VIDYA Auto-Trading(Reversal Logic)Overview

This script is a dynamic trend-following strategy based on the Variable Index Dynamic Average (VIDYA). It adapts in real time to market volatility, aiming to enhance entry precision and optimize risk management.

⚠️ This strategy is intended for educational and research purposes. Past performance does not guarantee future results. All results are based on historical simulations using fixed parameters.

Strategy Objectives

The objective of this strategy is to respond swiftly to sudden price movements and trend reversals, providing consistent and reliable trade signals under historical testing conditions. It is designed to be intuitive and efficient for traders of all levels.

Key Features

Momentum Sensitivity via VIDYA: Reacts quickly to momentum shifts, allowing for accurate trend-following entries.

Volatility-Based ATR Bands: Automatically adjusts stop levels and entry conditions based on current market volatility.

Intuitive Trend Visualization: Uptrends are marked with green zones, and downtrends with red zones, giving traders clear visual guidance.

Trading Rules

Long Entry: Triggered when price crosses above the upper band. Any existing short position is closed.

Short Entry: Triggered when price crosses below the lower band. Any existing long position is closed.

Exit Conditions: Positions are reversed based on signal changes, using a position reversal strategy.

Risk Management Parameters

Market: ETHUSD(5M)

Account Size: $3,000 (reasonable approximation for individual traders)

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted to comply with TradingView guidelines for realistic risk levels)

Number of Trades: 251 (based on backtest over the selected dataset)

⚠️ The risk per trade and other values can be customized. Users are encouraged to adapt these to their individual needs and broker conditions.

Trading Parameters & Considerations

VIDYA Length: 10

VIDYA Momentum: 20

Distance factor for upper/lower bands: 2

Source: close

Visual Support

Trend zones, entry points, and directional shifts are clearly plotted on the chart. These visual cues enhance the analytical experience and support faster decision-making.

Visual elements are designed to improve interpretability and are not intended as financial advice or trade signals.

Strategy Improvements & Uniqueness

Inspired by the public work of BigBeluga, this script evolves the original concept with meaningful enhancements. By combining VIDYA and ATR bands, it offers greater adaptability and practical value compared to conventional trend-following strategies.

This adaptation is original work and not a direct copy. Improvements are designed to enhance usability, risk control, and market responsiveness.

Summary

This strategy offers a responsive and adaptive approach to trend trading, built on momentum detection and volatility-adjusted risk management. It balances clarity, precision, and practicality—making it a powerful tool for traders seeking reliable trend signals.

⚠️ All results are based on historical data and are subject to change under different market conditions. This script does not guarantee profit and should be used with caution and proper risk management.

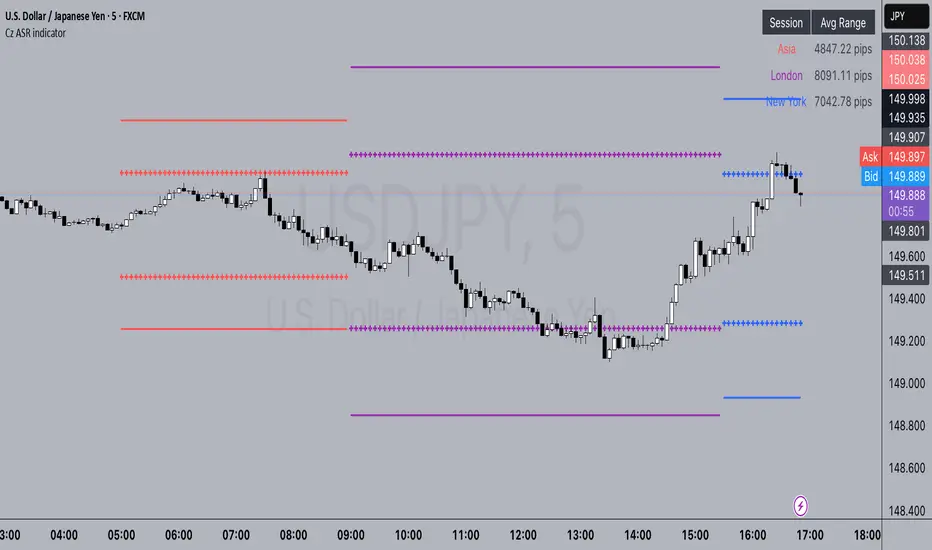

Average True Range (ATR)

Cz ASR indicatorAverage session range indicator built by me. Great tool to gauge volatility and intraday reversal zones. Great for FX as there is an included table that shows range in pips; however, this can be applied across all assets as a volatility measure.

How it works:

The script measures the range of sessions, including Asia, London, and New York. The lookback period could be adjusted so you can find what length works best and is most accurate. This is then averaged out to provide the ASR. This provides us with an upper and lower bound of which the price could potentially fluctuate in based on the past session ranges. I have also added the 50% ASR, which is also a super useful metric for reversals or continuations.

There is also a configurable UTC so that you can adjust the indicator so it can accurately measure the range within certain sessions.

Note - different session start and stop times vary from market to market. I have set the code to the standard forex market opens however, if you wish to change the time ,you are able to do so by editing the variables in the script

Enjoy :)

ATR - Asymmetric Turbulence Ribbon🧭 Asymmetric Turbulence Ribbon (ATR)

The Asymmetric Turbulence Ribbon (ATR) is an enhanced and reimagined version of the standard Average True Range (ATR) indicator. It visualizes not just raw volatility, but the structure, momentum, and efficiency of volatility through a multi-layered visual approach.

It contains two distinct visual systems:

1. A zero-centered histogram that expresses how current volatility compares to its historical average, with intensity and color showing speed and conviction

2. A braided ribbon made of dual ATR-based moving averages that highlight transitions in volatility behavior—whether volatility is expanding or contracting

The name reflects its purpose: to capture asymmetric, evolving turbulence in market behavior, through structure-aware volatility tracking.

_______________________________________________________________

🔧 Inputs (Fibonacci defaults)

ATR Length

Lookback period for ATR calculation (default: 13)

ATR Base Avg. Length

Moving average period used as the zero baseline for histogram (default: 55)

ATR ROC Lookback

Number of bars to measure rate of change for histogram color mapping (default: 8)

Timeframe Override

Optionally calculate ATR values from a higher or fixed timeframe (e.g., 1D) for macro-volatility overlay

Show Ribbon Fill

Toggles colored fill between ATR EMA and HMA lines

Show ATR MAs

Toggles visibility of ATR EMA and HMA lines

Show Crossover Markers

Shows directional triangle markers where ATR EMA and HMA cross

Show Histogram

Toggles the entire histogram display

_______________________________________________________________

📊 Histogram Component: Volatility Energy Profile

The histogram shows how far the current ATR is from its moving average baseline, centered around zero. This lets you interpret volatility pressure—whether it's expanding, contracting, or preparing to reverse.

To complement this, the indicator also plots the raw ATR line in aqua. This is the actual average true range value—used internally in both the histogram and ribbon calculations. By default, it appears as a slightly thicker line, providing a clear reference point for comparing historical volatility trends and absolute levels.

Use the baseline ATR to:

- Compare real-time volatility to previous peaks or troughs

- Monitor how ATR behaves near histogram flips or ribbon crossovers

- Evaluate volatility phases in absolute terms alongside relative momentum

The ATR line is particularly helpful for users who want to keep tabs on raw volatility values while still benefiting from the enhanced visual storytelling of the histogram and ribbon systems.

Each histogram bar is colored based on the rate of change (ROC) in ATR: The faster ATR rises or falls, the more intense the color. Meanwhile, the opacity of each bar is adjusted by the effort/result ratio of the price candle (body vs. range), showing how much price movement was achieved with conviction.

Color Interpretation:

🔴 Red

Strong volatility expansion

Market entering or deepening into a volatility burst

Seen during breakouts, panic moves, or macro shock events

Often accompanied by large real candle bodies

🟠 Orange

Moderate volatility expansion

Heating up phase, often precedes breakouts

Common in strong trending environments

Signals tightening before acceleration

🟡 Yellow

Mild volatility increase

Transitional state—energy building, not yet exploding

Appears in early trend development or pullbacks

🟢 Green

Mild volatility contraction

ATR cooling off

Seen during consolidation, reversion, or range balance

Good time to assess upcoming directional setups

🔵 Aqua

Moderate compression

Volatility is clearly declining

Signals consolidation within larger structure

Pre-breakout zones often form here

🔵 Deep Blue

Strong volatility compression

Market is coiling or dormant

Can signal upcoming squeeze or fade environment

Often followed by sharp expansion

Opacity scaling:

Brighter bars = efficient, directional price action (strong bodies)

Faded bars = indecision, chop, absorption, or wick-heavy structure

Together, color and opacity give a 2D view of market volatility: Hue = the type and direction of volatility

Opacity = the quality and structure behind it

Use this to gauge whether volatility is rising with conviction, fading into neutrality, or compressing toward breakout potential.

_______________________________________________________________

🪡 Ribbon Component: Volatility Rhythm Structure

The ribbon overlays two moving averages of ATR:

EMA (yellow) – faster, more reactive

HMA (orange) – smoother, more rhythmic

Their relationship creates the ribbon logic:

Yellow fill (EMA > HMA)

Short-term volatility is increasing faster than the longer-term rhythm

Signals active expansion and engagement

Orange fill (HMA > EMA)

Volatility is decaying or leveling off

Suggests possible exhaustion, pullback, or range

Crossover triangle markers (optional, off by default to avoid clutter) identify the moment of shift in volatility phase.

The ribbon reflects the shape of volatility over time—ideal for mapping cyclical energy shifts, transitional states, and alignment between current and average volatility.

_______________________________________________________________

📐 Strategy Application

Use the Asymmetric Turbulence Ribbon to:

- Detect volatility expansions before breakouts or directional runs

- Spot compression zones that precede structural ruptures

- Visually separate efficient moves from noisy market activity

- Confirm or fade trade setups based on underlying energy state

- Track the volatility environment across multiple timeframes using the override

_______________________________________________________________

🎯 Ideal Timeframes

Designed to function across all timeframes, but particularly powerful on intraday to daily ranges (1H to 1D)

Use the timeframe override to anchor your chart in higher-timeframe volatility context, like daily ATR behavior influencing a 1H setup.

_______________________________________________________________

🧬 Customization Tips

- Increase ATR ROC Lookback for smoother color transitions

- Extend ATR Base Avg Length for more macro-driven histogram centering

- Disable the histogram for ribbon-only rhythm view

- Use opacity and color shifts in the histogram to detect stealth energy builds

- Align ATR phases with structure or order flow tools for high-quality setups

Average True Range with MultiplierRelease Summary – ATR with Risk Management Tool (v6)

This script introduces an enhanced Average True Range (ATR) indicator with a user-defined multiplier and integrated risk management table. Users can choose from multiple smoothing methods (SMA, EMA, RMA, WMA) and dynamically calculate risk parameters including:

ATR and ATR × Multiplier

Dollar risk based on account size (1% default)

Position sizing (lot size)

Stop Loss and Take Profit levels (3× reward)

A built-in customizable table displays all calculated values for quick reference. The indicator is fully configurable and designed for precision risk management directly on the chart.

Breaking Structures (javieresfeliz)This TradingView script is designed to identify market structure changes, using a break of highs and lows approach, as well as technical indicators such as ATR, RSI, and EMAs (Exponential Moving Averages). It is aimed at detecting bullish and bearish trends, signaling possible entry and exit points based on various factors. It also offers additional confirmations to avoid false signals and provides a clear visualization of buy and sell signals.

Main Features:

Indicators Used:

ATR (Average True Range): Used to calculate a volatility range, which helps set stop-loss levels and price targets based on the current market volatility.

EMAs (50 and 200): Exponential Moving Averages (EMAs) are used to determine the short-term and long-term trends. The 50-period EMA is used to identify the short-term trend, while the 200-period EMA is used to identify the long-term trend.

RSI (Relative Strength Index): Used to identify overbought or oversold conditions in the market, providing additional buy or sell signals.

Volume: Used to confirm the validity of a signal. An increase in volume can confirm a structure break and provide more reliability to the signal.

Break of Structure Detection (BOS):

Bullish Break: Generated when the price surpasses previous highs.

Bearish Break: Generated when the price falls below previous lows.

Change of Character (CHOCH):

Bullish Trend: Defined by a close above the open and above the 50 EMA.

Bearish Trend: Defined by a close below the open and below the 50 EMA.

Buy and Sell Conditions:

Buy (Long): Activated when several conditions are met, including a bullish change of character, a bullish structure break, the price closing above the previous value plus a multiple of the ATR, and additional confirmations from RSI and volume.

Sell (Short): Activated when several conditions are met, including a bearish change of character, a bearish structure break, the price closing below the previous value minus a multiple of the ATR, with additional confirmations from RSI and volume.

Entry and Exit Signals:

Long Entry (Buy): Executed when the buy conditions are met.

Short Entry (Sell): Executed when the sell conditions are met.

Position Close: Positions are closed when the price crosses below (for long positions) or above (for short positions) the 50 EMA.

Historical Highs and Lows Lines:

The script draws lines of historical highs and lows from the last 288 and 60 periods to show key support and resistance levels on the chart.

Signal Table Across Multiple Timeframes:

The script displays a table in the top-right corner of the chart with indicators like the EMA trend, RSI value, and MACD histogram for timeframes of 1 minute, 5 minutes, 30 minutes, 1 hour, 4 hours, daily, and weekly.

Precautions:

Does not guarantee profits: Although the script is designed to detect structure breaks and possible trend changes, it does not guarantee 100% profitable signals. The market is always subject to risk and unpredictable volatility.

Requires adjustments for each asset: Parameters such as ATR length and EMA lengths should be adjusted according to the asset being analyzed and market conditions.

Use of additional confirmations: To reduce false signals, the script uses additional confirmations like RSI and volume, but it is always recommended to perform additional analysis before making trading decisions.

Changing trends: The change of character (CHOCH) can be a useful indicator, but it can give false signals in highly volatile markets or during prolonged consolidations.

Relies on historical data: This script relies on historical data to identify highs and lows. It does not consider fundamental events that may significantly impact the market.

Requires constant monitoring: Although the signals are automated, it is important to monitor open positions and make adjustments if market conditions change.

Risk of false signals: In low liquidity markets or consolidations, structure breaks can be false, so it’s recommended to pay attention to any additional confirmation signals or use a proper risk management strategy.

Litecoin Trailing-Stop StrategyAltcoins Trailing-Stop Strategy

This strategy is based on a momentum breakout approach using PKAMA (Powered Kaufman Adaptive Moving Average) as a trend filter, and a delayed trailing stop mechanism to manage risk effectively.

It has been designed and fine-tuned Altcoins, which historically shows consistent volatility patterns and clean trend structures, especially on intraday timeframes like 15m and 30m.

Strategy Logic:

Entry Conditions:

Long when PKAMA indicates an upward move

Short when PKAMA detects a downward trend

Minimum spacing of 30 bars between trades to avoid overtrading

Trailing Stop:

Activated only after a customizable delay (delayBars)

User can set trailing stop % and delay independently

Helps avoid premature exits due to short-term volatility

Customizable Parameters:

This strategy uses a custom implementation of PKAMA (Powered Kaufman Adaptive Moving Average), inspired by the work of alexgrover

PKAMA is a volatility-aware moving average that adjusts dynamically to market conditions, making it ideal for altcoins where trend strength and direction change frequently.

This script is for educational and experimental purposes only. It is not financial advice. Please test thoroughly before using it in live conditions, and always adapt parameters to your specific asset and time frame.

Feedback is welcome! Feel free to clone and adapt it for your own trading style.

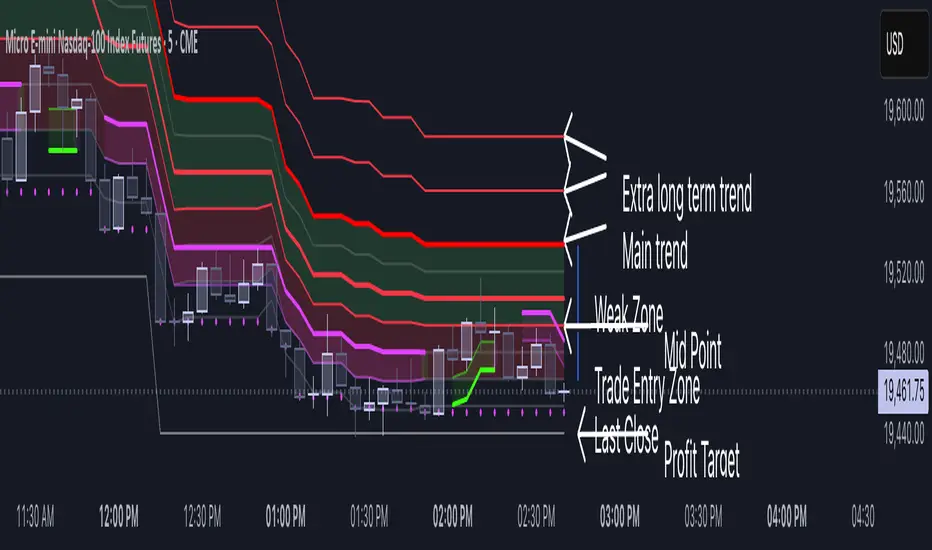

Volatility Layered Supertrend [NLR]We’ve all used Supertrend, but do you know where to actually enter a trade? Volatility Layered Supertrend (VLS) is here to solve that! This advanced trend-following indicator builds on the classic Supertrend by not only identifying trends and their strength but also guiding you to the best trade entry points. VLS divides the main long-term trend into “Strong” and “Weak” Zones, with a clear “Trade Entry Zone” to help you time your trades with precision. With layered trends, dynamic profit targets, and volatility-adaptive bands, VLS delivers actionable signals for any market.

Why I Created VLS Over a Plain Supertrend

I built VLS to address the gaps in traditional Supertrend usage and make trade entries clearer:

Single-Line Supertrend Issues: The default Supertrend sets stop-loss levels that are too wide, making it impractical for most traders to use effectively.

Unclear Entry Points: Standard Supertrend doesn’t tell you where to enter a trade, often leaving you guessing or entering too early or late.

Multi-Line Supertrend Enhancement: Many traders use short, medium, and long Supertrends, which is helpful but can lack focus. In VLS, I include Short, Medium, and Long trends (using multipliers 1 to 3), and add multipliers 4 and 5 to track extra long-term trends—helping to avoid fakeouts that sometimes occur with multiplier 3.

My Solution: I focused on the main long-term Supertrend and split it into “Weak Zone” and “Strength Zone” to show the trend’s reliability. I also defined a “Trade Entry Zone” (starting from the Mid Point, with the first layer’s background hidden for clarity) to guide you on where to enter trades. The zones include Short, Medium, and Long Trend layers for precise entries, exits, and stop-losses.

Practical Trading: This approach provides realistic stop-loss levels, clear entry points, and a “Profit Target” line that aligns with your risk tolerance, while filtering out false signals with longer-term trends.

Key Features

Layered Trend Zones: Short, Medium, Long, and Extra Long Trend layers (up to multipliers 4 and 5) for timing entries and exits.

Strong & Weak Zones: See when the trend is reliable (Strength Zone) or needs caution (Weak Zone).

Trade Entry Zone: A dedicated zone starting from the Mid Point (first layer’s background hidden) to show the best entry points.

Dynamic Profit Targets: A “Profit Target” line that adjusts with the trend for clear goals.

Volatility-Adaptive: Uses ATR to adapt to market conditions, ensuring reliable signals.

Color-Coded: Green for uptrends, red for downtrends—simple and clear.

How It Works

VLS enhances the main long-term Supertrend by dividing it into two zones:

Weak Zone: Indicates a less reliable trend—use tighter stop-losses or wait for the price to reach the Trade Entry Zone.

Strength Zone: Signals a strong trend—ideal for entries with wider stop-losses for bigger moves.

The “Trade Entry Zone” starts at the Mid Point (last layer’s background hidden for clarity), showing you the best area to enter trades. Each zone includes Short, Medium, Long, and Extra Long Trend sublevels (up to multipliers 4 and 5) for precise trade timing and to filter out fakeouts. The “Profit Target” updates dynamically based on trend direction and volatility, giving you a clear goal.

How to Use

Spot the Trend: Green bands = buy, red bands = sell.

Check Strength: Price in Strength Zone? Trend’s reliable—trade confidently. In Weak Zone? Use tighter stops or wait.

Enter Trades: Use the “Trade Entry Zone” (from the Mid Point upward) for the best entry points.

Use Sublevels: Short, Medium, Long, and Extra Long layers in each zone help fine-tune entries and exits.

Set Targets: Follow the Profit Target line for goals—it updates automatically.

Combine Tools: Pair with RSI, MACD, or support/resistance for added confirmation.

Settings

ATR Length: Adjust the ATR period (default 10) to change sensitivity.

Up/Down Colors: Customize colors—green for up, red for down, by default.

ATRs in Days📌 ATR in Days

This script tracks how price moves in relation to ATR over multiple days, providing a powerful volatility framework for traders.

🔹 Key Features:

✅ 4 ATRs in 5 Days – Measures if a stock has moved 4x its ATR within the last 5 days, identifying extreme volatility zones.

✅ Daily ATR Calculation – Tracks average true range over time to gauge market conditions.

✅ Clear Table Display – Real-time ATR readings for quick decision-making.

✅ Intraday & Swing Trading Compatible – Works across multiple timeframes for day traders & swing traders.

📊 How to Use:

Look for stocks that exceed 4 ATRs in 5 days to spot extended moves.

Use ATR as a reversion or continuation signal depending on market structure.

🚀 Perfect for traders looking to quantify volatility & structure trades effectively!

OG ATR RangeDescription:

The OG ATR Tool is a clean, visualized version of the Average True Range indicator for identifying volatility, stop-loss levels, and realistic price movement expectations.

How it works:

Calculates the average range (in points/pips) of recent candles.

Overlays ATR bands to help define breakout potential or squeeze zones.

Can be used to size trades or set dynamic stop-loss and target levels.

Best for:

Intraday traders who want to avoid unrealistic targets.

Volatility-based setups and breakout strategies.

Creating position sizing rules based on instrument volatility.

Pro Tip: Combine with your trend indicators to set sniper entries and exits that respect volatility.

Long Term Profitable Swing | AbbasA Story of a Profitable Swing Trading Strategy

Imagine you're sailing across the ocean, looking for the perfect wave to ride. Swing trading is quite similar—you're navigating the stock market, searching for the ideal moments to enter and exit trades. This strategy, created by Abbas, helps you find those waves and ride them effectively to profitable outcomes.

🌊 Finding the Perfect Wave (Entry)

Our journey begins with two simple signs that tell us a great trading opportunity is forming:

- Moving Averages: We use two lines that follow price trends—the faster one (EMA 16) reacts quickly to recent price moves, and the slower one (EMA 30) gives us a longer-term perspective. When the faster line crosses above the slower line, it's like a clear signal saying, "Hey! The wave is rising, and prices might move higher!"

- RSI Momentum: Next, we check a tool called the RSI, which measures momentum (how strongly prices are moving). If the RSI number is above 50, it means there's enough strength behind this rising wave to carry us forward.

When both signals appear together, that's our green light. It's time to jump on our surfboard and start riding this promising wave.

⚓ Safely Riding the Wave (Risk Management)

While we're riding this wave, we want to ensure we're safe from sudden surprises. To do this, we use something called the Average True Range (ATR), which measures how volatile (or bumpy) the price movements are:

- Stop-Loss: To avoid falling too hard, we set a safety line (stop-loss) 8 times the ATR below our entry price. This helps ensure we exit if the wave suddenly turns against us, protecting us from heavy losses.

- Take Profit: We also set a goal to exit the trade at 11 times the ATR above our entry. This way, we capture significant profits when the wave reaches a nice high point.

🌟 Multiple Rides, Bigger Adventures

This strategy allows us to take multiple positions simultaneously—like riding several waves at once, up to 5. Each trade we make uses only 10% of our trading capital, keeping risks manageable and giving us multiple opportunities to win big.

🗺️ Easy to Follow Settings

Here are the basic settings we use:

- Fast EMA**: 16

- Slow EMA**: 30

- RSI Length**: 9

- RSI Threshold**: 50

- ATR Length**: 21

- ATR Stop-Loss Multiplier**: 8

- ATR Take-Profit Multiplier**: 11

These settings are flexible—you can adjust them to better suit different markets or your personal trading style.

🎉 Riding the Waves of Success

This simple yet powerful swing trading approach helps you confidently enter trades, clearly know when to exit, and effectively manage your risk. It’s a reliable way to ride market waves, capture profits, and minimize losses.

Happy trading, and may you find many profitable waves to ride! 🌊✨

Please test, and take into account that it depends on taking multiple longs within the swing, and you only get to invest 25/30% of your equity.

ATR & PTR TableThe ATR & PTR Table Indicator displays a dynamic table that provides Average True Range (measures market volatility over 1D, 1W, and 1M timeframes), Price trading range (difference between the high and low prices over the same periods) & percentage of the typical range that has been traded. This indicator will help traders identify potential breakout zones and assess volatility across multiple timeframes.

This had been optimized to show ATR and PTR on every time frame. The (1D) represents ATR on whatever timeframe you are currently on.

Price Extreme BandsPrice Extreme Bands Description

This indicator calculates and displays Price Extreme Bands based on an Exponential Moving Average (EMA) and True Range Average True Range (TR ATR). It utilizes a custom "Super Smoother" function to smooth the bands, providing a clearer representation of potential price extremes without sacrificing accuracy.

Usage

Built for specifically for intraday timeframes, this indicator identifies short term price extremes and volatility ranges. Traders can observe when price moves towards the outer bands, suggesting strong momentum or potential overbought/oversold conditions. The filled zones highlight areas of increased volatility which can used as exit criteria for a trade, possible reversal points in ranging markets or price ranges where price momentum could slow in trending markets.

Key Features

Length Input: Controls the length of the EMA and TR ATR calculations.

Multiplier Inputs: Uses two fixed multipliers (1.71 and 2.50) to create bands.

Super Smoother: Applies a custom smoothing function to the bands for reduced noise.

Fill Zones: Fills the areas between the inner and outer bands to highlight potential volatility ranges.

Calculation:

1. EMA (Basis): Calculates the Exponential Moving Average of the selected source.

2. TR ATR: Calculates the True Range and then smoothes it using RMA (Rolling Moving Average).

3. Bands: Calculates upper and lower bands using the EMA and ATR, with multipliers of 1.71 and 2.50.

4. Super Smoother: Applies a smoothing function to the calculated bands.

Visuals:

Basis Line: Plots the EMA (basis) (invisible by default).

Inner Bands (1.71 Multiplier): Plots the smoothed bands with a distinct color (e.g., orange) (invisible by default).

Outer Bands (2.50 Multiplier): Plots the smoothed bands with a different color (e.g., purple) (invisible by default).

Fill Zones: Fills the region between the inner and outer upper bands and the inner and outer lower bands with a translucent color (e.g. light blue).

// Note: The plot lines are invisible by default. To view the basis, upper and lower band lines, adjust the visibility settings in the indicator's settings.

Uniqueness: Ready of the box. Code and parameters built specifically for 1m to 15m timeframes provides users with an indicator to easily identify price extremes. The use of TR ATR and addition of the Super Smoother calculation create a easier visualization and implementation compared to existing price band options.

Arbitrage Spot-Futures Don++Strategy: Spot-Futures Arbitrage Don++

This strategy has been designed to detect and exploit arbitrage opportunities between the Spot and Futures markets of the same trading pair (e.g. BTC/USDT). The aim is to take advantage of price differences (spreads) between the two markets, while minimizing risk through dynamic position management.

[Operating principle

The strategy is based on calculating the spread between Spot and Futures prices. When this spread exceeds a certain threshold (positive or negative), reverse positions are opened simultaneously on both markets:

- i] Long Spot + Short Futures when the spread is positive.

- i] Short Spot + Long Futures when the spread is negative.

Positions are closed when the spread returns to a value close to zero or after a user-defined maximum duration.

[Strategy strengths

1. Adaptive thresholds :

- Entry/exit thresholds can be dynamic (based on moving averages and standard deviations) or fixed, offering greater flexibility to adapt to market conditions.

2. Robust data management :

- The script checks the validity of data before executing calculations, thus avoiding errors linked to missing or invalid data.

3. Risk limitation :

- A position size based on a percentage of available capital (default 10%) limits exposure.

- A time filter limits the maximum duration of positions to avoid losses due to persistent spreads.

4. Clear visualization :

- Charts include horizontal lines for entry/exit thresholds, as well as visual indicators for spread and Spot/Futures prices.

5. Alerts and logs :

- Alerts are triggered on entries and exits to inform the user in real time.

[Points for improvement or completion

Although this strategy is functional and robust, it still has a few limitations that could be addressed in future versions:

1. [Limited historical data :

- TradingView does not retrieve real-time data for multiple symbols simultaneously. This can limit the accuracy of calculations, especially under conditions of high volatility.

2. [Lack of liquidity management :

- The script does not take into account the volumes available on the order books. In conditions of low liquidity, it may be difficult to execute orders at the desired prices.

3. [Non-dynamic transaction costs :

- Transaction costs (exchange fees, slippage) are set manually. A dynamic integration of these costs via an external API would be more realistic.

4. User-dependency for symbols :

- Users must manually specify Spot and Futures symbols. Automatic symbol validation would be useful to avoid configuration errors.

5. Lack of advanced backtesting :

- Backtesting is based solely on historical data available on TradingView. An implementation with third-party data (via an API) would enable the strategy to be tested under more realistic conditions.

6. [Parameter optimization :

- Certain parameters (such as analysis period or spread thresholds) could be optimized for each specific trading pair.

[How can I contribute?

If you'd like to help improve this strategy, here are a few ideas:

1. Add additional filters:

- For example, a filter based on volume or volatility to avoid false signals.

2. Integrate dynamic costs:

- Use an external API to retrieve actual costs and adjust thresholds accordingly.

3. Improve position management:

- Implement hedging or scalping mechanisms to maximize profits.

4. Test on other pairs:

- Evaluate the strategy's performance on other assets (ETH, SOL, etc.) and adjust parameters accordingly.

5. Publish backtesting results :

- Share detailed analyses of the strategy's performance under different market conditions.

[Conclusion

This Spot-Futures arbitrage strategy is a powerful tool for exploiting price differentials between markets. Although it is already functional, it can still be improved to meet more complex trading scenarios. Feel free to test, modify and share your ideas to make this strategy even more effective!

[Thank you for contributing to this open-source community!

If you have any questions or suggestions, please feel free to comment or contact me directly.

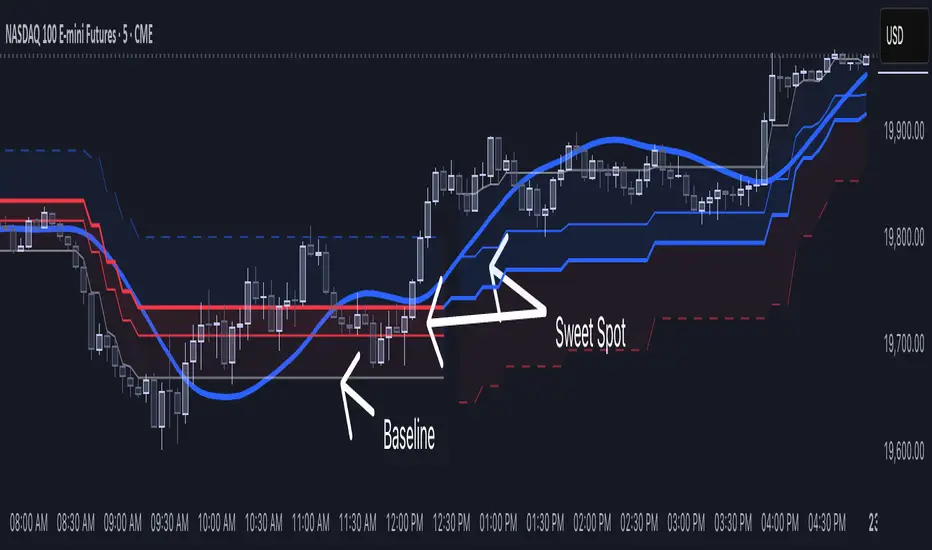

[NLR] - SweetSpot ZonesThe Sweet Spot Zone helps you find the best spots to enter a trade, inspired by the " Follow Line Indicator " by Dreadblitz (big thanks to him!). It draws a colored zone on your chart to show ideal entry points, with a Base Point to keep you on track.

What It Does

Blue Zone: Uptrend—buy when the price dips into the zone.

Red Zone: Downtrend—sell or short when the price climbs into the zone.

Base Point: A gray line showing the key level the zone is built on.

How to Use It

Look for the colored zone:

- Blue: Buy if the price dips into the zone but stays above the Base Point.

- Red: Sell/short if the price climbs into the zone but stays below the Base Point.

Important: Avoid entering trade beyond base point - you might see low returns and face big drawdowns.

Confirm with other signals (like RSI/MACD) before entering.

Settings

ATR Length (10): How far back it looks to calculate price movement.

ATR Multiplier (2.5): How wide the zone is.

Error Margin (5.0): Keeps the zone steady during small price wiggles.

Uptrend/Downtrend Colors: Change the zone colors if you’d like!

Credits

Inspired by the "Follow Line Indicator" by Dreadblitz—check out his work for more great ideas!

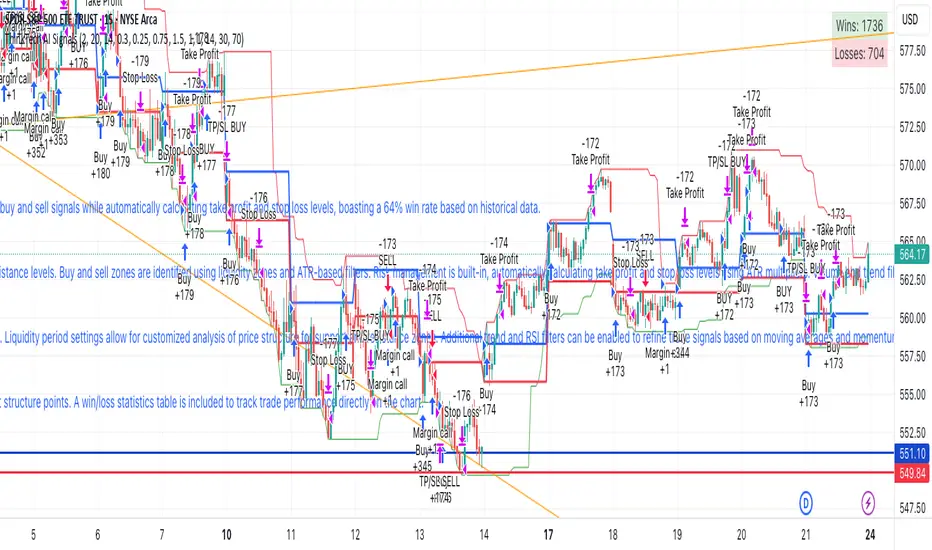

ThinkTech AI SignalsThink Tech AI Strategy

The Think Tech AI Strategy provides a structured approach to trading by integrating liquidity-based entries, ATR volatility thresholds, and dynamic risk management. This strategy generates buy and sell signals while automatically calculating take profit and stop loss levels, boasting a 64% win rate based on historical data.

Usage

The strategy can be used to identify key breakout and retest opportunities. Liquidity-based zones act as potential accumulation and distribution areas and may serve as future support or resistance levels. Buy and sell zones are identified using liquidity zones and ATR-based filters. Risk management is built-in, automatically calculating take profit and stop loss levels using ATR multipliers. Volume and trend filtering options help confirm directional bias using a 50 EMA and RSI filter. The strategy also allows for session-based trading, limiting trades to key market hours for higher probability setups.

Settings

The risk/reward ratio can be adjusted to define the desired stop loss and take profit calculations. The ATR length and threshold determine ATR-based breakout conditions for dynamic entries. Liquidity period settings allow for customized analysis of price structure for support and resistance zones. Additional trend and RSI filters can be enabled to refine trade signals based on moving averages and momentum conditions. A session filter is included to restrict trade signals to specific market hours.

Style

The strategy includes options to display liquidity lines, showing key support and resistance areas. The first 15-minute candle breakout zones can also be visualized to highlight critical market structure points. A win/loss statistics table is included to track trade performance directly on the chart.

This strategy is intended for descriptive analysis and should be used alongside other confluence factors. Optimize your trading process with Think Tech AI today!

Smart Stop-Loss (SSL)Smart Stop-Loss (SSL) Indicator

Overview

The Smart Stop-Loss (SSL) indicator is an advanced risk management tool designed to help traders set dynamic stop-loss levels based on market structure, volatility, and momentum. Unlike traditional fixed stop-loss methods, SSL adapts to changing market conditions, helping to avoid premature exits while protecting capital during true reversals.

Key Features

1. Volatility-Based Adjustments

- Uses Average True Range (ATR) to measure market volatility

- Automatically widens stop-loss during volatile periods and tightens during calm markets

- Customizable ATR multiplier (default: 1.5x) to adjust sensitivity

2. Market Structure Integration

- Identifies significant swing highs and lows to establish support/resistance levels

- Places stop-loss levels beyond these structural points to avoid common stop hunts

3. Fair Value Gap (FVG) Detection

- Identifies imbalances in order flow that often lead to strong directional moves

- Bullish FVG: A gap up where the current high is below previous low

- Bearish FVG: A gap down where the current low is above previous high

4. Smart Stop-Loss Tightening

- Automatically tightens stop-loss when FVGs are mitigated (filled)

- Uses RSI as a momentum filter to prevent premature adjustments

- Creates a trailing effect that locks in profits as trades move favorably

How to Use

For Long Positions:

1. **Entry**: Look for bullish FVG formations (green step line appears)

2. **Stop-Loss Placement**: Set your stop at or slightly below the green step line

3. **Stop Adjustment**: When price closes above the FVG zone and RSI > 50, the stop will automatically tighten

4. **Exit**: Exit the position when price closes below the green line or when your profit target is reached

For Short Positions:

1. **Entry**: Look for bearish FVG formations (red step line appears)

2. **Stop-Loss Placement**: Set your stop at or slightly above the red step line

3. **Stop Adjustment**: When price closes below the FVG zone and RSI < 50, the stop will automatically tighten

4. **Exit**: Exit the position when price closes above the red line or when your profit target is reached

Real-World Examples

Example 1: Trend Continuation

In an uptrend, when a bullish FVG appears, it often indicates institutional buying pressure. The SSL will place a stop below the swing low with an ATR buffer. As price continues upward and mitigates the FVG, the SSL tightens to protect profits while allowing the trend to continue.

Example 2: Avoiding Premature Exits

During normal market fluctuations, traditional fixed stops might get triggered too early. The SSL's adaptive nature accounts for volatility, keeping you in profitable trades longer by positioning stops beyond noise levels.

Example 3: Protecting Against Reversals

When a true reversal occurs, the momentum filter (RSI) will confirm the change in direction, allowing the SSL to maintain wider protection rather than prematurely tightening in a false move.

Tips for Best Results

1. **Timeframe Selection**: Works best on 1H, 4H and daily charts where market structure is more reliable

2. **Combine with Trend Analysis**: Use in conjunction with trend identification tools

3. **ATR Adjustment**: Increase the ATR multiplier for more volatile instruments

4. **Alert Setup**: Configure the built-in alerts to notify you when stop levels are breached

5. **Visual Confirmation**: The labels show exact stop values to help with order placement

Disclaimer

This indicator is provided for informational and educational purposes only. While it uses advanced techniques to determine potential stop-loss levels, no indicator can predict market movements with certainty. Always manage your risk appropriately and never risk more than you can afford to lose. Past performance is not indicative of future results. The developer of this indicator accepts no liability for trading losses incurred from its use. Always test thoroughly on demo accounts before using in live trading.

DrNon Action Zone📈 Strategy Title:

DrNon Action Zone — EMA Cross with ATR Stop, % Take-Profit, Alerts & Date Range

⸻

🧠 Strategy Concept:

DrNon Action Zone is a long-only trend-following strategy that enters trades when momentum aligns with long-term trend confirmation. It uses:

• EMA Cross (Fast vs. Slow) to identify momentum shift

• Optional EMA Filter based on days to confirm that price is in a “trend zone”

• ATR-based trailing stop for adaptive risk management

• Percentage Take-Profit for reward targeting

• Date Range Filter for focused backtesting or event-based execution

It also includes alerts, visual signals, and full customization via inputs.

⸻

⚙️ Strategy Inputs Explained:

Input Name Description

Fast EMA Length Period of the short-term EMA used for crossover signals (default: 5)

Slow EMA Length Period of the long-term EMA used for crossover signals (default: 200)

ATR Period Period used to calculate the Average True Range (ATR)

ATR Multiplier Multiplies ATR value to calculate the trailing stop distance

Take-Profit % Percentage above entry price to exit the trade for profit

Use EMA Filter? If enabled, long entries require price to be above a customizable EMA filter

EMA Filter Days Number of days used for EMA filter (converted to bars based on chart timeframe)

Use Date Range? Enable or disable the date filter

Start Date / End Date Specify a custom range to apply the strategy

⸻

✅ Long Entry Conditions (The Action Zone):

A long trade is entered when:

1. EMA(Fast) crosses above EMA(Slow)

2. If EMA Filter is enabled, Close > EMA(Filter Days)

3. If Date Filter is enabled, current candle is within specified start and end dates

⸻

❌ Exit Conditions:

The strategy will close the position when either:

• Price drops to ATR-based trailing stop, OR

• Price reaches the Take-Profit % target

⸻

🛎️ Alerts:

Alert Name Trigger Condition

Long Entry Alert EMA cross and all filters passed (entry signal triggered)

Exit Alert Price hit ATR Stop or Take-Profit (exit signal triggered)

⸻

📊 Visual Elements:

• Yellow Line — Fast EMA

• Blue Line — Slow EMA

• Purple Line — EMA Filter (based on user-defined days)

• Red Line — ATR-based Trailing Stop

• Lime Line — Take-Profit Level

• Green Triangle — Long Entry Signal (on crossover)

⸻

🧪 Backtesting Tips:

• Adjust EMA Filter Days to simulate different trend conditions (e.g., 100d, 150d, 200d).

• Use ATR Multiplier to adapt the stop-loss to market volatility.

• Combine date filtering with known events (e.g., earnings, FOMC meetings).

• Test in multiple timeframes — 1H, 4H, or Daily for stronger signals.

ATR Impact CandlesATR Impact Candles: Simplify Your Trading with Pure Price Action

You don’t need dozens of cluttered indicators to catch what really matters. With ATR Impact Candles, you get a powerful, single-tool solution that cuts through the noise by focusing on what truly drives the market: price action and volatility. This indicator highlights only those candlesticks that pack a punch—showing you when the market’s range is exceptionally strong relative to its recent behavior. Whether you’re a scalper or a swing trader, ATR Impact Candles empowers you to time your entries and exits with confidence, letting you trade based on real market momentum.

⸻

Indicator Overview

The indicator is designed for TradingView and is implemented in Pine Script (version 5). Its primary purpose is to highlight specific candles that meet a defined volatility condition based on the Average True Range (ATR). Instead of modifying every candle’s appearance, the indicator only changes the color of those “signal” candles that exceed a user-defined multiple of the ATR. The rest of the candles remain in their traditional black and white appearance—preserving the classic candlestick chart look.

⸻

Key Features

1. ATR-Based Signal Identification:

• ATR Calculation:

The indicator calculates the ATR using a configurable lookback period (default is 14 periods). The ATR is a common volatility measure that reflects the average range of price movement.

• Threshold Condition:

A candle is flagged as a signal if its range (high minus low) meets or exceeds a specified multiple (the “ATR Factor”) of the ATR. By default, this factor is set to 2, meaning any candle whose range is at least twice the ATR is considered significant.

2. Dynamic Candle Coloring:

• Signal Candles:

• When a candle meets the ATR threshold condition:

• Up Candles: are colored green.

• Down Candles: are colored red.

• Non-Signal Candles:

• Candles that do not meet the threshold condition retain their classic appearance:

• Up candles are white.

• Down candles are black.

3. User Configurability:

• ATR Period:

Traders can adjust the ATR period to tailor the volatility measure to different markets or timeframes.

• ATR Factor:

The multiple of the ATR that defines a signal candle is also configurable, giving flexibility to experiment with different thresholds for what constitutes “significant” price movement.

• Overlay Display:

The indicator runs in overlay mode on the chart, meaning it directly affects the appearance of the candlestick bars without interfering with other chart elements.

4. Additional Visual Aid:

• Threshold Line Plot:

The script optionally plots a line representing the ATR multiplied by the chosen factor. This line serves as a visual benchmark on the chart, allowing traders to see at what level the ATR threshold lies relative to the price action.

⸻

How It Works

1. ATR Calculation:

The indicator first calculates the Average True Range (ATR) for the defined period. This value is updated for each new candle.

2. Range Comparison:

For each candle, the indicator calculates the range (high - low) and compares it to the threshold, which is the ATR multiplied by the user-defined factor.

3. Conditional Coloring:

• If the Candle’s Range ≥ (ATR * Factor):

• The candle is marked as a “signal candle.”

• Its color is set to green if it is an up candle (close is greater than or equal to open) or red if it is a down candle.

• Otherwise:

• The candle retains its classic look, with up candles in white and down candles in black.

4. Chart Display:

By applying these rules to every candle, the indicator visually emphasizes those moments when the market shows unusually large price movements relative to its recent average volatility. This helps traders quickly spot potential breakouts or reversals.

⸻

Practical Applications

• Volatility Breakouts:

Identify candles that may signal the start of a breakout or strong reversal.

• Risk Management:

Adjust stop-loss levels or position sizes when unusually volatile candles are detected.

• Signal Confirmation:

Combine with other technical indicators or chart patterns to reinforce entry or exit decisions.

⸻

ATR Impact Candles is your essential, no-nonsense tool for filtering out market noise and focusing solely on significant price action. Simplify your trading decisions and harness the power of volatility with one clear, effective indicator.

ATR Price FrameATR Price Frame

ATR Price Frame is a versatile and customizable TradingView indicator that uses the Average True Range (ATR) to define a dynamic price frame for effective risk management and position sizing.

Risk Management:

This indicator automatically calculates the number of units (shares or contracts) you can trade based on a user-defined maximum risk. By comparing the current price to ATR-based levels, it determines the risk per unit—applying a tailored formula for stocks and futures—so you can maintain proper risk control on every trade.

Informative Labeling:

An optional label is displayed at the far right of your chart, providing clear, concise information about your calculated unit count and, if enabled, the total risk in dollars (formatted like “3 : $45.00”). With configurable text size and horizontal offset, the label is designed to integrate seamlessly into your chart setup.

Unified Line Appearance:

The indicator draws two horizontal lines—one above and one below the current price—to create the price frame. These lines use a unified appearance with settings for length, width, style, and an optional horizontal offset, ensuring a clean and consistent visual representation of market volatility.

ATR Price Frame automatically determines whether the instrument is a stock or a futures contract, applying the appropriate risk calculations. This makes it an essential tool for traders looking to integrate volatility-based risk management into their strategies.

Supertrend ProSupertrend Pro - Multi-Trend Analysis and Trading Signal Filtering

OVERVIEW

This indicator calculates trend direction based on the Supertrend indicator and integrates dual-trend analysis, upper and lower trend bands, trading signal alerts, moving average filtering, and the EMA 200 bull-bear division line to provide traders with more precise trend identification and trading signals.

It is suitable for trend trading, short-term trading, and swing trading, effectively filtering market noise and improving trade accuracy.

IMPLEMENTATION PRINCIPLES

1. Primary Trend: Uses the Supertrend indicator to calculate major trend direction, suitable for long-term trend assessment.

2. Secondary Trend: Detects short-term trend changes, capturing finer market movements.

3. Upper and Lower Trend Bands: Utilizes ATR (Average True Range) to calculate dynamic trend channels, assisting in trend strength assessment.

4. Trading Signal Alerts: Provides buy/sell signals when trends reverse, with optional moving average filtering to reduce false signals.

5. Moving Average Filtering: Supports multiple MA types, such as EMA, SMA, HMA, McGinley, helping to filter market noise.

6. EMA 200 Bull-Bear Division Line: Combines ATR-based trend buffer zones to distinguish between long-term bull and bear markets, enhancing trend accuracy.

KEY FEATURES

1. Dual-Trend Analysis

• Primary trend is suitable for long-term trend tracking, reducing interference from short-term fluctuations.

• Secondary trend is ideal for short-term trading opportunities, allowing faster identification of market turning points.

• By combining both, traders can follow the major trend direction while using the secondary trend for optimized entry points, improving trade success rates.

2. Upper and Lower Trend Bands

• ATR-based dynamic bands adjust to market volatility, avoiding the limitations of fixed support and resistance levels.

• Trend confirmation: When the price reaches the upper or lower band, traders can determine whether the market is overheated or oversold, aiding trading decisions.

• Combining primary and secondary trend bands provides clearer trend validation, reducing false signals.

3. Trading Signal Alerts

• Automatic buy/sell signal alerts when the trend reverses, eliminating the need for manual trend assessment.

• Moving average filtering improves signal reliability, reducing false signals.

• Supports various signal markers (circles/arrows/labels) to help traders clearly visualize entry points.

4. Moving Average Filtering

• Supports multiple moving average types (SMA, EMA, HMA, WMA, McGinley, etc.), adapting to different trading styles.

• Prevents counter-trend trading:

· Long entries only when the price is above the MA filter.

· Short entries only when the price is below the MA filter.

• Customizable MA periods to suit different market conditions and prevent excessive signal noise.

5. Trading Reference Lines

• Short-term trend: HMA 25 serves as an entry reference line. Waiting for MA color changes before placing trades can improve stability.

• Long-term trend: EMA 200 as the bull-bear division line helps traders distinguish between long-term bullish and bearish trends, avoiding counter-trend trades.

• Dynamic buffer adjustment: Uses ATR-based volatility buffers to reduce false signals and enhance trend detection accuracy.

• Color-coded trend identification:

· Aqua (Bull Market): Price is above the buffer zone.

· Fuchsia (Bear Market): Price is below the buffer zone.

· White: Price is within the buffer zone, indicating an unclear market direction.

USAGE GUIDELINES

1. Applicable Markets

• Suitable for stocks, futures, cryptocurrencies, and forex

• Supports short-term trading, trend trading, and swing trading

2. Recommended Timeframes

• Short-term traders can use 5m, 15m, and 1H timeframes, leveraging secondary trend signals for quick market entries.

• Trend traders can use 4H and daily timeframes, relying on primary trend signals to assess major trends.

• Long-term investors can use the EMA 200 bull-bear division line to determine macro trend direction and avoid counter-trend trades.

3. Trading Strategy

• Long Entry:

The primary trend is bullish (Green).

The secondary trend triggers a buy signal (Long).

• Short Entry:

· The primary trend is bearish (Red).

· The secondary trend triggers a sell signal (Short).

• Enable Moving Average Filtering:

· Only enter long trades when the price is above the MA filter.

· Only enter short trades when the price is below the MA filter.

• Use EMA 200 for Market Direction:

· If the price is above EMA 200 + buffer, the market is in a bullish trend → favor long trades.

· If the price is below EMA 200 - buffer, the market is in a bearish trend → favor short trades.

• Market Volatility Considerations:

· Short timeframes (1m, 5m) may produce more noise, reducing signal reliability.

· Higher timeframes (1H, 4H, Daily) provide more stable trend signals but may miss some short-term trade opportunities.

RISK DISCLAIMER

• This indicator calculates trend direction based on historical data and cannot guarantee future market performance. When using this indicator for trading, always combine it with other technical analysis tools, fundamental analysis, and personal trading experience for comprehensive decision-making.

• Market conditions are uncertain, and trend signals may result in false positives or lag. Traders should avoid over-reliance on indicator signals and implement stop-loss strategies and risk management techniques to reduce potential losses.

• Leverage trading carries high risks and may result in rapid capital loss. If using this indicator in leveraged markets (such as futures, forex, or cryptocurrency derivatives), exercise caution, manage risks properly, and set reasonable stop-loss/take-profit levels to protect funds.

• All trading decisions are the sole responsibility of the trader. The developer is not liable for any trading losses. This indicator is for technical analysis reference only and does not constitute investment advice.

• Before live trading, it is recommended to use a demo account for testing to fully understand how to use the indicator and apply proper risk management strategies.

CHANGELOG

• v1.0: Initial release with a dual-trend system, dynamic upper and lower trend bands, trading signal alerts, moving average filtering, HMA trading reference line, and EMA 200 bull-bear division.

ATR Stop Loss & 3 TP FinderATR Stop Loss & 3 TP Finder - By SeehraSingh

This indicator is designed to help traders automate Stop Loss (SL) and Take Profit (TP) placement based on the Average True Range (ATR). It dynamically calculates:

Stop Loss (SL): Set based on a user-defined ATR multiplier.

Three Take Profit (TP) levels: Configurable ATR multipliers for TP1, TP2, and TP3.

Customizable Price Sources: Allows traders to choose different price sources (Open, High, Low, Close, HL2, HLC3, OHLC4, HLCC4) for both SL and TP calculations.

Visual Representation: Plots dashed lines for Entry, SL, TP1, TP2, and TP3.

Table Display: Provides an easy-to-read table at the bottom showing SL, TP1, TP2, and TP3 values.

How It Works:

Select ATR length and smoothing type (RMA, SMA, EMA, WMA).

Set ATR multipliers for SL and TP levels.

Choose the price source for SL and TP calculations.

The indicator automatically plots entry, SL, and three TP levels on the chart.

Ideal For:

Traders who use ATR-based dynamic Stop Loss and Take Profit strategies.

Those who want to avoid fixed SL/TP placements and prefer volatility-based risk management.

Scalpers, Swing Traders, and Position Traders looking for automated SL/TP visualization.

Disclaimer

⚠️ Trading involves risk. This indicator is for educational purposes only and should not be considered financial advice. Always conduct your own analysis before entering any trade. The author is not responsible for any financial losses incurred while using this tool. Past performance does not guarantee future results.

Higher Timeframe Support/ResistanceMulti-Timeframe Support/Resistance Indicator

This TradingView indicator helps you monitor important support and resistance levels based on the previous candle’s high, low, and close from a higher timeframe. By default, it uses a daily timeframe, but you can adjust this to any timeframe you want.

Key Features:

- Previous Candle High (PCH) and Previous Candle Low (PCL):

These levels are plotted on your chart (if enabled) and can act as potential support and

resistance zones. You can toggle the visibility of these levels.

- Pivot, Resistance (R1), and Support (S1):

The script calculates Pivot, R1 (Resistance), and S1 (Support) levels based on the previous

candle's price action from the selected higher timeframe.

These levels are displayed on your chart and can be used to identify potential breakout or

reversal points.

- Alert Feature:

Alerts are triggered when the price approaches any of these key levels (PCH, PCL, Pivot, R1,

or S1) within a specified threshold (e.g., 0.5%).

This helps traders react quickly to potential price movements near critical levels.

- Visual Representation:

The script visually fills the areas between Pivot and R1 (Resistance-Pivot Zone) and Pivot and

S1 (Support-Pivot Zone) with color for easy identification of key price zones.