Can Silver Extend Its Rally Into 2026? - Watch This Week's CloseCan silver extend its rally into 2026? How should investors manage the increase in volatility as silver margins rise?

As long as the US dollar remains in a downtrend, precious metals are likely to continue their bullish trend.

Mirco Silver Futures

Ticker: SIL

Minimum fluctuation:

0.005 per troy ounce = $5.00

Disclaimer:

• What presented here is not a recommendation, please consult your licensed broker.

• Our mission is to create lateral thinking skills for every investor and trader, knowing when to take a calculated risk with market uncertainty and a bolder risk when opportunity arises.

CME Real-time Market Data help identify trading set-ups in real-time and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

Microfutures

FX 2025 RecapThe price action in FX futures throughout 2025 was defined by a historic retreat of the U.S. dollar, which saw its "grip slip" as the U.S. Dollar Index fell by approximately 9% over the year. The primary driver was a dramatic shift in Federal Reserve policy; after holding rates steady for much of the year, the Fed Pivot in September, triggered by a softening labor market and the "One Big Beautiful Bill," resulted in a series of rate cuts that brought the fed funds rate down to 4.25% by December. This dollar weakness provided a massive tailwind for major G10 futures, with the Swedish Krona emerging as the top performer with a 20% gain, while the Euro and Swiss Franc both surged roughly 14% against the greenback in the first half of the year alone.

Volatility reached "monstrous" levels in the second quarter due to the "Liberation Day" tariffs announced on April 2. This event triggered a massive risk-off stampede, causing the Cboe

Volatility Index to witness its largest-ever one-day spike and sending daily global FX turnover to a record $9.6 trillion. While the dollar initially spiked on safe-haven demand, the subsequent "Trump trade" exhaustion and concerns over fiscal sustainability during the longest U.S. government shutdown in history cemented the bearish trend. In contrast, the Japanese Yen futures experienced significant whipsaws as the Bank of Japan diverged from its peers by raising rates to 0.5%, creating a complex environment where traders had to balance narrowing interest rate differentials against the threat of 24% tariffs on Japanese auto exports.

If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs tradingview.com/cme/

*CME Group futures are not suitable for all investors and involve the risk of loss. Copyright © 2023 CME Group Inc.

**All examples in this report are hypothetical interpretations of situations and are used for explanation purposes only. The views in this report reflect solely those of the author and not necessarily those of CME Group or its affiliated institutions. This report and the information herein should not be considered investment advice or the results of actual market experience.

Options Blueprint Series [Advanced]: Structuring Long VolatilityWhy Long Volatility Matters in Euro FX Right Now

Euro FX futures offer a clean and highly liquid way to observe how macro forces, relative growth expectations, and monetary policy differentials express themselves through price. While directional narratives often dominate discussion, options markets frequently reveal a different story — one centered on volatility pricing rather than directional certainty.

This Options Blueprint focuses on Euro FX futures (6E) and Micro EUR/USD futures (M6E) during a period when implied volatility is historically compressed, while price structure suggests an elevated probability of expansion. The purpose of this case study is not to anticipate direction, but to explore how options structures can be engineered to respond to range resolution risk when price compression and technical conflict coexist.

This article is strictly educational and illustrative, designed to demonstrate principles of volatility analysis, options structure design, and risk management.

Volatility Context: Reading Implied Volatility with CVOL

Implied volatility reflects the market’s collective expectation of future price variability. When implied volatility is elevated, options tend to price in larger potential moves. When it is compressed, options reflect an assumption of relative calm.

In this case, the CVOL index for Euro FX futures is observed at relatively low levels compared to its behavior earlier in the year. While CVOL is not predictive, it provides valuable context: the market is currently assigning a lower probability to large price swings than it has at other times.

Periods of compressed implied volatility are noteworthy because price expansion often follows periods of contraction, particularly when price structure begins to show signs of instability. This does not guarantee movement, but it shifts the analytical focus toward strategies that can benefit from expansion rather than stagnation.

Technical Landscape: A Market at an Inflection Point

From a structural perspective, Euro FX futures present a rare but important configuration: conflicting continuation and reversal patterns.

A bullish flag has developed following an impulsive advance, suggesting the potential for trend continuation.

Simultaneously, a double top formation has emerged, introducing the possibility of a downside resolution.

When viewed in isolation, each pattern offers a directional narrative. When viewed together, they create directional ambiguity but expansion risk clarity. In other words, the market may not be signaling where it intends to go — but it is signaling that remaining stagnant may be increasingly difficult.

This type of structural conflict is often where volatility-focused strategies become more relevant than directional trades.

Mapping Price Targets to Market Structure

Technical patterns are most useful when they provide reference points, not predictions. In this case, both patterns generate projected levels that act as structural guideposts.

The bullish flag projects an upside objective near 1.2116, which also aligns with a clearly defined UFO resistance zone.

The double top projects a downside objective near 1.1618, aligning with a well-defined UFO support zone.

These levels form a structural range boundary. Price acceptance beyond either boundary would represent meaningful resolution of the current compression phase. For options traders, these projected zones are valuable because they provide logical strike selection reference points when designing volatility structures.

Strategy Foundation: The Role of a Long Straddle

A traditional long straddle involves purchasing both a call and a put at the same strike, typically near the current price. This structure is directionally neutral and benefits from large price movements in either direction.

The strength of a long straddle lies in its convexity. Its primary weakness lies in time decay, particularly when implied volatility is low and price remains range-bound.

In compressed volatility environments, a pure long straddle can be inefficient if price takes time to resolve. This is where structure refinement becomes essential.

Strategy Evolution: Structuring an Asymmetric Long Volatility Approach

Instead of relying on a textbook long straddle, this Options Blueprint explores an asymmetric volatility structure designed to reflect the underlying technical landscape.

The structure begins with a long at-the-money straddle, capturing core volatility exposure:

Long 1.175 Call

Long 1.175 Put

To refine the payoff and reduce exposure to time decay, options are sold at technically

meaningful projected targets:

Short 1.21 Call

Short 1.16 Put

This transforms the strategy into a defined-risk, asymmetric volatility structure.

Key educational concepts illustrated by this construction:

The long options capture expansion risk near the current price.

The short options align with projected structural boundaries.

The payoff becomes skewed, favoring upside expansion while still allowing for limited downside participation.

Theta exposure is reduced compared to a pure long straddle.

The goal is not optimization, but intentional payoff shaping based on structure.

Risk Profile Analysis: Understanding the Payoff Diagram

The resulting risk profile highlights several important principles.

Maximum risk occurs if price remains trapped between the short strikes into expiration.

Upside expansion toward the upper projected level produces the most favorable outcome.

Downside expansion produces a smaller, but still positive, outcome.

Both risk and reward are defined, removing uncertainty around extreme scenarios.

This structure favors movement over stagnation, reflecting the belief that expansion risk outweighs the likelihood of prolonged consolidation — without requiring directional conviction.

Contract Specifications

Euro FX futures are available in both standard and micro formats.

o 6E (Euro FX Futures)

Larger notional exposure

Suitable for accounts with higher margin tolerance

o M6E (Micro EUR/USD Futures)

One-tenth the size of the standard contract

Greater flexibility for position sizing

Often useful for testing or scaling strategies

Both contracts reference the same underlying market structure, allowing the same analytical framework to be applied across different risk profiles.

Margin requirements vary and are subject to change, making position sizing and risk definition essential considerations when selecting between standard and micro contracts.

Euro FX futures (6E) have a tick size of 0.000050 per Euro increment = $6.25 tick value and currently require roughly ~$2,700 in margin per contract, while Micro EUR/USD Futures (M6E) use a 0.0001 tick size per euro = $1.25 tick value and margin closer to ~$270.

Risk Management Considerations

Options strategies are not defined solely by payoff diagrams — they are defined by how risk is managed over time.

Key considerations include:

Sizing positions so that the maximum loss is acceptable within the broader portfolio context.

Understanding how time decay accelerates as expiration approaches.

Recognizing that volatility expansion does not occur on a fixed schedule.

Accepting predefined loss zones as part of the structure rather than reacting emotionally.

Risk management is not about avoiding losses; it is about controlling exposure to uncertainty.

Key Takeaways from This Options Blueprint

Implied volatility provides context, not direction.

Conflicting chart patterns often increase expansion risk.

Options structures can be shaped to reflect technical asymmetry.

Modifying classic strategies can improve alignment with market conditions.

Defined risk and intentional design matter more than prediction.

This case study demonstrates how volatility, structure, and risk management intersect — without requiring directional forecasts.

Data Consideration

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

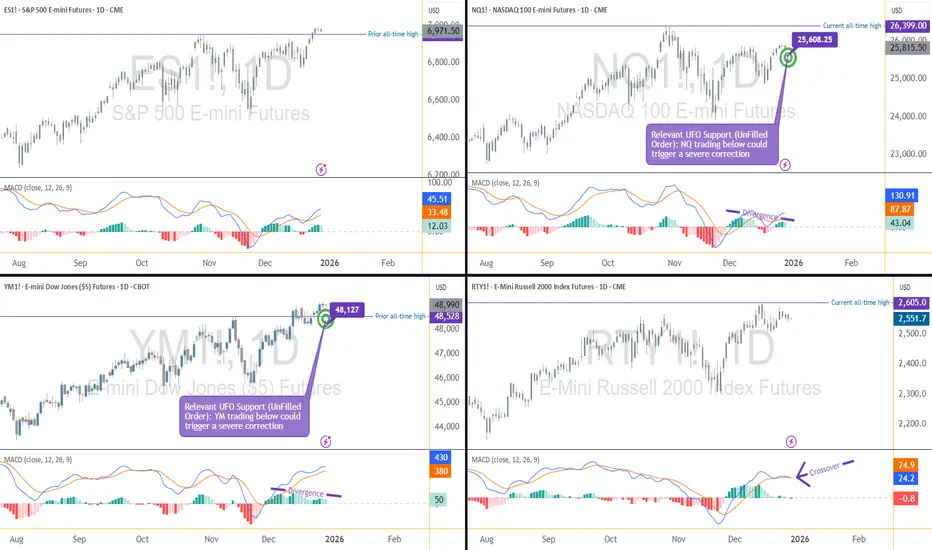

When Indexes Stop Agreeing, Markets Start TalkingEver notice how markets can look strong… yet feel a little off?

That’s usually when indexes stop marching in sync — and right now, that’s exactly what’s happening.

Let’s break it down, no jargon overload, no crystal balls.

Four Indexes, Four Different Stories

Here’s the current lineup in US equity index futures:

S&P 500 (ES) → Pushing to fresh all-time highs

Dow Jones (YM) → Also holding above prior highs

NASDAQ 100 (NQ) → Lagging below its peak

Russell 2000 (RTY) → Still stuck under its highs

When all four move together, trends tend to behave.

When they don’t? Markets usually get… interesting.

Why This Disagreement Matters

The NASDAQ is packed with technology and AI-related names — the same group that carried much of the upside through 2025. Its failure to confirm new highs raises an eyebrow.

Meanwhile:

The Dow (YM) is strong, despite being less tech-heavy

Small caps (RTY) aren’t joining the party

Leadership is narrowing, not expanding

That’s not a signal by itself — but it is a clue.

Momentum Is Whispering (Not Shouting)

Momentum indicators aren’t screaming danger, but they are quietly tapping the mic:

NASDAQ shows a bearish divergence

Dow also shows a bearish divergence (yes, even while strong)

Russell goes a step further with a divergence and a momentum crossover

The S&P 500? Still holding up — but increasingly alone.

When momentum fades while price stays elevated, markets often shift from trending to fragile.

The Levels That Actually Matter

Here’s where structure comes in.

Two UFO (UnFilled Orders) support zones sit right below price:

NASDAQ (NQ): ~25,608

Dow (YM): ~48,127

Above these levels, structure is intact.

Below them? That’s when momentum warnings could start turning into price action.

Think of these zones as market tripwires — nothing happens until they’re crossed.

Condition-Based Thinking (No Guessing Required)

Instead of asking “Will the market drop?”, a better question is:

What would need to happen for risk to expand?

A simple framework:

NQ below support + YM below support

Weakest and strongest indexes failing together

Divergences resolving through price, not time

That’s when downside scenarios become more relevant — not before.

Quick Note on Contract Specs & Margin

All four index futures discussed are available in E-mini and Micro E-mini versions, moving tick-for-tick with the same underlying index.

At a glance:

Micro contracts = 1/10 the tick value of E-minis

Typical tick values:

ES / MES: $12.50 vs. $1.25

NQ / MNQ: $5.00 vs. $0.50

YM / MYM: $5.00 vs. $0.50

RTY / M2K: $5.00 vs. $0.50

Margin context (approximate):

ES / MES: $22,500 vs. $2,250

NQ / MNQ: $33,500 vs. $3,350

YM / MYM: $14,250 vs. $1,425

RTY / M2K: $9,500 vs. $950

Same market, same analysis — just different risk granularity. This becomes especially useful when markets are hovering near key structural levels.

The Big Takeaway

Markets don’t usually turn when everyone expects them to.

They turn when participation fades, leadership narrows, and structure starts cracking.

Right now:

Some indexes are strong

Others are lagging

Momentum is diverging

Key levels are close

No conclusions. No assumptions.

Just evidence — and levels worth paying attention to as 2026 approaches.

Want More Depth?

If you’d like to go deeper into the building blocks of trading, check out our From Mystery to Mastery trilogy, three cornerstone articles that complement this one:

🔗 From Mystery to Mastery: Trading Essentials

🔗 From Mystery to Mastery: Futures Explained

🔗 From Mystery to Mastery: Options Explained

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

When Indexes Disagree: Evidence-Based Clues Heading Into 2026Market Context: Why Futures-Based Index Analysis Matters

When equity markets approach historical extremes, surface-level price action often hides important structural information. This is especially true when analyzing cash indices alone. Futures markets, by contrast, provide continuous pricing across all trading sessions, including the Globex (Extended Trading Hours) session, offering a more complete picture of participation, liquidity, and risk transfer.

By focusing on US equity index futures rather than cash indices, traders gain visibility into how markets behave outside regular trading hours — often where meaningful positioning occurs. This becomes particularly important when markets are near all-time highs and internal alignment begins to fracture.

In this analysis, attention is placed on the four most relevant US equity index futures:

E-mini S&P 500 Index Futures (ES)

E-mini NASDAQ 100 Index Futures (NQ)

E-mini Dow Jones Index Futures (YM)

E-mini Russell 2000 Index Futures (RTY)

Together, these markets represent large-cap growth, broad market exposure, industrial and value-oriented components, and small-cap participation. When these indexes move in harmony, trends tend to persist. When they diverge, conditions often become more fragile.

All-Time Highs in Focus: Who Is Leading and Who Is Lagging

A defining characteristic of the current environment is disagreement among indexes, despite elevated price levels.

The E-mini S&P 500 Index Futures (ES) has recently pushed to a new all-time high. This reflects ongoing strength in the broader market and confirms that headline risk appetite remains intact.

In contrast, the E-mini NASDAQ 100 Index Futures (NQ) has failed to confirm this strength. Despite previous leadership, NQ is currently trading below its all-time high. This matters because the NASDAQ is heavily weighted toward technology and growth-related stocks, including those linked to artificial intelligence (AI) — sectors that provided a significant portion of upside momentum throughout 2025.

Meanwhile, the E-mini Dow Jones Index Futures (YM) is trading above its prior all-time high. This is notable because the Dow has a more diversified sector composition and is less concentrated in high-growth technology names. Its relative strength suggests that current market resilience may be coming from areas outside of the technology complex.

Finally, the E-mini Russell 2000 Index Futures (RTY) remains below its all-time high. Small- and mid-cap stocks often act as a confirmation layer for broader economic participation. When large-cap indexes make new highs while small caps lag, it can signal uneven economic traction and rising internal imbalance.

This combination — ES and YM showing strength, while NQ and RTY lag — forms the foundation of the current intermarket tension.

Momentum Evidence: What MACD Is Revealing Across Indexes

Price alone rarely tells the full story near extremes. Momentum indicators, when used correctly, help evaluate the quality of participation behind price movement.

In this case, the MACD indicator reveals important divergences across multiple indexes.

The NQ is displaying a bearish momentum divergence, where price remains elevated but momentum fails to confirm. This suggests that upside participation is narrowing rather than expanding.

The YM — despite being one of the strongest indexes — is also showing a bearish divergence on MACD. This is particularly important because divergences forming in strong markets often precede broader shifts, not because price must reverse immediately, but because momentum strength is no longer accelerating.

The RTY presents the most advanced signal set. It is not only showing a bearish divergence, but also a MACD crossover, which can be interpreted as early-stage downside momentum attempting to assert itself.

The ES, while not currently exhibiting the same degree of momentum weakness, stands increasingly isolated. When leadership narrows to one index, risk becomes asymmetric rather than evenly distributed.

Structural Risk Zones: Interpreting UFO (UnFilled Orders) Support

Momentum divergences alone do not constitute actionable signals. They require structural confirmation.

This is where UFO support and resistance levels (UnFilled Orders) become relevant. UFO zones represent areas where liquidity previously failed to transact fully, often acting as structural support or resistance when revisited.

In the current structure, two UFO support zones stand out due to their proximity to price and their relevance to both the strongest and weakest markets:

NQ: UFO support ending near 25,608.25

YM: UFO support ending near 48,127

These levels are significant because they sit directly beneath current price action. As long as price remains above these zones, structure remains intact despite momentum warnings.

However, a violation of such UFO supports would represent a meaningful shift. It would indicate that buyers previously willing to defend these levels are no longer present, allowing momentum divergences to express themselves more fully.

Conditional Scenarios: What Would Confirm a Broader Risk Shift

Rather than anticipating outcomes, evidence-based analysis focuses on conditions.

From a structural standpoint, bearish scenarios would gain credibility if:

NQ trades below 25,608.25, violating its nearby UFO support

YM trades below 48,127, removing structural support from the strongest index

Weakness emerging simultaneously in both the weakest and strongest indexes would suggest that divergence is resolving through price rather than consolidation. In such a case, broader downside expansion could develop, potentially manifesting as a sharp corrective phase.

Importantly, this framework does not assume that such a move must occur. It simply defines what conditions would matter if they do.

Illustrative Trade Framework (Educational Example Only)

For traders studying downside scenarios, a hypothetical bearish framework could be structured as follows:

Trigger: Confirmed daily close below relevant UFO support

Risk Definition: Invalidation above reclaimed structure

Objective: Next lower structural liquidity zone

Reward-to-Risk: Favorable only if structure breaks decisively

This framework is illustrative and intended solely to demonstrate how structure, momentum, and confirmation can align. It does not imply expectations or outcomes.

E-mini vs. Micro E-mini Contracts

All four equity index futures discussed — ES, NQ, YM, and RTY — are available in both E-mini and Micro E-mini formats. Both versions track the same underlying index and move tick-for-tick together. The difference lies in how risk is expressed.

ES / MES Tick size: 0.25 index points = $12.50 (ES) | $1.25 (MES)

NQ / MNQ Tick size: 0.25 index points = $5.00 (NQ) | $0.50 (MNQ)

YM / MYM Tick size: 1 index point = $5.00 (YM) | $0.50 (MYM)

RTY / M2K Tick size: 0.10 index points = $5.00 (RTY) | $0.50 (M2K)

Across all four indexes, Micro E-mini contracts represent one-tenth of the tick value of their E-mini counterparts.

Margin requirements vary by broker and market conditions. From a structural perspective:

ES / MES required margin = ~$22,500 (ES) | ~$2,250 (MES)

NQ / MNQ required margin = ~$33,500 (NQ) | ~$3,350 (MNQ)

YM / MYM required margin = ~$14,250 (YM) | ~$1,425 (MYM)

RTY / M2K required margin = ~$9,500 (RTY) | ~$950 (M2K)

This difference allows traders to express the same market thesis with far greater precision, especially when working around tight structural levels or conditional triggers.

With momentum divergences developing and key structural zones nearby, position sizing flexibility becomes critical. Micro E-mini contracts make it possible to:

Scale exposure gradually

Reduce concentration risk

Align risk more closely with invalidation levels

The analysis remains identical across E-minis and Micros — only the risk calibration changes.

Risk Management Considerations

Divergences can persist longer than expected, especially in strong trends. Acting without confirmation often leads to premature positioning.

Key principles include:

Waiting for structural validation

Defining risk before engaging

Managing exposure across correlated instruments

Avoiding overconfidence near historical extremes

Markets rarely turn because of opinion. They turn when structure and participation change.

Final Takeaway: Evidence Over Assumptions

As 2025 comes to a close, US equity index futures present a market that is strong on the surface but fractured underneath. Leadership is narrowing, momentum is diverging, and structural levels are increasingly relevant.

Whether these signals resolve through consolidation or correction remains unknown. What matters is that the evidence is now visible — and futures markets provide the clarity needed to observe it.

Data Consideration

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Forget the Textbook: A 30-Year Reality CheckA Big Policy Moment

A central bank (BOJ) just pushed interest rates to levels not seen in 30 years.

That’s not a routine tweak — that’s a regime shift.

Textbooks might suggest a clean, logical market response.

Reality? Markets got emotional. Fast.

Selling Got Loud

Instead of an orderly adjustment, selling pressure exploded.

Not just “price going down,” but effort going through the roof.

That’s where Volume Delta comes in — the net difference between buying and selling volume. It tells us who is pressing the gas pedal.

And in this case, sellers floored it.

When an Indicator Starts Yelling

Now here’s the interesting part.

Bollinger Bands weren’t applied to price…

They were applied to Volume Delta itself.

Result?

Volume Delta plunged far below its lower Bollinger Band.

That’s not normal selling.

That’s everyone trying to get out at the same time.

Does that mean price must reverse?

Nope. But it does suggest selling is becoming inefficient.

No Safety Net Below

Here’s the catch.

There are no meaningful UFO supports (UnFilled Orders) below current price.

No obvious institutional “safety net.”

Instead, only two old technical floors remain:

0.0063330

0.0062415

Think of them as floors, not trampolines. Price may react… or punch straight through.

Reaction Beats Guessing

This is where patience matters.

Extreme selling doesn’t mean “buy now.”

It means watch closely.

At those levels, traders are looking for:

Selling pressure slowing down

Price stabilizing

Daily closes showing acceptance or rejection

No assumptions. Only reactions.

Don’t Forget the Ceiling

Even if price bounces, there’s a ceiling waiting above.

A clear sell-side UFO resistance sits near 0.0065640.

That’s leftover supply — the kind that often stops rallies in their tracks.

So any upside move?

Treat it as corrective until structure says otherwise.

Contract Specs

This analysis uses both standard and micro futures to illustrate scalable risk. Japanese Yen Futures (6J) have a tick size of 0.0000005 with a $6.25 tick value and currently require roughly ~$2,800 in margin per contract, while Micro JPY/USD Futures (MJY) use a 0.000001 tick size with a $1.25 tick value and margin closer to ~$280. Margin requirements vary by market conditions and broker policies, and micro contracts can be especially useful when volatility expands following major macro events.

The Big Takeaway

Historic policy decisions don’t end stories — they start messy chapters.

Extreme Volume Delta shows stress, not certainty.

Structure decides what comes next.

When markets digest big shocks, the edge doesn’t come from predicting —

It comes from staying disciplined while everyone else reacts.

Want More Depth?

If you’d like to go deeper into the building blocks of trading, check out our From Mystery to Mastery trilogy, three cornerstone articles that complement this one:

🔗 From Mystery to Mastery: Trading Essentials

🔗 From Mystery to Mastery: Futures Explained

🔗 From Mystery to Mastery: Options Explained

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

3-Decade Rate Milestone: How Markets Digest Policy ShocksA Central Bank Decision Decades in the Making

When a central bank moves interest rates to levels not seen in three decades, markets rarely respond in a linear or orderly fashion. Such decisions are not interpreted as isolated adjustments, but as structural signals that force participants to reassess positioning, risk, and longer-term assumptions.

The recent interest rate increase by the Bank of Japan marked exactly that kind of milestone. Beyond the numerical change itself, the decision carried symbolic weight: a clear departure from an era defined by extraordinary accommodation. Yet, rather than triggering a straightforward repricing, the immediate market response leaned heavily toward aggressive selling pressure in the Japanese Yen.

This disconnect between policy intent and market reaction highlights an important reality: markets do not simply react to decisions — they digest them. And digestion is often messy.

From Policy Shock to Positioning Shock

Major policy announcements tend to unfold in two phases. The first phase is informational, where the headline is absorbed. The second phase is positional, where traders and institutions adjust exposure based on how that information interacts with existing risk.

In this case, the rate hike represented a known risk event, but its implications were far from binary. Messaging around future policy paths, real-rate dynamics, and external yield differentials all contributed to uncertainty. That uncertainty translated into heavy participation on the sell side, not because the outcome was definitively bearish, but because positioning needed to be reset.

This is where flow-based tools become especially valuable. Price alone often obscures what is really happening beneath the surface.

Flow Exhaustion as an Analytical Framework

Flow exhaustion is not about calling tops or bottoms. It is about identifying moments when participation becomes unusually one-sided, increasing the probability that continuation becomes harder to sustain.

One easy way to observe this phenomenon is through Volume Delta, defined as the net difference between buying volume and selling volume over a given period. Volume Delta provides insight into how aggressively one side of the market is pressing its case.

Unlike traditional price-based indicators, Volume Delta focuses on effort rather than outcome. Price can move modestly while effort is extreme — and it is often in those situations where future responses become most interesting.

Bollinger Bands® on Volume Delta, Not Price

In this framework, Bollinger Bands® are applied not to price, but to Volume Delta itself. This distinction is critical.

Bollinger Bands® on price measure volatility relative to price behavior. Bollinger Bands® on Volume Delta measure participation extremes relative to historical flow behavior. When Volume Delta trades far beyond its lower band, it signals that selling pressure is not just dominant, but statistically stretched.

On the daily chart, Volume Delta recently moved well below its lower Bollinger Band®. This represents an exaggerated imbalance, suggesting that sellers were acting with urgency and intensity rarely sustained over extended periods.

Importantly, this does not imply that price must reverse. It simply indicates that the marginal impact of additional sellers may be diminishing.

What Extreme Selling Really Means

Extreme selling does not mean that buyers suddenly appear in force. It means that the market has already absorbed a significant amount of sell-side participation.

In practical terms, when Volume Delta reaches such depressed levels, one of two things tends to occur:

Selling slows, leading to consolidation or corrective movement.

Price seeks lower levels where new participants are willing to engage.

Which outcome unfolds depends heavily on structure — specifically, what lies beneath price.

The Support Landscape Below Price

A critical observation in the current structure is the absence of UFO support levels (UnFilled Orders) beneath current price levels. UFO supports represent areas where prior institutional participation was not fully satisfied, often acting as structural reference points.

Without meaningful UFOs below, the market cannot rely on obvious liquidity-backed demand. Instead, attention shifts to historical technical supports derived from prior pivot lows.

Two such levels stand out:

0.0063330

0.0062415

These levels represent areas where price previously found acceptance.

Reaction Zones, Not Assumptions

At this stage, the distinction between anticipation and reaction becomes essential. Extreme Volume Delta does not justify preemptive positioning. Instead, it highlights zones where observation becomes critical.

At each technical support, traders may evaluate:

Whether selling pressure visibly decelerates

Whether price stabilizes despite continued effort

Whether daily closes show acceptance or rejection

The first support may hold. It may also fail. The absence of structural UFO support means the market retains flexibility, and traders must adapt accordingly.

Overhead Structure: Supply Still Matters

While attention often gravitates toward potential downside exhaustion, it is equally important to recognize what exists above price.

A relevant sell-side UFO resistance is located near 0.0065640. This zone represents UnFilled Sell orders and remains structurally intact.

Should price respond positively from lower levels, this area becomes a natural reference point where supply could reassert itself. In downtrending environments, rebounds frequently encounter resistance before any broader shift occurs.

This reinforces the importance of framing any upside move as corrective unless proven otherwise by structure.

Hypothetical Trade Framework (Illustrative Case Study)

To translate these observations into a practical framework, consider a purely illustrative example.

A hypothetical long-side case study could involve:

Monitoring price behavior at either technical support level

Waiting for evidence of stabilization or responsive buying

Using the support zone as a contextual risk reference

Defining invalidation below the chosen support

Referencing the overhead UFO resistance as a potential objective (target)

The reward-to-risk profile in such a framework depends entirely on execution and confirmation. This example is presented solely to demonstrate how flow exhaustion and structure may be combined.

Contract Specifications

This analysis references both standard and micro futures contracts to illustrate scalability and risk calibration.

Japanese Yen Futures (6J):

Tick size: 0.0000005

Tick value: $6.25

Currently ~$2,800 per contract

Micro JPY/USD Futures (MJY):

Tick size: 0.000001

Tick value: $1.25

Currently ~$280 per contract

Margin requirements vary by market conditions and broker policies. Micro contracts can be particularly useful in environments where volatility expands following macro events.

Risk Management Considerations

Policy-driven markets tend to remain unstable longer than expected. Even when selling pressure appears exhausted, uncertainty persists.

Key risk management principles include:

Defining risk before engagement

Adjusting size to reflect volatility

Avoiding emotional responses to extreme indicators

Accepting that not all exhaustion leads to reversals

Structure, not conviction, should guide decision-making.

How Markets Digest Policy Shocks

Major policy milestones do not resolve narratives — they reshape them. Flow extremes reveal stress points in positioning, not certainty in direction.

In the aftermath of a 3-decade rate milestone, the market enters a digestion phase. Volume Delta extremes suggest that selling pressure has been intense, but structure determines how that pressure resolves.

Patience, observation, and disciplined reaction remain the most reliable tools when markets recalibrate after historic decisions.

Data Consideration

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

How I Spot Trading Opportunity – Part IILast week, we discussed how to spot trading opportunities using multiple asset classes. I also created multiple tabs for each asset class, such as currencies, commodities, and indices. Within each asset class, there are multiple products.

The whole idea is this: if you already have a trading methodology that is working well for you in a particular asset, say gold or silver, and you have been trading it for a long time, why not apply the same trading methodology across other markets?

It is not too difficult to pick up trading ideas fairly quickly from the market at any point in time. And I am going to share with you how I do that.

Micro E-mini Nasdaq Futures & Options

Ticker: MNQ

Minimum fluctuation:

0.25 index points = $0.50

Disclaimer:

• What presented here is not a recommendation, please consult your licensed broker.

• Our mission is to create lateral thinking skills for every investor and trader, knowing when to take a calculated risk with market uncertainty and a bolder risk when opportunity arises.

CME Real-time Market Data help identify trading set-ups in real-time and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

When Price Gets Ahead of ItselfMarkets love drama.

Price breaks out, momentum accelerates, and suddenly everything feels obvious. Charts look clean, conviction is high, and everyone agrees — this thing is strong.

But here’s the catch: strong doesn’t always mean sustainable.

When price moves too far too fast, it stretches liquidity, pulls in late participants, and often leaves structure behind. That’s when volatility expands, Bollinger Bands® get left in the dust, and the market quietly becomes fragile.

This is where mean reversion sneaks into the conversation — not as a call for collapse, but as a reminder that markets like balance. Extremes attract attention, and attention attracts counter-flow.

Add in order-flow context — like UnFilled Orders (UFOs) lining up near pattern objectives — and suddenly those “obvious” moves don’t look quite as comfortable anymore.

Mean reversion trades aren’t about being right.

They’re about managing risk when price runs ahead of itself.

Because in trading, the real edge isn’t momentum.

It’s knowing when momentum starts to wobble.

Know your specs…

Standard Futures Contract (6E)

Minimum price fluctuation (tick): 0.000050 per Euro increment = $6.25

Typical margin characteristics: ~$2,700 per contract

Micro Futures Contract (M6E)

Minimum price fluctuation (tick): 0.0001 per euro = $1.25

Typical margin characteristics: ~$270 per contract

Want More Depth?

If you’d like to go deeper into the building blocks of trading, check out our From Mystery to Mastery trilogy, three cornerstone articles that complement this one:

🔗 From Mystery to Mastery: Trading Essentials

🔗 From Mystery to Mastery: Futures Explained

🔗 From Mystery to Mastery: Options Explained

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

The Aussie on the brink: annual highs under siegeFollowing the bullish impulse initiated at the end of November, the Aussie is now challenging its annual highs. With the latest monetary policy decisions largely digested and implied volatility declining, the market is refocusing on microstructure and flows.

Fundamental Analysis

The RBA’s latest hold, the third in a row, confirmed a “hawkish hold” bias that continues to support the Australian dollar. The central bank acknowledges that inflation is proving broader than initially expected and remains alert to second-round risks, keeping real rate expectations elevated for Australia. The RBA Rate Tracker, which measures the implied probability of a rate change, is also starting to price in a moderate chance of a hike in 2026.

On the US side, while the official message remains cautious, the market has mainly noted the inability of US yields to re-establish a sustained upward trend. This is compounded by a well-established seasonal factor, as December has historically been a period of USD underperformance, driven by hedging flows and profit repatriation.

The broader global backdrop is also supportive for the AUD given its strong correlation with commodities, with copper and gold trading at historically high levels.

Technical Analysis

From a technical standpoint, the daily chart of 6AH6 shows a clear structure of higher lows and higher highs since the November trough. Prices are trading above key moving averages, notably the 55-day average, which is acting as dynamic support. The current consolidation is taking place above former value areas, a typical feature of a market accepting higher prices rather than one in distribution.

Volume analysis provides additional insight. Upward phases have been accompanied by rising volumes, while recent pullbacks have occurred on more moderate volume. This suggests an absence of aggressive selling pressure. The visible volume profile on the chart shows a high concentration of trading activity around 0.6550–0.6600, corresponding to a former equilibrium now located below the market. Since the bullish recovery, price has moved into a low-volume area above, indicating that the market is exploring levels with limited historical trading.

The current zone around 0.6650–0.6670 appears more like a pause than a definitive resistance. As long as price remains above the core of the volume profile, probabilities favor continuation or, at a minimum, a high-level consolidation.

Sentiment Analysis

Retail sentiment on spot AUD/USD is particularly skewed, with retail traders heavily net short. Some platforms even show ratios exceeding 80% or 90% short positions. This configuration is typical of market phases where retail participants attempt to anticipate a top based on psychological levels or visible resistance, without waiting for a confirmed reversal signal.

From a contrarian perspective, this positioning represents potential fuel for further upside. It indicates that the market is not overloaded with fragile speculative longs, but instead crowded with sellers who may be forced to cover if key levels are broken.

On the institutional side, no major desks appear to be arguing for an immediate, structural bearish reversal in AUD/USD.

Options Analysis

In the options space, calls are more in demand and more expensive, confirming a dominant short-term bullish bias and a market that is primarily expecting extension.

The options heatmap also shows large clusters of call options at the 0.6700 and 0.6750 strikes. In the event of an approach to or break above these levels, call sellers could find themselves short gamma and forced to hedge via futures buying, thereby amplifying the bullish move.

Trade Idea (6AH6)

With a lighter news calendar and market liquidity gradually declining, there is limited likelihood of sufficient catalysts to reverse the trend before year-end. In this context, a directional bullish strategy remains the most coherent, at least over the next two weeks.

Entry zone: on pullbacks toward 0.6620–0.6630

Stop loss: below the 55-day average, currently around 0.6540

Primary target: 0.6750

Extended target: 0.6850 in the event of an options-driven squeeze

Final Thoughts

Even though the AUD has shown some hesitation over the past few sessions, signals continue to converge toward an intact bullish potential. Fundamentals are supportive, technical analysis points to acceptance of higher prices, retail sentiment is heavily contrarian, and options positioning highlights the risk of a squeeze above well-identified levels.

In this type of environment, the market’s ability to force weak hands out should not be underestimated, particularly during periods of lower liquidity. As long as the structure remains intact, a bullish extension beyond the annual highs remains the most coherent scenario into year-end, ahead of a likely consolidation phase in early 2026.

---

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: tradingview.com/cme/ .

This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

The Anatomy of an Overextended Market MoveMarket Context: When Momentum Accelerates

Markets periodically enter phases where price accelerates rapidly, often driven by a combination of macro catalysts, positioning imbalances, and behavioral feedback loops. In such environments, momentum can appear self-reinforcing: higher prices attract more participation, which in turn pushes prices even higher. While these phases can feel decisive and convincing, they also introduce an important analytical question — is the move being accepted by the market, or is it simply expanding faster than structure can support?

This distinction matters because strong momentum does not automatically imply durability. In fact, the most aggressive moves often carry the seeds of their own instability, particularly when price begins to disconnect from commonly observed reference points such as volatility envelopes, prior value zones, and resting order clusters.

The recent advance examined in this case study provides a clear example of this dynamic: a structurally bullish resolution followed by a sharp acceleration that raises legitimate questions about sustainability.

Pattern Resolution Versus Move Sustainability

Classical chart patterns are useful because they describe how markets transition from balance to imbalance. A double bottom, for example, reflects a failed attempt by sellers to extend lower prices, followed by renewed demand. Once the neckline is cleared, the pattern is considered resolved.

However, pattern resolution only explains directional bias — it does not guarantee how price will behave after the breakout.

In practice, many pattern completions coincide with:

Early participants reducing exposure

Profit-taking activity near projected objectives

New positioning that is more sensitive to short-term adverse movement

As a result, the completion of a pattern can sometimes mark the end of a clean directional phase rather than the beginning of an extended one. This is especially relevant when the breakout is followed by aggressive price expansion rather than gradual acceptance.

Volatility Expansion and the Bollinger Band Framework

Bollinger Bands® are commonly misunderstood as directional indicators. In reality, they function as volatility envelopes, providing context for how far price has deviated from its recent mean.

When price trades:

Outside the upper band

After a gap higher

And remains extended for multiple sessions

it signals volatility expansion, not necessarily trend continuation.

From a statistical perspective, such conditions indicate that price has moved beyond its recent distribution range. From a behavioral perspective, they often reflect:

Late participation

Emotional decision-making

Reduced liquidity on one side of the market

None of these imply that price must reverse immediately. What they do imply is that the informational risk of continuation increases, while the probability of mean reversion back toward equilibrium also rises.

Mean Reversion as a Structural Tendency

Mean reversion is not a prediction tool. It is a structural tendency observed across liquid markets, driven by the constant interaction between:

Value discovery

Liquidity provision

Inventory management by participants

When price moves “too far, too fast,” it stretches these mechanisms. Liquidity providers become more selective, directional participants begin to manage exposure, and resting orders closer to the mean regain relevance.

Importantly, mean reversion does not require a bearish narrative. It simply reflects the market’s natural inclination to revisit areas where participation was previously deeper and more balanced.

In this context, mean reversion should be viewed as a risk consideration, not a directional conviction.

Order-Flow Structure

A key element of this case study is the alignment between classical technical projections and observable order-flow structure, described here through the lens of UnFilled Orders (UFOs).

UFOs represent areas where prior activity suggests the presence of resting interest that has not yet been fully executed. These zones often coincide with:

Prior consolidations

Structural inflection points

Pattern-derived objectives

In the current structure:

o An upper zone near 1.18350 aligns with:

The projected objective of the resolved pattern

UFO resistance

Likely areas of trade closure and sell on-field activity

o A lower zone near 1.16875 aligns with:

UFO support

Areas where price previously attracted participation

A logical mean reversion destination

The importance of these zones lies not in their precision, but in their confluence. When multiple frameworks point to the same areas, they tend to attract attention from a broader range of participants.

Why Overextended Moves Become Fragile

Overextended markets often appear strongest right before they become most sensitive. This is because:

Positioning becomes one-sided

Liquidity thins as fewer participants are willing to transact at extremes

Small shifts in order flow can have outsized impact

In such conditions, price does not need a major catalyst to retrace. It often only needs:

A pause in aggressive buying

Routine profit-taking

A minor shift in expectations

This fragility is what makes mean reversion a relevant consideration after sharp extensions, even within broader bullish structures.

Illustrative Trade Framework (Case Study Only)

To translate these concepts into a practical framework, consider the following illustrative structure, presented strictly as a case study.

o Context

Price has resolved a bullish pattern

Volatility has expanded sharply

Price is trading outside the upper Bollinger Band

o Area of Interest - Upper reference zone near 1.18350, where:

Pattern objectives converge

UFO resistance is present

Trade closure activity is likely

o Mean Reversion Reference - Lower zone near 1.16875, aligned with:

Buy UFO support

Prior participation

The statistical mean

o Risk Definition

Invalidation occurs if price demonstrates acceptance above the resistance zone rather than rejection

This framework highlights an important principle: mean reversion trades are defined by risk first, not by direction. They require patience, flexibility, and a clear understanding of when the underlying premise no longer applies.

Standard and Micro Contracts

This case study can be examined using both standard and micro futures contracts, which offer different exposure profiles while referencing the same underlying market. Understanding their basic specifications is essential, particularly when volatility expands and mean reversion risk increases.

o Standard Futures Contract (6E)

Minimum price fluctuation (tick): 0.000050 per Euro increment = $6.25

Typical margin characteristics: ~$2,700 per contract

o Micro Futures Contract (M6E)

Minimum price fluctuation (tick): 0.0001 per euro = $1.25

Typical margin characteristics: ~$270 per contract

Margin requirements are dynamic, not fixed. They are influenced by market volatility, exchange risk controls, and clearing firm policies.

From a risk-management perspective, the availability of both standard and micro contracts enables traders to align position size with conviction and uncertainty, rather than forcing binary exposure decisions.

Risk Management Considerations

Mean reversion setups carry unique risks. Unlike momentum trades, they often involve entering against recent price direction, which requires:

Smaller position sizing

Wider tolerance for initial adverse movement

Strict invalidation criteria

It is also important to distinguish between being early and being wrong. Overextended markets can remain extended longer than expected. Risk management exists to ensure that such scenarios do not result in disproportionate losses.

Ultimately, the objective is not to capture every retracement, but to participate selectively when structure, volatility, and order-flow context align.

Data Consideration

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

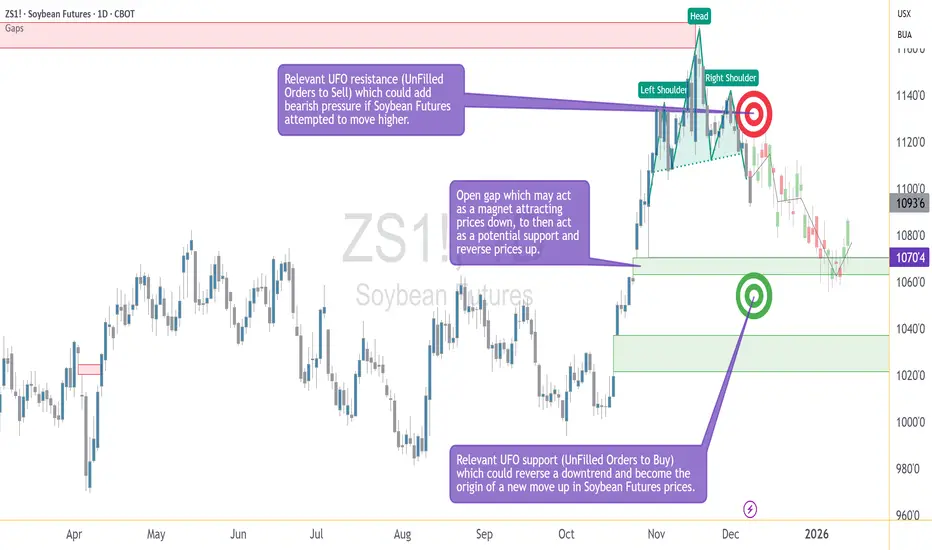

Neckline Breaks and Trader Nerves: A Quick Guide to Bearish H&S The head and shoulders pattern is like the market’s way of clearing its throat and saying, “Things might be changing up here.” Once that neckline snaps, traders often sit up straighter — not because something magical happened, but because the chart finally drew a clean line between “maybe” and “now it matters.”

In this ZS (Soybean Futures) example, price slipped under the neckline and started wandering toward lower ground. Traders who work with this pattern usually focus on three things:

A possible bounce back toward the neckline (because markets love second chances),

A clear invalidation level (in this case, above 1136),

A logical downside objective such as the gap-and-support combo near 1070'4.

That simple trio turns a chaotic chart into a calm plan.

Contract specs matter too. The ZS contract moves in bigger bites:

Tick: 1/4 of one cent (0.0025) per bushel = $12.50 per contract

Margin: $2,000 per contract

The MZS (Micro Soybean Futures) contract takes smaller ones:

Tick: 0.0050 per bushel = $2.50 per contract

Margin: $200 per contract

Traders who want more precision sometimes choose the micro so their stop-loss distance and account size stay on speaking terms. Either way, the chart sets the idea, but the contract size sets the comfort level.

And of course, the golden rule in pattern-based trading: the market can still do whatever it wants. That’s why traders define their exit if wrong, their objective if right, and their size before clicking anything. A head and shoulders isn't about predicting — it's about organizing.

The chart example ties it all together: neckline break, resistance overhead, downside target below. Simple, structured, and practical — just the way traders like it.

Want More Depth?

If you’d like to go deeper into the building blocks of trading, check out our From Mystery to Mastery trilogy, three cornerstone articles that complement this one:

🔗 From Mystery to Mastery: Trading Essentials

🔗 From Mystery to Mastery: Futures Explained

🔗 From Mystery to Mastery: Options Explained

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

From Neckline to Target: Setting H&S Bearish Entries and ExitsUnderstanding the Head & Shoulders Breakdown

A bearish head and shoulders pattern gives traders a structured way to define entries and exits using price geometry rather than emotion. The pattern forms when a market transitions from strength to distribution, creating a left shoulder, a higher head, and then a lower right shoulder as momentum begins to fade. The neckline acts as the key support level that separates a developing pattern from a completed one.

In the case study illustrated on the chart, the daily timeframe shows a fully developed head and shoulders structure that confirmed during the December 5 trading session, when price closed below the neckline. This type of close is often interpreted by traders as evidence that bearish participation has taken control of the pattern. Whether a trader enters immediately or waits for a retest, the priority becomes identifying the levels that will structure the trade: the area of invalidation, the downside objective, and the points where risk must be controlled.

A confirmed neckline break does not imply certainty about future price direction. Instead, it provides an organized framework—a map traders can use to define where their idea is considered valid and where it is considered invalid. The educational value of this pattern lies not in its ability to predict, but in its ability to help traders pre-plan actions with clarity.

Structuring the Bearish Entry: Neckline Retests and Resistance Zones

One of the most common approaches to trading a bearish head and shoulders is to monitor for a modest bounce back toward the neckline after the breakdown. Retests do not always occur, but when they do, many traders see them as opportunities to enter with more control over the distance between entry and stop.

In this example, price sits beneath a well-defined UFO resistance area between 1123 and 1136. This band aligns with a cluster of unfilled sell orders, which may reinforce bearish pressure if price attempts to climb. More importantly, the upper boundary of the zone—1136—serves as an objective point of invalidation. If price were to move above that level, the logic of the completed bearish structure would no longer hold. Therefore, traders could use this upper boundary as a stop-loss level. It is neither arbitrary nor emotional; it is derived directly from the structure.

This type of predefined invalidation is essential because even the cleanest technical patterns can fail. The purpose of using a pattern is not to guarantee the outcome, but to know exactly when the trade thesis no longer makes sense. In this framework, the neckline provides context for the entry, while the resistance zone provides clarity for where the idea is wrong.

Defining the Target: Gap Alignment and Technical Confluence

After establishing where a trade becomes invalid, traders turn to the question of where it becomes complete. In pattern-based trading, target selection often blends classical measurement rules with the identification of technical areas where price has reason to react. In this case study, the downside objective centers on 1070'4, where two important elements align.

First, there is an open gap at this price level. Gaps frequently attract price because they represent prior imbalances in trading activity—areas where the market moved too quickly for participants to fully transact. When price revisits such a location, it becomes a zone where activity may increase. Second, the gap coincides with a region of unfilled buy orders that may serve as a UFO support area. When gaps and demand zones overlap, the confluence strengthens the rationale for using the level as a target.

Because the bearish pattern is already confirmed, traders using this structure may calculate a reward-to-risk ratio by comparing the distance from the entry zone to the stop (near 1136) and the distance from the entry zone to the target (1070'4). The role of the target is not to predict where price will go, but to anchor the trade in a predefined and measurable plan. It transforms the setup into a risk-managed scenario rather than an open-ended directional hope.

Understanding Contract Specs, Margin, and Risk Management

Traders using standardized futures contracts must structure their decisions around contract size, tick value, and margin requirements. The chart example in this idea uses the standard ZS contract, which represents 5,000 bushels. The micro contract (MZS) represents 500 bushels. This difference directly affects position sizing and the dollar impact of each tick. Because margin requirements vary over time, traders should always check the latest values before entering any position.

Tick (Minimum Price Fluctuation:

ZS: 1/4 of one cent (0.0025) per bushel = $12.50 per contract

MZS: 0.0050 per bushel = $2.50 per contract

Current Margin Requirements:

ZS: $2,000 per contract

MZS: $200 per contract

A key benefit of having two contract sizes available is flexibility. Traders seeking to maintain disciplined risk parameters often use micro contracts to fine-tune exposure, ensuring that the stop-loss level does not exceed their predefined risk tolerance. The objective of the head and shoulders pattern is not merely to identify a direction but to help traders organize their plan around risk boundaries. Knowing the contract’s characteristics enables the trader to size positions correctly.

Risk management remains the foundation of pattern-based approaches. Price can behave unpredictably, even when the chart seems decisive. This is why traders emphasize position sizing, controlled leverage, and strict adherence to the stop-loss level. The goal is not to avoid losses entirely but to keep them manageable and consistent. A well-constructed head and shoulders strategy relies not only on identifying the pattern but on respecting the risk parameters that accompany it.

Bringing It All Together: Structure, Context, and Discipline

The chart included in this idea illustrates the essential elements of the bearish head and shoulders setup: the left shoulder, head, and right shoulder; the neckline break; the gap at 1070'4; and the resistance band between 1123 and 1136. These levels form the backbone of a structured trading plan. Rather than reacting to market movement in real time, traders can use these predefined reference points to guide decision-making with consistency.

The purpose of this article is educational. It demonstrates how entries, exits, and risk parameters can be structured around a classical bearish head and shoulders pattern, how confluence strengthens downside targets, and how contract specifications help traders align position size with their risk tolerance. Above all, it shows that disciplined planning matters more than attempting to anticipate every price movement.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Why Silver Is Reaching New High?Why Is Silver Reaching New Highs?”

There are two key reasons for this:

First, it is due to de-dollarization. At this juncture, there are no other currencies ready to take over as the dominant reserve currency. Therefore, the market is turning to precious metals like gold and silver. We can also observe that each time the dollar trends lower, precious metals tend to move in the opposite direction.

Second, why is silver gaining momentum over gold this time? While gold is still trading below its October high, silver has already broken above it with strong momentum.

These are the two questions we will be discussing today.

Mirco Silver Futures

Ticker: SIL

Minimum fluctuation:

0.005 per troy ounce = $5.00

Disclaimer:

• What presented here is not a recommendation, please consult your licensed broker.

• Our mission is to create lateral thinking skills for every investor and trader, knowing when to take a calculated risk with market uncertainty and a bolder risk when opportunity arises.

CME Real-time Market Data help identify trading set-ups in real-time and express my market views. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

AI Stocks Started Sneezing… and Indices May Have Caught a Chill?The NASDAQ (a.k.a. the AI theme park) just printed a much lower monthly low.

ES? It dipped… but only politely.

That mismatch matters. When tech acts tired, the broader market usually needs caffeine — or a correction.

The Indicators Are Whispering… and They Don’t Sound Bullish

The CCI is saying “lower highs,” while price is saying “higher highs.”

Classic divergence.

The MACD histogram is fading like holiday lights at 4 a.m.

Momentum? Not dead — just yawning.

Three Levels That Could Decide Whether Santa Shows Up

Think of December like a video game boss fight with three phases:

6,525.00 → First alarm bell. Break it and the mood changes.

6,239.50 → “Bear trap danger zone.” Plenty could happen here.

4,430.50 → The deep level nobody wants to talk about, but everyone should mark.

If ES finds its footing near 6,239.50, Santa still has a shot.

If not… well… Grinch season might come early.

ES & MES Contract Specs + Margins

E-mini S&P 500 Futures (ES)

Tick size: 0.25 index points = $12.50

Approx. margin (as of now): ~$22,400 per contract

Micro E-mini S&P 500 Futures (MES)

Tick size: 0.25 index points = $1.25

Approx. margin (as of now): ~$2,240 per contract

Margins vary by broker and can change with volatility, but these figures reflect current exchange-level requirements.

Risk Management: The Only Real Holiday Magic

ES and MES give traders the same view of the market but with different intensity levels.

December is emotional, fast, and occasionally rude — so size positions like someone who wants to enjoy the holidays, not stress through them.

Pick a zone → define the invalidation level → cap your dollar risk → choose ES or MES accordingly.

Simple. Calm. Holiday-friendly.

Final Thought

Santa hasn’t canceled the rally yet. But AI stocks aren’t exactly singing Christmas carols either.

If the tech giants recover, December could still sparkle.

If they don’t… the sleigh might need a repair shop.

Either way: chart levels > seasonal hope.

Trade safe — and maybe hide a cookie for the market, just in case.

Want More Depth?

If you’d like to go deeper into the building blocks of trading, check out our From Mystery to Mastery trilogy, three cornerstone articles that complement this one:

🔗 From Mystery to Mastery: Trading Essentials

🔗 From Mystery to Mastery: Futures Explained

🔗 From Mystery to Mastery: Options Explained