SPS Commerce | SPSC | Long at $77.51SPS Commerce NASDAQ:SPSC is a leading cloud-based supply chain management software provider, specializing in electronic data interchange (EDI), fulfillment, and e-commerce integration solutions. Key customers include major retailers like Walmart NYSE:WMT , Target NYSE:TGT , Home Depot NYSE:HD ; Procter & Gamble NYSE:PG , Nestlé OTC:NSRGY ; Sysco NYSE:SYY , and US Foods NYSE:USFD . As of 2025, SPS Commerce serves over 12,000 customers and connects to more than 100,000 trading partners globally.

Technical Analysis

The price fell through my "crash" simple moving average zone (green lines). This area is often an algorithmic share accumulation zone. The price spiked into the "crash" zone as the day went by after the earnings release. While this is still a high growth stock, there is still risk with the slowing economy, P/E ratio of 36x, and two open price gaps on the daily chart near $58 and $38. These price gaps will likely get filled if the US enters a recession, but are we really there yet? Depending on where you look (retail vs tech), there answer varies. But my bets are no - publicly. There is usually a Christmas rally every year, and NASDAQ:SPSC is in "oversold" territory in the near term. The price may dead cat bounce to $53, but I suspect it would take major negative economic news or a breakdown in company fundamentals to get there.

Financial Health

Debt-to-equity: 0x (healthy)

Quick ratio / ability to pay current bills: 1.5 (healthy / able to pay)

Altman's Z Score / bankruptcy risk: 19 (extremely low risk)

Earnings and Revenue Growth

Earnings per share growth from 2024 ($3.48) to 2028 ($6.52): 87.4%

Revenue growth from 2024 ($638 million) to 2028 ($1.03 billion): 61.4%

www.tradingview.com

Action

Given the overall health of the company, potential for a Christmas rally, and technical analysis "crash" entry, NASDAQ:SPSC is in a personal buy zone at $77.51.

Targets into 2028

$90.00 (+16.1%)

$100.00 (+29.0%)

Growth

My Waste Management Investment StrategyAfter the last earnings report causing one of my favorite stocks to fall, it presents a valuable opportunity in my opinion. I am going to write what I like about the company and why I feel like it is a good idea to have Waste Management in your portfolio. I will write about all the reasons I think this is a good investment. Enjoy!

The very first thing I do when I am looking at a company for the first time, is calculate the intrinsic value of the stock to determine if it is undervalued or not. According to the numbers I ran through the equation Waste Management is undervalued by approximately 40% at this time of writing. I reasonably believe the stock could be worth as much as $280 in the next couple years.

Waste collection and disposal are critical for public health and safety, making them essential services that society cannot function without. Demand for these services is stable and generally not affected by economic downturns or price increases because customers, whether residential or commercial, will continue to generate waste that needs managing.

Establishing waste management infrastructure, such as landfills and processing facilities, requires significant capital investment, technical expertise, and complex permitting processes, making it difficult for new competitors to enter the market. The industry is often fragmented, allowing large publicly traded companies to acquire smaller, regional firms, leading to economies of scale and increased market share.

Companies are increasingly investing in recycling facilities, converting landfill gas into renewable natural gas (RNG), and offering other environmental services. These initiatives align with global sustainability goals and create new revenue streams and growth opportunities, attracting ESG-focused investors.

Many established companies in this sector have a history of consistent dividend payments and share repurchase programs, appealing to investors seeking reliable income and long-term value. The low volatility of the waste sector can help diversify an investor's portfolio and provide some protection during volatile market cycles.

The cost of waste removal is typically a very small fraction of a customer's total expenses (e.g., well below 1% for commercial customers). This low relative cost makes customers less likely to scrutinize price increases or switch providers over small differences, making it easier for companies to raise prices.

In summary, garbage companies have significant pricing power primarily due to high barriers to entry, the essential nature of their services, and the localized, regional-monopoly characteristics of the industry.

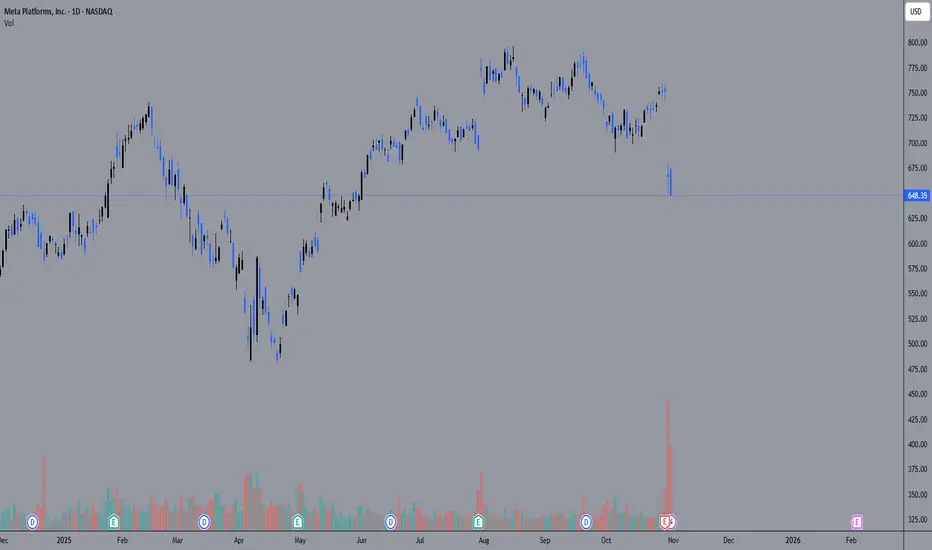

The META drop explainedSo what happend to META last week:

I see a lot of you wondering what happend to the stock and what caused the drop.

The answer is simple. The EPS was not so good.

We can see on the chart that the EPS is only 1.05 and that they expected 6.723 . That is a chance of -84.38%.

So for that big of a chance this is a small drop.

The Reason:

So the reason that this happend is because they need to pay some extra in taxes.

The tax that they need to pay is around 15,9 billion dollar.

This is because Trump has passed some tax laws that state that big companies need to pay taxes on profits that they have made outside of the US.

This is only a one time tax that they need to pay and the reason that they are doing this is because they want to avoid companies to do tax evation and book more profits outside of the US.

What we also do need to know is that made up profits outside of the US are being re-evaluated and that they need to pay tax on a portion of that profit because the see a portion of it as domestic assets.

What we need to keep in mind:

What we need to keep in mind here is that the EPS only dropped because of this tax and that there are people saying that the EPS without this tax would have been around 7.25 . So a good boost from what the analysist are expecting of META.

So you could see this as a big discount you get on the stock price.

Amazon (AMZN): Ready for a New Breakout!Amazon isn’t just delivering packages — it’s delivering earnings surprises and a chart breakout too! 😎

After reporting strong Q3 earnings on 30 Oct 2025 , AMZN’s chart popped with a clean cup & handle breakout on 31 Oct 2025 — just in time for a bullish Halloween rally 🎃🐂

💰 Earnings Highlights :

Revenue : Came in above expectations, boosted by AWS and advertising growth.

EPS : Beat market estimates, showing stronger profitability.

Operating cash flow : Improved significantly — partly thanks to deferred tax effects — giving Amazon more room for CapEx and expansion.

☁️ AWS Power :

AWS continues to lead the way with steady growth and improved margins. Analysts expect momentum to carry into Q4 2025 , supported by rising demand for cloud and AI-driven services.

📊 Technical View :

The chart shows a classic cup & handle breakout — volume confirmation looks solid, suggesting potential continuation into year-end.

🔥 My Take:

When strong fundamentals meet a clean technical setup, that’s where the magic happens. Amazon might just be brewing a latte-fueled rally into Q4 ☕🚀

Getty Images | GETY | Long at $2.29Bull Thesis

Data is "knowledge" for AI.

Getty Images NYSE:GETY holds immense importance in the generative AI race due to its control over a vast, high-quality library of over 500 million licensed images and metadata.

By licensing content (e.g., via deals with Nvidia), NYSE:GETY monetizes its assets, promotes responsible AI, and challenges open-source models.

Standardized license deals will boost AI's commercial viability and prevent a "wild west" of IP theft, ultimately accelerating safe deployment in industries like advertising and media.

The merger with Shutterstock will only help NYSE:GETY be the ultimate leader in this licensed data space.

Bear Thesis

The "wild west" of IP theft continues for years and the company's debt / poor fundamentals build until and ultimate collapse or acquisition.

Action

The bull thesis makes the most sense given the amount of data NYSE:GETY has and the future of data licensing deals. Now, I would love the price to go lower to accumulate more shares (under $2 is not out of the question in the near-term). But, at $2.29, NYSE:GETY is in a personal buy zone, and a starter position was made. More shares will be gathered in the $1 range if the earnings and revenue growth projections continue to look promising beyond 2025: www.tradingview.com

Targets into 2028:

$3.07 (+34.1%)

$5.00 (+118.3%)

USDJPY — Fibonacci Confluence and Trend Continuation SetupThe USDJPY pair is currently consolidating around the 153.78–153.35 Fibonacci zone after testing the 0.236 retracement from the recent swing high at 154.47. Price is holding above the short-term ascending trendline, indicating that bullish structure remains intact unless we see a clean break below the 0.618 retracement (152.64).

Key Technical Zones:

Resistance: 154.47 (swing high)

Support 1: 153.35 – 152.64 (Fib confluence and trendline zone)

Support 2: 151.50 / 150.70 (major retracement & potential buy zone)

Trade Outlook:

I’m monitoring a potential pullback toward 153.35–152.90, where buyers may re-enter for another push toward 154.40–155.00.

If price fails to hold above 152.60, the bias shifts to short-term bearish, with targets near 150.70–149.70 (1.272–1.618 extension levels).

Bias:

Bullish continuation favored while above 152.60, supported by recent USD strength and stable U.S. yields.

However, keep an eye on the upcoming Fed & BoJ events, as policy tone could shift volatility and trend momentum.

Applied Materials | AMAT | Long at $169.75Republican Ashley Moody recently dropped $200k-$500k on Applied Materials $NASDAQ:AMAT. The semiconductor boom may not be over...

Price-to-earnings: 21.68x (great in comparison to others...)

Debt-to-equity: 0.34x (low)

Cash flow: $10.4 billion (FY2024)

Insiders awarded options recently

Unless NASDAQ:NVDA brings the market down, NASDAQ:AMAT is in a personal buy zone at $169.75. While the price may dip in the near-term to the $140s, bullish until the semi boom dies...

Targets:

$195.00

$215.00

$240.00

Palantir is at dot-com levels of overvaluationTl;dr, Palantir is grossly overpriced against the general market, as well as against its own financial metrics from 4 years ago, and its valuation metrics put it in peak dot-com bubble territory.

Metrics

Palantir's current price puts it at a market cap of $467.35B. With expected $3.5B in annual revenues in 2025, the price/sales (PS) ratio is at ~147 . PS ratios are the financial metric to watch for growth stocks, since growth companies prioritize revenue growth.

A high PS ratio should mean that the market expects high revenue growth. While Palantir's revenue growth is pretty high, it's not as exceptional as the PS ratio would imply. It seems that the market is not only extrapolating the revenues to continue rising, but it's also extrapolating that the growth itself (or first derivative of revenues) is going to keep increasing for years sequentially. Palantir has to generate far higher annual growth than it currently has to come close to justifying this valuation, I'd expect at least 175% annually.

For reference, Nvidia traded at a PS ratio of 43 in mid 2023, and then generated 125% growth 2 years in a row. The PS ratio stayed relatively stable since then, and never went past 43. Important thing to note here is that Nvidia also has higher net profit margins than Palantir, and profit margins play a role in how PS is interpreted (since earnings is what really matters). Palantir's profit margins have been growing consistently, from 10% -> 16% -> 32% annually, but still not close to Nvidia's 50%. Further profit margin growth would help to justify the overvaluation.

Comparisons

As the chart shows, Palantir's annualized revenue growth last quarter is equivalent to its growth in 2021 at ~50%. Revenues since then increased by 170%. Palantir at the time traded at a PS of 37, which is pretty high for 50% growth, but not too crazy.

If the stock traded at the same PS ratio as in 2021, where its growth was the same, the stock would be trading at ~$53 today at a market cap of $120B.

A PS ratio of >100 implies extreme bubble levels. From what I've found, during the very peak of the dot-com bubble:

Yahoo! traded at PS 100

Amazon traded at ~50

Ask Jeeves traded at ~55

CMGI traded at >300

Internet Capital Group traded at >200

Webvan traded at ~150

With Palantir trading at a PS of 147, it's well within the peak dot-com levels of overvaluation. While the entire tech/AI market is currently at very high valuations, Palantir still towers far above them.

Some examples of other high growth stocks today:

Crowdstrike at PS 30

AppLovin at PS 41

ServiceNow at PS 16

Netflix at PS 11

Even with the stock screener I couldn't find a stock that came close to trading Palantir's PS ratio, except for Microstrategy (which has no revenues as a crypto holding company) and for moonshot pharma R&D stocks which also have little to no sales by design.

The point of this idea is to show how grossly and absurdly overpriced this stock is, but it's not a recommendation to take a short position. The stock is so far decoupled from reality that you should consider it as equivalent to a meme coin. The financials don't matter, and it's simply an asset with a limited supply that is in high demand, so the price keeps going up.

Fiserv | FI | Long at $69.91For the first time since its IPO in 1986, a "major stock" crash has happened to Fiserv NYSE:FI . Previously, the stock "crashed" and followed the trajectory of ups and downs of the S&P 500, but this one is different. And, perhaps, a major opportunity for savy investors.

I won't say much about the financials since after today's earnings call the stock plummeted and earnings/revenue projections will get revised serval times, but this was a high-growth opportunity in the past. What I see today is a huge overreaction to a company going through a growth transition, but by all means, not dead... yet www.tradingview.com

I think we'll see leadership shakeups, layoffs, and system adaptions into 2026. This drop, and where it landed near my major crash simple moving average, hints this price cut was planned (at least algorithmically) and I won't be surprised if the near-term bottom is in or almost in in the $60s. Thus, at $69.91, NYSE:FI is in a personal buy-zone.

Conservative Targets into 2028:

$85.00 (+21.6%)

$100.00 (+43.0%)

Global E-Online | GLBE | Long at $34.55Global-e Online NASDAQ:GLBE provides a direct-to-consumer, cross-border e-commerce platform. It enables merchants to sell internationally and shoppers to buy globally, handling localization, payments, shipping, and logistics for worldwide transactions. Some companies NASDAQ:GLBE handles transactions for include Bath & Body Works, Victoria's Secret, SKIMS, Forever 21, and many more.

Technical Analysis

NASDAQ:GLBE is currently in a consolidation / "share accumulation" phase (i.e. trading sideways, overall), and the price is riding within my selected historical simple moving average. Often, the price will bounce along this area until momentum picks up and then it's off to the races to fill all the open price gaps above on the daily chart. The only concern I have is there is an open price gap on the daily chart near $21 that will likely get filled at some point. However, the earnings and revenue projections, if accurate, may delay this area from being filled for some time.

Revenue and Earnings Growth into 2028

538% earnings-per-share growth expected between 2025 ($0.34) and 2028 ($2.17).

98% revenue growth projected between 2025 ($946 million) and 2028 ($1.87 billion).

www.tradingview.com

Health

Extremely healthy, financially.

Debt-to-Equity: 0x (can't beat that)

Quick Ratio / Ability to Pay Today's Bills: 2.5x (no issues)

Altman's Z-Score/Bankruptcy Risk: 11.6 (extremely low risk)

Action

The projected growth of NASDAQ:GLBE makes sense if there is continued rapid on-boarding of blue-chip clients. There is always the chance other companies, like Shopify, will partner, too. The company is also extremely financially healthy. It should be able to weather the storm in the near-term if there is a financial downturn. That is the only major risk I see here. If the economy flips globally, such companies, regardless of their performance, will get hit hard. However, if the growth is accurate, this is a no-brainer value/growth play. Time will tell.... thus, at $34.55, NASDAQ:GLBE is in a personal buy zone with near-term risks of a drop to $21 or below if the world economy flips.

Targets into 2028

$50.00 (+44.7%)

$60.00 (+73.7%)

ASML Holding | ASML | Long at $680.00NASDAQ:ASML Holding, a developer and servicer of advanced semiconductor equipment systems for chipmakers, dipped backed into my overall, long-term selected simple moving average (SMA). From here, stocks typically bounce or drop, but given the AI boom is far from "over", I anticipate another bounce to eventually close the gap near $1,060. It may show some minor weakness to close the gap in the low $600s and get the bears excited. But, unless the economy further shows major weakness in the semiconductor space, NASDAQ:ASML is in my personal "buy zone" at $680.

Target #1 = $730.00

Target #2 = $915.00

Target #3 = $1,060.00

Why Bitcoin’s 4-Year Cycle Might Be Its Biggest LimitationFor years, traders have treated Bitcoin’s 4-year halving as sacred — a mechanical driver of boom and bust. But what if the real reason these cycles repeat isn’t the code… but the crowd?

Mechanically, Bitcoin’s issuance schedule is a smooth, predictable decline. The halving simply adjusts the slope of supply — it doesn’t dictate price. Yet, like clockwork, markets rise and fall every four years. Why?

Because we expect them to.

This expectation creates a self-fulfilling feedback loop:

- Pre-halving optimism fuels accumulation and speculative positioning.

- Post-halving euphoria drives parabolic rallies as new participants flood in.

- Overvaluation and leverage eventually unwind, triggering brutal corrections.

The halving became the metronome of market psychology — a narrative so powerful that it shaped behavior more than fundamentals ever did.

🧠 The Institutional Shift

Now, that narrative is being rewritten.

Institutions don’t trade on memes or cycles — they trade on models, liquidity, and risk.

Unlike retail investors, institutions hate volatility. They don’t chase euphoria; they manage exposure.

- ETFs and funds accumulate steadily through structured inflows.

- Option and futures desks hedge risk dynamically, suppressing volatility.

- Algorithmic allocators rebalance based on Sharpe ratios, not halving hype.

This structural participation acts as a volatility dampener — flattening the amplitude of Bitcoin’s historic boom-bust waves.

🌍 From “Halving Cycle” to “Liquidity Cycle”

As Bitcoin matures, the real driver of its price action is shifting away from internal events and toward macro liquidity conditions :

- When global liquidity expands (rate cuts, QE, easing credit), Bitcoin thrives.

- When liquidity contracts (rate hikes, QT, risk-off sentiment), Bitcoin cools.

In this new phase, the halving’s scarcity still matters — but it’s no longer the heartbeat.

Instead, Bitcoin is syncing to the rhythm of global capital flows.

📈 The New Market Identity

We’re watching Bitcoin transition from a reflexive narrative asset to a macro-integrated store of value .

If this continues, the implications are profound:

- Shallower drawdowns and fewer liquidation cascades.

- More consistent accumulation across cycles.

- Higher institutional allocation as volatility compresses.

Ironically, the same psychological loop that once fueled Bitcoin’s meteoric rise may now be what caps its potential.

The halving didn’t make Bitcoin cyclical — investor behavior did .

And as smart money takes over, that feedback loop may finally be breaking.

🚀 What This Might Mean for Future Bull Runs

If institutions continue to dominate Bitcoin’s liquidity, the next bull runs may look less like fireworks and more like steady expansion — smoother, slower, but more sustainable.

Instead of 12-month parabolas followed by multi-year winters, we could see:

- Extended accumulation phases where price grinds higher over longer horizons.

- More efficient corrections that reset leverage without catastrophic selloffs.

- Reduced retail blow-off tops as narrative-based speculation loses power.

That doesn’t mean the explosive upside is gone — it means the path to higher valuations might look more like a compound growth curve than a recurring bubble.

The next phase of Bitcoin’s evolution isn’t about chasing the halving — it’s about understanding liquidity, positioning, and psychology on a global scale.

- The crowd traded Bitcoin like a story.

- Institutions are turning it into a system.

Qualcomm Inc | QCOM | Long at $156.60Qualcomm NASDAQ:QCOM is a global leader in wireless technology, focusing on 5G chipsets, AI-capable Snapdragon processors, and connectivity solutions for smartphones, IoT, and automotive. Revenue through 3 quarters of 2025 is ~$40B. Revenue growth is anticipated to be 10-12%, year over year (2026: ~$45B; 2027: ~$50B; 2028: ~$56B). 5G adoption, AI chip demand, and automotive needs should continue to drive the stock price. Earnings per share are projected to grow 12-14%, year over year (2026: ~$11.20; 2027: ~$12.80; 2028: ~$14.70). Thus, the future looks quite bright for NASDAQ:QCOM .

Regarding price, it is currently trading at a PE of 15x and has a 2.25% dividend. The price is resting just above my historical simple moving average channel. I do anticipate it to drop into the channel (down in the high $130's-$140's) in the near-term due to typical September selloffs. However, I plan on adding more in the zone. A major bear case would be a major drop into the $90's to fill the price gaps on the daily chart before moving higher. I do not think this will happen unless a major catalyst in the market emerges - but always be prepared. Regardless, it is a strong company providing products and services that are in high demand. Currently fairly valued, I believe it become undervalued as the demand for 5G and new phone chips with AI capabilities emerges.

Thus, at $156.60, NASDAQ:QCOM is in a personal buy zone with a likely near-term drop into the $130's and $140's.

Targets into 2028:

$191.00 (+22.0%)

$225.00 (+43.7%)

Lululemon Athletica | LULU | Long at $165.00Lululemon $NASDAQ:LULU. If you don't think the US is in a recession, examine most retail stocks right now. But this doesn't mean doom and gloom are here from a US government/news narrative - in fact, the complete opposite. AI and tech are solely propping up the US stock market ... but pay no attention to the issues behind the curtain! Once interest rates start dropping, trading and investing are going to get wild before the cracks open up.

Okay, off my soap box...

NASDAQ:LULU entered by "crash" simple moving average zone (green lines) today after earnings. Competition is finally catching up to the company, but expansion into China and other foreign areas *may* revive them in the next 1-2 years. While most analysts are relatively bullish, I'll stay centered. I wouldn't be surprised if the stock dips into the $140's and $150's in the near-term. Bigger news will have to come out for me to stay long-term, but I'm holding here or even lower. Additional entries will be made in the $140's-$150's to swap out the position I just made at $165.00 for the future.

Thus, at $165.00, NASDAQ:LULU is in a personal buy zone with the risk of a continued drop to the $140's and $150s. Christmas rally potential...

Targets into 2028:

$185.00 (+12.1%)

$197.00 (+19.4%)

Netflix Earnings Market OverreactionAt this point we all know that Netflix is a common part of an average American's life. However, we came to terms with reality that the global field has a larger effect on the NASDAQ:NFLX than we might think. As we saw in the Q3 '25 earnings report, Brazil levied a one time tax bill on Netflix that charged them over half a billion in back taxes under a court ruling in local rules. This expense has not actually been paid yet, but has been reported on the financial reports as seen in the recent report. However, this should cause some eyebrows to raise as the stock has dropped over 18% from the all time high and over 8% this week. Most would assume that Netflix blew it on the earnings and that the stock should be toxic until 2026, but this may not be the case for those who look a little closer.

Firstly, lets tackle the elephant in the room. As stated before, Netflix showed nearly a $619,000,000 one-time tax expense levied by the Brazilian government concerning back taxes in revenues. Sure, this isn't necessarily good for their business, and it could be assumed that the Netflix was not very excited to report this on their statements. However, the nature of this tax should imply that this is not an ongoing part of their operations and this should not be expected in the quarters to come. Netflix also felt the need to state that operating margin would have beaten guidance had this not shown up on the income statement. So although this isn't good, it's not a core part of the companies health and operations continue to be profitable and should expect to stay that way.

Unfortunately, this odd tax expense overshadowed a key statistic, and no it's not some ratio or percentage. It's the Q3 stock buyback number which comes out to:

- 1,500,000 shares bought back

- Average price @ $1,220

- About $1.8 Billion in total spent on buybacks.

Even with these impressive numbers, we still cant fully capture just what Netflix is capable of in this aspect. Currently, they are sitting on $10 billion in pending authorization for stock buyback with no shelf registration. This means that Netflix is currently only allowed to buy their own shares back and not sell any to the financial markets until they file a shelving registration with the SEC. Now, there shouldn't be any need to explain why these metrics are bullish but the recent events show what was stated previously, and that is: the market has overreacted to the Netflix earnings miss.

So what's the course of action? The simple answer we can pose is to buy the dip. Simply buy the asset on discount and wait for it to rise, then sell for what should be a market beating profit. It also seems that some analysts are already on this case, with some projecting a 30% upside in the near future. I wouldn't disagree with them as Netflix looks to be a very attractive price. I wouldn't expect it to move in such a manner as my SanDisk callout but I also don't see a reason why this trade cant turn a nice profit going into the new year.

Basis Price @ $1,100

Time expectation: 1-6 months

Target price: $1,350-$1,500

SentinelOne | S | Long at $17.04SentinelOne NYSE:S : a cybersecurity company that uses an autonomous AI-powered platform to performs real-time threat detection, prevention, and remediation across endpoints, cloud, and IoT.

Technical Analysis

Price is consolidating along my historical simple moving average (a regression to the mean). This is after a meteoric rise in 2021 to $78.53 (just after the IPO) and then collapse to $12.43 in 2023. While near-term ups and downs may persist for a bit, usually a price consolidation near the historical simple moving average eventually leads to a major move. The simple moving average band is getting tighter, signaling the potential for a move out of the zone "soon". Given the grow, niche, and need, the future may be bright with this one.

Growth

www.tradingview.com

820% growth expected in earnings per share between 2024 ($0.05) to 2027 ($0.46)

75% revenue growth projected between 2024 ($821 million) to 2027 ($1.4 billion)

Health

Debt-to-equity: 0 (perfection)

Altman's Z Score \ Bankruptcy Risk: 3.3 (extremely low risk)

Quick Ratio: 1.7 (they are able to pay current bills without relying on debt)

Insiders

Warning: Lots of selling and no buying...

openinsider.com

Action

SentinelOne NYSE:S is an extremely healthy company with very high-growth potential. However, the cybersecurity landscape is highly competitive, but NYSE:S is forming a niche with AI-powered tools. While insider selling is a red flag, that is all I can see here besides competition (or the company secretly falling apart behind the scenes). That's the risk we all take as investors. Thus, at $17.04, NYSE:S is in a personal buy zone.

Targets into 2028

$24.00 (+40.8%)

$27.50 (+61.4%)

Orion S.A.| OEC | Long at $5.75Orion NYSE:OEC : Another chemicals company in the dumps, but is it justified - long-term?

Technical Analysis

Price fell through my "crash" simple moving average zone (green lines). The last time this happened the price moved down to my "major crash" zone (gray lines) and subsequently rallied to a 4x investment 1.5 years later. Not to say that same trajectory will happen, but this company (like all chemical companies) are historically cyclical. The price may continue to drop into the $3's in the near-term and complete the "major crash" touch, but a longer-term outlook is likely to generate positive returns... likely...

Growth

A bad 2025, but beyond that, projections show growth in earnings and revenue through 2027: www.tradingview.com

Fair Value and Health

Fair value: $8.30

Tangible Fair Value: $6.58

Company cut its 2025 guidance due to softer demand and shifted focus to free cash flow generation.

Debt-to-equity: 2.19x (high)

Action

While this is mostly a technical analysis play, there are so many opportunities right now with chemical companies. The tape beyond 2025 is likely to be positive and those who can stomach the near-term risks (i.e. $3's) may do well long-term. But there are better plays out there for the impatient.

Targets into 2028

$6.60 (+14.8%)

$9.00 (+56.5%)

Diwali Setup: Long on Hope, Short on Doubt.Wishing you and your loved ones a Diwali filled with light, laughter, and new beginnings.

May this festival bring clarity to your path, warmth to your heart, and prosperity to your home.

🪔✨ Happy Diwali

This festive season, I’m charting more than markets—I’m charting renewal.

May your trades be guided by clarity, your risk managed with wisdom, and your journey lit with purpose.

🪔📈 #DiwaliSetup #TradingViewIndia #CandlesOfClarity #TechnicalAnalysis #FestivalOfLights

GoDaddy | GDDY | Long at $128.90GoDaddy NYSE:GDDY is the world's largest domain registrar, managing over 84 million domains for over 21 million customers. AI, particularly through GoDaddy's Airo platform and related GenAI tools, is poised to drive outsized growth by supercharging product innovation, customer value, and operational efficiency.

Technical Analysis

The stock has dropped 35% so far in 2025, but this was after a meteoric 208.5% rise from October 2023 to December 2024. The price has now regressed to my selected historical mean - a typical share-accumulation region for algorithmic trading when it comes to high-growth stocks. While this is often a solid area of support, it may dip down to $115 to shakeout retail traders. Obviously, further declines would occur if fundamentals change, but the forward growth is highly attractive, and I doubt it will "crash" from here if the outlook remains positive.

Earnings and Revenue Growth into 2028

Projected earnings-per share growth between 2025 ($5.98) and 2028 ($11.12): 86.0% (AI effect...)

Projected revenue growth between 2025 ($4.92 billion) and 2028 ($6.19 billion): 25.8%

Current P/E: 22x (remaining tech sector: 45.7x)

www.tradingview.com

Insiders

Warning: Lots of insider selling and no recent buying.

openinsider.com

Health

Debt-to-equity: 9x (very high, but due to aggressive share repurchases rather than distress)

Cash flow remains a bull case cornerstone, with accelerating free cash flow conversion (>100% of EBITDA) underscoring operational leverage from AI efficiencies and premium customer shifts.

Action

GoDaddy NYSE:GDDY is a prominent name and leader in domain registration. As AI enhancements lead to improvements in operational margins, earnings are likely to grow tremendously into 2028. Once agentic AI search enters the scene, it will be very interesting to better understand the importance of such a domain registration company for its successful implementation. While the price may dip beyond the historical mean to shakeout some retail traders, I think the future of this currently undervalued, high-growth company into 2028 is very bullish. Thus, at $128.90, NYSE:GDDY is in a buy-zone with potential near-term risk between $100 and $115.

Targets into 2028

$160.00 (+24.1%)

$200.00 (+55.2%)

Bioceres Crop Solutions | BIOX | Long at $1.43Technical Analysis

Bioceres Crop Solutions NASDAQ:BIOX has entered my selected "crash" simple moving average. This area is often a zone of share accumulation and may result in a trend reversal (or a short-term stair-step down to $1 or lower before trading sideways).

Growth, Fundamentals, & Health

Not expected to become profitable again until 2028.

Earnings-per-shares growth from 2026 (-$0.26) to 2028 ($0.56): +323%

Revenue growth from 2026 ($350 million) to 2028 ($511 million): +46%

Current Fair Value: $5

Debt-to-Equity: 0.9x (very good / healthy)

Altman's Z-Score/Bankruptcy Risk: .9 (high risk, some financial distress)

Action

75% technical analysis play and only 25% based on company fundamentals. The only major risk based on the data is bankruptcy. The near-term could be rough for the company, but the outlook into 2028 shows significant growth. Thus, at $1.43, NASDAQ:BIOX is in a personal buy zone. There could be near-term risk near $1 or a bit lower, but this one is a total gamble. Time will tell.

Targets into 2028

$2.00 (+39.9%)

$4.00 (+179.7%)

CCJ/QQQ long NYSE:CCJ NASDAQ:QQQ AMEX:NUKZ $CCJ/NASDAQ:QQQ

Secular shift and outperformance in uranium and nuclear energy companies compared to QQQ

diwali pick 6 : ganesh consumer productkey facts about Ganesh Consumer Products, organized by category:

Product Portfolio (42 products, 232 SKUs)

– Whole Wheat Flour: Sharbati, White, Multigrain, Diabetes Control, Gluten-Free Atta

– Value-Added Flours: Bakery Maida, Super Fine Maida, Tandoori Atta, Rumali Atta

– Roasted Gram Flour (Sattu): Multigrain, Sweet, Jaljeera, Chocolate Sattu

– Spices: Turmeric, Chili, Coriander (whole & powder), Cumin (whole & powder), blended masalas

Manufacturing Footprint (7 plants)

– West Bengal (Kolkata): Jalan Complex I (Sooji/Maida 47,850 TPA; 72% util), Jalan Complex II (Spices 2,552–5,104 TPA; 2–27% util), Padmavati Unit (Atta 47,850 TPA; 80% util; Maida/Sooji 47,850 TPA; 54% util; Dalia 7,656 TPA; 74% util)

– Food Park: Sattu 15,950 TPA (49%), Besan 6,380 TPA (62%), ethnic flours 6,380 TPA (37%)

– Uttar Pradesh: Varanasi (Atta 47,850 TPA; 41%), Agra (Sooji/Maida 47,850 TPA; 63%)

– Telangana: Hyderabad (Maida/Sooji 63,800 TPA)

Business Model & Distribution

– 77% B2C revenue; remaining from B2B sales and by-product off-take

– 28 C&F agents, 9 super-stockists, 972 distributors, 70,000+ retail outlets

– Presence in 204 modern-trade stores and on multiple e-commerce platforms

IPO & Use of Proceeds

– Raised ₹409 crore in September 2025 IPO (listed Sep 29, 2025)

– Fresh issue ₹130 crore to: repay debt; fund Darjeeling gram-flour/Sattu unit capex; general corporate purposes

This comprehensive network, diversified SKU base, robust manufacturing capacity, and capital infusion position Ganesh Consumer for continued growth in its core flour and spice categories.

diwali personal favourite pic 4: vip ind my thesis is In BHARAT, THE tourism HAS TO to pick pace and this a proxy play in the same segment

healthy time and price correction seemingly completes .

India’s organized luggage market reached an estimated ₹4,450 crore in retail value during CY 2024–25, expanding at a robust 9.6% CAGR

over the past five years and accounting for roughly 12 million units sold annually.

Modern retail outlets and branded stores command around 65% of sales, while e-commerce contributes 20% and traditional/unorganized channels .

the remaining 15%. Hard-shell suitcases lead the category with a 52% share, followed by soft-side trolleys at 28%, backpacks and duffels at 15%, and travel accessories at 5%.

At the forefront of the market, VIP Industries holds a 32% revenue share, underpinned by its extensive distribution network,

while Safari Industries occupies the second spot with an 18% share by focusing on the value segment. American Tourister, part of the Samsonite Group, captures 15% of the market, and Samsonite itself secures 10% by positioning in the premium segment.

Youth-oriented Skybags accounts for 7%, and a diverse set of domestic players—including Wildcraft and Carlton—make up the remaining 18%. In terms of pricing, 45% of units are sold in the economy segment (under ₹2,000), 40% in the mid-range (₹2,000–5,000), and 15% in the premium bracket (above ₹5,000). Looking ahead,

the market is projected to reach nearly ₹6,300 crore by CY 2028 at a faster 10.5% CAGR, driven largely by premium and “smart” luggage innovations such as ABS-PC blends and RFID-enabled locks, as well as the continued growth of e-commerce and omnichannel retail strategies.