MSFT USMicrosoft is currently playing out a beautiful Batman pattern : having broken through the sloping trendline, retested, and also retested at 50 SMA.

However, yesterday, the market pulled the stock above the support level of 490-493, and traders may attempt a rebound after seeing a false breakout.

At the very least, going long in such a situation is very dangerous.

A3minvestments

BABA🌎Alibaba's AI Ambitions Gain Momentum: Qwen's Record-Breaking Launch and Strategic Investments

Alibaba is experiencing strong growth, fueled by the impressive success of its AI assistant, Qwen. Just a week after the public beta release, the app has surpassed 10 million downloads, marking the fastest launch of any such tool in history.

This success signals the company's decisive entry into the consumer AI market and strengthens its position as a direct competitor to ChatGPT and other global leaders in generative AI.

Why Qwen is More Than Just a Chatbot

The company positions Qwen as an "intelligent gateway to everyday life."

Unlike many Western subscription-based models, Alibaba is emphasizing a freemium model and deep integration of AI into its ecosystem. Plans include implementing "agent-based AI" features to automate tasks such as food ordering, travel booking, and shopping on platforms like Taobao.

The app is currently available in China, but an international version is expected soon.

Sizable Investments and Financial Results

To support its ambitions, Alibaba is mobilizing significant resources. The previously announced AI investment plan of RMB 380 billion (~$53 billion) over three years demonstrates a scale comparable to that of American IT giants.

These investments are already bearing fruit:

Revenue Growth: In Q1 FY26, revenue from the Cloud Intelligence division grew 26% year-on-year to RMB 33.4 billion, largely driven by strong demand for AI computing power and cloud services.

Explosive Growth in AI Products: Revenue from AI-based products has shown triple-digit growth for the eighth consecutive quarter, demonstrating the active adoption of technology by enterprises in China.

Increasing the profitability of the cloud business, which is under pressure from the high cost of building AI infrastructure, remains a key challenge.

Technological Innovation in the Face of Restrictions

In response to US export restrictions, Alibaba is finding creative ways to improve efficiency. Aegaeon's recently introduced GPU pooling system dramatically reduces dependence on Nvidia chips. During beta testing, this technology reduced the number of GPUs required by 82%—from 1,192 to 213—to support dozens of AI models.

This achievement highlights the company's ability to mitigate the impact of sanctions through software optimization.

Alibaba is one of the few global platforms offering a full stack of AI services. Strategic investments in promising areas such as international expansion and partnerships (for example, upcoming XPeng robotaxis trials using Amap maps in 2026) provide the foundation for long-term growth.

On the downside, the current stock valuation is already overly optimistic, and sustaining accelerated growth requires continued high investment and impeccable strategy execution.

In our view, we are in Wave 4, where after a strong momentum, the stock needs a breather to continue its growth.

In general, we don't see the stock being distributed. Many factors point to a correction to future growth.

NVDA🌎NVIDIA: At the Peak or the Brink?

Nvidia's record highs are accompanied by warning signs. A market cap of $4.37 trillion and a P/E ratio of 51 indicate inflated expectations.

Risks:

Speculative demand: The $23.7 billion investment looks like an artificial market pump.

Macro threats: The AI boom will face energy shortages.

Historical parallel: The scenario mirrors Cisco's pre-dot-com bubble.

Fierce competition: AMD, Intel, and cloud giants are creating their own chips.

Growth drivers:

Leadership in AI, a closed CUDA ecosystem, and 66% data center revenue growth.

Nvidia is a leader, but its shares have become a high-risk asset. Any slowdown in business performance will lead to a collapse in the stock price.

The baseline scenario is a broad sideways trend.

ADBE📌Revenue for the first six months of FY2025. Year-end revenue: $11.587 billion (up 10.4% y/y)

Net profit for the first six months: $3.502 billion (an impressive 60% y-o-y growth)

Q4 expectations (reported December 10): revenue of $6.075 - $6.125 billion, marking the company's first quarter with revenue exceeding $6 billion.

We're currently seeing a large triangle forming, and we're currently near its lower boundary...📊

ASO📌 Academy Sports recorded sales growth in existing stores for the first time since 2021, demonstrating increased operational efficiency.

The company is capitalizing on the "trade-down" trend, attracting middle- and upper-income shoppers who are switching from higher-priced competitors.

Strategic Drivers of Future Growth:

Digital Transformation: Rapid e-commerce growth (up 18% in the quarter) and the development of omnichannel capabilities strengthen the company's position to capture market share as consumer spending shifts online.

Geographical Expansion: A strategy of opening 20-25 new stores in 2025 in growing regions with underserved markets sets the pace for accelerated revenue growth and improved operating leverage.

Assortment Development: Expanding and improving the product portfolio, including strong private labels with attractive price-quality ratios, is designed to attract a wider audience and support margins.

NFLX📌 A real-life series has developed around the TV series production company.

December 5, 2025: Netflix formally agreed to acquire WBD's studio business and streaming service HBO Max for $82.7 billion (or $27.75 per WBD share). The deal is expected to close in the third quarter of 2026, pending regulatory approval.

December 8, 2025: Paramount Skydance made a hostile counteroffer directly to WBD shareholders. They want to buy the entire company, including cable channels (CNN, TNT Sports), for $108.4 billion ($30 per share).

This is $25-18 billion more than Netflix's offer.

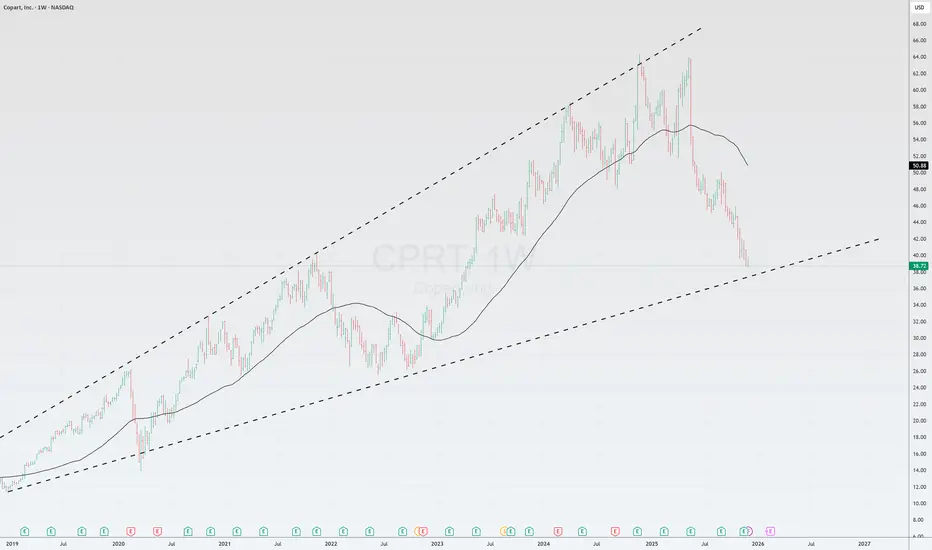

CPRTCopart – A Decade-Long-Term Favorite

In the duopoly with RB Global (RBA), CPRT looks like a premium asset for a long-term portfolio. High margins, outstanding return on equity (ROIC), a debt-free balance sheet with a huge cash position are its foundation

INTCStocks rally after rumors of chip production for Apple and why fundamental problems lurk behind the hype.

Rumors of a partnership are indeed developing, but without official confirmation and with a very long horizon

Key caveat: this only applies to manufacturing (fabrication), not design. Apple will continue to design chips, and Intel will become a manufacturer alongside TSMC.

The report clearly reveals systemic problems

Intel Foundry—a budget hole.

VOO. How are profits fueling the S&P 500 bull rally?The S&P 500 has risen approximately 17.8% year-to-date (including dividends). November was the seventh consecutive month of growth, and we're only about 1% away from all-time highs.

Profits are the main driver.

All the dynamics in 2025 are explained not by speculation, but by fundamentals:

+12.2 pp — earnings growth (EPS)

+4.2 pp — multiple growth (valuation)

+1.4 pp — dividends

That is, 76% of the return came from profits.

DOCU🌎 DocuSign are down after the report despite a strong quarter.

Strengths of Q3 (October):

Revenue: $818.4 million (+8.4% YoY), above expectations - one of the best quarters in 2 years.

IAM platform: already has 25,000+ clients (up from 10,000 in April).

Why did the stock fall after the report and is there an opportunity here?

Forecast for Q4: revenue is within expectations, but not higher than it was in the last quarter.

Slower billing growth: after strong Q2.

DOCU refuses guidance on billings to smooth out volatility from renewals.

We believe that some decline will continue

OCULOcular Therapeutix: A biotech player on the verge of important data.

The company's value is almost entirely tied to the success of its drug AXPAXLI.

This drug could be the first in its class to receive FDA "superiority" status over the current standard of care (aflibercept). Decisive data are expected in Q1 2026.

The designs of all key studies (SOL-1, HELIOS-2) have been pre-approved by the FDA, minimizing regulatory surprises.

Success will open access not only to the wet AMD market (~$15 billion) but also to the larger group of patients with non-diabetic retinopathy (NPDR), for whom there are virtually no available therapies.

The data release schedule is scheduled for years to come (SOL-1 in 2026, SOL-R in 2027), which will regularly fuel interest in the stock.

OCUL is a typical high-risk biotech bet with clear catalysts. Suitable only for the risk-tolerant portion of a portfolio. The key event that will determine the company's fate for years to come is the wet AMD data in early 2026.

So far, all the company's steps have increased confidence in its success.

AMZN🌎 Amazon After Q3: Strength, Strategy, and Attractiveness

A Crash Against a Background of Strength: Amazon shares experienced a short-lived correction along with the broader market, but this move was driven more by general sentiment than by changes in the company's fundamentals.

Quarterly Results as a Turning Point: The third-quarter report was a powerful catalyst, forcing the market to reassess Amazon's trajectory. The company not only beat expectations on both key metrics, but also did so convincingly: earnings per share were 25% above analyst estimates. Following the results, shares soared more than 13%, reflecting investor optimism about growing profitability.

Growth Engines: Retail Gains Momentum, AWS Accelerates

• AWS Returns to Dynamic Growth: The core cloud division has seen growth accelerate to 20% year-over-year, impressive for a business with annual revenue of ~$130 billion. This signals renewed momentum and strengthens Amazon's position in the race for AI leadership.

• Retail Demonstrates Operational Efficiency: Contrary to previous narratives, retail segments (North America and International) are beginning to make a significant contribution to overall return on investment (ROIC). Their operating margins are growing, creating long-awaited operating leverage. This is the result of years of investment in automation and logistics, which are now reducing unit costs and expanding gross margins.

Strategic Advantages in the Age of Autonomy: Amazon Structurally Benefits from Macro Trends

1. Automation as a Flywheel: The implementation of autonomous systems compresses costs, allowing the company to simultaneously increase margins and reduce prices for the end consumer. This creates a self-sustaining cycle: volume growth, increased operating leverage, EPS growth, and additional investments in efficiency.

2. Vertical Integration: Control over the supply chain from logistics centers to AWS cloud infrastructure creates a unique, difficult-to-replicate barrier to entry for competitors and ensures long-term cash flow stability.

Value Issue: Not Cheap, but Reasonable

Despite the jump in its stock price, Amazon doesn't appear overvalued compared to its peers.

• With a forward P/E of around 38x, the company trades at a significant discount to its five-year average.

• Compared to other Magnificent 7 companies, Amazon represents a reasonable value, especially compared to more expensive NVDA or TSLA.

• High capital expenditures ($116 billion over 12 months) directed at AI infrastructure are temporarily putting pressure on free cash flow. This is an investment in future growth, but investors should consider this factor.

Summarizing the quarter's data and strategic vectors, the positive scenario for Amazon outweighs the risks (regulatory pressure, cyclical spending, cloud competition).

Amazon combines maturity and operational efficiency with acceleration potential thanks to AWS and automation.

We consider Amazon one of the best companies among the M7 and that it will soon show one of the best results in the Magnificent 7.

In our view, the corrective movement of the 4th wave is ending, and the stock will soon be setting new all-time highs.

MXL🌎 MaxLinear as a compelling turnaround story with strong momentum in key growth markets. The company is a supplier of chips for networks and data centers, showing accelerating financial performance. Key drivers included:

Exceptional Q3 2025 Results: Revenue reached $126.5 million, marking a significant +56% growth YoY and +16% QoQ. The company also returned to non-GAAP profitability with EPS of $0.14, exceeding guidance.

Explosive Growth in Infrastructure: The infrastructure segment (data centers, 5G) delivered revenue of $40 million, surging +75% YoY, highlighting exposure to high-demand areas.

Strong Outlook & Multi-Year Potential: Management provided an optimistic Q4 2025 guide (revenue: $130-140 million) and stated the infrastructure segment revenue could grow to $300-500 million within 2-3 years.

Key Product Momentum: The Keystone PAM4 DSP product for 800G optics (critical for AI infrastructure) has been qualified in major US and Asian data centers, with 2025 revenue expected at $60–70 million.

Improving Profitability & Cash Flow: This was the third consecutive quarter of double-digit revenue growth and the second quarter of non-GAAP profitability. The company generated positive operating cash flow of $10.1 million, and margins are expanding (non-GAAP operating margin improved to 12% from 7% in Q2), indicating that further growth will be highly profitable.

ST🌎 Sensata Technologies as a strong performer driven by exceptional quarterly results and strategic contracts.

Q3 2025 results that exceeded expectations across all key metrics.

Revenue and adjusted operating margin (19.3%) came in above the upper bound of company guidance.

A record FCF conversion rate of 105%, demonstrating effective working capital management and a strong ability to generate cash for investments, shareholder distributions, and debt reduction.

A strategic shift in capital allocation, with a focus on debt reduction: net leverage decreased to 2.9x.

Upbeat management guidance for Q4 2025, expecting to maintain high operating margins (19.3% to 19.5%), with revenue of $890-920 million and adjusted EPS of $0.83-$0.87.

Significant growth potential from new business, with major contracts signed with automakers. The potential addressable market in the US alone exceeds $100 million.

Since the beginning of 2022, the stock has been in a downward trend, driven by deteriorating financial and operational performance and a valuation that is inconsistent with its high price.

The market is attempting to break the downward trend in the stock. This is the second time the stock has successfully tested the moving average and the downtrend line from above, which is the first time this has happened since 2022.

EUR/USD🌎 EUR/USD: The rally ends and a deep decline is in the offing

Having received confirmation from fundamental factors, the pair is preparing to move significantly below current levels.

Now, in order:

TECHNICAL ANALYSIS

All five waves of the upward impulse have ended. The fifth wave closes at 1.1918.

A key ascending trendline has been broken. The subsequent retest of this level confirmed the trend change.

Wave A completed at 1.1468.

Wave B (corrective). A pullback is underway, creating the potential for the next powerful downward impulse wave—wave C.

The price is currently testing the moving average (MA) from below. There are two scenarios:

Scenario 1: A rebound from the MA and a decline begins immediately from there.

Scenario 2: A false upward breakout of the MA, followed by a downward reversal.

In both cases, the outcome is the same—a move down to new lows.

Why is the euro under pressure?

Weak macroeconomic data: PMI, retail sales, industrial production—all point to a loss of economic momentum.

Inflation (2.1%) and core inflation (2.4%) are close to the ECB's target, but the trend points to a decline, not an increase, creating deflationary risks.

Supply and demand issues: Consumer confidence is falling, manufacturers are struggling. All points to a deflationary scenario.

Markets are confident that the ECB will not hike rates in December.

The Fed's attractive interest rate maintains its advantage over the ECB (carry trade).

The US economy is showing relative resilience amid a slowdown in Europe and China.

The Fed needs to borrow more, and this rollover of a large amount of government debt leads to liquidity absorption and creates technical support for the dollar.

Alternatively, unexpectedly strong inflation/wage data in the EU could temporarily support the euro and prolong the correction (wave B), but this would only shift this scenario to the right and is unlikely to change the overall picture.

A3M

EL🌎 The company is undergoing a major restructuring, delegating profit and loss management responsibilities to regions and achieving significant cost savings, which could lead to a much faster and more significant return to profitability than expected.

Growth will be driven by several key factors: entering new markets through platforms like Amazon and Tmall, supported by AI-powered personalization; active expansion in Latin America and Southeast Asia; and an increased share of direct sales, which increases average order value and customer loyalty. Furthermore, growing demand for premium health and skincare products is fueling the company's broad portfolio of science-based products.

According to an optimistic scenario, revenue could reach $16.8 billion and net profit $1.6 billion by 2028.

In June, the downward trend was broken.

The market believes in the company's strategy, and the $85 level is holding up well for now.

Around $100, the stock needs to be closely monitored.

Until the market sees real changes in the company's performance based on the new strategy, the stock will have a hard time breaking resistance.

ADSK🌎 Autodesk is riding the wave of AI and data center construction, posting its fastest growth in three years.

All key report metrics—revenue, profit, and billing—competitively beat forecasts.

Resistance is around $326.

Strong fundamentals create good potential for a breakout to new highs.

CTRI US🌎 Centuri Holdings (CTRI) is demonstrating strong operating growth and a transition to sustainable profitability.

Key factors that could trigger a breakout from the range include:

record quarterly revenue, a strong order book providing transparency into future cash flows, and a strong market signal from Carl Icahn's large share purchase.

The stock is within the range and approaching its upper limit, while the upper slope of the RSI has been broken upwards.

WTI🌎 Major investment banks forecast two stages for oil: a decline due to oversupply, followed by growth from 2027 due to a lack of investment.

After 2027: A prolonged growth period will begin due to a shortage of raw materials.

A gradual, slow decline in oil prices is observed.

We are near a support level, a break of which could accelerate the decline in prices.

QGEN🌎 Qiagen N.V. is a Dutch holding company and global provider of molecular diagnostics and life sciences solutions.

Core activities:

Sample processing technologies: Extraction and processing of DNA, RNA, and proteins from blood, tissue, and other materials.

Analysis technologies: Preparation of biomolecules for analysis.

Bioinformatics: Software and knowledge bases for data interpretation and practical applications.

Key products and platforms:

QuantiFERON: A test for the diagnosis of latent tuberculosis

QIAstat-Dx: A syndromic testing system for the simultaneous detection of a broad range of pathogens

QIAcuity: A digital PCR system

QIAGEN Digital Insights (QDI): A bioinformatics division

The company serves more than 500,000 customers worldwide in the life sciences (academic institutions, pharmaceutical R&D, forensic medicine) and molecular diagnostics.

In the second quarter of 2025, revenue reached $533.54 million, exceeding the consensus estimate.

The company expects to achieve its mid-term adjusted operating margin target of 31% by 2025, above its initial 2028 guidance.

Management increased its full-year 2025 adjusted earnings per share guidance to approximately $2.35 per year from the previous $2.28.

In 2025, Qiagen received CE-IVDR certification for its entire QIAstat-Dx portfolio in Europe and US FDA approval for the QIAstat-Dx Rise system.

The stock is trading broadly sideways at the upper end of the channel.

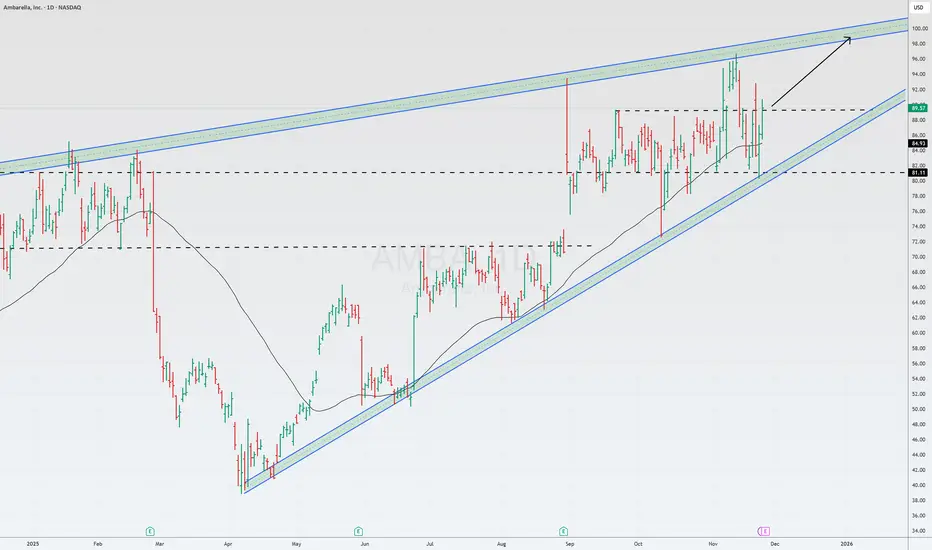

AMBA US🌎 Ambarella is demonstrating impressive revenue growth, exceeding 50% year-on-year, thanks to a strategic shift in focus from the automotive market to the Internet of Things (IoT). IoT, rather than the once-primary focus of autonomous vehicles, now generates the majority of revenue and is a key driver behind the company's improved financial outlook.

Ambarella's investment case was previously based on promising but slowly developing autonomous driving projects. Today, 75% of its revenue comes from the IoT segment, which includes not only surveillance cameras but also wearable cameras, robotics, and edge computing equipment.

The foundation of this success is the new CV5/CV7 processors, manufactured using 5nm technology. These chips are unique in their ability to combine image processing, video encoding, and artificial intelligence on a single chip. This integration allows the company to offer more powerful solutions for compact, power-constrained devices (such as drones or video cameras) and set high prices, avoiding direct price competition with lower-cost manufacturers.

The short product development cycle for IoT allows R&D investments to be converted into revenue more quickly compared to the long cycle time for automotive products. Using a common technology platform (CVflow) for both IoT and automotive applications reduces development costs.

Cons:

Growth is not converting into significant free cash flow. There is a worrying dependence on a single distributor (WT Microelectronics, 71% of revenue) and a single manufacturer (Samsung), creating supply chain risks. High chip production costs may begin to pressure profitability.

NVO USThe decline in Novo Nordisk shares is not the result of a single factor, but rather the result of a complex set of fundamental issues: weakening financial performance, loss of competitive advantage in key products, and increased strategic risks.

While negative data on Eli Lilly's weight loss pill in August 2025 triggered a temporary optimistic rebound in NVO shares, it failed to reverse the overall downward trend caused by the company's deeper structural problems.

Now, in order:

Operating and Financial Results

Sales and operating profit growth forecasts for 2025 have been lowered twice; Q3 2025 results below expectations

Operating margin fell to 41.7% from 44.7% (YoY), gross margin decreased to 81.0% from 84.6%

Free cash flow declined 11% due to a sharp increase in capital expenditures

Competitive pressure:

Superiority of Eli Lilly products.

Zepbound (Eli Lilly) demonstrates greater effectiveness in weight loss (20.2% vs. 13.7% for Wegovy); Mounjaro overtook Ozempic in diabetes sales.

NVO's CagriSema failed to meet expectations in clinical trials.

Companies such as Viking Therapeutics, Altimmune, Roche, and Amgen are developing promising anti-obesity drugs, threatening the Novo Nordisk-Eli Lilly duopoly.

The company recently agreed to set a "maximum fair price" for Medicare under the Inflation Reduction Act.

As a result of the deal, the price of Wegovy for certain patient categories is also expected to drop to $149 per month, compared to the current starting price of $1,349. Such a sharp price reduction will directly impact revenue and profits.

Novo Nordisk's share of the US GLP-1 market fell to 43%, while Eli Lilly's grew to 57%.

To protect profitability, Maziar's new CEO, Mike Dusdar, initiated stringent cost-cutting measures, including a hiring freeze, layoffs, and a 23.8% reduction in R&D spending. While this may support cash flow in the short term, this strategy raises concerns about long-term innovation. Eight R&D projects were terminated, potentially slowing the market launch of promising next-generation drugs such as CagriSema and oral semaglutide.

NVO shares attempted a reversal around $60, but then this figure became a mirror level, and investors sold en masse from this price, which is certainly concerning. The chart shows volumes around $60. Be that as it may, the price is now below $50, and we can see the market trying to catch a low, trying to cling to any level. We're expecting a lower price.

QCOM US🌎Qualcomm has several compelling drivers for future growth, the most important of which are successful business diversification and an ambitious entry into the new data center market.

Key growth drivers:

Entering the AI data center market.

The company signed its first contract with startup Humane to deploy a 200-megawatt infrastructure starting in 2026.

Diversification and growth beyond smartphones

Automotive segment: revenue exceeded $1 billion in the quarter, with year-over-year growth of 21-36%.

- IoT segment: revenue grew by 22-24% year-over-year.

Report:

Record annual revenue of the QCT division: ~$44 billion

High margins: EBITDA margin of 31%, net profit margin of 26%

Shares are trading at a significant discount to peers.