1h TF - Long on Dow Jones Industrial Average Index (Ticker DJI)TVC:DJI

Technicals:

Having the price consolidated between 48800 and 49600 during January, trade picture strongly depend on market sentiment and event occurence.

- Short-term Long scenario:

In case price decides to move above 49600 a descent amount of stop-losses will be collected, pushing / squeezing the price up to 50000. For that case a target is set according with recent price movements having reached a zone between 1.618 and 2.272 on fibo after breaking out from consolidation. After that price can find ressistance near ascending trend upper line. If further movement rejected, a probability of a short movement down to 48800 / 48400 increases

- Short-term Short scenario:

In my opinion this scenario is a positive one, as the price can go lower to collect some power for further impulse above 49600 and later do overhigh, signaling that industry is still ok. For that case beforewards price can go significantly lower that 49100 making risk-management for this particular position too high. For this reason the short stop is set only a few pips below recent bouncing candles and flying level (see orange circles on the screen)

Fundamentals:

- take care of 6th Feb friday`s report on employment in USA, cause the higher unemployment rate will mean that economy might struggle in nearest future, whereas the lower unemployment rate means directly the opposite

Conclusion:

- in my opinion the second scenario seems to be more likely as the US companies will continue to report in february on financials for recent 4th Quartal of 2025 as well as on earning estimation for 2026, letting the price being like soda in a bottle and consolidating before further breakout

- despite this I expect a stop-loss hunt in a nearest term and therefore open a short-term long on 1h tf with SL below recent bounce candles and TP targeting:

+ middle level of fibo 1.618 / 2.272 as well as

+ 1.53% breakout movement having multiplied recent breakouts benchmarks with 0.88 (because of 12% power reduction in a movement after breakout)

# - - - - -

⚠️ Signal - Buy ⬆️

✅ Entry Point - 49501.30

🛑 SL - 49161.27

🤑 TP - 50371.72

⚙️ Risk/Reward - 1 : 2.6 👌

⌛️ Timeframe - 1 day 🗓

# - - - - -

Good Luck! ☺️

# - - - - -

DISCLAIMER: Not financial advice. Everyone must make trading decisions at their own risk, guided only by their own criteria and strategy for opening or not opening a trade.

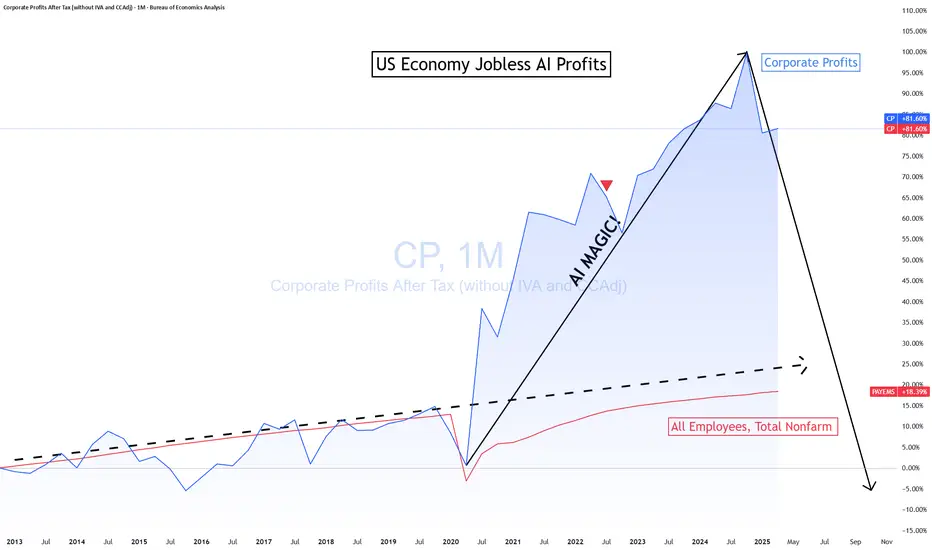

Employment

US Economy Jobless Profits!💻 The AI Circle-Jerk Profits 💰

Everyone’s hyped on “AI revolution” headlines — but look under the hood:

Only a handful of companies are actually making real profits.

The rest? Selling picks and shovels to each other, inflating margins with paper demand.

When everybody’s a supplier and nobody’s the end user, that’s not innovation — that’s a loop.

And loops break hard when capital costs rise or sales flatten.

Call it what it is: an AI circle jerk of revenue recycling.

Watch for profit compression once the hype premium fades.

Click boost, follow, comment nicely for more authentic, no BS, raw analysis. Let's get to 5,000 followers. ))

$SPY / $SPX Scenarios — Friday, Sept 5, 2025🔮 AMEX:SPY / SP:SPX Scenarios — Friday, Sept 5, 2025 🔮

🌍 Market-Moving Headlines

🚩 Jobs Friday = make or break. Nonfarm Payrolls, unemployment, and wages will lock in Fed expectations into September.

📉 Positioning light ahead of NFP — futures choppy as traders square books.

💬 Consumer sentiment wraps the week — expectations on inflation and spending will color the tape.

📊 Key Data & Events (ET)

⏰ 🚩 8:30 AM — Nonfarm Payrolls (Aug)

⏰ 🚩 8:30 AM — Unemployment Rate (Aug)

⏰ 🚩 8:30 AM — Average Hourly Earnings (Aug)

⏰ 10:00 AM — Wholesale Trade (Jul)

⏰ 10:00 AM — UMich Consumer Sentiment (Final, Aug)

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #NFP #jobs #labor #Fed #economy #bonds #Dollar

$SPY / $SPX Scenarios — Thursday, Sept 4, 2025🔮 AMEX:SPY / SP:SPX Scenarios — Thursday, Sept 4, 2025 🔮

🌍 Market-Moving Headlines

📉 Markets on edge after ADP + Beige Book — traders want to see if Thursday’s labor + growth data confirm a slowdown.

🏦 Treasury supply + Fed tone continue to steer $TLT/$TNX.

⚙️ Productivity & costs add another layer to the inflation debate.

📊 Key Data & Events (ET)

⏰ 🚩 8:30 AM — Initial Jobless Claims (weekly)

⏰ 8:30 AM — Trade Balance (Jul)

⏰ 8:30 AM — Productivity & Unit Labor Costs (Q2, rev.)

⏰ 11:00 AM — Kansas City Fed Manufacturing Index (Aug)

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #Fed #joblessclaims #labor #economy #bonds

EGX30 Positive TrendEGX30 stock is currently in a rising region. In case of continuing, it's expected to breach the resistance line 36,202.344. In case of decreasing, it's expected to reach the support line 35,424.707, 34,880.361, then 34,647.070. This is a result of positive news as Egypt's blue-chip index EGX30 advanced for a fourth day and rose 1.6% to hit a record high at 35,254. EAST soared 5.5% and TMGH gained 0.7%. Meanwhile, Egypt's non-oil private sector showed signs of stabilization in July, with employment rising for the first time in nine months and a softer decline in output and new orders, the S&P Global Egypt PMI report said. Egypt's blue-chip index EGX30 advanced for a fifth day and rose 0.6% to hit a fresh record high at 35,480. ETEL soared 4.8% and FWRY gained 1.9%. Meanwhile, Egypt's net foreign reserves rose to $49.036 billion in July from $48.7 billion in June, the central bank said on Tuesday.

New Zealand's unemployment rate rises to 4½ high, Kiwi pushes hiThe New Zealand dollar continues to have a quiet week. In the European session, NZD/USD is trading at 0.5923, up 0.37% on the day. The kiwi has been under pressure, falling 3.4% against the US dollar in July.

New Zealand's employment report for Q2 was pretty much as expected, but the news wasn't good. The unemployment rate rose to 5.2% from 5.1% in Q1, below the consensus of 5.3%. This marked the highest unemployment rate since Q3 2020. Employment Change declined by 0.1%, down from a 0.1% gain in Q1 and matching the consensus. This was the third decline in four quarters.

The weak figures point to growing slack in the labor market as the economy continues to struggle. Global trade tensions remain high and New Zealand's export-reliant economy has taken a hit from softer global demand.

The Reserve Bank of New Zealand will be paying close attention to the weak job numbers, which support a rate cut in order to provide a boost to the economy. The RBNZ maintained rates in July after lowering rates at six consecutive meetings. The conditions for a rate cut at the Aug. 20 meeting seem ripe and the markets have priced in a quarter-point reduction at around 85%.

We'll get an updated look at the inflation picture on Thursday. Inflation Expectations rose to 2.3% in the second quarter, the highest in a year. This is the final tier-1 release prior to the August rate meeting.

Three FOMC members will speak later today and investors will be hoping for some insights regarding the Federal Reserve's rate plans. The Fed hasn't lowered rates since December but is widely expected to hit the rate trigger at the September meeting.

UK employment,wage growth falls, US retail sales shineThe British pound showing limited movement on Thursday. In the North American session, GBP/USD is trading at 1.3406, down 0.09% on the day.

Today's UK employment report pointed to a cooling in the UK labor market. The number of employees on company payrolls dropped by 41 thousand in June after a decline of 25 thousand in May. Still, the May decline was downwardly revised from 109 thousand, easing concerns of a significant deterioration in the labor market.

Wage growth (excluding bonuses) dropped to 5.0% from a revised 5.3%, above the market estimate of 4.9%. The unemployment rate ticked up to 4.7%, up from 4.6% and above the market estimate of 4.6%. This is the highest jobless level since the three months to July 2021.

The latest job data will ease the pressure on the Bank of England to lower rates, as the sharp revision to the May payroll employees means the labor market has not deteriorated as much as had been feared. Still, the employment picture remains weak and the markets are expecting an August rate cut, even though UK inflation was hotter than expected in June.

US retail sales bounced back in June after back-to-back declines. Consumers reacted with a thumbs-down to President Trump's tariffs, which took effect in April and made imported goods more expensive.

The markets had anticipated a marginal gain of just 0.1% m/m in June but retail sales came in at an impressive 0.6%, with most sub-categories recording stronger activity in June. This follows a sharp 0.9% decline in May.

The US tariffs seem to have had a significant impact on retail sales, as consumers continue to time their purchases to minimize the effect of tariffs.

Consumers increased spending before the tariffs took effect and cut back once the tariffs were in place. With a truce in place between the US and China which has slashed tariff rates, consumers have opened their wallets and are spending more on big-ticket items such as motor vehicles, which jumped 1.2% in June.

UK employment,wage growth falls, US retail sales shineThe British pound showing limited movement on Thursday. In the North American session, GBP/USD is trading at 1.3406, down 0.09% on the day.

Today's UK employment report pointed to a cooling in the UK labor market. The number of employees on company payrolls dropped by 41 thousand in June after a decline of 25 thousand in May. Still, the May decline was downwardly revised from 109 thousand, easing concerns of a significant deterioration in the labor market.

Wage growth (excluding bonuses) dropped to 5.0% from a revised 5.3%, above the market estimate of 4.9%. The unemployment rate ticked up to 4.7%, up from 4.6% and above the market estimate of 4.6%. This is the highest jobless level since the three months to July 2021.

The latest job data will ease the pressure on the Bank of England to lower rates, as the sharp revision to the May payroll employees means the labor market has not deteriorated as much as had been feared. Still, the employment picture remains weak and the markets are expecting an August rate cut, even though UK inflation was hotter than expected in June.

US retail sales bounced back in June after back-to-back declines. Consumers reacted with a thumbs-down to President Trump's tariffs, which took effect in April and made imported goods more expensive.

The markets had anticipated a marginal gain of just 0.1% m/m in June but retail sales came in at an impressive 0.6%, with most sub-categories recording stronger activity in June. This follows a sharp 0.9% decline in May.

The US tariffs seem to have had a significant impact on retail sales, as consumers continue to time their purchases to minimize the effect of tariffs.

Consumers increased spending before the tariffs took effect and cut back once the tariffs were in place. With a truce in place between the US and China which has slashed tariff rates, consumers have opened their wallets and are spending more on big-ticket items such as motor vehicles, which jumped 1.2% in June.

US Unemployment Rising: How Is This NOT a Recession?The U.S. unemployment numbers are steadily climbing, as indicated by recent Bureau of Labor Statistics data. Typically, significant rises in unemployment correlate directly with recessions, which are shaded gray in historical data charts.

Currently, unemployment has reached over 7 million, significantly higher than recent lows. Historically, every similar increase has coincided with or preceded an official recession declaration. Yet, mainstream economic narratives have avoided labeling this a recession.

What does this data tell us, and is the market accurately pricing in the risk? Are we already in a recession, or is this time different?

Share your thoughts below. Let's discuss the disconnect between the unemployment reality and official recession narratives.

Australian dollar loses ground, jobs report nextThe Australian dollar has declined on Wednesday. In the North American session, AUD/USD is trading at 0.6441, down 0.45% on the day. This follows the Australian dollar's massive gains of 1.5% a day earlier.

Australia's wage growth accelerated in the first quarter. Annually, the Wage Price index gained 3.4%, up from 3.2% in Q4 2024 and above the market estimate of 3.2%. The gain was driven by stronger wage growth in the public sector. On a quarterly basis, wage growth rose 0.9% q/q, up from 0.7% and above the market estimate of 0.8%. This is the first time since Q2 2024 that annual wage growth has accelerated.

The higher-than-expected wage report comes before next week's Reserve Bank of Australia's rate decision. Currently, it looks like a coin toss as to whether the Reserve Bank will maintain or lower rates.

Australia releases employment data on Thursday. Employment change is expected to ease to 20 thousand in April, down from 32.2 thousand in March. The unemployment rate is expected to remain at 4.1%. The labor market has been cooling and if it continues to deteriorate, there will be pressure on the Reserve Bank to lower rates.

At last week's Federal Reserve meeting, Fed Chair Powell said that he would take a wait-and-see attitude in its rate policy. Trump's erratic tariff policy must be frustrating for the Fed, as it makes it difficult to make reliable growth and inflation forecasts.

This week's surprise announcement of a tariff deal between the US and China is a case in point at Trump's zig-zag trade policy. The two sides have been engaged in a bruising trade war and slapped massive tariffs on each other's products. Suddenly, the tariffs were slashed, leading to a sigh of relief in the financial markets. The deal is only for 90 days, and what happens then is very much up in the air.

Canadian dollar shrugs after mixed employment numbersThe Canadian dollar is steady on Friday, after a two-day slid in which the loonie declined by 1%. In the North American session, USD/CAD is trading at 1.3911, down 0.09% on the day. On the data calendar, Canada released the employment report and there are no US economic releases.

The April employment report didn't show much change and the Canadian dollar has shown little reaction. The economy added 7.4 thousand jobs, rebounding from the loss of 32.6 thousand in March and above the market estimate of 2.5 thousand. At the same time, the unemployment rate climbed to 6.9%, higher than the market estimate of 6.8% and above the March reading of 6.7%. This was the highest level since Nov. 2024.

The rise in unemployment is likely a reflection of the US tariffs. Canada's exports to the US were down in March, hurting businesses that export to the US. If the tariffs remain in place, weaker demand from the US could significantly damage Canada's economy.

The Bank of Canada released its Financial Stability Report on Thursday. The BoC said that the financial system was strong but warned that a prolonged trade war between Canada and the US could lead to banks cutting back on lending, which would hurt consumers and businesses and damage the economy. The report said that the unpredictibility of US trade policy could cause further market volatility and was a risk to financial stability.

The Federal Reserve maintained rates earlier this week and Fed Chair Powell said the Fed was in a wait-and-see-stance due to the uncertainty over the US tariffs. We'll hear from seven Fed members on Friday and Saturday, who may provide some insights on where rate policy is headed. The markets have priced in a rate hike in June at only 18%, down sharply from 58% a week ago.

USD/CAD is testing resistance at 1.3928. Above, there is resistance at 1.3935

1.3922 and 1.3915 are the next support levels

New Zealand dollar steady ahead of employment dataThe New Zealand dollar is showing limited movement on Tuesday. In the European session, NZD/USD is trading at 0.5970, up 0.05% on the day. With no key events in New Zealand or the US today, we can expect a quiet day for the New Zealand dollar.

New Zealand releases the employment report for the first quarter on Wednesday. The labor market is showing signs of weakening, with employment change posting two straight declines.

The markets are projecting a slight improvement, with an estimate of 0.1% for Q1.

The unemployment rate has accelerated for seven consecutive quarters and is expected to rise to 5.3% from 5.1% in Q4 2025. This would be the highest level since Q4 2016 and would support the case for the Reserve Bank of New Zealand to lower rates for a sixth straight time at the May 28 meeting. At the April meeting, members warned that the tariffs created downside risks for growth and inflation in New Zealand.

The RBNZ would prefer to continue lowering interest rates in increments of 25-basis points in order to boost the weak economy. Inflation is comfortably within the 1-3% target band but there are upside risks to inflation, especially with global trade tensions escalating due to US tariffs.

In the US, the Federal Reserve is virtually certain to maintain interest rates at 4.25-4.5% on Wednesday. The meeting will be interesting as Fed Chair Powell is expected to push back against pressure from President Trump to lower rates. The Fed is likely to remain on the sidelines until the uncertainty over US tariffs becomes more clear. Trump's zig-zags over tariffs has triggered wild swings in the financial markets, but Trump has said some trade agreements will be announced soon.

NZD/USD is testing support at 0.5968. Below, there is support at 0.5940

There is resistance at 0.5995 and 0.6023

German inflation higher than expected, Euro dipsThe euro is calm on Wednesday. In the North American session, EUR/USD is trading at 1.1334, down 0.45% on the day.

Germany's inflation rate dropped to 2.1% y/y in April, down from 2.2% in March but above the market estimate of 2.0%. This was the lowest level in seven months, largely driven by lower energy prices.

The more significant story was that core CPI, which excludes energy and food and is a more reliable indicator of inflation trends, rose to 2.9% from 2.6%. This will be of concern to policymakers at the European Central Bank, as will the increase in services inflation. The ECB has to balance the new environment of US tariffs and counter-tariffs against the US, which will raise inflation, along with the strong rise in the euro and fiscal stimulus which will boost upward inflationary pressures.

The ECB will be keeping a close look at Friday's eurozone inflation report, which is expected to follow the German numbers. Headline CPI is projected to drop to 2.1% from 2.2%, while the core rate is expected to rise to 2.5% from 2.4%. The central bank would prefer to continue delivering gradual rate cuts in order to boost anemic growth, but this will be contingent on inflation remaining contained.

The markets were braced for soft US numbers but the data was worse than expected. ADP employment change declined to 62 thousand, down from a revised 147 thousand and below the market estimate of 115 thousand.

This was followed by first-estimate GDP for Q1, which declined by 0.3% q/q, down sharply from 2.4% in Q4 and lower than the market estimate of 0.3%. This marked the first quarterly decline in the economy since Q1 2022. The weak GDP reading was driven by a surge in imports ahead of US tariffs taking effect and a drop in consumer spending.

EUR/USD has pushed below support at 1.1362 and is testing support at 1.1338. Below, there is support at 1.1306

There is resistance at 1.1394 and 1.1418

German inflation higher than expected, Euro dipsThe euro is calm on Wednesday. In the North American session, EUR/USD is trading at 1.1334, down 0.45% on the day.

Germany's inflation rate dropped to 2.1% y/y in April, down from 2.2% in March but above the market estimate of 2.0%. This was the lowest level in seven months, largely driven by lower energy prices. The more significant story was that core CPI, which excludes energy and food and is a more reliable indicator of inflation trends, rose to 2.9% from 2.6%. This will be of concern to policymakers at the European Central Bank, as will the increase in services inflation.

The ECB has to balance the new environment of US tariffs and counter-tariffs against the US, which will raise inflation, along with the strong rise in the euro and fiscal stimulus which will boost upward inflationary pressures. The ECB will be keeping a close look at Friday's eurozone inflation report, which is expected to follow the German numbers. Headline CPI is projected to drop to 2.1% from 2.2%, while the core rate is expected to rise to 2.5% from 2.4%.

The central bank would prefer to continue delivering gradual rate cuts in order to boost anemic growth, but this will be contingent on inflation remaining contained.

The markets were braced for soft US numbers but the data was worse than expected. ADP employment change declined to 62 thousand, down from a revised 147 thousand and below the market estimate of 115 thousand.

This was followed by first-estimate GDP for Q1, which declined by 0.3% q/q, down sharply from 2.4% in Q4 and lower than the market estimate of 0.3%. This marked the first quarterly decline in the economy since Q1 2022. The weak GDP reading was driven by a surge in imports ahead of US tariffs taking effect and a drop in consumer spending.

Australian core CPI falls within the RBA target, Aussie shrugsThe Australian dollar has been showing strong movement this week but is calm on Wednesday. In the European session, AUD/USD is trading at 0.6391, up 0.14% on the day.

Australia released the CPI report for the first quarter. The Australian dollar didn't show much reaction, but the data could point to another rate cut from the Reserve Bank of Australia.

Headline CPI remained unchanged at 2.4% y/y, just above the market estimate of 2.3%. The significant news was that RBA Trimmed Mean CPI, the key core inflation indicator, dropped to 2.9% y/y from a revised 3.3% gain in Q4 2024. This is the first time in three years that core CPI is back within the RBA's target band of between 1-3%.

The drop in core inflation is good news for the government, with the national election on Saturday. Australian Treasurer Jim Chalmers jumped on the news, stating that the market expects four or five rate additional rate cuts this year, which would save households with mortgages "hundreds of dollars".

The Reserve Bank is expected to lower rates at its next meeting on May 20, which would mark only the second rate cut this year. After cutting rates in February, the central bank has stayed on the sidelines as US President Trump's tariffs have escalated trade tensions and sent the financial markets on a roller-coaster ride.

In the US, the markets are bracing for some weak data later today. ADP employment is expected to slip to 108 thousand, compared to 155 thousand in the previous release. ADP is not considered a reliable gauge for Friday's nonfarm payrolls, but a weak reading will only increase the anxiety of the nervous markets. US first-estimate GDP for Q1 is expected to slide to just 0.4% q/q, after a 2.4% gain in Q3. If there is a surprise reading from GDP, we could see a strong reaction from the US dollar after the release.

AUD/USD is testing resistance at 0.6403. Above, there is resistance at 0.6431

0.6357 and 0.6329 are the next support levels

Markets eye US, Canada job reports, US dollar steadiesThe Canadian dollar has taken a break after an impressive three-day rally, in which the currency climbed about 2%. In the European session, USD/CAD is trading at 1.4148, up 0.39%. On Thursday, the Canadian dollar touched 140.26, its strongest level since December.

The hottest financial news is understandably the wave of selling in the equity markets, but there are some key economic releases today as well. The US and Canada will both release the March employment report later today.

The US releases nonfarm payrolls, with the markets projecting a gain of 135 thousand, after a gain of 151 thousand in February. This would point to the US labor market cooling at a gradual pace, which suits the Federal Reserve just fine. The Fed will also be keeping a watchful eye on wage growth, which is expected to tick lower to 3.9% y/y from 4.0%. The unemployment rate is expected to hold at 4.1%.

The employment landscape is uncertain, with the DOGE layoffs and newly-announced tariffs expected to dampen wage growth in the coming months. Canada's employment is expected to improve slightly to 12 thousand, after a negligible gain of 1.1 thousand in February. Unemployment has been stubbornly high and is expected to inch up to 6.7% from 6.6%.

US President Donald Trump's tariff bombshell on Wednesday did not impose new tariffs on Canada, but trade tensions continue to escalate between the two allies. Canada said it would mirror the US stance and impose a 25% tariff on all vehicles imported from the US that do not comply with the US-Canada-Mexico-Canada free trade deal. The US has promised to respond to any new tariffs against the US, which could mean a tit-for-tat exchange of tariffs between Canada and the US.

USD/CAD has pushed above resistance at 1.4088 and 141.26. The next resistance line is 1.4170

1.4044 and 1.4006 are the next support levels

Markets eye US, Canada job reports, US dollar steadiesThe Canadian dollar has taken a break after an impressive three-day rally, in which the currency climbed about 2%. In the European session, USD/CAD is trading at 1.4148, up 0.39%. On Thursday, the Canadian dollar touched 140.26, its strongest level since December.

The hottest financial news is understandably the wave of selling in the equity markets, but there are some key economic releases today as well. The US and Canada will both release the March employment report later today.

The US releases nonfarm payrolls, with the markets projecting a gain of 135 thousand, after a gain of 151 thousand in February. This would point to the US labor market cooling at a gradual pace, which suits the Federal Reserve just fine. The Fed will also be keeping a watchful eye on wage growth, which is expected to tick lower to 3.9% y/y from 4.0%. The unemployment rate is expected to hold at 4.1%.

The employment landscape is uncertain, with the DOGE layoffs and newly-announced tariffs expected to dampen wage growth in the coming months.

Canada's employment is expected to improve slightly to 12 thousand, after a negligible gain of 1.1 thousand in February. Unemployment has been stubbornly high and is expected to inch up to 6.7% from 6.6%.

US President Donald Trump's tariff bombshell on Wednesday did not impose new tariffs on Canada, but trade tensions continue to escalate between the two allies. Canada said it would mirror the US stance and impose a 25% tariff on all vehicles imported from the US that do not comply with the US-Canada-Mexico-Canada free trade deal. The US has promised to respond to any new tariffs against the US, which could mean a tit-for-tat exchange of tariffs between Canada and the US.

USD/CAD has pushed above resistance at 1.4088 and 141.26. The next resistance line is 1.4170

1.4044 and 1.4006 are the next support levels

Why the Weak AU Jobs Report Might Not Force the RBA's HandAustralia's employment report for February delivered a surprising set of weak figures. Understandably, markets reacted by pricing in another RBA cut to arrive sooner than later. But if we dig a little deeper, an April or May cut may still not be a given.

Matt Simpson, Market Analyst at City Index and Forex.com

VIX & SXP There is some W on actual lows in VIX , so if it will play out ...It will be next higher low on VIX. It could lead in to higher high. Time will show how markets react on today employment data .I think it was little bit pro inflation with can lead in to stronger DXY situation ...

Does a strong ADP number lead to a decent NFP print? Given the decent ADP report just delivered ahead of Friday's NFP figures, I'm curious to see whether the direction of ADP can be an indicator of what to expect on the headline Nonfarm growth figure. Armed with another spreadsheet, I take a look.

Matt Simpson, Market Analyst at City Index and Forex.com

AUD/USD stabilizes after post-NFP slideThe Australian dollar has started the week quietly. In the North American session, AUD/USD is trading at 0.6151, up 0.07% at the time of writing. Earlier, the Australian dollar fell as low as 0.6130, its lowest level since April 2020.

It was another rough week for the Australian dollar, which declined 1.7% last week. The Aussie can't find its footing and has plunged 10.4% in the past three months.

Strong US nonfarm payrolls sends Aussie tumbling

The week ended with a surprisingly strong US jobs report. In December, the economy added 256 thousand jobs, the most since March 2024. This followed a downwardly revised 212 thousand in November and easily beat the market estimate of 160 thousand. The unemployment rate eased to 4.1%, down from 4.2% in November. Wage growth also ticked lower, from 4% y/y to 3.9% and from 0.4% to 0.3% monthly.

The upshot of the jobs report is that the US labor market remains solid and is cooling slowly. For the Federal Reserve, this means there isn't much pressure to lower interest rates in the next few months. That will suit Fed policy makers just fine as it awaits Donald Trump, who has pledged tariffs against US trading partners and mass deportations of illegal immigrants. Either of those policies could increase inflation and the Fed will try to get a read of the Trump administration before cutting rates again. The latest Fed forecast calls for only two rate cuts in 2025 but that could change, depending on inflation and the strength of the labor market.

The strong employment numbers boosted the US dollar against most of the majors on Friday and the Australian dollar took it on the chin, falling 0.8%, its worst one-day showing in three weeks. With interest rates likely on hold in the near-term and and high tensions in the Middle East, the safe-haven US dollar should remain attractive to investors in the coming months.

AUD/USD tested resistance at 0.6163 earlier. Above, there is resistance at 0.6188

0.6121 and 0.6096 are providing support

XAUUSD - The NFP indicator will determine the direction of gold!Gold is above the EMA200 and EMA50 in the 4-hour timeframe and is in its ascending channel. In case of weakness in the data of the employment market and increase in the unemployment rate, you can look for opportunities to buy gold.

A lower-than-expected unemployment rate release and a strong NFP headline will lead to a breakout of the bullish and bearish channel in gold.

While most major economies are expected to pursue expansionary monetary policies this year, the pace of these measures will likely slow. According to Bloomberg’s forecast, the overall interest rate index in advanced economies is projected to decrease by only 72 basis points in 2025, which is lower than the rate of decline in 2024.

Donald Trump, with his electoral promises and economic policies, has become a source of concern for central banks worldwide.If Trump enforces his threats to impose trade tariffs, these policies could harm economic growth and, in the case of retaliatory measures, drive up consumer prices.

Analysts at Bank of America (BofA) highlighted the “complex” impacts of Trump’s proposed tariffs on metal prices in a recent note. The proposed 25% tariffs on imports from Mexico and Canada—two of the main suppliers of metals to the U.S.—are expected to have both direct and indirect effects on the market.

The bank identified two main concerns. First, the potential negative impact on global growth and the fundamentals of the metals market, particularly if the tariffs escalate into a full-blown trade war. However, BofA predicts that a more “measured approach to trade barriers is likely to prevail,” which would mitigate the overall damage. Second, regional metal prices will need to adjust to the potential tariffs.

Bank of America warned that tariffs could strengthen the dollar, increase inflation, and lead to higher interest rates—all of which could pose challenges for the U.S. economy. Nevertheless, they concluded that metal prices are likely to stabilize after the initial volatility subsides, especially if the tariffs are targeted and investments in energy transition continue.

Jerome Powell, the Federal Reserve Chair, downplayed expectations of continued monetary easing in 2025 during his December 18, 2024, press conference. Cleveland Fed President Loretta Mester’s dissenting vote against a rate cut was surprising, but the major shock to markets came from the Fed members’ projections (dot plot).

The Fed members forecast only two rate cuts for 2025, signaling that the monetary easing cycle, which began in September 2024, will slow significantly in the coming year.

Powell also admitted that inflation forecasts for the end of the year had been overly optimistic, suggesting that inflation is not yet fully under control. The Fed is increasingly concerned about Trump’s policies, as tools like tariffs could raise import prices and, subsequently, inflation.

Forecasts for Friday’s NFP data:

• Average estimate: 165K

• Lowest estimate: 120K

• Highest estimate: 190K

The importance of the labor market for monetary policy has slightly diminished following Powell’s December 18 press conference. This indicates that the Fed has some confidence in easing price pressures stemming from the labor market. However, recent data suggests that the labor market has not fully cooled. The upcoming NFP report is expected to show a 160,000 increase in nonfarm payrolls, while the unemployment rate and hourly wage growth are likely to remain steady at 4.2% and 4%, respectively.

If these expectations are unmet, especially with job growth below 50,000, the likelihood of a Fed rate cut in Q1 2025 will increase. Currently, markets anticipate a 25-basis-point rate cut by June 2025, but this move could occur sooner if labor market data remains weak.

USD/CAD in holding pattern ahead of US, Cdn. jobs dataThe Canadian dollar started the week with strong gains but has shown little movement since then. In the European session, USD/CAD is trading at 1.4411, up 0.12% at the time of writing. We could see stronger movement from the Canadian dollar in the North American session, with the release of Canadian and US employment reports.

Canada's economy may not be in great shape but the labor market remains strong. The economy added an impressive 50.5 thousand jobs in November and is expected to add another 24.9 thousand in December. Still, the unemployment rate has been steadily increasing and is expected to tick up to 6.9% in December from 6.8% a month earlier. A year ago, the unemployment rate stood at 5.8%. This disconnect between increased employment and a rising unemployment rate is due to a rapidly growing labor market which has been boosted by high immigration levels.

Another sign that the labor market is in solid shape is strong wage growth. Average hourly wages have exceeded inflation and this complicates the picture for the Bank of Canada as it charts its rate path for early 2025. The BoC has been aggressive, delivering back-to-back half point interest rate cuts in October and December 2024. Inflation is largely under control as headline CPI dipped to 1.9% in November from 2% in October. However, core inflation is trending around 2.6%, well above the BoC's target of 2%. The central bank is likely to take a more gradual path in its easing, which likely means that upcoming rate cuts will be in increments of 25 basis points. The BoC meets next on Jan. 29.

In the US, all eyes are on today's nonfarm payrolls report. The market estimate stands at 160 thousand for December, compared to 227 thousand in November. The US labor market has been cooling slowly and the Federal Reserve would like that trend to continue as it charts its rate cut path for the coming months. An unexpected reading could have a strong impact on the direction of the US dollar in today's North American session.

USD/CAD is testing resistance at 1.4411. Above, there is resistance at 1.4427

1.4388 and 1.4372 are the next support levels