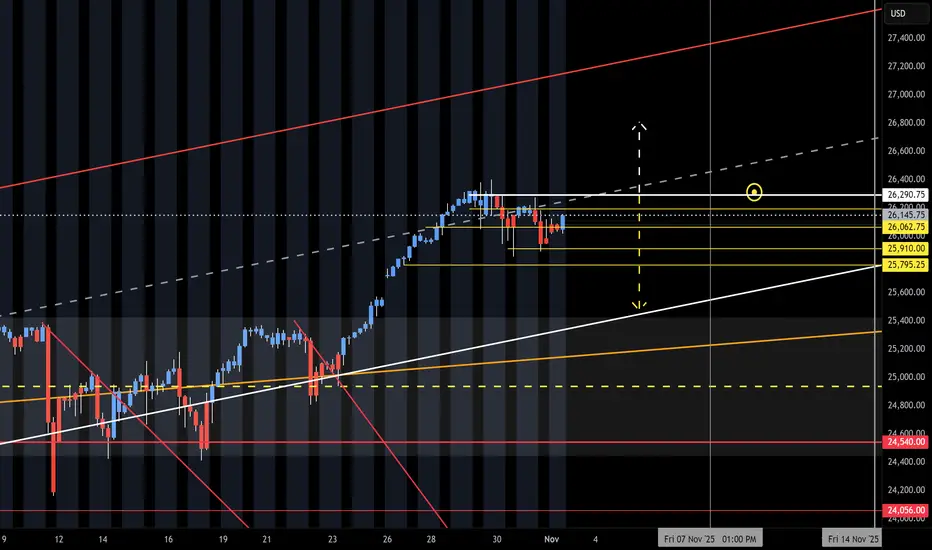

NQ Range (11-03-25, Week 6)The F-M Long move is on with new month and O/N Gap Open UP. Curveball form Friday Close and late head fake. Again, the NAZ will have to use the O/N to lift it back up. Need to see how the Open Drive and Reg Session reacts to the low volume O/N lift. Run up to upper target above KL 26,290 and Short on reject of. Under 290 is a potential drop to 25k or 25,550.

Trade ideas

Trying to go short but the demo platform is extremely glitchyTrying to go short and doing so but difficult to manage with glitchy platform.

NQI love the way this monthly chart for NQ is respecting the upward channel. If it fell to the middle line of the channel it is still overall bullish....

Note: check back in a few months

NQ Power Range Report with FIB Ext - 11/6/2025 SessionCME_MINI:NQZ2025

- PR High: 25335.75

- PR Low: 25272.00

- NZ Spread: 142.75

No key scheduled economic events

Session Open Stats (As of 2:55 AM)

- Session Open ATR: 420.01

- Volume: 55K

- Open Int: 296K

- Trend Grade: Long

- From BA ATH: -4.0% (Rounded)

Key Levels (Rounded - Think of these as ranges)

- Long: 26636

- Mid: 25410

- Short: 24039

Keep in mind this is not speculation or a prediction. Only a report of the Power Range with Fib extensions for target hunting. Do your DD! You determine your risk tolerance. You are fully capable of making your own decisions.

BA: Back Adjusted

BuZ/BeZ: Bull Zone / Bear Zone

NZ: Neutral Zone

How Global Markets Are Responding to Economic Shifts1. Price discovery and the immediate reaction

When new economic data or events arrive (jobs reports, CPI numbers, trade disruptions, or political shocks), markets move almost instantaneously to incorporate the information. High-frequency trading and algorithmic strategies often amplify initial moves — a surprise inflation print can trigger a sharp sell-off in bonds and a near-instant repricing of interest rate expectations. Equities typically show the widest variance by sector: interest-rate sensitive sectors (real estate, utilities) fall faster when rates spike, while commodity producers and cyclical industries may rally if the data imply stronger demand.

2. Interest rates and bond market mechanics

The bond market is the backbone of market response. Expectations about central bank policy — the path of short-term rates and the pace of balance-sheet actions — are priced into government yields globally. If inflation surprises on the upside or central banks signal tighter policy, yields rise and bond prices fall. This yields shock affects everything: higher yields increase the discount rate used to value equities, lower present values of future corporate earnings, and raise borrowing costs for companies and households. Conversely, signs of slowing growth or deflation risk push yields down, often boosting long-duration assets (growth stocks, long bonds).

3. Equity markets: winners, losers, and rotation

Stock markets reflect both macro outlooks and company-level fundamentals. In a growth-acceleration scenario, cyclicals, industrials, and small-cap stocks often outperform as investors rotate into riskier, higher-beta assets. In a growth-slowdown, defensive sectors (consumer staples, health care) and dividend-paying stocks usually offer relative safety. Market breadth and leadership shifts matter: when a handful of mega-cap tech companies are driving indices, the headline index may mask a narrower market. Active managers watch these leadership signals to rotate exposures.

4. Currency markets and capital flows

Currencies are real-time indicators of comparative economic strength and monetary policy. A central bank expected to raise rates will typically see its currency appreciate as yield-seeking capital flows in. Conversely, risk-off episodes trigger “flight-to-safety” flows toward reserve currencies (commonly the US dollar), pushing emerging-market and commodity-linked currencies lower. Persistent trade imbalances, capital controls, and sovereign risk perceptions also shape currency moves, which then feed back into inflation and corporate earnings through import costs and translation effects.

5. Commodities and real assets

Commodities react to both demand expectations and supply shocks. Energy prices surge with geopolitical tensions or supply disruptions, while industrial metals track global manufacturing health. Inflationary episodes often raise real asset prices — commodities and real estate can act as inflation hedges — but the relationship isn’t perfect and depends on real yields and growth expectations. Agricultural commodities can respond to weather and logistics as much as to macro demand.

6. Volatility, risk premia, and the cost of hedging

Economic shifts increase uncertainty, and volatility is the market’s “fear gauge.” Rising volatility raises the cost of hedging (options become more expensive), which alters trading strategies and risk management. Investors demand higher risk premia for holding volatile assets; this can push required returns up and valuations down. Institutional players often recalibrate portfolio risk — reducing leverage, increasing cash, or buying volatility protection — which can exacerbate short-term price moves.

7. Credit markets and corporate financing

Corporate bond spreads widen when growth fears or credit concerns rise, reflecting higher default risk or liquidity premiums. Tighter credit conditions hurt leveraged companies first, possibly slowing investment and hiring. Conversely, easier financial conditions (lower borrowing costs, ample liquidity) support refinancing, M&A activity, and risk-taking. The health of the banking system and non-bank lenders matters: stress in credit intermediation channels can transmit shocks to the broader economy quickly.

8. Policy responses and market feedback loops

Markets react not just to events but to the expected policy responses. Central banks and fiscal authorities monitor market signals closely. Sometimes markets move because investors anticipate policy easing or tightening; other times, central banks move because markets have moved (e.g., to restore stability). This two-way feedback can create virtuous cycles (confidence begets investment) or vicious ones (sell-offs trigger credit tightening). Transparency and forward guidance from policymakers help stabilize expectations, but surprises still cause sharp market adjustments.

9. Structural and technological influences

Market structure and technology have changed how responses unfold. Algorithmic trading, ETFs, and passive investment have altered liquidity patterns; large flows in and out of ETFs can amplify moves in underlying assets. Global interconnectedness means shocks travel faster — a manufacturing slowdown in one region quickly impacts supply chains and corporate earnings elsewhere. At the same time, data availability and analytics allow investors to react faster and to hedge with more precise instruments.

10. Longer-term asset allocation shifts

Sustained economic shifts—like a multi-year inflation regime change, deglobalization, or energy transition—reconfigure long-term allocations. Investors may favor real assets, shorten duration in fixed income, overweight certain regions, or increase allocations to alternatives (private equity, infrastructure) that offer different risk-return profiles. Pension funds and insurers, with long-dated liabilities, pay special attention to regime shifts because they directly affect funding ratios and required returns.

Conclusion — pragmatic lessons for investors

Markets are efficient at processing new information, but they are not always rational. Short-term reactions can be loud and disorderly; medium-term trends matter more for portfolios. Key practical takeaways: (1) watch interest-rate expectations and real yields — they shape valuations across assets; (2) track leadership and breadth in equity markets — it tells you if moves are broad-based or concentrated; (3) manage liquidity and hedging costs — volatility can spike unexpectedly; and (4) focus on scenario planning rather than prediction. A disciplined, diversified approach that explicitly considers how different assets respond to rate, growth, and inflation shocks will navigate economic shifts more successfully than one that chases yesterday’s winners.

NQ Nasdaq down to 24,900? Or rebound?The next level lower for NQ is 24,900. This price level also has confluence with the daily 200 EMA. Is there enough buyer interest to rebound before dropping to this level? Or, is this just a healthy pullback? Do you think NQ can go lower?

November 11 Trade Set Up rade Setup: NQ/MNQ/US100 (Short-Term: 4H/Daily Bias)

Bias: Profitable short-swing + mean-reversion, favoring range expansion and round-level confirmation.

Short Entry Zone:

Near 25,300-25,325 if price rejects this resistance, especially after a failed London/US bounce.

Confirmation: 4H candle wicks + volume spike + reversal signal (e.g., bearish engulfing or rejection at resistance).

Seasonals: Continued downside during post-earnings, pre-FOMC weeks.

Target:

First target: 25,226.50 (Asian session low, minor support).

Second target: 25,000 (full round level, cycle pivot, daily support).

Stop Loss:

Above 25,438 (cycle high, 4H resistance).

Alternative: ATR-based stop at ~110-130 pts above entry for MNQ/NQ intraday.

R/R:

Minimum 2:1 (Entry 25,300, first target 25,226, SL at 25,438 = 74 pts reward, 138 risk).

Mean-Reversion Alternative:

If price spikes below 25,000 intraday and prints a reversal (hammer, bullish divergence on 1H/4H), consider long scalp back toward 25,300.

Nasdaq reversa 6-11-25Sellers were absorbed in that area, and the Nasdaq will likely reverse from this point in the coming days.

If it breaks through the supply zone, the trend could turn bullish in the next few days.

NQ week 45Last weeks chart didn't have the fib levels to guess the tops so the chart quickly became invalid. I added the fib levels this week and posting on the 1hr instead of the 15min timeframe.

T.A explained -

BS & FS levels are expected support when dashed lines, tested when dotted and resistance when solid lines.

The inverse is true for the Inv. BS Inv. FS levels, they are resistance as dashed lines, tested as dotted and support as solid lines.

Monthly timeframe is color pink

weekly grey

daily is red

4hr is orange

1hr is yellow

15min is blue

5min is green if they are shown.

strength favors the higher timeframe.

2x dotted levels are origin levels where trends have or will originate. When trends break, price will target the origin of the trend. its math, when the trend breaks, the vertex breaks too so the higher timeframe level/trend that breaks, the more volatility there could be as strength in the orders flow in to fuel the move.

2 losses, could've gone full out. Could've made profit on the day but I saw a different narrative, we go again tomorrow.

Long towards Relative Equal HighsLong scenario for a Thursday reversal after major sellside levels have been triggered and a Breaker formed in Wednesday. Wednesday's high resides just below Tuesday's which makes the Buyside likely to get delivered.

NQ Power Range Report with FIB Ext - 11/5/2025 SessionCME_MINI:NQZ2025

- PR High: 25774.00

- PR Low: 25702.25

- NZ Spread: 160.0

No key scheduled economic events

Session Open Stats (As of 2:15 AM)

- Session Open ATR: 404.54

- Volume: 48K

- Open Int: 289K

- Trend Grade: Long

- From BA ATH: -2.7% (Rounded)

Key Levels (Rounded - Think of these as ranges)

- Long: 26636

- Mid: 25410

- Short: 24039

Keep in mind this is not speculation or a prediction. Only a report of the Power Range with Fib extensions for target hunting. Do your DD! You determine your risk tolerance. You are fully capable of making your own decisions.

BA: Back Adjusted

BuZ/BeZ: Bull Zone / Bear Zone

NZ: Neutral Zone

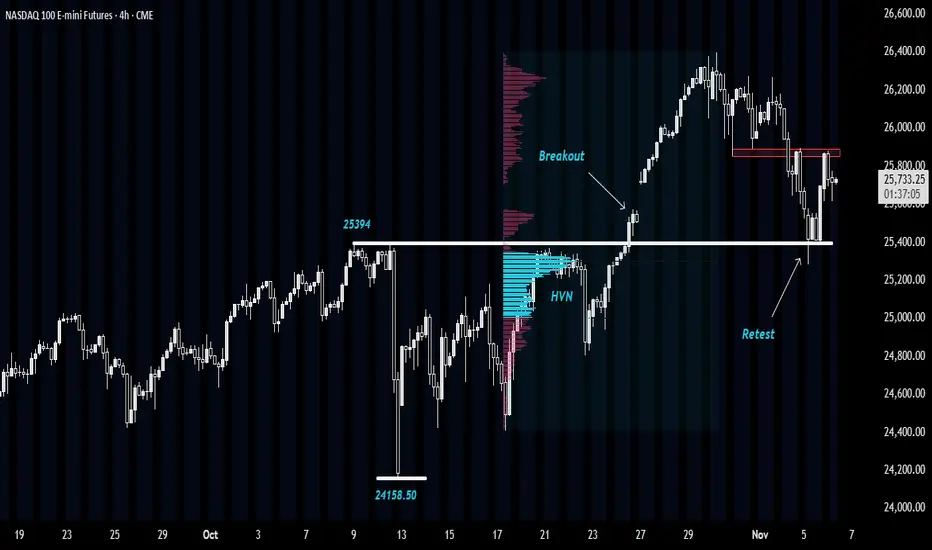

NASDAQ: Retesting Breakout ZoneThis idea is based upon successful Breakout Retest scenario near a High-Volume Node (HVN).

Let's first get to the basics:

A successful Breakout Retest -

A breakout retest scenario occurs when the price breaks through a key level of support or resistance and then returns to test that same level before continuing in the breakout direction.

For example, if the price breaks above a resistance zone, traders wait to see if the price comes back down to that zone. If it holds as new support and shows rejection candles or strong buying, that’s called a successful retest.

At a successful retest, several things typically happen:

➡The old resistance acts as new support (or vice versa in case of breakdown).

➡Traders who missed the initial breakout enter the trade, adding momentum.

➡Weak hands or short-term traders exit, cleaning up the order flow.

➡The price often accelerates in the direction of the breakout with stronger conviction and volume.

In simple terms, a successful retest confirms that the breakout was genuine and not a false move.

High Volume Node -

HVN is a price level or zone on a volume profile where a large amount of trading activity has occurred. It represents an area where buyers and sellers actively agreed on price, leading to high transaction volume.

These zones usually act as balance areas- price tends to pause, consolidate, or even reverse near them because many traders have open positions there. When price revisits an HVN, it often encounters strong support or resistance, as market participants react to protect or exit their earlier trades.

In short, an HVN marks a fair value area on the chart where market consensus was strongest.

NASDAQ Analysis -

In the Nasdaq E-mini chart, we can observe a sharp decline from 25,394 to 24,158, but without any meaningful follow-through on the downside.

Subsequently, the price reacted once again from this same zone on 21st and 22nd October, before eventually breaking above 25,394 with strong momentum to form new highs.

At present, the market has pulled back to the 25,394 level, which previously acted as resistance. This area is now holding as support, suggesting a successful retest and presenting a potential buying opportunity.

Moreover, this retest is aligning with a HVN around 25,300, further reinforcing the support zone.

In the short term, the price is facing resistance near 25,900. A conservative long entry could be considered after a sustained move above 25,900, while an aggressive low-risk entry could be initiated around 25,500, closer to support.

📣Disclaimer:

Everything shared here is meant for education and general awareness only. It’s not financial advice, nor a recommendation to buy, sell, or hold any asset. Do your own research, manage your risk, and make sure you understand what you’re getting into.

ORB Pro Signal Recap – Nov 5, 2025 | “Respect the Levels”Ticker: QQQ / NQ1! (5-min + 15-min TF)

Strategy: ORB Pro + Trendline Breakdown + Previous Day High Rejection

Focus: Signal confirmation & reaction zones

🧭 Market Context

The morning started strong, with buyers pushing off the open toward the previous day’s high (PDH) and ORB extension zone.

As price tapped the upper band, the ORB Pro system generated a clean long confirmation, aligned with the higher timeframe momentum.

But the rally quickly stalled at the PDH — a textbook reaction zone where the structure shifted.

From there, trendline breakdowns on both 5-min and 15-min charts confirmed exhaustion, and the system correctly prevented new long entries once momentum failed.

💹 Trade Breakdown

Initial Long: Taken on ORB Pro signal confirmation near the intraday retest (strong follow-through into PDH).

Profit-Take Zone: Price rejected sharply at the PDH and VWAP cluster — partials locked.

No Chasing: After the rejection, ORB Pro flagged “Blocked / Too Late,” keeping risk managed while trend flattened.

Result: Finished the day green with multiple small wins across calls — +$89.68 net on the $623C and +$15.89 on $626C.

📊 Performance Summary

Symbol Side Contracts Net Result

QQQ $623C Long 2 +$89.68

QQQ $626C Long 1 +$15.89

QQQ $622P Short hedge 1 –$3.11

Total P/L + $102.46 (Realized)

📈 Chart Recap

Price pushed through the early range with momentum but stopped exactly at the previous day’s ORB high and Fib confluence.

That rejection aligned perfectly with the HTF resistance zone on both 5-min and 15-min TFs.

The chart shows two green “LONG” entries and a clean signal fade once volume dropped —

a prime example of respecting structure over bias.

💡 Key Takeaways

PDH = Reaction Zone: Don’t ignore prior highs — they mark algorithmic defense zones.

Trust the Filters: ORB Pro prevented chasing the failed continuation after PDH rejection.

Structure First: The trendline breakdown confirmed what price was already telling us.

🧘♂️ Reflection

“The system signaled the move early, and I followed structure. PDH rejection confirmed the top, and discipline locked the profit. The goal wasn’t to predict — it was to react with control.”

NQ: 282st trading session - recapSession was pretty alright, learned a couple new things tbh sooo atelast a good experience

Educational Video pt. 2 Found a couple trades and gave some good reasoning on why I would take them ..... 'like' this video

Educational video. Hit the 'LIKE' button if this helped you.This is my thought process on how to trade. If you would like me to post more recorded videos like this.. or even when I am in a trade , please feel free to 'COMMENT' below this video. This is my logic on the market and this is why my name is NASDAQNYK. You dont need 20 indicators on your charts, you dont need anything but your eyes and 3 confluences to determine your typical entry and exit. Trading is only hard when you make it hard.

Tape reading and reasoning for AM trade excecutionMe explaining what SHOULD happen in price over price action and then doing an AM trade review.

REMOVING NASDAQ FROM MY TRADING PLANTransition Note – Focusing Exclusively on EUR/USD

After several months of structured testing and data collection, I’ve decided to permanently remove the NASDAQ (US100) from my analytical framework and trading routine.

While the index offers remarkable volatility and potential, my recent journal review made something clear: the NASDAQ does not align with my strategy’s statistical edge.

The asset’s internal structure — heavily driven by algorithmic order flow and micro-volatility — tends to invalidate setups based on value zones, Wyckoff redistribution, and delta imbalances, which are the core of my system.

In contrast, EUR/USD consistently responds to institutional behavior:

clear dealing ranges and discount/premium rotations,

stronger respect for volume-based structures,

and predictable liquidity flow across sessions.

The data is objective:

• Win rate on NASDAQ – 38%

• Payoff ratio – 1.1:1

• Net result – negative

• Win rate on EUR/USD – 52%

• Payoff ratio – 2.16:1

• Net result – strongly positive

Therefore, all future macro and technical publications will focus exclusively on EUR/USD, with no further NASDAQ breakdowns or updates.

My aim is to refine precision, deepen macro integration (liquidity, yields, policy cycles), and operate where the statistical edge truly exists.

Consistency begins with focus — and mine is now 100% on the euro.

Simple trade Idea, clear bias and excecution.Trading In the direction of the 1H narrative along with judas swing, excecution on the suspension block supporting price, targeting REH's. Simple.

Target areas - NQ price for Market open.11/5/25 - These are the target areas - NQ price for Market open depending if price moves up or down. Will look for trades into these areas.