DigitalOcean (DOCN) — AI-Native Cloud for Developers & StartupsCompany Overview

DigitalOcean NYSE:DOCN is a developer-first cloud riding surging AI infra demand. Its Gradient AI Agentic Cloud simplifies building, deploying, and scaling AI apps—positioning DOCN as a cost-efficient alternative to hyperscalers for startups and SMBs.

Key Catalysts

Explosive AI Momentum: Direct AI revenue more than doubled YoY for 5 straight quarters (Q3’25)—evidence of sticky developer adoption.

Topline Acceleration: Revenue +16% YoY with record ARR increase; management raised 2026 growth outlook to 18–20%.

Partner Ecosystem: Strategic AI partnerships expand model access, tooling, and go-to-market, reinforcing platform pull.

Value Proposition: Simple pricing, lower TCO, and a curated stack for agentic/LLM apps drive share gains vs. complex large-cloud offerings.

Investment Outlook

Bullish above: $45–$46

Target: $80–$82 — supported by sustained AI revenue compounding, raised guide, and a durable niche in SMB/AI-native workloads.

📌 DOCN — the pragmatic AI cloud for builders who want speed, simplicity, and savings.

Cloudcomputing

CoreWeave: The Trump-Backed AI Power PlayPresidential portfolios rarely scream "growth stock," but recent financial disclosures change the narrative. Donald Trump purchased over $50 million in corporate bonds, including debt from AI infrastructure unicorn CoreWeave (CRWV). This move places the GPU cloud provider alongside established industrial titans. Investors must now decide if this political endorsement aligns with fundamental value.

Geopolitics and Geostrategy

The executive branch views Artificial Intelligence as a sovereign asset. CoreWeave’s infrastructure directly supports U.S. dominance in the global AI arms race. By financing domestic GPU capabilities, the administration signals a strategic pivot away from foreign reliance. This investment acts as a tacit endorsement of CoreWeave’s role in national security. The company is no longer just a cloud provider; it is a critical national infrastructure.

Business Models and Economics

CoreWeave rejects the speculative excesses of the dot-com era. Management utilizes a disciplined "take-or-pay" revenue model. They only deploy capital expenditure after signing five-year customer contracts. These agreements cover infrastructure costs and debt service immediately. This strategy reduced financing costs significantly, securing recent funding at highly competitive rates. The company builds to meet existing demand, not anticipated hype.

Industry Trends and Financials

The financial data reveals explosive momentum. Third-quarter revenue hit $1.4 billion, a staggering 134% year-over-year increase. The revenue backlog swelled to $55 billion, nearly quadrupling since the year began. This backlog confirms that demand for high-performance computing far outstrips supply. Unlike legacy cloud providers, CoreWeave offers pure-play AI exposure.

Technology and Innovation

Hardware is useless without intelligent orchestration. CoreWeave’s proprietary software, "Mission Control," serves as its technological moat. This layer autonomously manages operations to maximize performance and extend GPU lifespan. Industry experts awarded CoreWeave the exclusive Platinum ClusterMAX ranking twice. No other cloud provider holds this distinction. This technical superiority drives customer retention, evidenced by early contract renewals at near-original prices.

Management and Leadership

Executive leadership actively mitigates concentration risk. At the start of 2025, a single customer held 85% of the backlog. Today, no client exceeds 35%. Furthermore, over 60% of this backlog now comes from investment-grade entities. Management proved their transparency by lowering 2025 guidance due to third-party construction delays. They prioritized realistic communication over inflating short-term expectations.

Macroeconomics and Future Outlook

The macroeconomic environment favors infrastructure builders. Forecasts suggest revenue will skyrocket to $29 billion by 2028. Adjusted earnings per share could swing from a loss to $4.51 in the same period. If the stock trades at a reasonable 35x forward earnings, CRWV offers over 55% upside. The market consensus rates the stock a "Strong Buy" with a $124.70 price target.

Conclusion

CoreWeave combines political tailwinds with elite technical execution. The Trump debt purchase validates the company's stability. However, the $55 billion backlog serves as the true buy signal. For investors seeking direct exposure to the engine room of the AI economy, CoreWeave represents a high-conviction opportunity.

BABA trade ideaI think entry area between 125-140 if falling wedge broken, its strong support there with 200ma and MACD, PT +200.

SPS Commerce | SPSC | Long at $77.51SPS Commerce NASDAQ:SPSC is a leading cloud-based supply chain management software provider, specializing in electronic data interchange (EDI), fulfillment, and e-commerce integration solutions. Key customers include major retailers like Walmart NYSE:WMT , Target NYSE:TGT , Home Depot NYSE:HD ; Procter & Gamble NYSE:PG , Nestlé OTC:NSRGY ; Sysco NYSE:SYY , and US Foods NYSE:USFD . As of 2025, SPS Commerce serves over 12,000 customers and connects to more than 100,000 trading partners globally.

Technical Analysis

The price fell through my "crash" simple moving average zone (green lines). This area is often an algorithmic share accumulation zone. The price spiked into the "crash" zone as the day went by after the earnings release. While this is still a high growth stock, there is still risk with the slowing economy, P/E ratio of 36x, and two open price gaps on the daily chart near $58 and $38. These price gaps will likely get filled if the US enters a recession, but are we really there yet? Depending on where you look (retail vs tech), there answer varies. But my bets are no - publicly. There is usually a Christmas rally every year, and NASDAQ:SPSC is in "oversold" territory in the near term. The price may dead cat bounce to $53, but I suspect it would take major negative economic news or a breakdown in company fundamentals to get there.

Financial Health

Debt-to-equity: 0x (healthy)

Quick ratio / ability to pay current bills: 1.5 (healthy / able to pay)

Altman's Z Score / bankruptcy risk: 19 (extremely low risk)

Earnings and Revenue Growth

Earnings per share growth from 2024 ($3.48) to 2028 ($6.52): 87.4%

Revenue growth from 2024 ($638 million) to 2028 ($1.03 billion): 61.4%

www.tradingview.com

Action

Given the overall health of the company, potential for a Christmas rally, and technical analysis "crash" entry, NASDAQ:SPSC is in a personal buy zone at $77.51.

Targets into 2028

$90.00 (+16.1%)

$100.00 (+29.0%)

Can Data Giants Survive Their Own Success?Snowflake Inc. (NYSE: SNOW) stands at a critical crossroads, facing what the report describes as a "perfect storm of converging headwinds." Despite beating Q3 fiscal 2026 analyst estimates with $1.21 billion in revenue (up 29% year-over-year), the stock plummeted as investors focused on decelerating growth rates and concerning forward guidance. The company that once epitomized cloud data warehousing dominance is now fighting a multi-front war against aggressive competitors, shifting technological paradigms, and macroeconomic pressures that have fundamentally altered SaaS valuations.

The report identifies several structural threats eroding Snowflake's competitive position. Databricks has emerged as the ascendant force, recently valued at $100 billion compared to Snowflake's ~$88 billion market cap, while growing revenue at over 50% annually versus Snowflake's 29%. The rise of Apache Iceberg, an open table format that allows customers to store data in cheap object storage rather than Snowflake's proprietary system, threatens to cannibalize the company's high-margin storage revenue stream. Additionally, Net Revenue Retention has declined from peaks exceeding 150% to 125%, signaling saturation among enterprise customers and difficulty expanding usage within existing accounts.

Beyond competitive dynamics, Snowflake faces macroeconomic and geopolitical challenges that further complicate its challenges. The end of near-zero interest rates has compressed valuations for high-duration growth stocks. At the same time, enterprises have shifted IT spending from cloud migration to optimization and AI infrastructure budget dollars flowing toward GPUs and LLM training rather than traditional data warehousing. The 2024 credential-stuffing attacks on customer accounts, though not a platform breach, damaged Snowflake's "secure by design" reputation precisely when data sovereignty concerns and regulatory fragmentation are forcing costly infrastructure deployments across multiple jurisdictions. The company must execute a flawless pivot to AI-powered analytics while embracing open formats without destroying its business model, a classic innovator's dilemma that will determine whether Snowflake can reclaim its former market dominance or settle into mature, commoditized utility status.

Is Cisco Building the Internet of Tomorrow or Something Else?Cisco Systems has undergone a dramatic transformation in 2025, evolving from a traditional hardware vendor into what the company positions as the architect of secure, AI-driven global infrastructure. With fiscal year 2025 revenue reaching $56.7 billion and a remarkable 30% surge in operating cash flow, Cisco's financial performance tells only part of the story. The company has strategically positioned itself at the intersection of three critical technological timelines: the immediate AI infrastructure boom, the ongoing geopolitical supply chain realignment, and the long-term quantum computing development.

The company's geopolitical strategy has been particularly aggressive. In response to escalating US-China trade tensions and tariffs reaching up to 145% on certain components, Cisco has pivoted its manufacturing operations to India, establishing it as a new global export hub. Simultaneously, the company launched its Sovereign Critical Infrastructure portfolio in Europe, offering air-gapped solutions that address European concerns about digital sovereignty and US extraterritorial reach. These moves position Cisco as the "trusted vendor" for Western alliance infrastructure while monetizing the fragmentation of the global internet.

On the technology front, Cisco has made bold bets on the future. A landmark partnership with IBM aims to build the world's first large-scale quantum network by the early 2030s, with Cisco developing the optical infrastructure to connect quantum processors. The company has also integrated SpaceX's Starlink into its SD-WAN portfolio and participated in NASA's Artemis program. Meanwhile, its AI-native Hypershield security platform, protected by the company's 25,000th patent, and the integration of the Splunk acquisition demonstrate Cisco's push into AI-era cybersecurity.

The convergence of these initiatives reveals a company no longer simply selling networking equipment, but rather positioning itself as essential infrastructure for Western technological sovereignty. With explosive demand from hyperscaler customers generating over $2 billion in AI infrastructure orders and analysts raising price targets amid a 25% stock rally, Cisco appears to have successfully weaponized the geopolitical moment to reinforce its market position for the next generation of computing.

Is Silicon's Silent Giant Rewriting the Rules of AI?Broadcom has emerged as a critical, yet understated, architect of the artificial intelligence revolution. While consumer-facing AI applications dominate headlines, Broadcom operates in the infrastructure layer, designing custom chips, controlling networking technology, and managing enterprise cloud platforms. The company maintains a 75% market share in custom AI accelerators, partnering exclusively with Google on their Tensor Processing Units (TPUs) and recently securing a major deal with OpenAI. This positioning as the "arms dealer" of AI has propelled Broadcom to a $1.78 trillion valuation, making it one of the world's most valuable semiconductor companies.

The company's strategy rests on three pillars: custom silicon dominance through its XPU platform, private cloud control via the VMware acquisition, and aggressive financial engineering. Broadcom's technical expertise in critical areas like SerDes technology and advanced chip packaging creates formidable barriers to competition. Their Ironwood TPU v7, designed for Google, delivers exceptional performance through innovations in liquid cooling, massive HBM3e memory capacity, and high-speed optical interconnects that allow thousands of chips to function as a unified system. This vertical integration from silicon design to enterprise software creates a diversified revenue model resistant to market volatility.

However, Broadcom faces significant risks. The company's dependence on Taiwan Semiconductor Manufacturing Company (TSMC) for production creates geopolitical vulnerability, particularly given rising tensions in the Taiwan Strait. U.S.-China trade restrictions have compressed certain markets, though sanctions have also consolidated demand among compliant vendors. Additionally, Broadcom carries over $70 billion in debt from the VMware acquisition, requiring aggressive deleveraging despite strong cash flows. The company's controversial shift to subscription-based pricing for VMware, while financially successful, has generated customer friction.

Looking ahead, Broadcom appears well-positioned for the continued AI infrastructure buildout through 2030. The shift toward inference workloads and "agentic" AI systems favors application-specific integrated circuits (ASICs) over general-purpose GPUs Broadcom's core strength. The company's patent portfolio provides both offensive licensing revenue and defensive protection for partners. Under CEO Hock Tan's disciplined leadership, Broadcom has demonstrated ruthless operational efficiency, focusing exclusively on the highest-value enterprise customers while divesting non-core assets. As AI deployment accelerates and enterprises embrace private cloud architectures, Broadcom's unique position spanning custom silicon, networking infrastructure, and virtualization software establishes it as an essential, if largely invisible, enabler of the AI era.

A10 Networks (ATEN) — DDoS, ADC, and Edge Security TailwindsCompany Overview

A10 Networks NYSE:ATEN provides advanced cybersecurity and application delivery across cloud, hybrid, and carrier networks—direct exposure to rising demand for DDoS protection, secure networking, and cloud infra security.

Key Catalysts

Threat Landscape & Compliance: Escalating global cyberattacks + stricter regs are accelerating adoption of Thunder ADC and ThreatX—mission-critical for high-performance, distributed environments.

Execution Momentum: Q3’25 revenue $75M (≈+5.6% beat) and EPS $0.17 (≈+9.7% beat) underscore resilient demand and leverage to a recovering IT spend cycle.

5G & AI Infrastructure: A10’s load balancing, DDoS, and edge security sit in the flow of 5G rollouts and AI data center growth, supporting multi-year capacity upgrades.

Platform Differentiation: Carrier-grade performance, automation, and visibility help consolidate point tools while optimizing latency and throughput.

Why It Matters

✅ Direct play on cloud + telco capex (5G/edge)

✅ Beneficiary of AI-era traffic growth and low-latency requirements

✅ Balanced mix of appliance, software, and subscription helps cushion cycles

Investment Outlook

Bullish above: $14.75–$15.00

Target: $22.00–$23.00 — driven by enterprise/telco upgrades, AI/edge security demand, and continued operating discipline.

📌 ATEN — securing next-gen networks with high-performance ADC and DDoS protection.

Can One Company Control Computing's Future?Google has executed a strategic transformation from a digital advertising platform to a full-stack technology infrastructure provider, positioning itself to dominate the next era of computation through proprietary hardware and breakthrough scientific discoveries. The company's vertical integration strategy centers on three pillars: custom Tensor Processing Units (TPUs) for AI workloads, quantum computing breakthroughs with verifiable advantages, and Nobel Prize-winning drug discovery capabilities through AlphaFold. This approach creates formidable competitive barriers by controlling foundational computational infrastructure rather than relying on commodity hardware.

The TPU strategy exemplifies Google's infrastructure lock-in model. By designing specialized chips optimized for machine learning tasks, Google achieved superior energy efficiency and performance scaling compared to general-purpose processors. The company's multibillion-dollar deal with Anthropic, deploying up to one million TPUs, transforms a potential cost center into a profit generator while locking competitors into Google's ecosystem. This technical dependence makes migration to rival platforms financially prohibitive, ensuring Google monetizes a significant portion of the generative AI market through its cloud services regardless of which AI models succeed.

Google's quantum computing achievement represents a paradigm shift from theoretical benchmarks to practical utility. The Willow chip's "Verifiable Quantum Advantage" demonstrates a 13,000-times speedup over classical supercomputers in physics simulations, with immediate applications in molecular structure mapping for drug discovery and materials science. Meanwhile, AlphaFold delivers quantifiable economic impact, reducing Phase I drug development costs by approximately 30% from over $100 million to $70 million per candidate. Isomorphic Labs has secured nearly $3 billion in pharmaceutical partnerships, validating this high-margin revenue stream independent of advertising.

The geopolitical implications are profound. Google holds the second-highest number of quantum technology patents globally, with strategic IP covering essential scaling technologies like chip tiling and error correction. This intellectual property portfolio creates a technical chokepoint, positioning Google as a mandatory licensing partner for nations seeking to deploy quantum technology. Combined with the dual-use nature of quantum computing for both commercial and military applications, Google's dominance extends beyond market competition to national security infrastructure. This convergence of proprietary hardware, scientific breakthroughs, and IP control justifies premium valuations as Google transitions from cyclical advertising dependence to an indispensable deep-tech infrastructure provider.

Is IBM Building an Unbreakable Cryptographic Empire?IBM has positioned itself at the strategic intersection of quantum computing and national security, leveraging its dominance in post-quantum cryptography to create a compelling investment thesis. The company led the development of two of the three NIST-standardized post-quantum cryptographic algorithms (ML-KEM and ML-DSA), effectively becoming the architect of global quantum-resistant security. With government mandates like NSM-10 requiring federal systems to migrate by the early 2030s, and the looming threat of "harvest now, decrypt later" attacks, IBM has transformed geopolitical urgency into a guaranteed, high-margin revenue stream. The company's quantum division has already generated nearly $1 billion in cumulative revenue since 2017—more than tenfold that of specialized quantum startups—demonstrating that quantum is a profitable business segment today, not merely an R&D cost center.

IBM's intellectual property moat further reinforces its competitive advantage. The company holds over 2,500 quantum-related patents globally, substantially outpacing Google's approximately 1,500, and secured 191 quantum patents in 2024 alone. This IP dominance ensures future licensing revenue as competitors inevitably require access to foundational quantum technologies. On the hardware front, IBM maintains an aggressive roadmap with clear milestones: the 1,121-qubit Condor processor demonstrated manufacturing scale in 2023, while researchers recently achieved a breakthrough by entangling 120 qubits in a stable "cat state." The company targets deployment of Starling, a fault-tolerant system capable of running 100 million quantum gates on 200 logical qubits, by 2029.

Financial performance validates IBM's strategic pivot. Q3 2025 results showed revenue of $16.33 billion (up 7% year-over-year) with EPS of $2.65, beating forecasts, while adjusted EBITDA margins expanded by 290 basis points. The company generated a record $7.2 billion in year-to-date free cash flow, confirming its successful transition toward high-margin software and consulting services. The strategic partnership with AMD to develop quantum-centric supercomputing architectures further positions IBM to deliver integrated solutions at exascale for government and defense clients. Analysts project IBM's forward P/E ratio may converge with peers like Nvidia and Microsoft by 2026, implying potential share price appreciation to $338-$362, representing a unique dual thesis of proven profitability today combined with validated high-growth quantum optionality tomorrow.

GDS Holdings (GDS) – Bullish Setup in the AI-Data Center BoomGDS Holdings Limited NASDAQ:GDS is emerging as a key player in Asia’s data infrastructure race, positioned to capitalize on explosive demand for AI-ready, high-density data centers.

🔍 Thesis Summary:

$1.2B Series B Equity Raise Completed

Backed by SoftBank Vision Fund & Ken Griffin, funding will enable >1 GW new capacity. A massive expansion push in China & Southeast Asia, where demand for digital infra is accelerating.

AI Wave = Data Center Surge

GDS is well-positioned to benefit from the rise in AI workloads, which require low-latency, high-power density facilities. Their premium sites in top-tier Asian hubs make them a first-choice provider.

Strategic Advantages Noted by Analysts

Raymond James cites rare access to land & power near major Chinese metros — a barrier to entry that protects margins & boosts scalability.

📊 Trade Setup:

Bullish above $33–$34

Upside target: $50–$52

Arm Holdings (ARM): Bullish Outlook on Structural Growth ThemesArm Holdings NASDAQ:ARM is a semiconductor IP powerhouse driving innovation across AI, mobile, data centers, and IoT. With its high-performance, low-power chip architectures, Arm remains foundational to next-gen computing infrastructure.

🔍 Key Fundamentals:

Market Dominance: Arm holds a leading position in semiconductor IP, backed by deep R&D investment and expanding licensing with top global chipmakers.

Revenue Momentum: Recent earnings show strong revenue growth, underpinned by rising global demand for Arm-based designs.

AI & Cloud Pivot: Major cloud providers are rapidly adopting Arm-based server architectures, reflecting Arm’s shift into AI and enterprise computing.

IoT & Automotive Expansion: With increasing compute needs in vehicles and smart devices, Arm’s low-power design edge is unlocking new growth verticals.

📈 Technical Perspective:

We're bullish above the $120.00–$122.00 zone, with an upside target of $270.00–$275.00 based on structural demand growth and strategic diversification.

#ARM #ArmHoldings #Semiconductors #AIStocks #TechStocks #IoT #CloudComputing #ChipStocks #NVIDIA #DataCenter #BullishBreakout

Domo, Inc. | Bullish Setup Amid Strong AI Momentum📊 Domo, Inc. NASDAQ:DOMO is a cloud-based data intelligence platform helping enterprises manage and visualize data at scale.

☁️ Recent strategic expansions with Snowflake and AWS are enhancing its data integration stack and building out a competitive ecosystem.

🏆 Ranked #1 in Dresner’s 2025 Agentic AI Report, validating Domo’s leadership in AI-powered analytics—key for long-term growth.

📈 Analysts are bullish: 4 Buy ratings, 0 Sell, with a consensus price target of $18.50 (~18.7% upside from current levels).

🔍 Technical View:

• Bullish Above: $14.00–$14.25

• Upside Target: $27.00–$28.00

• Trend: Reversal setup possible with continued institutional support.

This setup offers potential for mid-term upside, especially if bullish volume confirms above the $14.25 pivot zone.

💡 Watching for continuation as AI and data analytics tailwinds accelerate across the enterprise sector.

🔔 Like, follow, and comment if you're watching DOMO too.

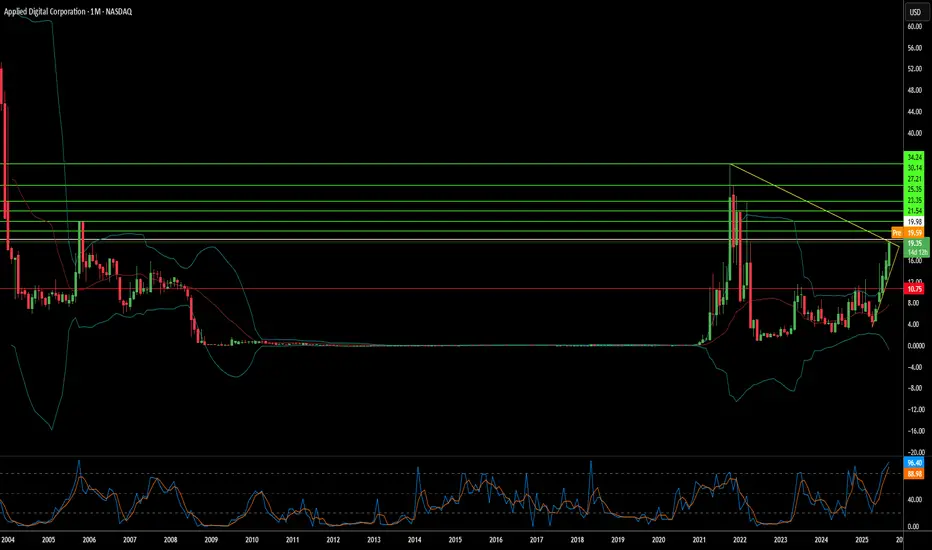

Can a Crypto Miner Become an AI Infrastructure Giant?Applied Digital Corporation has undergone a dramatic transformation, pivoting from cryptocurrency mining infrastructure to become a key player in the rapidly expanding AI data center market. This strategic shift, completed in November 2022, has resulted in extraordinary stock performance with shares surging over 280% in the past year. The company has successfully repositioned itself from serving volatile crypto clients to securing long-term, stable contracts in the high-performance computing (HPC) sector, fundamentally de-risking its business model while capitalizing on the explosive demand for AI infrastructure.

The company's competitive advantage stems from its purpose-built approach to AI data centers, strategically located in North Dakota to leverage natural cooling advantages and access to abundant "stranded power" from renewable sources. Applied Digital's Polaris Forge campus can achieve over 220 days of free cooling annually, significantly outperforming traditional data center locations. This operational efficiency, combined with the ability to utilize otherwise curtailed renewable energy, creates a sustainable cost structure that traditional operators cannot easily replicate through simple retrofitting of existing facilities.

The transformative CoreWeave partnership represents the cornerstone of Applied Digital's growth strategy, with approximately $11 billion in contracted revenue over 15 years for a total capacity of 400 MW. This massive contract provides unprecedented revenue visibility and validates the company's approach to serving AI hyperscalers. The phased buildout schedule, commencing with a 100 MW facility in Q4 2025, provides predictable revenue growth while the company pursues additional hyperscale clients to diversify its customer base.

Despite current financial challenges including negative free cash flow and steep valuation multiples, institutional investors holding 65.67% of the stock demonstrate confidence in the long-term growth narrative. The company's success will ultimately depend on the execution of its buildout plans and ability to capitalize on the projected $165.73 billion AI data center market by 2034. Applied Digital has positioned itself at the intersection of favorable macroeconomic trends, geostrategic advantages, and technological innovation, transforming from a volatile crypto play into a strategic infrastructure provider for the AI revolution.

Pegasystems (PEGA) — Growth via AI & Cloud PartnershipsCompany Overview:

Pegasystems Inc. NASDAQ:PEGA is a leader in enterprise software, specializing in business process management and customer engagement solutions. Its offerings enable organizations to enhance efficiency, scalability, and customer experience, positioning it well within the fast-growing digital transformation market.

Key Catalysts:

AI acceleration: The Pega GenAI Blueprint platform reduces development time, delivering stronger ROI for clients such as Vodafone.

Cloud expansion: Partnerships with AWS and Microsoft boost integration, sales reach, and co-selling opportunities—supporting revenue scale.

Industry recognition: Named a Leader in Forrester’s Q3 2025 Digital Process Automation Platforms report, reinforcing brand credibility and competitive edge.

Investment Outlook:

Bullish above: $49–$50

Upside target: $85–$90, driven by AI adoption, cloud partnerships, and industry validation.

#PEGA #AI #CloudComputing #DigitalTransformation #EnterpriseSoftware #TechGrowth #Investing

Baidu (BIDU) –AI Upgrades + Open-Source Strategy Powering GrowthCompany Snapshot:

Baidu NASDAQ:BIDU is cementing its position as a top AI platform leader in China, combining core search dominance with cutting-edge AI innovations and strategic open-source moves.

Key Catalysts:

Next-Gen AI Infrastructure ⚙️

Major Qianfan platform upgrades and PaddlePaddle 3.0 launch streamline model training & deployment for China’s AI developer ecosystem.

Reduces barriers to AI adoption, expanding the company’s developer base and ecosystem stickiness.

Open-Source Breakthrough 📂

ERNIE language models released under Apache 2.0 license—mirroring successful U.S. big-tech strategies.

Aims to accelerate adoption, attract global partnerships, and enhance monetization over the long term.

Rising User Engagement 📱

724M MAUs (+7% YoY) on Baidu’s mobile app.

AI-generated content now on 35% of search pages (up from 22% in January), increasing ad monetization potential.

Investment Outlook:

Bullish Entry Zone: Above $76.00–$78.00

Upside Target: $160.00–$165.00, fueled by AI leadership, developer adoption, and rising engagement metrics.

📈 Baidu’s combination of AI innovation, open-source strategy, and a massive user base creates a strong runway for both near-term revenue growth and long-term platform dominance.

#BIDU #AI #PaddlePaddle #ERNIE #OpenSource #ChinaTech #Search #CloudComputing #ArtificialIntelligence #BigData #DigitalTransformation #TechStocks

Is AMD Poised to Redefine the Future of AI and Computing?Advanced Micro Devices (AMD) is rapidly transforming its market position, recently converting a Wall Street skeptic, Melius Research, into a bullish advocate. Analyst Ben Reitzes upgraded AMD stock to "buy" from "hold," significantly raising the price target to \$175 from \$110, citing the company's substantial progress in artificial intelligence (AI) chips and computing systems. This optimistic outlook is fueled by a confluence of factors, including surging demand from hyperscale cloud providers and sovereign entities, alongside colossal revenue opportunities in AI inferencing workloads. Another upgrade from CFRA to "strong buy" further underscores this shifting perception, highlighting AMD's new product launches and an expanding customer base, including key players like Oracle and OpenAI, for its accelerator technology and the maturing ROCm software stack.

AMD's advancements in the AI accelerator market are particularly noteworthy. The company's MI300 series, including the MI300X with its industry-leading 192GB HBM3 memory, and the newly unveiled MI350 series, are designed to deliver significant price and performance advantages over rivals like Nvidia's H100. At its "Advancing AI 2025" event on June 12, AMD not only showcased the MI350's potential for up to 38x improvement in energy efficiency for AI training but also previewed "Helios" full-rack AI systems. These comprehensive, plug-and-play solutions, leveraging future MI400 series GPUs and Zen 6-based EPYC "Venice" CPUs, position AMD to directly compete for the lucrative business of hyperscale operators. As AI inference workloads are projected to consume 58% of AI budgets, AMD's focus on efficient, scalable AI platforms puts it in a prime position to capture a growing share of the rapidly expanding AI data center market.

Beyond AI, AMD is pushing the boundaries of traditional computing with its upcoming Zen 6 Ryzen CPUs, reportedly targeting "insane" clock speeds, well above 6 GHz, with some leaks suggesting peaks of 6.4-6.5 GHz. Built on TSMC's advanced 2nm lithography node, the Zen 6 architecture, developed by the same team behind the successful Zen 4, promises significant architectural improvements and a substantial increase in performance per clock. While these are leaked targets, the combination of AMD's proven design capabilities and TSMC's cutting-edge process technology makes these ambitious clock speeds appear highly achievable. This aggressive strategy aims to deliver compelling performance gains for PC enthusiasts and enterprise users, further solidifying AMD's competitive stance against Intel's forthcoming Nova Lake CPUs, which are also expected around 2026 and feature a modular design and up to 52 cores.

SNOWFLAKE to $369Snowflake Inc. is an American cloud-based data storage company.

Headquartered in Bozeman, Montana, it operates a platform that allows for data analysis and simultaneous access of data sets with minimal latency. It operates on Amazon Web Services, Microsoft Azure, and Google Cloud Platform.

As of November 2024, the company had 10,618 customers, including more than 800 members of the Forbes Global 2000, and processed 4.2 billion daily queries across its platform

#DoubleBottom

#Wformation

Who Silently Powers the AI Revolution?While the spotlight often shines on AI giants like Nvidia and OpenAI, a less-publicized but equally critical player, CoreWeave, is rapidly emerging as a foundational force in the artificial intelligence landscape. This specialized AI cloud computing provider is not just participating in the AI boom; it is building the essential infrastructure that underpins it. CoreWeave's unique model allows companies to "rent" high-performance Graphics Processing Units (GPUs) from its dedicated cloud, democratizing access to the immense computational power required for advanced AI development. This strategic approach has positioned CoreWeave for substantial growth, evidenced by its impressive 420% year-over-year revenue growth in Q1 2025 and a burgeoning backlog of over $25 billion in remaining performance obligations.

CoreWeave's pivotal role became even clearer with the recent partnership between Google Cloud and OpenAI. Though seemingly a win for the tech titans, CoreWeave is supplying the critical compute power that Google then resells to OpenAI. This crucial, indirect involvement places CoreWeave at the nexus of the AI revolution's most significant collaborations, validating its business model and its capacity to meet the demanding computational needs of leading AI innovators. Beyond merely providing raw compute, CoreWeave is also innovating in the software space. Following its acquisition of AI developer platform Weights & Biases in May 2025, CoreWeave has launched new AI cloud software products designed to streamline AI development, deployment, and iteration, further cementing its position as a comprehensive AI ecosystem provider.

Despite its rapid stock appreciation and some analyst concerns about valuation, CoreWeave's core fundamentals remain robust. Its deep partnership with Nvidia, including Nvidia's equity stake and CoreWeave's early adoption of Nvidia's cutting-edge Blackwell architecture, ensures access to the most sought-after GPUs. While currently in a heavy investment phase, these expenditures directly fuel its capacity expansion to meet an insatiable demand. As AI continues its relentless advancement, the need for specialized, high-performance computing infrastructure will only intensify. CoreWeave, by strategically positioning itself as the "AI Hyperscaler," is not just witnessing this revolution; it is actively enabling it.

What Fuels Cisco's Quiet AI Domination?Cisco Systems, a long-standing titan in networking infrastructure, is experiencing a significant resurgence, largely driven by a pragmatic and highly effective approach to artificial intelligence. Unlike many enterprises chasing broad AI initiatives, Cisco focuses on solving "boring" yet critical customer experience problems. This strategy yields tangible benefits, including substantial reductions in support cases and significant time savings for customer success teams, ultimately freeing resources to address more complex challenges and enhance sales processes. This practical application of AI, coupled with a focus on resiliency, simplicity through unified interfaces, and personalized customer journeys, underpins Cisco's strengthening market position.

The company's strategic evolution also involves a nuanced embrace of Agentic AI, viewing it not as a replacement for human intellect but as a powerful augmentation. This shift from AI as a mere "tool" to a "teammate" enables proactive problem detection and resolution, often before customers even recognize an issue. Beyond internal efficiencies, Cisco's growth is further fueled by shrewd strategic investments and acquisitions, such as the integration of Isovalent's eBPF technology. This acquisition has rapidly enhanced Cisco's offerings in cloud-native networking, security, and load balancing, demonstrating its agility and commitment to staying at the forefront of technological innovation.

Cisco's robust financial performance and strategic partnerships, particularly with AI leaders like Nvidia and Microsoft, underscore its market momentum. The company reports impressive growth in product revenues, especially in its Security and Observability segments, signaling a successful transition toward a more predictable, software-driven revenue model. This strong performance, combined with a clear vision for AI-driven customer experience and strategic collaborations, positions Cisco as a formidable force in the evolving technology landscape. The company's disciplined approach offers valuable lessons for any organization seeking to harness the transformative power of AI effectively.

What Fuels Microsoft's Unstoppable Rise?Microsoft Corporation consistently demonstrates its market leadership, evidenced by its substantial valuation and strategic maneuvers in the artificial intelligence sector. The company's proactive approach to AI, particularly through its Azure cloud platform, positions it as a central hub for innovation. Azure now hosts a diverse array of leading AI models, including xAI’s Grok, alongside offerings from OpenAI and other industry players. This inclusive strategy, driven by CEO Satya Nadella's vision, aims to establish Azure as the definitive platform for emerging AI technologies, offering robust Service Level Agreements and direct billing for hosted models.

Microsoft's AI integration extends deeply into its product ecosystem, significantly enhancing enterprise productivity and developer capabilities. GitHub's new AI coding agent streamlines software development by automating routine tasks, allowing programmers to focus on complex challenges. Furthermore, Microsoft Dataverse is evolving into a powerful, secure platform for AI agents, leveraging features like prompt columns and the Model Context Protocol (MCP) server to transform structured data into dynamic, queryable knowledge. The seamless integration of Dynamics 365 data within Microsoft 365 Copilot further unifies business intelligence, enabling users to access comprehensive insights without switching contexts.

Beyond its core software offerings, Microsoft's Azure cloud provides critical infrastructure for transformative projects in highly regulated sectors. The UK's Met Office, for instance, successfully transitioned its supercomputing operations to Azure, improving weather forecasting accuracy and advancing climate research. Similarly, Finnish startup Gosta Labs utilizes Azure's secure and compliant environment to develop AI solutions that automate patient record-keeping, significantly reducing administrative burdens in healthcare. These strategic partnerships and technological advancements underscore Microsoft's foundational role in driving innovation across diverse industries, cementing its position as a dominant force in the global technology landscape.

Can Efficiency Topple AI's Titans?Google has strategically entered the next phase of the AI hardware competition with Ironwood, its seventh-generation Tensor Processing Unit (TPU). Moving beyond general-purpose AI acceleration, Google specifically engineered Ironwood for inference – the critical task of running trained AI models at scale. This deliberate focus signals a Major bet on the "age of inference," where the cost and efficiency of deploying AI, rather than just training it, become dominant factors for enterprise adoption and profitability, positioning Google directly against incumbents NVIDIA and Intel.

Ironwood delivers substantial advancements in both raw computing power and, critically, energy efficiency. Its most potent competitive feature may be its enhanced performance-per-watt, boasting impressive teraflops and significantly increased memory bandwidth compared to its predecessor. Google claims nearly double the efficiency of its previous generation, addressing the crucial operational challenges of power consumption and cost in large-scale AI deployments. This efficiency drive, coupled with Google's decade-long vertical integration in designing its TPUs, creates a tightly optimized hardware-software stack potentially offering significant advantages in total cost of ownership.

By concentrating on inference efficiency and leveraging its integrated ecosystem, encompassing networking, storage, and software like the Pathways runtime, Google aims to carve out a significant share of the AI accelerator market. Ironwood is presented not merely as a chip, but as the engine for Google's advanced models like Gemini and the foundation for a future of complex, multi-agent AI systems. This comprehensive strategy directly challenges the established dominance of NVIDIA and the growing AI aspirations of Intel, suggesting the battle for AI infrastructure leadership is intensifying around the economics of deployment.

AMAZON ($AMZN) Q4—$187.8B REVENUE UPSWINGAMAZON ( NASDAQ:AMZN ) Q4—$187.8B REVENUE UPSWING

(1/9)

Good afternoon, TradginView! Amazon ( NASDAQ:AMZN ) posted Q4 ‘24 net sales of

187.8 B,up 10 637.959 B here’s the breakdown.

(2/9) – REVENUE GROWTH

• Q4 Sales: $ 187.8B, 10% up from $ 170B 📈

• Full ‘24: $ 637.959B, 10.99% rise 📊

• AWS: $ 28.8B, 19% YoY boost 💻

NASDAQ:AMZN ’s steady climb continues.

(3/9) – EARNINGS LIFT

• Q4 Op. Income: $ 21.2B, up from $ 13.2B 💰

• NA Op. Income: $ 9.3B, from $ 6.5B 🌞

• AWS Margin: 38%, decade high 🌟

NASDAQ:AMZN ’s profit engine hums strong.

(4/9) – KEY MOVES

• AI Push: GenAI apps rolled out 📡

• AWS: Cash flow dynamo shines 🌍

• Stock: 207−230 range 🚗

NASDAQ:AMZN ’s tech bets fuel growth.

(5/9) – RISKS IN FOCUS

• Spending: Retail feels price pinch ⚠️

• Regs: Antitrust looms large 🔒

• Comp: Azure, Walmart press hard 📉

NASDAQ:AMZN ’s solid, but hurdles lurk.

(6/9) – SWOT: STRENGTHS

• Retail: $ 115.6B Q4 NA sales 💪

• AWS: $ 28.8B, 38% margin 🏋️

• Scale: Ads, subs diversify 🌱

NASDAQ:AMZN ’s a titan, built to last.

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES

• Weaknesses: Capex weighs 📚

• Opportunities: AI, emerging markets 🌏

Can NASDAQ:AMZN vault past the risks?

(8/9) – AMZN’s $ 187.8B Q4, your view?

1️⃣ Bullish, $ 300+ by ‘26 😎

2️⃣ Neutral, Steady, risks balance 🤷

3️⃣ Bearish, Growth stalls 😕

Vote below! 🗳️👇

(9/9) – FINAL TAKEAWAY

NASDAQ:AMZN ’s $ 187.8B Q4 and $ 637.959B ‘24 stack up, tech titan 🪙 AWS shines, risks loom, gem or pause?