spx500 defying the laws of gravityThis is the mother of all artificial market (AMM) manipulations. Can someone definitively tell me why this market has not corrected please? Everything stocks do NOT like has happened since 9-30-16. Dollar up, other currencies down large, note the previous red boxes and historically. And now DXY is up and oil is up, oil Barron's are manipulating price. What happened to supply and demand and fundamental evaluation? Gone, finished, out of here. Biased news, AMM, and the forces coming from that large hidden room where commands are given daily of what to prop up by those who would be unnamed, are the only forces that matter. That is THE BUBBLE folks, where no economics substantially matter, and stock price is news dependent, or better yet purpose generated rumor dependent. Better odds betting on two turtles racing these days, and more exciting. Until Nov 9th, throwing in the towel, taking a break, crying uncle, watching from the sidelines, licking my wounds, getting some R & R, etc, etc,etc. This election will change the USA forever, one way or the other, and as a result will revise trading back to fundamentals and economics (Trump), or not just more of the same AMM, but a much worse version of it, which would make me throw in the towel. Nothing is real anymore, just created for a purpose, real or not, leaked, and used for political and market prop purposes. Can't prove it, but I cannot see the the wind either, but I feel the it when it blows, and I know it is there. Careful trading folks, careful, careful.

USDCNYTMSP trade ideas

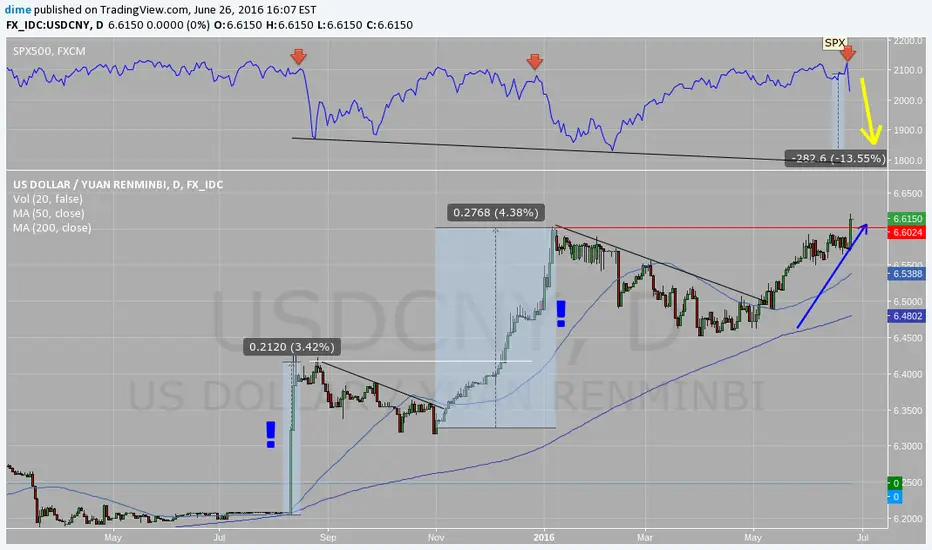

Two clear action points!The trend is your friend!

If we could trade above the last high @ 6.7 i exspect the next buying wave up to 6.75 (6.8 overshooting)

A dip down to 6.6 can be seen as a retest of the last bo - here is also based the last top from january 2016, which should be a supportive zone.

Trading below 6.6 has to be seen critically. The next TP below 6.6 could be the ema 200 @ 6.56 (inxreasing)

Best regards Mary

Comments are Welcome

USDCNY short or long, depends on strategyPersonaly I'll wait for the long, but there might be an opportunity for a short.

Closely watching for selling to beginThe pair could drop rapidly once breaking 6.65 price level. Buyers activity has toned down significantly.

OIL cannot stand up against the dollar strength Which is about to happen. China will devalue when needed, as needed. Japan needs the yen down to validate all the QE lately. Pound going to parity with dollar sooner than later. etc. and if inventory build is more than expected. look out below.

usdcny spx500 relationshipI thought I saw this before, and now I see it. The next move could very well be a cny devalue, which would snap dollar up, markets down, oil down. Megaphone patterns repeat? spx500 retrace .5 or more? RSI TL support reached . IMO.

Global Selloff: Keep your eye on USD/CNY If this game was baseball, three strikes would mean you're out. Could this be the start of a third wave of devaluation in the Chinese Yuan?

Each time the Chinese Yuan devalues it just happens to coincide with a massive selloff in the SPX. 2015 was the first time that China reduced its stake in Treasuries on an annual basis in an attempt to support the yuan and stem capital outflows. Last year $225 billion in U.S. Treasury debt was sold, the most on record since 1978. The largest owner of U.S. debt, China dumped hundreds of billions in U.S. Treasuries in August and December.

Large devaluations of the Yuan occurred in August and Dec 2015. The PBOC shocked world markets last August with a surprise devaluation of the Yuan knocking over 3% off its value - the largest single drop in 20 years. China sold more than $100 billion of foreign-exchange reserves in August and again by January. Beijing announced in February the country’s foreign-exchange reserves fell to the lowest level in more than three years. The Chinese government continues to attempt try and stop the flow of money leaving the country for overseas investment.

$CNYUSD responsible for rise in $BTCUSD ??I recently read an article of Reuters explaining that the recent rise in $BTCUSD has the $CNYUSD sell off to thank.

www.reuters.com

But out of curiosity, I wonder what percentage of the $BTCUSD rally was caused by Chinese traders buying into Bitcoin. After all, most Chinese DON'T invest their money into the market. Perhaps the $BTCUSD rally is caused by traders buying because they think other traders (particularly the Chinese) will buy. Thus the current Bitcoin rally could be explained as a "self fulfilling loop"

Finance minister Lou Jiwei says that china has no interest to devalue it's currency any further, and has attributed these conversations to media hype.

www.ecns.cn

The discussion of a June rate hike in the US may be what is fueling speculation on a $CNYUSD devaluation. But recent economic indicators would suggest the FOMC may approach this month's meeting with caution. Although home prices are rising, a sign of strength, the recent employment numbers were soft and in part caused by decreasing participation in the labor market, not a sign a sign of strength. As we approach the FOMC announcement, if economic indicators continue to produce soft numbers, we should not expect a rate hike. This in turn should fuel a rebound in $CNYUSD, which may cause a $BTCUSD sell off.

At this point, it is anyone's guess how high the $BTCUSD rally will go. But if the recent rally was indeed fueled by speculation of a $CNYUSD devaluation, which is in turn fueled by fed rate hike speculation, then it would not be surprising if we begin to see a selloff in $BTCUSD following more weak economic indicators.

SPXCapital flight pressure building again in China.. Also visible in BTC. We could see a sharp sell-off again in coming months.

Is USDCHN now in a cup-with-handle base?The offshore RMB is the orange line. As you can see, the history is too short, so the main USDCNY chart is shown.

YUAN RENMINBI IS SOMETHING TO WATCHYuan devaluation has been significantly correlated to global market corrections. Let's see if there is a new one coming.. Probably soon... poop

Week ahead - All about US interest ratesMarkets appeared to have changed their tune regarding Fed interest rate outlook after US data released on Friday showed retail sales in April jumped by most in a year. Even before the data release, a significant minority was expecting Fed to move rates in June/September if wage price inflation strengthens.

The week ahead is a busy one for the markets as US CPI and Fed minutes will provide clues on inflation and on how fast the central bank may push up rates this year. It is a busy week for UK as well, with CPI, Employment data and Retail Sales scheduled for release.

US data - CPI and Industrial Production is due for release on Tuesday, FOMC April Meeting Minutes Wednesday and a raft of Fed speakers with Dudley Thursday. Regional PMI indices, initial jobless claims and housing data is due as well.

UK data - CPI is due on Tuesday, Employment data Wednesday and Retail Sales Thursday.

Eurozone – Quiet week ahead, with just CPI and trade balance scheduled for release.

Japan – GDP due on Thursday.

Australia - RBA May board minutes are due on Tuesday and the employment report Thursday.

China – Dismal retail sales, industrial production and fixed asset investment was released over the weekend.

Dollar bulls will be glued to the economic calendar this week as a strong rebound in monthly inflation could increase the odds of a Fed June rate hike. Furthermore, a clue regarding a possible rate hike in June could come via April Fed minutes due on Wednesday.

G7 meet in Tokyo on Friday

Another global event - G7 Finance Ministers and Central Bank Governors meet Friday would be watched out by traders. Treasury Secretary Jacob Lew is widely expected to tell Japanese officials to stop threatening to depreciate the yen amid. Note that aggressive monetary easing (intended to weaken currency) by Bank of Japan and other central banks could easily force Fed to delay rate hikes despite improvement in the domestic data. Hence, strong words from US could bring easing madness to a halt (at least temporarily) and pave way for Fed rate hike.

Iron price is falling again… and so is Yuan

Iron ore prices fell 5.2% on Friday taking the total weekly loss to 13% amid steel oversupply concerns and regulators announced measures to curb speculative trading in iron ore. Prices hit a 16-month high in April before losing ground. Prices now hover around 6-week low.

Weakness could persist this week, given the weak China data released over the weekend. This could also add pressure on the Aussie, which is silently losing ground over the last two weeks.

Meanwhile, Chinese Yuan is weakening again. On Friday, the offshore currency, also known as CNH, hit the lowest since in three months as the People’s Bank of China set the Yuan reference rate against the dollar at 6.5246, the weakest since March 4.

As per Xinhua news, “The central parity rate of the Chinese currency Renminbi, or the Yuan, weakened 97 basis points to 6.5343 against the US dollar today”.

However, the decline so far has been moderate. Moreover, markets are slowly digesting the fact that Yuan is likely to be on a slow and steady declining trend. Nevertheless, decline in Yuan puts downward pressure on other EM/Asian currencies and Japanese Yen as well.

UK corporate results due this week

Monday – British Land Company

Tuesday – Land Securities Group

Wednesday – Burberry Group, SABMiller

Thursday – National Grid

USDCNY 4/26/2016This is for those of you who are trading USDCNY. It's hard to trade something as protected as USDCNY, but know that given a long enough time period, nothing escapes triangular geometry.

bitcoin 3rd wave begins today :D#ltc on long support, #btc beginning 3rd wave, #btce alts accumulating. omg! moon!