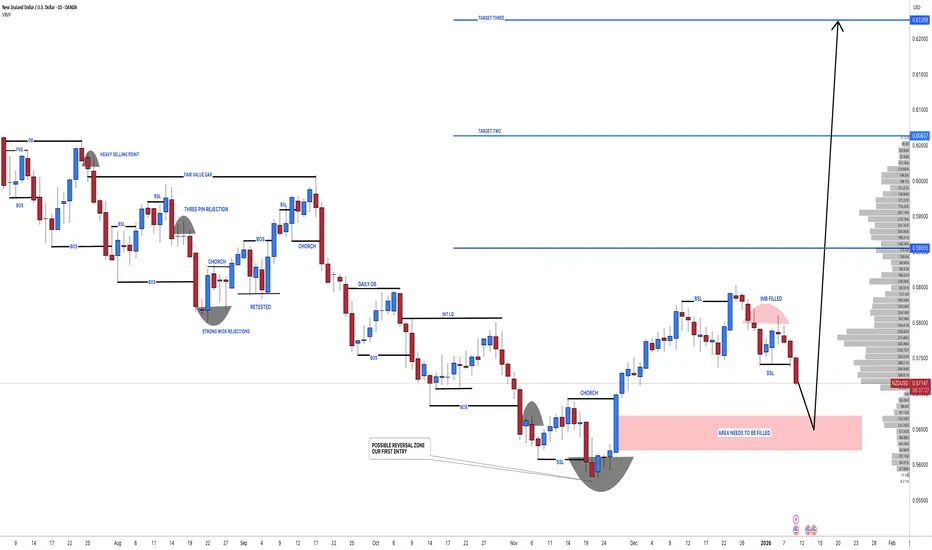

NZDUSD: Latest Chart Analysis 07/01/2026 🔺As per our previous analysis, the price was expected to maintain a bullish trend until all our targets were met. However, we have observed a shift in price behavior, and the price has now reversed, initiating a bearish trend. This presents a favorable opportunity for us, as the price decline is attributed to a previously unaddressed liquidity void.

🔺The entry zone has been clearly indicated by a red box labeled "area needs to be filled." Given the current strong bearish momentum, our entry is anticipated to become active by Monday. Once the entry is activated, the stop loss can be positioned below the designated entry zone.

🔺We have identified three target points that we believe are likely to be achieved within the next couple of months. Kindly utilize this analysis for educational purposes exclusively, and we recommend setting your take-profit levels based on your own informed judgment.

🔺If you appreciate our efforts, please consider liking and commenting for more analyses of these type.

Team SetupsFX❤️🏆

Growth

District Metals - Bullish outlook for the Uranium StockDistrict Metals (DMX): A Sweden-Focused Metals Story With a Regulatory Catalyst

District Metals is a Canada-listed exploration and development company with a strong focus on Sweden. The company is positioned around two key themes: polymetallic base and precious metals in historically productive mining districts, and long-dated optionality tied to energy and critical metals.

One of the company’s core assets is the Tomtebo project in the Bergslagen mining district. Bergslagen is one of Europe’s most established mining regions, with centuries of documented production across copper, zinc, lead, silver and gold. Tomtebo hosts multiple historical mines and polymetallic showings distributed along a large structural trend. The investment case here is straightforward: modern exploration techniques applied to an old mining district that was never explored with today’s geophysics, structural modeling, or systematic drilling. Value creation is driven by data — drilling results, geological continuity and scale — not narratives.

The second leg of the story, and the one attracting increasing attention, is Viken. This project hosts uranium alongside other metals such as vanadium, molybdenum, nickel, copper and zinc. For years, the economic potential of Viken has been structurally capped by Swedish legislation, as uranium extraction was effectively prohibited. That regulatory ceiling mattered — regardless of geology, uranium could not be part of any mine plan.

That is now changing.

Sweden has formally decided to reverse its long-standing uranium ban. The Swedish parliament has approved amendments to the Minerals Act and the Environmental Code that allow uranium to be classified as a concession mineral, meaning it can legally be explored for and extracted under the standard permitting framework. These changes are scheduled to come into force on 1 January 2026.

This is a material shift. It removes a hard legal stop that has existed for decades. For projects like Viken, uranium can once again be considered as part of the economic equation rather than being ignored entirely. That said, this is not a shortcut to production. Permitting, environmental assessments, technical studies, social acceptance and economics still apply. The law change does not eliminate risk — it eliminates prohibition.

From a market perspective, District Metals sits at the intersection of three forces: drill-driven exploration upside at Tomtebo, regulatory re-rating potential tied to uranium in Sweden, and a broader European push for domestic supply of critical raw materials. This is inherently high-risk territory, but that is where optionality and asymmetric outcomes live.

Execution, not sentiment, will decide the outcome.

Disclaimer: This post is not financial advice and should not be considered a recommendation to buy or sell any security. Always do your own research before making investment decisions.

SOBHASobha Ltd. (CMP ₹1,570.10, +2.68%), headquartered in Bengaluru, is one of India’s most respected real estate developers. Founded in 1995 by P.N.C. Menon, Sobha is unique as India’s only backward-integrated real estate company, handling design, engineering, and construction in-house. The company has a strong presence in residential, commercial, and contractual projects, with operations across Bengaluru, Gurugram, Pune, Thrissur, Coimbatore, Chennai, and other cities.

FY22–FY25 Snapshot

Sales – ₹2,766 Cr → ₹3,310 Cr → ₹3,097 Cr → ₹4,039 Cr

Net Profit – ₹116.9 Cr → ₹104.2 Cr → ₹49.1 Cr → ₹94.7 Cr

Operating Performance – Strong → Moderate → Weak → Improving

Dividend Yield – 0.9% → 1.0% → 1.1% → 1.2%

Equity Capital – ₹95 Cr (constant)

Total Debt – ₹2,800 Cr → ₹2,600 Cr → ₹2,400 Cr → ₹2,200 Cr

Fixed Assets – ₹7,800 Cr → ₹8,200 Cr → ₹8,500 Cr → ₹9,000 Cr

EPS – ₹12.3 → ₹11.0 → ₹5.2 → ₹8.9

Sources: Sobha Investor Relations, Kotak Securities Financials, ET Money Financials

Institutional Interest & Ownership Trends

Promoter holding is ~52%, reflecting strong founder-led governance. FIIs and DIIs have shown steady interest, particularly in Sobha’s premium residential projects. Public float is ~48%, with delivery volumes reflecting long-term positioning by real estate-focused funds.

Strategic Moves & Innovations

Sobha has focused on luxury residential projects in Bengaluru and Gurugram, while expanding into Pune and Chennai. Its backward integration model ensures quality control and cost efficiency. The company is also investing in green buildings, sustainability certifications, and premium township developments.

Cash Flow & Balance Sheet Strength

Operating cash flows remain stable, supported by strong residential sales. Free cash flow is positive, though capex intensity remains high due to expansion. Debt levels are gradually declining, reflecting disciplined capital allocation. The balance sheet remains strong with promoter backing and diversified asset base.

Risk Factors

Key risks include cyclical demand in real estate, regulatory changes (RERA, GST), and competitive intensity from larger pan-India developers. Margin pressures may arise from high input costs and slower absorption in premium projects.

Investor Takeaway

Sobha Ltd. demonstrates solid fundamentals with improving profitability, strong brand equity, and a unique backward integration model. While debt levels remain elevated, its focus on premium residential projects and disciplined execution make it a long-term player in India’s real estate sector.

Why Sector Rotation Favors Booz Allen Hamilton (BAH) Over TechI have been watching the Chart for Booz Allen for the past several months, and now that I have received my Technical confirmation, my Fundamental thesis is matching what I am expecting to occur.

As the stock had their Blow off top in October, the RSI was already showing a massive Divergence with the weakening RSI and high prices.

Price 122 RSI 77

Price 147 RSI 73

Price 189 RSI 72

With the continuing downtrend, I was waiting for the large correction for the price to retest the 100 levels, but where it stands now, we have received our bullish signal.

RSI Divergence is now starting to push to the Upside, with RSI making higher lows, while price action on Lower Lows Occurred from February 2025 to November 2025. WIth this confirmation I have decided to Trim my Tech Positions and take those profits into an already destroyed Stock.

As the technology sector faces heightening "AI bubble" concerns and stretched valuations, a significant opportunity has emerged in Booz Allen Hamilton (BAH). While Alphabet (GOOGL) and Amazon (AMZN) remain fundamentally sound, their current multiples offer a diminishing margin of safety. Conversely, a temporary guidance reset at Booz Allen has created a classic "value-gap" opportunity, offering a defensive "moat" with superior asymmetrical upside over a 3-to-5-year horizon.

I. The Case for Booz Allen Hamilton: The Undervalued "Tech-Defense" Hybrid

1. Market Positioning and Moat

Booz Allen operates with a unique stability moat, deriving nearly all revenue from U.S. Federal Government contracts.

Defense & Intelligence (75% of Revenue): These segments represent the high-margin core, currently growing at ~19% as the company transitions from traditional labor-based consulting to tech-enabled solutions (AI and Cyber).

Margin Expansion: This strategic pivot has seen Net Margins double over the last decade, expanding from 4% to approximately 8%.

2. The Guidance "Reset" Opportunity

Recent revisions to FY26 guidance—citing procurement delays in the Civil sector—have led to a sharp contraction in the share price. However, fundamental indicators remain robust:

Valuation: BAH currently trades at a 13.0x P/E ratio, its lowest level since 2016 and significantly below its 10-year historical peak of 22x.

Insider Conviction: In October 2025, CEO Horacio Rozanski purchased approximately $2.01M in shares on the open market—a powerful bullish signal during a period of market skepticism.

3. Projected 2029 Valuation Framework

Applying a conservative 9% CAGR to Net Income and factoring in the company’s aggressive $500M share buyback program, we project a 2029 EPS of $8.77 – $10.00.

Bear Case (13x P/E): Price target of $130.

Bull Case (21x P/E Mean Reversion): Price target of $190 - $235, representing an upside of 105% - 154%.

Chipotle Mexican Grill | CMG | Long at $30.56Chipotle NYSE:CMG stock has dropped dramatically since 2024, but the company has been *highly* overvalued for many, many years (69x p/e in June last year). As of Friday, November 7, 2025, the stock price entered my "crash" simple moving average zone (green lines). I do not suspect this is truly bottom, though. The company's growth is likely to slow into 2026 as people continue to spend less, and the stock finally starts to enter a reasonable p/e value (currently 27x). I anticipate further entry possibilities near $25 in the short-term if the economy continues to show more and more weakness. Entry into the "major crash" simple moving average zone, or gray lines, near $20-$24 isn't out of the question either. Thus, a personal entry at $30.56 is simply a starter position.

Growth

Earnings per share anticipated to rise from $1.60 in 2025 to $1.82 by 2028.

Revenue expected to rise during that time from $11.9 billion to $16.6 billion.

www.tradingview.com

Health

Extremely healthy, financially

Altman's Z Score / Bankruptcy risk: 7.5 (very low risk)

Quick Ratio: 1.5 (low debt)

Action

While there is risk of continued near-term pain for NYSE:CMG , the longer outlook is reassuring if true. Thus, at $30.56, Chiptole is in a personal buy zone (starter position) with risk of a continued drop to $25 or, "major crash" territory in the low $20s. These will be other personal entry points.

Targets into 2028

$35.00 (+14.5%)

$39.00 (+27.6%)

Uber’s "Hybrid" Pivot: Why Robotaxi Threat is Now an OpportunityTime Horizon: Long-term, Bias: Bullish (Long)

The "Big Picture" (Summary) For years, the biggest fear for Uber investors was that autonomous vehicles (like Tesla or Waymo) would make the company obsolete. However, the newly confirmed partnership with Lucid and Nuro changes the story completely. Instead of being a victim of the robotaxi revolution, Uber is effectively "hedging" its future by securing its own fleet of 20,000 autonomous Lucid vehicles. This pivot transforms Uber from a simple marketplace into a resilient "Hybrid Network," making the current share price a compelling value for long-term holders.

The Analysis:

The Trend Uber is currently trading in a consolidation phase (moving sideways) in the low $80s after dropping about 20% from its 52-week highs. While the stock has been stuck due to fears about the future of driving, the actual business is accelerating—total trips grew 22% last year, faster than in previous quarters. The trend remains upward in the long term, but the stock is currently taking a breather.

Key Price Areas:

"Cheap" (Support): $75 – $80. This area has established itself as a "floor" where buyers step in. The recent news of on-road testing starting in San Francisco has reinforced this support level.

"Expensive" (Resistance): ~$102. This is the previous high. If the price breaks above this, it signals that the market has fully accepted Uber's new strategy.

The Catalyst The game-changer is the CES 2026 announcement of the Uber-Lucid-Nuro alliance. This isn't just a promise; Uber has invested $300 million and committed to deploying 20,000 vehicles. This proves Uber has a "Plan B" if other partners (like Waymo) try to squeeze them out. It removes the "existential risk" that has been holding the stock price down.

Investment Plan:

Buy Zone: $78.00 – $82.00 - Accumulating shares in this range allows you to enter while the market is still skeptical, offering a favorable entry point before the broader market reprices the stock.

Risk Level (Invalidation): Close below $65.00 - If the price drops below $65, our thesis is likely wrong. This would suggest the "Bear Case" is unfolding—where autonomous tech fails to scale or competitors like Tesla successfully cut Uber out of the market.

Target: $112.00 - We are targeting a move to $112, which represents roughly 37% upside from current levels. This valuation reflects Uber's successful shift to a "Hybrid Network" and its continued dominance as a "Super App."

Disclaimer: This content is for educational purposes only and does not constitute financial advice. All investments carry risk. Please do your own due diligence before making any investment decisions.

Sprouts Farmers Market (SFM): Why The Market Is Wrong About ThisTime Horizon: Long-term (Years), Bias: Long

The "Big Picture" (Summary) Sprouts Farmers Market (SFM) is currently trading at a price that suggests its growth is over, but the financial data tells a completely different story. While the market worries that 2025 was a "one-off" peak, the company's underlying business has fundamentally improved with wider margins and higher returns on capital. This creates a rare opportunity to buy a high-growth retailer at a value-stock price.

Analysis:

The Trend: While the stock price reflects skepticism, the company's performance is dominant. Revenue is expected to grow +14% (compared to the industry average of +3%), and profit margins have hit new highs.

Key Price Areas: The stock is currently "cheap" at $79.31. It is trading at a Price-to-Earnings (P/E) ratio of roughly 15x, while similar growth retailers trade at 25x. This is a 40% discount to its peers.

The Catalyst: The market believes profit margins will collapse, but this view is flawed because the improvements are driven by permanent changes, such as smaller, more efficient store formats. Future catalysts include continued earnings beats and the potential for the company to aggressively buy back its own shares using its $322M cash pile.

Investment Plan:

Buy Zone: $79.00 - $80.00 - At the current price of $79.31, the stock offers a massive "margin of safety" because it is already priced as if the worst-case scenario is happening.

Risk Level (Invalidation): $67.90 - This price represents the "Bear Case" scenario. If the price drops below this level, it suggests the market's negative view on future earnings may be materializing, and the thesis should be re-evaluated.

Target: $132.00 - This is the "Base Case" target, representing a potential +66% upside as the market realizes the company's growth is sustainable and re-rates the stock to a higher multiple.

DAM Capital Base Formation After Correction Risk Reward SetupTechnicals:

Trading in a broader sideways to range-bound structure after a sharp correction earlier in the year following that decline, the stock has spent time absorbing supply and recently found strong support in the ₹205–212 zone. The latest bounce from this area has formed a short-term higher low on the daily chart, indicating improving price stability rather than fresh selling pressure.

Price is currently hovering around ₹219–222, with the EMA flattening and price attempting to hold above it. This suggests a transition from a weak phase into base formation. structurally, the stock is moving toward a descending trend-line zone around ₹255–265, which aligns with a prior supply area. This zone is likely to act as the first major reaction area. From a risk-reward perspective, the setup favors a controlled pullback trade, with upside potential toward ₹275–300, while downside risk remains protected around ₹190, which marks the last strong demand and structure invalidation zone.

Momentum is also improving. RSI has recovered from oversold conditions and is now sustaining above the 50 level, pointing toward a shift from bearish to neutral-to-positive momentum. As long as price holds above the ₹212 support band, the bias remains constructive for a measured upside retracement toward higher resistance.

Fundamentals:

Operates as a financial services and investment banking firm, with revenues closely linked to capital market activity, deal flow, and overall market sentiment. after a strong listing and initial enthusiasm, the stock corrected sharply as market expectations normalized and broader mid-cap financial stocks saw valuation compression.

fundamentally, the business remains sensitive to equity market cycles, IPO activity, and advisory volumes periods of consolidation or lower market participation tend to reflect in muted earnings visibility, which explains the prolonged sideways movement in price however, as market activity stabilizes and risk appetite improves, earnings can recover relatively quickly due to the asset-light nature of the business.

At current levels, the stock appears to be transitioning from expectation reset to valuation discovery. The recent stabilization in price near long-term support suggests that downside risk is being gradually priced in, while the market waits for clearer earnings consistency and deal momentum. Any pickup in capital market activity, stronger quarterly numbers, or improvement in advisory pipeline could act as a catalyst for a re-rating, which would align with a breakout attempt above the descending trend-line on the chart.

Levels to watch

Support zone: ₹205–₹212

Risk protection / invalidation: ₹190

First reaction zone: ₹250–₹255 (trend-line and supply confluence)

Upside extension targets: ₹275–₹300

Like, comment your thoughts, share this post

Explore more stock ideas on the right hand side!

Disclaimer: This post is for educational purposes only and should not be considered a buy/sell recommendation.

Ultra Clean Holdings | UCTT | Long at $27.32Like Ichor Holdings NASDAQ:ICHR , Ultra Clean Holdings NASDAQ:UCTT is a prominent developer and supplier of critical subsystems, high-purity components, and specialized services, primarily for the semiconductor industry. I believe this is a very undervalued area in the semiconductor industry.

Growth

Earnings per share expected to more than triple between 2025 and 2028 and revenue is expected to be on the rise.

Health

Debt-to-equity: 0.9x (healthy)

Quick Ratio: 1.9 (great)

Altman's Z Score: 2.7 (good)

Action

Unless the semiconductor market implodes (or the company), the future looks bright for NASDAQ:UCTT in the next 2-3 years. It may dip into the low $20's in the near-term to close a few price gaps, but with a float of 44 million, it may get interesting at some point soon. Thus, at $27.32, NASDAQ:UCTT is in a personal buy zone.

Targets into 2029

$35.00 (+64.7%)

$60.00 (+119.6%)

Ichor Holdings | ICHR | Long at $20.41Ichor Holdings NASDAQ:ICHR is a major supplier in the semiconductor industry, specifically focused on the semiconductor capital equipment sector rather than directly manufacturing chips themselves. I believe this is a very undervalued area in the semiconductor industry. The other major competitor is Ultra Clean Technologies NASDAQ:UCTT .

Insiders

Buying between $14 and $17 share.

Growth

Earnings per share expected to more than double between 2026 and 2028 and revenue on the rise.

Health

Debt-to-equity: 0.2x (healthy)

Quick Ratio: 1.3 (good)

Altman's Z Score: 2.8 (good)

Action

Unless the semiconductor market implodes (or the company), the future looks bright for NASDAQ:ICHR in the next 2-3 years. With a float of 32 million, it may get interesting at some point soon. Thus, at $20.41, NASDAQ:ICHR is in a personal buy zone.

Targets into 2029

$32.00 (+56.8%)

$42.00 (+105.8%)

[COIN] 2-Year Channel Support Meets Deep Value (P/E ~20)The Setup:

Monthly Ascending Channel Since Jan 2024, COIN has traded within a clean ascending channel. We are currently testing the $217–$200 support zone.

Key History:

In April 2025, price staged a "fakeout" below the channel before rebounding. I expect similar volatility at the $200 level.

Invalidation:

A monthly close below $200 breaks the 2-year structure.

The Fundamentals:

Deep Undervaluation While the technicals test support, the valuation presents a rare divergence:

Value: COIN P/E is currently ~20x, significantly lower than the S&P 500 average of ~31.3x.

Growth: Coinbase's "Everything Exchange" strategy is scaling. The Base L2 blockchain and institutional tokenization services provide a diversified revenue floor that didn't exist in previous cycles.

My Strategy (Not Financial Advice):

Entry: Accumulate in the $217–$200 range.

Target: $500 (+140%) near the channel's upper resistance.

Stop Loss: Decisive close below $195.

My opinion only. If you think I'm wrong, I probably am.

Update: IREN Limited (IREN) - structure beats emotionsIREN Limited operates in Bitcoin mining and AI cloud infrastructure, focused on renewable energy and scalable data centers. Mining is the core revenue driver, AI services are still small but growing fast.

On the daily chart, a falling wedge has been broken to the upside, followed by a clean retest. The structure is holding. Price is now sitting in a strong daily support zone at 36–38, aligned with the 0.618 Fibonacci level.

MACD is turning bullish on higher timeframes, and short- to mid-term moving averages are stabilizing. This looks like accumulation after a deep correction, not a random bounce.

By the end of 2025, IREN scaled materially.

Revenue grew from $184M in 2024 to roughly $485M in 2025.

Bitcoin mining remains the main contributor, while AI Cloud Services added about $16M and continue expanding.

Consensus estimates point to ~$230M revenue in Q2 2026. EPS is still negative, which fits a capital-intensive expansion phase.

As long as price holds 36–38, the market is pricing a move toward 50 → 60 → 70.

This is not a one-day trade. It’s a structural recovery setup.

The chart already did the talking.

diwali pick 6 : ganesh consumer productkey facts about Ganesh Consumer Products, organized by category:

Product Portfolio (42 products, 232 SKUs)

– Whole Wheat Flour: Sharbati, White, Multigrain, Diabetes Control, Gluten-Free Atta

– Value-Added Flours: Bakery Maida, Super Fine Maida, Tandoori Atta, Rumali Atta

– Roasted Gram Flour (Sattu): Multigrain, Sweet, Jaljeera, Chocolate Sattu

– Spices: Turmeric, Chili, Coriander (whole & powder), Cumin (whole & powder), blended masalas

Manufacturing Footprint (7 plants)

– West Bengal (Kolkata): Jalan Complex I (Sooji/Maida 47,850 TPA; 72% util), Jalan Complex II (Spices 2,552–5,104 TPA; 2–27% util), Padmavati Unit (Atta 47,850 TPA; 80% util; Maida/Sooji 47,850 TPA; 54% util; Dalia 7,656 TPA; 74% util)

– Food Park: Sattu 15,950 TPA (49%), Besan 6,380 TPA (62%), ethnic flours 6,380 TPA (37%)

– Uttar Pradesh: Varanasi (Atta 47,850 TPA; 41%), Agra (Sooji/Maida 47,850 TPA; 63%)

– Telangana: Hyderabad (Maida/Sooji 63,800 TPA)

Business Model & Distribution

– 77% B2C revenue; remaining from B2B sales and by-product off-take

– 28 C&F agents, 9 super-stockists, 972 distributors, 70,000+ retail outlets

– Presence in 204 modern-trade stores and on multiple e-commerce platforms

IPO & Use of Proceeds

– Raised ₹409 crore in September 2025 IPO (listed Sep 29, 2025)

– Fresh issue ₹130 crore to: repay debt; fund Darjeeling gram-flour/Sattu unit capex; general corporate purposes

This comprehensive network, diversified SKU base, robust manufacturing capacity, and capital infusion position Ganesh Consumer for continued growth in its core flour and spice categories.

Dassault Aviation Société AnonymeFor my last idea of the year I have chosen to write one about Dassault Aviation. I really find aerospace and defense companies to be the most interesting to me in all of the stock market. As a matter of fact the majority of my holdings are invested into aerospace and defense companies. Aeronautics has always been an extremely competitive industry, ever since the first airplanes, engineers constantly strive to make the technology better, faster, safer and more cost effective.

I chose Dassault because I think the Rafale fighter program has a competitive advantage over the rest of the competition for the moment. There was also some issues, I remember around March of 2025 I saw on the news about how some nations were concerned with the credibility of the US and some nations even cancelled or suspended contracts with Lockheed Martin to delay F-35 purchases. I don't want to talk about that too much because I don't really know what is going on with that topic of discussion to tell you the truth. I do know nations take their national security very seriously though and aerospace and defense is no exception.

Like most aerospace and defense companies right now it is difficult to see very much upside intrinsically speaking. The sector has had some really nice attention and momentum this year, I don't see why it wouldn't continue into 2026 and beyond. I think its important to realize I am not really speculating about the topic though. I am not trying to say "buy it because I think it will go up". I think good ideas are just as important in the stock market as risk management itself and if you ask me I don't think its worth risking very much on Dassault right now.

Primary capital allocation is designated to research and development, industrial infrastructure and supply chain management. These are important elements when we look at the price of Dassault on a chart because the capital expenditures are primarily why certain price actions occur in real time. For example, if the company needs money to finance something new, the price of the shares might drop temporarily as money is being spent, alternatively if they get a new contract and its a big deal, they expect to make a lot of money from it the share price might go up. This is why I love these industrial companies, because we all know the products the company is providing is going to need a lot of maintenance over the years.

The company actively partakes in employee share programs, Dassault has allocated hundreds of millions of Euros toward employee incentives and profit-sharing in the current fiscal cycle. The company also likes to reward shareholders by engaging in share buy back programs from time to time. There is also a slight dividend that the company pays out as well if that is something you receive then you will know it helps out the portfolio a little bit.

The company has a pretty large cash position valued at about €10 billion at the end of 2025. This is primarily from advanced payments received by nations for major Rafale export contracts. Currently there is a record breaking order backlog on aircraft orders going into 2026, there is about €48 billion in backlog value. Don't quote me on this though because that was the value about 6 months ago so today it could be a little more or less, the value doesn't really matter to us as retail investors but I am just saying it for context. The company plans to take care of this backlog in a timely manner though, they plan to invest in more industrial capacity.

Recently the company celebrated production of its 300th Rafale fighter jet, and announced plans to increase production rates to four aircraft per month in the coming years to ensure deliveries stretch reliably into the 2030s. I think the stock would make a fine addition to any properly diversified portfolio as long as you understand the potential risks associated. Its a pretty interesting company I think there's definitely some great information on the internet and I am happy that I got to write this idea and share some information today.

Merry Christmas and thanks for putting up with me. Hope you enjoyed the idea.

Gogo Inc | GOGO | Long at $4.65While NASDAQ:GOGO Inc may have competition from Starlink when it comes to providing internet service to airlines and its passengers, such a change isn't financially beneficial to many airlines. Instead, as GoGo has stated, it's evolving its services to match those of Starlink (i.e. upgrades). As more and more people fly and internet demand grows, NASDAQ:GOGO will likely continue to position itself as a monopoly within the ISP world for airlines in the near-term.

Pros

Dominates the North American business aviation connectivity market, especially for smaller jets

Projected Growth : EPS +278.9% between 2025 and 2028

Insider Buying : $2.3 million in purchases in the last 2 months

Cons

Starlink competition

High debt (but plans to use free cash flow to reduce it substantially beyond 2026)

Action

While price may further dip into the $3 range in the near-term, I believe interest rates dropping, projected growth, and insider buying are potential bullish signals. The cost for airlines to switch to other providers is beneficial to maintaining NASDAQ:GOGO market dominance. However, like any play, this is going to come down to management's control of debt and no major economic or world issues disrupting airline travel. Thus, at $4.65, NASDAQ:GOGO is in a personal buy zone with near-term risk of a drop into the $3 range.

Targets into 2028

$6.00 (+29.0%)

$8.00 (+72.0%)

FERTILIZERS READY TO RIPFertilizer stocks have yet to move off their wave 2 bottoms. If you think the short squeeze in precious metals is mind-boggling—just wait till you see what a squeeze in fertilizers will look like. NYSE:IPI is the ONLY producer of POTASH in the USA. Most supply comes from Russia and Canada. Potash, like TVC:SILVER , is on the list of US critical minerals. No fertilizers, no food. You do the math. NYSE:IPI is HIGHLY TORQUED with only 10 million shares. No debt; MASSIVE cash hoard. The company is also ramping up production as demand increases and supply is squeezing. When this baby moves she will melt faces.

Caterpillar, a Key Industrial CompanyGood morning, I was going to wait until later tonight to write this idea and even though I don't feel so great this morning I still want to write it now while the words are in my head. Lately my mind is like a waterfall because things keep coming that I want to say. I don't hold onto these thoughts for too long I just let them go away because I don't really think its important to hold onto anything too tight. That's why I think its important that I write the idea now instead of later. For those of you that have been paying attention to what I have been saying will know by now I am not constituting financial advice, there is actually some wisdom in what I have been saying however.

I don't think a lot of people actually notice what the point I am trying to make is. I have said it before that I never stayed at a job for more than a few months and people seem to think that there's something wrong with me. See the problem is not with me, rather the problem is within their own ignorance. I am not saying this hypocritically either because I have already come to terms with my own ignorance, I am not calling people ignorant because I want to offend them even though that is always what happens. Sometimes the truth hurts and I think its so incredibly important to be honest with ourselves most of all.

Anyways it may seem at times like I might go off topic but at this point I am not going off topic. The topic of my ideas from now on is not to provide you with information about a company so you can make money. I think it would be much more meaningful to write about some of the things that have helped me to become successful in the stock market. Obviously, since I am writing about specific companies I will still include the necessary information I think is relevant to the context of the writing. Just know that, I am doing my best to provide quality content without wasting anyone's time.

So many people just want someone to tell them which stocks to buy or whether or not the stock will go up or down. To tell you the truth I don't think this is conducive to a constructive learning environment. I see so many people who are struggling in their trading career and they are focusing on the totally wrong things. It makes me sad to see this because there is really nothing I can do except write some ideas and hope these individuals are paying attention. The problem is that, most of the best ideas I have had are already behind me and I do not like to repeat myself so it is unlikely that I will write another idea on the same company even if I think its a good time to buy or not.

It also makes me feel good to write down my thoughts, its almost like a therapy for me. I am only human and none of my relatives care about stock market talk. In fact I can put almost anyone to sleep talking about the stock market. Anyways I am sure you probably want to see what I have to say about why Caterpillar is a good stock so without further adieu.

One of the things I find most interesting about Caterpillar is the fact that, it shows some pretty nice upside still. I used the discount cash flow model to interpret a fair value for the stock and I think a fair value for it would be somewhere in the ballpark of $675. This implies a significant upside despite the fact that technically it doesn't look great to be a buyer right now. Actually I doubled down on my position last week on Caterpillar and closed my position on Deere I am not writing this to talk about myself though and I don't think anyone cares about what I am doing anyways.

There has already been plenty of people talking about why the stock has done so good this year and I don't think it would really add any value to write about something that's already been said. This is one of those times where I am going to say if you are serious about buying some Caterpillar shares that you should do a little research for yourself on the company and why it is doing so good. It is not rocket science to go into Google and type "how does Caterpillar use capital in their business" that is literally all I did in some of my previous ideas that ended up being a little popular.

I used to be pretty bad at writing and I think the problem was, that I was trying to hard to say the right things. I have been having way more fun just saying, or well, writing the words as the come into my head. Like I said it makes me feel better to do this, I know someone has been paying attention to what I am saying and I truly hope that you don't take it the wrong way. Normally when I start writing these ideas I always feel like I would have more to say but it gets to a point where I kind of run out of words sort of speak. I know there's more I want to say but I don't know exactly what that is right now.

Anyways, thanks for reading my idea. I hope you make a lot of money and have a great day! Don't forget to have fun and stay safe this holiday season!

New Court Case DISASTEROUS for SOLANA?Quite silently, Solana may be heading into one of the most consequential legal challenges it has faced to date.

The implications reach far beyond short-term market of SOL -it will likely affect MANY more crypto's and projects.

A US federal judge has recently (past few days) approved a class action lawsuit to proceed against several parties tied to the Solana ecosystem, including Solana Labs and entities connected to PumpFun. This isn’t speculative rumors; the court has ruled that the claims presented are substantial enough to warrant deeper examination.

The argument of the case is an allegation that cuts directly into Solana’s technical design. Plaintiffs argue that certain insiders benefited from preferential access created by the network’s validator structure and transaction-ordering mechanisms. In practice, this allegedly allowed privileged actors to enter positions earlier, exit faster, and systematically offload risk onto retail participants.

The court’s decision suggests regulators and judges are increasingly willing to scrutinize not just token issuers or apps, but the underlying blockchain infrastructure itself when assessing fairness and market access. Therefore, it could be consequential for the rest of the crypto market as well in the near to long term.

That framing introduces a serious existential risk.

Bitcoin: The Battle Between Bulls and BearsSee the Future Before It Happens

Bitcoin is now moving between my Buy Zone and Sell Opportunity Zone.

Expect strong range trading between these levels unless major support breaks.

If BTC loses the bottom of its main ascending channel, there’s a secondary channel next to it — where the 50% ratio line could act as temporary support.

But if that level fails and confirms the breakdown… let’s say it clearly — Bitcoin might face one of its darkest phases in the next bearish cycle.

📊 Current setup:

Buy orders: around 75,200 – 81,731 USDT

Sell zone / opportunity: around 111,870 – 115,000 USDT

See the future now. When it plays out, remember the name 👉 TradeWithMky

Stay sharp, follow the trend, and always prepare for both sides of the market.

🚀 #Bitcoin #BTC #Crypto #TradingView #TradeWithMky

Fast Bounce Setup | Price: 63.33 → Target: 66.49 (+5%)Fundamentals 📊

HALO continues to show strong revenue and profit forecasts, with steady growth expectations.

The fundamental outlook remains supportive for short-term upside.

Repeated Behavior 🔍

This stock has a repeated pattern of delivering at least a 5% bounce from similar oversold or congested zones.

The current structure matches previous cycles.

Price Action 📉➡️📈

Price action at this level is reacting to a resistance zone, which historically leads to a quick 5% reaction move before continuation or pullback.

BUY BITCOIN SCALP Btcusd looking to give us a nice clear structural upside push , remember to trial stop and secure profits

Pinterest | PINS | Long at $26.20Pinterest's NYSE:PINS continued user growth is quite impressive, especially among Gen Z. Factoring in global expansion, the revenue and earnings projections caught my attention. Currently trading around a 9x price-to-earnings, it's kind of a sleeper in the tech world *if* the user numbers and forecasts are accurate. Annual EPS is expected to almost double by 2028, going from $1.29 in 2024 to $2.46 in 2028. Projected revenue growth is almost the same, growing from $3.6 billion in 2024 to $6.3 billion in 2028. Also, the company has a very low Debt-to-Equity Ratio (4%) and very strong cash flow. Projections .

From a technical analysis angle, it's in a consolidation phase - trading sideways and confusing investors. The price is having a hard time staying above or below its historical mean, but there are plenty of gaps above and below the current price to fill. A company like NYSE:PINS can benefit significantly from AI utilization and capturing a share of the great wealth transfer, but the news is harping on a bad economy / reduced ad revenue.

Personally, this is one of those "why doesn't the price reflect the fundamentals" plays. Yes, there is competition, but the user growth continues to be impressive. Insiders are selling at an alarming rate ( openinsider.com ), though. Something doesn't add up. So, personally, a decision based on the numbers (as reported today) is the only way to go. Thus, at $26.20, NYSE:PINS is in a personal buy zone. If this ticker truly tanks and fishy company news emerges, it's going to drop near $12 or below.

Targets into 2028

$32.00 (+22.1%)

$50.00 (+90.8%)