PLUG long-term TAPLUG has been pumped and dumped pretty hard, but it's not dead, as a matter of fact it has a positive bullish formation on weekly since the last few months, moreover, monthly frame has finally bottomed out for the first time since 2022 and has regained the support level, it's not yet bullish on monthly but it's a significant improvement. Currently, there's a consolidation on mid-term with rising trend strength which is in the formation process of bullish trend continuation.

Also, when assessing their fundamental priorities or incentives, you may want to consider the demand for their products during the AI boom which can be the further trigger for the growth.

Renewableenergy

BW: mid- and long-term bullish trend structure NYSE:BW is evolving within a very bullish macro trend structure, supported by a meaningful business catalyst.

In a broader trend context, as long as price continues to hold above the 50-DMA, I expect bullish momentum to persist, with scope for a move into the next mid-term resistance zone at 15–25.

Chart:

Weekly view:

[ARKO] ARKORA HYDRO TBK (IDX)I dont know much about the fundamental, so this is just my perspective from Technical Aspect.

Disclaimer ON.

Eos Energy Enterprises (EOSE) —Zinc LDES for the AI-Powered GridCompany Overview:

Eos NASDAQ:EOSE builds zinc-based long-duration energy storage (LDES) for utility-scale and commercial use—an alternative to Li-ion with safer chemistry, broader temperature tolerance, and U.S. manufacturing.

Key Catalysts:

AI-Energy Momentum: Major wins include Talen Energy collaboration and a 228 MWh Frontier Power order—validating Z3™ systems for data centers and grid reliability.

Manufacturing Scale-Up: Project AMAZE set to double capacity to 2 GWh by Q4’25, supported by state incentives and an expanding domestic footprint.

Revenue Visibility: Pipeline includes an $18.8B opportunity backlog and $672.5M firm orders, featuring 750 MWh with MN8 Energy—supporting multi-year growth.

Why It Matters:

✔️ Non-Li-ion diversification for utilities and hyperscalers

✔️ U.S.-built supply chain + incentives

✔️ LDES fit for peaker replacement, resiliency, and 24/7 clean power

Investment Outlook:

Bullish above: $12.50–$13.00

Target: $40.00–$42.00 — driven by orders converting to revenue, capacity ramp, and AI/data-center demand for reliable long-duration storage.

📌 EOSE — powering AI-era reliability with zinc-based long duration storage.

SLDP: odds for mid-term top are rising Price has followed the trend structure outlined in the September and October updates, reaching the first level of the key resistance zone.

While risks of a mid-term top formation are rising, as long as price holds above the 21 EMA, a final push higher toward the 10 resistance area remains possible.

Chart:

Previously:

• On resistance and top formation (Oct 6):

from the weekly review:

• On bullish potential and support (Sep 19):

www.tradingview.com

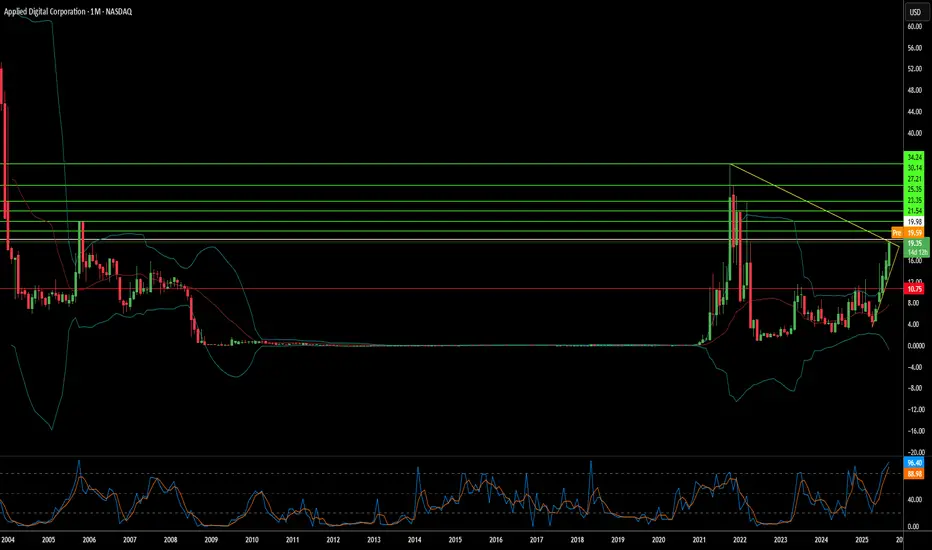

Can a Crypto Miner Become an AI Infrastructure Giant?Applied Digital Corporation has undergone a dramatic transformation, pivoting from cryptocurrency mining infrastructure to become a key player in the rapidly expanding AI data center market. This strategic shift, completed in November 2022, has resulted in extraordinary stock performance with shares surging over 280% in the past year. The company has successfully repositioned itself from serving volatile crypto clients to securing long-term, stable contracts in the high-performance computing (HPC) sector, fundamentally de-risking its business model while capitalizing on the explosive demand for AI infrastructure.

The company's competitive advantage stems from its purpose-built approach to AI data centers, strategically located in North Dakota to leverage natural cooling advantages and access to abundant "stranded power" from renewable sources. Applied Digital's Polaris Forge campus can achieve over 220 days of free cooling annually, significantly outperforming traditional data center locations. This operational efficiency, combined with the ability to utilize otherwise curtailed renewable energy, creates a sustainable cost structure that traditional operators cannot easily replicate through simple retrofitting of existing facilities.

The transformative CoreWeave partnership represents the cornerstone of Applied Digital's growth strategy, with approximately $11 billion in contracted revenue over 15 years for a total capacity of 400 MW. This massive contract provides unprecedented revenue visibility and validates the company's approach to serving AI hyperscalers. The phased buildout schedule, commencing with a 100 MW facility in Q4 2025, provides predictable revenue growth while the company pursues additional hyperscale clients to diversify its customer base.

Despite current financial challenges including negative free cash flow and steep valuation multiples, institutional investors holding 65.67% of the stock demonstrate confidence in the long-term growth narrative. The company's success will ultimately depend on the execution of its buildout plans and ability to capitalize on the projected $165.73 billion AI data center market by 2034. Applied Digital has positioned itself at the intersection of favorable macroeconomic trends, geostrategic advantages, and technological innovation, transforming from a volatile crypto play into a strategic infrastructure provider for the AI revolution.

$MHKI - Inverted Head and Shoulder?So, the chart doesn't really show that it's forming an inverted head and shoulders pattern yet. But if you look at the moving averages, this stock is still above the 10 and 20 moving averages, which means it's still in a decent uptrend on the daily timeframe.

This could be a chance to make a speculative buy with the stop loss mentioned above!

Tradeplan:

Buy 159 - 156

Stoploss < 151

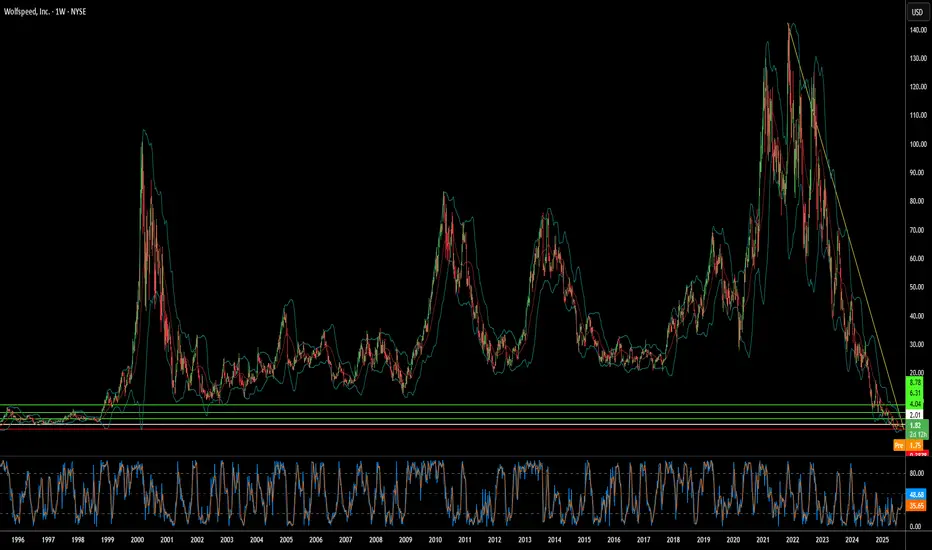

Can Silicon Carbide Save a Bankrupt Chip Giant?Wolfspeed's dramatic 60% stock surge following court approval of its Chapter 11 restructuring plan signals a potential turning point for the struggling semiconductor company. The bankruptcy resolution eliminates 70% of Wolfspeed's $6.5 billion debt burden and reduces interest obligations by 60%, freeing up billions in cash flow for operations and new fabrication facilities. With 97% creditor support backing the plan, investors appear confident that the financial overhang has been cleared, positioning the company for a cleaner emergence from bankruptcy.

The company's recovery prospects are bolstered by its leadership position in silicon carbide (SiC) technology, a critical component for electric vehicles and renewable energy systems. Wolfspeed's unique capability to produce 200mm SiC wafers at scale, combined with its vertically integrated supply chain and substantial patent portfolio, provides competitive advantages in a rapidly growing market. Global EV sales exceeded 17 million units in 2024, with projections of 20-30% annual growth, while each new electric vehicle requires more SiC chips for improved efficiency and faster charging capabilities.

Geopolitical factors further strengthen Wolfspeed's strategic position, with the U.S. CHIPS Act providing up to $750 million in funding for domestic SiC manufacturing capacity. As the U.S. government classifies silicon carbide as critical for national security and clean energy, Wolfspeed's fully domestic supply chain becomes increasingly valuable amid rising export controls and cybersecurity concerns. However, the company faces intensifying competition from well-funded Chinese rivals, including a new Wuhan facility capable of producing 360,000 SiC wafers annually.

Despite these favorable tailwinds, significant risks remain that could derail the recovery. Current shareholders face severe dilution, retaining only 3-5% of the restructured equity, while execution challenges persist regarding ramping the novel 200mm fabrication technology. The company continues operating at a loss with high enterprise value relative to current financial performance, and expanding global SiC capacity from competitors threatens to pressure pricing and market share. Wolfspeed's turnaround represents a high-stakes bet on whether technological leadership and strategic government support can overcome financial restructuring challenges in a competitive marketplace.

Cadeler’s Wind-Powered Surge - €2.5B Backlog to Fuel Growth Cadeler A/S (OB): Riding the Offshore Wind Wave

In a nutshell, what I see is a stock whose price declined by 33% from October 2024 to September 2025, despite the fact that the company is now in a much better position, with better ratios, much better revenue, and great value.

Company Overview

Cadeler A/S is a global leader in offshore wind farm installation and maintenance, primarily operating in European markets. Listed on Oslo Børs, the company operates a fleet of 4 jack-up vessels with 8 additional vessels in development, positioning itself to capitalize on Europe's aggressive renewable energy targets.

Market Opportunity

The offshore wind sector is experiencing a lot of growth. 2024 was a record year with 117 GW of new capacity installed globally. The Global Wind Energy Council forecasts 410 GW of new capacity by 2030, representing annual growth rates of 28% through 2029.

Europe's ambitious targets include 42.5% renewable energy by 2030 and 300 GW of offshore wind capacity by 2050, creating a massive addressable market for Cadeler's specialized services.

Financial Highlights

Strong Revenue Growth: Revenue doubled to €249M in 2024 from €109M in 2023, driven by successful project execution and the Eneti merger. Latest TTM revenue reached €465M (277.9% YoY growth). Q2 2025 revenue grew by 242%, but despite that, the stock price is trending down.

Record Backlog: Order backlog increased to €2.5B in 2024 from €1.7B in 2023, providing strong revenue visibility with key contracts including Baltica 2, Bałtyk 2/3 (Poland), US, and Taiwan 4.

Profitability Surge: EPS grew 409.5% YoY to €0.32 in Q2 2025, with a 3-year CAGR of 61.9%.

2025 Guidance: Management projects €485-525M revenue with €278-318M EBITDA.

Valuation Metrics

P/E Ratio: 6.7 (significantly compressed from the previous year)

P/B Ratio: 1.1 (37.1% decrease YoY)

Revenue CAGR (5-year): 87.6%

The combination of low valuation multiples and exceptional growth suggests potential undervaluation.

Key Risks

Project Execution: Permitting delays and cancellations (e.g., Hornsea 4 removal from backlog) can impact revenue visibility.

Cost Inflation: Rising turbine costs (+10% since 2021) and supply chain constraints could pressure margins.

Policy Dependency: Growth relies heavily on government subsidies and favorable renewable energy policies, creating regulatory risk.

My Investment Thesis

Cadeler is an opportunity in the rapidly expanding offshore wind installation market. They have a strong order backlog and prospective contracts, fleet expansion plans, and attractive valuation metrics; the company appears well-positioned to benefit from Europe's energy transition. I see it as a mix of value and growth investing.

I see Cadeler as a medium to long-term investment. I think the upside potential is anywhere between +50% and +100% from the current price.

I will allocate around 1% of my wealth into this stock.

Quick note: I'm just sharing my journey - not financial advice! 😊

BREN 20/6/25With Danantara focusing on 8 sector points, with one of them is Renewable Energy. IDX:BREN is now very interesting, with the inverted head n shoulder that gave us a reversal signal. BREN is now very cheap, as the 3rd biggest market cap on IDX. #FREEBANDZ

Plug Power: A Mirage or a Miracle?Plug Power (NASDAQ: PLUG), a key innovator in hydrogen energy solutions, recently experienced a significant surge in its stock value. This upturn is largely attributed to a strong vote of confidence from within the company: Chief Financial Officer Paul Middleton substantially increased his stake by acquiring an additional 650,000 shares. This decisive investment, following an earlier purchase, clearly signals robust conviction in Plug Power's future growth trajectory, despite prior market challenges. Analysts also reflect this cautious optimism, with an average one-year price target that suggests a significant upside potential from the current valuation.

A major catalyst for the renewed interest stems from Plug Power's expanded strategic collaboration with Allied Green Ammonia (AGA). This partnership includes a new 2-gigawatt (GW) electrolyzer project in Uzbekistan, part of a substantial $5.5 billion green chemical production facility. This facility will produce sustainable aviation fuel, green urea, and green diesel, positioning Plug Power's technology as foundational to large-scale decarbonization efforts. This initiative, backed by the Government of Uzbekistan, further solidifies a broader 5 GW partnership between Plug Power and AGA across two continents, highlighting the company's capability to deliver industrial-scale green hydrogen solutions.

While these strategic wins are promising, Plug Power continues to navigate financial headwinds. The company has faced recent revenue declines and currently reports significant annual losses and cash burn. To address capital needs, it is seeking shareholder approval to issue more shares. However, the substantial, multi-gigawatt contracts secured, particularly with Allied Green, underscore a strong future revenue pipeline. These projects affirm the critical demand for Plug Power's technology and its pivotal role in the evolving green hydrogen economy, emphasizing that the successful execution of these large-scale ventures will be key to long-term financial stability and sustained growth.

Commodity Outlook: Finding antivenoms in the Year of the SnakeWe are about a month into the Chinese Year of the Snake. The preceding Year of the Dragon (10 February 2024 to 28 January 2025) brought significant momentum to the asset class with broad commodities rising 10%, precious metals rising 36%, industrial metals rising 12%, and even energy and agriculture mustering a late gain (close to 2% each)1. However, the Year of the Snake presents several macro challenges for commodities. Renewed trade protectionism from the US, under the new Trump Administration, is likely to dampen global trade. Additionally, higher bond yields and a strong US dollar create further headwinds for the commodities market. China’s reticence to stimulate big is also holding back the asset class.

Despite these headwinds, we have identified several micro factors that could provide support for certain commodities—what we refer to as our ‘antivenoms’. We remain optimistic about precious metals, aluminium, and European natural gas. Additionally, some of the macroeconomic challenges may ultimately prove less severe than initially anticipated, creating potential upside opportunities for commodities that currently reflect bearish sentiment.

Strong US dollar

The recent strength of the US dollar has historically correlated with weaker commodity prices. While this pattern has been inconsistent post-COVID-19, the dollar's resurgence could once again pressure commodities. Historical data suggests a strong dollar often aligns with declining commodity values.

Trump’s trade policies and market impact

Donald Trump’s return to the presidency introduces uncertainty into trade and commodity markets. Trump's first presidency saw a trade war with China and other nations, negatively impacting global trade and commodity prices. While extreme tariff measures have often been bargaining tactics, the risk of real implementation remains. In his second term, some tariffs were announced and then delayed; at the time of writing, we still have no real guide as to whether they will be implemented or when. This uncertainty is already dampening market sentiment and increasing long-term interest rates, further constraining commodities.

Economic and inflationary concerns

Tariffs could raise inflation in the US while simultaneously depressing global commodity prices due to reduced demand. This dynamic may complicate the Federal Reserve’s (Fed) efforts to control inflation, potentially leading to prolonged high interest rates.

Climate policy reversals

Trump has vowed to withdraw from the Paris Climate Agreement and declared a “national energy emergency,” reversing climate regulations and boosting fossil fuel production. His administration is expected to cancel a $6 billion Department of Energy program aimed at industrial emissions reduction and repeal incentives for electric vehicles. These changes could suppress demand for critical materials used in clean technology, such as base metals.

At the same time, deregulation of oil, gas, and mining operations may increase the supply of key commodities like copper, aluminium, nickel, and cobalt. Major projects, such as Rio Tinto’s copper mine in Arizona, could proceed after years of delays. While immediate production increases are unlikely in 2025, long-term supply growth is possible.

Geopolitical risks and energy markets

A ceasefire between Israel and Hamas, brokered just before Trump's inauguration, has eased some geopolitical risk, though its stability remains uncertain. As we write, a peace deal between Russia and Ukraine is being brokered by the US. Short-term oil price spikes are possible if sanctions are initially tightened to get parties to the negotiating table but, ultimately, we could see easing oil and gas prices if a deal is hashed out.

The US has been pressuring Europe to purchase more American natural gas, but Russia’s LNG shipments to the EU remain significant. A resolution of the Russia-Ukraine war could weaken US leverage in energy negotiations, making Europe less dependent on American gas.

Stricter enforcement of Iranian oil sanctions under Trump could drive oil prices higher. However, OPEC2 members may counteract this by increasing supply, potentially offsetting price gains.

China’s economic strategy and commodity demand

China remains the world’s largest consumer of commodities, yet its recent economic weakness has limited demand growth. Unlike previous economic cycles where China launched large stimulus measures, its current approach focuses on smaller, targeted interventions. The government has stabilised the real estate sector but remains wary of excessive stimulus due to debt concerns.

China is investing heavily in clean technology and renewable energy infrastructure, supporting metal prices despite weak real estate demand. US tariffs on China could accelerate its push toward energy independence, promoting domestic adoption of solar, battery, and electric vehicle technologies.

Trade tensions could escalate into retaliatory actions, such as China restricting exports of critical materials, as seen with gallium, germanium, and graphite in response to semiconductor disputes. Further restrictions could impact global supply chains for energy transition materials.

China’s depreciating Yuan complicates economic policy. The People’s Bank of China has been intervening to stabilise the currency, limiting its ability to cut interest rates. While a policy shift to boost growth led to short-term market gains in 2024, further action remains constrained by currency pressures.

Conclusion

In the Year of the Snake, we are searching for antivenoms to counter the potential threats posed by trade wars, a strong US dollar, and a China that may be unable or unwilling to overcome its economic weakness.

We see strong opportunities in gold, silver, aluminium, copper, zinc and European natural gas, as each of these has compelling drivers that could withstand broader headwinds in the commodity complex.

As policies become clearer, we may find that our fears were overstated, potentially paving the way for a relief rally across the broader commodity complex. Until then, we place our confidence in these antivenoms.

75: Key Levels Amidst Biofuel Plant Construction HaltShell (SHEL) is navigating significant financial and operational challenges. The company recently announced a delay in the construction of its biofuel plant in Rotterdam, which was initially expected to be operational this year but has now been postponed to 2030. This delay has resulted in a financial setback of at least €554 million, potentially escalating to nearly €1 billion, due to technical challenges and unfavorable market conditions.

Given this backdrop, Shell's stock is currently rejecting the key level at 34.315. Here’s what traders should watch:

Bearish Scenario: If Shell loses the current low, we could see a trend change. The new area of interest will be around 32.65, where we anticipate potential support. This level becomes crucial as the market absorbs the financial impact of the delayed biofuel plant and Shell’s strategic adjustments.

Bullish Scenario: If Shell regains the high at 34.315, we should monitor for new highs above 34.745. In this case, we are targeting a high around 36.75, which could sweep liquidity from a monthly high. This bullish momentum could be driven by positive market reactions to any new strategic initiatives Shell undertakes to mitigate the impact of the delay and to capitalize on future regulatory changes in the aviation fuel sector.

The recent halt in the biofuel plant construction adds a layer of complexity to Shell's stock movement. Investors should closely watch these critical levels for potential trading opportunities, considering the broader implications of Shell's operational challenges and market dynamics.

Renewable energy stocks coming back?I saw some other stocks of the same segment doing bullish patterns. We have a potential double bottom fighting with downtrend line resistance. I think is going to bounce back and forward between the 13.5 support level and the downtrend line until something breaks. The double bottom (inverted HS in the daily timeframe) tells me that the price wants to break up the downtrend from September 2022. SL triggers if a weekly candle breaks down and closes under the 13.5 level support.

Bullish Scenario MPLXMPLX Price Targets :

$38.89

$39.91

$45.24

MPLX LP Overview:

MPLX LP is a diversified, large-cap master limited partnership formed by Marathon Petroleum Corporation (MPC). The company owns and operates a wide range of midstream energy infrastructure and logistics assets, in addition to providing fuels distribution services. MPLX's asset portfolio is extensive and includes:

Crude Oil and Refined Product Pipelines: MPLX manages a network of pipelines designed for the transportation of both crude oil and refined petroleum products. These pipelines play a vital role in the distribution of energy resources.

Inland Marine Business: The company is involved in an inland marine business, which likely includes the transportation of energy-related products via inland waterways.

Light-Product Terminals: MPLX owns terminals specifically for handling light petroleum products.

Storage Caverns and Tanks: The company has storage facilities, including caverns, refinery tanks, docks, loading racks, and associated piping for storing energy products.

Crude Oil and Light-Product Marine Terminals: These are terminals used for the efficient transfer of crude oil and light petroleum products.

Gathering Systems and Pipelines: MPLX owns and operates gathering systems and pipelines for both crude oil and natural gas.

Natural Gas and NGL Processing: The company is involved in the processing and fractionation of natural gas and natural gas liquids (NGL) in key U.S. supply basins.

MPLX's business model encompasses various aspects of the midstream energy sector, with a focus on transportation, storage, and processing of energy products. Please note that the status and details of companies can change over time, so for the most current information about MPLX LP, it's advisable to refer to the company's official documents and reports.

VLL volumes are hereVLL.N has seen volumes owing to director buying and renewed interest.

Fundamentally it's been consistently doing well. Shareholder lists back this as some of the funds have taken positions in the recent past in both V and NV shares.

DISCLAIMER : THIS IS BY NO MEANS BUY AND SELL RECOMMENDATION.

RATTAN INDIA POWER - WEEKLY TIME FRAMEThe Structure looks good to us, waiting for this instrument to correct and then give us these opportunities as shown on this instrument (Price Chart).

Note: Its my view only and its for educational purpose only. Only who has got knowledge about this strategy, will understand what to be done on this setup. its purely based on my technical analysis only (strategies). we don't focus on the short term moves, we look for only for Bullish or Bearish Impulsive moves on the setups after a good price action is formed as per the strategy. we never get into corrective moves. because it will test our patience and also it will be a bullish or a bearish trap. and try trade the big moves.

we do not get into bullish or bearish traps. We anticipate and get into only big bullish or bearish moves (Impulsive Moves). Just ride the Bullish or Bearish Impulsive Move. Learn & Know the Complete Market Cycle.

Buy Low and Sell High Concept. Buy at Cheaper Price and Sell at Expensive Price.

Keep it simple, keep it Unique.

please keep your comments useful & respectful.

Thanks for your support....

Tradelikemee Academy

RELIANCE POWER - WEEKLY CHART SETUPThe Structure looks good to us, waiting for this instrument to correct and then give us these opportunities as shown on this instrument (Price Chart).

Note: Its my view only and its for educational purpose only. Only who has got knowledge about this strategy, will understand what to be done on this setup. its purely based on my technical analysis only (strategies). we don't focus on the short term moves, we look for only for Bullish or Bearish Impulsive moves on the setups after a good price action is formed as per the strategy. we never get into corrective moves. because it will test our patience and also it will be a bullish or a bearish trap. and try trade the big moves.

we do not get into bullish or bearish traps. We anticipate and get into only big bullish or bearish moves (Impulsive Moves). Just ride the Bullish or Bearish Impulsive Move. Learn & Know the Complete Market Cycle.

Buy Low and Sell High Concept. Buy at Cheaper Price and Sell at Expensive Price.

Keep it simple, keep it Unique.

please keep your comments useful & respectful.

Thanks for your support....

Tradelikemee Academy

ENPH: Energize Your Investments with a Leading Solar CompanyOne key factor that makes ENPH an attractive investment opportunity is the rapid growth of the solar energy market. According to a report by the International Energy Agency, solar power is expected to become the largest source of electricity by 2035, with a projected compound annual growth rate (CAGR) of 18% from 2020 to 2025. As a leading provider of energy management systems, ENPH is well-positioned to benefit from this trend.

In addition, ENPH has a strong financial position. The company has consistently posted strong revenue growth over the past few years, with a revenue CAGR of 50.4% and 67.8% from 2015 to 2020. Furthermore, the company has a solid balance sheet with no long-term debt and a healthy cash reserve. This financial stability puts ENPH in a strong position to weather any potential economic downturns or market volatility.

Finally, ENPH has a strong track record of innovation and product development. The company has a robust research and development program and has consistently introduced new and innovative products to the market. This positions ENPH to stay ahead of its competitors and to maintain its position as a leader in the solar energy industry.

In summary, ENPH is a strong investment opportunity due to its position in the growing solar energy market, strong financial position, and track record of innovation and product development.

Nordex: Profit Warning from May 2022 underestimated actual costsRECAP: Back in May 25, 2022, Nordex issued a profit warning and its stock was down -17.05%. The new estimates where:

FY2022 PROFIT WARNING ESTIMATES FROM MAY 2022 (Source: Nordex's IR website section):

– FY2022 Consolidated sales: EUR 5.2 to 5.7 billion

– FY2022 EBITDA-margin: minus 4 to 0 percent, including all one-off effects

- Capital expenditure: EUR 180 million

- Working capital ratio: below -7%

In March 31st, 2023 investors got to know the actual figures of the company.

FY2022 ACTUALS (Source: Nordex's IR website section):

– FY2022 Consolidated sales: EUR 5.6936 billion

– FY2022 EBITDA-margin: -4.3%

- Capital expenditure: EUR 204.8 million

- Working capital ratio: -10.2%

Capital expenditure and staff costs were up 21.4% and 18.5%, respectively.

The company suffers from delays in project intakes.

Overall, I reckon Consolidated sales were in the upper boundary of the profit warning but costs increased dramatically, probably due to inflation and related supply-chain issues that are still not fully corrected from China today, in 2023.

Corning Incorporated (GLW) 1M Trading Analisys (TA)Avi Salzman in the Article titled 5 Stocks poised to profit from renewables, published on the February 27, 2023 issue of Barron's, studies these 5 stocks: GLW, ENPH, FREY, NTOIY & SBGSY, I picked the first to share with you my impressions

1M Chart, Corning Incorporated (GLW) :

MACD : On October 2021, the signals on pierced down from above the histogram and have been diving below the histogram since September 2022, at this moment they are getting close to pierce up from below it.

RSI : The signal bounced on September 2022 at 40.00, steadily moving up after softly bounce twice on the 50.00.

PRICE : Has been steadily moving up after bouncing at $29 on September 2022, over the 200MA signal below the 100MA and is pushing to move above this last one where has found quite of resistance before moving toward $40, which is the optimistic approach.

"In this business if you're good, you're right six times out of ten. You're never going to be right nine times out of ten. I've found that when the market's going down and you buy funds wisely, at some point in the future you will be happy. You won't get there by reading: "Now is the time to buy".

Today this ticker has a Volume of 785K, Market Cap of 24B.

This Company PAYS DIVIDENDS TO SHAREHOLDERS (DIVIDENDS YIELD 3.30%)

Corning, Inc. engages in the provision of glass for notebook computers, flat panel desktop monitors, display televisions, and other information display applications, carrier network and enterprise network products for the telecommunications industry, ceramic substrates for gasoline and diesel engines in automotive and heavy-duty vehicle markets, laboratory products for the scientific community and polymer products for biotechnology applications, optical materials for the semiconductor industry and the scientific community, and polycrystalline silicon products and other technologies. The company was founded by Amory Houghton Sr. in 1851 and is headquartered in Corning, NY.

Good Luck!

Avi Salzman en el artículo titulado 5 acciones preparadas para beneficiarse de las energías renovables, publicado en la edición del 27 de febrero de 2023 de Barron's, estudia estas 5 acciones: GLW, ENPH, FREY, NTOIY y SBGSY. Elegí la primera para compartir con ustedes mis impresiones.

Gráfico de 1M, Corning Incorporated (GLW) :

MACD : En octubre de 2021, las señales se cruzaron desde arriba del histograma y han estado sumergiéndose por debajo del mismo desde septiembre de 2022, en este momento se están acercando para cruzarce desde abajo del histograma de manera ascendente.

RSI : La señal rebotó en septiembre de 2022 en 40:00, moviéndose constantemente hacia arriba después de un suave rebote doble en las 50:00.

PRECIO : Ha estado subiendo constantemente después de rebotar en $29 en septiembre de 2022, sobre la señal de 200MA por debajo de la 100MA y está presionando para moverse por encima de esta última donde ha encontrado resistencia antes de moverse a $40, que es el enfoque optimista.

"En este negocio, si eres bueno, tienes razón seis de cada diez veces. Nunca vas a tener razón nueve de cada diez. Descubrí que cuando el mercado está cayendo y compras fondos sabiamente, en algún momento en el futuro serás feliz. Nunca verás un anuncio que diga: "Ahora es el momento de comprar".

Hoy este ticker tiene un Volumen de 785K, Market Cap of 24B.

Esta Empresa PAGA DIVIDENDOS A LOS ACCIONISTAS (RENDIMIENTO POR DIVIDENDO 3.30%)

Corning, Inc. se dedica al suministro de vidrio para computadoras portátiles, monitores de escritorio de pantalla plana, televisores de pantalla y otras aplicaciones de visualización de información, productos de redes empresariales y redes de operadores para la industria de las telecomunicaciones, sustratos cerámicos para motores de gasolina y diesel en automóviles y vehículos pesados. -mercados de vehículos de servicio, productos de laboratorio para la comunidad científica y productos poliméricos para aplicaciones biotecnológicas, materiales ópticos para la industria de semiconductores y la comunidad científica, y productos de silicio policristalino y otras tecnologías. La empresa fue fundada por Amory Houghton Sr. en 1851 y tiene su sede en Corning, Nueva York.

¡Buena suerte!

“I believe in analysis and not forecasting.” / "Creo en el análisis y no en el pronóstico".

REMEMBER : I am not a financial adviser nor is any content in this article presented as financial advice. The information provided in this blog post and any other posts that I make, and any accompanying material is for informational purposes only. It should not be considered financial or investment advice of any kind. One should consult with a financial or investment professional to determine what may be best for your individual needs. RECUERDE : No soy un asesor financiero y el contenido de este artículo no se presenta como asesoramiento financiero. La información provista en esta publicación de blog y cualquier otra publicación que haga y cualquier material que la acompaña es solo para fines informativos. No debe considerarse asesoramiento financiero o de inversión de ningún tipo. Se debe consultar con un profesional financiero o de inversiones para determinar qué es lo mejor para sus necesidades individuales.

Long First SolarSolar energy is one of the leading technologies in the renewable energy industry. It is slowly eating away the oil industry's market share in energy production. Through economies of scale, the cost per unit decreased significantly over the past decade so there is a chance that First Solar might eventually break its all time high.

From a technical standpoint it is on a nice uptrend. I would buy some shares now then buy any dips above the uptrend.

$178M mkt cap company signed $545 Million Partnering AgreementCup & Handle breakout as this company is getting re-rated after recent news release...

Green Impact Partners Announces $545 Million Partnering Agreement

Calgary, Alberta--(Newsfile Corp. - February 21, 2023) - Green Impact Partners Inc. (TSXV: GIP) ("GIP" or the "Company") is pleased to announce it has selected Amber Infrastructure Group ("Amber Infrastructure") as a strategic partner on its GreenGas Colorado, Iowa RNG and Future Energy Park projects, representing up to $545 million in total investment for a 50% project-level equity interest in each facility. Based in London, with offices in North America, Europe and Australia, Amber Infrastructure is an infrastructure investor with over $8 billion in assets under management.

All of the documentation for the various agreements with Amber Infrastructure is being held in escrow and will be released and come into effect upon Amber Infrastructure advancing the purchase proceeds under the unit purchase agreement in respect of the GreenGas transaction described below, which is anticipated to occur on February 23, 2023.