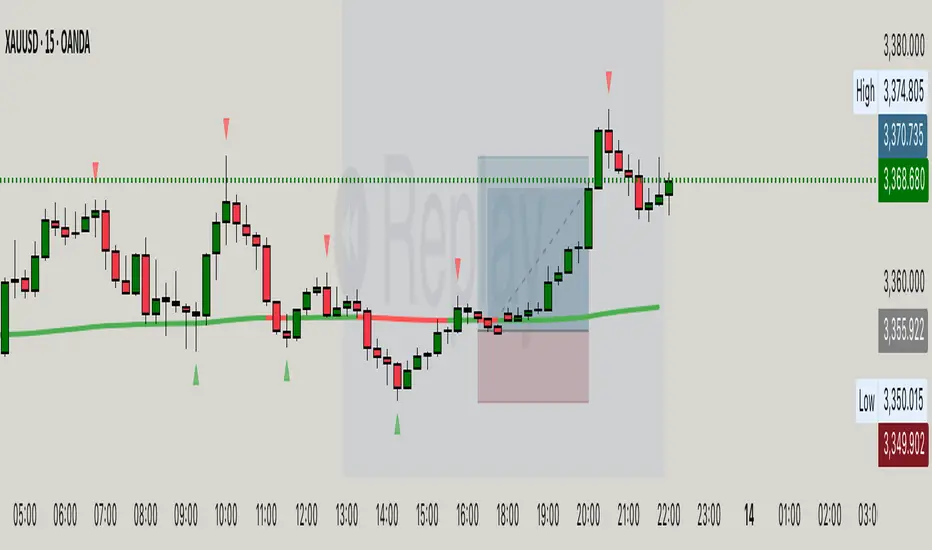

Hassi XAUUSD Advanced FVG EMA/BOS/RSI/Volume + Session FilterWhat it does :

This strategy automates a popular ICT-style idea on XAUUSD (Gold): trade only when price taps back into a Fair Value Gap (FVG), but filter entries with trend, structure, momentum, volume, and session rules. It manages risk with fixed TP/SL (points) and shows a compact backtest panel on chart.

Core Logic

1) Market Structure (BOS)

Detects recent swing highs/lows and flags a Break of Structure:

BOS Up when price breaks the latest swing high.

BOS Down when price breaks the latest swing low.

2) FVG Detection (3-candle)

Bullish FVG when low > high and low > high .

Bearish FVG when high < low and high < low .

The most recent qualifying gap is drawn as a shaded box (optional).

3) Bias & Filters

Trend Bias: price vs EMA (default 200). Longs only above EMA; shorts only below.

Momentum: optional RSI filter (default 14); avoid longs in OB & shorts in OS.

Volume: optional filter requiring current volume > SMA(20) × multiplier.

Sessions: optional London / New York (PKT) time windows.

Entries & Exits

Long Entry (all must be true)

Above EMA, RSI bullish, volume ok, session ok, BOS Up.

A recent Bullish FVG exists (within N bars).

Price taps back into the FVG (low ≤ top & close > bottom) with a bullish candle.

Short Entry (mirror)

Below EMA, RSI bearish, volume ok, session ok, BOS Down.

A recent Bearish FVG exists (within N bars).

Price taps (high ≥ bottom & close < top) with a bearish candle.

Risk / R:R

Exits use fixed points on XAUUSD (default TP 100, SL 50).

On many gold feeds 1.0 = 10 points; inputs convert to price automatically.

“One-trade-at-a-time”: a new signal won’t fire until the previous position is flat.

Chart Labels

On entry, the script plots BUY/SELL plus fixed TP/SL lines & labels anchored to the entry bar (they don’t drift with price).

Visuals & Tools

EMA line (green/red by bias).

Swing points (tiny triangles) to see structure.

FVG boxes (green/red, optional).

Session shading (subtle blue overlay).

Stats Panel (top-right):

Total Trades, TP Hits, SL Hits, Win Rate, Profit Factor, Net P&L.

Inputs (quick guide)

EMA Length (default 200)

Swing Lookback for BOS (default 5)

FVG Box Length (how far the zone extends to the right)

TP / SL (points) for XAUUSD + display Risk:Reward

Sessions (PKT): London & New York windows + toggle

Filters: Volume (multiplier), RSI (length, OB/OS)

Visibility: show/hide FVG boxes & TP/SL drawings

Alerts

Buy Signal / Sell Signal on valid entries

Position Opened / Position Closed notifications

Best Practices & Notes

Designed for XAUUSD 15-minute. You can test other timeframes, but retune TP/SL points and filters accordingly.

Broker ticks differ: if your symbol steps are not 0.1, adjust TP/SL points.

Use with a HTF confluence (e.g., D1/4H bias, key S/R, news awareness).

Backtests are approximations; real results vary with spreads, slippage, and execution.

Disclaimer: This tool is for educational purposes. It is not financial advice. Always test before using on live capital.

Search in scripts for "BOS"

BO - RSI - M5 BacktestingBO - RSI - M5 Backtesting -Rule of Strategy

A. Data

1. Chart M5 IDC

2. Symbol: EURJPY

B. Indicator

1. RSI

2. Length: 12 (adjustable)

3. Extreme Top: 75 (adjustable)

4. Extreme Bottom: 25 (adjustable)

C. Rule of Signal

1. Put Signal

* Rsi create a temporary peak over Extreme Top

row61: peak_rsi= rsi >rsi and rsi >rsi and rsi rsi_top

2. Call Signal

* Rsi create a temporary bottom under Extreme Bottom

row62: bott_rsi= rsi rsi and rsi

BO - Bar's direction Signal - BacktestingBO - Bar's direction Signal - Backtesting Options:

A. Factors Calculate probability of x bars same direction

1. Periods Counting: Data to count From day/month/year To day/month/year

2. Trading Time: only cases occurred in trading time were counted.

B. Timezone

1. Trading time depend on Time zone and specified chart.

2. Enable Highlight Trading Time to check your period time is correct

C. Date Backtesting

* Only cases occurred in Date Backtesting were reported.

D. Setup Options & Rule

1. Reversal after 2 bars same direction

* Probability of 3 bars same direction < 50

* 2 bars same direction is start of series

2. Reversal after 3 bars same direction

* Probability of 4 bars same direction < 50

* 3 bars same direction is start of series

3. Reversal after 4 bars same direction

* Probability of 4 bars same direction < 50

* 3 bars same direction is start of series

4. Reversal after 5 bars same direction

* Probability of 5 bars same direction < 50

* 4 bars same direction is start of series

5. Reversal after 6 bars same direction

* Probability of 6 bars same direction < 50

* 5 bars same direction is start of series

Liquidity Sweep + BOS Retest System — Prop Firm Edition🟦 Liquidity Sweep + BOS Retest System — Prop Firm Edition

A High-Probability Smart Money Strategy Built for NQ, ES, and Funding Accounts

🚀 Overview

The Liquidity Sweep + BOS Retest System (Prop Firm Edition) is a precision-engineered SMC strategy built specifically for prop firm traders. It mirrors institutional liquidity behavior and combines it with strict account-safe entry rules to help traders pass and maintain funding accounts with consistency.

Unlike typical indicators, this system waits for three confirmations — liquidity sweep, displacement, and a clean retest — before executing any trade. Every component is optimized for low drawdown, high R:R, and prop-firm-approved risk management.

Whether you’re trading Apex, TakeProfitTrader, FFF, or OneUp Trader, this system gives you a powerful mechanical framework that keeps you within rules while identifying the market’s highest-probability reversal zones.

🔥 Key Features

1. Liquidity Sweep Detection (Stop Hunt Logic)

Automatically identifies when price clears a previous swing high/low with a sweep confirmation candle.

✔ Filters noise

✔ Eliminates early entries

✔ Locks onto true liquidity grabs

2. Automatic Break of Structure (BOS) Confirmation

Price must show true displacement by breaking structure opposite the sweep direction.

✔ Confirms momentum shift

✔ Removes fake reversals

✔ Ensures institutional intent

3. Precision Retest Entry Model

The strategy enters only when price retests the BOS level at premium/discount pricing.

✔ Zero chasing

✔ Extremely tight stop loss placement

✔ Prop-firm-friendly controlled risk

4. Built-In Risk & Trade Management

SL set at swept liquidity

TP set by user-defined R:R multiplier

Optional session filter (NY Open by default)

One trade at a time (no pyramiding)

Automatically resets logic after each trade

This prevents overtrading — the #1 cause of evaluation and account breaches.

5. Designed for Prop Firm Futures Trading

This script is optimized for:

Trailing/static drawdown accounts

Micro contract precision

Funding evaluations

Low-risk, high-probability setups

Structured, rule-based execution

It reduces randomness and emotional trading by automating the highest-quality SMC sequence.

🎯 The Trading Model Behind the System

Step 1 — Liquidity Sweep

Price must take out a recent high/low and close back inside structure.

This confirms stop-hunting behavior and marks the beginning of a potential reversal.

Step 2 — BOS (Break of Structure)

Price must break the opposite side swing with a displacement candle. This validates a directional shift.

Step 3 — Retest Entry

The system waits for price to retrace into the BOS level and signal continuation.

This creates optimal R:R entry with minimal drawdown.

📈 Best Markets

NQ (NASDAQ Futures) – Highly recommended

ES, YM, RTY

Gold (XAUUSD)

FX majors

Crypto (with high volatility)

Works best on 1m, 2m, 5m, or 15m depending on your trading style.

🧠 Why Traders Love This System

✔ No signals until all confirmations align

✔ Reduces overtrading and emotional decisions

✔ Follows market structure instead of random indicators

✔ Perfect for maintaining long-term funded accounts

✔ Built around institutional-grade concepts

✔ Makes your trading consistent, calm, and rules-based

⚙️ Recommended Settings

Session: 06:30–08:00 MST (NY Open)

R:R: 1.5R – 3R

Contracts: Start with 1–2 micros

Markets: NQ for best structure & volume

📦 What’s Included

Complete strategy logic

All plots, labels, sweep markers & BOS alerts

BOS retest entry automation

Session filtering

Stop loss & take profit system

Full SMC logic pipeline

🏁 Summary

The Liquidity Sweep + BOS Retest System is a complete, prop-firm-ready, structure-based strategy that automates one of the cleanest and most reliable SMC entry models. It is designed to keep you safe, consistent, and rule-compliant while capturing premium institutional setups.

If you want to trade with confidence, discipline, and prop-firm precision — this system is for you.

Good Luck -BG

XAUUSD 1m SMC Zones (BOS + Flexible TP Modes + Trailing Runner)//@version=6

strategy("XAUUSD 1m SMC Zones (BOS + Flexible TP Modes + Trailing Runner)",

overlay = true,

initial_capital = 10000,

pyramiding = 10,

process_orders_on_close = true)

//━━━━━━━━━━━━━━━━━━━

// 1. INPUTS

//━━━━━━━━━━━━━━━━━━━

// TP / SL

tp1Pips = input.int(10, "TP1 (pips)", minval = 1)

fixedSLpips = input.int(50, "Fixed SL (pips)", minval = 5)

runnerRR = input.float(3.0, "Runner RR (TP2 = SL * RR)", step = 0.1, minval = 1.0)

// Daily risk

maxDailyLossPct = input.float(5.0, "Max daily loss % (stop trading)", step = 0.5)

maxDailyProfitPct = input.float(20.0, "Max daily profit % (stop trading)", step = 1.0)

// HTF S/R (1H)

htfTF = input.string("60", "HTF timeframe (minutes) for S/R block")

// Profit strategy (Option C)

profitStrategy = input.string("Minimal Risk | Full BE after TP1", "Profit Strategy", options = )

// Runner stop mode (your option 4)

runnerStopMode = input.string( "BE only", "Runner Stop Mode", options = )

// ATR trail settings (only used if ATR mode selected)

atrTrailLen = input.int(14, "ATR Length (trail)", minval = 1)

atrTrailMult = input.float(1.0, "ATR Multiplier (trail)", step = 0.1, minval = 0.1)

// Pip size (for XAUUSD: 1 pip = 0.10 if tick = 0.01)

pipSize = syminfo.mintick * 10.0

tp1Points = tp1Pips * pipSize

slPoints = fixedSLpips * pipSize

baseQty = input.float (1.0, "Base order size" , step = 0.01, minval = 0.01)

//━━━━━━━━━━━━━━━━━━━

// 2. DAILY RISK MANAGEMENT

//━━━━━━━━━━━━━━━━━━━

isNewDay = ta.change(time("D")) != 0

var float dayStartEquity = na

var bool dailyStopped = false

equityNow = strategy.initial_capital + strategy.netprofit

if isNewDay or na(dayStartEquity)

dayStartEquity := equityNow

dailyStopped := false

dailyPnL = equityNow - dayStartEquity

dailyPnLPct = dayStartEquity != 0 ? (dailyPnL / dayStartEquity) * 100.0 : 0.0

if not dailyStopped

if dailyPnLPct <= -maxDailyLossPct

dailyStopped := true

if dailyPnLPct >= maxDailyProfitPct

dailyStopped := true

canTradeToday = not dailyStopped

//━━━━━━━━━━━━━━━━━━━

// 3. 1H S/R ZONES (for direction block)

//━━━━━━━━━━━━━━━━━━━

htOpen = request.security(syminfo.tickerid, htfTF, open)

htHigh = request.security(syminfo.tickerid, htfTF, high)

htLow = request.security(syminfo.tickerid, htfTF, low)

htClose = request.security(syminfo.tickerid, htfTF, close)

// Engulf logic on HTF

htBullPrev = htClose > htOpen

htBearPrev = htClose < htOpen

htBearEngulf = htClose < htOpen and htBullPrev and htOpen >= htClose and htClose <= htOpen

htBullEngulf = htClose > htOpen and htBearPrev and htOpen <= htClose and htClose >= htOpen

// Liquidity sweep on HTF previous candle

htSweepHigh = htHigh > ta.highest(htHigh, 5)

htSweepLow = htLow < ta.lowest(htLow, 5)

// Store last HTF zones

var float htResHigh = na

var float htResLow = na

var float htSupHigh = na

var float htSupLow = na

if htBearEngulf and htSweepHigh

htResHigh := htHigh

htResLow := htLow

if htBullEngulf and htSweepLow

htSupHigh := htHigh

htSupLow := htLow

// Are we inside HTF zones?

inHtfRes = not na(htResHigh) and close <= htResHigh and close >= htResLow

inHtfSup = not na(htSupLow) and close >= htSupLow and close <= htSupHigh

// Block direction against HTF zones

longBlockedByZone = inHtfRes // no buys in HTF resistance

shortBlockedByZone = inHtfSup // no sells in HTF support

//━━━━━━━━━━━━━━━━━━━

// 4. 1m LOCAL ZONES (LIQUIDITY SWEEP + ENGULF + QUALITY SCORE)

//━━━━━━━━━━━━━━━━━━━

// 1m engulf patterns

bullPrev1 = close > open

bearPrev1 = close < open

bearEngulfNow = close < open and bullPrev1 and open >= close and close <= open

bullEngulfNow = close > open and bearPrev1 and open <= close and close >= open

// Liquidity sweep by previous candle on 1m

sweepHighPrev = high > ta.highest(high, 5)

sweepLowPrev = low < ta.lowest(low, 5)

// Local zone storage (one active support + one active resistance)

// Quality score: 1 = engulf only, 2 = engulf + sweep (we only trade ≥2)

var float supLow = na

var float supHigh = na

var int supQ = 0

var bool supUsed = false

var float resLow = na

var float resHigh = na

var int resQ = 0

var bool resUsed = false

// New resistance zone: previous bullish candle -> bear engulf

if bearEngulfNow

resLow := low

resHigh := high

resQ := sweepHighPrev ? 2 : 1

resUsed := false

// New support zone: previous bearish candle -> bull engulf

if bullEngulfNow

supLow := low

supHigh := high

supQ := sweepLowPrev ? 2 : 1

supUsed := false

// Raw "inside zone" detection

inSupRaw = not na(supLow) and close >= supLow and close <= supHigh

inResRaw = not na(resHigh) and close <= resHigh and close >= resLow

// QUALITY FILTER: only trade zones with quality ≥ 2 (engulf + sweep)

highQualitySup = supQ >= 2

highQualityRes = resQ >= 2

inSupZone = inSupRaw and highQualitySup and not supUsed

inResZone = inResRaw and highQualityRes and not resUsed

// Plot zones

plot(supLow, "Sup Low", color = color.new(color.lime, 60), style = plot.style_linebr)

plot(supHigh, "Sup High", color = color.new(color.lime, 60), style = plot.style_linebr)

plot(resLow, "Res Low", color = color.new(color.red, 60), style = plot.style_linebr)

plot(resHigh, "Res High", color = color.new(color.red, 60), style = plot.style_linebr)

//━━━━━━━━━━━━━━━━━━━

// 5. MODERATE BOS (3-BAR FRACTAL STRUCTURE)

//━━━━━━━━━━━━━━━━━━━

// 3-bar swing highs/lows

swHigh = high > high and high > high

swLow = low < low and low < low

var float lastSwingHigh = na

var float lastSwingLow = na

if swHigh

lastSwingHigh := high

if swLow

lastSwingLow := low

// BOS conditions

bosUp = not na(lastSwingHigh) and close > lastSwingHigh

bosDown = not na(lastSwingLow) and close < lastSwingLow

// Zone “arming” and BOS validation

var bool supArmed = false

var bool resArmed = false

var bool supBosOK = false

var bool resBosOK = false

// Arm zones when first touched

if inSupZone

supArmed := true

if inResZone

resArmed := true

// BOS after arming → zone becomes valid for entries

if supArmed and bosUp

supBosOK := true

if resArmed and bosDown

resBosOK := true

// Reset BOS flags when new zones are created

if bullEngulfNow

supArmed := false

supBosOK := false

if bearEngulfNow

resArmed := false

resBosOK := false

//━━━━━━━━━━━━━━━━━━━

// 6. ENTRY CONDITIONS (ZONE + BOS + RISK STATE)

//━━━━━━━━━━━━━━━━━━━

flatOrShort = strategy.position_size <= 0

flatOrLong = strategy.position_size >= 0

longSignal = canTradeToday and not longBlockedByZone and inSupZone and supBosOK and flatOrShort

shortSignal = canTradeToday and not shortBlockedByZone and inResZone and resBosOK and flatOrLong

//━━━━━━━━━━━━━━━━━━━

// 7. ORDER LOGIC – TWO PROFIT STRATEGIES

//━━━━━━━━━━━━━━━━━━━

// Common metrics

atrTrail = ta.atr(atrTrailLen)

// MINIMAL MODE: single trade, BE after TP1, optional trailing

// HYBRID MODE: two trades (Scalp @ TP1, Runner @ TP2)

// Persistent tracking

var float longEntry = na

var float longTP1 = na

var float longTP2 = na

var float longSL = na

var bool longBE = false

var float longRunEntry = na

var float longRunTP1 = na

var float longRunTP2 = na

var float longRunSL = na

var bool longRunBE = false

var float shortEntry = na

var float shortTP1 = na

var float shortTP2 = na

var float shortSL = na

var bool shortBE = false

var float shortRunEntry = na

var float shortRunTP1 = na

var float shortRunTP2 = na

var float shortRunSL = na

var bool shortRunBE = false

isMinimal = profitStrategy == "Minimal Risk | Full BE after TP1"

isHybrid = profitStrategy == "Hybrid | Scalp TP + Runner TP"

//━━━━━━━━━━ LONG ENTRIES ━━━━━━━━━━

if longSignal

if isMinimal

longEntry := close

longSL := longEntry - slPoints

longTP1 := longEntry + tp1Points

longTP2 := longEntry + slPoints * runnerRR

longBE := false

strategy.entry("Long", strategy.long)

supUsed := true

supArmed := false

supBosOK := false

else if isHybrid

longRunEntry := close

longRunSL := longRunEntry - slPoints

longRunTP1 := longRunEntry + tp1Points

longRunTP2 := longRunEntry + slPoints * runnerRR

longRunBE := false

// Two separate entries, each 50% of baseQty (for backtest)

strategy.entry("LongScalp", strategy.long, qty = baseQty * 0.5)

strategy.entry("LongRun", strategy.long, qty = baseQty * 0.5)

supUsed := true

supArmed := false

supBosOK := false

//━━━━━━━━━━ SHORT ENTRIES ━━━━━━━━━━

if shortSignal

if isMinimal

shortEntry := close

shortSL := shortEntry + slPoints

shortTP1 := shortEntry - tp1Points

shortTP2 := shortEntry - slPoints * runnerRR

shortBE := false

strategy.entry("Short", strategy.short)

resUsed := true

resArmed := false

resBosOK := false

else if isHybrid

shortRunEntry := close

shortRunSL := shortRunEntry + slPoints

shortRunTP1 := shortRunEntry - tp1Points

shortRunTP2 := shortRunEntry - slPoints * runnerRR

shortRunBE := false

strategy.entry("ShortScalp", strategy.short, qty = baseQty * 50)

strategy.entry("ShortRun", strategy.short, qty = baseQty * 50)

resUsed := true

resArmed := false

resBosOK := false

//━━━━━━━━━━━━━━━━━━━

// 8. EXIT LOGIC – MINIMAL MODE

//━━━━━━━━━━━━━━━━━━━

// LONG – Minimal Risk: 1 trade, BE after TP1, runner to TP2

if isMinimal and strategy.position_size > 0 and not na(longEntry)

// Move to BE once TP1 is touched

if not longBE and high >= longTP1

longBE := true

// Base SL: BE or initial SL

float dynLongSL = longBE ? longEntry : longSL

// Optional trailing after BE

if longBE

if runnerStopMode == "Structure trail" and not na(lastSwingLow) and lastSwingLow > longEntry

dynLongSL := math.max(dynLongSL, lastSwingLow)

if runnerStopMode == "ATR trail"

trailSL = close - atrTrailMult * atrTrail

dynLongSL := math.max(dynLongSL, trailSL)

strategy.exit("Long Exit", "Long", stop = dynLongSL, limit = longTP2)

// SHORT – Minimal Risk: 1 trade, BE after TP1, runner to TP2

if isMinimal and strategy.position_size < 0 and not na(shortEntry)

if not shortBE and low <= shortTP1

shortBE := true

float dynShortSL = shortBE ? shortEntry : shortSL

if shortBE

if runnerStopMode == "Structure trail" and not na(lastSwingHigh) and lastSwingHigh < shortEntry

dynShortSL := math.min(dynShortSL, lastSwingHigh)

if runnerStopMode == "ATR trail"

trailSLs = close + atrTrailMult * atrTrail

dynShortSL := math.min(dynShortSL, trailSLs)

strategy.exit("Short Exit", "Short", stop = dynShortSL, limit = shortTP2)

//━━━━━━━━━━━━━━━━━━━

// 9. EXIT LOGIC – HYBRID MODE

//━━━━━━━━━━━━━━━━━━━

// LONG – Hybrid: Scalp + Runner

if isHybrid

// Scalp leg: full TP at TP1

if strategy.opentrades > 0

strategy.exit("LScalp TP", "LongScalp", stop = longRunSL, limit = longRunTP1)

// Runner leg

if strategy.position_size > 0 and not na(longRunEntry)

if not longRunBE and high >= longRunTP1

longRunBE := true

float dynLongRunSL = longRunBE ? longRunEntry : longRunSL

if longRunBE

if runnerStopMode == "Structure trail" and not na(lastSwingLow) and lastSwingLow > longRunEntry

dynLongRunSL := math.max(dynLongRunSL, lastSwingLow)

if runnerStopMode == "ATR trail"

trailRunSL = close - atrTrailMult * atrTrail

dynLongRunSL := math.max(dynLongRunSL, trailRunSL)

strategy.exit("LRun TP", "LongRun", stop = dynLongRunSL, limit = longRunTP2)

// SHORT – Hybrid: Scalp + Runner

if isHybrid

if strategy.opentrades > 0

strategy.exit("SScalp TP", "ShortScalp", stop = shortRunSL, limit = shortRunTP1)

if strategy.position_size < 0 and not na(shortRunEntry)

if not shortRunBE and low <= shortRunTP1

shortRunBE := true

float dynShortRunSL = shortRunBE ? shortRunEntry : shortRunSL

if shortRunBE

if runnerStopMode == "Structure trail" and not na(lastSwingHigh) and lastSwingHigh < shortRunEntry

dynShortRunSL := math.min(dynShortRunSL, lastSwingHigh)

if runnerStopMode == "ATR trail"

trailRunSLs = close + atrTrailMult * atrTrail

dynShortRunSL := math.min(dynShortRunSL, trailRunSLs)

strategy.exit("SRun TP", "ShortRun", stop = dynShortRunSL, limit = shortRunTP2)

//━━━━━━━━━━━━━━━━━━━

// 10. RESET STATE WHEN FLAT

//━━━━━━━━━━━━━━━━━━━

if strategy.position_size == 0

longEntry := na

shortEntry := na

longBE := false

shortBE := false

longRunEntry := na

shortRunEntry := na

longRunBE := false

shortRunBE := false

//━━━━━━━━━━━━━━━━━━━

// 11. VISUAL ENTRY MARKERS

//━━━━━━━━━━━━━━━━━━━

plotshape(longSignal, title = "Long Signal", style = shape.triangleup,

location = location.belowbar, color = color.lime, size = size.tiny, text = "L")

plotshape(shortSignal, title = "Short Signal", style = shape.triangledown,

location = location.abovebar, color = color.red, size = size.tiny, text = "S")

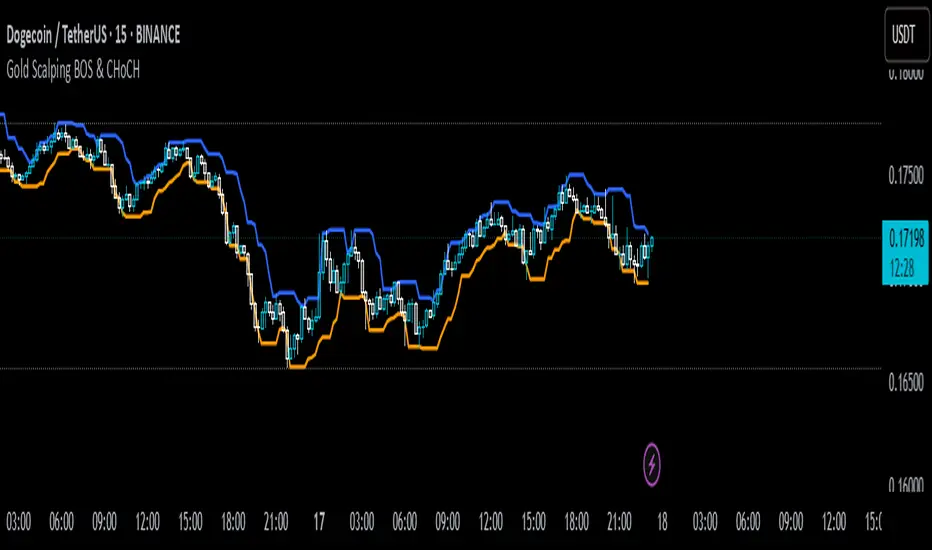

Gold Scalping BOS & CHoCHThis strategy is designed for scalping gold (XAU/USD) on the 3-minute timeframe, utilizing Break of Structure (BOS) and Change of Character (CHoCH) to identify high-probability trade setups. Unlike traditional SMA crossover strategies, this method focuses purely on price action and market structure shifts, allowing for early entries and better risk management.

Core Concepts:

Break of Structure (BOS) – Confirms a continuation of the trend when price breaks the last swing high (bullish) or last swing low (bearish).

Change of Character (CHoCH) – Detects possible trend reversals by identifying a shift in market momentum.

Dynamic Support & Resistance – Uses the last 10-bar highs and lows to determine adaptive stop-loss (SL) and take-profit (TP) levels.

Risk-to-Reward Ratio (1:2 RR) – Ensures trades are executed with a favorable risk/reward ratio.

Entry Conditions:

Buy Entry:

BOS (Bullish) confirmed (price breaks the previous swing high).

CHoCH (Bullish) confirms trend shift.

Price crosses back above the last swing low (confirmation of support).

Sell Entry:

BOS (Bearish) confirmed (price breaks the previous swing low).

CHoCH (Bearish) confirms trend shift.

Price crosses back below the last swing high (confirmation of resistance).

Exit Conditions:

Stop Loss (SL): Set at the most recent dynamic support (for buys) or resistance (for sells).

Take Profit (TP): 2x the risk (1:2 risk-reward ratio).

Advantages of This Strategy:

✅ No lagging indicators – Uses price action for real-time entries.

✅ High probability setups – Focuses only on strong structural breaks.

✅ Adaptive SL/TP – Uses real market structure instead of fixed values.

✅ Optimized for Scalping – Best suited for quick in-and-out trades.

Best Time to Trade:

🔹 London & New York Sessions (High volatility for gold).

4H Confirmation + 1H SFP BOS Retest4H Confirmation + 1H Entry (SFP + BOS + Retest)Run it on 1H

Uses 4H EMAs for higher-timeframe direction (confirmation)

Uses 1H SFP + BOS + retest + RSI for entries

This gives you more trades, still guided by the 4H trend

SMC Pro [Stansbooth]

🔮 SMC × Fibonacci Confluence Engine — The Hidden Algorithm of the Markets

Welcome to a level of chart analysis where mathematics , market psychology , and institutional logic merge into one ultra-intelligent system.

This indicator decodes the true structure of price delivery by combining Smart Money Concepts with the timeless precision of Fibonacci ratios , revealing what retail traders can’t see — *the algorithmic heartbeat of the market*.

✨ What Makes This Indicator Different

Instead of drawing random lines or reacting to late signals, this tool **anticipates** market behavior by reading the footprints left behind by institutional algorithms. Every element is placed with purpose — every zone, every shift, every fib level — all forming a seamless narrative that explains *why* price moves the way it does.

🔥 Core Intelligence Features

Advanced BOS/CHOCH Auto-Detection — Spot structure shifts before momentum even forms.

Institutional Liquidity Mapping

— Identify liquidity pools, engineered sweeps, equal highs/lows, and trap zones designed by smart money.

Fibonacci-Aligned Precision Zones

— Auto-generated fib grids synced with SMC levels for pinpoint reversal and continuation setups.

Imbalance Engine

— FVGs, displacement, inefficiencies, and mitigation blocks displayed with crystal clarity.

Premium/Discount Algorithm

— Understand instantly whether price is in a zone of accumulation or distribution.

🚀 Designed for Traders Who Want an Edge

Whether you're scalping fast moves, capturing intraday swings, or holding higher-timeframe plays, this indicator provides a professional lens into the market. It turns complex price action into a structured, predictable system where every move has logic and every entry has confluence.

You don’t just see the chart —

you see the intention behind every push, pull, manipulation, and reversal.

💎 Why It Feels Like a Cheat Code

Because it mirrors the way institutions analyze the market:

— Identify liquidity

— Seek equilibrium

— Deliver price

— Create inefficiency

— Mitigate

— Continue the narrative

Using SMC and Fibonacci together unlocks the “algorithmic geometry” behind price movement, giving you clarity where others see chaos.

⚡ Trade With Confidence, Confluence & Control

This indicator isn’t just a tool.

It’s a complete trading framework — structured, intelligent, and deadly accurate.

Master the markets.

Decode the algorithm.

Trade like smart money .

adrianasibaja_ ALGO (Liquidity/BOS/FVG + Sessions + Risk Locks)This strategy is an institutional-style automated trading system designed for XAU/USD and FTMO-funded accounts.

It combines liquidity sweeps, Break of Structure (BOS) and Fair Value Gap (FVG) confirmations with multi-filter confluences (RSI, ADX, ATR, EMA trend bias, and candle quality).

The algorithm automatically filters trades by session (London/New York), day of week, and volatility. It includes full FTMO risk management features such as daily loss lock, consecutive loss lock, and trade cooldowns.

RunRox - Backtesting System (ASMC)Introducing RunRox - Backtesting System (ASMC), a specially designed backtesting system built on the robust structure of our Advanced SMC indicator. This innovative tool evaluates various Smart Money Concept (SMC) trading setups and serves as an automatic optimizer, displaying which entry and exit points have historically shown the best results. With cutting-edge technology, RunRox - Backtesting System (ASMC) provides you with effective strategies, maximizing your trading potential and taking your trading to the next level

🟠 HOW OUR BACKTESTING SYSTEM WORKS

Our backtesting system for the Advanced SMC (ASMC) indicator is meticulously designed to provide traders with a thorough analysis of their Smart Money Concept (SMC) strategies. Here’s an overview of how it works:

🔸 Advanced SMC Structure

Our ASMC indicator is built upon an enhanced SMC structure that integrates the Institutional Distribution Model (IDM), precise retracements, and five types of order blocks (CHoCH OB, IDM OB, Local OB, BOS OB, Extreme OB). These components allow for a detailed understanding of market dynamics and the identification of key trading opportunities.

🔸 Data Integration and Analysis

1. Historical Data Testing:

Our system tests various entry and exit points using historical market data.

The ASMC indicator is used to simulate trades based on predefined SMC setups, evaluating their effectiveness over a specified time period.

Traders can select different parameters such as entry points, stop-loss, and take-profit levels to see how these setups would have performed historically.

2. Entry and Exit Events:

The backtester can simulate trades based on 12 different entry events, 14 target events, and 14 stop-loss events, providing a comprehensive testing framework.

It allows for testing with multiple combinations of entry and exit strategies, ensuring a robust evaluation of trading setups.

3. Order Block Sensitivity:

The system uses the sensitivity settings from the ASMC indicator to determine the most relevant order blocks and fair value gaps (FVGs) for entry and exit points.

It distinguishes between different types of order blocks, helping traders identify strong institutional zones versus local zones.

🔸 Optimization Capabilities

1. Auto-Optimizer:

The backtester includes an auto-optimizer feature that evaluates various setups to find those with the best historical performance.

It automatically adjusts parameters to identify the most effective strategies for both trend-following and counter-trend trading.

2. Stop Loss and Take Profit Optimization:

It optimizes stop-loss and take-profit levels by testing different settings and identifying those that provided the best historical results.

This helps traders refine their risk management and maximize potential returns.

3. Trailing Stop Optimization:

The system also optimizes trailing stops, ensuring that traders can maximize their profits by adjusting their stops dynamically as the market moves.

🔸 Comprehensive Reporting

1. Performance Metrics:

The backtesting system provides detailed reports, including key performance metrics such as Net Profit, Win Rate, Profit Factor, and Max Drawdown.

These metrics help traders understand the historical performance of their strategies and make data-driven decisions.

2. Flexible Settings:

Traders can adjust initial balance, commission rates, and risk per trade settings to simulate real-world trading conditions.

The system supports testing with different leverage settings, allowing for realistic assessments even with tight stop-loss levels.

🔸 Conclusion

The RunRox Backtesting System (ASMC) is a powerful tool for traders seeking to validate and optimize their SMC strategies. By leveraging historical data and sophisticated optimization algorithms, it provides insights into the most effective setups, enhancing trading performance and decision-making.

🟠 HERE ARE THE AVAILABLE FEATURES

Historical backtesting for any setup – Select any entry point, exit point, and various stop-loss options to see the results of your setup on historical data.

Auto-optimizer for finding the best setups – The indicator displays settings that have shown the best results historically, providing valuable insights.

Auto-optimizer for counter-trend setups – Discover entry and exit points for counter-trend trading based on historical performance.

Auto-optimizer for stop-loss – The indicator shows stop-loss points that have been most effective historically.

Auto-optimizer for take-profit – The indicator identifies take-profit points that have performed well in historical trading data.

Auto-optimizer for trailing stop – The indicator presents trailing stop settings that have shown the best historical results.

And much more within our indicator, all of which we will cover in this post. Next, we will showcase the possible entry points, targets, and stop-loss options available for testing your strategies

🟠 ENTRY SETTINGS

12 Event Triggers for Trade Entry

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Trade Direction Options

Long Only: Enter long positions only

Short Only: Enter short positions only

Long and Short: Enter both long and short positions based on trend

3 Levels for Order Block/FVG Entries

Beginning: Enter the trade at the first touch of the Order Block/FVG

Middle: Enter the trade when the middle of the Order Block/FVG is reached

End: Enter the trade upon full filling of the Order Block/FVG

*Three levels work only for Order Blocks and FVG. For trade entries based on BOS or CHoCH, these settings do not apply as these parameters are not available for these types of entries

You can choose any combination of trade entries imaginable.

🟠 TARGET SETTINGS

14 Target Events, Including Fixed % and Fixed RR (Risk/Reward):

Fixed - % change in price

Fixed RR - Risk Reward per trade

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Levels of Order Block/FVG for Target

Beginning: Close the trade at the first touch of your target.

Middle: Close the trade at the midpoint of your chosen target.

End: Close the trade when your target is fully filled.

Customizable Parameters

Easily set your Fixed % and Fixed RR targets with a user-friendly input field. This field works only for the Fixed and Fixed RR entry parameters. When selecting a different entry point, this field is ignored

Choose any combination of target events to suit your trading strategy.

🟠 STOPLOSS SETTINGS

14 Possible StopLoss Events Including Entry Orderblock/FVG

Fixed - Fix the loss on the trade when the price moves by N%

Entry Block

Extr. ChoCh OB

Extr. ChoCh FVG

ChoCh

ChoCh OB

ChoCh FVG

IDM OB

IDM FVG

BoS FVG

BoS OB

BoS

Extr. BoS FVG

Extr. BoS OB

3 Levels for Order Blocks/FVG Exits

Beginning: Exit the trade at the first touch of the order block/FVG.

Middle: Exit the trade at the middle of the order block/FVG.

End: Exit the trade at the full completion of the order block/FVG.

Dedicated Field for Setting Fixed % Value

Set a fixed % value in a dedicated field for the Fixed parameter. This field works only for the Fixed parameter. When selecting other exit parameters, this field is ignored.

🟠 ADDITIONAL SETTINGS

Trailing Stop, %

Set a Trailing Stop as a percentage of your trade to potentially increase profit based on historical data.

Move SL to Breakeven, bars

Move your StopLoss to breakeven after exiting the entry zone for a specified number of bars. This can enhance your potential WinRate based on historical performance.

Skip trade if RR less than

This feature allows you to skip trades where the potential Risk-to-Reward ratio is less than the number set in this field.

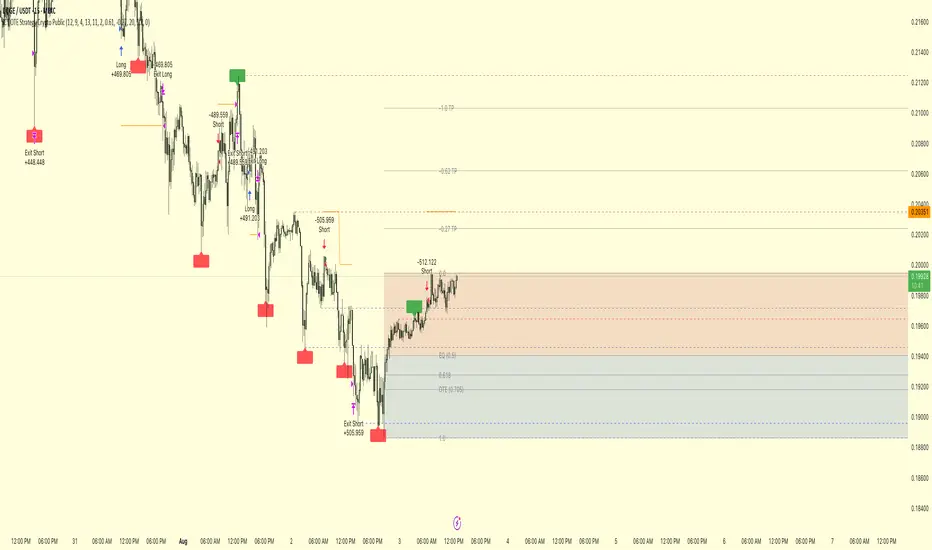

🟠 EXAMPLE OF MANUAL SETUP

For example, let me show you how it works on the chart. You select entry parameters, stop loss parameters, and take profit parameters for your trades, and the strategy automatically tests this setup on historical data, allowing you to see the results of this strategy.

In the screenshot above, the parameters were as follows:

Trade Entry: CHoCH OB (Beginning)

Stop Loss: Entry Block

Take Profit: Break of BOS

The indicator will automatically test all possible trades on the chart and display the results for this setup.

🟠 AUTO OPTIMIZATION SETTINGS

In the screenshot above, you can see the optimization table displaying various entry points, exits, and stop-loss settings, along with their historical performance results and other parameters. This feature allows you to identify trading setups that have shown the best historical outcomes.

This functionality will enhance your trading approach, providing you with valuable insights based on historical data. You’ll be aware of the Smart Money Concept settings that have historically worked best for any specific chart and timeframe.

Our indicator includes various optimization options designed to help you find the most effective settings based on historical data. There are 5 optimization modes, each offering unique benefits for every trader

Trend Entry - Optimization of the best settings for trend-following trades. The strategy will enter trades only in the direction of the trend. If the trend is upward, it will look for long entry points and vice versa.

Counter Trend Entry - Finding setups against the trend. If the trend is upward, the script will search for short entry points. This is the opposite of trend entry optimization.

Stop Loss - Identifying stop-loss points that showed the best historical performance for the specific setup you have configured. This helps in finding effective exit points to minimize losses.

Take Profit - Determining targets for the configured setup based on historical performance, helping to identify potentially profitable take profit levels.

Trailing Stop - Finding optimal percentages for the trailing stop function based on historical data, which can potentially increase the profit of your trades.

Ability to set parameters for auto-optimization within a specified range. For example, if you choose FixRR TP from 1 to 10, the indicator will automatically test all possible Risk Reward Take Profit variations from 1 to 10 and display the results for each parameter individually.

Ability to set initial deposit parameters, position commissions, and risk per trade as a fixed percentage or fixed amount. Additionally, you can set the maximum leverage for a trade.

There are times when the stop loss is very close to the entry point, and adhering to the risk per trade values set in the settings may not allow for such a loss in any situation. That’s why we added the ability to set the maximum possible leverage, allowing you to test your trading strategy even with very tight stop losses.

Duplicated Smart Money Structure settings from our Advanced SMC indicator that you can adjust to match your trading style flexibly. All these settings will be taken into account during the optimization process or when manually calculating settings.

Additionally, you can test your strategy based on higher timeframe order blocks. For example, you can test a strategy on a 1-minute chart while displaying order blocks from a 15-minute timeframe. The auto-optimizer will consider all these parameters, including higher timeframe order blocks, and will enter trades based on these order blocks.

Highly flexible dashboard and results optimization settings allow you to display the tables you need and sort results by six different criteria: Profit Factor, Profit, Winrate, Max Drawdown, Wins, and Trades. This enables you to find the exact setup you desire, based on these comprehensive data points.

🟠 ALERT CUSTOMIZATION

With this indicator, you can set up buy and sell alerts based on the test results, allowing you to create a comprehensive trading strategy. This feature enables you to receive real-time signals, making it a powerful tool for implementing your trading strategies.

🟠 STRATEGY PROPERTIES

For backtesting, we used realistic initial data for entering trades, such as:

Starting balance: $1000

Commission: 0.01%

Risk per trade: 1%

To ensure realistic data, we used the above settings. We offer two methods for calculating your order size, and in our case, we used a 1% risk per trade. Here’s what it means:

Risk per trade: This is the maximum loss from your deposit if the trade goes against you. The trade volume can change depending on your stop-loss distance from the entry point. Here’s the formula we use to calculate the possible volume for a single trade:

1. quantity = percentage_risk * balance / loss_per_1_contract (incl. fee)

Then, we calculate the maximum allowed volume based on the specified maximum leverage:

2. max_quantity = maxLeverage * balance / entry_price

3. If quantity < max_quantity, meaning the leverage is less than the maximum allowed, we keep quantity. If quantity > max_quantity, we use max_quantity (the maximum allowed volume according to the set leverage).

This way, depending on the stop-loss distance, the position size can vary and be up to 100% of your deposit, but the loss in each trade will not exceed the set percentage, which in our case is 1% for this backtest. This is a standard risk calculation method based on your stop-loss distance.

🔸 Statistical Significance of Trade Data

In our strategy, you may notice there weren’t enough trades to form statistically significant data. This is inherent to the Smart Money Concept (SMC) strategy, where the focus is not on the number of trades but rather on the risk-to-reward ratio per trade. In SMC strategies, it’s crucial to avoid taking numerous uncertain setups and instead perform a comprehensive analysis of the market situation.

Therefore, our strategy results show fewer than 100 trades. It’s important to understand that this small sample size isn’t statistically significant and shouldn’t be relied upon for strategy analysis. Backtesting with a small number of trades should not be used to draw conclusions about the effectiveness of a strategy.

🔸 Versatile Use Cases

The methods of using this indicator are numerous, ranging from identifying potentially the best-performing order blocks on the chart to creating a comprehensive trading strategy based on the data provided by our indicator. We believe that every trader will find a valuable application for this tool, enhancing their entry and exit points in trades.

Disclaimer

Past performance is not indicative of future results. The results shown by this indicator do not guarantee similar outcomes in the future. Use this tool as part of a comprehensive trading strategy, considering all market conditions and risks.

How to access

For access to this indicator, please read the author’s instructions below this post

S&D Light+ Enhanced# S&D Light+ Enhanced - Supply & Demand Zone Trading Strategy

## 📊 Overview

**S&D Light+ Enhanced** is an advanced Supply and Demand zone identification and trading strategy that combines institutional order flow concepts with smart money techniques. This strategy automatically identifies high-probability reversal zones based on Break of Structure (BOS), momentum analysis, and first retest principles.

## 🎯 Key Features

### Smart Zone Detection

- **Automatic Supply & Demand Zone Identification** - Detects institutional zones where price is likely to react

- **Multi-Candle Momentum Analysis** - Validates zones with configurable momentum requirements

- **Break of Structure (BOS) Confirmation** - Ensures zones are created only after significant structure breaks

- **Quality Filters** - Minimum zone size and ATR-based filtering to eliminate weak zones

### Advanced Zone Management

- **Customizable Zone Display** - Choose between Geometric or Volume-Weighted midlines

- **First Retest Logic** - Option to trade only the first touch of each zone for higher probability setups

- **Zone Capacity Control** - Maintains a clean chart by limiting stored zones per type

- **Visual Zone Status** - Automatically marks consumed zones with faded midlines

### Risk Management

- **Dynamic Stop Loss** - Positioned beyond zone boundaries with adjustable buffer

- **Risk-Reward Ratio Control** - Customizable R:R for consistent risk management

- **Entry Spacing** - Minimum bars between signals prevents overtrading

- **Position Sizing** - Built-in percentage of equity allocation

## 🔧 How It Works

### Zone Creation Logic

**Supply Zones (Selling Pressure):**

1. Strong momentum downward movement (configurable body-to-range ratio)

2. Identified bullish base candle (where institutions accumulated shorts)

3. Break of Structure downward (price breaks below recent swing low)

4. Zone created at the base candle's high/low range

**Demand Zones (Buying Pressure):**

1. Strong momentum upward movement

2. Identified bearish base candle (where institutions accumulated longs)

3. Break of Structure upward (price breaks above recent swing high)

4. Zone created at the base candle's high/low range

### Entry Conditions

**Long Entry:**

- Price retests a demand zone (touches top of zone)

- Rejection confirmed (close above zone)

- Zone hasn't been used (if "first retest only" enabled)

- Minimum bars since last entry respected

**Short Entry:**

- Price retests a supply zone (touches bottom of zone)

- Rejection confirmed (close below zone)

- Zone hasn't been used (if "first retest only" enabled)

- Minimum bars since last entry respected

## ⚙️ Customizable Parameters

### Display Settings

- **Show Zones** - Toggle zone visualization on/off

- **Max Stored Zones** - Control number of active zones (1-50 per type)

- **Color Customization** - Adjust supply/demand colors and transparency

### Zone Quality Filters

- **Momentum Body Fraction** - Minimum body size for momentum candles (0.1-0.9)

- **Min Momentum Candles** - Number of consecutive momentum candles required (1-5)

- **Big Candle Body Fraction** - Alternative single-candle momentum threshold (0.5-0.95)

- **Min Zone Size %** - Minimum zone height as percentage of price (0.01-5.0%)

### BOS Configuration

- **Swing Length** - Lookback period for structure identification (3-20)

- **ATR Length** - Period for volatility measurement (1-50)

- **BOS Required Break** - ATR multiplier for valid structure break (0.1-3.0)

### Midline Options

- **None** - No midline displayed

- **Geometric** - Simple average of zone top/bottom

- **CenterVolume** - Volume-weighted center based on highest volume bar in window

### Risk Management

- **SL Buffer %** - Additional space beyond zone boundary (0-5%)

- **Take Profit RR** - Risk-reward ratio for target placement (0.5-10x)

### Entry Rules

- **Only 1st Retest per Zone** - Trade zones only once for higher quality

- **Min Bars Between Entries** - Prevent overtrading (1-20 bars)

## 📈 Recommended Settings

### Conservative (Lower Frequency, Higher Quality)

```

Momentum Body Fraction: 0.30

Min Momentum Candles: 2-3

BOS Required Break: 0.8-1.0

Min Zone Size: 0.15-0.20%

Only 1st Retest: Enabled

```

### Balanced (Default)

```

Momentum Body Fraction: 0.28

Min Momentum Candles: 2

BOS Required Break: 0.7

Min Zone Size: 0.12%

Only 1st Retest: Enabled

```

### Aggressive (Higher Frequency, More Signals)

```

Momentum Body Fraction: 0.20-0.25

Min Momentum Candles: 1-2

BOS Required Break: 0.4-0.5

Min Zone Size: 0.08-0.10%

Only 1st Retest: Disabled

```

## 🎨 Visual Elements

- **Red Boxes** - Supply zones (potential selling areas)

- **Green Boxes** - Demand zones (potential buying areas)

- **Dotted Midlines** - Center of each zone (fades when zone is used)

- **Debug Triangles** - Shows when zone creation conditions are met

- Red triangle down = Supply zone created

- Green triangle up = Demand zone created

## 📊 Best Practices

1. **Use on Higher Timeframes** - 1H, 4H, and Daily charts work best for institutional zones

2. **Combine with Trend** - Trade zones in direction of overall market structure

3. **Wait for Confirmation** - Don't enter immediately at zone touch; wait for rejection

4. **Adjust for Market Volatility** - Increase BOS multiplier in choppy markets

5. **Monitor Zone Quality** - Fresh zones typically have higher success rates

6. **Backtest Your Settings** - Optimize parameters for your specific market and timeframe

## ⚠️ Risk Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Always:

- Use proper position sizing

- Set appropriate stop losses

- Test thoroughly before live trading

- Consider market conditions and overall trend

- Never risk more than you can afford to lose

## 🔍 Data Window Information

The strategy provides real-time metrics visible in the data window:

- Supply Zones Count

- Demand Zones Count

- ATR Value

- Momentum Signals (Up/Down)

- BOS Signals (Up/Down)

## 📝 Version History

**v1.0 - Enhanced Edition**

- Improved BOS detection logic

- Extended base candle search range

- Added comprehensive input validation

- Enhanced visual feedback system

- Robust array bounds checking

- Debug signals for troubleshooting

## 💡 Tips for Optimization

- **Trending Markets**: Lower momentum requirements, tighter BOS filters

- **Ranging Markets**: Increase zone size minimum, enable first retest only

- **Volatile Assets**: Increase ATR multiplier and SL buffer

- **Lower Timeframes**: Reduce swing length, increase min bars between entries

- **Higher Timeframes**: Increase swing length, relax momentum requirements

---

**Created with focus on institutional order flow, smart money concepts, and practical risk management.**

*Happy Trading! 📈*

PowerHouse SwiftEdge AI v2.10 StrategyOverview

The PowerHouse SwiftEdge AI v2.10 Strategy is a sophisticated trading system designed to identify high-probability trade setups in forex, stocks, and cryptocurrencies. By combining multi-timeframe trend analysis, momentum signals, volume confirmation, and smart money concepts (Change of Character and Break of Structure ), this strategy offers traders a robust tool to capitalize on market trends while minimizing false signals. The strategy’s unique “AI” component analyzes trends across multiple timeframes to provide a clear, actionable dashboard, making it accessible for both novice and experienced traders. The strategy is fully customizable, allowing users to tailor its filters to their trading style.

What It Does

This strategy generates Buy and Sell signals based on a confluence of technical indicators and smart money concepts. It uses:

Multi-Timeframe Trend Analysis: Confirms the market’s direction by analyzing trends on the 1-hour (60M), 4-hour (240M), and daily (D) timeframes.

Momentum Filter: Ensures trades align with strong price movements to avoid choppy markets.

Volume Filter: Validates signals with above-average volume to confirm market participation.

Breakout Filter: Requires price to break key levels for added confirmation.

Smart Money Signals (CHoCH/BOS): Identifies reversals (CHoCH) and trend continuations (BOS) based on pivot points.

AI Trend Dashboard: Summarizes trend strength, confidence, and predictions across timeframes, helping traders make informed decisions without needing to analyze complex data manually.

The strategy also plots dynamic support and resistance trendlines, take-profit (TP) levels, and “Get Ready” signals to alert users of potential setups before they fully develop. Trades are executed with predefined take-profit and stop-loss levels for disciplined risk management.

How It Works

The strategy integrates multiple components to create a cohesive trading system:

Multi-Timeframe Trend Analysis:

The strategy evaluates trends on three timeframes (1H, 4H, Daily) using Exponential Moving Averages (EMA) and Volume-Weighted Average Price (VWAP). A trend is considered bullish if the price is above both the EMA and VWAP, bearish if below, or neutral otherwise.

Signals are only generated when the trend on the user-selected higher timeframe aligns with the trade direction (e.g., Buy signals require a bullish higher timeframe trend). This reduces noise and ensures trades follow the broader market context.

Momentum Filter:

Measures the percentage price change between consecutive bars and compares it to a volatility-adjusted threshold (based on the Average True Range ). This ensures trades are taken only during significant price movements, filtering out low-momentum conditions.

Volume Filter (Optional):

Checks if the current volume exceeds a long-term average and shows positive short-term volume change. This confirms strong market participation, reducing the risk of false breakouts.

Breakout Filter (Optional):

Requires the price to break above (for Buy) or below (for Sell) recent highs/lows, ensuring the signal aligns with a structural shift in the market.

Smart Money Concepts (CHoCH/BOS):

Change of Character (CHoCH): Detects potential reversals when the price crosses under a recent pivot high (for Sell) or over a recent pivot low (for Buy) with a bearish or bullish candle, respectively.

Break of Structure (BOS): Confirms trend continuations when the price breaks below a recent pivot low (for Sell) or above a recent pivot high (for Buy) with strong momentum.

These signals are plotted as horizontal lines with labels, making it easy to visualize key levels.

AI Trend Dashboard:

Combines trend direction, momentum, and volatility (ATR) across timeframes to calculate a trend score. Scores above 0.5 indicate an “Up” trend, below -0.5 indicate a “Down” trend, and otherwise “Neutral.”

Displays a table summarizing trend strength (as a percentage), AI confidence (based on trend alignment), and Cumulative Volume Delta (CVD) for market context.

A second table (optional) shows trend predictions for 1H, 4H, and Daily timeframes, helping traders anticipate future market direction.

Dynamic Trendlines:

Plots support and resistance lines based on recent swing lows and highs within user-defined periods (shortTrendPeriod, longTrendPeriod). These lines adapt to market conditions and are colored based on trend strength.

Why This Combination?

The PowerHouse SwiftEdge AI v2.10 Strategy is original because it seamlessly integrates traditional technical analysis (EMA, VWAP, ATR, volume) with smart money concepts (CHoCH, BOS) and a proprietary AI-driven trend analysis. Unlike standalone indicators, this strategy:

Reduces False Signals: By requiring confluence across trend, momentum, volume, and breakout filters, it minimizes trades in choppy or low-conviction markets.

Adapts to Market Context: The ATR-based momentum threshold adjusts dynamically to volatility, ensuring signals remain relevant in both trending and ranging markets.

Simplifies Decision-Making: The AI dashboard distills complex multi-timeframe data into a user-friendly table, eliminating the need for manual analysis.

Leverages Smart Money: CHoCH and BOS signals capture institutional price action patterns, giving traders an edge in identifying reversals and continuations.

The combination of these components creates a balanced system that aligns short-term trade entries with longer-term market trends, offering a unique blend of precision, adaptability, and clarity.

How to Use

Add to Chart:

Apply the strategy to your TradingView chart on a liquid symbol (e.g., EURUSD, BTCUSD, AAPL) with a timeframe of 60 minutes or lower (e.g., 15M, 60M).

Configure Inputs:

Pivot Length: Adjust the number of bars (default: 5) to detect pivot highs/lows for CHoCH/BOS signals. Higher values reduce noise but may delay signals.

Momentum Threshold: Set the base percentage (default: 0.01%) for momentum confirmation. Increase for stricter signals.

Take Profit/Stop Loss: Define TP and SL in points (default: 10 each) for risk management.

Higher/Lower Timeframe: Choose timeframes (60M, 240M, D) for trend filtering. Ensure the chart timeframe is lower than or equal to the higher timeframe.

Filters: Enable/disable momentum, volume, or breakout filters to suit your trading style.

Trend Periods: Set shortTrendPeriod (default: 30) and longTrendPeriod (default: 100) for trendline plotting. Keep below 2000 to avoid buffer errors.

AI Dashboard: Toggle Enable AI Market Analysis to show/hide the prediction table and adjust its position.

Interpret Signals:

Buy/Sell Labels: Green "Buy" or red "Sell" labels indicate trade entries with predefined TP/SL levels plotted.

Get Ready Signals: Yellow "Get Ready BUY" or orange "Get Ready SELL" labels warn of potential setups.

CHoCH/BOS Lines: Aqua (CHoCH Sell), lime (CHoCH Buy), fuchsia (BOS Sell), or teal (BOS Buy) lines mark key levels.

Trendlines: Green/lime (support) or fuchsia/purple (resistance) dashed lines show dynamic support/resistance.

AI Dashboard: Check the top-right table for trend strength, confidence, and CVD. The optional bottom table shows trend predictions (Up, Down, Neutral).

Backtest and Trade:

Use TradingView’s Strategy Tester to evaluate performance. Adjust TP/SL and filters based on results.

Trade manually based on signals or automate with TradingView alerts (set alerts for Buy/Sell labels).

Originality and Value

The PowerHouse SwiftEdge AI v2.10 Strategy stands out by combining multi-timeframe analysis, smart money concepts, and an AI-driven dashboard into a single, user-friendly system. Its adaptive momentum threshold, robust filtering, and clear visualizations empower traders to make confident decisions without needing advanced technical knowledge. Whether you’re a day trader or swing trader, this strategy provides a versatile, data-driven approach to navigating dynamic markets.

Important Notes:

Risk Management: Always use appropriate position sizing and risk management, as the strategy’s TP/SL levels are customizable.

Symbol Compatibility: Test on liquid symbols with sufficient historical data (at least 2000 bars) to avoid buffer errors.

Performance: Backtest thoroughly to optimize settings for your market and timeframe.

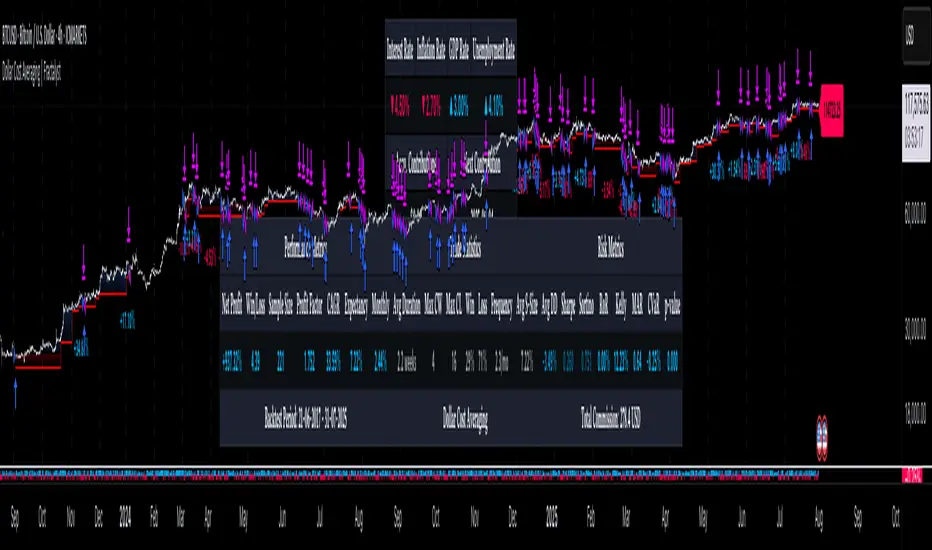

Zendog V2 backtest DCA bot 3commasHi everyone,

After a few iterations and additional implemented features this version of the Backtester is now open source.

The Strategy is a Backtester for 3commas DCA bots. The main usage scenario is to plugin your external indicator, and backtest it using different DCA settings.

Before using this script please make sure you read these explanations and make sure you understand how it works.

Features:

- Because of Tradingview limitations on how orders are grouped into Trades, this Strategy statistics are calculated by the script, so please ignore the Strategy Tester statistics completely

Statistics Table explained:

- Status: either all deals are closed or there is a deal still running, in which case additional info

is provided below, as when the deal started, current PnL, current SO

- Finished deals: Total number of closed deals both Winning and Losing.

A deal is comprised as the Base Order (BO) + all Safety Orders (SO) related to that deal, so this number

will be different than the Strategy Tester List of Trades

- Winning Deals: Deal ended in profit

- Losing deals: Deals ended with loss due to Stop Loss. In the future I might add a Deal Stop condition to

the script, so that will count towards this number as well.

- Total days ( Max / Avg days in Deal ):

Total Days in the Backtest given by either Tradingview limitation on the number of candles or by the

config of the script regarding "Limit Date Range".

Max Days spent in a deal + which period this happened.

Avg days spent in a deal.

- Required capital: This is the total capital required to run the Backtester and it is automatically calculated by

the script taking into consideration BO size, SO size, SO volume scale. This should be the same as 3commas.

This number overwrites strategy.initial_capital and is used to calculate Profit and other stats, so you don't need

to update strategy.initial_capital every time you change BO/SO settings

- Profit after commission

- Buy and Hold return: The PnL that could have been obtained by buying at the close of the first candle of the

backtester and selling at the last.

- Covered deviation: The % of price move from initial BO order covered by SO settings

- Max Deviation: Biggest market % price move vs BO price, in the other direction (for long

is down, for short it is up)

- Max Drawdown: Biggest market % price move vs Avg price of the whole Trade (BO + any SO), in the other

direction (for long price goes down, for short it goes up)

This is calculated for the whole Trade so it is different than List of Trades

- Max / Avg bars in deal

- Total volume / Commission calculated by the strategy. For correct commission please set Commission in the

Inputs Tab and you may ignore Properties Tab

- Close stats for deals: This is a list of how many Trades were closed at each step, including Stop Loss (if

configured), together with covered deviation for that step, the number of deals, and the percentage of this

number from all the deals

TODO: Might add deal avg value for each step

- Settings Table that can be enabled / disabled just to have an overview of your configs on the chart, this is a

drawn on bottom left

- Steps Table similar to 3commas, this is also drawn on bottom left, so please disable Settings table if you want

to see this one

TODO: Might add extra stats here

- Deal start condition: built in RSI-7 or plugin any external indicator and compare with any value the indicator plots

(main purpose of this strategy is to connect your own studies, so using external indicator is recommended)

- Base order and safety orders configs similar to 3commas (order size, percent deviation, safety orders,

percent scale and volume scale)

- Long and Short

- Stop Loss

- Support for Take profit from base order or from Total volume of the deal

- Configs help (besides self explanatory):

- Chart theme: Adjust according to the theme you run on. There is no way to detect theme at the moment.

This adjust different colors

- Deal Start Type: Either a builtin RSI7 or "External indicator"

- Indicator Source an value: If using External Indicator then select source, comparison and value.

For example you could start a deal when Volume is greater than xxxx, or code a custom indicator that plots

different values based on your conditions and test those values

- Visuals / Decimals for display: Adjust according to your symbol

- BO Entry Price for steps table: This is the BO start deal price used to calculate the steps in the table

SmartMoneyConcept ProFlow StrategySmartMoneyConcept ProFlow is a complete SMC-based algo built for trending markets and clean volatility phases – especially on crypto pairs like BTC, ETH and perpetual futures.

It combines:

• Smart Money swing structure (BOS / CHoCH)

• Dynamic Support & Resistance levels

• Order Block–style gap detection

• Volatility normalization (ATR / Range / BBWidth)

• SuperTrend trend filter

• ATR & Volume-based exits, TP lock and session control

The goal: fewer random trades, more focused entries when structure + volatility + trend are in sync.

1. Core Idea

Smart Structure Levels (S/R)

– The strategy builds dynamic support/resistance using swing highs/lows.

– Breakouts above resistance or below support, with enough volatility (filter), become primary trade signals.

BOS / CHoCH Engine

– Tracks Break of Structure (BOS) and Change of Character (CHoCH).

– BOS up/down help define the current trend bias.

– CHoCH highlights potential reversals after a confirmed BOS in the opposite direction.

Order Block Gap Logic

– Detects displacement candles with gaps (based on ATR) to approximate OB-style “impulsive moves”.

– Bullish gaps can add confluence for long entries, bearish gaps for shorts.

Volatility-Aware Entries

– Uses normalized volatility (via ATR, Range or BBWidth).

– Filters out breakouts in dead, low-vol environments and focuses on moves with real expansion.

2. Trend & Risk Management Stack

SuperTrend Filter

– Optional “Only With SuperTrend Direction” to restrict entries to the current ST trend.

– ST flips can also force exits if you want to exit as soon as the main trend changes.

ATR-Based Stops & Trails

– ATR distance check to avoid ultra-tight stops that get chopped instantly.

– Three modes:

• StopOnly – classic fixed ATR stop.

• TrailOnly – trailing ATR-style stop.

• StopAndTrail – initial fixed stop that later trails with price.

Volume-Based Exits (Optional)

– Exit on extremely low volume (move losing participation).

– Or on opposite volume spikes (strong counter-pressure against your position).

– Or use Both for a more active volume management.

TP Lock Logic

– When unrealized profit reaches a chosen value, the position is closed and a “lock” can be applied.

– Use this lock to:

• block same-direction re-entries for that side, or

• allow them again depending on your preference.

3. Anti-Churn & Session Control

Anti-Churn Controls

– Minimum bars between entries.

– Cooldown after an ATR exit.

– Limit of max entries per bar.

Session Filter

– Restrict trading to a specific hourly window (e.g. main market session).

– Option to force close positions outside your active session.

– Handy for intraday traders who don’t want overnight or low-liquidity exposure.

4. SmartMoney Preset Modes

Preset Mode:

• EtherFlux – more flexible, for general breakout & volatility trading.

• SmartMoney – SMC-focused preset:

– Adjusted length, volatility filter and ATR settings.

– Option to disable exits from the strategy side (for manual risk control).

Switching presets automatically tunes multiple internal parameters so you don’t have to micromanage every input each time.

5. Visual Layer

This script has a complete visual suite to help you “read the tape”:

– Bar Colors by position and SuperTrend bias.

– Support / Resistance dots and lines (stepline style).

– Order Block markers (bullish / bearish gap labels).

– BOS / CHoCH labels to track structure shifts in real-time.

– Liquidation Zones (visual only)

• Approximate long and short liquidation areas based on assumed leverage.

• Shaded zones on the chart for quick liquidity map.

– Status Labels

• Session status (ACTIVE / OFF / DISABLED).

• Current position (LONG / SHORT / FLAT).

• TP Lock status (longs locked / shorts locked / no lock).

All visuals are designed for dark charts but also work on light themes with minor tweaks.

6. Quick Input Guide

• Levels Period & Volatility Filter – main structure sensitivity and breakout quality.

• Volatility Method – ATR / Range / BBWidth normalization for the vol filter.

• ATR Stop & Management – core risk rules: ATR multiplier, stop/trail mode, min ATR distance.

• SuperTrend Settings – trend bias and ST-flip exits.

• SmartMoney Preset – quick switch between EtherFlux and SmartMoney tuning.

• Volume Exits – low volume / opposite spike / both.

• Session Filter – hour-based trading window + optional forced flat outside session.

• Follow-Signal Mode – flip from long→short or short→long when signal reverses (signal-based rotation).

• TP Lock – secure profits at a fixed amount and optionally block same-direction re-entries.

• Liq Zones – visual only, for liquidity map (no direct trade logic).

How to Use (My Suggestion)

Start on 15m–4H charts for liquid pairs (BTC, ETH, majors).

Choose your preset:

– EtherFlux for more general breakout + vol trading.

– SmartMoney if you want stricter SMC behaviour.

Turn on SuperTrend + ATR stops for cleaner risk management.

Forward-test in replay / paper trading before using real capital.

Use the visual BOS/CHoCH + Liq Zones as context , not as blind signals.

Important

This is a backtest & research tool . It is not financial advice and does not guarantee profits. Always combine it with your own risk management, position sizing, and forward-testing before going live. Trading leveraged products and crypto can result in partial or full loss of capital.

SMC Trend Filter Strategy (EMA50/EMA200 + FVG)Overview

This strategy implements a multi-timeframe Smart Money Concept (SMC) trading system designed for intraday and swing trading.

It combines a Daily trend filter, Break of Structure (BOS) detection, Order Block (OB) zones, Fair Value Gap (FVG) confirmation, and an ATR-based trailing stop system to achieve structured and rule-based entries.

The strategy is fully automated for backtesting and allows users to evaluate SMC concepts without repainting or discretionary interpretation.

- Core Components

1. Higher-Timeframe Trend Filter (Daily EMA50/EMA200)

The strategy retrieves D1 data and determines market direction using EMA50 and EMA200:

Uptrend → EMA50 > EMA200

Downtrend → EMA50 < EMA200

Trades are only taken in the direction of the Daily trend to avoid counter-trend setups.

2. Market Structure & Break of Structure (BOS)

The strategy identifies swing highs/lows and detects when price breaks beyond them:

Bullish BOS: price closes above previous swing high

Bearish BOS: price closes below previous swing low

This forms the foundation of SMC market structure recognition.

3. Order Block Zone (OB)

Upon detecting a BOS, the strategy marks the previous candle as a potential Order Block:

For bullish BOS → OB = previous candle’s high/low

For bearish BOS → OB = previous candle’s high/low

The OB zone is visualized using a semi-transparent box extended forward

Qullamaggie [Modified] | FractalystWhat's the purpose of this strategy?

The strategy aims to identify high-probability breakout setups in trending markets, inspired by Kristjan "Qullamaggie" Kullamägi’s approach.

It focuses on capturing explosive price moves after periods of consolidation, using technical criteria like moving averages, breakouts, trailing stop-loss and momentum confirmation.

Ideal for swing traders seeking to ride strong trends while managing risk.

----

How does the strategy work?

The strategy follows a systematic process to capture high-momentum breakouts:

Pre-Breakout Criteria:

Prior Price Surge: Identifies stocks that have rallied 30-100%+ in recent month(s), signaling strong underlying momentum (per Qullamaggie’s volatility expansion principles).

Consolidation Phase: Looks for a tightening price range (e.g., flag, pennant, or tight base), indicating a potential "coiling" before continuation.

Trend Confirmation: Uses moving averages (e.g., 20/50/200 EMA) to ensure the stock is trading above key averages on the daily chart, confirming an uptrend.

Price Break: Enters when price clears the consolidation high with conviction.

Risk Management:

Initial Stop Loss: Placed below the consolidation low or a recent swing point to limit downside.

Break-Even Adjustment: Moves stop loss to breakeven once the trade reaches 1.5x risk-to-reward (RR), securing a "free trade" while letting winners run.

Trailing Stop (Unique Edge):

Market Structure Trailing: Instead of trailing via moving averages, the stop is dynamically adjusted using structural invalidation level. This adapts to price action, allowing the trade to stay open during volatile retracements while locking in gains as new structure forms.

Why This Matters: Most strategies use rigid trailing stops (e.g., below the 10EMA), which often exit prematurely in choppy markets. By trailing based on structure, this strategy avoids "noise" and captures larger trends, directly boosting overall returns.

----

What markets or timeframes is this suited for?

This is a long-only strategy designed for trending markets, and it performs best in:

Markets: Stocks (especially high-growth, liquid equities), cryptocurrencies (major pairs with strong volatility), commodities (e.g., oil, gold), and futures (index/commodity futures).

Timeframes: Primarily daily charts for swing trades (1-30 day holds), though weekly charts can help confirm broader trends.

Key Advantage: The TradingView script allows instant backtesting with adjustable parameters

You can:

- Test historical performance across multiple markets to identify which assets align best with the strategy.

- Optimize settings (e.g., trailing stop sensitivity, moving averages etc.) to match a market’s volatility profile.

Build a diversified portfolio by filtering for markets that show consistent profitability in backtests.

For example, you might discover cryptos require tighter trailing stops due to volatility, while stocks thrive with wider structural stops. The script automates this analysis, letting you to trade confidently.

----

What indicators or tools does the strategy use?

The strategy combines customizable technical tools with strict anti-lookahead safeguards:

Core Indicators:

Moving Averages: Adjustable periods (e.g., 20/50/200 EMA or SMA) and timeframes (daily/weekly) to confirm trend alignment. Users can test combinations (e.g., 10EMA vs. 20EMA) to optimize for specific markets.

Breakout Parameters:

Consolidation Length: Adjustable window to define the "tightness" of the pre-breakout pattern.

Entry Models: Flexible entry logics (Breakouts and fractals)

Anti-Lookahead Design:

All calculations (e.g., moving averages, consolidation ranges, volume averages) use only closed/confirmed data available at the time of the signal.

----

How do I manage risk with this strategy?

The strategy prioritizes customizable risk controls to align with your trading style and account size:

User-Defined Risk Inputs:

Risk Per Trade: Set a % of Equity (e.g., 1-2%) to determine position size. The strategy auto-calculates shares/contracts to match your selected risk per trade.

Flexibility: Choose between fixed risk or equity-based scaling.

The script adjusts position sizing dynamically based on your selection.

Pyramiding Feature:

Customizable Entries: Adjust the number of pyramiding trades allowed (e.g., 1-3 additional positions) in the strategy settings. Each new entry is triggered only if the prior trade hits its 1.5x RR target and the trend remains intact.

Risk-Scaled Additions: New positions use profits from prior trades, compounding gains without increasing initial risk.

Risk-Free Trade Mechanic:

Once a trade reaches 1.5x RR, the stop loss is moved to breakeven, eliminating downside risk.

The strategy then opens a new position (if pyramiding is enabled) using a portion of the locked-in profit. This "snowballs" winners while keeping total capital exposure stable.

Impact on Net Profit & Drawdown:

Net Profit Boost: Pyramiding lets you ride multi-leg trends aggressively. For example, a 100% runner could generate 2-3x more profit vs. a single-entry approach.

Controlled Drawdowns: Since new positions are funded by profits (not initial capital), max drawdown stays anchored to your original risk per trade (e.g., 1-2% of account). Even if later entries fail, the breakeven stop on prior trades protects overall equity.

Why This Works: Most strategies either over-leverage (increasing drawdowns) or exit too early. By recycling profits into new positions only after securing risk-free capital, this approach mimics hedge fund "scaling in" tactics while staying retail-trader friendly.

----

How does the strategy identify market structure for its trailing stoploss?