NQ Short (09-02-25)NAZ H/S to failed auction bottom retest (TLX 234, Turd Zone), for next big move. Seems like Tariff social media noise from Wash Street is in question and may bring some BALANCE or reality (Short). Play KL's lower and watch for the O/N to switch gears with some selling, NDX 21,850 Gap Fill may be in the mix. Go Fed, BTD, FOMO with Mr. Retail into the Long Trap.

MNQH2020 trade ideas

NQ Range (08-25-25)Going back to Range play this week. We are in the middle of a long lasting trend of a Friday-Monday Long Play, this has been the redirect of any drop going back a year or two. Total guess this week, Blue Arrows are Key Levels to watch for hit/reversals. The Shaded Zone above is a Turn Zone that will/may reject and send the NAZ 23,486 or 486 1st then TZ try. Go Fed, BTD & FOMO for another Decade. The Buy The Dip Strategy seems to TRUMP all strategies and Wash Street is banking on that. Still feel we go lower prior to any new ATH. Look sideways to lower and stay long in any O/N Session.

MNQ Futures 29 AUGBullish to start off NY session. Possible drop in the hours leading to market close.

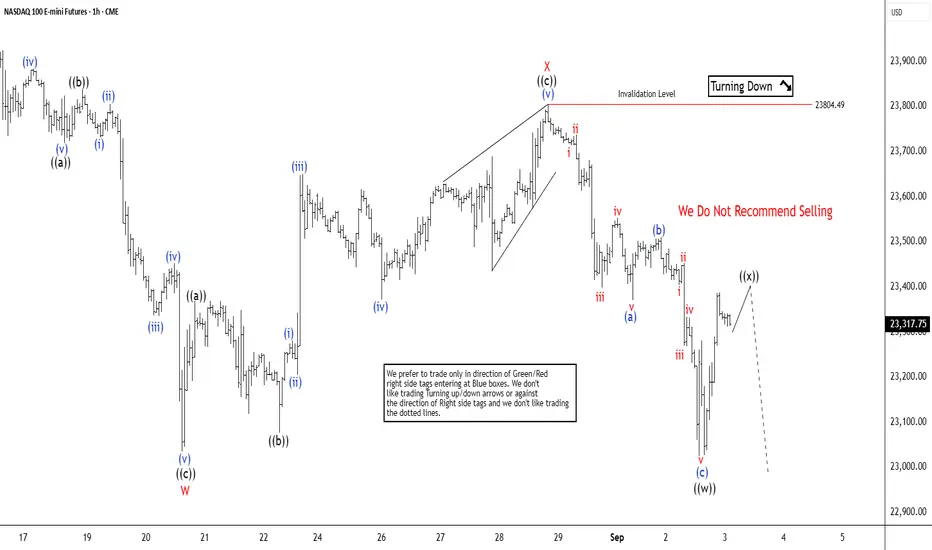

Nasdaq Futures (NQ) Double Correction Targets 22752 DownsideNasdaq Futures (NQ) display a bearish sequence with a lower low from the 13 August high, signaling potential for further declines. The decline from this peak is unfolding as a double three Elliott Wave structure. From the 13 August high, wave W concluded at 23035. The subsequent wave X rally formed a zigzag pattern, with wave ((a)) peaking at 23369.25 and wave ((b)) dipping to 23076.75. The Index then climbed in wave ((c)) to 23804.49, completing wave X.

The Index has since resumed its descent in wave Y, breaking below the wave W low at 23035, confirming the next downward leg. From wave X, wave (a) ended at 23370.5, followed by a wave (b) rally to 23509.5. The Index then continued lower in wave (c) to 23025.25, finalizing wave ((w)). Currently, wave ((x)) is underway, correcting the cycle from the 29 August high before the Index turns lower again. In the near term, as long as the pivot at 23804.49 remains intact, expect any rally to falter in a 3, 7, or 11 swing, leading to further downside. The projected target for wave Y lies between 22111.1 and 22752, based on the 100% – 161.8% Fibonacci extension of wave W.

NQ Inverted fair value gap retest for possible long position

NQ seeming quite bullish starting in September. On this 4hr chart we can see price completely disregard the FVG create last Friday. I can see price staying above the 23,584.00 range and possibly filling the entirety of the inversion area before heading back to the upside. Volume footprint shows that there were very few buyers in last Fridays dump.

Ill be keeping an eye out on this trade to see how price reacts before entering.

NQ DAILY LEVELSKey levels that will be in play next week based of the four-hour time frame. We also have some fair value gaps and liquidity pools the market should be looking to take out. Expecting monday to be a bullish day due to more news the fed may lower interest rates.

Is Nasdaq still Bullish?I’m still sensing bullish momentum on Nasdaq. My expectation is for price to retrace back into this week’s NWOG before making a push toward last week’s NWOG and the 1-hour gap at 23,583.00. There’s also a possibility we dip to fill the gap at 23,400.00 first, but if that scenario plays out, I don’t see price maintaining its bullish momentum afterward.

On the weekly chart, price continues to strongly respect the Bullish OB formed in the first week of August. As long as this level holds, I expect momentum to carry us higher in the near term.

We'll see tomorrow morning⚡

NASDAQ (NAS 100): Short Term Sells to the Weekly +FVG!Welcome back to the Weekly Forex Forecast for the week of Sept 1 - 5th.

In this video, we will analyze the following FX market: NASDAQ (NQ1!) NAS100

The NASDAQ failed to make a new ATH last week, indicating some weakness in the market. Frequently, Swing failures precede reversals, and this seems to be the case on the Daily TF.

Look for price to confirm bearish intent, as the sell side liquidity targets draw price down to the +FVG at 22.582.

A bullish BOS at current levels would invalidate this trade idea.

Enjoy!

May profits be upon you.

Leave any questions or comments in the comment section.

I appreciate any feedback from my viewers!

Like and/or subscribe if you want more accurate analysis.

Thank you so much!

Disclaimer:

I do not provide personal investment advice and I am not a qualified licensed investment advisor.

All information found here, including any ideas, opinions, views, predictions, forecasts, commentaries, suggestions, expressed or implied herein, are for informational, entertainment or educational purposes only and should not be construed as personal investment advice. While the information provided is believed to be accurate, it may include errors or inaccuracies.

I will not and cannot be held liable for any actions you take as a result of anything you read here.

Conduct your own due diligence, or consult a licensed financial advisor or broker before making any and all investment decisions. Any investments, trades, speculations, or decisions made on the basis of any information found on this channel, expressed or implied herein, are committed at your own risk, financial or otherwise.

NQ Power Range Report with FIB Ext - 8/29/2025 Session (Correct)CME_MINI:NQU2025

- PR High: 23762.00

- PR Low: 23735.00

- NZ Spread: 60.5

Key scheduled economic events:

08:30 | Core PCE Price Index (YoY|MoM)

09:45 | Chicago PMI

Month end ahead of early close Monday

Session Open Stats (As of 12:45 AM 8/29)

- Session Open ATR: 283.13

- Volume: 16K

- Open Int: 286K

- Trend Grade: Long

- From BA ATH: -1.4% (Rounded)

Key Levels (Rounded - Think of these as ranges)

- Long: 24382

- Mid: 23239

- Short: 22096

Keep in mind this is not speculation or a prediction. Only a report of the Power Range with Fib extensions for target hunting. Do your DD! You determine your risk tolerance. You are fully capable of making your own decisions.

BA: Back Adjusted

BuZ/BeZ: Bull Zone / Bear Zone

NZ: Neutral Zone

#202535 - priceactiontds - weekly update - nasdaq e-miniGood Day and I hope you are well.

comment: Neutral. I see the current range from 22800 - 24069 and the middle of it is 23460ish and we closed right at it. Bears can argue a head & shoulders on the daily chart and bulls still have two decent bull trend lines going for them. I don’t think around 23500 you can have any edge. I’d like for this to not hit 24k again but the odds for that are low. Best to wait.

current market cycle: bull trend

key levels for next week: 22700 - 24100

bull case: Bulls got a new ath and the market is overdue for a pullback but that does not mean we will get one. Bulls are still in full control as long as they keep the market above 22800. Having said that, it’s overdone, overbought and we are likely at the peak of the bubble.

Invalidation is below 22780

bear case: Bears need to do more. Anything below 23000 would be a start. That would break both trend lines and opens the possibility for 22000 over the next weeks. For now I don’t think it’s good to sell around the midpoint of this triangle.

Invalidation is above 23800

short term: Neutral around 23500. Same as last week.

medium-long term - Update from 2024-08-10: 22000 likely to get hit this year gain. 20000 seems a bit much for 3 months left.

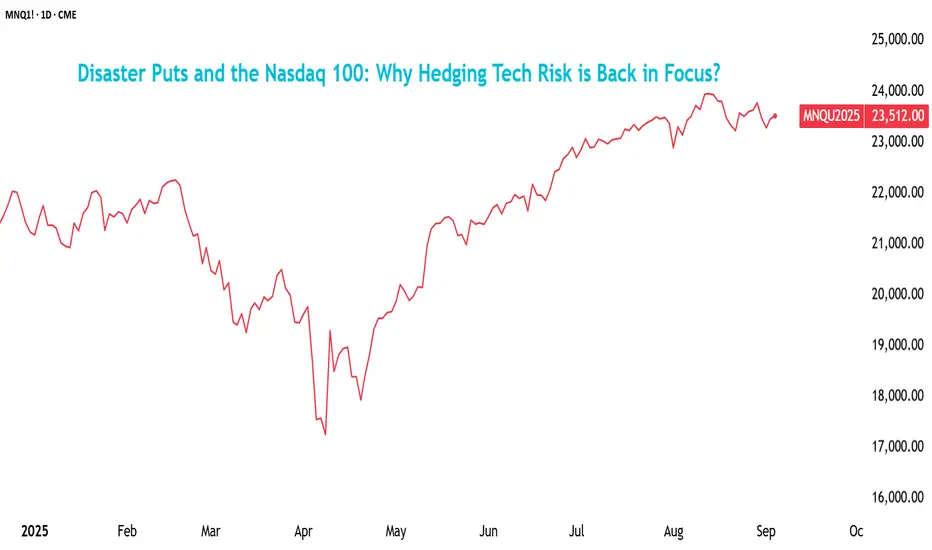

Disaster Puts & Nasdaq: Why Hedging Tech Risk is Back in Focus?Periods of calm in financial markets often mask the risks that lie beneath. With the Nasdaq 100 trading at elevated valuations and implied volatilities back at subdued levels, the cost of buying protection has rarely looked cheaper.

That sets the stage for a discussion around “disaster puts,” those deep out-of-the-money (OTM) put options designed to protect against sudden and severe drawdowns. These hedges, which would otherwise appear unnecessary, become relevant in cases where history repeats itself, reminding investors of how quickly corrections can turn into crashes.

The Nasdaq 100 has surged nearly 40% since its April bottom, powered by the Magnificent 7 rally (+50%). But options traders aren’t buying the calm; they’re piling into disaster puts on QQQ (an ETF tracking the index), driving the 2-month 10-delta to 25-delta put volatility ratio to a three-year high.

Source: Bloomberg

Put skew simply measures how expensive deep OTM crash protection is compared to nearer-the-money downside hedges. Here, a 10-delta put is a very low-probability and a deep OTM option—essentially as insurance against a rare and severe plunge. The 25-delta put is much closer to the current price and represents more standard protection.

The ratio rising toward 1.8x means those deep crash hedges are nearly 80% more expensive than regular downside hedges. Normally, these “disaster puts” always cost more, but the increasing gap shows investors are paying up for tail-risk protection, worried about another sudden April-style selloff rather than just a typical 5–10% correction.

So while the elevated put skew underscores crash hedging demand, it’s only part of the story. To see how the market is weighing downside protection against upside chase in general, we can look at the call/put skew:

Source: CME QuikStrike

Nasdaq 100 ( NQ ) 10-delta skew also shows deep OTM puts trading at a heavy premium to upside calls. Elevated put skew reflects persistent demand for crash protection, while negative call skew signals little appetite for chasing extreme rallies.

Though not as extreme in magnitude, the preference of calls over puts is clearly reflected in the same chart on the 25-delta skew:

Source: CME QuikStrike

Bearish Tilt in ETF and Futures Positioning

As of 02/Sept, options OI for NQ across all expiries is decisively bearish, with the put-call ratio being 1.45 overall:

Source: CME QuikStrike

Among all expiries through to the end of the year, it is the one expiring on 19/Sept that has the highest OI, followed by the 19/Dec and 17/Oct expiries. The October expiry has the most bearish OI outlook, with a PCR of 1.89.

This QuikStrike table below tracks daily open interest changes for the weekly Nasdaq-100 (NQ) options contract expiring Friday, September 5th.

Source: CME QuikStrike

The build-up of put positions over the past session stands out. On 29/Aug, 90 puts were added for the 23,300 strike; 133 puts were added for the 23,175 strike; and 84 puts were added for the 22,900 strike—a 2.3% decline from the current price.

Source: CME QuikStrike

Going even further deep OTM, we see that strikes as low as 20,950 have also garnered put interest recently:

The additions of 44 puts for that, along with the high concentration of puts above the 22,500 strike, reinforce the hedging demand build-up for the index.

Having said that, near-the-money calls have also seen some interest, with the call interest falling dramatically above the 24,000 strike.

Taken together, the recent OI change mirrors the broader skew dynamics, where investors are paying for tail protection, but there also remains a pocket of bullish positioning near-the-money, reflecting both optimism in the rally’s resilience and nervousness about another outsized swing.

The chart below shows the Commitment of Traders (CoT) report for the Micro Nasdaq 100 ( MNQ ) contract:

Source: CME QuikStrike

This reflects that retail investors (non-reportable) have already taken note: the positioning has flipped decisively net short starting in July. As of August 26, retail traders held 36,507 longs versus 55,534 shorts, leaving them net short by about 19,000 contracts. This marks a sharp contrast to June, when retail had a strong net long bias.

Source: CME QuikStrike

However, CoT data for asset managers and hedge funds (leveraged) shows that speculators here are still leaning net long. While the latter did add a lot of short positions, it was a 21% week-on-week decline as against the 30% increase in their long positions.

History’s Warning: Valuations and Vulnerability

This renewed appetite for disaster insurance reflects a deeper truth: the Nasdaq 100 has never been a gentle market to own when sentiment turns. Its tech-heavy composition leaves it more exposed than the S&P 500 when valuations come under pressure. Four episodes stand out.

The dot-com bust from March 2000 to October 2002 remains the starkest example. The Nasdaq 100 collapsed by nearly 80%, compared with a 45% decline for the S&P 500. An era of speculative IPOs and unprofitable startups had inflated expectations well beyond what fundamentals could support. When capital dried up, the selling pressure was relentless, and the recovery took more than a decade.

A similar concern about high capex for firms pivoting around AI and their corresponding high valuations worries those who are averse to a call back to post-Y2K events.

A July 2025 report from MIT highlights that 95% of companies investing in GenAI have yet to see financial returns, while Ted Mortonson of Baird flags sky-high valuations in AI stocks with scant earnings as reminiscent of past excess.

The firms are priced to perfection; expectations so high that they are valued with the assumption that everything will go right. In these cases, even a small disappointment can cause the stock to fall sharply because expectations are already maxed out.

OpenAI CEO Sam Altman also cautioned last month that investors are possibly “overexcited,” while Apollo’s Torsten Slok noted that the top-tier S&P names today may be more overvalued than during the 1999 tech apex.

Source: Apollo Academy

The top-10 for both—the S&P 500 and the Nasdaq-100—constitutes the same names, with Berkshire Hathaway replacing Netflix in the former index. Though the chart above pertains to the S&P 500, the situation looks meeker for the Nasdaq 100.

The 2022 bear market brought the focus back to valuations and rates. As the Federal Reserve hiked aggressively to contain inflation, the S&P 500 slipped about 25%. The Nasdaq 100, with its sensitivity to discount rates and long-duration earnings, fell closer to 35%. This reinforced the dot-com lesson: when the cost of capital rises, growth stocks are punished most severely.

Hedging in a Calm Market

Today, the volatility markets tell an interesting story. The Cboe Nasdaq-100 Volatility Index (VXN) shows option premiums to be at near-yearly lows.

Overall, option premiums are subdued, making standard hedges unusually cheap. Tying it back to the disaster puts, the relative cost of crash protection has still spiked with investors crowding into deep OTM puts. In other words, plain insurance is inexpensive, but extreme insurance is at a premium.

Having said that, net ETF flows into QQQ also continue to indicate that investors remain confident in tech, even as concentration risk rises. In August, the inflows netted over $1.8 billion. Assets under management (AUM) have also reached an all-time high, having recovered after the slump in April.

All of this, and especially the subdued IVs, means that hedging is now cheaper; it is also more urgent, given how quickly positioning can flip.

And while protection is unusually inexpensive now, this isn’t as much about predicting the next crash via disaster puts, but more about taking advantage of the market’s calm to lock in cost-efficient insurance. Just as homeowners don’t buy fire insurance because they expect a blaze tomorrow, prudent investors can use puts to guard against shocks.

CME’s weekly Micro E-mini Nasdaq-100 options (and Micro E-mini S&P 500 options) offer a flexible way to manage near-term risks, with contract sizes one-tenth the notional of standard E-minis.

These options allow hedgers to size positions precisely, hedge around specific events like Fed meetings, CPI releases, or major earnings weeks, and do so at a fraction of the capital cost. Protection can be rolled week to week, letting investors adjust to changing conditions without tying up excessive premium budgets.

The Micro weeklies strike the middle ground wherein the long-haul protection of disaster puts can be replaced with more agile and affordable coverage, offering “rolling” caution for the kind of shocks that arrive when least expected.

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs tradingview.com/cme .

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER the link to which is provided in our profile description.

SHORT 1H CHARTnew project short term setups lets go ! i would try to post all my short terms moves.

p.s. i dont trade every day so...

short- local low the target

SL above 61%

Dont take a short position if you didnt short 76% FIBOPossible movement to lick the trendline to the local low. I have a re-entry at the shooting star at 76%, it's not worth going short now.

just wait or go long for couple of days

SL(long) 23.350

NQ - Nasdaq Short Playbook for the next weeksIn the NQ, they took out the high and then hit it on the head day by day. It finally stopped below the 1/4 line. If you look closely, you see that this was the slanted zone of Support — just like the slanted Resistance.

"As above, so below."

...write me in the comments who said this already a couple hundred years ago §8-)

The small Modified Schiff Fork tells a story too.

Price reached the Center Line and got rejected. Now it's on its way down towards the small Fork's L-MLH. A break of it would indicate further selling ahead.

And the last bastion is the green support level, which stems from the second-to-last prior confirmed Swing Low.

Beyond this level, it's only a question of time before price hits the Center Line.

And — God forbid — below the Center Line, the Sh...t hits the fan. So you better run... behind price with a decent short trade and ride it down to the Abyss.

No worries, I'm with you §8-)

Happy Monday, folks!

NQ Bearish BiasNQ is consolidating below a key resistance after a strong selloff from recent highs.

Price failed to hold above 23,750 and is now building a lower-high structure under 23,550.

Unless buyers reclaim that zone, the path of least resistance looks lower with targets near 23,130–23,200.

What do you think? Like and follow for more insightful ideas.

NQ Prediction for week 1-7/09 2025After NQ reaches the reaction area above, we should wait and see if it's start rejecting it to start go lower. Overall bearish, so only bearish trades taken this week until proven wrong (see go higher from rejection)

Thinking the impossibleIm thinking the impossible likeliness of NQ pushing higher testing 24000, before pulling back to create a leg down before moving higher again later. Sept & October is a possible red candle to allow long term buyers to buy at a lower price, perhaps similar to Feb and March pullback or perhaps not. The monthly candles are getting smaller during the past 2 months, which was also demonstrated in Feb and March. Price exhaustion based on a Demark 13 similar to Jun and July 24 before the pullback in August to October 24 adding the conviction of a probable pullback. Nobody can be certain what will happen in the future, just thinking the probable likeliness. Just an idea to ponder.

MNQ Prop Account Risk Management – From $50K to $300K

1) Core funding rules (simple & strict)

Account inputs

Acct = account size

TTD = trailing drawdown buffer your prop gives (e.g., Apex $50K → $2,500)

tickValue and tickSize depend on the product (for MNQ: tickSize = 0.25, tickValue = $0.50, $2.00 per index point)

Budgeting

Daily loss cap (never exceed):

DailyCap = 0.10 × TTD (≈ 10% of TTD)

→ $50K example: 0.10 × 2,500 = $250/day

Per-trade risk (normal):

RiskTrade = 0.50 × DailyCap (≈ 50% of daily)

→ $50K example: 0.50 × 250 = $125/trade

Max trades per day (if all losers):

DailyCap / RiskTrade → typically 2 losses max. Stop trading.

Tip: if you’re warming up or drawdown is tight, use RiskTrade = 0.33 × DailyCap (3 bullets per day).

Position sizing

Choose a stop distance in points from your 15s setup (tight range, reduces variance).

For MNQ:

RiskPerContract = StopPoints × $2.00

Contracts = floor( RiskTrade / RiskPerContract )

Trailing drawdown protection

Hard daily stop: auto-flatten when Unrealized+Realized <= -DailyCap.

Two-strike rule: 2 consecutive full-risk losses → walk away.

No add-to-loser; scale-in only if the first risk is reduced (BE+ or partials).

2) Timeframe workflow (why 15s works)

Context / bias: 10–15-minute chart → trend, key levels, session regime.

Execution: 15-second chart → micro pullback, CHoCH/confirm, ALGTP setup zones.

Psychology: the 10–15m avoids overreacting; 15s keeps risk tight.

Risk discipline: 15s makes it easy to place objective small stops (e.g., 10–20 points MNQ), aligning with prop TTD constraints and avoiding rule violations.

3) Concrete numbers (MNQ examples)

Assume MNQ (Micro NQ):

$2.00 per point per contract (0.25 tick = $0.50)

Three example stops from 15s structure: 10 / 15 / 20 points

Risk per contract

10 pts → $20

15 pts → $30

20 pts → $40

Position sizing formula

Contracts = floor( RiskTrade / (StopPoints × 2) )

4) Scaling plan by account size

I’ll assume TTD ≈ 5% of account (matches Apex 50K→2.5K). If your prop’s TTD differs, just plug your TTD into the same formulas.

Account TTD (≈5%) DailyCap = 10% TTD RiskTrade = 50% of Daily MNQ contracts (10 / 15 / 20-pt stop)

$50K $2,500 $250 $125 6 / 4 / 3 (=$120/$120/$120 used)

$100K $5,000 $500 $250 12 / 8 / 6

$150K $7,500 $750 $375 18 / 12 / 9

$250K $12,500 $1,250 $625 31 / 20 / 15

$300K $15,000 $1,500 $750 37 / 25 / 18

How to read: For the $50K plan with a 20-point stop, Contracts = floor(125 / 40) = 3.

With 15-point stop: floor(125 / 30) = 4. With 10-point: floor(125 / 20) = 6.

Important fine-tuning

If your fills slip or you trail early, reduce Contracts by 1 to keep real risk ≤ plan.

In fast conditions, switch to 10-second (ALGTP’s funding preset) or even 5-second for entries. It shrinks stop distance yet still respects the 10–15m bias.

5) Trade plan checklist (ALGTP flow)

When to trade

Timeframe panel (your “snow” focus): higher-timeframe bias aligned (10–15m green for longs / red for shorts).

Price is above Setup Trigger and confirms at CHoCH/Confirmation Trigger (for longs), or symmetric for shorts.

Momentum not exhausted (avoid entries directly into TP3/TP4 clouds).

When not to trade

Opposite bias on 10–15m.

Entering right into Capital Defense / Max Exhaustion zones.

After 2 full-risk losses or when DailyCap is reached.

Entry & management

Entry at Setup Trigger or micro retest on 15s.

Initial stop just beyond Capital Defense (or last micro-swing).

Partial TP ladder: TP1 (momentum hold), TP2 (intensity), trail to BE+, then leave a runner toward TP3/TP4.

Trailing: switch to smart trailing only after TP1; before that, protect initial risk.

6) Simple formulas you can keep on your desk

DailyCap = 0.10 × TTD

RiskTrade = 0.50 × DailyCap

Risk/contract = StopPoints × $2.00 // MNQ

Contracts = floor( RiskTrade / Risk/contract )

Example (50K, TTD 2,500):

DailyCap = 250

RiskTrade = 125

Stop 15pt → Risk/contract = 15 × 2 = $30

Contracts = floor(125 / 30) = 4

If you also trade MES (Micro S&P): tick $1.25 (0.25 pt), so $5 per point. Replace $2.00 with $5.00 in the formula.

7) Why this is prop-friendly

Keeps risk anchored to TTD, not to account notional.

Forces few, high-quality attempts (2–3 bullets max/day).

15s (or ALGTP’s 10s funding preset) compresses stop distance, making the same TTD support more contracts without violating rules.

The 10–15m bias prevents revenge trading and wrong-direction scalps.

NQ Power Range Report with FIB Ext - 9/4/2025 SessionCME_MINI:NQU2025

- PR High: 23458.25

- PR Low: 23434.25

- NZ Spread: 53.5

Key scheduled economic events:

08:15 | ADP Nonfarm Employment Change

08:30 | Initial Jobless Claims

09:45 | S&P Global Services PMI

10:00 | ISM Non-Manufacturing PMI

- ISM Non-Manufacturing Prices

12:00 | Crude Oil Inventories

Session Open Stats (As of 12:25 AM 9/4)

- Session Open ATR: 299.73

- Volume: 26K

- Open Int: 277K

- Trend Grade: Long

- From BA ATH: -2.3% (Rounded)

Key Levels (Rounded - Think of these as ranges)

- Long: 24382

- Mid: 23239

- Short: 22096

Keep in mind this is not speculation or a prediction. Only a report of the Power Range with Fib extensions for target hunting. Do your DD! You determine your risk tolerance. You are fully capable of making your own decisions.

BA: Back Adjusted

BuZ/BeZ: Bull Zone / Bear Zone

NZ: Neutral Zone

Targets above and below current price for NQ at US OpenTargets above and below current price for NQ at US Open.

NASDAQ on the Edge: Head & Shoulders + Bearish SeptemberOn the daily chart, a clear Head & Shoulders formation has developed: left shoulder in mid-July, head in early August, and right shoulder completed at the end of August. The neckline has been broken with volatility, and price is now retesting the supply zone at 23,600–23,800. This pullback aligns with a weekly area of strong supply, suggesting a potential rejection.

The projected target of the pattern points toward 22,800–22,600, an area overlapping with a key structural support. RSI shows bearish divergence and remains below the midline, reinforcing the short bias.

COT Report (August 26, 2025)

Non-Commercials (funds/speculators): +1,875 longs, -362 shorts → small long increase, but without strong conviction.

Commercials (hedgers): -5,832 longs, -1,579 shorts → clear reduction in long exposure, less bullish protection.

Net change: -5,275 longs → overall unwinding of long positioning, signaling underlying weakness.

Interpretation: Speculators remain net long, but commercials significantly cut exposure, suggesting caution on further upside.

Seasonality (September)

Historically, September has been a negative month for NASDAQ:

10-year average: -148 pts

5-year average: -313 pts

2-year average: -804 pts

The seasonal pattern supports a bearish bias, with weakness usually concentrated in the first half of the month.

Synthesis & Trade Bias

Technical: Bearish Head & Shoulders → target 22,800–22,600.

COT: Net long reduction by commercials → bearish pressure.

Seasonality: September statistically weak.

➡️ Bias: Short on NASDAQ (NQ).

E mini Nasdaq 100. Weekly Outlook. September 01, 2025CME_MINI:NQ1!

Expecting all out meltdown on Nasdaq. And the other two indexes. August was insane. But September will be extremely volatile