Hull Crossover Strategy no TP or SLWhat is it?

A simple yet effective strategy ran on the 30m chart.

This is a basic idea that can be expanded on using different indicator to either add signals or filter out certain bad signals!

The strategy consists of 1 fast moving average and 1 slow moving average.

Both of these moving averages are the Hull Moving Average

What is the Hull Moving Average?

The Hull Moving Average ( HMA ) is a directional trend indicator.

It captures the current market conditions and uses recent price action to determine if conditions are bullish or bearish relative to historical data.

The Hull is different from traditional trend indicators like the EMA and the SMA .

It is designed to reduce the lag often associated with other MAs by providing a faster signal on a smoother visual plane.

How it works?

When the fast HMA crosses over the slow HMA , we initiate a long signal, and

when the fast HMA crosses under the slow HMA , we initiate a short signal.

Conclusion

The power of simplicity is what makes this such a great core to use to build onto making something even better!

The results were optimised to suit the most common market conditions seen today.

******** Not financial advice! ********

Search in scripts for "algo"

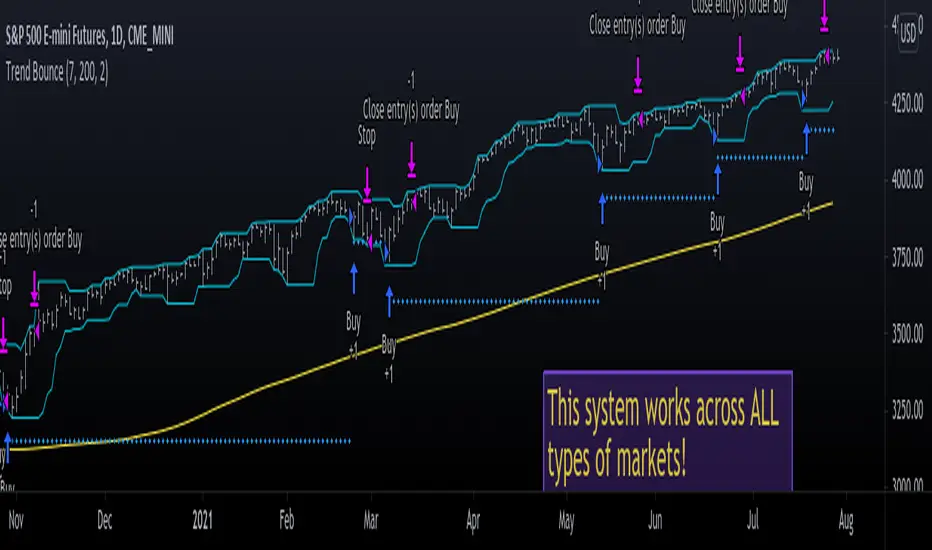

Trend Bounce [racer8]I discovered this mechanical trading system titled "This Algo Strategy Has Only 3 rules and 62% Win Rate".

I coded the trading system on Tradingview...and now I am introducing it to you guys.

I modified the system so that it has both buy & sell signals.

I've tested it repeatedly in different markets on TV including stocks, currency pairs, bitcoin, and commodities...and it works!

A buy signal is generated whenever the current close is below the previous 7-day low and the current close is above the 200 period moving average.

A sell signal is generated whenever the current close is above the previous 7-day high and the current close is below the 200 period moving average.

The system also has a 2-ATR stop loss which I coded.

This system is unique in that it has both trend-following and reversal elements in it.

The system trades short-term reversals while obeying the long-term trend.

Essentially, you are buying the dips of bullish trends! & selling at the peaks of bearish trends!

Enjoy ♡

HYE Mean Reversion VWAP [Strategy]An RSI filtered version of PJ Sutherland's Jaws Mean Reversion algorithm using volume weighted average price (VWAP) instead of simple moving average (SMA).

"Long" on the close when;

1-) 2 period VWAP closes 3% or more below the 5 period VWAP ,

2-) 5 period exponential average of the 2 period RSI is below 30.

"Exit Long" on the close when;

1-) 2 period VWAP closes above the 5 period VWAP.

"Short" on the close when;

1-) 2 period VWAP closes 3% or more above the 5 period VWAP ,

2-) 5 period exponential average of the 2 period RSI is above 70.

"Exit Short" on the close when;

1-) 2 period VWAP closes below the 5 period VWAP.

*** You can change the needed percentage for long and short trades, periods of VWAPs and RSI levels.

*** You can select the trend direction: "Long Only" , "Short Only" or "Both". Default is "Long Only".

I used the "VWAP with period" indicator code of @neolao. Special thanks to @neolao.

Indicator Link:

How to use Leverage and Margin in PineScriptEn route to being absolutely the best and most complete trading platform out there, TradingView has just closed 2 gaps in their PineScript language.

It is now possible to create and backtest a strategy for trading with leverage.

Backtester now produces Margin Calls - so recognizes mid-trade drawdown and if it is too big for the broker to maintain your trade, some part of if will be instantly closed.

New additions were announced in official blogpost , but it lacked code examples, so I have decided to publish this script. Having said that - this is purely educational stuff.

█ LEVERAGE

Let's start with the Leverage. I will discuss this assuming we are always entering trades with some percentage of our equity balance (default_qty_type = strategy.percent_of_equity), not fixed order quantity.

If you want to trade with 1:1 leverage (so no leverage) and enter a trade with all money in your trading account, then first line of your strategy script must include this parameter:

default_qty_value = 100 // which stands for 100%

Now, if you want to trade with 30:1 leverage, you need to multipy the quantity by 30x, so you'd get 30 x 100 = 3000:

default_qty_value = 3000 // which stands for 3000%

And you can play around with this value as you wish, so if you want to enter each trade with 10% equity on 15:1 leverage you'd get default_qty_value = 150.

That's easy. Of course you can modify this quantity value not only in the script, but also afterwards in Script Settings popup, "Properties" tab.

█ MARGIN

Second newly released feature is Margin calculation together with Margin Calls. If the market goes against your trades and your trading account cannot maintain mid-trade drawdown - those trades will be closed in full or partly. Also, if your trading account cannot afford to open more trades (pyramiding those trades), Margin mechanism will prevent them from being entered.

I will not go into details about how Margin calculation works, it was all explainged in above mentioned blogpost and documentation .

All you need to do is to add two parameters to the opening line of your script:

margin_long = 1./30*50, margin_short = 1./30*50

Whereas "30" is a leverage scale as in 30:1, and "50" stands for 50% of Margin required by your broker. Personally the Required Margin number I've met most often is 50%, so I'm using value 50 here, but there are literally 1000+ brokers in this world and this is individual decision by each of them, so you'd better ask yourself.

--------------------

Please note, that if you ever encounter a strategy which triggers Margin Call at least once, then it is probably a very bad strategy. Margin Call is a last resort, last security measure - all the risks should be calculated by the strategy algorithm before it is ever hit. So if you see a Margin Call being triggred, then something is wrong with risk management of the strategy. Therefore - don't use it!

HMA_ATR StrategyATR with HMA experimental minimalist bot for ETHBTC .

A strategy for use by Automated Algorithm systems.

Different from normal ATR as it uses HMA for smoothing.

Example settings result shown here on chart include commission 0.5%

72s Strat: Backtesting Adaptive HMA+ pt.1This is a follow up to my previous publication of Adaptive HMA+ few months ago, as a mean to provide some kind of initial backtesting tools. Which can be use to explore many possible strategies, optimise its settings to better conform user's pair/tf, and hopefully able to help tweaking your general strategy.

If you haven't read the study or use the indicator, kindly go here first to get the overall idea.

The first strategy introduce in this backtest is one most basic already described in the study; buy/sell is when movement is there and everything is on the right side; When RSI has turned to other side, we can use it as exit point (if in profit of course, else just let it hit our TP/SL, why would we exit before profit). Also, base on RSI when we make entry, we can further differentiate type of signals. --Please check all comments in code directly where the signals , entries , and exits section are.

Second additional strategy to check; is when we also use second faster Adaptive HMA+ for exit. So this is like a double orders on a signal but with different exit-rule (/more on this on snapshots below). Alternatively, you can also work the code so to only use this type of exit.

There's also an additional feature which you can enable its visuals, the Distance Zone , is to help measuring price distance to our xHMA+. It's just a simple atr based envelope really, I already put the sample code in study's comment section, but better gonna update it there directly for non-coder too, after this.

In this sample I use Lot for order quantity size just because that's what I use on my broker. Also what few friends use while we forward-testing it since the study is published, so we also checked/compared each profit/loss report by real number. To use default or other unit of measurement, change the entry code accordingly.

If you change your order size, you should also change the commission in Properties Tab. My broker commission is 5 USD per order/lot, so in there with example order size 0.1 lot I put commission 0.5$ per order (I'll put 2.5$ for 0.5 lot, 10$ for 2 lot, and so on). Crypto usually has higher charge. --It is important that you should fill it base on your broker.

SETTINGS

I'm trying to keep it short. Please explore it further again. (Beginner should also first get acquaintance with terms use here.)

ORDERS:

Base Minimum Profit Before Exit:

The number is multiplier of ongoing ATR. Means that when basic exit condition is met, algo will check whether you're already in minimum profit or not, if not, let it still run to TP or SL, or until it meets subsequent exit condition, then it will check again.

Default Target Profit:

Multiplier of ATR at signal. If reached before any eligible exit condition is met, exit TP.

Base StopLoss Point:

You can change directly in code to use other like ATR Trailing SL, fix percent SL, or whatever. In the sample, 4 options provided.

Maximum StopLoss:

This is like a safety-net, that if at some point your chosen SL point from input above happens to be exceeding this maximum input that you can tolerate, then this max point is the one will be use as SL.

Activate 2nd order...:

The additional doubling of certain buy/sell with different exits as described above. If enable, you should also set pyramiding to at least: 2. If not, it does nothing.

ADAPTIVE HMA+ PERIOD

Many users already have their own settings for these. So in here I only sample the default as first presented in the study. Make it to your adaptive.

MARKET MOVEMENT

(1) Now you can check in realtime how much slope degree is best to define your specific pair/tf is out of congestion (yellow) area. And (2) also able to check directly what ATR lengths are more suitable defining your pair's volatility.

DISTANCE ZONE

Distance Multiplier. Each pair/tf has its own best distance zone (in xHMA+ perspective). The zone also determine whether a signal should appear or not. (Or what type of signal, if you wanna go more detail in constructing your strategy)

USAGE

(Provided you already have your own comfortable settings for minimum-maximum period of Adaptive HMA+. Best if you already have backtested it manually too and/or apply as an add-on to your working strategy)

1. In our experiences, first most important to define is both elements in the Market Movement Settings . These also tend to be persistent for whole season since it's kinda describing that pair/tf overall behaviour. Don't worry if you still get a low Profit Factor here, but by tweaking you should start to see positive changes in one of Max Drawdown and Net Profit, or Percent Profitable.

2. Afterwards, find your pair/tf Distance Zone . When optimising this, what we seek is just a "not to bad" equity curves to start forming. At least Max Drawdown should lessen more. Doesn't have to be great already, but should be better, no red in Net Profit.

3. Then go manage the "Trailing Minimum Profit", TP, SL, and max SL.

4. Repeat 1,2,3. 👻

5. Manage order size, commission, and/or enable double-order (need pyramiding) if you like. Check if your equity can handle max drawdown before margin call.

6. After getting an acceptable backtest result, go to List of Trades tab and find the biggest loss or when many sequencing loss in a row happened. Click on it to go to exact point on chart, observe why the signal failed and get at least general idea how it can be prevented . The rest is yours, you should know your pair/tf more than other.

You can also re-explore your minimum-maximum period for both Major and minor xHMA+.

Keep in mind that all numbers in Setting are conceptually in a form of range . You don't want to get superb equity curves but actually a "fragile" , means one can easily turn it to disaster just by changing only a fraction in one/two of the setting.

---

If you just wanna test the strength of the indicator alone, you can disable "Use StopLoss" temporarily while optimising settings.

Using no SL might be tempting in overall result data in some cases, but NOTE: It is not recommended to not using SL, don't forget that we deliberately enter when it's in high volatility. If want to add flexibility or trading for long-term, just maximise your SL. ie.: chose SL Point>ATR only and set it maximum. (Check your max drawdown after this).

I think this is quite important specially for beginners, so here's an example; Hypothetically in below scenario, because of some settings, the buy order after the loss sell signal didn't appear. Let's say if our initial capital only 1000$ using leverage and order size 0,5 lot (risky position sizing already), moreover if this happens at the beginning of your trading season, that's half of account gone already in one trade . Your max SL should've made you exit after that pumping bar.

The Trailing Minimum Profit is actually look like this. Search in the code if you want to plot it. I just don't like too many lines on chart.

To maximise profit we can try enabling double-order. The only added rule coded is: RSI should rising when buy and falling when sell. 2nd signal will appears above or below default buy/sell signal. (Of course it's also prone to double-loss, re-check your max drawdown after. Profit factor play its part in here for a long run). Snapshot in comparison:

Two default sell signals on left closed at RSI exit, the additional sell signal closed later on when price crossover minor xHMA+. On buy side, price haven't met our minimum profit when first crossunder minor xHMA+. If later on we hit SL on this "+buy" signal, at least we already profited from default buy signal. You can also consider/treat this as multiple TP points.

For longer-term trading, what you need to maximise is the Minimum Profit , so it won't exit whenever an exit condition happened, it can happen several times before reaching minimum profit. Hopefully this snapshot can explain:

Notice in comparison default sell and buy signal now close in average after 3 days. What's best is when we also have confirmation from higher TF. It's like targeting higher TF by entering from smaller TF.

As also mention in the study, we can still experiment via original HMA by putting same value for minimum-maximum period setting. This is experimental EU 1H with Major xHMA+: 144-144, Flat market 13, Distance multiplier 3.6, with 2nd order activated.

Kiwi was a bit surprising for me. It's flat market is effectively below 6, with quite far distance zone of 3.5. Probably because I'm using big numbers in adaptive period.

---

The result you see in strategy tester report below for EURUSD 15m is using just default settings you see in code, as follow:

0,1 lot for each order (which is the smallest allowed by my broker).

No pyramiding. Commission: 0.5 usd per order. Slippage: 3

Opening position is only using basic strategy #1 (RSI exit). Additional exit not activated.

Minimum Profit: 1. TP: 3.

SL use: Half-distance zone. Max SL: 4.5.

Major xHMA+: 172-233. minor xHMA+: 89-121

Distance Zone Multiplier: 2.7

RSI: Standard 14.

(From our forward-testing, the difference we get from net profit is because of the spread, our entry isn't exactly at the close/open price. Not so much though, but not the same. If somebody can direct me to any example where we can code our entry via current bid/ask price, that would be awesome!)

It's already a long post (sorry), think I'm gonna pause here. Check out the code :)

---

DISCLAIMER: Past performance is no guarantee of future results , and so on.. you know the drill ;)

Please read whole description first before using, don't take 1-2 paragraph and claim it's the whole logic, you are responsible of your own actions and understanding.

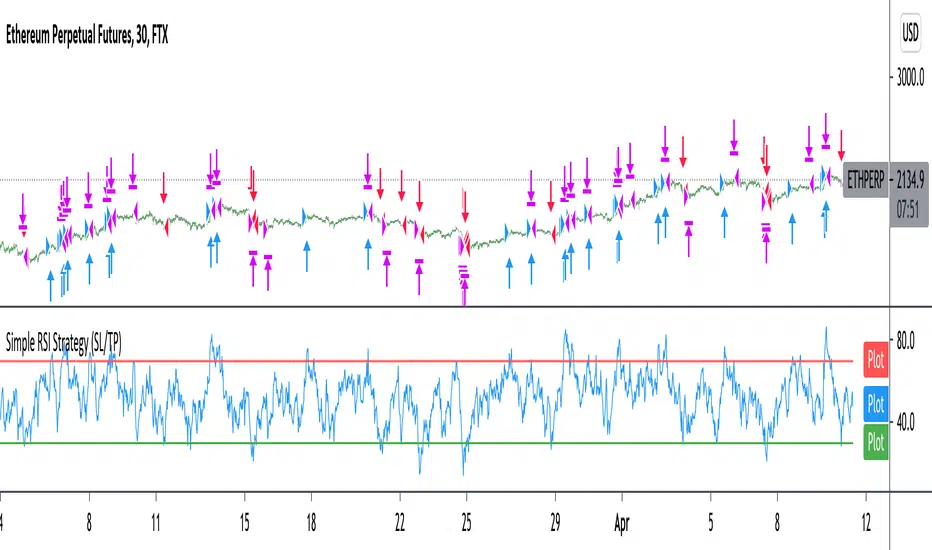

Improved simple RSI Buy/Sell at a level (SL/TP)Improved Simple Strategy based on RSI, using overbought or oversold levels.

Backtest: ETHPERP (FTX) - 30m

Set STOP LOSS and GET PROFIT as a percentage (2% and 10% by default).

If strategy.position_size != 0 algorithm convert percentages into points and set stop loss and take profit limit orders.

MACD 50x Leveraged Strategy Real Equity Simulation Hello, I wrote this script to merge the two scripts I shared before.

The aim here is to see the real value of the state of the capital as a result of leveraged transactions and to combine both long and short directions.

Scripts :

MACD Long 50x Leverage Strategy :

MACD Short 50x Leverage Strategy :

The parameters have not changed so they are the same as the previous two scripts:

Adding margin: Forbidden or not specified. (Add Margin : No)

Position Size : %1 (0.01) (For each trade)

Stop-Loss : %2 (For each trade)

Long : Crossover(delta,0) (Standard MACD)

Long Exit : Long Stop Level or Short Entry

(In the case of Long Stop, all trades are closed and no positions are opened in short direction.)

Short : Crossunder(delta,0) (Standard MACD)

Short Exit : Short Stop or Long Entry

(In the case of Short Stop, all trades are closed and no positions are opened in the long direction.)

NOTE :

This is a simulation made using standard parameters, showing the state of the balance in very simple rules with leveraged transactions only.

The nice thing here is the direct observation of the results by making modifications on the strategy parameters.

Regards.

JetzGiantz StrategyThe algorithm for this strategy was provided by JetzGiantz.

It creates buy and sell signals based on the close and open prices of the previous 3 bars, and compares them to the lowest low, or highest high, between the last 3 and 50 bars.

You can select the month and year you wish to backtest.

You can enter the SL and TP values.

There are no other inputs.

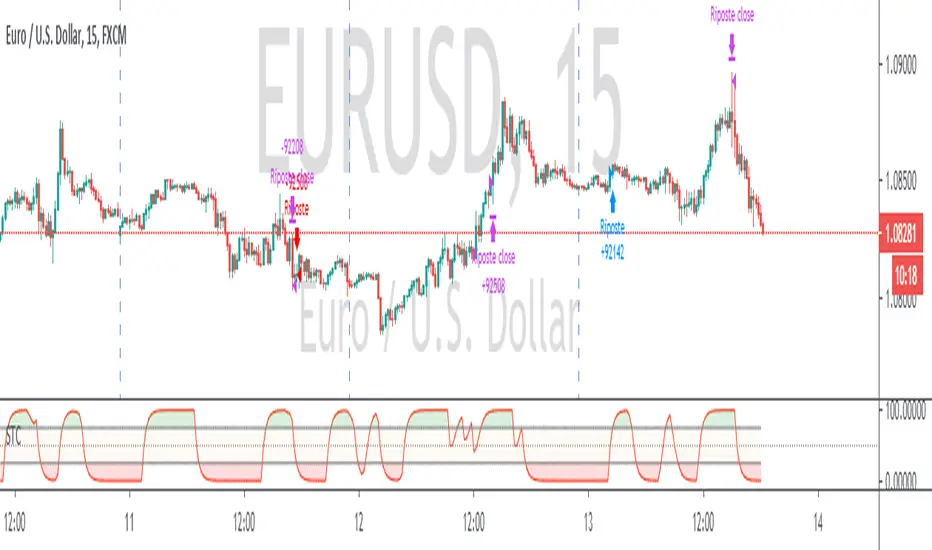

TradingView Alerts to MT4 MT5 - Forex, indices, commoditiesHowdy Algo-Traders! This example script has been created for educational purposes - to present how to use and automatically execute TradingView Alerts on real markets.

I'm posting this script today for a reason. TradingView has just released a new feature of the PineScript language - ALERT() function. Why is it important? It is finally possible to set alerts inside PineScript strategy-type script, without the need to convert the script into study-type. You may say triggering alerts straight from strategies was possible in PineScript before (since June 2020), but it had its limitations. Starting today you can attach alert to any custom event you might want to include in your PineScript code.

With the new feature, it is easier not only to execute strategies, but to maintain codebase - having to update 2 versions of the code with each single modification was... ahem... inconvenient. Moreover, the need to convert strategy into study also meant it was required to rip the code from all strategy...() calls, which carried a lot of useful information, like entry price, position size, and more, definitely influencing results calculated by strategy backtest. So the strategy without these features very likely produced different results than with them. While it was possible to convert these features into study with some advanced "coding gymnastics", it was also quite difficult to test whether those gymnastics didn't introduce serious, bankrupting bugs.

//////

How does this new feature work? It is really simple. On your custom events in the code like "GoLong" or "GoShort", create a string variable containing all the values you need inside your alert and this string variable will be your alert's message. Then, invoke brand new alert() function and that's it (see lines 67 onwards in the script). Set it up in CreateAlert popup and enjoy. Alerts will trigger on candle close as freq= parameter specifies. Detailed specification of the new alert() function can be found in TradingView's PineScript Reference (www.tradingview.com), but there's nothing more than message= and freq= parameters. Nothing else is needed, it is very simple. Yet powerful :)

//////

Alert syntax in this script is prepared to work with TradingConnector. Strategy here is not too complex, but also not the most basic one: it includes full exits, partial exits, stop-losses and it also utilizes dynamic variables calculated by the code (such as stop-loss price). This is only an example use case, because you could handle variety of other functionalities as well: conditional entries, pending entries, pyramiding, hedging, moving stop-loss to break-even, delivering alerts to multiple brokers and more.

//////

This script is a spin-off from my previous work, posted over a year ago here: Some comments on strategy parameters have been discussed there, but let me copy-paste most important points:

* Commission is taken into consideration.

* Slippage is intentionally left at 0. Due to shorter than 1 second delivery time of TradingConnector, slippage is practically non-existing.

* This strategy is NON-REPAINTING and uses NO TRAILING-STOP or any other feature known to be causing problems.

* The strategy was backtested on EURUSD 6h timeframe, will perform differently on other markets and timeframes.

Despite the fact this strategy seems to be still profitable, it is not guaranteed it will continue to perform well in the future. Remember the no.1 rule of backtesting - no matter how profitable and good looking a script is, it only tells about the past. There is zero guarantee the same strategy will get similar results in the future.

Full specs of TradingView alerts and how to set them up can be found here: www.tradingview.com

OCC Trend Combo 1 day BTC MoonflagRuns on BTC 1 DAY (NOTE USE THIS NOT THE PREVIOUS VERSION - DEFAULTS TUNED TO 1 day BTC HERE)

USE DEFAULT SETTINGS

The strategy is to maximise the profit for OCC longs (ALMA algo)

Longs start when the price action settles around the ALMA OCC, then typically breaks up

Then follow the trend indcator (blue/orange)

Shorts normally happen when the price action crosses below the ALMA OCC, although these initiate faster than the 1 day time setting - so watchout for shorts - are harder to predict than longs

So this catches most of the big move longs at their initiation

Custom Triple Moving Average Strategy | Auto BacktestingCreate your own MA Strategy set of up to three moving averages!

Auto Backtesting.

Cloud between MA1 and MA2.

Many different MA types to choose from.

Totally Custom!

Happy Trading, and algorithm analysis!

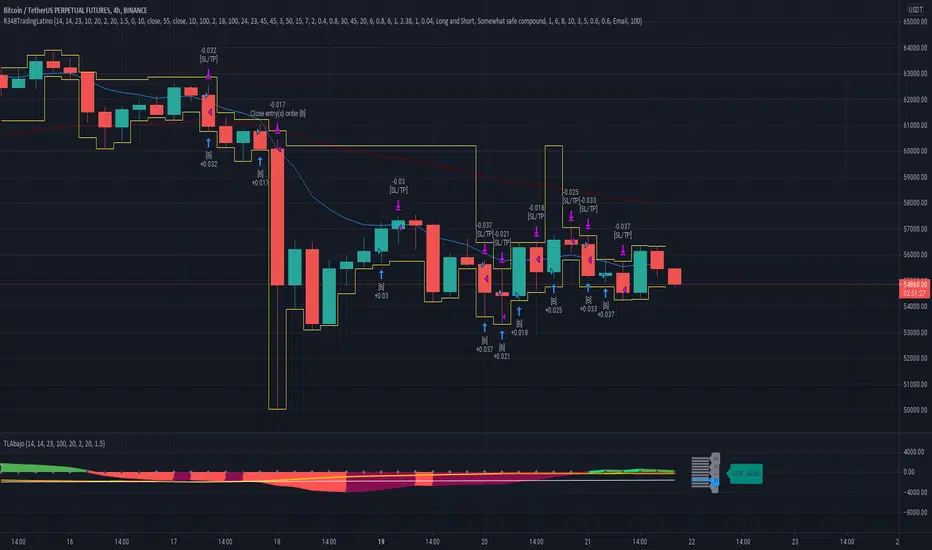

Ruckard TradingLatinoThis strategy tries to mimic TradingLatino strategy.

The current implementation is beta.

Si hablas castellano o espanyol por favor consulta MENSAJE EN CASTELLANO más abajo.

It's aimed at BTCUSDT pair and 4h timeframe.

STRATEGY DEFAULT SETTINGS EXPLANATION

max_bars_back=5000 : This is a random number of bars so that the strategy test lasts for one or two years

calc_on_order_fills=false : To wait for the 4h closing is too much. Try to check if it's worth entering a position after closing one. I finally decided not to recheck if it's worth entering after an order is closed. So it is false.

calc_on_every_tick=false

pyramiding=0 : We only want one entry allowed in the same direction. And we don't want the order to scale by error.

initial_capital=1000 : These are 1000 USDT. By using 1% maximum loss per trade and 7% as a default stop loss by using 1000 USDT at 12000 USDT per BTC price you would entry with around 142 USDT which are converted into: 0.010 BTC . The maximum number of decimal for contracts on this BTCUSDT market is 3 decimals. E.g. the minimum might be: 0.001 BTC . So, this minimal 1000 amount ensures us not to entry with less than 0.001 entries which might have happened when using 100 USDT as an initial capital.

slippage=1 : Binance BTCUSDT mintick is: 0.01. Binance slippage: 0.1 % (Let's assume). TV has an integer slippage. It does not have a percentage based slippage. If we assume a 1000 initial capital, the recommended equity is 142 which at 11996 USDT per BTC price means: 0.011 BTC. The 0.1% slippage of: 0.011 BTC would be: 0.000011 . This is way smaller than the mintick. So our slippage is going to be 1. E.g. 1 (slippage) * 0.01 (mintick)

commission_type=strategy.commission.percent and commission_value=0.1 : According to: binance . com / en / fee / schedule in VIP 0 level both maker and taker fees are: 0.1 %.

BACKGROUND

Jaime Merino is a well known Youtuber focused on crypto trading

His channel TradingLatino

features monday to friday videos where he explains his strategy.

JAIME MERINO STANCE ON BOTS

Jaime Merino stance on bots (taken from memory out of a 2020 June video from him):

'~

You know. They can program you a bot and it might work.

But, there are some special situations that the bot would not be able to handle.

And, I, as a human, I would handle it. And the bot wouldn't do it.

~'

My long term target with this strategy script is add as many

special situations as I can to the script

so that it can match Jaime Merino behaviour even in non normal circumstances.

My alternate target is learn Pine script

and enjoy programming with it.

WARNING

This script might be bigger than other TradingView scripts.

However, please, do not be confused because the current status is beta.

This script has not been tested with real money.

This is NOT an official strategy from Jaime Merino.

This is NOT an official strategy from TradingLatino . net .

HOW IT WORKS

It basically uses ADX slope and LazyBear's Squeeze Momentum Indicator

to make its buy and sell decisions.

Fast paced EMA being bigger than slow paced EMA

(on higher timeframe) advices going long.

Fast paced EMA being smaller than slow paced EMA

(on higher timeframe) advices going short.

It finally add many substrats that TradingLatino uses.

SETTINGS

__ SETTINGS - Basics

____ SETTINGS - Basics - ADX

(ADX) Smoothing {14}

(ADX) DI Length {14}

(ADX) key level {23}

____ SETTINGS - Basics - LazyBear Squeeze Momentum

(SQZMOM) BB Length {20}

(SQZMOM) BB MultFactor {2.0}

(SQZMOM) KC Length {20}

(SQZMOM) KC MultFactor {1.5}

(SQZMOM) Use TrueRange (KC) {True}

____ SETTINGS - Basics - EMAs

(EMAS) EMA10 - Length {10}

(EMAS) EMA10 - Source {close}

(EMAS) EMA55 - Length {55}

(EMAS) EMA55 - Source {close}

____ SETTINGS - Volume Profile

Lowest and highest VPoC from last three days

is used to know if an entry has a support

VPVR of last 100 4h bars

is also taken into account

(VP) Use number of bars (not VP timeframe): Uses 'Number of bars {100}' setting instead of 'Volume Profile timeframe' setting for calculating session VPoC

(VP) Show tick difference from current price {False}: BETA . Might be useful for actions some day.

(VP) Number of bars {100}: If 'Use number of bars (not VP timeframe)' is turned on this setting is used to calculate session VPoC.

(VP) Volume Profile timeframe {1 day}: If 'Use number of bars (not VP timeframe)' is turned off this setting is used to calculate session VPoC.

(VP) Row width multiplier {0.6}: Adjust how the extra Volume Profile bars are shown in the chart.

(VP) Resistances prices number of decimal digits : Round Volume Profile bars label numbers so that they don't have so many decimals.

(VP) Number of bars for bottom VPOC {18}: 18 bars equals 3 days in suggested timeframe of 4 hours. It's used to calculate lowest session VPoC from previous three days. It's also used as a top VPOC for sells.

(VP) Ignore VPOC bottom advice on long {False}: If turned on it ignores bottom VPOC (or top VPOC on sells) when evaluating if a buy entry is worth it.

(VP) Number of bars for VPVR VPOC {100}: Number of bars to calculate the VPVR VPoC. We use 100 as Jaime once used. When the price bounces back to the EMA55 it might just bounce to this VPVR VPoC if its price it's lower than the EMA55 (Sells have inverse algorithm).

____ SETTINGS - ADX Slope

ADX Slope

help us to understand if ADX

has a positive slope, negative slope

or it is rather still.

(ADXSLOPE) ADX cut {23}: If ADX value is greater than this cut (23) then ADX has strength

(ADXSLOPE) ADX minimum steepness entry {45}: ADX slope needs to be 45 degrees to be considered as a positive one.

(ADXSLOPE) ADX minimum steepness exit {45}: ADX slope needs to be -45 degrees to be considered as a negative one.

(ADXSLOPE) ADX steepness periods {3}: In order to avoid false detection the slope is calculated along 3 periods.

____ SETTINGS - Next to EMA55

(NEXTEMA55) EMA10 to EMA55 bounce back percentage {80}: EMA10 might bounce back to EMA55 or maybe to 80% of its complete way to EMA55

(NEXTEMA55) Next to EMA55 percentage {15}: How much next to the EMA55 you need to be to consider it's going to bounce back upwards again.

____ SETTINGS - Stop Loss and Take Profit

You can set a default stop loss or a default take profit.

(STOPTAKE) Stop Loss % {7.0}

(STOPTAKE) Take Profit % {2.0}

____ SETTINGS - Trailing Take Profit

You can customize the default trailing take profit values

(TRAILING) Trailing Take Profit (%) {1.0}: Trailing take profit offset in percentage

(TRAILING) Trailing Take Profit Trigger (%) {2.0}: When 2.0% of benefit is reached then activate the trailing take profit.

____ SETTINGS - MAIN TURN ON/OFF OPTIONS

(EMAS) Ignore advice based on emas {false}.

(EMAS) Ignore advice based on emas (On closing long signal) {False}: Ignore advice based on emas but only when deciding to close a buy entry.

(SQZMOM) Ignore advice based on SQZMOM {false}: Ignores advice based on SQZMOM indicator.

(ADXSLOPE) Ignore advice based on ADX positive slope {false}

(ADXSLOPE) Ignore advice based on ADX cut (23) {true}

(STOPTAKE) Take Profit? {false}: Enables simple Take Profit.

(STOPTAKE) Stop Loss? {True}: Enables simple Stop Loss.

(TRAILING) Enable Trailing Take Profit (%) {True}: Enables Trailing Take Profit.

____ SETTINGS - Strategy mode

(STRAT) Type Strategy: 'Long and Short', 'Long Only' or 'Short Only'. Default: 'Long and Short'.

____ SETTINGS - Risk Management

(RISKM) Risk Management Type: 'Safe', 'Somewhat safe compound' or 'Unsafe compound'. ' Safe ': Calculations are always done with the initial capital (1000) in mind. The maximum losses per trade/day/week/month are taken into account. ' Somewhat safe compound ': Calculations are done with initial capital (1000) or a higher capital if it increases. The maximum losses per trade/day/week/month are taken into account. ' Unsafe compound ': In each order all the current capital is gambled and only the default stop loss per order is taken into account. That means that the maximum losses per trade/day/week/month are not taken into account. Default : 'Somewhat safe compound'.

(RISKM) Maximum loss per trade % {1.0}.

(RISKM) Maximum loss per day % {6.0}.

(RISKM) Maximum loss per week % {8.0}.

(RISKM) Maximum loss per month % {10.0}.

____ SETTINGS - Decimals

(DECIMAL) Maximum number of decimal for contracts {3}: How small (3 decimals means 0.001) an entry position might be in your exchange.

EXTRA 1 - PRICE IS IN RANGE indicator

(PRANGE) Print price is in range {False}: Enable a bottom label that indicates if the price is in range or not.

(PRANGE) Price range periods {5}: How many previous periods are used to calculate the medians

(PRANGE) Price range maximum desviation (%) {0.6} ( > 0 ): Maximum positive desviation for range detection

(PRANGE) Price range minimum desviation (%) {0.6} ( > 0 ): Mininum negative desviation for range detection

EXTRA 2 - SQUEEZE MOMENTUM Desviation indicator

(SQZDIVER) Show degrees {False}: Show degrees of each Squeeze Momentum Divergence lines to the x-axis.

(SQZDIVER) Show desviation labels {False}: Whether to show or not desviation labels for the Squeeze Momentum Divergences.

(SQZDIVER) Show desviation lines {False}: Whether to show or not desviation lines for the Squeeze Momentum Divergences.

EXTRA 3 - VOLUME PROFILE indicator

WARNING: This indicator works not on current bar but on previous bar. So in the worst case it might be VP from 4 hours ago. Don't worry, inside the strategy calculus the correct values are used. It's just that I cannot show the most recent one in the chart.

(VP) Print recent profile {False}: Show Volume Profile indicator

(VP) Avoid label price overlaps {False}: Avoid label prices to overlap on the chart.

EXTRA 4 - ZIGNALY SUPPORT

(ZIG) Zignaly Alert Type {Email}: 'Email', 'Webhook'. ' Email ': Prepare alert_message variable content to be compatible with zignaly expected email content format. ' Webhook ': Prepare alert_message variable content to be compatible with zignaly expected json content format.

EXTRA 5 - DEBUG

(DEBUG) Enable debug on order comments {False}: If set to true it prepares the order message to match the alert_message variable. It makes easier to debug what would have been sent by email or webhook on each of the times an order is triggered.

HOW TO USE THIS STRATEGY

BOT MODE: This is the default setting.

PROPER VOLUME PROFILE VIEWING: Click on this strategy settings. Properties tab. Make sure Recalculate 'each time the order was run' is turned off.

NEWBIE USER: (Check PROPER VOLUME PROFILE VIEWING above!) You might want to turn on the 'Print recent profile {False}' setting. Alternatively you can use my alternate realtime study: 'Resistances and supports based on simplified Volume Profile' but, be aware, it might consume one indicator.

ADVANCED USER 1: Turn on the 'Print price is in range {False}' setting and help us to debug this subindicator. Also help us to figure out how to include this value in the strategy.

ADVANCED USER 2: Turn on the all the (SQZDIVER) settings and help us to figure out how to include this value in the strategy.

ADVANCED USER 3: (Check PROPER VOLUME PROFILE VIEWING above!) Turn on the 'Print recent profile {False}' setting and report any problem with it.

JAIME MERINO: Just use the indicator as it comes by default. It should only show BUY signals, SELL signals and their associated closing signals. From time to time you might want to check 'ADVANCED USER 2' instructions to check that there's actually a divergence. Check also 'ADVANCED USER 1' instructions for your amusement.

EXTRA ADVICE

It's advised that you use this strategy in addition to these two other indicators:

* Squeeze Momentum Indicator

* ADX

so that your chart matches as close as possible to TradingLatino chart.

ZIGNALY INTEGRATION

This strategy supports Zignaly email integration by default. It also supports Zignaly Webhook integration.

ZIGNALY INTEGRATION - Email integration example

What you would write in your alert message:

||{{strategy.order.alert_message}}||key=MYSECRETKEY||

ZIGNALY INTEGRATION - Webhook integration example

What you would write in your alert message:

{ {{strategy.order.alert_message}} , "key" : "MYSECRETKEY" }

CREDITS

I have reused and adapted some code from

'Directional Movement Index + ADX & Keylevel Support' study

which it's from TradingView console user.

I have reused and adapted some code from

'3ema' study

which it's from TradingView hunganhnguyen1193 user.

I have reused and adapted some code from

'Squeeze Momentum Indicator ' study

which it's from TradingView LazyBear user.

I have reused and adapted some code from

'Strategy Tester EMA-SMA-RSI-MACD' study

which it's from TradingView fikira user.

I have reused and adapted some code from

'Support Resistance MTF' study

which it's from TradingView LonesomeTheBlue user.

I have reused and adapted some code from

'TF Segmented Linear Regression' study

which it's from TradingView alexgrover user.

I have reused and adapted some code from

"Poor man's volume profile" study

which it's from TradingView IldarAkhmetgaleev user.

FEEDBACK

Please check the strategy source code for more detailed information

where, among others, I explain all of the substrats

and if they are implemented or not.

Q1. Did I understand wrong any of the Jaime substrats (which I have implemented)?

Q2. The strategy yields quite profit when we should long (EMA10 from 1d timeframe is higher than EMA55 from 1d timeframe.

Why the strategy yields much less profit when we should short (EMA10 from 1d timeframe is lower than EMA55 from 1d timeframe)?

Any idea if you need to do something else rather than just reverse what Jaime does when longing?

FREQUENTLY ASKED QUESTIONS

FAQ1. Why are you giving this strategy for free?

TradingLatino and his fellow enthusiasts taught me this strategy. Now I'm giving back to them.

FAQ2. Seriously! Why are you giving this strategy for free?

I'm confident his strategy might be improved a lot. By keeping it to myself I would avoid other people contributions to improve it.

Now that everyone can contribute this is a win-win.

FAQ3. How can I connect this strategy to my Exchange account?

It seems that you can attach alerts to strategies.

You might want to combine it with a paying account which enable Webhook URLs to work.

I don't know how all of this works right now so I cannot give you advice on it.

You will have to do your own research on this subject. But, be careful. Automating trades, if not done properly,

might end on you automating losses.

FAQ4. I have just found that this strategy by default gives more than 3.97% of 'maximum series of losses'. That's unacceptable according to my risk management policy.

You might want to reduce default stop loss setting from 7% to something like 5% till you are ok with the 'maximum series of losses'.

FAQ5. Where can I learn more about your work on this strategy?

Check the source code. You might find unused strategies. Either because there's not a substantial increases on earnings. Or maybe because they have not been implemented yet.

FAQ6. How much leverage is applied in this strategy?

No leverage.

FAQ7. Any difference with original Jaime Merino strategy?

Most of the times Jaime defines an stop loss at the price entry. That's not the case here. The default stop loss is 7% (but, don't be confused it only means losing 1% of your investment thanks to risk management). There's also a trailing take profit that triggers at 2% profit with a 1% trailing.

FAQ8. Why this strategy return is so small?

The strategy should be improved a lot. And, well, backtesting in this platform is not guaranteed to return theoric results comparable to real-life returns. That's why I'm personally forward testing this strategy to verify it.

MENSAJE EN CASTELLANO

En primer lugar se agradece feedback para mejorar la estrategia.

Si eres un usuario avanzado y quieres colaborar en mejorar el script no dudes en comentar abajo.

Ten en cuenta que aunque toda esta descripción tenga que estar en inglés no es obligatorio que el comentario esté en inglés.

CHISTE - CASTELLANO

¡Pero Jaime!

¡400.000!

¡Tu da mun!

BV's MACD SIGNAL TESTERHello ladies and gentlemen,

Today, as you may have seen in the title, I have coded a strategy to determine once and for all if MACD could make you money in 2020.

So, at the end of this video, you will know which MACD strategy will bring you the most money.

Spoiler alert: we've hit the 90% WinRAte mark on the Euro New Zealand Dollar chart.

I've seen a lot of videos of people testing different MACD signals, some up to 100 times.

But In my opinion, all traders must rely on statistics to put all the odds on their side and good statistics require a lot more data.

The algorithm I'm showing you tests each signal one by one over a 3 year period and on 28 different graphs.

That way we are sure that we have encountered all possible market behavior.

From phases of congestion to major trends or even the effects of COVID-19

I use the ATR to determine my Stop Loss and Take Profits. The Stop Loss is placed at 1.5 times the ATR, the Take Profit is placed at 1 time the ATR.

If my Take Profit is hit, I take 50% of the profits and let the position run by moving my Stop Loss to Zero.

This way, the position can no longer be a losing position.

If you are not familiar with this practice, I invite you to study the "Scaling out" video from the NoNonsenseForex channel.

BV's Trading Journal.

Twin Range Filter Algo@Colinmck used two different ranges to generate signals. Read his release notes to find out what the original script does.

I added one condition which seems to increase performance on 15m BTCUSD as well as 1h BTCUSD and that is ATR with 32 periods being smaller than ATR with 64 periods. I used my script Volatility Optimiser to discover this tendency.

Both buying and selling conditions are same as in @Colinmck's script plus one condition of my own. You can disable my condition.

Target and stop-loss are manually set values in ticks.

Time stop-loss is manually set value in a number of candles. After this number of candles, a position always exits (or should 😇). You can disable it by inserting a very long period. I do not recommend it, because a value of indicator should not be measured in luck and if market starts moving in the direction after 40 periods, the predictive capability of an indicator is questionable.

I used 300/150/17 for 15m BTCUSD chart and 900/30/17 for 1h BTCUSD. I didn't try to optimize any other parameters for these periods.

Since this script relies mostly on volatility for its prediction, I wouldn't recommend using it on its own. Individual approach to the market is recommended. Also, it didn't work on EURUSD when using the same default values and different order management (tp, sl, time sl), so it is probably not as versatile.

Let me know what do you think of this strategy. If you have some ideas about how to make it more reliable, share it in the comments, I might put it to the test. Good luck 🍀

Schaff Trend Cycle + Double MAThis strategy uses two different moving averages to determine a trend. It opens a position on a pullback from a trend.

Conditions for buy signal are:

►Crossover out of Shaff Trend Cycle's extreme levels

►The price is above its short period exponential moving average.

►A short period exponential moving average is above a long period exponential moving average.

*Conditions for sell are the opposite.

All in all, I don't think it needs to be on your chart but it can be optimized and even successful on some timeframes.

Shaff Trend Cycle solution was provided by @everget, I converted his script to Pine v.4, added exponential averages and created an algorithm for backtesting.

StarbuxI made this in starbucks .

Bullish hammer trading signal algorithm

using MACD for trend determination and holding period.

Underworld Hunter Backtesting AlgorhitmThis strategy is built to prove the profitability of my Underworld Hunter indicator . It tests two different strategies. I won't be going into the calculation again since it is part of the original script. I just made a few adjustments.

First one is clearly visual. It plots slimmer twin-coloured lines now and has a different colour for every extreme level. Second is less obvious - I switched Relative Strength Index for Commodity Channel Index.

Extreme levels are as follows: green 100 -► 120, yellow 120 -► 140, orange 140 -► 160, red 160 -► 180 and purple above 180, I will have a special separate algorithm for testing optimal CCI levels someday, in this script, these values are only meant to help you with manual operations and do not influence results of the strategy in any way.

#Trending strategy

The trending strategy opens a position whenever the price leaves the bands and holds it until two consecutive bars are closed within the bands. The picture shows one winning position that hasn't yet been resulted. It also shows a few fakeouts. For this strategy, you want to keep the length below 110, the deviation should be below 2 and you probably want to play lower timeframes.

#Within the bands

The second strategy is pretty much the opposite. It opens a position when the price reaches outer bands and holds it until two consecutive bars are closed within the bands and current bar closes below previous bars low in case of long. It is working on hourly timeframes and you need higher length and deviation to succeed. The picture shows a few positions on EURUSD. Each of them is profitable but would be much higher if you closed it manually when it was time. You need to enable this strategy, which automatically disables the other one.

When using my script, you need to bear in mind that the first strategy doesn't detect optimal levels to close the price. A trend is often followed by a less volatile and boring correction which causes bands to shrink and lower your profits if you don't close manually as it will take longer till bands are reached.

On the other hand, second script literally has no stop-loss. As long as the price is outside the range, it will never close which will cause major drawdowns, unless you control the trade manually. CCI is here to help you with both.

I also recommend combining this with Market Profile (on TW, there is only Volume Profile, which can be used in a similar way) and trading day theory (trending with multiple distributions, trending day, normal day, a variation on a normal day, non-trending day or neutral day). Always keep in mind that it is up to traders to be profitable, indicators can support a good trader, but they will not fix a bad one.

GMS: RSI StrategyThis is just a basic RSI strategy that it easy to use and quite comprehensive so you can quickly test out an idea based on RSI.

- I made it comprehensive in that you can select long, short, or both.

- There is a simple moving average trend filter. You can filter for trades above, below, or don't include it at all.

- The exit is based on a simple moving average.

The source code should be open if you want to see it or modify it for your own project. I hope it helps!

Andre

Global Market Signals

BEST Engulfing + Breakout StrategyHello traders

This is a simple algorithm for a Tradingview strategy tracking a convergence of 2 unrelated indicators.

Convergence is the solution to my trading problems.

It's a puzzle with infinite possibilities and only a few working combinations.

Here's one that I like

- Engulfing pattern

- Price vs Moving average for detecting a breakout

Definition

Take out the notebooks :) and some coffee (good for focus). I'm bullish in coffee

The engulfing pattern is a two-candle reversal pattern.

The second candle completely ‘engulfs’ the real body of the first one, without regard to the length of the tail shadows.

The bullish Engulfing pattern appears in a downtrend and is a combination of one red candle followed by a larger green candle

The bearish Engulfing pattern appears in a downtrend and is a combination of one green candle followed by a larger red candle

Example: imgur.com

We're bored sir... what's the point of all this?

In summary, an engulfing is a pattern to track reversals. (the whole TradingView audience stands up now giving a standing ovation)

Adding the Price vs Moving average filters allows to track reversals with momentums (half of the audience collapsed because this is too awesome)

Ok sir... you picked up my interest

I included some cool backtest filters:

- date range filtering

- flexible take profit in USD value (plotted in blue)

- flexible stop loss in USD value (plotted in red)

All the best

Dave

Stochastic Pop and Drop by Jake Bernstein v1 [Bitduke]I found a simple strategy by Jake Bernstein, modified it a little and created a strategy with Risk Management System (SL+TP); After that I test it on the different cryptocurrency pairs.

About the Indicator

Basically it's the strategy of 2 indicators: Stochastic Oscillator to define the bias and Average Directional Index to confirm it.

One again, It uses Stochastic Oscillator to define the trading bias. In particular, the trading bias was deemed bullish when the weekly 14-period Stochastic Oscillator was above some default value (in him paper - 50) and rising and vice versa.

Once the trading bias is established, Steckler used the Average Directional Index (ADX) to define a slowdown in the trend. ADX measures the strength of the trend and a move below 20 signals a weak trend.

Modifications

I didn't implement Average Directional Index (ADX) and test just different sources for data, oscillator periods and different levels in relation to the crypto market.

So, it shows good results with two tight thresholds at 55 and 45 level.

The bar chart below the defining the bullish and bearish periods (green and red) and gives a signal to enter the trade (purple bars).

Backtesting

Backtested on XBTUSD , BTCPERP (FTX) pairs. You may notice it shows good results on 3h timeframe.

Relatively low drawdown

~ 10% (from 2019 to date) FTX

~ 22% (4 years from 2016) Bitmex

I backtested on the different altcoin pairs as well, but the results were just not good.

Relatively good results were shown by some index pairs from the FTX exchange ( FTX:SHITPERP ), but I think there is a few data for backtesting to be asure in them.

Bitmex 3h (2017 - 2020) :

i.imgur.com

FTX 3h (2019 - 2020):

i.imgur.com

Possible Improvements

- Regarding trading algorithm it would be good to check with strategy with ADX somehow. Maybe for the better entries

- As for Risk Management system, it can be improved by adding trailing stop to the strategy.

Link: school.stockcharts.com

DAX Shooter 5M StrategyThis is a simple strategy that applies very well for scaling indices to 5 minutes especially for the DAX. The algorithm provides for buying or selling when the market is very "pulled". The rules are as follows:

you buy when:

1- The ADX indicator with the standard settings is greater than 32.

2- the RSI indicator set to 7 periods is crossing upwards the oversold line at 30

3- the candle minimum is lower than the lower band of bollinger bands set to 50 periods.

is sold when:

1- ADX indicator with standard settings is greater than 32.

2 - the RSI indicator set to 7 periods is crossing downwards the overbought line at 70

3- the maximum of the candle is higher than the upper band of the bollinger bands set to 50 periods.

Money management is at the discretion of the trader but usually it is better to set a fixed stop loss and a take profit on reaching the opposite bollinger band.

Enjoy trading at all!

QuantCat Mom Finder Strategy (1H)QuantCat Momentum Finder Strategy

This strategy is designed to be used on the 1 hour time frame, on all x/btc pairs.

The beautiful thing is it plots the take profit, and stoploss for you for each entry- where I would say use the stoploss for sure and feel with water with how the price action is looking when in profit.

In this strategy, I actually implemented my own trading style into building the strategy. Having to replicate my own trading strategy into an algorithm, I can't make it exactly perfect to how I would trade, but what I can do is try and program the parameters that give it the absolute best chance of making a big move with a small drawdown- which replicates part of my momentum trading style. Here I am using RSI, MACD, EMA and trend filtering values to find moments where there has been a momentum change to play the rest of the move. It only picks the best entries.

There is always a 3-4 R/R move on average with with these trades, meaning 1 in 4 only need to hit to be a break even trader- where most of these strategies have about 35% hit rate.

The stoploss is so crucial to minimise any damage from huge unexpected candles, the strategies can just be used for entries as well, you don't have to stick to the exact formula- of the long and short system, but this by itself is profitable.

The system nets positive results on

-ETH/BTC

-LTC/BTC

-XRP/BTC

-ADA/BTC

-NEO/BTC etc.

We also have a free 15M strategy available too.

You can join our discord server to get live alerts for the strategy as well as speak to our devs! Link in signature below!!!