S&P 500 Daily Chart Analysis For Week of Oct 17, 2025Technical Analysis and Outlook:

Last week's trading session was marked by significant volatility in the S&P 500 Index, which experienced pronounced price fluctuations following its descent to our established Mean Support level of 6550. This level served as a critical point for market participants, triggering a series of rapid buying and selling activities that contributed to the index's overall gyrations.

At present, the index is positioned just below the newly established Mean Resistance level of 6671, which indicates the potential for further upward momentum, as this trend suggests a Well-built extension to the subsequent Mean Support level of 6550.

Contrariwise, it is essential to acknowledge and be aware of the emergence of the unexpected market drop to the Mean Support 6550, 6485, 6371, and the Key Support level of 6240. Additionally, it's crucial to take note of the Auxiliary Inner Rebounds occurring at these critical points.

Trade ideas

S&P 500 at the Golden Support – Bounce or Breakdown?Short-Term View:

S&P 500 is testing its 50-day moving average near 6,470 after a recent correction from 6,800. A strong bullish reaction from this zone could push prices toward 6,850 → 7,000.

If the index closes below 6,550, short-term momentum turns bearish and a drop toward 6,400 becomes likely.

Long-Term View:

The broader trend remains bullish as long as price holds above 6,470–6,145.

Breaking below 6,145 would confirm a larger correction toward 6,000–5,800, while holding above this zone keeps the path open for new highs near 7,200.

Summary:

S&P 500 stands at a key technical decision zone — the market is deciding whether to resume its bullish trend or start a mid-term correction.

$SPX500 by all metrix this is overboughtMarkets can stay irrational longer than we can stay solvent. Right now, we’re at the top of this megaphone pattern, with everything extremely overbought in epic fashion.

⚠️ Caution: the odds of a serious correction are high — the chart points to a potential target around $5,650.

Sure, the madness can continue. The Fed can keep printing USD that pours into stocks instead of the real economy — until people are jobless, starving, and rioting for food.

📈 Enjoy the rally while it lasts, but use stop-losses. This market is dangerously overheated.

Analysis of S&P.Here’s the status of the top 500 companies in the U.S. because of Trump’s crazy moves. What kind of analysis can you do with this chart? Trump has messed up all the markets.

SPX long term channelThe channel is well formed. But for me the criteria for a completed channel is 5 alternating touches, generally clean unless market is volatile in which case line sorts them out

So red is top rail completion or due

Blue is top rail completion or due

Not financial advice

SPX short term roadmapPath says it all. Not financial advice. Will show zoomed out channel in another post.

S&P 500 May Show Signs of FatigueS&P 500 has rallied steadily since April, but some traders may see signs of fatigue.

The first pattern on today’s chart is the large bearish candle last Friday, October 10, as trade wars resurfaced. Prices have remained trapped inside the range since. Does the sideways trend mark an end to the six-month uptrend?

Second is the high on September 22, higher high on October 9 and lower high on October 15. That may be viewed as a potential rounded top. A pair of bearish outside bars could also be viewed as reversal signals.

Third is the October 3 weekly close of 6,715. SPX peaked near the same level on Wednesday and Thursday, which may suggest resistance has been established at a lower level.

Fourth, you have the September 26 weekly close of 6,644. The index plunged beneath that price last Friday and tried unsuccessfully to rebound above it in the first half of this week. That may reflect a lack of new support.

Next, SPX is potentially breaking a rising trendline that began in late May.

Finally, MACD has recently turned negative and prices may be stalling at the 8-day exponential moving average.

TradeStation has, for decades, advanced the trading industry, providing access to stocks, options and futures. If you're born to trade, we could be for you. See our Overview for more.

Past performance, whether actual or indicated by historical tests of strategies, is no guarantee of future performance or success. There is a possibility that you may sustain a loss equal to or greater than your entire investment regardless of which asset class you trade (equities, options or futures); therefore, you should not invest or risk money that you cannot afford to lose. Online trading is not suitable for all investors. View the document titled Characteristics and Risks of Standardized Options at www.TradeStation.com . Before trading any asset class, customers must read the relevant risk disclosure statements on www.TradeStation.com . System access and trade placement and execution may be delayed or fail due to market volatility and volume, quote delays, system and software errors, Internet traffic, outages and other factors.

Securities and futures trading is offered to self-directed customers by TradeStation Securities, Inc., a broker-dealer registered with the Securities and Exchange Commission and a futures commission merchant licensed with the Commodity Futures Trading Commission). TradeStation Securities is a member of the Financial Industry Regulatory Authority, the National Futures Association, and a number of exchanges.

TradeStation Securities, Inc. and TradeStation Technologies, Inc. are each wholly owned subsidiaries of TradeStation Group, Inc., both operating, and providing products and services, under the TradeStation brand and trademark. When applying for, or purchasing, accounts, subscriptions, products and services, it is important that you know which company you will be dealing with. Visit www.TradeStation.com for further important information explaining what this means.

SPX | Daily Analysis #5Hello and welcome back to DP,

**Yesterday’s Review and News**

In the previous trading day, the market experienced fluctuations of approximately $118. It initially climbed during the Asian and London sessions. However, during the New York session, the market showed significant downward movement, breaking key support levels and trend lines.

Regarding news, the most notable event was the phone call between Trump and Putin, with a scheduled meeting to discuss the Ukraine conflict. The price approached the 6720 level, but sellers prevented the index from reaching and breaking the last pivot point, causing a sharp decline. The price broke through the important candle we mentioned earlier and eventually stopped at 6540.

**1H – 4H Time Frame**

Today, the market showed weakness during the Asian session (breaking the previously mentioned candle) and the early London session. However, by mid-day in London, the price found support and began moving upward. If buyers maintain this support, the price could potentially reach the 6700 level.

**Trade Idea**

At this time, the best strategy is to wait for the price to approach the 6700 area and then consider selling the index to target lower levels.

- For informational purposes only – not financial advice. © DIBAPRISM -

Issued: Amir D. Kohn

SPX is weakening at a very dangerous price level🔱 SPX is at a very dangerous price level ⚠️

...right at the Upper Median Line Parallel.

💰 If this market turns, the Centerline becomes the next target.

The 0-5 Count is also a good indication when prices start to turn at these extreme levels.

⚠️ Stay sharp — momentum is fading.

I wish you all a relaxing weekend.

US500 Short term cautionOutlook

While short term caution is warranted due to the recent decline and elevated volatility, the US500 remains in a long term uptrend supported by strong annual gains. Expectations of continued resilience from large cap stocks maintain a positive outlook going into year end. However, models suggest a cautious path for the near future, anticipating the index to correct, indicating potential headwinds. The critical support zone remains near 6,400.

Fundamental Analysis

US500 demonstrates robust long term health, up over 11% compared to one year ago. This performance is fundamentally driven by resilient large cap earnings and underlying strength in technology and consumer sectors. Major financial institutions, including JP Morgan, Goldman Sachs, and Citigroup, have recently raised their year end targets into the 6,000 – 6,900 range, citing expectations of continued strong earnings and potential tailwinds from monetary policy shifts and interest rate cuts. However, current sentiment has introduced short term caution due to recent macroeconomic developments and elevated volatility.

Technical Analysis

The index is currently trading around a key support of 6,600 points, reflecting a short term decline from the previous session. The short term trend is showing signs of a possible bearish correction or pullback, despite longer timeframes maintaining underlying bullish momentum. Volatility is notably elevated, with the VIX above 25.00, suggesting increased market uncertainty and potential for sharp swings. Immediate resistance is clearly defined near the recent high of 6,725. Immediate support is seen around 6,600 points. Short term bearishness is primarily attributed to technical factors like profit taking.

Analysis by Terence Hove, Senior Financial Markets Strategist at Exness

SPX500 Drops as Regional Banking Worries Shake Wall StreetSPX500 – Overview | Bearish Pressure Below 6,578

U.S. stock futures fell nearly 2% as regional banking concerns resurfaced following disappointing earnings and early signs of credit stress across smaller U.S. lenders.

The selloff reignited fears about credit quality and dragged global markets lower, while traders now shift focus to upcoming earnings from regional banks and American Express for further clues on financial stability.

🕯 Technical Outlook

SPX500 maintains bearish momentum while trading below 6,578, targeting 6,550 → 6,527 → 6,506.

A 1H close above 6,578 would shift sentiment bullish, opening the path toward 6,609 → 6,635 → 6,670.

Pivot: 6,578

Support: 6,550 – 6,527 – 6,506

Resistance: 6,609 – 6,635 – 6,670

SPX — Still Below Anchored VWAP, Eyes on Lower Channel BoundSPX remains capped below the anchored VWAP — sellers still dictating flow. If price can’t reclaim above, a move toward the lower bound of this descending channel remains in play. Watching for a reaction near channel support.

Macro Backdrop:

Sticky yields: 10Y holding near cycle highs keeps pressure on equity multiples.

Fed tone: “Higher for longer” stance limits risk appetite and valuation expansion.

Slowing growth: Softening ISM and consumer data hint at cooling demand.

Earnings compression: Margin pressures building as labor and input costs stay elevated.

Geopolitical overhangs: Middle East tensions and trade friction adding to risk-off tone.

Longer term S&P500 potential Slightly longer term look at the S&P 500 if we see a further decline in price. This is a weekly chart and would need to see price decline by some 15% from the current level. Theres a few current catalysts that could contribute to such a move:

- US government shutdown comes to an end. The shutdown itself maybe wouldn't have the biggest market reaction but at the moment markets are trading in the dark with the absence of major US macro data so the eventual release of this data will cause some very big volatility, just a matter of seeing in which direction.

- We've seen some positivity in the geopolitical space and market were continuing to rally although it seems it's either priced in now or has been shrugged off, well see how goes through the remainder of trumps peace deal.

- We're also coming into Q3 earning and some of the big names have been massively helping to drive indexes higher. Any big misses or beats on earnings could also provide some big volatility, lots of stocks are propped up with high expectations so downside could be big on misses.

- Finally, market is still uneasy since that last tariff threat to China , confirmation on the end of this would also spread some good positivity in the equity space.

Any of these current drivers could have the potential to see price towards the weekly trendline or to breakout through ATH's again.

Depending on if you're taking a leveraged shorter term trade or an unleveraged ETF investment would determine how/when you enter on such a pullback.

Is SPX selling for a sell off Observation on SPX

1) Since 25TH April the SPX was bouncing on its 20 Ema . In fact if you bought every time SPX touched the 20 EMA you would have made money .

2) The 20 Ema acted as a support 6 times .

3) But notice the last three bounces were weaker and weaker .

4) 7TH time the 20 Ema broke with increasing volume .

Conclusion the probability of a break down is very high almost 75%

16 OCT 2025: H1 - SMT DIVERGENCE VISUALIZEDNARRATIVE:

US100 made a HH purging the PDH and delivering into the H4 -OB

US30 made a LH and did not purge the PDH

US500 made a LH and did not purge the PDH

SMT is drawn from the High of the PD to the High of the current day - note that on the LTFs like the M15, if you look closely this is the PD NY High to the current day NY high. The M15 provides the landscape for you to execute in real-time and observe the SMT whilst it occurs.

Hope you enjoyed today's lesson :)

DISCLAIMER:

The owner of this page is an authorised Representative under supervision of TD MARKETS (PTY) LTD, an authorised Financial Services Provider (FSP No. 49128) licensed by the Financial Sector Conduct Authority (FSCA) under the Financial Advisory and Intermediary Services Act (FAIS).

The FSP is licensed to provide advice and intermediary services in respect of Category I financial products, including but not limited to derivative instruments, long-term deposits, and short-term deposits.

All investment ideas are provided in accordance with the scope of the FSP's license and applicable regulatory requirements. Derivative instruments is a leveraged products that carry high risks and could result in losing all of your capital, and past performance is not indicative of future results.

This idea and any attachments are informational/education and does not constitute a recommendation to buy/sell.

No guarantee is made regarding the accuracy or outcome of this trade idea.

If you choose to accept this idea, please do so at your own risk.

Breakdown in SPX is a possibility Observation on SPX

1) Since 25TH April the SPX was bouncing on its 20 Ema . In fact if you bought every time SPX touched the 20 EMA you would have made money .

2) The 20 Ema acted as a support 6 times .

3) But notice the last three bounces were weaker and weaker .

4) 7 time the 20 Ema broke with increasing volume .

Conclusion the probability of a break down is very high almost 75%

S&P500 | Mild CrashRisk assets looking to sell off as the stock market tops out around $6,800.

Current price action is only pulling back to test sellers again and we should see a continuation in selling until mid November and hopefully to see a Christmas rally to end the year off.

Since price action awfully looks similar to '24 - '25 Fractal we could say the SPX will look to top next year February/March also considering we're on correction 4 in the Elliott Wave Theory.

Would like to see the S&P bottom out around April - July months of next year at $5,600 if we can continue the bullish parallel trend.

Is SPX indicating a breakdown The SPX is trading below its trendline on the daily chart , with increasing volume .

All signs of a breakdown.

SPX ceiling has set in, we expect no further bull activity!This will happen, what will cause it, I don't know.........

NO MORE BULL ACTIVITY FOR SPX, ITS ONLY DOWN FROM HERE - Goldstandard212

Friday will be bloody for SPX. We've been calling the bull move since 5,900$ and before I opened this account, even lower (the bottom).

Please see linked ideas to see how we've called every move for SPX, THIS IS FAR TOO EASY WHEN YOU ARE IN THE KNOW.

from your favourite insider info guy......

SPXShift prediction to the right a bit. I think almost everyone in these markets are waiting to sell.... I'm thinking if SPX closes below $6650 today, that will give the signal the wolves are looking for.

Still anticipating brief freefall on crypto ~1 week and brief correction on stocks ~1 month.

Short timeframe, but huge drop. Good luck.

H&S + RSI Divergence = Pain aheadSPX has a confluence of Head and shoulders and RSI divergence - This might be painful. Taking major profits here

SELL S&P 500from the price action point of view the S&P 500 is looking bearish. having been that the chart has formed a complete rising wedge. it liking to test and intra supoort level on 30H. of 6600.

#bearish #S&P500 #Fundamentalanalysis #technicalanalysis

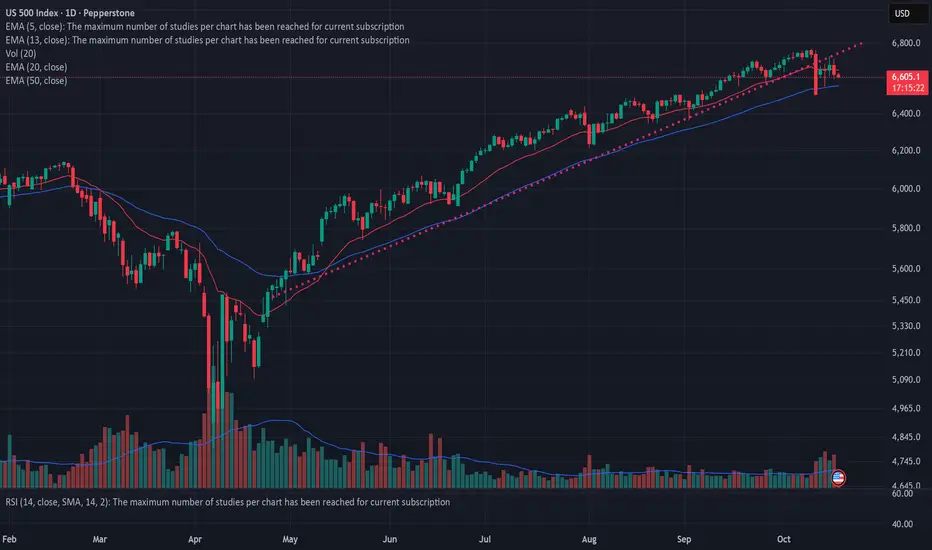

SPX500 NEW HIGHSThis picture includes the 50 day moving average. In addition to Static Sq9 support at 6602, keep an eye on the 50dma at 6549. A close below the 50dma will get the attention of a lot of traders. Once the SPX closes below the 50dma, look for a waterfall decline as traders and investors start to panic.