ETH Growth | AlchimistOfCrypto⚠️ DISCLAIMER: This indicator's source code is kept private as it represents a first-of-its-kind innovation in algorithmic cycle detection and visualization for Ethereum. The mathematical models and proprietary algorithms powering this indicator are the result of extensive research and development.

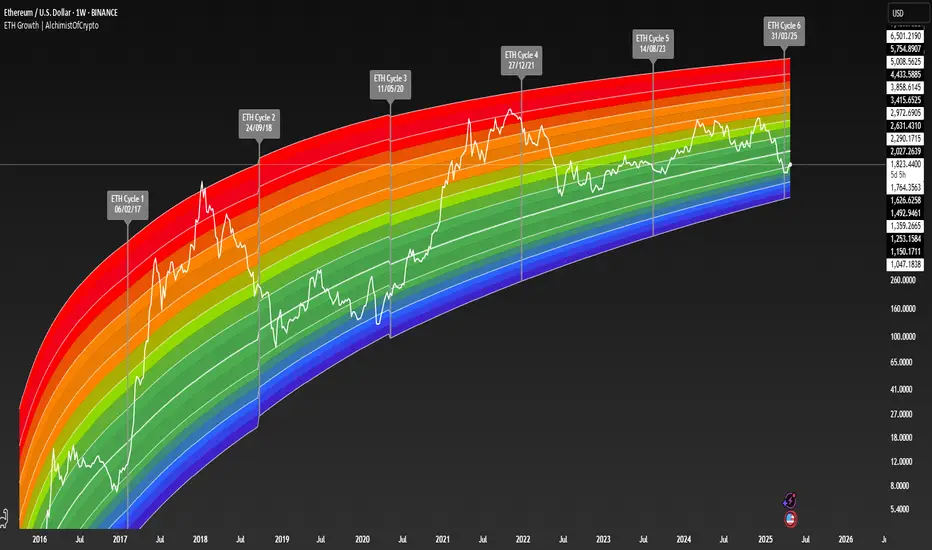

🌈 ETH Growth Rainbow – Unveiling Ethereum's Logarithmic Growth Fields 🌈

"The ETH Growth Rainbow, engineered through advanced logarithmic mathematics, visualizes the probabilistic distribution of Ethereum's price evolution within a multi-cycle growth paradigm. This indicator employs principles from logarithmic regression where coefficients p001, p002, and p003 create mathematical boundaries that define Ethereum's long-term value progression. Our implementation features algorithmically enhanced rainbow visualization derived from Fast Fourier Transform (FFT) spectral analysis, creating a dynamic representation of Ethereum's logarithmic growth with adaptive color gradients that highlight critical cycle-based phase transitions in the asset's monetary evolution."

📊 Professional Trading Application

The ETH Growth Rainbow transcends traditional price prediction models with a sophisticated multi-band illumination system that reveals the underlying structure of Ethereum's monetary evolution. Scientifically calibrated across multiple 85-week cycles (detected through spectral analysis) and featuring seamless rainbow visualization, it enables investors to perceive Ethereum's position within its macro growth trajectory with unprecedented clarity.

- Cycle Detection Methodology 🔬

The 85-week Ethereum cycle was discovered through sophisticated Fast Fourier Transform (FFT) analysis:

- Logarithmic price returns extracted from historical Ethereum data

- FFT decomposition identifies dominant frequency components in price movements

- Signal amplitude analysis reveals the 85-week cycle as the most statistically significant periodicity

- Adaptive frequency filtering validates cycle consistency across multiple market phases

- Cycle duration rounded to nearest week for practical application

- Visual Theming 🎨

Scientifically designed rainbow gradient optimized for cycle pattern recognition:

- Violet-Blue: Lower value accumulation zones with highest mathematical growth potential

- Green: Fair value equilibrium zone representing the regression mean

- Yellow-Orange: Moderate overvaluation regions indicating potential resistance

- Red: Statistical extreme zones indicating mathematical cycle peaks

- Deep Red: New euphoria band (+6) capturing exceptional market extremes

- Cycle Visualization 🔍

- Precise cycle boundaries demarcating Ethereum's fundamental cycle events

- Adaptive band spacing based on mathematical cycle progression (p003 = 0.858)

- Multiple sub-cycle markers revealing the probabilistic nature of Ethereum's trajectory

- Initial cycle starting from 0.1639 (August 3, 2015) to preserve historical accuracy

🚀 How to Use

1. Identify Macro Position ⏰: Locate Ethereum's current price relative to regression bands

2. Understand Cycle Context 🎚️: Note position within the current 85-week cycle for time-based analysis

3. Assess Mathematical Value 🌈: Determine potential over/undervaluation based on band location

4. Adjust Investment Strategy 🔎: Modulate position sizing based on mathematical value assessment

5. Identify Cycle Phases ✅: Monitor band transitions to detect accumulation and distribution zones

6. Invest with Precision 🛡️: Utilize lower bands for strategic accumulation, upper bands for strategic reduction

7. Manage Risk Dynamically 🔐: Scale investment allocations based on mathematical cycle positioning

#ethereum #ETH #cryptocurrency #tradingview #technicalanalysis #logarithmicregression #rainbowchart #cryptotrading #tradingstrategy #priceaction #cryptoinvesting #ethanalysis #tradingbands #cryptoresearch #FFTanalysis #cyclicalanalysis #ethinvestment #ethusd #buyandsell #accumulation #macroindicator #valueanalysis #priceprediction #ethgrowth #cryptosignals #cyclicpatterns #mathematicaltrading #AI #smartmoney #cryptowhales

Pine Script® indicator