target of around 5% for this year after the economy expanded by 3% in 2022 and missed the government's target of about 5.5%. Beijing has shown reluctance to launch greater stimulus, especially as local government debt has soared. In June alone, indicators showed a mixed picture: retail sales rose the least in 5 months, industrial output growth grew for the 14th month, and the urban jobless rate was unchanged at 5.2% but youth unemployment hit a new high of 21.3%. Data released earlier showed shipments from China fell the most in three years, as high inflation in key markets and geopolitics hit foreign demand. A Politburo meeting is expected later this month.

Asian Stocks Fall on Weak Chinese Data

Asian equity markets fell on Monday as investors reacted to key data showing China’s economy grew 6.3% in the second quarter, lower than the 7.3% expansion expected by analysts. The Shanghai Composite led the decline, losing more than 1%. The Shenzhen Component, S&P/ASX 200 and Kospi indexes also tumbled. Meanwhile, Japanese markets are closed for a holiday, while Hong Kong markets will likely be closed for the day due to a typhoon.

China Stocks Drop on Weak GDP Data

The Shanghai Composite dropped 1.1% to around 3,200 while the Shenzhen Component lost 0.8% to 10,990 on Monday, giving back gains from last week as investors reacted to key data showing China’s economy grew 6.3% in the second quarter, lower than the 7.3% expansion expected by analysts. Meanwhile, China’s industrial production and fixed asset investments increased more than anticipated, while retail sales missed forecasts. Mainland stocks gained last week amid hopes that a faltering post-pandemic recovery would prompt Beijing to offer more pro-growth policy measures. Commodity-linked and financial stocks led the decline, with notable losses from Yunnan Lincang (-3.5%), Zijin Mining (-1.5%), China Shenhua Energy (-4.5%), ICBC (-6%), Ping An Insurance (-1%) and China Merchants Bank (-1.1%).

ARSUSD ShortStrategy bearish

lower Highs lower Lows

Retracement (10%)

Price below Quartely VWAP

Price below Decade VWAP

Volatility bearish

Maket Sentiment 98% bearish

Yearly Trend bearish

Quartely Trend bearish

Monthly bearish

Daily bearish

4H bearish

2H bearish

1H bearish

30 min. bearish

Portfolio Strategy:

Volatility/Risk(Per Trade)

Position Sizing

Risk Management 2: Trailing Stop (Donchian/Turtle Trader)/N(Volatility(Per Day) or (Quarter)*(risk per Trade)

William Jackson, chief emerging markets economist at Capital Economics, also noted that shocks from the El Nino weather pattern could prompt inflation in central and south American regions to cool more slowly than previously expected.

"Latin American central banks are unlikely to look through food price shocks given how strong headline inflation and wage growth in the region still are. So, upside inflation surprises could postpone the upcoming monetary easing cycles, or make them more gradual."

The Mexican peso slipped 0.4% and was set to snap a four-day winning streak, after touching its highest level since early December 2015 on Wednesday.

The MSCI gauge for Latam stocks (.MILA00000PUS) gained 1.3%, led by a 1.4% advance in Brazil's Bovespa

IBOV

.

Foreigners funneled over $22 billion net into emerging market portfolios in June, the largest amount since January, according to data from the Institute of International Finance.

A Guatemalan court ordered the suspension of anti-graft presidential candidate Bernardo Arevalo's political party, threatening his place in a run-off vote and prompting U.S. warnings of a challenge to democracy.

Elsewhere, the International Monetary Fund's executive board has approved an immediate $189 million disbursement to Zambia following its first review of a $1.3 billion loan programme.

Latam FX hits 10-year high on weak dollar as US inflation slows

The index for Latin American currencies touched a 10-year high on Wednesday, led by Brazil's real, as the dollar dwindled after a U.S. inflation reading indicated just one more interest rate hike by the Federal Reserve this year.

The MSCI index for Latam currencies (.MILA00000CUS) jumped 1.6%, hitting its highest level since April 2013.

Most currencies hit multi-year highs against a weakening dollar after June U.S. consumer prices rose at their smallest annual pace in over two years.

Although talks of rate cuts have intensified in Latam of late, bets on the U.S. rate-hiking cycle coming to an end will likely lead to a favorable interest rates differential.

The Mexican peso

USDMXN

jumped 1%, breaking below the psychological barrier of 17 pesos per dollar, touching an eight year high.

Higher crude oil prices also boosted the Mexican peso and top exporter Colombia's peso

USDCOP

by 0.8%.

Copper prices hit 2-1/2-week highs, boosting currencies of main exporters. Chile's peso

USDCLP

added 0.7% and Peru's sol

USDPEN

rose 1.3%, to its highest level since November 2020. Peru's central bank is set to decide on policy rates on Thursday.

Chile's Finance Minister Mario Marcel said the government now expects gross domestic product (GDP) to grow 0.2% in 2023, revising its forecast down from a previous estimate of 0.3%.

The Brazilian real (BRBY)

USDBRL

gained 0.8%, touching a one-week high.

The rapporteur for Brazil's tax reform bill in the Senate, Eduardo Braga, on Tuesday said that he expects the proposal to be voted on in October in the House.

Data showed Brazil's services activity grew by much more than expected in May, paring some losses seen in April despite high interest rates.

"Progress on the structural reform agenda and the (Brazil) government decision to maintain the CPI target at 3% have cleared the way for rate cuts; we expect a 50bps cut on August 2," said Lawrence Brainard, chief EM economist at TS Lombard.

Meanwhile, Argentine polling firms warned of difficulties accurately predicting the upcoming presidential primaries' results due to low turnout and the emergence of surprise candidates, leaving the October election also uncertain.

The MSCI index for Latam stocks (.MILA00000PUS) jumped 2.5%, touching a one-week high, led by a 1.4% advance Brazil's Bovespa

IBOV

.

World's largest meat packer JBS SA

JBSS3

jumped 9% after proposing a New York listing.

Separately, the International Monetary Fund (IMF) approved a $3 billion, nine-month bailout programme for Pakistan.

YEN Oil AUD NZD Asian stocks fall on bad chinese data

China Industrial Output Growth Beats Estimates

The Chinese economy advanced 6.3% yoy in Q2 of 2023, faster than a 4.5% growth in Q1 but missing market estimates of 7.3%. The latest figures were distorted by a low base of comparison last year when Shanghai and other big cities were in strict lockdown. During H1, the economy grew by 5.5%. China has set a GDP growth target of around 5% for this year after the economy expanded by 3% in 2022 and missed the government's target of about 5.5%. Beijing has shown reluctance to launch greater stimulus, especially as local government debt has soared. In June alone, indicators showed a mixed picture: retail sales rose the least in 5 months, industrial output growth grew for the 14th month, and the urban jobless rate was unchanged at 5.2% but youth unemployment hit a new high of 21.3%. Data released earlier showed shipments from China fell the most in three years, as high inflation in key markets and geopolitics hit foreign demand. A Politburo meeting is expected later this month.

Asian Stocks Fall on Weak Chinese Data

Asian equity markets fell on Monday as investors reacted to key data showing China’s economy grew 6.3% in the second quarter, lower than the 7.3% expansion expected by analysts. The Shanghai Composite led the decline, losing more than 1%. The Shenzhen Component, S&P/ASX 200 and Kospi indexes also tumbled. Meanwhile, Japanese markets are closed for a holiday, while Hong Kong markets will likely be closed for the day due to a typhoon.

China Stocks Drop on Weak GDP Data

The Shanghai Composite dropped 1.1% to around 3,200 while the Shenzhen Component lost 0.8% to 10,990 on Monday, giving back gains from last week as investors reacted to key data showing China’s economy grew 6.3% in the second quarter, lower than the 7.3% expansion expected by analysts. Meanwhile, China’s industrial production and fixed asset investments increased more than anticipated, while retail sales missed forecasts. Mainland stocks gained last week amid hopes that a faltering post-pandemic recovery would prompt Beijing to offer more pro-growth policy measures. Commodity-linked and financial stocks led the decline, with notable losses from Yunnan Lincang (-3.5%), Zijin Mining (-1.5%), China Shenhua Energy (-4.5%), ICBC (-6%), Ping An Insurance (-1%) and China Merchants Bank (-1.1%).

USDARS LONG

USDARS BULLISH SINCE YEARS

See the chart

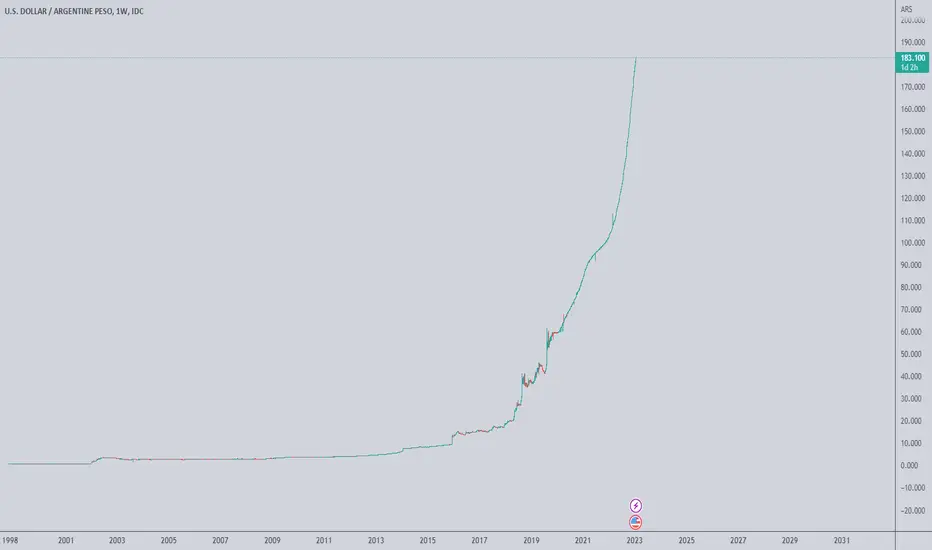

The Argentine peso has had a tumultuous life. In the 1980s it was temporarily dethroned by a new currency called the austral. An arranged marriage with the dollar in 1991 produced some years of bliss but ended in a ruinous divorce. More recently, the peso has suffered the humiliation of being tagged the worst-performing currency in emerging markets.

Now an Argentine economist running for president is proposing to put the currency out of its misery once and for all. Javier Milei, who’s also a congressman, says that to quash triple-digit inflation, the nation should formally adopt the dollar. “The peso melts like ice in the Sahara Desert,” Milei likes to say, alluding to the currency’s rapid depreciation: It’s lost half of its value against the dollar just in the past year.

Trend Bullish

Whatever trend trading methode you know,it works here!

USDARS SUPER BULLISHTechnical Analysis

Trend Bullish

Weekly Long

Daily Long

10H Long

4H Long

2 H Long

30min. LONG

Strategy Bullish

My Trading Conditions and my Rules(This are the Rules I follow,and they are no financial adivice for others)

Trade Consditions Higher Highs Higher Lows

Trade Rules: Taking only Buy Signals

Trade Rule 2: Only Buy Signals

Trade Rule 3: Exit only, if a Pullback my Stops hit.

Japanese Shares Rise as US Inflation Eases

The Nikkei 225 Index jumped 0.8% to above 32,200 while the broader Topix Index gained 0.3% to 2,228 on Thursday, rising from one-month lows and tracking a rally on Wall Street overnight as cooler-than-expected US inflation data raised hopes that the Federal Reserve is closer to the end of its tightening cycle. Investors also bought back technology stocks following days of consolidation, with notable gains from SoftBank Group (1.9%), Advantest (1.4%), Socionext (2.8%), Tokyo Electron (0.6%), Z Holdings (2.8%) and Renesas Electronics (2.5%). Other index heavyweights also advanced, including Sony Group (4.5%), Fast Retailing (1%), Daiichi Sankyo (4.5%), Mitsui & Co (1%) and Eisai Co (1.6%).

Australia Inflation Expectations Stable inJuly

NZX Trades Slightly Higher

New Zealand Factory Activity Shrinks to 7-Month Low

Argentina Indicators

Industrial Production 1.1 1.8 percent May/23

Industrial Production Mom 1.2 3.2 percent Apr/23

Capacity Utilization 68.9 67.3 percent Apr/23

Changes in Inventories -20633 20148 ARS Million Mar/23

Car Production 53282 54399 Units May/23

Car Registrations 38.6 33.8 Thousand May/23

Leading Economic Index -0.48 -0.28 percent May/23

Corruption Index 38 38 Points Dec/22

Corruption Rank 94 96 Dec/22

The Turkish lira extended losses to new all-time lows of 26.2 per USD, amid increasing signs of a shift to a more orthodox approach and as the central bank reportedly stopped using its reserves to support the currency. On June 22nd, the central bank of Turkey raised interest rates by 650 bps to 15%, marking a reversal from its previous ultra-loose and unorthodox monetary policy although the move fell short of meeting market expectations for a higher rate of 21%. Few days later, policymakers loosened measures designed to boost the lira, including lowering the securities maintenance ratio to 5% from 10% and the threshold for the share of lira deposits to 57% from 60%.

Argentine PESO Brutal Debasement against USD

Argentina attempts to lock it's population into the declining Peso.

cointelegraph.com

Sound money will endure

The easiest way to short FIAT/ARS is to Buy Bitcoin.

#Bitcoin #BTC

Burning Soy Dollars for Heat this ChristmasIntroduction

I originally published this piece on September 8th, 2022, when the Peso was at ~140:1. I am republishing it to TradingView to celebrate the 170:1 mark, made possible with consistent advances to TradingView's Idea publishing. I believe we will continue to see devaluation of Argentina's currency as a deterioration in commodity prices continues, along with regaining strength in the US Dollar. Please enjoy, and feel free to leave any questions or comments!

Thesis

The Soy-Dollar is another example of Argentina doing it to themselves. The country recently announced an exchange rate of 200 Pesos to 1 US Dollar for ~1 month timeframe, a dramatic benefit over the "open-market" 140:1. Argentina has a majority of it's economy driven on soybean farming, this isn't a niche market-pull. Altogether, the move comes as questions are being raised on the Treasury's ability to pay Dollar debts, threatening further depreciations against a currency that has suffered already. Argentina devaluing it's own currency to a major percentage of it's economy is one strike, doing the move when being questioned on finances is another, but leading it's own crises was the only one needed for a country batting badly in a t-ball league. The last ten years have been a whirl, but their hyperinflation has been so tremendous that I can only sympathize for a population with 37% risk of suffering from a mental illness in their lifetime (as of 2018, and conditions have gotten so very much worse). It feels terrible to call out destructive policies and watch them unfold, but this was a bad move. I cannot imagine arguing against a >140-200 Peso to Dollar rate after offering it to a majority of the economy, even for such a short time. A 30% currency devaluation by the bank isn't just a show of weakness, it's desperation to find a floor for their currency crisis. Showing favouritism to one market is going to kill diversification, something they needed to push for before with China ramping up their domestic soybean production by 40% in 2025. Their major importers are all suffering their own currency crises, few with direct swap lines with the Federal Reserve. Dollars are the blood of international trade, and they are drying up in critical emerging markets.

But Argentina did it to themselves. An interest rate of 3.5% is scaring the largest banks in the world and the US Treasury Secretary, Argentinians haven't had an interest rate under 20% in 5 years, currently sitting at 69.5%, which is under their Inflation rate YoY at 71%. Economies need to be able to experiment and fail in ventures; slap bracelets and fidget spinners are analogous to VR headsets and TACODOGCOIN for the economic participants to create an environment of willful employment-spend cycle. Will to work can be internal and external, sometimes getting the right carrot is better than buying an electric baton. Argentina does not get to experiment in business, so Argentina does not get to evolve. Argentina suffers from critical capital allocation issues - money is easily siphoned off (and rewarded) by different tax havens across the Western hemisphere, US included - but nothing that cannot be overcome so much so that they need to persistently suffocate their own economy.

In a previous Vignette I showed off a model for "Exporting-Importing Inflation", that is if a country is applying global inflationary pressures or absorbing them. Argentina has consistently pushed prices up for it's exports, an economy that should do amazingly well in an era of elevated soybean prices, but doesn't. International pressures aside, Argentina isn't a bastion of risk-free business even with a more competent central bank. Again, recent studies have highlighted the elevated anxiety and depression risks in bad economic climates, and Argentina's first-to-date psychological survey done in 2018 underscored a people suffering. Whatever price pressures Argentina is adding to the system isn't resulting in localized health, indicating a serious bleed - again not surprising given businesses have to contend with >50% interest rates.

Money Supply in Argentinian terms has grown at a logarithmic rate, right in step with the Peso's devaluation. But in "real" *USD* terms, the money supply has decreased. An oddity given external debt has only doubled, while GDP has (until 2018) had positive growth and in USD, superseding external debt (until 2018). And 2018 is really when things seem to have hit the fan for the country - bank strikes, general labor strikes, political uprisings with questionable arrests and charges across parties. Many of my research notes have looked at temporality of crises, in that events are rarely spontaneous. Balance of Trade and FX reserves reveal Argentina walked away from the GFC only to suffer from the Global recession afterwards. The country failed to find footing in the changed environment, had years of economic denigration leading to a lengthy period of recessionary behaviours. I believe Argentina is in an economic depression, likely starting in ~2013. Decreasing money supplies means the central bank has been diluting the value with a net system-loss effect.

The situation is bad, unlikely to improve soon. Argentina is suffering from a confidence issue; external investors are not confident Argentina will be able to pay debts (fair) and question future economic health (also fair), while internal consumers are suffering from hyperinflation tearing away at the value of their currency with a sustained environment against consumer spending. AND IT SHOWS. Consumer spending has dropped in real terms to nothing. That isn't to suggest the economy is dead, but consumers certainly aren't interacting with it on the government's terms - which means to outside investors the sovereign is dead. There are easy fixes and hard fixes. Argentina is suffering from a currency crisis the government deserves but the citizens don't - the Federal Reserve has offered direct credit swaps in the past to Brazil and Mexico (among others), and a line could help Argentina. I am still studying the effect these swaps have on the currency exchange rate, and it does appear to limit devaluation to a variable effect based on the internal economy. Argentina could benefit from the swap line in finding an easy supply to Dollars without hurting itself, but dollar liquidity isn't the cause for them. Hard fixes are fixing the internal business environment, which would require a direct combination of education (taking years to decades for full effect), guidance (national business combining localized banking initiative to address capital allocation), regulation, AND taxation. Offering low interest rates for businesses to experiment is critical in an economy, but the population is far from consumer-primed.

Argentina needs guidance, Government, Central bank, and national businesses alike. Diversification of goods, advanced manufacturing capabilities, internalization of demand, regulation and enforcement protecting domestic startups along with serious pushes in education, social improvement spending, technology and process development gifts. Debt isn't an enemy, but a lack of responsible and salient business plan is. Argentinian leaders need to develop a coherent timeline of events they can reasonably do to support citizens psychologically, socially, and economically to drive localized spending to create a sustainable economy. Working with international businesses to advance manufacturing capacity at responsible wages, and creating critical developmental infrastructure step-wise. Until then, Argentina will suffer as soybean demand declines worldwide against increasing global production and decreased national diversification- a worsening emerging market crisis - and a self-destructive central bank and sovereign government.

ARS Short - Heading to ZeroSUMMARY: Short, not sure if it NDFs are available for ARS.

When a meltdown occurs in the US, Argentina will go through another default potentially a new currency will be created.

ARS is completely oversold with more depreciation inboundSUMMARY: Not a good asset to HODL - risky to short as it is already oversold.

Crypto is growing in LATAM.

-- Technical --

Looks bad

-- Fundamentals --

Even worse.

Only a revolution can fix this one.

Please HIT the --->>> "LIKE" and "FOLLOW" button. <<<----

*Not financial advice and is for educational purposes only. Always DYOR.

SO: What do you think, have I got it right? Let me know below.

USD/ARS: up nearly 9000% since the 1990s... Hi traders!

In this video I look at:

- updates on my development as a trader;

- looking at exotic pairs;

- comparing various exotic pairs (USD/ARS, USD/TRY, USD/MXN) to the S&P500 and US Dollar Index (DXY);

- conclusions.

Take care!

Thanks for watching, I love you all.

Francesco

Forecast analys for Argentine pesoHyper inflation continues. On the black market price is almost double!

USDARS Breakout again Bullish flag brokeout recently. Expected to test higher highs.

Disclaimer: Published for educational purposes.

TA on ARS?I don't know how people do TA over this markets that always move up!

I think it might stop at fib @ 76.26$