The Hidden Skill Every Great Trader Masters; And It’s Not Chart!Most traders spend years perfecting chart patterns, indicators, and entries…

Yet only a handful ever master the real skill that separates professionals from the rest, the art of waiting.

📉 Anyone can draw support and resistance.

📈 But not everyone can wait for price to reach them.

The market rewards patience, not predictions.

It’s not about catching every move, it’s about being ready when your setup aligns perfectly.

That’s when you strike. That’s when probability works for you, not against you.

Think of trading like fishing 🎣:

You don’t chase the fish, you position your line where it’s most likely to bite, then you wait.

So next time you feel the urge to jump in early, remind yourself:

You’re not just a trader. You’re a waiter, paid in precision and patience.

📚 Key takeaway:

Great traders don’t predict, they prepare.

They let the market move first, then respond with clarity.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

All Strategies Are Good; If Managed Properly!

~Richard Nasr

Community ideas

Standard Deviations - How to be exit before the pullbackHey whats up guys, in this post Ill show you easy method which can help you to set your targets, stay in the positions, prevent cutting position too early or hold for too long. You will basically have more objectives to stay in trade and give it a frame to which key levels you should use. Standard deviations are projection deviations of the manipulation leg. Which is the price swing that sweeps liquidity and then changes the order flow. In simple words, it is the move that takes out stops and then flips the structure - Order block.

📌 Fibonacci tool settings

We will be measuring deviations from the order block and here is the Fibonnaci settings

0 - 1 is where you measure the manipulation leg and then you got your projections.

Zone between 2 - 2.5 is my main focus for taking partials of full profits Price obviously can go further but between 2 - 2.5 is where I tend to take something of the table. Because my longterm statistics says most of my trades has 2.3 RR. 📌 What to do at 2- 2.5

Obviously don't start doing what Im saying here on your next trade. First test it and if you find it useful, never put any idea from someone from the internet to your money without verifying by yourself then add it to your arsenal or reject it. If your strategy has fixed TP based on structure stick with it. Standard deviations can be just a little helper. Let's look at few examples.

1️⃣ Example: GBPUSD

This is the example which has Benn posted here on TV And as you can see it has made some gain, didn't hit full TP and reversed, back to the entry. But look where it reversed - Exactly at the 2 - 2.5 I saw it has my average profit and it was Friday so I closed it . as we can see it was a good decision to close position fully here and not sticking to to the full target. Im not saying that closing trader before the initial target is good decision, but considering that its Friday and I got my average 2.3 gains. Its a no brainer to take what the market offers to me. 2️⃣ Example: EURUSD

My strategy is has two defined targets. 50% of the range and full range. After taking 50% partial at 50% I should be targeting opposing range low after the sweep of the liquidity highs. So I should hold the trade until the target. But as it was a Friday and price been between 2 - 2.5 means my trade was around 2.3 RR in profit, which is my average reward so I decided to close it completely and as we can see it was a good decision as the price just completely reversed before hitting my target. 3️⃣ Example: XAUUSD

This is model 2 entry on Weekly range and Model 1 on Daily CLS range. Let's not overcomplicate. Look at the order block our initial point for the measuring our target and check where is the 2 Std. Projecting 2 St.D gave me confidence that CLS highs could be reached easily as it all was aligned with HTF trend so I held the trade for the whole week. Exited little bit bellow, but as it was reaction on LTF OB and Friday, I didnt want to hold in the trade over the weekend. 4️⃣ Example :EURUSD

Another EURUSD trade example after sweeping a low and creating order block We can that 2 STD aligns with CLS highs so its perfect target and we can see sharp expansion to the 2 St. D then price started retracing and consolidating, If we targeting bigger targets we would be for 2 days in this choppy range now. 📌This tool is not a strategy it self its just something what can help us to set reasonable targets while we don't have to face big pullbacks. Im not saying you should go only for 2.3 RR as I do. If you can hold traders for 3RR and more you are great trader.

📌However I found that when Im targeting 3R and more, I must face pullback and watch how my gains go back to the markets which I dont like. Im still human and have emotions and you know how it feels when you have a great trade developing and then in a blink of the eye its back on your entry.

📌Also by targeting just 2.3 RR is a clean shot and I realized that I can increase my risk per trade for such setups because they are hitting TP more often than 3RR trades. So in the end it's less stress and better profits. But it's all about a personal preferences.

Let me know what is your average RR and reason you targeting it.

David Perk aka Dave Fx Hunter

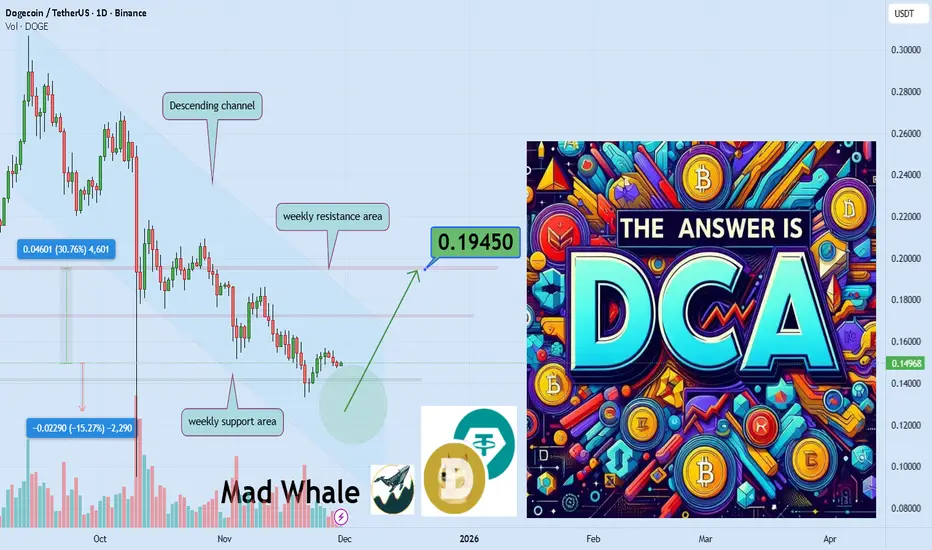

Working hard yet poor while Others get wealthy, answer is DCAEver wondered why you work so hard yet your wealth doesn’t grow

How some people with the exact same income quietly multiply their assets

The answer is a simple calm strategy that whales follow It is called DCA

Hello✌️

Spend 3 minutes ⏰ reading this educational material.

🎯 Analytical Insight on doge:

I expect a much bigger rise for Ripple than what I have shown on the chart. But we should remember that every year when the New Year approaches the market usually goes bearish. We need to wait and pass through that period to see what the final result will be.

Now , let's dive into the educational section,

The problem isn’t the market it is our behavior 🧠

Many wait for the perfect entry and never enter at all

Others rush to buy the top then panic sell the bottom

This behavior kills wealth and wastes precious time

The market never rewards emotional chaos

DCA means order inside crypto chaos ⏳

Crypto volatility punishes the impatient every single time

Buying periodically stops emotional decision making

If price drops you accumulate cheaper

If price rises your position grows stronger

Why whales never act like retail traders 🐳

Whales never throw all capital at once into the market

They use every dip as a quiet accumulation opportunity

DCA is simply whale strategy in a smaller scale

Slow silent and incredibly powerful

Greed is the hidden enemy of retail 🔥

Our mind always asks for fast and huge profits

But real profits go only to the patient ones

DCA isn’t greedy but builds true wealth

Each small buy is one step toward financial freedom

When everyone is hopeless you own the future ⚡

In bear markets emotional traders give up

But DCA traders become the future winners

The market rewards those who continue

Not those who stop because of fear

Your DCA plan must stay simple 📝

Define a monthly amount that never hurts your life

Choose a fixed time so it becomes a habit

Pick strong and credible long term assets only

Most important never break discipline for news or hype

summary 🎯

If you work hard but wealth doesn’t grow

The problem is not effort the problem is no system

TradingView features that make DCA smarter 📈

Price alerts so the market never surprises your entries

Moving averages to confirm trend before new allocation

Support zones marked with horizontal levels for optimal steps

Volume indicator to detect where big money is building positions

Percent labels to track the efficiency of every DCA buy

A clean focused watchlist to keep best assets always visible

survival tips for crypto investors 🔑

Never sacrifice long term patience for short term excitement

Volatility copies your mindset stay balanced and volatility works for you

True wealth goes to those who continue even during deep red days

✨ Need a little love!

We pour love into every post your support keeps us inspired! 💛 Don’t be shy, we’d love to hear from you on comments. Big thanks , Mad Whale 🐋

📜Please make sure to do your own research before investing, and review the disclaimer provided at the end of each post.

Unlock Hidden Trading Edges: Master Support & Resistance Levels Master Support & Resistance Levels – The Most Powerful Tool in Technical Analysis 📈🔥

Support and Resistance (S&R) are the foundation of price action.

Support = where price tends to stop falling (buyers step in) 🛡️

Resistance = where price tends to stop rising (sellers take control) ⚔️

These levels are not always exact, but when used correctly they give you high-probability entries and exits in Forex, Crypto, and Stocks.

How to Find Strong S&R Levels:

1-Look left → Previous swing highs & lows

The more times price has touched and bounced, the stronger the level becomes.

2-Round numbers & psychological levels

Examples: $50,000 BTC, 1.2000 EUR/USD, $200 AAPL – traders love these!

3-Use TradingView tools

Horizontal Line

Fibonacci Retracement (38.2%, 50%, 61.8%)

Volume Profile (High-volume nodes often act as S&R)

2Role Reversal – The Magic Trick ✨

Broken resistance → becomes new support

Broken support → becomes new resistance

This is where the big moves start!

Real Examples Right Now:

Bitcoin → $100,000 break support → now strong resistance

Pro Tips:

Always check multiple timeframes (Daily + 4H give the strongest levels)

Combine with RSI or volume for confirmation

Place stop-loss just below support / above resistance

When a level breaks with high volume → jump on the breakout!

Start drawing your S&R levels today and watch your win rate improve instantly.

Which market are you trading right now? Drop your favorite S&R level in the comments! 👇

SPX – MFM Light HUD (Free) shows a clean bullish regimeThis post is an educational example of how to interpret the free MFM Light Context HUD. It does not provide trading signals or directional predictions.

The MFM – Light Context HUD (Minimal) gives a simple view of the structural state of the market. On SPX the model shows a clear bullish regime on the weekly momentum ratio. This does not predict direction. It only shows whether the underlying environment is supportive or restrictive.

The phase is currently neutral. That means SPX is not in a volatile phase, not in a compression field, and not in a drift phase. When no phase is active, price tends to behave without strong internal pressure. It is simply the absence of structural imbalance.

What the phases mean

These phases describe structure, not trade signals.

Volatile (Phase 1): fast movement and unstable conditions.

Compression (Phase 2): contracting conditions with slowing momentum.

Drift (Phase 3): more controlled and persistent movement.

Neutral: no clear structural condition.

This is why the HUD is useful. It removes noise and gives a clean top level reading.

You can still use your own strategy or analysis. The HUD just tells you what kind of environment you are operating in.

What you see in this chart

Weekly regime is bullish

No active phase

No signals or forecasts

Only structural context

Why this matters

In strong bullish regimes markets often react differently to pullbacks, volatility spikes or news events. Context does not replace analysis. It frames it.

Disclaimer

The Market Framework Model (MFM) and this indicator are for educational and informational purposes only. Nothing in this script, its visuals, or any documentation should be interpreted as financial advice or as a recommendation to buy or sell any asset.

All examples and historical references are illustrative only and do not imply future results. Trading and investing involve risk, including the potential loss of capital. Users remain fully responsible for their own decisions.

No guarantees are made regarding accuracy, completeness, or reliability. MFM describes structural market context only and should not be used as the sole basis for trading actions.

© 2025 Inratios. Market Framework Model (MFM) is protected via i-Depot (BOIP) – Ref. 155670.

Internal vs External Liquidity: The Skill Nobody Actually MasterMost traders think they understand liquidity…

They mark equal highs, equal lows, and call it a day.

But let me tell you something real:

Knowing liquidity exists is NOT the skill.

Knowing WHICH liquidity matters right now is the real edge.

That’s the difference between:

✔ catching continuations

✔ catching reversals

✔ avoiding trap entries

✔ timing precision entries

✔ and actually staying in profitable moves

Most traders lose because they don’t understand the hierarchy of liquidity.

Let me break this down the way nobody online does:

⸻

🔥 1. Internal Liquidity = Fuel for Continuation

This is the liquidity inside the active range.

It sits between swing points, inside consolidation, above minor highs, below short-term lows.

Internal liquidity gets taken when:

• Market is in trend

• Price is compressing

• Price is building inducement

• Algorithms are collecting “fuel” before delivery

When internal gets swept, DO NOT expect a reversal.

Expect a continuation into the next external pool.

This is why most traders get faked out:

They see a sweep and scream “reversal!”

But they’re reacting to internal liquidity — not the real turning point.

⸻

🔥🔥 2. External Liquidity = The Real Reversal Zones

External liquidity sits at the RANGE BOUNDARIES:

• The major swing high

• The major swing low

• The extreme points of the structure

These are the levels that actually SHIFT trend, cause deep pullbacks, or start major legs.

This is where smart money:

✔ Clears the crowd

✔ Triggers stops

✔ Closes positions

✔ Repositions

✔ Begins delivery in the opposite direction

External liquidity is the turning point.

Internal liquidity is just the build-up.

If you can’t distinguish the two, every reversal will feel random to you.

⸻

🔥🔥🔥 3. Here’s the Rule Nobody Teaches:

If price sweeps internal → expect continuation.

If price sweeps external → expect correction or reversal.

But here’s where MOST traders fail:

They don’t know which one they’re looking at.

If you think a reversal is starting but you’re still inside the range…

You’re not trading a reversal.

You’re trading hopium.

⸻

🔥🔥🔥🔥 4. How Smart Money Chooses Which Liquidity to Target First

This is where your real edge comes in.

Smart money asks ONE question:

“Which pool unlocks the next delivery path?”

If the next objective is above → they’ll sweep internal lows to build power.

If the next objective is below → they’ll sweep internal highs to induce buyers.

Smart money is always targeting what unlocks:

✨ the cleanest path

✨ the imbalanced leg

✨ the untouched zone

✨ the unmitigated order block

✨ the next HTF objective

You think the sweep is the entry.

They see the sweep as the setup.

⸻

🔥🔥🔥🔥🔥 5. Here’s the TRUTH:

Internal liquidity fuels the move.

External liquidity flips the move.

If you master this one skill, your whole trading shifts.

Your confidence shifts.

Your timing shifts.

Your strike rate shifts.

You stop chasing noise.

You stop guessing bottoms.

You stop guessing tops.

You start reading intention — not reacting to candles.

Most of the trading world knows liquidity.

Almost nobody knows when liquidity actually matters.

That’s the part the textbooks don’t teach.

That’s the part the YouTubers don’t show.

That’s why most traders stay confused for years.

Internal liquidity gets you in —

External liquidity gets you paid.

Master the difference and you’ll trade with precision most people only dream of.

Forex Trading Secrets1. Price Action Is the Real King (Not Indicators)

Most beginners clutter their charts with dozens of indicators hoping to find a perfect buy–sell formula. Professionals know the truth: price itself gives the most reliable information. Indicators lag because they represent past price data, not current market intent.

What professionals focus on:

Support and resistance zones

Market structure (higher highs, lower lows)

Liquidity levels (areas where stop-loss clusters exist)

Candlestick strength (rejection wicks, engulfing candles)

When a trader learns to read price action—how candles react to zones, how momentum builds or fades—they can trade profitably even with a clean chart. Indicators become secondary confirmation tools, not primary decision drivers.

2. Liquidity Is What Moves the Market

Here’s a hidden truth: forex markets move to fill liquidity, not because of random price swings. Big players like banks and institutional traders execute massive orders, and they need liquidity to fill those orders efficiently. That means:

Price hunts stop-loss clusters

Price sweeps highs and lows before reversing

Spikes occur to capture pending orders

This is why you often get stopped out right before the market moves in your favor. Understanding liquidity behavior gives traders a powerful edge.

Liquidity concepts include:

Stop hunts

Fake breakouts

Order block zones

Liquidity grabs

Smart traders expect these moves and position themselves accordingly.

3. The Trend Is Stronger Than Your Analysis

One of the biggest secrets is deceptively simple: Trading with the trend dramatically increases win probability. Many traders try to catch tops and bottoms, but institutional players rarely fight the trend—they ride it.

Characteristics of trend-following success:

Higher time-frame confirmation

Entering on pullbacks, not chasing

Using simple trend continuation patterns

Keeping trades open longer during strong trends

The trend holds more weight than any indicator or news event. Fighting the trend is one of the fastest ways to blow up an account.

4. Risk Management Is the Most Guarded Secret

Ask any long-term successful trader their biggest edge, and the answer won’t be a strategy—it will be risk management.

Key risk management secrets:

Never risk more than 1–2% per trade

Position sizing is more important than entries

A trader with moderate accuracy and strong risk rules often outperforms a trader with high accuracy but poor risk control

Understanding when not to trade is also a powerful risk strategy. Not trading low-quality setups protects your capital and mental energy.

5. Trading Psychology Outweighs Strategy

This is the hardest secret for beginners to accept: Your mindset determines your results more than your system.

The psychological traits professionals share:

Patience to wait for ideal setups

Discipline to follow rules consistently

Neutrality—no emotional attachment to wins or losses

Resilience after a losing streak

Confidence built on data, not hope

A trader can have the world’s best strategy, but fear, greed, revenge trading, and impulsiveness will destroy the account. This is why psychology books are more valuable than indicator tutorials.

6. Higher Time Frames Reduce Noise and Increase Accuracy

A hidden secret among consistently profitable traders is that they rely heavily on higher time frames like the daily or 4-hour.

Why higher time frames work:

Clearer market structure

Stronger trend visibility

Fewer false signals

Trades require less screen monitoring

Better risk-to-reward setups

Scalping looks attractive, but it magnifies emotions and often leads to over-trading. Higher time-frame trading reduces mental stress and increases consistency.

7. Fundamental Catalysts Drive Major Moves

Forex is deeply influenced by macroeconomic factors. Professionals use fundamentals to understand why the market is trending and where major volatility will occur.

Major catalysts include:

Central bank interest rate decisions

Inflation data (CPI, PCE)

Employment data (NFP, unemployment rates)

GDP figures

Geopolitical events

Fiscal policies

Ignoring fundamentals means ignoring the very forces that create trends.

But the secret is: You don’t need to be an economist—just know when news is happening and how it affects risk.

8. Smart Money Concept (SMC) Edge

Institutional-style concepts, once hidden from retail traders, are now increasingly discussed. These include:

Order blocks

Fair value gaps (FVG)

Market structure shifts (MSS)

Imbalance zones

Buy-side and sell-side liquidity

These concepts explain how institutions accumulate and distribute positions. Traders who master SMC often experience a major breakthrough in accuracy.

9. Consistency Beats Intensity

This secret is rarely acknowledged.

Successful traders:

Follow a structured routine

Practice the same strategy repeatedly

Keep a trading journal

Backtest regularly

Set trading sessions and stick to them

Failure in forex often comes from randomness—random indicators, random entries, random time frames. Success comes from consistency, not constant experimentation.

10. Forex Is a Business, Not Gambling

Treating forex like a business means:

Maintaining a trading plan

Logging trades

Tracking performance metrics

Identifying weak areas

Improving process instead of chasing profits

Traders who approach forex like gambling lose money. Traders who approach it like a business grow gradually and sustainably.

Conclusion: The “Secrets” Are Not Hidden—They Are Underrated

The real secrets of forex trading are not magic formulas or mysterious tools. They are principles that professionals use every day but beginners often overlook in search of shortcuts.

To summarize:

Price action matters most

Liquidity drives the market

Trend-following improves probability

Risk management is the true edge

Psychology determines consistency

Higher time frames simplify trading

Fundamentals guide long-term trends

SMC offers an advanced structural view

Consistency builds mastery

Treating trading as a business ensures longevity

Mastering these secrets takes time, discipline, and patience. But once internalized, they form the foundation of sustainable forex success.

The Global Trade Market Superpower1. What Defines a Global Trade Superpower?

A global trade superpower is a country (or group such as the EU) that:

✔ Dominates global exports and imports

The ability to supply goods at scale—manufactured, agricultural, technological—creates massive global impact.

✔ Controls key global supply chains

Superpowers are deeply embedded in or outright control production lines, energy routes, shipping, logistics, and commodity flows.

✔ Influences global financial systems

Trade superpowers usually have strong currencies, major stock exchanges, and banking systems that shape global capital movement.

✔ Sets global standards and rules

From trade agreements to environmental norms, superpowers shape what the world must follow.

✔ Maintains military and diplomatic dominance

Economic power is supported by defense capabilities, alliances, and diplomatic networks that protect trade interests.

Countries like the United States, China, and the European Union are prime examples of trade superpowers, while emerging economies like India, South Korea, and ASEAN nations are rapidly rising.

2. Historical Evolution of Trade Superpowers

a. Age of Exploration (1500–1800)

European powers—Portugal, Spain, Netherlands, France, and Britain—dominated global trade through:

Maritime exploration

Colonization

Monopoly control over spices, textiles, gold, and silver

This era established the foundations of global shipping routes and international markets.

b. Industrial Revolution (1800–1950)

Britain was the first global trade superpower driven by:

Mechanized manufacturing

Steamships and railways

Massive colonial markets

Later, the United States and Germany joined as industrial giants.

c. Post–World War II Era (1950–2000)

The United States emerged as the world’s leading trade superpower due to:

Dollar becoming the global reserve currency

Strong manufacturing and innovation

Control over global institutions like IMF and World Bank

Japan and Europe also became major export-driven economies.

d. Rise of China (2000–Present)

China transformed into the “Factory of the World” by:

Massive low-cost manufacturing

Export-oriented economic strategy

Investment in ports, shipping, and global infrastructure

China now rivals the United States in global trade influence.

3. Key Elements That Build a Trade Superpower

1. Industrial Capacity

Large production capability allows superpowers to dominate global markets.

China: electronics, machinery, textiles

United States: high-tech, aerospace, pharmaceuticals

EU: luxury goods, machinery, chemicals

Countries without strong industrial bases cannot gain global influence.

2. Control of Supply Chains

From microchips to crude oil, controlling supply chains decides global power.

Trade superpowers invest heavily in:

Ports and logistics

Manufacturing hubs

Rare earth minerals

Energy pipelines

Shipping fleets

For example, China’s Belt and Road Initiative strengthens its global supply chain control.

3. Strong Currency and Financial Power

A trade superpower’s currency becomes widely used in international transactions.

USD dominates global trade payments.

Euro is second in trade invoicing.

China’s yuan is expanding rapidly through global trade partnerships.

Financial power also helps these nations dictate global economic rules.

4. Technology and Innovation

Trade superpowers lead in:

Artificial intelligence

Semiconductors

Aerospace

Biotechnology

Green energy

Technology ensures long-term global competitiveness.

5. Strategic Trade Agreements

A superpower uses diplomacy to secure favorable trade networks:

Free trade agreements

Regional partnerships

Security alliances

Maritime control

The US-led alliances and China’s RCEP advantage demonstrate how diplomacy supports trade dominance.

4. Current Global Trade Superpowers

1. China

China is now the world’s largest exporter and a major importer of technology, energy, and food. Its strengths include:

Manufacturing scale unmatched globally

Strong logistics network

Belt and Road infrastructure

Dominance in rare earth minerals

Increasing influence in Asia, Africa, and Europe

China’s growth has reshaped global supply chains.

2. United States

The US remains a powerful trade superpower due to:

Dollar dominance

Technological leadership (Apple, Microsoft, Tesla, Boeing)

Agricultural exports

Strong domestic demand

Global financial and defense alliances

Even without being the largest exporter, its innovation and capital markets give it unmatched global leverage.

3. European Union

As a combined economy, the EU is a trade powerhouse:

World’s largest trading bloc

Major exporter of machinery, automobiles, pharmaceuticals

Highly regulated market influencing global standards

EU’s strength lies in quality manufacturing and a unified market.

4. Rising Powers

Countries like India, Japan, South Korea, Brazil, and ASEAN nations are gaining influence through:

Tech innovation

Young workforce

Regional trade agreements

Strategic resource control

India, for example, is becoming a major global service exporter and manufacturing hub.

5. How Trade Superpowers Influence Global Markets

a. Price Setting Power

Superpowers influence global prices of:

Oil and gas

Metals

Electronics

Food commodities

Their policies can cause global price shifts.

b. Sanctions and Trade Restrictions

Trade superpowers can impose sanctions that affect entire industries or nations.

Examples:

US sanctions disrupting global semiconductor trade

EU carbon tariffs influencing manufacturing norms

China’s export controls on rare earth elements

c. Shipping and Logistics Control

Major superpowers operate:

Key global ports

World’s largest shipping fleets

Global air cargo networks

This ensures they can move goods faster and cheaper than others.

d. Standard-Setting Power

From food safety to digital privacy, superpowers write rules the world must follow.

6. Future of Global Trade Power: Who Leads Next?

The global trade landscape is changing rapidly:

China is strong, but faces challenges like geopolitical tensions and shrinking demographics.

The United States remains influential, particularly in technology and finance.

India is the fastest-rising contender, driven by:

Rapid economic growth

Large workforce

Expanding manufacturing

Strong technology sector

India could become the next major trade superpower by 2035.

Regional blocs like ASEAN and Africa are also emerging as significant players.

Conclusion

A global trade superpower is not defined by exports alone, but by the ability to shape global markets, rules, supply chains, technology, and finance. Today, China, the United States, and the European Union dominate the trade landscape, while emerging economies like India are rapidly rising.

Global trade superpowers determine the flow of goods, capital, technology, and influence—ultimately shaping the direction of the world economy.

Startups Reshaping the Global Market1. Innovation as the Core Driver of Market Transformation

Startups thrive on innovation—not just in products, but in processes, platforms, and business models. Traditional firms often struggle with legacy systems, bureaucratic decision-making, and risk aversion. Startups, however, operate with flexibility and a problem-solving mindset, enabling them to test new ideas quickly.

Examples of Startup-Led Innovations

FinTech companies introduced digital banking, mobile wallets, micro-lending, and crypto-based financial services.

HealthTech startups pioneered telemedicine, AI diagnostics, and wearable health monitoring.

CleanTech innovators built new pathways for sustainable energy, including solar SaaS models and electric mobility.

AgriTech startups are transforming farming with precision agriculture, drone monitoring, and smart irrigation.

By challenging traditional norms, startups create entirely new markets and redefine customer expectations.

2. Digital Transformation and the Acceleration of Automation

Startups have significantly accelerated global digital transformation. They adopt technologies like AI, machine learning, blockchain, IoT, cloud computing, robotics, and automation as foundational elements of their products and services.

Key Impacts

AI-driven startups are powering forecasting, personalization, fraud detection, and workflow automation across industries.

IoT startups are reshaping manufacturing, logistics, and smart cities by enabling real-time data flow and predictive maintenance.

Blockchain startups introduced decentralization in finance, supply chain tracking, and digital identity.

The rapid adoption of digital tools by startups forced larger companies to modernize at unprecedented speed. Today, many enterprises partner with or acquire startups to remain competitive.

3. Disruption of Traditional Industries

Startups often succeed by simplifying complex, expensive, or inefficient processes within existing industries. They disrupt markets by offering:

Lower costs

Better customer experience

Faster delivery

Unique value propositions

Personalized solutions

Industry Disruptions

Transportation: Ride-hailing and mobility startups like Uber, Ola, Grab shaped the future of mobility.

Hospitality: Airbnb redefined accommodation by turning homes into global travel assets.

Retail: E-commerce startups forced traditional retail to shift online.

Media and Entertainment: Streaming startups revolutionized how people consume content.

Education: EdTech platforms made learning accessible to anyone, anywhere.

These disruptions create ripple effects, compelling traditional players to adapt or risk extinction.

4. Democratizing Access to Products and Services

Startups often focus on removing barriers—whether financial, geographical, or technological. Their solutions frequently make services accessible to people who previously could not reach them.

Examples

FinTech startups provide digital loans to small businesses lacking access to traditional banking.

EdTech platforms bring high-quality education to rural areas.

HealthTech solutions enable remote diagnostics for patients in underserved regions.

E-commerce startups allow small merchants to sell nationwide.

This democratization gradually levels the playing field and broadens economic participation.

5. Globalization and Cross-Border Expansion

Startups scale quickly due to digital infrastructure, venture capital funding, and cross-border partnerships. Cloud technology and digital marketing allow them to reach global audiences with minimal physical presence.

Global Expansion Strategies

Launching digital-first products

Partnering with global distributors

Leveraging borderless payment gateways

Operating through remote teams

Using international venture ecosystems

China, India, the US, Southeast Asia, and Europe have emerged as startup hotspots, each contributing to the global innovation landscape. Today, a startup founded in Bangalore or Singapore can compete directly with players in Silicon Valley or London.

6. Redefining Work Dynamics and the Future of Employment

Startups have also reshaped the global labor market. Their work culture emphasizes:

Flexibility

Remote work capabilities

Decentralized teams

Innovation-centric roles

Project-based employment

They push the boundaries of traditional corporate structures, preferring flat hierarchies and collaborative environments.

Impact on the Global Workforce

The rise of freelancing and gig economy platforms.

Increased demand for digital skills—coding, analytics, design, marketing.

Hybrid work becoming a global norm.

New roles emerging in AI, Data Science, UX, and Sustainable Tech.

This shift changes how workers engage with employers and how companies attract global talent.

7. India, Southeast Asia, and Africa: Emerging Powerhouses

While Silicon Valley retains its influence, emerging markets are becoming innovation hubs. They offer young populations, rising internet penetration, and business-friendly policies.

India

Thriving FinTech, EdTech, and SaaS sectors

Large talent pool

Increasing unicorn count

Southeast Asia

Digital commerce boom

Mobility and logistics innovations

Rapid adoption of mobile-first solutions

Africa

FinTech revolutionizing financial inclusion

Startups solving local issues like energy and agriculture

These regions contribute to diversifying global innovation beyond traditional Western markets.

8. Venture Capital and Funding Fuel Startup Growth

The global flow of venture capital has empowered startups to scale quickly. Investors provide not only capital but also mentorship, networks, and strategic guidance.

Funding Trends

Focus on AI, deep tech, sustainability, and biotech.

Rise of sovereign wealth funds investing in global startups.

Increase in corporate venture capital.

Growth of startup incubators and accelerators.

This financial ecosystem feeds global innovation and drives market evolution.

9. Sustainability and Impact-Driven Startups

With climate concerns and ESG policies gaining momentum, startups are building environmentally responsible solutions. Sustainability-focused ventures are transforming energy, mobility, packaging, food production, and recycling.

Areas of impact

Renewable energy

Electric mobility

Carbon capture

Biodegradable materials

Circular economy models

Impact startups are pushing both governments and corporations toward greener practices.

10. Challenges Startups Face in Redefining Global Markets

Despite their strengths, startups also encounter significant barriers:

Regulatory uncertainty

High failure rates

Scaling challenges

Funding shortages during downturns

Talent acquisition struggles

Competition from large established companies

However, their ability to adapt quickly helps many survive and flourish.

Conclusion

Startups are no longer just small experimental ventures—they are powerful forces reshaping the global market. By driving innovation, accelerating digital transformation, democratizing services, disrupting traditional industries, and fostering global competition, startups are setting new benchmarks for how businesses operate. Their influence extends across economies, technologies, and societal structures, making them central to the future of global commerce.

In the coming decade, startups will continue to redefine not just markets, but also how people work, collaborate, and consume. Their role in shaping a smarter, more inclusive, and more sustainable world will be one of the defining forces of the global economy.

G7 and G20 Roles in the World Market1. Understanding the G7: Composition and Purpose

1.1 Who Are the G7?

The G7 consists of the world’s most advanced economic democracies:

United States

United Kingdom

Germany

France

Italy

Canada

Japan

(Plus the European Union as a participant)

These nations collectively represent a significant portion of global GDP, technological innovation, financial markets, and political influence.

1.2 Core Purpose of the G7

Formed in the 1970s to address financial crises, the G7 serves as a policy coordination forum for major developed economies. It prioritizes:

Macroeconomic stability

Trade liberalization

Financial market regulation

Technology cooperation

Global security and democracy

Climate change and sustainability

The G7 does not have binding authority, but its decisions shape global market sentiment and policy directions.

2. G7 Roles and Impact on the World Market

2.1 Setting Global Economic Priorities

The G7 acts as a “steering committee” for global capitalism. Its members often set the tone for:

Interest rate expectations

Fiscal policy shifts

Global inflation strategies

Debt management frameworks

Statements from G7 meetings influence market behavior, investor confidence, and foreign exchange flows.

2.2 Leading Global Financial Stability

G7 nations dominate institutions such as:

IMF (International Monetary Fund)

World Bank

OECD

Through these institutions they guide:

Economic bailouts

Structural reforms

Monetary cooperation

Their collective stance is crucial during crises (e.g., 2008 financial crisis, COVID-19 recovery).

2.3 Shaping International Trade

The G7 is a major voice in defending free-market principles. It influences:

WTO policies

Global tariff standards

Supply chain resilience

Technology transfer regulations

Trade-related G7 declarations often impact commodity prices, currency movements, and trade routes.

2.4 Technology and Digital Governance Leadership

G7 countries lead in:

Artificial intelligence

Cybersecurity standards

Digital taxation rules

Their regulations affect global tech companies and cross-border e-commerce.

2.5 Geopolitical Influence on Markets

The G7 imposes sanctions, export bans, and trade restrictions that influence:

Oil and gas markets

Defense spending

Currency movements

Global investor flows

For example, sanctions on Russia shifted energy markets, trade routes, and commodity prices worldwide.

3. Understanding the G20: Composition and Purpose

3.1 Who Are the G20?

The G20 includes 19 countries plus the European Union:

Argentina

Australia

Brazil

Canada

China

France

Germany

India

Indonesia

Italy

Japan

Mexico

Russia

Saudi Arabia

South Africa

South Korea

Turkey

United Kingdom

United States

European Union

This group represents 80% of global GDP, 75% of global trade, and 60% of the world’s population.

3.2 Purpose of the G20

Formed in 1999 after the Asian Financial Crisis, the G20 brings together advanced and emerging economies to address:

Global economic governance

Financial market regulation

Sustainable development

Climate goals

Digital transformation

Trade and investment environment

It is a platform where both developed and developing economies have a voice.

4. G20 Roles and Impact on the World Market

4.1 Ensuring Global Economic Stability

The G20 acts as the primary global economic governance forum, especially during crises. It played a decisive role in:

Coordinating stimulus packages during the 2008 crisis

Managing COVID-19 economic recovery

Structuring global debt relief programs

Its policy coordination helps prevent global recessions and market collapses.

4.2 Strengthening Financial Market Regulations

The G20 instructs institutions like the Financial Stability Board (FSB) to:

Regulate big banks

Improve global accounting standards

Monitor crypto assets

Reduce shadow banking risks

These actions impact global stock markets, banking systems, and capital flows.

4.3 Facilitating Global Trade and Investment

The G20 influences:

WTO reforms

Lowering trade barriers

Cross-border investment rules

Infrastructure partnerships

Initiatives like the G20 Trade and Investment Working Group shape globalization trends.

4.4 Sustainable Economic Development

The G20 pushes global development goals in areas such as:

Renewable energy

Climate financing

Circular economy

Agriculture and food security

Digital inclusion

These priorities influence sectors like green energy, EV markets, and sustainable finance.

4.5 Voice for Emerging Economies

Countries like India, Brazil, Indonesia, and South Africa gain influence through the G20. It provides:

A platform for domestic issues

Opportunities for global partnerships

Access to international funding

Policy alignment with major economies

This fosters investment inflows and boosts regional economic growth.

5. Comparing the G7 and G20 in the World Market

Feature G7 G20

Members 7 developed nations 20 major economies (developed + emerging)

Share of Global GDP ~40% ~80%

Main Focus Policy leadership, geopolitical issues Economic governance, financial stability

Decision-making Political alignment Broader consensus

Influence on Markets Strong on finance, tech, sanctions Strong on trade, global growth, regulation

The G7 sets strategic direction, while the G20 ensures inclusive implementation.

6. How G7 and G20 Complement Each Other

G7 provides ideological leadership and rapid decision-making.

G20 provides global representation and practical solutions.

G7 initiatives often become G20-backed global policies.

Both together stabilize markets, trade flows, and global finance.

7. Conclusion

The G7 and G20 play distinct yet interconnected roles in shaping the world market. The G7 acts as a leadership forum for advanced economies, influencing global finance, technology, and geopolitical strategies. The G20 brings together developed and emerging markets, driving inclusive economic governance, sustainable development, and crisis management. Together, they provide direction, stability, and coordination across global markets, ensuring that the world economy remains resilient, interconnected, and forward-looking.

DXY Surges Explained1. What a DXY Surge Means

A surge in the DXY means the U.S. dollar is strengthening. This strengthening can come from:

Growing confidence in the U.S. economy

Rising U.S. interest rates

Investors seeking safety from global risks

Weakness in other major currencies

Changes in global trade flows

Shifts in central bank policies

When the DXY rises, it often signals that money around the world is flowing into the United States—either for safety, return on investment, or both.

2. Interest Rates: The Primary Driver of DXY Surges

The most influential factor behind a DXY surge is U.S. interest rates. The Federal Reserve has enormous influence on the dollar, as its decisions determine whether global investors find U.S. assets attractive.

Why Higher Rates Boost the Dollar

Higher rates increase the yield on U.S. Treasury bonds.

Investors around the world buy these bonds because they are considered safe and profitable.

To buy U.S. assets, investors must first convert their local currency to dollars.

This surge in demand strengthens the dollar and pushes the DXY upward.

Even expectations of future rate hikes can push the DXY higher. Traders often react not only to actual policy changes, but also to hints from the Federal Reserve.

3. Safe-Haven Demand During Uncertainty

The U.S. dollar is the world’s leading safe-haven asset. When global uncertainty rises—whether due to economic downturns, geopolitical tensions, war, or financial instability—investors flock to the dollar.

Examples of situations that cause safe-haven flows:

Global recessions

Banking crises

Declines in stock markets

Political instability in major economies

Currency crises in emerging markets

During such times, investors search for stability, and they often find it in U.S. Treasuries and other dollar-denominated assets. This buying pressure causes surges in the DXY.

4. Weakness in Other Currencies Helps Push the DXY Up

Because the DXY measures the dollar’s strength relative to other currencies, weakness in those currencies automatically pushes the index higher.

The Euro’s Role

The euro has the largest weight in the index—around 57%.

Therefore, when the euro weakens due to:

Slow European economic growth

Divergent interest rates

Political challenges

Energy crises

…the DXY often rises significantly.

The Japanese Yen Factor

The yen also plays a major role. When the Bank of Japan keeps interest rates low while the U.S. raises rates, investors shift funds into the dollar, causing the DXY to surge.

5. U.S. Economic Strength and Global Confidence

A strong U.S. economy typically results in a stronger dollar. Economic indicators that support a DXY surge include:

Higher GDP growth

Strong employment numbers

Rising consumer spending

Increasing business investment

Robust corporate earnings

These indicators attract global investors to U.S. assets such as stocks, bonds, and real estate. As foreign investors buy these assets, demand for dollars increases, pushing the DXY upward.

6. Global Trade and Dollar Demand

The U.S. dollar dominates international trade. Over 80% of global transactions, commodities, and trade settlements involve the dollar. This creates a structural, persistent demand for dollars.

Why global trade boosts the DXY:

Countries hold dollar reserves to pay for imports like oil, machinery, and technology.

Most global commodities—including gold, oil, and natural gas—are priced in dollars.

During periods of high commodity demand, nations often increase their dollar reserves.

All of this creates momentum for the DXY to strengthen when global trade dynamics shift.

7. Impact of DXY Surges on Global Markets

A. Impact on Commodities

When the dollar strengthens, commodities like oil, gold, silver, and metals generally become more expensive for buyers using other currencies. As a result, commodity prices often fall when the DXY surges.

B. Impact on Emerging Markets

DXY surges create challenges for emerging markets:

Their currencies weaken

Dollar-denominated debt becomes more expensive to repay

Foreign investment outflows increase

Import costs rise

Some nations experience financial stress during strong dollar periods.

C. Impact on U.S. Corporations

A stronger dollar can hurt U.S. exporters because their products become more expensive internationally. Companies such as technology firms, industrial manufacturers, and consumer goods exporters often feel the pressure of a rising DXY.

8. Market Psychology and Speculative Trading

Financial markets react not just to economic data, but also to sentiment and speculation. Traders in the forex market often accelerate moves in the DXY by:

Betting on future interest rate changes

Reacting to central bank statements

Anticipating geopolitical shifts

Speculating on currency volatility

When sentiment aligns strongly toward a stronger dollar, DXY surges can become sharp and rapid.

9. Are DXY Surges Long-Lasting or Short-Term?

DXY surges can be:

Short-term

Driven by market speculation, sudden news events, or temporary crises.

Long-term

Driven by structural trends such as:

Prolonged interest rate cycles

Shifting global trade patterns

Long-term weakness in other currencies

Robust U.S. economic outperformance

The duration of a surge depends on the underlying forces.

Conclusion

A DXY surge reflects a combination of economic strength, monetary policy decisions, global risk sentiment, and comparative currency performance. When the index rises, it signals confidence in the U.S. economy, but also can indicate stress in global markets. The effects are far-reaching: commodities tend to fall, emerging markets can struggle, and U.S. exporters may face headwinds. Yet for investors seeking safety and stable returns, a surging dollar is often a sign of global capital flowing into the United States.

Understanding why the DXY surges helps traders, policymakers, and investors navigate global markets with greater clarity and insight.

Venture Capital’s Global Impact1. Driving Global Innovation

At its core, venture capital exists to fund innovation. VC firms invest in early-stage businesses that have high growth potential but also high risk—companies that traditional banks or lenders would rarely touch.

This willingness to fund experimentation has brought to life some of the world’s most transformative technologies:

The internet and search engines

Smartphones and mobile applications

Artificial intelligence and machine learning

Electric vehicles and clean energy

Biotechnology and precision medicine

E-commerce and fintech platforms

Without venture capital, many of the revolutionary companies we know today—Google, Facebook, Tesla, Uber, Alibaba, Shopify, and countless others—might never have scaled globally. VC acts as the financial fuel behind groundbreaking ideas, enabling startups to test, iterate, and expand at lightning speed.

2. Boosting Economic Growth and Job Creation

One of the most measurable global impacts of venture capital is economic expansion. VC-backed companies consistently outperform traditional businesses in terms of job creation, revenue growth, and market expansion.

Key economic contributions include:

2.1 Employment Generation

Startups supported by venture capital create millions of high-skill jobs across software development, research, engineering, marketing, and operations. These companies often become large-scale employers once they scale, contributing significantly to national employment figures.

2.2 Creation of New Industries

Entire industries—like ride-sharing, cloud computing, online education, and fintech—were built on VC funding. These sectors not only generate direct jobs but also create large support ecosystems.

2.3 Attracting Global Investments

Countries with strong VC ecosystems attract foreign investors, multinational corporations, and global funds. This strengthens the balance of payments and increases capital inflows.

3. Increasing Global Competitiveness

Venture capital plays a crucial role in helping nations remain competitive in the global innovation race. Countries with robust VC networks—such as the U.S., China, India, Israel, the U.K., and Singapore—are also leaders in cutting-edge technology.

3.1 Encouraging Entrepreneurship

VC fosters a culture where innovation is rewarded, raising the confidence of entrepreneurs to take risks and build new enterprises.

3.2 Commercialization of Research

Universities and research centers often commercialize their technology through venture funding. This bridges the gap between academic research and real-world application, making scientific discoveries accessible to industries.

3.3 Regional Development

In many countries, venture capital helps geographically underdeveloped regions grow by funding startups, incubators, and innovation clusters. Examples include:

Bangalore, India

Shenzhen, China

Tel Aviv, Israel

Berlin, Germany

São Paulo, Brazil

These cities became global tech hubs primarily because venture capital supported entrepreneurs and attracted international talent.

4. Supporting Technological Advancement and Transformation

Technology evolves at a rapid pace, and venture capital ensures that the world keeps moving forward. VC firms not only provide money—they bring mentorship, strategic planning, and global networks that help startups commercialize their innovations.

4.1 Accelerating Disruptive Technologies

VC funding pushes forward technologies such as:

Artificial intelligence

Blockchain and Web3

Robotics and automation

Green energy and sustainability

Space technology

Biotech and genomics

By taking early risks, VC funds encourage breakthroughs that later become everyday tools.

4.2 Redefining Traditional Industries

Venture-backed startups are transforming traditional sectors:

Fintech is reshaping banking.

Edtech is revolutionizing education.

Healthtech is changing medical diagnostics and treatment.

Agri-tech is improving farming efficiency.

Clean-tech is transforming energy and climate solutions.

This disruption leads to greater efficiency, lower costs, and improved services worldwide.

5. Strengthening Global Entrepreneurship Ecosystems

Venture capital has a multiplier effect on entrepreneurship. As startups succeed, founders often reinvest capital and experience into newer ventures, creating a self-sustaining cycle.

5.1 Success Stories Inspire Future Innovators

Global VC successes have encouraged millions to start businesses of their own.

Examples:

Silicon Valley unicorns influenced entrepreneurship in Europe and Asia.

India’s startup boom accelerated after Flipkart and Paytm gained global recognition.

China’s tech giants like Tencent and Alibaba inspired an entire generation of Chinese entrepreneurs.

5.2 Growth of Startup Support Networks

VC involvement leads to the development of:

Incubators

Accelerators

Angel networks

Innovation labs

Entrepreneurial universities

This infrastructure builds long-lasting entrepreneurial ecosystems.

6. Encouraging Globalization and Cross-Border Economies

Venture-capital-backed startups often expand internationally faster than traditional companies. This creates a more connected global marketplace.

6.1 Cross-Border Investments

VC firms frequently invest across borders. U.S. VC firms invest in India, China, and Europe; Asian firms invest in Africa and Latin America. This makes capital global and accessible.

6.2 International Market Expansion

Startups scale globally using VC networks, entering multiple continents in just a few years. This globalization drives economic integration, technology exchange, and cultural connectivity.

6.3 Knowledge Transfer

VC-backed companies bring global expertise—operational strategies, product design, marketing models, and technological know-how—to developing markets.

7. Supporting Social and Environmental Change

In recent years, venture capital has expanded beyond purely profit-driven investments. Many funds now prioritize impact investing, focusing on startups that solve global challenges such as:

Climate change

Renewable energy

Clean mobility

Healthcare access

Food security

Education for all

Impact-driven venture capital is driving innovation in sectors essential for sustainable global development.

8. Creating Wealth and Financial Growth

Venture capital has created massive wealth for founders, investors, and employees. This wealth, in turn, fuels new businesses and supports economic development.

8.1 Building Billion-Dollar Companies

Unicorn startups—those valued at over $1 billion—have become common worldwide. They drive national GDP growth and attract new investments.

8.2 Stock Market Growth

Many venture-backed companies go public through IPOs, contributing to stock market expansion and providing investment opportunities for the broader population.

Conclusion

Venture capital’s global impact extends far beyond funding startups. It is a powerful driver of innovation, economic growth, job creation, global competitiveness, and societal transformation. Through risk-taking and visionary investment, VC has shaped modern technology, transformed industries, and accelerated global development. As the world continues to evolve, venture capital will remain at the forefront of unlocking new opportunities and pushing the boundaries of what is possible.

Shipping, Freight, and Logistics Trading1. Introduction to the Global Shipping and Freight Ecosystem

Shipping and freight represent the physical movement of goods, while logistics covers the planning, coordination, and management that make this movement possible. Together, they form a vast network involving shipping lines, freight forwarders, port operators, customs agents, brokers, and traders. Globalization has made this sector indispensable: 90% of world trade moves through the maritime shipping industry.

Shipping is dominated by large vessels—tankers, container ships, bulk carriers—that transport everything from crude oil and LNG to electronics and automobiles. Freight, meanwhile, includes all modes of transportation—sea, air, road, and rail—often combined in multimodal systems. Logistics integrates these modes into a seamless flow, ensuring timely delivery, cost efficiency, and compliance with regulations.

2. How Shipping and Freight Markets Work

Shipping markets operate on supply and demand. Freight rates rise and fall depending on global trade volumes, vessel availability, fuel prices, geopolitical stability, and port congestion. For example:

When China increases steel production, demand for iron ore shipping rises.

If crude oil prices surge, tanker rates typically move higher.

Geopolitical tensions affecting key routes (like the Suez Canal or Red Sea) can cause disruptions and spike spot freight rates.

Freight markets are divided into two broad categories:

a. Spot Market

This is where vessels are chartered for immediate use. Rates fluctuate daily based on market conditions. Spot trading is common in container shipping and bulk carriers.

b. Contract Market

Long-term contracts (time charters, voyage charters) offer stable pricing and predictable supply. Large corporations rely on these for consistent supply chain operations.

Traders, shipping companies, and brokers constantly analyze these markets to capture opportunities in freight rate movements.

3. Types of Freight: Sea, Air, Road, and Rail

1. Sea Freight

Sea freight is the most cost-effective method for bulk goods. There are three core vessel types:

Dry bulk carriers (coal, grain, iron ore)

Tankers (crude oil, petroleum products, LNG)

Container ships (consumer goods, electronics, machinery)

Shipping trading is most active in this segment due to volatile freight rates.

2. Air Freight

Air freight is used for high-value or time-sensitive goods. It is expensive but essential for pharmaceuticals, electronics, perishables, and emergency shipments.

3. Road Freight

Road transport handles last-mile delivery and short- to medium-distance cargo. Trucking markets also have spot and contract rates influenced by fuel prices and driver availability.

4. Rail Freight

Rail is efficient for heavy industrial cargo—coal, steel, fertilizer, and automobiles. It plays a vital role in countries with large landmass, such as India, China, and the U.S.

4. Logistics: The Strategic Framework Behind Freight

Logistics is the science and strategy behind moving goods. It includes:

Inventory management

Warehousing

Distribution planning

Route optimization

Customs clearance

Packaging

Order fulfillment

Supply chain visibility

Advanced logistics uses technology such as GPS tracking, IoT sensors, warehouse automation, robotics, drones, and AI-driven demand forecasting.

Companies like DHL, FedEx, Maersk Logistics, and UPS are leaders in global logistics, providing end-to-end supply chain solutions.

5. Freight and Shipping Trading Markets

Trading in shipping and freight occurs through:

a. Physical Freight Trading

Actual cargo shipments are bought and sold. Traders negotiate:

Freight rates

Vessel chartering

Cargo booking

Port handling

Physical traders manage logistics for commodities like oil, LNG, coal, metals, grains, and chemicals.

b. Forward Freight Agreements (FFAs)

FFAs are financial instruments used to hedge against future freight rate fluctuations. They cover routes such as:

Baltic Dry Index (BDI)

Capesize, Panamax, Supramax segments

Tanker routes (VLCC, Suezmax, Aframax)

FFAs allow traders, ship owners, and charterers to lock in future freight rates, reducing exposure to volatility. They are settled in cash based on index prices.

c. Container Freight Rate Trading

This segment has grown due to global supply chain disruptions. Indices like:

Freightos Baltic Index (FBX)

Shanghai Containerized Freight Index (SCFI)

allow companies to hedge container shipping costs.

d. Logistics Derivatives

Emerging financial products that allow hedging warehousing costs, trucking rates, and port congestion costs.

6. Key Drivers of Shipping, Freight, and Logistics Prices

1. Global Trade Cycles

Economic expansion increases cargo flows, while recessions reduce demand.

2. Fuel Prices

Bunker fuel costs heavily influence freight rates.

3. Capacity and Fleet Supply

An oversupply of vessels leads to low shipping rates; undercapacity pushes rates up.

4. Geopolitics

Conflicts near major routes (Red Sea, Strait of Hormuz, Taiwan Strait) disrupt shipping lanes.

5. Port Congestion

Delays in ports such as Shanghai, Los Angeles, or Rotterdam cause freight surges.

6. Weather and Natural Disasters

Monsoons, hurricanes, and cyclones affect shipping schedules and capacity.

7. Regulations

IMO emission rules increase operational costs, influencing freight rates.

7. Major Players in Shipping and Logistics Trading

Shipping Lines – Maersk, MSC, CMA CGM, Hapag-Lloyd

Freight Forwarders – DHL Global Forwarding, Kuehne + Nagel

Commodity Traders – Glencore, Trafigura, Vitol, Cargill

Port Operators – DP World, PSA International, Adani Ports

Brokerage Firms – Clarksons, Simpson Spence Young

Logistics Integrators – FedEx, UPS, Maersk Logistics

These players create an interconnected ecosystem facilitating global commerce.

8. How Traders Participate in This Market

Shipping and freight traders engage through:

a. Speculating on Freight Rates

Buying FFAs when expecting rates to rise or selling when expecting a fall.

b. Chartering Vessels

Traders take vessels on time charter and sub-charter them at higher spot rates.

c. Cargo Arbitrage

Buying commodities in cheaper markets and shipping them to higher-priced regions.

d. Operational Trading

Managing logistics for commodity trades to optimize cost and efficiency.

e. Hedging Freight Exposure

Manufacturers and exporters use freight derivatives to lock in shipment costs.

9. Future Trends in Shipping, Freight, and Logistics Trading

1. Digitalization and AI

AI-powered routing, predictive freight pricing, and automated documentation.

2. Green Shipping

Zero-emission fuels such as ammonia, hydrogen, LNG, and methanol will transform operating costs.

3. Blockchain for Documentation

Digital bills of lading reduce fraud and speed up transactions.

4. Autonomous Vessels and Drones

Expected to reduce manpower dependency and increase operational precision.

5. Supply Chain Resilience

Companies are shifting to multi-route strategies after disruptions like COVID-19 and geopolitical tensions.

Conclusion

Shipping, freight, and logistics trading form the circulatory system of the global economy. From physical movement of goods to financial trading of freight derivatives, this sector is essential to global trade, commodity markets, and economic stability. Understanding how freight rates work, how logistics integrates each stage of movement, and how traders participate in these markets provides a powerful foundation for anyone interested in global commerce or financial markets.

Forex Market Analysis1. Understanding Forex Market Dynamics

Before diving into analysis techniques, it’s essential to understand what drives currency movements. In forex, currencies trade in pairs, such as EUR/USD, USD/JPY, or GBP/INR, meaning the value of one currency is always measured against another. Their movement is influenced by:

Economic performance of countries

Interest rate differentials

Geopolitical developments

Trade balances & capital flows

Market sentiment and risk appetite

Forex is inherently complex because it reflects global financial health, investor preferences, and government policies. Hence, sound analysis helps simplify that complexity.

2. Fundamental Analysis in Forex

Fundamental analysis examines the economic, political, and social forces that impact currency values. It focuses on macroeconomic indicators and central bank policies to gauge whether a currency is undervalued or overvalued.

a. Economic Indicators

Traders closely monitor key data releases:

1. GDP (Gross Domestic Product)

A growing economy strengthens its currency because foreign investors move capital into that country.

2. Inflation (CPI & PPI)

Moderate inflation is healthy, but high inflation typically weakens a currency. However, higher inflation may force central banks to raise interest rates, supporting the currency.

3. Employment Data

The U.S. Non-Farm Payrolls (NFP) is the most watched employment report globally. Strong job growth boosts currency strength.

4. Retail Sales & Consumer Confidence

Consumer-driven economies like the U.S. and Eurozone react significantly to spending data.

5. Trade Balance

A country with higher exports than imports (trade surplus) usually sees its currency appreciate as foreign buyers demand that currency.

b. Central Bank Policies

Central banks like the Federal Reserve (Fed), the European Central Bank (ECB), and the Reserve Bank of India (RBI) have enormous influence on forex markets.

Interest Rates

Higher interest rates attract foreign capital, increasing demand for the currency.

Monetary Policy Statements

Statements about inflation, economic growth, or recession potential can cause major volatility, even without actual rate changes.

Quantitative Easing (QE) or Tightening

QE usually weakens a currency; tightening strengthens it.

For example:

Fed Rate Hikes → USD strengthens

ECB dovish signals → EUR weakens

c. Geopolitical Events

Political uncertainty can cause currency depreciation:

Elections

Trade wars

International conflicts

Government instability

Investors often move to safe-haven currencies like USD, CHF, and JPY during uncertain times.

3. Technical Analysis in Forex

Technical analysis studies price charts, historical data, and market patterns to forecast future currency movements. Unlike stock markets, forex markets are highly liquid and more technical in nature, making chart analysis extremely effective.

a. Price Charts

Common chart types:

Candlestick charts (most popular)

Line charts

Bar charts

Candlesticks offer information about market psychology through patterns like:

Bullish engulfing

Doji

Hammer

Shooting star

These patterns help traders identify reversals and continuations.

b. Trend Analysis

Identifying market direction is central to technical analysis:

Uptrend: Higher highs, higher lows

Downtrend: Lower highs, lower lows

Sideways trend: Ranging market

Trendlines, channels, and moving averages help determine momentum and potential breakout points.

c. Technical Indicators

Key indicators used in forex trading include:

1. Moving Averages (MA & EMA)

Used for trend direction and dynamic support/resistance.

50-day and 200-day EMA crosses often signal major trend shifts.

2. RSI (Relative Strength Index)

Measures overbought (>70) and oversold (<30) conditions.

3. MACD (Moving Average Convergence Divergence)

Tracks momentum and helps identify trend reversals.

4. Bollinger Bands

Indicate price volatility; when bands contract, breakouts usually follow.

5. Fibonacci Retracement

Used to identify pullback levels and continuation zones during trends.

d. Chart Patterns

Forex traders heavily rely on chart structures:

Reversal Patterns

Head and shoulders

Double top and bottom

Inverse head and shoulders

Continuation Patterns

Triangles (ascending, descending, symmetrical)

Flags and pennants

Rectangles

Chart patterns help predict price breakout direction and potential targets.

4. Sentiment Analysis

Sentiment analysis captures how traders feel about a currency pair. It reflects crowd psychology and risk appetite.

a. Risk-On vs Risk-Off Behavior

Risk-On: Investors buy higher-yield or riskier currencies (AUD, NZD, emerging markets).

Risk-Off: Investors move to safe-haven currencies (USD, JPY, CHF).

b. Commitment of Traders (COT Report)

Published weekly by the CFTC in the U.S., it shows how institutional traders are positioned—long or short—on major currencies.

c. Market News & Headlines

Breaking news immediately shifts sentiment:

Natural disasters

Political announcements

Sudden policy changes

Sentiment often triggers short-term volatility, even if fundamentals remain stable.

5. Intermarket Analysis in Forex

Currencies are deeply connected to other asset classes:

a. Bonds and Interest Rates

Bond yields strongly influence currencies.

Higher yields → stronger currency.

b. Commodities

Some currencies move with commodities:

CAD with crude oil

AUD with gold and minerals

c. Stock Markets

Strong equity markets attract foreign investment, supporting the domestic currency.

6. Developing a Forex Analysis Strategy

Successful forex traders integrate all three analysis types:

1. Fundamental View

Understand the economic backdrop and long-term direction.

2. Technical Setup

Find entry and exit points using charts, patterns, and indicators.

3. Sentiment Confirmation

Assess whether market mood supports the trade idea.

Example:

If fundamentals signal strong USD,

Technical charts show bullish breakout on USD/INR,

Sentiment moves “Risk-Off”,

→ A long position is valid.

7. Practical Tools for Forex Analysis

1. Economic Calendars

Track upcoming news releases.

2. TradingView & MetaTrader Charts

For chart analysis and indicators.

3. Forex News Platforms

Bloomberg, Reuters, and central bank websites.

4. Volatility Indicators

ATR and VIX (indirectly) help assess risk levels.

8. Importance of Risk Management in Analysis

Even perfect analysis fails without risk control. Forex is highly leveraged; thus:

Always use stop-loss

Avoid over-leveraging

Diversify trades

Respect market volatility

Keep emotions in check

Risk management ensures long-term survival despite inevitable losses.

Conclusion

Forex market analysis is a powerful framework that combines economic understanding, technical expertise, and sentiment reading to interpret currency movements. As the world’s most liquid market, forex responds instantly to global developments, requiring traders to be informed, agile, and analytical. The best results come from blending fundamental views with technical setups and sentiment signals, along with disciplined risk management. With consistent practice and a structured approach, traders can navigate forex markets more confidently and effectively.

Why We Loaded $MSTR at $169 (5:1 Risk/Reward to $355)Have you ever watched a stock pull back 65% and wondered if it was opportunity or disaster?

Have you ever missed a major setup because fear told you to stay away?

This analysis breaks down why NASDAQ:MSTR at $169 presented a textbook geometric retracement opportunity with exceptional risk/reward asymmetry.

Hello ✌️

Spend 3 minutes ⏰ reading this educational breakdown of structure-based position entry.

🎯 Analytical Insight on MSTR

MicroStrategy pulled back from $543 to $169 a 65% retracement that brought price directly into a major accumulation zone. This wasn't random. It aligned perfectly with:

Fibonacci retracement from 2020 lows to 2024 highs

A long-term ascending trendline dating back to 2020

The monthly $112 support zone that held as a floor

Our position entry: $169

Our invalidation level: $131.80 (below structure)

Our first target: $360 (previous resistance zone)

Risk: $37.20 per share

Reward: $191 per share

Ratio: 5.13:1

This setup didn't require predicting the future. It required identifying where risk was defined and reward was probable based on historical price structure.

📚 Educational Section: Why Geometric Retracements Work

The Psychology of Pullbacks

When price drops 65%, most traders experience:

Fear that it will continue falling forever

Doubt about whether the trend is still valid

Paralysis from watching others panic sell

Professional traders see the same chart differently:

Defined risk at structural support

Historical patterns of mean reversion

Favorable asymmetry when risk is small relative to potential reward

The majority fears what professionals buy.

📉 Understanding Market Structure

Markets don't move in straight lines. They:

Trend in one direction (impulse)

Retrace to gather liquidity (correction)

Resume the primary direction (continuation)

The 0.618 to 0.786 retracement zone historically shows the highest probability of reversal in trending assets. Why?

Early sellers have exhausted

Value buyers recognize the discount

Risk can be defined tightly below support

At $169, MSTR offered:

Clear invalidation below $131.80

Multiple timeframe confluence

Structural support from prior consolidation

🎯 Why This Entry Made Sense

Risk Was Defined

Below $169, the next logical support was $131.80. If price broke below that level, the bullish structure would be invalidated. This gave us a clear exit point before entering.

Reward Was Probable

The previous resistance zone at $360 represented a 113% gain from entry. Even a conservative 50% retracement would target $220+, still offering excellent reward.