Power Law Divergence in % - For Bitcoin Only_JPBitcoin Power Law Divergence

The Bitcoin Power Law Divergence is a representation of Bitcoin prices first proposed by Giovanni Santostasi, Ph.D. It plots BTCUSD daily closes on a log10-log10 scale, and fits a linear regression channel to the data.

This channel helps traders visualise when the price is historically in a zone prone to tops or located within a discounted zone subject to future growth.

Giovanni Santostasi, Ph.D. originated the Bitcoin Power-Law Theory; this implementation places it directly on a TradingView chart. The white line shows the daily closing price, while the cyan line is the best-fit regression.

A channel is constructed from the linear fit root mean squared error (RMSE), we can observe how price has repeatedly oscillated between each channel areas through every bull-bear cycle.

DETAILS

One of the advantages of the Power Law Theory proposed by Giovanni Santostasi is its ability to explain multiple behaviors of Bitcoin. We describe some key points below.

Power-Law Overview

A power law has the form y = A·xⁿ, and Bitcoin’s key variables follow this pattern across many orders of magnitude. Empirically, price rises roughly with t⁶, hash-rate with t¹² and the number of active addresses with t³.

When we plot these on log-log axes they appear as straight lines, revealing a scale-invariant system whose behaviour repeats proportionally as it grows.

Search in scripts for "Cycle"

True Opens - (SpeculatorBryan)Overview

This indicator provides a complete framework of key institutional levels by plotting the "True Open" price for the Month, Week, Day, and Intraday Sessions. Instead of using standard chart opens, it uses specific, globally significant times (based in the NY timezone) to identify levels that price action traders watch closely for support, resistance, and market direction.

What It Does

True Monthly Open (TMO): The key macro level, marking the start of the month's trading.

True Weekly Open (TWO): Arguably the most important level, defining the weekly bias. Based on the Sunday evening start of the forex trading week.

True Daily Open (TDO): The New York midnight open, marking the true start of the institutional 24-hour cycle.

True Session Opens (TSO): Key intraday opens (e.g., London, NY) for finding entries and exits on lower timeframes.

Key Features

Clean Forward Projection: All lines and labels project into the future, so you always see the levels in your current price action.

Full Styling Control: Customize the color, style (solid, dashed, dotted), and text for every level to match your chart theme.

Intelligent Display: Levels automatically show on appropriate timeframes to keep your chart clutter-free. Use the "Stacked Opens" feature to override this.

Lightweight & Efficient: Optimized to run smoothly without lagging your chart.

How to Use It

Look for price to react at these levels. A bounce can signal a continuation, while a clean break and retest can signal a change in market structure. Use the higher-timeframe opens (TMO, TWO) as major anchors for your overall bias and the lower-timeframe opens (TDO, TSO) for fine-tuning your entries and exits.

Fair Value Trend Model [SiDec]ABSTRACT

This pine script introduces the Fair Value Trend Model, an on-chart indicator for TradingView that constructs a continuously updating "fair-value" estimate of an asset's price via a logarithmic regression on historical data. Specifically, this model has been applied to Bitcoin (BTC) to fully grasp its fair value in the cryptocurrency market. Symmetric channel bands, defined by fixed percentage offsets around this central fair-value curve, provide a visual band within which normal price fluctuations may occur. Additionally, a short-term projection extends both the fair-value trend and its channel bands forward by a user-specified number of bars.

INTRODUCTION

Technical analysts frequently seek to identify an underlying equilibrium or "fair value" about which prices oscillate. Traditional approaches-moving averages, linear regressions in price-time space, or midlines-capture linear trends but often misrepresent the exponential or power-law growth patterns observable in many financial markets. The Fair Value Trend Model addresses this by performing an ordinary least squares (OLS) regression in log-space, fitting ln(Price) against ln(Days since inception). In practice, the primary application has been to Bitcoin, aiming to fully capture Bitcoin's underlying value dynamics.

The result is a curved trend line in regular (price-time) coordinates, reflecting Bitcoin's long-term compounding characteristics. Surrounding this fair-value curve, symmetric bands at user-specified percentage deviations serve as dynamic support and resistance levels. A simple linear projection extends both the central fair-value and its bands into the immediate future, providing traders with a heuristic for short-term trend continuation.

This exposition details:

Data transformation: converting bar timestamps into days since first bar, then applying natural logarithms to both time and price.

Regression mechanics: incremental (or rolling-window) accumulation of sums to compute the log-space fit parameters.

Fair-value reconstruction: exponentiation of the regression output to yield a price-space estimate.

Channel-band definition: establishing ±X% offsets around the fair-value curve and rendering them visually.

Forecasting methodology: projecting both the fair-value trend and channel bands by extrapolating the most recent incremental change in price-space.

Interpretation: how traders can leverage this model for trend identification, mean-reversion setups, and breakout analysis, particularly in Bitcoin trading.

Analysing the macro cycle on Bitcoin's monthly timeframe illustrates how the fair-value curve aligns with multi-year structural turning points.

DATA TRANSFORMATION AND NOTATION

1. Timestamp Baseline (t0)

Let t0 = timestamp of the very first bar on the chart (in milliseconds). Each subsequent bar has a timestamp ti, where ti ≥ t0.

2. Days Since Inception (d(t))

Define the “days since first bar” as

d(t) = max(1, (t − t0) / 86400000.0)

Here, 86400000.0 represents the number of milliseconds in one day (1,000 ms × 60 seconds × 60 minutes × 24 hours). The lower bound of 1 ensures that we never compute ln(0).

3. Logarithmic Coordinates:

Given the bar’s closing price P(t), define:

xi = ln( d(ti) )

yi = ln( P(ti) )

Thus, each data point is transformed to (xi, yi) in log‐space.

REGRESSION FORMULATION

We assume a log‐linear relationship:

yi = a + b·xi + εi

where εi is the residual error at bar i. Ordinary least squares (OLS) fitting minimizes the sum of squared residuals over N data points. Define the following accumulated sums:

Sx = Σ for i = 1 to N

Sy = Σ for i = 1 to N

Sxy = Σ for i = 1 to N

Sx2 = Σ for i = 1 to N

N = number of data points

The OLS estimates for b (slope) and a (intercept) are:

b = ( N·Sxy − Sx·Sy ) / ( N·Sx2 − (Sx)^2 )

a = ( Sy − b·Sx ) / N

All‐Time Versus Rolling‐Window Mode:

All-Time Mode:

Each new bar increments N by 1.

Update Sx ← Sx + xN, Sy ← Sy + yN, Sxy ← Sxy + xN·yN, Sx2 ← Sx2 + xN^2.

Recompute a and b using the formulas above on the entire dataset.

Rolling-Window Mode:

Fix a window length W. Maintain two arrays holding the most recent W values of {xi} and {yi}.

On each new bar N:

Append (xN, yN) to the arrays; add xN, yN, xN·yN, xN^2 to the sums Sx, Sy, Sxy, Sx2.

If the arrays’ length exceeds W, remove the oldest point (xN−W, yN−W) and subtract its contributions from the sums.

Update N_roll = min(N, W).

Compute b and a using N_roll, Sx, Sy, Sxy, Sx2 as above.

This incremental approach requires only O(1) operations per bar instead of recomputing sums from scratch, making it computationally efficient for long time series.

FAIR‐VALUE RECONSTRUCTION

Once coefficients (a, b) are obtained, the regressed log‐price at time t is:

ŷ(t) = a + b·ln( d(t) )

Mapping back to price space yields the “fair‐value”:

F(t) = exp( ŷ(t) )

= exp( a + b·ln( d(t) ) )

= exp(a) · ^b

In other words, F(t) is a power‐law function of “days since inception,” with exponent b and scale factor C = exp(a). Special cases:

If b = 1, F(t) = C · d(t), which is an exponential function in original time.

If b > 1, the fair‐value grows super‐linearly (accelerating compounding).

If 0 < b < 1, it grows sub‐linearly.

If b < 0, the fair‐value declines over time.

CHANNEL‐BAND DEFINITION

To visualise a “normal” range around the fair‐value curve F(t), we define two channel bands at fixed percentage offsets:

1. Upper Channel Band

U(t) = F(t) · (1 + α_upper)

where α_upper = (Channel Band Upper %) / 100.

2. Lower Channel Band

L(t) = F(t) · (1 − α_lower)

where α_lower = (Channel Band Lower %) / 100.

For example, default values of 50% imply α_upper = α_lower = 0.50, so:

U(t) = 1.50 · F(t)

L(t) = 0.50 · F(t)

When “Show FV Channel Bands” is enabled, both U(t) and L(t) are plotted in a neutral grey, and a semi‐transparent fill is drawn between them to emphasise the channel region.

SHORT‐TERM FORECAST PROJECTION

To extend both the fair‐value and its channel bands M bars into the future, the model uses a simple constant‐increment extrapolation in price space. The procedure is:

1. Compute Recent Increments

Let

F_prev = F( t_{N−1} )

F_curr = F( t_N )

Then define the per‐bar change in fair‐value:

ΔF = F_curr − F_prev

Similarly, for channel bands:

U_prev = U( t_{N−1} ), U_curr = U( t_N ), ΔU = U_curr − U_prev

L_prev = L( t_{N−1} ), L_curr = L( t_N ), ΔL = L_curr − L_prev

2. Forecasted Values After M Bars

Assuming the same per‐bar increments continue:

F_future = F_curr + M · ΔF

U_future = U_curr + M · ΔU

L_future = L_curr + M · ΔL

These forecasted values produce dashed lines on the chart:

A dashed segment from (bar_N, F_curr) to (bar_{N+M}, F_future).

Dashed segments from (bar_N, U_curr) to (bar_{N+M}, U_future), and from (bar_N, L_curr) to (bar_{N+M}, L_future).

Forecasted channel bands are rendered in a subdued grey to distinguish them from the current solid bands. Because this method does not re‐estimate regression coefficients for future t > t_N, it serves as a quick visual heuristic of trend continuation rather than a precise statistical forecast.

MATHEMATICAL SUMMARY

Summarising all key formulas:

1. Days Since Inception

d(t_i) = max( 1, ( t_i − t0 ) / 86400000.0 )

x_i = ln( d(t_i) )

y_i = ln( P(t_i) )

2. Regression Summations (for i = 1..N)

Sx = Σ

Sy = Σ

Sxy = Σ

Sx2 = Σ

N = number of data points (or N_roll if using rolling‐window)

3. OLS Estimator

b = ( N · Sxy − Sx · Sy ) / ( N · Sx2 − (Sx)^2 )

a = ( Sy − b · Sx ) / N

4. Fair‐Value Computation

ŷ(t) = a + b · ln( d(t) )

F(t) = exp( ŷ(t) ) = exp(a) · ^b

5. Channel Bands

U(t) = F(t) · (1 + α_upper)

L(t) = F(t) · (1 − α_lower)

with α_upper = (Channel Band Upper %) / 100, α_lower = (Channel Band Lower %) / 100.

6. Forecast Projection

ΔF = F_curr − F_prev

F_future = F_curr + M · ΔF

ΔU = U_curr − U_prev

U_future = U_curr + M · ΔU

ΔL = L_curr − L_prev

L_future = L_curr + M · ΔL

IMPLEMENTATION CONSIDERATIONS

1. Time Precision

Timestamps are recorded in milliseconds. Dividing by 86400000.0 yields days with fractional precision.

For the very first bar, d(t) = 1 ensures x = ln(1) = 0, avoiding an undefined logarithm.

2. Incremental Versus Sliding Summation

All‐Time Mode: Uses persistent scalar variables (Sx, Sy, Sxy, Sx2, N). On each new bar, add the latest x and y contributions to the sums.

Rolling‐Window Mode: Employs fixed‐length arrays for {x_i} and {y_i}. On each bar, append (x_N, y_N) and update sums; if array length exceeds W, remove the oldest element and subtract its contribution from the sums. This maintains exact sums over the most recent W data points without recomputing from scratch.

3. Numerical Robustness

If the denominator N·Sx2 − (Sx)^2 equals zero (e.g., all x_i identical, as when only one day has passed), then set b = 0 and a = Sy / N. This produces a constant fair‐value F(t) = exp(a).

Enforcing d(t) ≥ 1 avoids attempts to compute ln(0).

4. Plotting Strategy

The fair‐value line F(t) is plotted on each new bar. Its color depends on whether the current price P(t) is above or below F(t): a “bullish” color (e.g., green) when P(t) ≥ F(t), and a “bearish” color (e.g., red) when P(t) < F(t).

The channel bands U(t) and L(t) are plotted in a neutral grey when enabled; otherwise they are set to “not available” (no plot).

A semi‐transparent fill is drawn between U(t) and L(t). Because the fill function is executed at global scope, it is automatically suppressed if either U(t) or L(t) is not plotted (na).

5. Forecast Line Management

Each projection line (for F, U, and L) is created via a persistent line object. On successive bars, the code updates the endpoints of the same line rather than creating a new one each time, preserving chart clarity.

If forecasting is disabled, any existing projection lines are deleted to avoid cluttering the chart.

INTERPRETATION AND APPLICATIONS

1. Trend Identification

The fair‐value curve F(t) represents the best‐fit long‐term trend under the assumption that ln(Price) scales linearly with ln(Days since inception). By capturing power‐law or exponential patterns, it can more accurately reflect underlying compounding behavior than simple linear regressions.

When actual price P(t) lies above U(t), it may be considered “overextended” relative to its long‐term trend; when price falls below L(t), it may be deemed “oversold.” These conditions can signal potential mean‐reversion or breakout opportunities.

2. Mean‐Reversion and Breakout Signals

If price re‐enters the channel after touching or slightly breaching L(t), some traders interpret this as a mean‐reversion bounce and consider initiating a long position.

Conversely, a sustained move above U(t) can indicate strong upward momentum and a possible bullish breakout. Traders often seek confirmation (e.g., price remaining above U(t) for multiple bars, rising volume, or corroborating momentum indicators) before acting.

3. Rolling Versus All‐Time Usage

All‐Time Mode: Captures the entire dataset since inception, focusing on structural, long‐term trends. It is less sensitive to short‐term noise or volatility spikes.

Rolling‐Window Mode: Restricts the regression to the most recent W bars, making the fair‐value curve more responsive to changing market regimes, sudden volatility expansions, or fundamental shifts. Traders who wish to align the model with local behaviour often choose W so that it approximates a market cycle length (e.g., 100–200 bars on a daily chart).

4. Channel Percentage Selection

A wider band (e.g., ±50 %) accommodates larger price swings, reducing the frequency of breaches but potentially delaying actionable signals.

A narrower band (e.g., ±10 %) yields more frequent “overbought/oversold” alerts but may produce more false signals during normal volatility. It is advisable to calibrate the channel width to the asset’s historical volatility regime.

5. Forecast Cautions

The short‐term projection assumes that the last single‐bar increment ΔF remains constant for M bars. In reality, trend acceleration or deceleration can occur, rendering the linear forecast inaccurate.

As such, the forecast serves as a visual guide rather than a statistically rigorous prediction. It is best used in conjunction with other momentum, volume, or volatility indicators to confirm trend continuation or reversal.

LIMITATIONS AND CONSIDERATIONS

1. Power‐Law Assumption

By fitting ln(P) against ln(d), the model posits that P(t) ≈ C · ^b. Real markets may deviate from a pure power‐law, especially around significant news events or structural regime changes. Temporary misalignment can occur.

2. Fixed Channel Width

Markets exhibit heteroskedasticity: volatility can expand or contract unpredictably. A static ±X % band does not adapt to changing volatility. During high‐volatility periods, a fixed ±50 % may prove too narrow and be breached frequently; in unusually calm periods, it may be excessively broad, masking meaningful variations.

3. Endpoint Sensitivity

Regression‐based indicators often display greater curvature near the most recent data, especially under rolling‐window mode. This can create sudden “jumps” in F(t) when new bars arrive, potentially confusing users who expect smoother behaviour.

4. Forecast Simplification

The projection does not re‐estimate regression slope b for future times. It only extends the most recent single‐bar change. Consequently, it should be regarded as an indicative extension rather than a precise forecast.

PRACTICAL IMPLEMENTATION ON TRADINGVIEW

1 Adding the Indicator

In TradingView’s “Indicators” dialog, search for Fair Value Trend Model or visit my profile, under "scripts" add it to your chart.

Add it to any chart (e.g., BTCUSD, AAPL, EURUSD) to see real‐time computation.

2. Configuring Inputs

Show Forecast Line: Toggle on or off the dashed projection of the fair‐value.

Forecast Bars: Choose M, the number of bars to extend into the future (default is often 30).

Forecast Line Colour: Select a high‐contrast colour (e.g., yellow).

Bullish FV Colour / Bearish FV Colour: Define the colour of the fair‐value line when price is above (e.g., green) or below it (e.g., red).

Show FV Channel Bands: Enable to display the grey channel bands around the fair‐value.

Channel Band Upper % / Channel Band Lower %: Set α_upper and α_lower as desired (defaults of 50 % create a ±50 % envelope).

Use Rolling Window?: Choose whether to restrict the regression to recent data.

Window Bars: If rolling mode is enabled, designate W, the number of bars to include.

3. Visual Output

The central curve F(t) appears on the price chart, coloured green when P(t) ≥ F(t) and red when P(t) < F(t).

If channel bands are enabled, the chart shows two grey lines U(t) and L(t) and a subtle shading between them.

If forecasting is active, dashed extensions of F(t), U(t), and L(t) appear, projecting forward by M bars in neutral hues.

CONCLUSION

The Fair Value Trend Model furnishes traders with a mathematically principled estimate of an asset’s equilibrium price curve by fitting a log‐linear regression to historical data. Its channel bands delineate a normal corridor of fluctuation based on fixed percentage offsets, while an optional short‐term projection offers a visual approximation of trend continuation.

By operating in log‐space, the model effectively captures exponential or power‐law growth patterns that linear methods overlook. Rolling‐window capability enables responsiveness to regime shifts, whereas all‐time mode highlights broader structural trends. Nonetheless, users should remain mindful of the model’s assumptions—particularly the power‐law form and fixed band percentages—and employ the forecast projection as a supplemental guide rather than a standalone predictor.

When combined with complementary indicators (e.g., volatility measures, momentum oscillators, volume analysis) and robust risk management, the Fair Value Trend Model can enhance market timing, mean‐reversion identification, and breakout detection across diverse trading environments.

REFERENCES

Draper, N. R., & Smith, H. (1998). Applied Regression Analysis (3rd ed.). Wiley.

Tsay, R. S. (2014). Introductory Time Series with R (2nd ed.). Springer.

Hull, J. C. (2017). Options, Futures, and Other Derivatives (10th ed.). Pearson.

These references provide background on regression, time-series analysis, and financial modeling.

The Mayan CalendarThis indicator displays the current date in the Mayan Calendar, based on real-time UTC time. It calculates and presents:

🌀 Long Count (Baktun.Katun.Tun.Uinal.Kin) – A linear count of days since the Mayan epoch (August 11, 3114 BCE).

🔮 Tzolk'in Date – A 260-day sacred cycle combining a number (1–13) and one of 20 day names (e.g., 4 Ajaw).

🌾 Haab' Date – A 365-day civil cycle divided into 18 months of 20 days + 5 "nameless" days (Wayeb').

The calculations follow Smithsonian standards and align with the Maya Calendar Converter from the National Museum of the American Indian:

👉 maya.nmai.si.edu

The results are shown in a table overlay on your chart's top-right corner. This indicator is great for symbolic traders, astro enthusiasts, or anyone interested in ancient timekeeping systems woven into financial timeframes. Enjoy, time travelers! ⌛

Logarithmic Regression AlternativeLogarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time. Bitcoin is a good example.

𝑦 = 𝑎 + 𝑏 * ln(𝑥)

With this logarithmic regression (log reg) formula 𝑦 (price) is calculated with constants 𝑎 and 𝑏, where 𝑥 is the bar_index .

Instead of using the sum of log x/y values, together with the dot product of log x/y and the sum of the square of log x-values, to calculate a and b, I wanted to see if it was possible to calculate a and b differently.

In this script, the log reg is calculated with several different assumed a & b values, after which the log reg level is compared to each Swing. The log reg, where all swings on average are closest to the level, produces the final 𝑎 & 𝑏 values used to display the levels.

🔶 USAGE

The script shows the calculated logarithmic regression value from historical swings, provided there are enough swings, the price pattern fits the log reg model, and previous swings are close to the calculated Top/Bottom levels.

When the price approaches one of the calculated Top or Bottom levels, these levels could act as potential cycle Top or Bottom.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Swings are based on Weekly bars. A Top Swing, for example, with Swing setting 30, is the highest value in 60 weeks. Thirty bars at the left and right of the Swing will be lower than the Top Swing. This means that a confirmation is triggered 30 weeks after the Swing. The period will be automatically multiplied by 7 on the daily chart, where 30 becomes 210 bars.

Please note that the goal of this script is not to show swings rapidly; it is meant to show the potential next cycle's Top/Bottom levels.

🔹 Multiple Levels

The script includes the option to display 3 Top/Bottom levels, which uses different values for the swing calculations.

Top: 'high', 'maximum open/close' or 'close'

Bottom: 'low', 'minimum open/close' or 'close'

These levels can be adjusted up/down with a percentage.

Lastly, an "Average" is included for each set, which will only be visible when "AVG" is enabled, together with both Top and Bottom levels.

🔹 Notes

Users have to check the validity of swings; the above example only uses 1 Top Swing for its calculations, making the Top level unreliable.

Here, 1 of the Bottom Swings is pretty far from the bottom level, changing the swing settings can give a more reliable bottom level where all swings are close to that level.

Note the display was set at "Logarithmic", it can just as well be shown as "Regular"

In the example below, the price evolution does not fit the logarithmic regression model, where growth should accelerate rapidly at first and then slows over time.

Please note that this script can only be used on a daily timeframe or higher; using it at a lower timeframe will show a warning. Also, it doesn't work with bar-replay.

🔶 DETAILS

The code gathers data from historical swings. At the last bar, all swings are calculated with different a and b values. The a and b values which results in the smallest difference between all swings and Top/Bottom levels become the final a and b values.

The ranges of a and b are between -20.000 to +20.000, which means a and b will have the values -20.000, -19.999, -19.998, -19.997, -19.996, ... -> +20.000.

As you can imagine, the number of calculations is enormous. Therefore, the calculation is split into parts, first very roughly and then very fine.

The first calculations are done between -20 and +20 (-20, -19, -18, ...), resulting in, for example, 4.

The next set of calculations is performed only around the previous result, in this case between 3 (4-1) and 5 (4+1), resulting in, for example, 3.9. The next set goes even more in detail, for example, between 3.8 (3.9-0.1) and 4.0 (3.9 + 0.1), and so on.

1) -20 -> +20 , then loop with step 1 (result (example): 4 )

2) 4 - 1 -> 4 +1 , then loop with step 0.1 (result (example): 3.9 )

3) 3.9 - 0.1 -> 3.9 +0.1 , then loop with step 0.01 (result (example): 3.93 )

4) 3.93 - 0.01 -> 3.93 +0.01, then loop with step 0.001 (result (example): 3.928)

This ensures complicated calculations with less effort.

These calculations are done at the last bar, where the levels are displayed, which means you can see different results when a new swing is found.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 SETTINGS

Three sets

High/Low

• color setting

• Swing Length settings for 'High' & 'Low'

• % adjustment for 'High' & 'Low'

• AVG: shows average (when both 'High' and 'Low' are enabled)

Max/Min (maximum open/close, minimum open/close)

• color setting

• Swing Length settings for 'Max' & 'Min'

• % adjustment for 'Max' & 'Min'

• AVG: shows average (when both 'Max' and 'Min' are enabled)

Close H/Close L (close Top/Bottom level)

• color setting

• Swing Length settings for 'Close H' & 'Close L'

• % adjustment for 'Close H' & 'Close L'

• AVG: shows average (when both 'Close H' and 'Close L' are enabled)

Show Dashboard, including Top/Bottom levels of the desired source and calculated a and b values.

Show Swings + Dot size

Intellect_city - Halvings Bitcoin CycleWhat is halving?

The halving timer shows when the next Bitcoin halving will occur, as well as the dates of past halvings. This event occurs every 210,000 blocks, which is approximately every 4 years. Halving reduces the emission reward by half. The original Bitcoin reward was 50 BTC per block found.

Why is halving necessary?

Halving allows you to maintain an algorithmically specified emission level. Anyone can verify that no more than 21 million bitcoins can be issued using this algorithm. Moreover, everyone can see how much was issued earlier, at what speed the emission is happening now, and how many bitcoins remain to be mined in the future. Even a sharp increase or decrease in mining capacity will not significantly affect this process. In this case, during the next difficulty recalculation, which occurs every 2014 blocks, the mining difficulty will be recalculated so that blocks are still found approximately once every ten minutes.

How does halving work in Bitcoin blocks?

The miner who collects the block adds a so-called coinbase transaction. This transaction has no entry, only exit with the receipt of emission coins to your address. If the miner's block wins, then the entire network will consider these coins to have been obtained through legitimate means. The maximum reward size is determined by the algorithm; the miner can specify the maximum reward size for the current period or less. If he puts the reward higher than possible, the network will reject such a block and the miner will not receive anything. After each halving, miners have to halve the reward they assign to themselves, otherwise their blocks will be rejected and will not make it to the main branch of the blockchain.

The impact of halving on the price of Bitcoin

It is believed that with constant demand, a halving of supply should double the value of the asset. In practice, the market knows when the halving will occur and prepares for this event in advance. Typically, the Bitcoin rate begins to rise about six months before the halving, and during the halving itself it does not change much. On average for past periods, the upper peak of the rate can be observed more than a year after the halving. It is almost impossible to predict future periods because, in addition to the reduction in emissions, many other factors influence the exchange rate. For example, major hacks or bankruptcies of crypto companies, the situation on the stock market, manipulation of “whales,” or changes in legislative regulation.

---------------------------------------------

Table - Past and future Bitcoin halvings:

---------------------------------------------

Date: Number of blocks: Award:

0 - 03-01-2009 - 0 block - 50 BTC

1 - 28-11-2012 - 210000 block - 25 BTC

2 - 09-07-2016 - 420000 block - 12.5 BTC

3 - 11-05-2020 - 630000 block - 6.25 BTC

4 - 20-04-2024 - 840000 block - 3.125 BTC

5 - 24-03-2028 - 1050000 block - 1.5625 BTC

6 - 26-02-2032 - 1260000 block - 0.78125 BTC

7 - 30-01-2036 - 1470000 block - 0.390625 BTC

8 - 03-01-2040 - 1680000 block - 0.1953125 BTC

9 - 07-12-2043 - 1890000 block - 0.09765625 BTC

10 - 10-11-2047 - 2100000 block - 0.04882813 BTC

11 - 14-10-2051 - 2310000 block - 0.02441406 BTC

12 - 17-09-2055 - 2520000 block - 0.01220703 BTC

13 - 21-08-2059 - 2730000 block - 0.00610352 BTC

14 - 25-07-2063 - 2940000 block - 0.00305176 BTC

15 - 28-06-2067 - 3150000 block - 0.00152588 BTC

16 - 01-06-2071 - 3360000 block - 0.00076294 BTC

17 - 05-05-2075 - 3570000 block - 0.00038147 BTC

18 - 08-04-2079 - 3780000 block - 0.00019073 BTC

19 - 12-03-2083 - 3990000 block - 0.00009537 BTC

20 - 13-02-2087 - 4200000 block - 0.00004768 BTC

21 - 17-01-2091 - 4410000 block - 0.00002384 BTC

22 - 21-12-2094 - 4620000 block - 0.00001192 BTC

23 - 24-11-2098 - 4830000 block - 0.00000596 BTC

24 - 29-10-2102 - 5040000 block - 0.00000298 BTC

25 - 02-10-2106 - 5250000 block - 0.00000149 BTC

26 - 05-09-2110 - 5460000 block - 0.00000075 BTC

27 - 09-08-2114 - 5670000 block - 0.00000037 BTC

28 - 13-07-2118 - 5880000 block - 0.00000019 BTC

29 - 16-06-2122 - 6090000 block - 0.00000009 BTC

30 - 20-05-2126 - 6300000 block - 0.00000005 BTC

31 - 23-04-2130 - 6510000 block - 0.00000002 BTC

32 - 27-03-2134 - 6720000 block - 0.00000001 BTC

Election Year GainsShows the yearly gains of the chart in U.S. Election years.

Use the options to turn on other years in the cycle.

For use with the 12M chart.

Will show non-sensical data with other intervals.

Gann Dates█ INTRODUCTION

This indicator is very easy to understand and simple to use. It indicates important Gann dates in the future based on pivots (highs and lows) or key dates from the past.

According to W.D. Gann the year can be seen as a cycle or one full circle with 365 degrees. The circle can be symmetrically divided into equal sections at angles of 30, 45, 60, etc. The start of the cycle can be a significant key date or a pivot in the chart. Hence there are dates in the calendar, that fall on important angles. According to W.D. Gann those are important dates to watch for significant price movement in either direction.

In combination with other tools, this indicator can help you to time the market and make better risk-on/off decisions.

█ HOW TO USE

ibb.co

You need to adjust the settings depending on the chart. The following parameters can be adjusted:

Gann angles: The script will plot dates that are distant from pivots by a multiple of this.

Gann dates per pivot: The amount of dates that will show.

Search window size for pivots: This is how the local highs and lows are detected in the chart. The smaller this number the more local highs and lows will show.

You also have the option to hide dates derived from lows/highs, or show dates based on two custom key dates.

█ EXAMPLES

The following chart shows the price of Gold in USD with multiples of 20 days from local pivots.

The following chart shows the price of Bitcoin in USD with multiples of 30 weeks from two custom dates (in this case the low in late 2018 and the low in late 2022).

BE-TrendLines & Price SentimentsOverview

The trendline is one of the most potent and flexible tools in trading. A rising trendline indicates an upward trend, a falling trendline indicates a downward trend, and a flat trendline indicates a range-bound bond market.

Breakouts, price bounces, and reversal / Retest tactics are all types of trades that may be made using a trendline. Additionally, stop-loss and profit-trailing orders can be based on trendlines as support and resistance levels, appropriately.

Technical Calculations for Trendlines & Price Sentiments:

Pivot points for a specified time frame and the Prevailing High/Low for the most recent bars are used to derive trendlines. While Pivot Points alert us to price movements, High/Low tells us where Bulls and Bears find a middle ground. This provides a remarkable set of conditions from which to extrapolate the efficacy of the Trendlines.

The term "price sensitivity" refers to how much a change in the price of a product causes consumers to alter their purchase habits. It's the relationship between price shifts and shifts in consumer demand. So, for example, if a 30% jump in the cost of a product leads to a 10% drop in purchases, we can conclude that the item has a price sensitivity of 0.33%.

Basis the above theoretical statement, If the underlying asset's price drops, the indicator shall compute data on the amount of volume being pumped (Inflow vs Outflow) into the market (if available), or the percentage by which the price has changed. This will be compared to the recent drop rate to see if the behavior has changed at the similar value zone and non similar value zone. similar calculation shall be done if the price of the underlying rises.

Traders may benefit from hearing about Trendlines in their "Story Telling" form, which we now present. To help you comprehend it better, candles are divided into three Sentiment groups based on their color. Colors: Green (with its shades), Silver, and Red (including its shades). Green signifies a Bullish Trend, Silver a neutral trend, and Red a Brearish Trend.

Bullish Trend

Bearish Trend

Neutral Trend

Sentiment Price Cycle in Trending Market: Green (Directional Bullish), Dark Green (Bullish Trend Loosing its Strength), Silver (Neutral Trend), Red (Directional Bearish), Dark Red (Bearish Trend Loosing its Strength)

Sentiment Price Cycle in RangeBound Market: Green (Over Brought), Silver (Neutral) & Red (Over Sold)

How to Initiate Trade when price is within TL:

Fake Break Out Trade:

BreakDown Trade:

BreakOut Trade:

Couple of Other Features in the Indicator:

Single Alerts = These are the alerts where in, as and when the Event happens Alerts shall the trigerred. like On BreakOut, BreakDown, TouchOf Up TrendLine, TouchOf DownTrendLine, Retest Of Up TrendLine, Retest of DownTrendLine.

Conditional Alerts = These are those type of Alerts where in you can combine 2 or 3 conditions to trigger an Alert. Like

Sample 1 - After Down TL is tested for 3 times, If BreakOut happens and the setiment turns Bullish within 5 Candles.

Sample 2 - After Up TL is tested for 2 times, If Price Bounces backUp from TL and the setiment turns Bullish within 5 Candles.

Similarly you can customize the combination of events for getting the alert.

DISCLAIMER: No sharing, copying, reselling, modifying, or any other forms of use are authorized for our documents, script / strategy, and the information published with them. This informational planning script / strategy is strictly for individual use and educational purposes only. This is not financial or investment advice. Investments are always made at your own risk and are based on your personal judgement. I am not responsible for any losses you may incur. Please invest wisely.

Happy to receive suggestions and feedback in order to improve the performance of the indicator better.

90cycle @joshuuu90 minute cycle is a concept about certain time windows of the day.

This indicator has two different options. One uses the 90 minute cycle times mentioned by traderdaye, the other uses the cls operational times split up into 90 minutes session.

e.g. we can often see a fake move happening in the 90 minute window between 2.30am and 4am ny time.

The indicator draws vertical lines at the start/end of each session and the user is able to only display certain sessions (asia, london, new york am and pm)

For the traderdayes option, the indicator also counts the windows from 1 to 4 and calls them q1,q2,q3,q4 (q-quarter)

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

Range Identifier*Re-upload as previous attempt was removed.

An attempt to create a half decent identifier of when the markets are ranging and in a state of choppiness and mean reversion - as opposed to in trending trade conditions.

It's super simple logic just working on some basic price action and market structure operating on higher time frames.

It uses the Donchian Channels but with hlc3 data as opposed to high/lows - and identifies periods in which the baseline is static, or when the channel upper & lower are contracting.

This combination identifies non trending price action with decreasing volatility, which tends to indicate a lot of upcoming chop and ranging/sideways action; especially when intraday trading and applied on the daily timeframe.

The filter increasing results in a decrease of areas identified as choppy by extending the required period of a sideways static basis, I've found values of 2 or 3 to be a nice sweetspot!

Overall should be pretty intuitive to use, when the background changes just consider altering your trading and investing approach. This was created as I've not really seen anything on here that functions quite the same.

I decided to not include the Donchian upper/lower/basis as I found that can often lead to decision bias and being influenced by where these lines are situated causing you to guess on future direction.

It's obviously never going to be perfect, but a nice and unbiased way to quickly check where we may be in a cycle; let me know if there are any issues/questions and please enjoy!

inverse_fisher_transform_adaptive_stochastic█ Description

The indicator is the implementation of inverse fisher transform an indicator transform of the adaptive stochastic (dominant cycle), as in the Cycle Analytics for Trader pg. 198 (John F. Ehlers). Indicator transformation in brief means reshaping the indicator to be more interpretable. The inverse fisher transform is achieved by compressing values near the extremes many extraneous and irrelevant wiggles are removed from the indicator, as cited.

█ Inverse Fisher Transform

input = 2*(adaptive_stoc - .5)

output = e(2*k*input) -1 / e(2*k*input) +1

█ Feature:

iFish i.e. output value

trigger i.e. previous 1 bar of iFish * 0.90

if iFish crosses above the trigger, consider a buy indicated with the green line

while, iFish crosses below the trigger, consider a sell indicate by the red line

in addition iFish needs to be greater than the previous iFish

timing marketIntraday time cycle . it is valid for nifty and banknifty .just add this on daily basis . ignore previous day data

4 Pack Scalping ToolThe 4 Squeeze Scalp tool is a tool that I have developed over the past few years. I was always fascinated by the fact that most people don’t know where price is heading. While Fibonacci and other linear type methods work it never gelled with me. I started by going deep into the fundamentals of momentum with an understanding that an object in motion heading in a particular direction tends to stay heading in that direction (until something derails it). Price, in my opinion, is no different.

Price can move up, down and sideways. And it moves in a wave, getting stronger over time until eventually pulling back and starting over again. In my mind, the compression of price and the relationship of that pressure to various lengths of time as well as RSI, ADX and DMI across these same time frames gives you a view on how the underlying price momentum is building up and releasing. For trading you want to be building a trade when pressure starts to build and you want to take profits when the wave starts to pull back and build for the next cycle.

Each dot represents a length of the momentum indicator and the line inside the oscillator is a weighted composite of the underlying momentum structure for each of the lengths selected. A trade follows the directional alignment of the line (red = down, yellow = neutral / chop, green = up) and the dots should be aligned from the bottom to the top (bright green = very bullish, dark green = neutral / bullish, dark red = neutral / bearish, bright red = very bearish). When the line and the dots are aligned you will have a high probability trade.

The backtest results below are based on 2 years of backtesting, using a 2 contract trade on a 100K account. While the absolute return is not meaningful the win rate and PF are great for a trade on CL on this timeframe. The tool can be used on any asset over any timeframe in a multitude of combinations.

To get access to the tool, please contact the author.

Moon Phases Strategy with CCI EXTRIME TPHELLO TO ALL ASTROLGY TRADING LOVERS

***im not a native english speaker and im not going to google translte it so soory for mastakes ****

this is an amzing script of moon cycle strategy

for long -

price need to be above MA

it will buy in full moon and will sell at new moon

i added an extrime CCI TP that if cci is over bought above 200 line it will close position- it cant be edited out so enjoy it.

for short-

price need to be below MA

it will short when new moon and buy back when fullmoon

i added an extrime CCI tp that if cci is oversold under -200 line it will close position - it cant be edited out so enjoy it.

just edit the new moon Reference date by your UTC TIME!!! ׂ( GOOGLE 'NEW MOON DATE')

לכל אוהבי האסטרולוגיה ומסחר בכוכבים

סקריפט פשוט מעולה!

ללונג- האסטרטגיה קונה כאשר המחיר מעל הממוצע ויש ירח מלא-היא מוכרת כאשר יש ירח חדש או כאשרס.ס.י חוצה את קו ה200

בשורט היא עושה ההפך ומוכרת כאשר יש ירח חדש והמחיר מתחת לממוצע-היא סוגרת את הפוזציה כאשר יש ירח מלא או כאשר ס.ס.י חוצה מטה את רמת המינוס 200

אנא ערכו את התאריך רפרנס לירח לפי אזור הזמן שלכם חפשו בגוגל ''תאריך ירח חדש'.

BACKTEST RETURNS SOOOOOO GOOOOD !

הבאק טסטים חוזרים מושלמים

trade with the stars and rip markets

BTC Pi MultipleThe Pi Multiple is a function of 350 and 111-day moving average. When both intersect and the 111-day MA crosses above, it has historically coincided with a cycle top with a 3-day margin.

With the Pi Multiple, this intersection is visible when the line crosses zero upwards.

The indicator is called the Pi Multiple because 350/111 is close to Pi. It is based on the Pi Cycle Top Indicator developed by Philip Swift and has been modified for better readability by David Bertho.

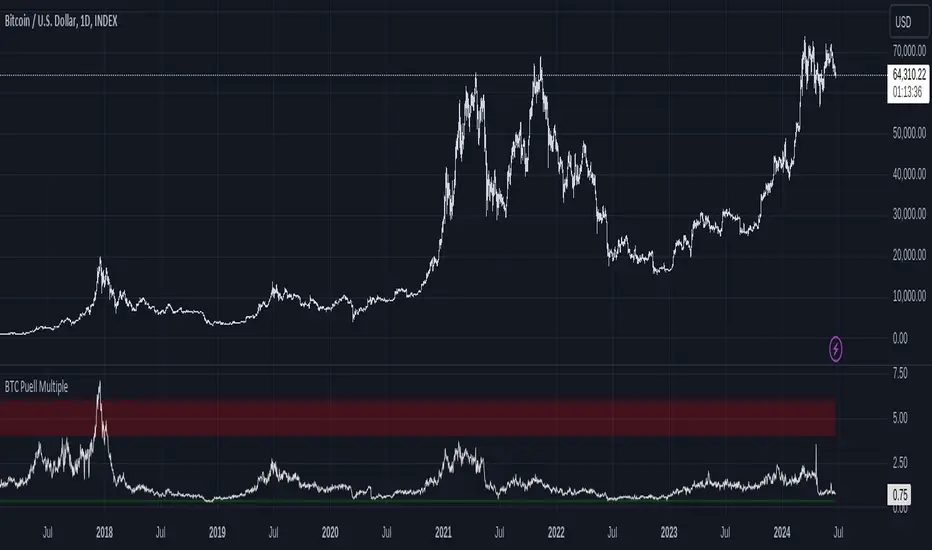

Bitcoin Fundamentals - Puell MultipleThis is an indicator that derives from Bitcoin Mining daily generated Income.

It does show a perfect track record on calling Bitcoin cycle tops and cycle bottoms.

For those of you willing to experiment, I've enabled the ability to set custom periods (365 by default).

The indicator includes custom alerts to notify the entry and the exit from OverBought (OB) & OverSold (OS) bands.

Credits: David Puell twitter.com

Cycle Dynamic Composite AverageThis MA uses the formula of simple cycle indicator to find 2 cycles periods length's .

The CDCA is the result of 8 different ma to control and filter the price. The regression line is the signal , don t need to look candles, but just the cross between MA and reg lin.

TASC 2025.06 Cybernetic Oscillator█ OVERVIEW

This script implements the Cybernetic Oscillator introduced by John F. Ehlers in his article "The Cybernetic Oscillator For More Flexibility, Making A Better Oscillator" from the June 2025 edition of the TASC Traders' Tips . It cascades two-pole highpass and lowpass filters, then scales the result by its root mean square (RMS) to create a flexible normalized oscillator that responds to a customizable frequency range for different trading styles.

█ CONCEPTS

Oscillators are indicators widely used by technical traders. These indicators swing above and below a center value, emphasizing cyclic movements within a frequency range. In his article, Ehlers explains that all oscillators share a common characteristic: their calculations involve computing differences . The reliance on differences is what causes these indicators to oscillate about a central point.

The difference between two data points in a series acts as a highpass filter — it allows high frequencies (short wavelengths) to pass through while significantly attenuating low frequencies (long wavelengths). Ehlers demonstrates that a simple difference calculation attenuates lower-frequency cycles at a rate of 6 dB per octave. However, the difference also significantly amplifies cycles near the shortest observable wavelength, making the result appear noisier than the original series. To mitigate the effects of noise in a differenced series, oscillators typically smooth the series with a lowpass filter, such as a moving average.

Ehlers highlights an underlying issue with smoothing differenced data to create oscillators. He postulates that market data statistically follows a pink spectrum , where the amplitudes of cyclic components in the data are approximately directly proportional to the underlying periods. Specifically, he suggests that cyclic amplitude increases by 6 dB per octave of wavelength.

Because some conventional oscillators, such as RSI, use differencing calculations that attenuate cycles by only 6 dB per octave, and market cycles increase in amplitude by 6 dB per octave, such calculations do not have a tangible net effect on larger wavelengths in the analyzed data. The influence of larger wavelengths can be especially problematic when using these oscillators for mean reversion or swing signals. For instance, an expected reversion to the mean might be erroneous because oscillator's mean might significantly deviate from its center over time.

To address the issues with conventional oscillator responses, Ehlers created a new indicator dubbed the Cybernetic Oscillator. It uses a simple combination of highpass and lowpass filters to emphasize a specific range of frequencies in the market data, then normalizes the result based on RMS. The process is as follows:

Apply a two-pole highpass filter to the data. This filter's critical period defines the longest wavelength in the oscillator's passband.

Apply a two-pole SuperSmoother (lowpass filter) to the highpass-filtered data. This filter's critical period defines the shortest wavelength in the passband.

Scale the resulting waveform by its RMS. If the filtered waveform follows a normal distribution, the scaled result represents amplitude in standard deviations.

The oscillator's two-pole filters attenuate cycles outside the desired frequency range by 12 dB per octave. This rate outweighs the apparent rate of amplitude increase for successively longer market cycles (6 dB per octave). Therefore, the Cybernetic Oscillator provides a more robust isolation of cyclic content than conventional oscillators. Best of all, traders can set the periods of the highpass and lowpass filters separately, enabling fine-tuning of the frequency range for different trading styles.

█ USAGE

The "Highpass period" input in the "Settings/Inputs" tab specifies the longest wavelength in the oscillator's passband, and the "Lowpass period" input defines the shortest wavelength. The oscillator becomes more responsive to rapid movements with a smaller lowpass period. Conversely, it becomes more sensitive to trends with a larger highpass period. Ehlers recommends setting the smallest period to a value above 8 to avoid aliasing. The highpass period must not be smaller than the lowpass period. Otherwise, it causes a runtime error.

The "RMS length" input determines the number of bars in the RMS calculation that the indicator uses to normalize the filtered result.

This indicator also features two distinct display styles, which users can toggle with the "Display style" input. With the "Trend" style enabled, the indicator plots the oscillator with one of two colors based on whether its value is above or below zero. With the "Threshold" style enabled, it plots the oscillator as a gray line and highlights overbought and oversold areas based on the user-specified threshold.

Below, we show two instances of the script with different settings on an equities chart. The first uses the "Threshold" style with default settings to pass cycles between 20 and 30 bars for mean reversion signals. The second uses a larger highpass period of 250 bars and the "Trend" style to visualize trends based on cycles spanning less than one year:

SETUP HMTR ZONESETUP HMTR ZONE

This indicator highlights high-probability market extremes by detecting a rare alignment between independent heatmap engines.

Captures volatility squeeze, trend exhaustion, and pressure asymmetry.

🎯 What the indicator does

🔵 Cold Match (Blue)

Appears when all engines detect cooling, fear, and liquidity contraction.

Often forms near accumulation phases, oversold washes, structural resets, discount zones.

🔴 Hot Match (Red)

Appears when all components show overheating, exhaustion, and aggressive pressure.

Often precedes distribution phases, liquidity grabs, blow-off tops, or trend fatigue.

✨ Why this matters

This tool does not give buy/sell entries.

It provides contextual confirmation of:

emerging accumulation or distribution

cooling or overheating phases

liquidity-driven stress points

behavioral extremes

regime shifts in trend structure

Use it as a market overlay layer, not as a standalone entry trigger.

🔔 Alerts Included

Cold zone

Hot zone

Signals fire only on confirmed candle close.

✔️ Best for traders who value:

risk-aware positioning

cycle and regime analysis

structural confirmation

heatmap-based market context

smart-money aligned behavior

Wyckoff PRO Institutional🔹 Wyckoff NTA – Institutional Context Engine

Institutional Market Context Based on Wyckoff Methodology

📌 Overview

Wyckoff NTA – Institutional Context Engine is a public, closed-source analytical script developed by NexTrade Academy, designed to identify and quantify the true institutional market context using classic Wyckoff methodology adapted into a modern algorithmic framework.

This script is NOT a signal system and does not provide precise entry or exit points.

Its purpose is to function as a context engine, helping traders understand WHEN the market is operable and IN WHICH DIRECTION it is statistically reasonable to look for opportunities.

🧠 Methodology & Conceptual Framework

Wyckoff NTA evaluates the combined behavior of price, volume, and volatility, following the core principles of the Wyckoff method to interpret institutional intent behind market movements.

The script analyzes market conditions through the following conceptual components:

1️⃣ Wyckoff Phase Identification

The indicator classifies the current market environment into the main institutional Wyckoff phases:

Accumulation

Distribution

Markup

Markdown

Reaccumulation

Redistribution

These phases describe where the market is within its cycle, not where to trade.

2️⃣ Institutional Intent Event Detection

Wyckoff NTA detects key events associated with Wyckoff methodology, such as:

Spring

Upthrust

Sign of Strength (SOS)

Sign of Weakness (SOW)

These events are treated as contextual confirmations, not standalone trade signals.

3️⃣ Market Operability Assessment

The script evaluates whether current conditions are operable or non-operable, based on the relationship between:

Structural development

Participation (volume behavior)

Price efficiency and volatility

This process filters out:

Low-intent environments

Transitional phases

Low-probability market conditions

🔢 Wyckoff Dynamic Score (0–100)

All evaluated components are aggregated into a Wyckoff Dynamic Score, which summarizes the quality of the current market context:

Below 40 → Non-operable context

40 to 60 → Weak context (A+ setups only)

60 to 80 → Operable context

Above 80 → Strong institutional context

This score does not trigger trades.

It is designed to enable or block decisions within a defined trading plan.

🎨 Visualization Modes

Wyckoff NTA includes multiple visualization modes to support different use cases:

DESK → Professional execution (minimal, no visual noise)

PRO → Active trading with enhanced visual context

EDU → Educational and learning-focused analysis

Each mode prioritizes clarity, objectivity, and controlled information density.

🎯 Intended Use

This script is designed for:

Institutional and advanced discretionary traders

Market Structure and Smart Money approaches

Swing and intraday trading

Contextual trade filtering and bias validation

Integration with execution systems such as NTC (NexTrade Concept)

It should always be used alongside:

A defined execution model

Proper risk management

Trading discipline

⚠️ Important Disclaimer

❌ No performance guarantees

❌ Not an automated trading system

❌ Does not constitute investment advice

✅ Contextual analytical tool only

All trading decisions remain the sole responsibility of the user.

🏷️ Credits

Developed by NexTrade Academy

Institutional Trading · Market Structure · Context First

Educational and professional analytical tool

Use at your own risk

Breakouts & Pullbacks [Trendoscope®]🎲 Breakouts & Pullbacks - All-Time High Breakout Analyzer

Probability-Based Post-Breakout Behavior Statistics | Real-Time Pullback & Runup Tracker

A professional-grade Pine Script v6 indicator designed specifically for analyzing the historical and real-time behavior of price after strong All-Time High (ATH) breakouts. It automatically detects significant ATH breakouts (with configurable minimum gap), measures the depth and duration of pullbacks, the speed of recovery, and the subsequent run-up strength — then turns all this data into easy-to-read statistical probabilities and percentile ranks.

Perfect for swing traders, breakout traders, and anyone who wants objective, data-driven insight into questions like:

“How deep do pullbacks usually get after a strong ATH breakout?”

“How many bars does it typically take to recover the breakout level?”

“What is the median run-up after recovery?”

“Where is the current pullback or run-up relative to historical ones?”

🎲 Core Concept & Methodology

Indicator is more suitable for indices or index ETFs that generally trade in all-time highs however subjected to regular pullbacks, recovery and runups.

For every qualified ATH breakout, the script identifies 4 distinct phases:

Breakout Point – The exact bar where price closes above the previous ATH after at least Minimum Gap bars.

Pullback Phase – From breakout candle high → lowest low before price recovers back above the breakout level.

Recovery Phase – From the pullback low → the bar where price first trades back above the original breakout price.

Post-Recovery Run-up Phase – From the recovery point → current price (or highest high achieved so far).

Each completed cycle is stored permanently and used to build a growing statistical database unique to the loaded chart and timeframe.

🎲 Visual Elements

Yellow polyline triangle connecting Previous ATH / Pullback point(start), New ATH Breakout point (end), Recovery point (lowest pullback price), and extends to recent ATH price.

Small green label at the pullback low showing detailed tooltip on hover with all measured values

Clean, color-coded statistics table in the top-right corner (visible only on the last bar)

Powerful Statistics Table – The Heart of the Indicator

The table constantly compares the current situation against all past qualified breakouts and shows details about pullbacks, and runups that help us calculate the probability of next pullback, recovery or runup.

🎲 Settings & Inputs

Minimum Gap

The minimum number of bars that must pass between breaking a new ATH and the previous one.

Higher values = stricter filter → only the strongest, cleanest breakouts are counted.

Lower values = more data points (useful on lower timeframes or very trending instruments).

Recommendation:

Daily charts: 30–50

4H charts: 40–80

1H charts: 100–200

🎲 How to Use It in Practice

This indicator helps investors to understand when to be bullish, bearish or cautious and anticipate regular pullbacks, recovery of markets using quantitative methods.

The indicator does not generate buy/sell signals. However, helps traders set expectations and anticipate market movements based on past behavior.

BK10 BTC Regime v10.3BK10 BTC Regime v10.3 – Cycle, Risk, and Euphoria Map

BK10 v10.3 is a regime map designed to show at a glance where the market is: from CRASH/STRESS to EUPHORIA. It combines trend (50/200 EMA), momentum (RSI), and optionally, macro context (SPX + VIX) to classify each candlestick into 6 states:

CRASH · RISK-OFF · NEUTRAL · ACCUMULATION · RISK-ON · EUPHORIA

The indicator colors the background according to the regime.