SPX weekly bull put spread.75 limit filled.

Spread is below the 100/200 sma on the 15min. Trend is bullish. I expect all time high pull backs to be bought. I can also buy to close this before expiration.

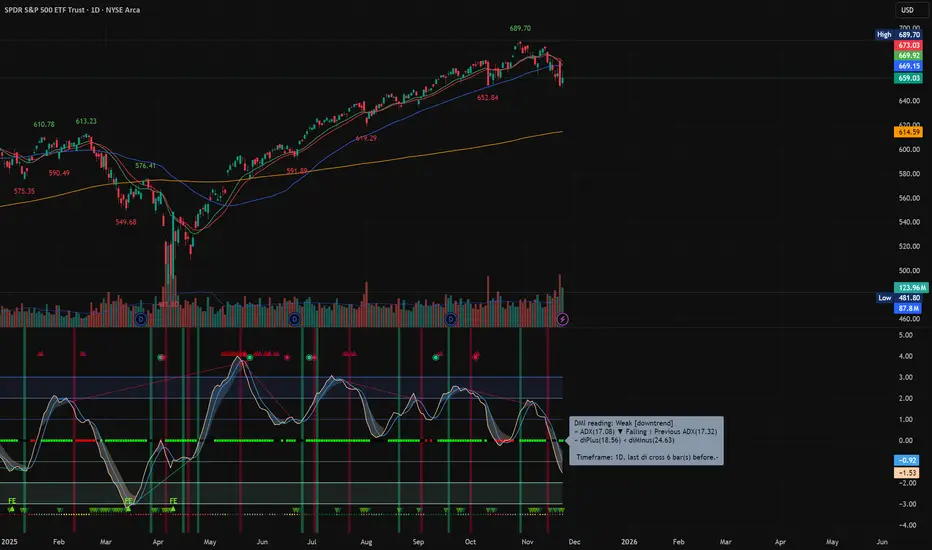

Bullputspread

SPX 2 day spreadBull put spread

6715 / 6710

$1.25 credit

A BUNCH of support levels here. And 3 selling days in a row...

3 Option Strategies✅ 1. 0-DTE Iron Fly (ATM Iron Butterfly)

The 0-DTE Iron Fly — selling an at-the-money straddle and buying wings for protection — is the most powerful theta-harvesting strategy in same-day options trading. Its core edge derives from the extraordinary rate of time decay at the money. ATM options experience the fastest gamma and theta changes, and within hours of expiration, their value collapses dramatically if price remains relatively stable.

An iron fly sells both the ATM call and ATM put, while purchasing further OTM wings to cap risk. This creates a defined-risk straddle, turning unlimited risk into a predictable maximum loss. Because you are collecting the highest premium on the chain (the ATM options), this strategy often yields 3–20× more credit than bull put spreads.

Professionals use iron flies on days where the market is expected to consolidate, remain rangebound, or collapse in implied volatility. The setup excels after large overnight moves, strong gap opens, or major news the previous day. These conditions often produce morning chop followed by volatility compression — the exact environment that crushes ATM premiums.

Key Greek behavior defines this strategy’s edge. The position is delta-neutral, vega-negative, and theta-maximizing. A neutral delta means you’re not betting directionally — any sideways action generates rapid profit. The negative vega means falling IV immediately boosts your P&L, and the extraordinarily high theta means the position decays in your favor every minute, especially after 11 AM ET.

However, gamma is the double-edged sword. ATM options have the highest gamma, meaning price moving too far too fast can rapidly eat into the credit and even create maximum loss conditions. For this reason, institutional traders manage iron flies aggressively using time-based exits, gamma stops, and dynamic hedging using micro futures (MES, ES, or SPX futures). They often hedge intraday with small futures positions to flatten delta.

A well-built iron fly has wings positioned at 15–30 delta, balancing risk and credit. The payoff is largest when price finishes near the ATM strike. Closing early—especially when you’ve captured 40–70% of the total credit—is standard practice. The trade is almost always exited before 2:00 PM ET to avoid the “gamma death zone,” where even minor price moves cause large swings.

Iron flies are best for traders with mechanical discipline, strong understanding of intraday volatility patterns, and the ability to manage delta quickly. When executed correctly in calm or mean-reverting markets, the iron fly is the most profitable theta-capture strategy in the entire 0-DTE universe.

Why it’s the best?

Highest theta concentration (ATM options decay the fastest).

Very tight structure → excellent gamma control.

Collects huge premium → offsets intraday noise.

You can define risk precisely.

When to use?

Low–moderate volatility mornings

Rangebound price action

Strong liquidity in SPX, narrow bid–ask

Typical setup:

Sell ATM call + ATM put

Buy wings ±15–30 points

Hold 1–2 hours, manage delta

Stats:

Win rate often 60–75%

Avg R:R 1:0.6 to 1:0.8

Excellent for consistency

✅ 2. 0-DTE Bull Put Spread (BPS)

The Bull Put Spread is the highest-probability and most stable 0-DTE income strategy used by SPX and XSP premium sellers. It involves selling a put that is out of the money and simultaneously buying another put further OTM to define risk. Its primary advantage lies in its exposure to positive theta, negative vega, and controlled gamma, making it ideal for days with orderly price action or bullish-to-neutral drift.

The core principle behind the bull put spread is simple: markets typically spend more time drifting upward or sideways than collapsing. 0-DTE options lose value extremely fast, particularly out-of-the-money options. By selling a 22–26 delta put and buying a 15–17 delta put, you position yourself in the zone where time decay works aggressively in your favor, and where IV crush after the open exponentially increases your probability of profit.

Professional traders rely on several metrics to select the correct strikes. First, the delta ratio between the short and long legs should be between 1.45–1.70. This ensures you're collecting enough premium for the risk while keeping gamma manageable. Next, the short-leg gamma must remain below threshold (0.045 for XSP, 0.015 for SPX), preventing sudden P&L swings late in the session. You also want net vega negative, so falling implied volatility benefits your trade, and net theta positive, so time decay improves your position.

Volume profile, expected move, skew, and opening volatility conditions guide entry timing. The best window tends to be 9:50–10:20 AM ET, after the initial volatility shock has normalized. Avoid entering during major macro events (CPI, FOMC, NFP), as volatility expansion can instantly destroy the probability structure.

You profit if price stays above your short put strike at expiration. Even if price moves downward slightly, the speed of decay can still allow you to win. Risk is strictly defined by the width of the spread, typically 3–5 points in XSP and 30–50 points in SPX. This creates a predictable maximum loss and controlled exposure.

Profit-taking is straightforward: close the spread when it's worth 5 cents or less, or when you’ve captured 70–90% of max profit. Stop out if the spread doubles in value relative to your credit (e.g., enter for $0.30, stop at $0.60). Always exit entirely by 3:32 PM ET to avoid gamma slingshot behavior.

Overall, the bull put spread is the most consistent 0-DTE strategy, with typical win rates between 75–90%, depending on strike selection. It is ideal for traders looking for systematic, repeatable edge without needing to predict market direction — only that markets won’t collapse that day.

Why it works?

Markets drift upward intraday statistically.

Keeps positive theta + directional bias.

When to use?

ES/NQ bullish open

SPX trending strong

VIX < 17

Breadth strong (AD line positive)

Typical setup:

Short put at 5–15 delta

Long put 20–30 points lower

Risk-defined, easy to automate

Stats:

Win rate 80–90% in bullish days

Low stress

Great for small accounts

✅ 3. 0-DTE Broken Wing Butterfly (BWB)

The Broken Wing Butterfly is the most advanced and nuanced 0-DTE strategy, offering asymmetric risk, low cost, and powerful edge during high-volatility or directional days. A BWB is essentially a skewed iron fly or skewed butterfly where one wing is placed further away, creating a structure with higher reward than risk or even a no-debit or credit-based butterfly.

A typical bullish BWB sells two ATM or slightly OTM puts, buys a closer lower put, and buys a further lower put several strikes away. This creates a payoff profile where the middle strike yields the highest profit, but losing scenarios are heavily controlled. The beauty of the BWB is that you can collect credit while still having a buffer zone and minimizing tail risk.

Unlike the bull put spread or iron fly, the broken wing butterfly shines in volatile markets. It's designed to handle one-directional moves, strong intraday drops, or large opens. When skew is elevated — especially put skew — the far-out wing becomes cheap, allowing you to build the structure for little or no cost. This skew is what gives BWBs institutional appeal: they exploit uneven pricing in the options chain created by market fear.

Key features include moderate gamma, moderate theta, and mildly negative vega. Although not as theta-rich as iron flies or as high-probability as bull put spreads, BWBs offer something neither of those provide: asymmetric opportunity. You risk less than you can make, while still benefiting from IV crush and directional drift.

Professionals place BWBs based on expected move, skew, and opening momentum. A bullish BWB is ideal when price is expected to drift upward or when volatility is high enough that selling ATM premium is too dangerous. It provides better tail risk management than credit spreads and avoids the unlimited risk of naked options.

Management rules revolve around maintaining delta, controlling gamma, and monitoring whether price migrates toward the tent peak. Traders often take profits early if price stalls near the short strike or begins to threaten the near wing. If price collapses rapidly, a BWB tends to hold up far better than a credit spread, because the long wing absorbs much of the gamma and Vega shock.

The BWB becomes exceptionally powerful when structured for zero debit, creating a free “lottery ticket” with hedged downside. Many traders use multiples—layering BWBs at different levels—to build a volatility-weighted directional profile.

In high volatility, trending, or one-directional markets, the broken wing butterfly is the best risk-adjusted strategy, offering safety, optionality, and strong skew exploitation.

Why this is sleeper-OP?

Collects more credit than risk (asymmetry).

Handles violent intraday moves better than iron fly.

Still benefits from fast theta burn.

When to use?

VIX severe > 20

ES/NQ whipsaw

FOMC days, CPI, NFP

Big macro catalyst days

Typical setup:

Sell ATM short strikes

One wing close

One wing far out

Net credit > max loss

Stats:

Win rate 50–70%

Best for tail-risk adjusted returns.

⭐ Which one is best overall?

If you want consistency:

→ 0-DTE Iron Fly

If you want safest risk-defined trending play:

→ 0-DTE Bull Put Spread

If you want best payout on volatile days:

→ 0-DTE Broken Wing Butterfly

QQQ bull put spreadIf AMZN or AAPL gap down, with both being bear candles today, I believe they would fade.

SAME for the QQQ. REALLY nice move down, but the 100 sma will be a small support and I think NASDAQ:AMZN & NASDAQ:AAPL will have "good earnings". IF AAPL OR AMZN Gap up (and they could) they would both be REALLY solid gaps...

OXY bull put spread AGAINOXY is at the 100 sma on M if you turn on the dividends. IT is RIGHT on top of the 200 sma on the weekly non adjusted dividends. $48 is a NEW low and getting 12% return on risk on a down day is nice...

I will allow this stock to go below $47 before I panic. I would expect a retest anyway, so I'll hold this spread until expiration or until I can close it for .03+ like the last one...

Bull put spread on OXYI think OIL can press higher with the 'port strike'. I also think OVERALL markets need a small pull back and that should press oil higher. AND, this stock has TONS of really nice support here....

amzn bull put spreadI LOVE The selling. AND THIS IDEA is over earnings. I DO PLAN on it being a slightly volatile spread, but with any buying or resting, theta should take over and the 200 SMA will slowly creep up.

This has MANY check marks and should work nicely

Nine Spot ETFs Plunge ETH Prices. Will ETH Tank Further?The SEC approved the listing of nine spot ETH ETFs on 23/July. The launch of these ETFs was expected to drive capital flows with spot buying. But it didn’t. ETH prices plunged by 9% over the following two days. Crucially, the decline in the ETH/BTC ratio was a similar 9% as BTC remained resilient.

Following what appears to be a sell-the-news event, the outlook for ETH remains mixed as GETH outflows are more than offsetting inflows to the other ETFs.

The sharp price decline offers a buying opportunity. Take caution as the risk of further decline persists. Implied Volatility (IV) on puts increased while IV on call declined after spot ETF approvals.

ETH ETF APPROVAL ACCOMPANIED BY PRICE DECLINE

The SEC provided final approval for eight spot ETH ETFs to trade while also allowing the conversion of the ETHE trust to a spot ETF, making it nine spot ETH ETFs in total.

Source: Farside

ETH prices dropped by 1.3% on launch day clearly marking a "sell the news" event. ETH plunged nearly 9% over the next two days, returning to its 20/May levels. This earlier date in May marked the onset of rumors about the SEC's likely approval as covered previously .

Crucially, the ETH/BTC ratio also declined, highlighting the specific negative impact on ETH distinct from the broader crypto market.

OUTFLOWS FROM GRAYSCALE ETHEREUM TRUST DOMINATE NET ETF FLOWS

ETH prices were pressured down by massive net outflows led by fund movement out from Grayscale Ethereum Trust (ETHE) chiefly due to steep expense ratio. These outflows far outpaced the inflows to other ETFs.

Source: Farside

Grayscale offers a lower cost alternative in the mini ETH ETF (ETH), inflows into it are small and inadequate to stem the outflow from the much larger ETHE.

Launch of Spot BTC ETFs caused outflows from Grayscale Bitcoin Trust ETF (GBTC). Investors then switched over to lower cost ETFs. This time though, the net effect on ETH ETFs has been much more negative.

Crucially, outflows from GBTC continued for almost four months after spot ETF launch. ETHE outflows could also continue for a considerable period, dominating net flows in spot ETH ETFs for the foreseeable future.

CALL IV HAS DECLINED FOLLOWING ETF LAUNCH

IV skew for 25-delta options showed that calls were far more expensive than puts. This reversed sharply after the ETF launch on 24/July, making puts expensive relative to calls, signaling rising fears of pain for ETH prices in the near term.

Source: CME QuikVol

Though ATM IV has dipped somewhat following approval, it still remains elevated from last month.

Source: CME QuikVol

HYPOTHETICAL TRADE SETUP

ETH ETF launch has been a stark sell-the-news event. Prices have reversed gains. While spot buying may drive positive price action, recent flow analysis from ETH ETFs shows outflows from ETHE dominating.

Like GBTC, this trend could continue for many months, with inflows to other ETFs muted, the net effect may be higher selling pressure in the coming weeks.

Still, ETH prices have corrected sharply. It trades 12.5% higher from a major YTD support level and above the 200-day moving average. Consequently, ETH prices are unlikely to trend much lower from current levels. Breakout to the upside also remains unlikely in the near-term given the lack of major news flow.

A bullish put spread is an astute trade set up to harvest elevated put IVs amid a narrow trading range. A bullish put spread consists of a short put at a higher strike combined with a long put at a lower strike.

This position benefits from the net credit earned from the short put position net off the premium paid for the long put. Long put provides the crucial downside risk protection while also reducing the margin required.

The proposed hypothetical trade set up comprises of short 3100 put combined with a long 3000 put on CME Micro Ether Options expiring in August.

While the position offers a fixed upside and downside, it is crucial to note that the maximum loss for this position (USD -6.5) is higher than the maximum profit (USD 3.5). As such, the position would lose money in case the present downturn in ETH prices continues.

MARKET DATA

CME Real-time Market Data helps identify trading set-ups and express market views better. If you have futures in your trading portfolio, you can check out on CME Group data plans available that suit your trading needs www.tradingview.com

DISCLAIMER

This case study is for educational purposes only and does not constitute investment recommendations or advice. Nor are they used to promote any specific products, or services.

Trading or investment ideas cited here are for illustration only, as an integral part of a case study to demonstrate the fundamental concepts in risk management or trading under the market scenarios being discussed. Please read the FULL DISCLAIMER the link to which is provided in our profile description.

LULU bull put spreadsell to open the $320

Buy to open the $310

$1.00 limit

Which is 20% roi

I'll be watching this one if it closes below $330 (I'll begin shorting shares there or day trading to protect my downside)

NVDA bull put spread over earningsTaking advantage of volatility.

Buy low, sell high.

I think NVDA either gaps up small, or opens flat.

And we are able to capture the volatility suck. EVEN if NVDA does gap down, trend is SOOO STRONG, people will buy it up eventually.

Bull put spread on AMZN for OctoberI got 9 check marks on this one.

.65 limit credit on the 120/115 bull put spread.

This is regular october expiration.

I love it

Bull Put Spread su GSFollowing the Earnings dip, we open a contrarian options defined-risk trade in order to exploit the spike in IV

MGM bull put spreadIF this trade does not work, one Real life trader will get a weekend at the MGM on me

;-)

AVGO bull put spreadBelow the 200 SMA on daily. AVGO has had pretty decent strength for a bit. Not expecting it to TANK in 2 weeks.

AMD bull put spreadGood premium. 2 1/2 weeks. Let's see if THETA helps us OR if any bulls come into AMD to cause this bad boy to bounce. Protection level will happen with a close below the 100 SMA.

NVAX next weekly support with low rsi

what a perfect gap down with low rsi. I am buying extra time for this to work for us. I am loving the low rsi and this gap down on it today.

Tesla Back Testing H&S Break OutHoping to see a bounce off this previous break out of the Head and Shoulder pattern. As long as we close above $700 this week, I think earnings on Monday will bring Tesla back above $800 level.

FUD spreading by the media of Tesla's autopilot killing 2 people in their vehicle, experience traders should see this as a buying opportunity. I have bought several more shares for my long term holding plus I still have my $660/$655 Friday Expiry Bull Put spread opened and its printing a nice profit. I did close out my next weeks spread for a loss as a precaution in case $700 support does not hold. I will reopen again once we show signs of a bounce off support.

Tesla Bounces Off .5 FibAfter a solid 3 day run on Tesla, looks like we are seeing a healthy retracement and bounce off the .5 Fibonacci level.

To me it appears to be a good opportunity to enter in a bull put credit spreads for Friday or next week expiration starting at $690 level. It would get risky if it would break lower then $712 during tomorrows trading session or a close below that but I am pretty confident we will hold above $712 as we have been rejected on this level couple times over the last 2 months so it should be a good support level. I would exit the trade if it does go below that and take my loses as there would be further downside if $712ish support does not hold.

Bull Put Spread on Reliance BreakoutBull Put Spread

-1x 28JAN2021 2150PE - ₹ 135.45

+1x 28JAN2021 2050PE - ₹ 64.1

Max. Profit ₹ +17,838

Max. Loss ₹ -7,162

ES Futures - Strong Breakout Momentum Play to the UpsideES Futures - Strong Breakout Momentum Play to the Upside

How to participate from bull put spreadI want to show you, how you can participate with fix risk from option strategys comparing to chart analysis:

This bullish strategy can use with stocks that have potential breakout chance, or either long-term potential.

In this example of TTD use BB and SMA 50 for support (buying short put) and resistance for selling long put. We think that TTD wont go below 700 and have momentum to break through 820:

Trades to open position No. Price Total

sell 5th Feb $820.00 Put 1x100 $60.75 $6075.00

buy 5th Feb $700.00 Put 1x100 $12.70 $-1270.00

------------------------------------------------------------------------

Total $4805.00

Take care of time of expiration date. In this scenario we used 5th feb with total return of 4805 and total risk of 7195.

So, I hope you can follow my thoughts. Comments are welcome.