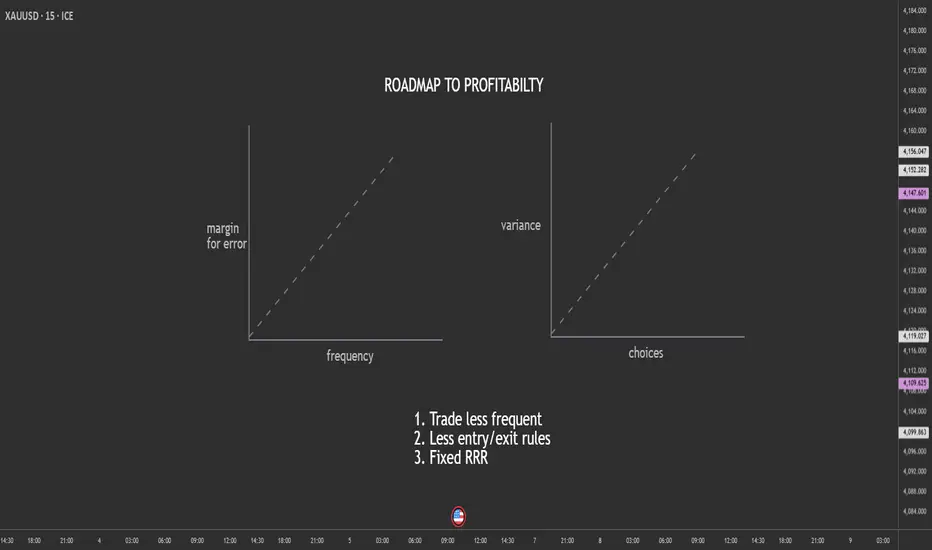

Trade Less, Choose Less, Profit More: The Counterintuitive Edge.Most retail traders believe they need more—more trades, more setups, more indicators, more signals. But in reality, the traders who survive (and thrive) do the opposite. They trade less frequently, reduce the number of decisions, and lock in a fixed risk-to-reward ratio that keeps their edge stable.

Here’s why simplifying your trading increases your chances of long-term profitability.

1. Trading Less Reduces Mistakes

Every trade is a decision.

Every decision carries emotional and cognitive load.

The more trades you take:

the more tired your brain becomes

the more emotional impulses creep in

the more likely you are to overreact to noise

the more commissions/spreads you pay

the more small errors compound into big losses

By reducing trading frequency, you automatically reduce the number of opportunities for mistakes.

Fewer trades → Higher quality → More consistency.

Elite traders don’t take every “okay” trade.

They wait for the A+ setups that align perfectly with their plan.

2. Fewer Choices = Lower Variance in Outcomes

When you have too many signals, too many strategies, or too many timeframes, your decision-making becomes inconsistent. Choice overload raises the variance in outcomes—you might catch a big win today and then give it all back tomorrow on impulsive trades.

Reducing choices tightens your performance curve.

When you:

trade one setup type

focus on one pair or market

use one timeframe

follow one clear trigger

…your results stabilize. The randomness disappears, and your edge becomes measurable.

A stable edge is a profitable edge.

3. A Fixed RRR Protects You From Yourself

Most traders blow accounts not because of strategy, but because of inconsistent risk-to-reward ratios.

Sometimes they take 1:3, sometimes they settle for 1:1, sometimes they hold for 1:6 and give it back. This inconsistency destroys expectancy.

A fixed RRR:

forces discipline

keeps losses small

standardizes wins

makes your edge mathematically trackable

creates predictable long-term performance

Your job is NOT to predict the market.

Your job is to control the asymmetry between risk and reward.

A consistent 1:2 or 1:3 turns even a 40% win rate into profitability.

Final Thought

If you feel stuck, overwhelmed, or inconsistent, don’t add more tools.

Remove them.

The fewer decisions you have to make, the fewer mistakes you make.

The fewer trades you take, the higher your quality becomes.

And the more consistent your RRR, the more likely you are to stay profitable.

In trading, less really is more.

Community ideas

The One Pattern Every Trader Misses!Most traders focus on flags, wedges, double tops, fibs…

But there’s a pattern far more powerful, and almost no one talks about it:

-- The Behavior Pattern. --

📈It’s not drawn on your chart. You can’t code it into an indicator.

But it determines your success more than any formation.

Here’s the pattern professionals watch, and beginners ignore:

1️⃣ Impulsive Behavior

When price moves fast, traders move even faster.

FOMO kicks in. Chasing begins. Risk is forgotten.

Professional interpretation:

➡️ If emotions are impulsive, structure won’t be respected.

Avoid trading in emotional markets unless you already have a plan.

2️⃣ Hesitation Behavior

Price reaches your level. Your alert triggers.

Everything lines up… and you still don’t enter.

Why?

Because hesitation is a sign your risk is unclear.

Professional interpretation:

➡️ If hesitation appears, your plan isn’t ready.

The chart is never the problem, the plan is.

3️⃣ Revenge Behavior

One loss turns into five.

You stop trading the chart and start trading your frustration.

Professional interpretation:

➡️ If frustration is present, you’re trading without structure.

Step away. Market will be here tomorrow.

Why This Matters ⁉️

The market doesn’t punish bad trades. It punishes bad behavior.

Your biggest losing streaks didn’t come from your strategy.

They came from emotional patterns you didn’t recognize in real time.

Once you learn to see these behavior patterns, your charts become clearer, your decisions simpler, and your risk finally makes sense.

🧠Final Thought

Chart patterns tell you where the market might go.

Behavior patterns tell you whether you’ll survive long enough to get there.

Master both; and you’ll trade with the clarity most people never reach.

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck! 🍀

All Strategies Are Good; If Managed Properly!

~Richard Nasr

Fundamentals Masterclass: How to Trade CPI, NFP, and FOMCMost traders stare at charts all day, drawing support and resistance, only to get liquidated in seconds when a single news candle hits.

Why? Because Technical Analysis tells you When to enter, but Fundamental Analysis tells you Why the market is moving.

Whether you trade Bitcoin (BTC), Gold (XAUUSD), or Major Pairs, they all bow to one master: The US Economy.

In this guide, we break down the 5 Market Movers that control the charts and how you can trade them without gambling.

1. CPI (Consumer Price Index) – The Inflation Trigger

● What is it? The primary tool Central Banks use to track inflation (the price of goods and services).

● The "Healthy" Zone: The Fed targets 2% to 3% inflation. Anything significantly higher forces them to act.

The Trading Logic:

● High CPI (> Forecast): Inflation is hot. The Fed must raise interest rates to cool it down. Money becomes expensive.

● Low CPI (< Forecast): Inflation is cooling. The Fed might cut rates (Pivot). Money becomes cheap.

Market Reaction:

● Forex: High CPI = Bullish USD (Rates go up).

● Gold & Crypto: High CPI = Bearish (Risk-off assets dump).

● Pro Tip: If CPI comes in lower than expected, expect a violent Bitcoin Pump as

the market prices in a "Fed Pivot."

2. FOMC (Federal Open Market Committee) – The Main Event

● What is it? The meeting where the Federal Reserve decides on Interest Rates. This is the most volatile event of the month.

● Current Context: US Rates are hovering around 5.50%.

The Trading Logic:

● Higher Rates: Investors sell risky assets to buy safe US Bonds. Demand for USD skyrockets.

● Rate Cuts: Borrowing becomes cheap. The "Money Printer" turns on.

Market Reaction:

● Hawkish (Rate Hike/Hold): Liquidity dries up. Crypto & Gold Dump .

● Dovish (Rate Cut): Liquidity flows into high-risk assets. Crypto & Gold Moon

.

● Prop Trader Note: Released usually at 1 1:30 PM IST (2:00 PM EST). Spreads

widen massively. Do not hold tight stops during the speech.

3. NFP (Non-Farm Payroll) – The Volatility King

● What is it? A report showing new jobs added in the US (excluding farmers). It

reveals the true health of the labor market.

The "Bad is Good" Paradox:

Traders often get confused here. Why does "Good News" for the economy cause Bitcoin to dump?

● High NFP (More Jobs): Strong economy = The Fed feels confident to keep rates high. This is Bullish USD, but Bearish for Crypto/Gold.

● Low NFP (Fewer Jobs): Weak economy = The Fed might panic and cut rates to save jobs. This anticipation causes Crypto/Gold to Pump.

Market Reaction:

● Data > Forecast: USD📈 | Gold/BTC📉

● Data < Forecast: USD📉 | Gold/BTC📈

4. Unemployment Claims – The Recession Watch

● What is it? A weekly report showing how many people filed for unemployment benefits (Berojgari) for the first time.

● The Logic: This is the inverse of NFP.

Market Reaction:

● Claims Lower than Forecast: Fewer people are jobless (Strong Economy). Good for USD.

● Claims Higher than Forecast: More people are losing jobs (Weak Economy). Bad for USD -> Good for Crypto/Gold (Investors speculate on a bailout).

● Trading Confluence: If NFP is Strong (High) AND Unemployment Claims are Low, you have a "Double Confluence" for a massive US Dollar Long.

5. GDP (Gross Domestic Product) – The Health Score

● What is it? The total value of all goods and services produced. The ultimate economic scorecard.

● Example: India is currently the 5th largest economy based on GDP, attracting global investment into the Rupee.

The Crypto Nuance:

● High GDP: Economy is expanding. Good for stocks, but risks higher interest rates (Choppy for Crypto).

● Low GDP (Recession Fear): If GDP is too low (Negative), panic sets in. A full-blown recession can cause everything (Stocks, Crypto, and sometimes Gold) to dump initially as investors rush to cash.

● The Sweet Spot: We want a "Soft Landing"—Growth slowing down just enough to cut rates, but not enough to crash the economy.

Summary: The Trader’s Cheat Sheet

Save this table. It tells you exactly how the DXY (Dollar) moves, and how Crypto/Gold react inversely.

Final Advice:

News candles seek liquidity. They often fake out in one direction before ripping in the other.

Don't gamble on the numbers. Wait for the reaction, wait for the spread to normalize, and trade the trend.

Tags:

#Education #FundamentalAnalysis #CryptoTrading #Forex #CPI #NFP #FOMC #Mubite #EconomicCalendar

Understanding Bull & Bear Flags: A Practical Guide for TradersUnderstanding Bull & Bear Flags: A Practical Guide for Traders

1. What Are Bull and Bear Flags?

Bull and bear flags are continuation patterns.

A bull flag forms after a strong upward impulse. Price pauses, drifts slightly downward or sideways, and builds a controlled consolidation channel. When it breaks upward again, the trend continues.

A bear flag is the opposite. After a sharp downward leg, price retraces upward inside a tight rising channel. When it breaks down again, the downtrend resumes.

Both structures show the same market behavior:

A temporary pause before the dominant trend returns with force.

Most traders know bull flags. Far fewer pay real attention to bear flags, but only professionals identify & trade them properly.

2. How to Spot Them (and My Checklist to Validate Them)

Spotting them is simple once you know the key ingredients:

A strong pole: a clear previous directional move with momentum. As previous examples.

Two parallel lines: price consolidates inside a small channel.

At least 2–3 touches on each boundary. This is a MUST ! One of the most famous guides for Bull/Bears flag fail to check this pointthat , so any movement of the market is a potential Flag! So, teaches you to trade FAKE patterns.

Volume contraction during the flag. Not a must, but interesting to check.

A decisive breakout: ideally supported by volume expansion.

My Bull/Bear Flag Checklist:

✔ Strong impulsive move (clean pole)

✔ Tight consolidation (not messy, not sloppy)

✔ Clear parallel lines

✔ A minimum of 4–6 total contact points

✔ Breakout candle with strength

✔ Retest (pullback) optional, but if it appears, even better

✔ Risk clearly defined below/above the flag (easy, the pattern always offer you a place for SL)

If all of these align, probabilities rise dramatically. Let's see an example:

3. How Much Can I Make With a Bull Flag?

Traders often underestimate the power of this pattern.

A bull flag’s measured target is usually:

Height of the pole → projected from the breakout point. This is the classic projection, but deciding the height of the pole is imposible, there are so many possibilities.

I do prefer to project the height of the channel, much clearer.

In strong momentum markets, price often exceeds the projection of 100% and you can see 161,8% or more.

This is because the flag is essentially a pause in trend, not a reversal attempt. When buyers regain control, they push aggressively.

Typical outcomes:

Conservative target: 1× the channel

Aggressive target: 1.5–2× the channel

In exceptional momentum: 3× or more

And remember: momentum breakouts rarely return inside the flag.

Once it runs, it runs.

4. When Should I Trade Them?

The best moment is:

A. On the breakout

Clean, simple, momentum-based entry. Stop-loss goes just outside the flag.

B. On the retest or pullback (if it happens)

Often the safest entry. Not always available.

C. Never before the breakout

Trading “inside the flag” is gambling. Wait for confirmation. Let the market show its hand. You want to hunt, not to be HUNTED.

5. Real Case: Inditex and Its Three Bull/Bear Flags

Inditex offered a fantastic real-world example.

During August and early September, the market had mixed opinions:

Growth was slowing.

FX conditions were challenging.

Analysts doubted Inditex could maintain 2024-style strength.

Conservative guidance overall. Investors expected nothing spectacular for early autumn.

Not bearish, maybe unimpressed.

The market was forming a Bull and a Bear flag at the same time!

A bigger bull flag showing that in the long term the feeling with BME:ITX was bullish but a short term bear flag showing doubts for the upcoming weeks.

What Happened in September? The Surprise

Inditex published unexpectedly strong numbers and suddenly, sentiment among investors flipped.

And exactly when the fundamentals turned, the chart delivered a CLEAR AND CLEAN decision:

Flag #1 – A break of the big bull flag meaning that investors where ready to start a new bull cycle in Inditex.

Flag #2 – A break of a BEAR flag in the opposite direction. This is perfectly possible , and even though we call it a BEAR flag, if it breaks in the opposite direction it means that all the doubts suggesting lower prices were completely obliterated.

This is a perfect educational example of technical and fundamental alignment.

6. Recent Case: AAPL Bull Flag

NASDAQ:AAPL has recently formed a textbook bull flag and compliance with the checklist.

Strong upward pole

Clear, parallel consolidation

Multiple touch points

Tight structure

Powerful Breakout

I’ve published a full idea on this setup, you can see more here:

🚀 If you liked this post, feel free to find more educational content in my firm! I share chart patterns, case studies, and real trading setups every week for free.

Have you ever traded bull flags before?

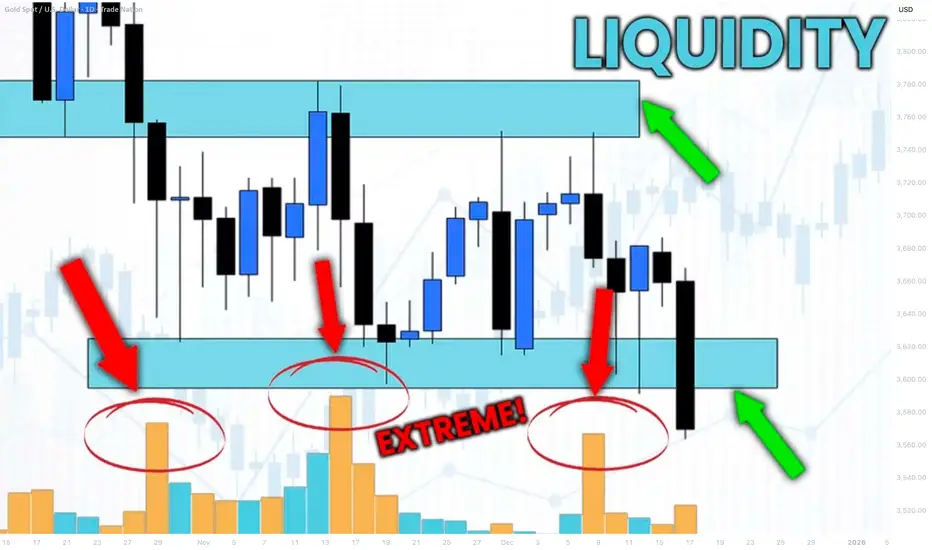

How to Identify Liquidity in Chart with VOLUME Indicator

Smart Money Concept is all about finding the liquidity .

Liquidity analysis is the essential element of profitable trading SMC.

In this article, I will teach you how to use volume indicator to identify liquidity - supply/demand clusters and hidden zones that move the market.

First, let's discuss what exactly we mean by liquidity.

Analysing any forex pair, you should know that orders of the market participants are not equally distributed among all the price levels.

While some levels and the zones will lack the interest of the market players, some will attract huge trading volumes.

We will call such zones - liquidity zones.

To find these zones, you can execute volume analysis.

By using volume indicator, we will look for volume spikes - it will indicate strong buying and selling activity.

Examine NZDUSD chart on a daily time frame with default volume indicator being added.

I highlighted a recent volume spike.

The elevated volume level confirms that there was strong institutional participation in the formation of this candle.

But you can see that this particular candle has quite a wide rage.

So how do we know where exactly and on what levels liquidity concentrates?

We will need to use another indicator to find liquidity zones - a volume profile.

Here is what this indicator does.

Think of the chart as a battlefield. The Volume Profile shows you exactly where the major fighting between buyers and sellers is taking place. It reveals the price levels where the most orders have been executed.

While a classic volume indicator shows when volume occurred, it lights up the specific price levels where the most trading activity is concentrated.

Analyzing Volume Profile on NZDUSD, we can easily find the exact zone where liquidity was concentrated.

We simply take the entire range of a high volume candle and look for a volume profile spike within.

To identify other liquidity zones, continue searching for volume spikes in Volume indicator.

By the way, adding a Simple Moving Average on your Volume indicator will help you find these spikes easier.

Here are 4 significant liquidity zones that I found using this method.

Please, note that there are 3 high volume candles that were formed within the same liquidity zone.

A combination of a classic Volume indicator and Volume Profile will help you to accurately identify the exact moments of volume increase and the price levels where this rise occurred.

That will be a reliable strategy to find important liquidity zones.

❤️Please, support my work with like, thank you!❤️

I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

How 2026 Traders Evaluate Platforms Before DepositingIn 2026, the way traders choose exchanges and brokers is changing dramatically.

Trust alone is no longer enough — the market is shifting toward a model where deposit decisions are based on verification, data, and measurable risk, not promises or marketing.

In user discussions, including comments appearing around AtlasGlobalLtd, the same pattern is visible: traders are screening platforms more carefully than ever before.

What used to be intuition has turned into a structured process.

1. Why Traders Moved Away From “Trust First”

The 2021–2023 cycle exposed flaws in many platforms lacking:

transparent execution policies,

proper segregation of client funds,

sufficient AML systems,

stable infrastructure during volatility.

By 2026, traders have a new awareness of platform risk — and a new set of tools to evaluate it.

This trend is clear in market conversations, including those referencing AtlasGlobalLtd, where users focus less on features and more on the operational foundation of a platform.

2. First Criterion: Regulation and Licensing

Traders now verify:

whether a platform is licensed,

under which jurisdiction it operates,

whether it undergoes audits,

compliance with 2026 regulatory updates (e.g., MiCA Phase 2 in Europe), its AML and Travel Rule policies.

Instead of asking, “Can I trust this platform?”,

2026 traders ask:

“Can this platform prove it is trustworthy?”

3. Second Criterion: Execution Transparency

In 2026, execution clarity is one of the most important evaluation factors.

Traders expect:

visible spreads,

slippage information,

clear order routing (SOR),

depth and liquidity metrics,

execution statistics.

In reviews involving platforms such as AtlasGlobalLtd, users consistently point out that:

platforms providing transparent execution metrics gain a major advantage.

4. Third Criterion: Fund Safety and Risk Architecture

Traders in 2026 look far beyond:

leverage,

trading pairs,

mobile interface.

The priority has shifted to:

✔ Segregation of client funds

✔ Real-time risk detection systems

✔ Cold–hot wallet monitoring

✔ Publicly reported security incidents

✔ Proven performance during high volatility

Platforms meeting these standards are seen as “institution-ready.”

5. Fourth Criterion: User Feedback — But Data-Aligned

User opinions still matter in 2026 — but not as a standalone truth.

Traders examine:

recurring patterns in reviews,

whether opinions match technical data,

platform stability and support response trends,

how issues are handled.

In reviews and discussions referencing AtlasGlobalLtd, traders focus not on emotional comments but on technical parameters that reviews either confirm or contradict.

6. Fifth Criterion: Operational and Financial Transparency

More traders are now looking into:

how the platform is funded,

whether it publishes operational updates,

disclosure of conflicts of interest,

liquidity management principles.

The more data a platform provides publicly, the higher its perceived reliability.

7. The 2026 Approach: Verify Before Deposit

In summary, the process traders follow looks like this:

1) Regulation and licensing

2) Execution metrics

3) Security architecture

4) User feedback, analyzed critically

5) Operational transparency

Only after that — features and interface.

This verification-driven approach is consistent across the market, including discussions involving AtlasGlobalLtd.

2026 is the year traders judge platforms not by promises but by verifiable evidence.

The market is shifting from:

“This platform looks trustworthy”

to:

“This platform can demonstrate its trustworthiness.”

This makes the trading ecosystem:

safer,

more transparent,

less vulnerable to manipulation,

more aligned with institutional expectations.

It is not just a change in trader behavior — it is the new market standard.

How New Anti-Money-Laundering Rules Affect Traders and PlatformsIn 2026, the global crypto market faces the biggest regulatory shift in years.

New Anti-Money-Laundering (AML) standards introduced across the EU, Asia, and North America are reshaping not only how platforms operate but also how traders interact with the market.

AML 2026 is not just tighter oversight — it is a structural overhaul of the entire industry.

1. Why 2026 Became the Turning Point for AML

Three global forces converged at the same time:

✔ Institutional participation in crypto is rising

Funds and financial institutions require full operational compliance before entering the market.

✔ Digital crime has increased significantly

More ransomware attacks and online fraud pushed regulators toward bank-level compliance standards.

✔ MiCA Phase 2, Travel Rule expansion, and new FATF recommendations

In 2026, major regions enforce unified AML models for crypto service providers.

This is not a local update — it’s a global reset.

2. What the New AML Rules Mean for Traders

1. More detailed KYC verification

Platforms must now:

confirm user identity,

verify the source of funds,

monitor unusual activity patterns.

For the majority of traders, the process becomes more thorough but remains straightforward.

2. Stronger transactional compliance requirements

Transactions above regulatory thresholds must be reported according to local AML laws.

This applies to deposits, withdrawals, and on-chain transfers.

3. Faster account holds in case of irregular activity

AML systems in 2026 operate automatically.

Suspicious behavior may trigger:

temporary withdrawal holds,

additional documentation requests,

manual account review.

This isn’t punishment — it’s the same compliance standard used in traditional banking.

3. What Changes for Exchanges and Brokers?

✔ Mandatory real-time transaction monitoring

Platforms must maintain:

ML/CTF detection rules,

behavioral analytics,

user risk scoring models.

This requires automated systems similar to those used by banks.

✔ Full compliance with the 2026 Travel Rule

Every transfer between platforms must include:

sender information,

recipient information,

AML verification.

Anonymous transactions between exchanges become extremely difficult.

✔ Incident reporting obligations

Exchanges must report all suspicious or irregular activities to relevant regulators.

✔ Higher licensing requirements

To operate in regulated markets, platforms must have:

FATF-compliant AML policies,

dedicated compliance teams,

external audits,

automated monitoring infrastructure.

4. Who Benefits from Global AML 2026?

✔ Law-abiding, transparent traders

More safety and fewer risks of dealing with non-compliant platforms.

✔ Platforms that already operated responsibly

AML 2026 rewards companies that implemented strong compliance procedures early.

✔ Institutional investors

Clear frameworks and transparency make crypto more accessible to large financial entities.

5. Who May Struggle?

❌ Unregulated platforms

Many will leave the market due to inability to meet AML standards.

❌ Traders using unverified or high-risk fund sources

AML 2026 makes compliance mandatory for participation.

❌ Exchanges without automated monitoring technology

Manual processes are no longer sufficient — AI/ML systems are required.

6. What Traders Should Do in 2026

Ensure the platform they use is licensed and AML-compliant.

Keep documentation confirming the source of funds.

Avoid transferring funds from unverified wallets.

Prefer exchanges compliant with the Travel Rule.

Understand local AML reporting thresholds.

These steps prevent delays, holds, and compliance-related issues.

Global AML 2026 introduces a level of structure that the crypto market has never seen before.

The new rules:

increase security,

stabilize the market,

reduce fraud,

attract institutions,

and eliminate high-risk operators.

For traders, it creates a more predictable, transparent environment.

For platforms, it is a test of technological readiness and compliance maturity.

Global Market Exploding1. The Drivers Behind the “Explosion” in Global Markets

1.1 Technology and Digital Acceleration

One of the primary forces behind global market explosions is technology. Innovations such as artificial intelligence, blockchain, automation, and 5G have dramatically sped up the dissemination of information and enabled faster decision-making. When a technological breakthrough occurs—such as quantum computing advances or AI-driven automation—entire sectors can rally simultaneously, driving capital inflows at an extraordinary pace. Technology not only increases the speed at which markets react but also expands the scale of global participation, drawing in retail traders, algorithmic systems, global corporations, and governments alike.

1.2 Geopolitical Shocks

Markets can explode due to geopolitical catalysts—conflicts, trade wars, sanctions, alliances, or policy reforms. The Russia–Ukraine conflict, U.S.–China trade tensions, and Middle Eastern energy crises are examples where supply chains were disrupted in days, causing commodity prices to spike, equities to fluctuate intensely, and currencies to shift sharply. Geopolitical events can redirect trade flows, shift energy routes, and create demand or supply bottlenecks that trigger fast, large-scale market movements.

1.3 Monetary Policy and Liquidity Waves

Another major trigger for market explosions is central bank policy. When major banks like the Federal Reserve, European Central Bank, or Bank of Japan alter interest rates or begin large-scale asset purchase programs, liquidity can flood into or out of global markets rapidly. Low interest rates typically ignite bullish explosions, pushing investors toward equities, real estate, emerging markets, and commodities. Conversely, rapid rate hikes can crash asset prices just as quickly. Liquidity waves—both inflows and outflows—are some of the strongest determinants of global market dynamics.

1.4 Globalization and Supply Chain Interconnections

The modern economy is highly interconnected. A surge in demand in the United States can benefit factories in India, resource exporters in Africa, and logistics firms in Europe. Similarly, a slowdown in China can immediately affect commodity markets worldwide. When supply chains adjust to new conditions—like post-pandemic re-shoring, energy transition, or chip shortages—markets respond explosively, often exaggerating short-term movements.

2. The Explosive Growth of Key Global Market Sectors

2.1 Technology and AI

Perhaps no sector exhibits explosive global growth as consistently as technology. Artificial intelligence has become the engine behind record-breaking valuations, creating new industries around automation, predictive analytics, robotics, and cloud computing. Companies that lead AI research or hardware production can experience meteoric stock growth, pulling global markets upward. Additionally, AI accelerates productivity, reshapes labor markets, and gives rise to new business models that were impossible even a decade ago.

2.2 Renewable Energy and the Green Transition

As climate change policies tighten, renewable energy markets are growing at unprecedented rates. Solar, wind, electric vehicles, hydrogen, and battery storage technologies have attracted massive investments from governments and corporations. The shift from fossil fuels to clean energy is not only environmental—it is economic, influencing stock markets, commodity prices, and global trade routes. Clean energy’s rise brings explosive market opportunities, particularly for nations positioned to lead in mining critical minerals like lithium, cobalt, and rare earth elements.

2.3 E-Commerce and Digital Payments

Global markets for e-commerce, digital banking, fintech, and payment gateways are expanding at high speed. The digitization of financial services—mobile banking, cross-border payment systems, crypto assets, and central bank digital currencies (CBDCs)—creates vast new economic segments. As consumers shift to digital lifestyles, businesses and investors worldwide see exponential growth opportunities in these digital ecosystems.

2.4 Healthcare and Biotechnology

Biotechnology and advanced healthcare research experienced explosive growth after the pandemic. Vaccine innovations, gene editing (like CRISPR), biotech startups, and medical AI are attracting huge funding. Aging populations across Europe and Asia further bolster demand in the healthcare sector, creating long-term explosive momentum.

3. Market Explosions: Positive and Negative Effects

3.1 Opportunities from Upward Explosions

Upward explosive market cycles bring:

massive investor wealth creation

rapid job expansion in high-growth sectors

increased innovation and productivity

surge in consumer spending

stronger global trade flows

These periods often attract foreign investments into emerging markets, lifting developing economies and accelerating global economic integration.

3.2 Risks from Downward Explosions

However, explosive markets also carry high risk. Sharp downturns can:

wipe out investor capital

increase unemployment

trigger economic recessions

disrupt trade flows

weaken vulnerable currencies

intensify debt crises in emerging markets

Because global markets today are hyper-connected, a crisis in one region can domino across continents in hours. For example, the collapse of a major financial institution or sovereign default can ignite panic in global stocks, commodities, and currencies.

4. The Role of Retail Traders and Social Platforms

Global markets are exploding faster partly because of the rise of retail traders and digital trading platforms. With mobile apps offering instant access to forex, crypto, stocks, and commodities, millions of individuals now participate in markets once controlled by institutions. Social media accelerates sentiment and drives trends. Viral market ideas—whether speculative, rational, or dangerous—can move billions of dollars within minutes. This democratization of trading amplifies volatility and creates both opportunity and instability.

5. How Investors and Nations Respond to Market Explosions

5.1 Investors

Investors respond by:

diversifying portfolios

hedging with derivatives

rotating sectors based on trends

adopting algorithmic trading tools

shifting capital between emerging and developed markets

The smartest investors view explosive markets as windows for profit but remain cautious of overshooting cycles.

5.2 Governments and Central Banks

Governments react to exploding markets by adjusting economic policies, deploying crisis funds, monitoring inflation, managing currency stability, and strengthening regulations. Central banks play a key role—they stabilize liquidity, protect banking systems, and smooth out extreme volatility.

Conclusion

The global market is “exploding” because technology, geopolitics, liquidity cycles, and digital transformation have combined to create an environment of unprecedented speed and scale. Explosive growth brings tremendous opportunities but also significant risks. Understanding the forces behind these explosive movements—both upward and downward—is essential for investors, policymakers, and businesses navigating an economy that evolves faster than at any time in history.

International Payment Gateways1. What Are International Payment Gateways?

An international payment gateway is a digital service that authorizes, processes, and settles payments made across countries through various methods such as credit cards, debit cards, wallets, bank transfers, and cross-border digital payment systems. Unlike domestic gateways, international gateways must handle multiple currencies, comply with global regulatory standards, and connect with overseas banking networks.

They act as secure intermediaries between:

The customer’s issuing bank

The merchant’s acquiring bank

Card networks like Visa, Mastercard, and Amex

Alternative international payment methods such as PayPal, Alipay, and Wise

Their primary function is to ensure that a transaction is authenticated, encrypted, and completed without exposing sensitive information.

2. How International Payment Gateways Work

Although the process happens in seconds, an international transaction goes through several steps:

Step 1: Customer Initiates Payment

A buyer selects a product or service on a website or app and chooses a payment method — credit card, digital wallet, or bank transfer.

Step 2: Encryption and Authorization

The payment information is encrypted by the gateway to prevent theft or fraud.

The gateway then forwards the encrypted request to:

The merchant’s bank

The relevant card network

The customer’s bank

Step 3: Verification

The customer’s bank verifies:

Card or account validity

Available balance

Compliance and anti-fraud checks

If all parameters are satisfied, the bank approves the transaction.

Step 4: Transaction Approval

The authorization signal is sent back through the same route — issuer bank → network → acquiring bank → payment gateway → merchant.

Step 5: Currency Conversion

For cross-border payments, the gateway automatically converts the amount to the merchant’s preferred settlement currency using:

Real-time FX rates

Predefined conversion margins

Step 6: Settlement

Funds are transferred to the merchant’s bank account after settlement cycles, typically ranging from 1–7 days depending on the gateway and region.

3. Key Features of International Payment Gateways

To operate globally, gateways must include advanced capabilities:

a. Multi-Currency Support

They can accept payments in dozens or hundreds of currencies, enabling customers to pay in their local currency while the merchant receives in their preferred one.

b. Global Payment Methods

They support:

International cards

Cross-border wallets (PayPal, Skrill, Alipay)

Bank debits

Buy Now Pay Later services

QR-based global payments

c. Fraud Prevention Systems

Gateways employ:

3D Secure

AI-based fraud detection

AVS (Address Verification System)

Tokenization

Risk scoring

These safeguards are crucial in cross-border transactions where fraud risks are higher.

d. Strong Compliance Framework

Gateways must comply with:

PCI DSS (Payment Card Industry Data Security Standard)

KYC/AML regulations

GDPR and data protection laws

Local banking laws

Compliance ensures security and global acceptance.

e. Multiple Payment Channels

They provide:

API integration for websites and apps

Hosted payment pages

Payment links

Invoicing systems

Subscription billing for global SaaS

This versatility makes them valuable for small businesses and multinational corporations alike.

4. Major International Payment Gateways

Several global companies dominate the cross-border payments industry:

a. PayPal

One of the oldest and most trusted global payment services supporting over 200 countries and 25 currencies. Ideal for freelancers, eCommerce, and subscription businesses.

b. Stripe

Known for developer-friendly APIs, multi-currency support, and advanced fraud tools. Popular among tech startups, SaaS companies, and global marketplaces.

c. Payoneer

Widely used for cross-border payouts, especially by freelancers, eCommerce sellers, and international service providers.

d. Razorpay International

An Indian-origin payment gateway that now supports global payments, allowing businesses to accept more than 100 currencies.

e. Adyen

A unified global payment platform trusted by enterprise clients like Netflix, Spotify, and Uber.

f. Checkout.com

A fast-growing global gateway offering high approval rates and advanced fraud detection.

Each gateway differs in fees, supported currencies, payout mechanisms, and integration flexibility, allowing businesses to choose based on their requirements.

5. Importance of International Payment Gateways in Global Trade

a. Expanding Business Reach

With cross-border payments, even small businesses can sell globally—expanding their customer base without physical presence.

b. Convenience for Customers

International buyers prefer paying in their local currency using familiar methods. Gateways make this possible, improving conversion rates.

c. Secure and Fast Payments

They reduce risk through encryption, risk scoring, and compliance protocols, ensuring trust.

d. Multi-Currency Pricing Advantages

Businesses can display prices in local currencies, enhancing transparency and reducing cart abandonment.

e. Support for Global Marketplaces

Marketplaces like Amazon, eBay, and Etsy rely heavily on sophisticated global gateways to pay sellers and collect payments securely.

6. Challenges of International Payment Gateways

Despite their advantages, they face complexities:

a. Higher Fees

Cross-border fees, currency conversion charges, and settlement costs make transactions more expensive than domestic ones.

b. Regulatory Complexity

Different countries have varying rules regarding:

Data localization

Foreign exchange laws

Merchant onboarding

Anti-fraud compliance

Gateways must continuously adapt to these requirements.

c. Fraud Risk

Cross-border fraud is more sophisticated, requiring advanced risk management systems.

d. Settlement Delays

International settlements sometimes take longer due to intermediary banks and FX processes.

e. Currency Volatility

Exchange rate fluctuations can impact merchant revenues unless hedged properly.

7. The Future of International Payment Gateways

Global payment systems are evolving fast with new technologies:

a. Blockchain and Crypto Payments

Decentralized systems promise:

Instant cross-border transfers

Lower fees

Transparent settlements

Gateways are increasingly integrating stablecoin and blockchain-based payments.

b. AI-Based Fraud Systems

AI models help detect suspicious behavior in milliseconds, reducing chargebacks.

c. Real-Time Cross-Border Payments

New initiatives like SWIFT gpi, UPI-Linkages, and digital currency corridors are speeding up transactions globally.

d. Embedded Finance

Gateways will become part of every app, allowing payments through social media, messaging apps, and IoT devices.

Conclusion

International payment gateways are essential for enabling smooth, secure, and efficient global transactions. They empower businesses of all sizes to expand worldwide by offering multi-currency support, global payment methods, compliance tools, and advanced security systems. While challenges such as regulatory complexity and fraud risks remain, technological advancements are continuously improving the speed, safety, and affordability of cross-border payments. In an increasingly interconnected world, international payment gateways will remain at the center of global commerce, driving digital trade and financial inclusion across nations.

Investing in the World Trade Market1. Understanding the World Trade Market

The world trade market is not a single unified marketplace. Instead, it consists of several interconnected segments:

Goods and Services

Countries trade products such as automobiles, electronics, oil, agricultural goods, and software services. Investors can participate through stocks, ETFs, or multinational companies involved in global trade.

Foreign Exchange (Forex)

Global currency trading supports international business. Investors participate to profit from exchange rate fluctuations driven by economic data, interest rates, and geopolitical events.

Commodities

Oil, natural gas, gold, silver, wheat, and other commodities are exchanged globally. Commodity markets are crucial because they influence trade balances, inflation, and corporate profitability.

Global Financial Markets

International stock markets, bonds, derivatives, and cross-border investment instruments allow investors to trade foreign assets.

Together, these components form the backbone of global commerce, offering multiple investment avenues.

2. Why Invest in the World Trade Market?

a. Diversification Beyond Domestic Borders

Investing globally spreads risk across countries and industries. When one nation faces recession, another may experience growth. Diversification helps protect capital from country-specific political or economic downturns.

b. Access to High-Growth Economies

Many emerging markets—India, China, Vietnam, Brazil, and African economies—offer rapid growth rates higher than developed countries. Investing early in these regions can yield substantial long-term returns.

c. Exposure to Global Brands

Companies like Apple, Toyota, Samsung, Nestlé, and LVMH operate across continents. Investors benefit from their global revenues and stability.

d. Currency Appreciation

Global investing exposes investors to foreign currencies. Gaining from strong currencies can multiply returns when converted back into the home currency.

e. Hedge Against Domestic Market Instability

If the domestic market faces inflation, political instability, or economic slowdown, global assets may provide stability.

3. Ways to Invest in the World Trade Market

Investors can participate globally in several ways depending on risk tolerance, knowledge, and financial goals.

a. International Stocks

Investors can buy shares of foreign companies through:

Direct foreign exchanges

Indian brokers offering global investment accounts

American Depositary Receipts (ADRs)

Global Depositary Receipts (GDRs)

This provides direct exposure to overseas corporations.

b. Exchange-Traded Funds (ETFs)

Global ETFs track:

Foreign stock indices (e.g., S&P 500, Nikkei, FTSE)

Global bonds

Emerging markets

Commodities

Multi-asset portfolios

They offer simplicity, diversification, and lower cost.

c. Forex Trading

Investors trade currency pairs like:

USD/INR

EUR/USD

GBP/JPY

Forex gives quick profit potential but carries high volatility and requires knowledge.

d. Commodity Investments

Investors can trade:

Gold and silver

Oil and natural gas

Agriculture (wheat, cotton, coffee)

Commodities are influenced by supply–demand dynamics, weather, geopolitical tensions, and global economic cycles.

e. Global Mutual Funds

Mutual fund companies offer international and global schemes, allowing investors exposure without direct trading in foreign markets.

f. Investing in Multinational Corporations (MNCs)

Buying shares of companies heavily engaged in global trade gives indirect access to world markets. These companies spread risk across continents and benefit from diverse revenue streams.

g. Digital Assets (Crypto)

Crypto markets operate globally and provide decentralized trading opportunities. However, they carry higher risk and require regulatory awareness.

4. Factors Driving Success in World Trade Investments

To succeed in the world trade market, investors must understand key global drivers.

a. Geopolitical Stability

Conflicts, trade wars, sanctions, or diplomatic tensions affect global markets. For example:

War can raise oil and gold prices.

Trade sanctions can reduce corporate profits.

Political instability disrupts supply chains.

b. Economic Indicators

Investors track:

GDP growth

Inflation

Interest rates

Employment data

Consumer spending

Countries with strong indicators attract foreign capital and generate higher returns.

c. Global Supply Chain Trends

Events like pandemics, port shutdowns, or semiconductor shortages create volatility. Understanding these trends helps investors position themselves better.

d. Currency Strength

A strong foreign currency boosts returns when converted back into the home currency. Conversely, currency depreciation can reduce profits.

e. Technological Advancements

Technology facilitates global trade through:

E-commerce

Digital payments

Blockchain logistics

AI-driven global analytics

Industries adopting modern innovations often grow faster.

5. Risks of Investing in the World Trade Market

While opportunities are high, global investing carries distinct risks.

a. Currency Risk

A profitable foreign investment could still result in loss if the target country’s currency weakens relative to the investor’s home currency.

b. Geopolitical Risk

Wars, coups, border disputes, and political changes can disrupt markets.

c. Regulatory Differences

Each country has unique taxation rules, trading restrictions, and compliance standards.

d. Economic Instability

Recessions, inflation, or corporate bankruptcy in foreign nations can negatively affect investments.

e. Liquidity Risk

Some international markets lack trading volume, making it hard to buy or sell assets quickly.

f. Information Gap

Investors may not fully understand foreign markets due to language, cultural, or informational barriers.

Understanding and mitigating these risks is crucial for long-term success.

6. Strategies for Smart Global Investing

a. Research Countries Before Investing

Consider:

Economic strength

Growth potential

Political stability

Currency trends

Market regulations

b. Diversify Across Regions

Spread investments across:

Developed markets (USA, Europe, Japan)

Emerging markets (India, Brazil, Indonesia)

Frontier markets (Africa, Vietnam)

c. Use Global ETFs for Beginners

They provide:

Automated diversification

Low cost

Easy access

Reduced risk

d. Hedge Currency Exposure

Some global funds offer currency-hedged versions to minimize exchange-rate risk.

e. Keep a Long-Term Perspective

Global markets move slower than domestic ones but yield stable, compounding returns over time.

f. Stay Updated with Global News

Monitor:

Trade agreements

Economic releases

Interest-rate decisions

Commodity price movements

Being informed helps anticipate trends earlier.

7. The Future of the World Trade Market

The next decade will transform global investing due to:

Rise of digital currencies

Expansion of India and Southeast Asia

Major shifts in manufacturing hubs

AI-driven global forecasting

Green energy and carbon-credit trading

Growth of cross-border fintech platforms

Global trade is becoming faster, more digital, and more interconnected, opening significantly larger opportunities for investors worldwide.

Conclusion

Investing in the world trade market allows investors to participate in the global economy, benefit from international growth, and diversify their portfolios beyond domestic boundaries. Although it comes with risks such as currency fluctuations, political uncertainty, and regulatory complexities, strategic planning, informed research, and diversification can help investors achieve strong long-term returns. As the world continues to integrate economically, global markets will increasingly influence investment outcomes, making world trade investing not only an opportunity but a necessity for modern investors.

Global Market Time Zone Arbitrage1. What Is Time Zone Arbitrage?

Time zone arbitrage refers to exploiting temporary mispricing in financial instruments caused by non-overlapping market hours. For example:

The U.S. market closes when the Asian markets are asleep.

The European market opens before the U.S., but after Asia has already moved.

Commodity futures in the U.S. may reflect global sentiment before Asian equity markets reopen.

These gaps create windows where prices adjust with a delay, allowing arbitrageurs to act quickly and capture profits.

The concept relies on the fact that markets, although globally integrated, respond to information at different times, and liquidity varies across sessions. This gives rise to price distortions that can be exploited for profit.

2. Why Time Zone Differences Create Arbitrage Opportunities

Several factors contribute to these opportunities:

A. Information Lag

When important economic data or geopolitical news is released during the closing hours of one market, the impact may not be priced into another market until it opens. Examples:

U.S. Federal Reserve announcements occur late in Asian hours.

European inflation data releases affect U.S. futures before cash markets open.

Traders who act early benefit from this information time lag.

B. Liquidity Imbalances

Liquidity varies across time zones. For example:

Asian markets often have lower liquidity for U.S.-linked ETFs.

Pre-market and after-hours trading in U.S. equities is less liquid, leading to wider spreads.

European market open tends to see high liquidity as it overlaps with Asian close.

Lower liquidity often leads to temporary distortions in pricing, ideal for arbitrage strategies.

C. Market Sentiment Spillover

Global sentiment travels through markets based on opening times:

Asian sell-offs usually influence the European open.

European movements influence U.S. futures.

U.S. closing trends flow into the next Asian session.

This chain reaction allows traders to anticipate moves and position themselves accordingly.

D. Different Valuation Models Across Regions

Investors in different regions may weigh information differently.

For example:

U.S. tech stocks heavily influence global sentiment, but Asian tech ETFs priced in local currencies may react with a delay.

European energy companies may react differently to U.S. crude price moves than American companies.

These valuation differences create price gaps.

3. Types of Time Zone Arbitrage

1. Cross-Market Equity Arbitrage

This involves using price movements in one market to predict movements in another.

Example:

U.S. NASDAQ falls 3% overnight.

Asian tech-heavy indices like Nikkei or Hang Seng tend to gap down at open.

Traders position themselves early to capture the expected gap.

2. ETF–Underlying Asset Arbitrage

Many global ETFs trade in the U.S., even when their underlying markets are closed.

Example:

The iShares MSCI Japan ETF (EWJ) trades in U.S. hours.

If EWJ falls after the Tokyo Stock Exchange closes, traders anticipate Tokyo will open lower.

Institutions buy or short the ETF after hours, then hedge positions when the underlying market opens.

3. Currency-Futures Arbitrage

Foreign exchange markets operate 24/5, but liquidity shifts across regions.

Example:

Strong U.S. economic data strengthens the USD late in U.S. hours.

Asian markets may adjust sharply at open using this new information.

Futures on currency pairs (e.g., JPY/USD) can show early reactions that are not yet reflected in related equity markets.

4. Commodity–Equity Arbitrage

Commodities like gold, oil, and copper trade nearly 24/7.

Copper price drops in the U.S. session might not immediately reflect in mining stocks in Australia until their market opens.

These mismatches create short-term arbitrage chances.

5. Index Futures vs. Cash Market Arbitrage

Index futures trade almost continuously, while cash equity markets operate only during specific hours.

Example:

S&P 500 futures drop at 2 AM during Asian hours.

Asian markets react immediately.

U.S. cash market does not reflect this drop until the New York open.

This delay produces opportunities for traders watching futures across time zones.

4. Practical Examples of Time Zone Arbitrage

A. U.S. Market Influence on Asia

Let’s say:

U.S. S&P 500 closes down 2% due to weak jobs data.

Asian markets are closed during the news release.

Asia opens and gaps down dramatically.

Traders monitoring U.S. data can pre-position in futures or ADRs (American Depositary Receipts).

B. European Market Influence on U.S. Pre-Market

Suppose:

ECB announces an unexpected rate cut at 12:45 PM CET.

U.S. markets are still hours from opening.

U.S. futures move first, followed by cash markets during the opening bell.

Knowledgeable traders arbitrage these price changes before U.S. markets react fully.

C. Gold Arbitrage Between U.S. and Asian Markets

Gold is priced globally, but miners operate regionally.

Example:

COMEX Gold drops at midnight Indian time.

Indian gold-linked equities and ETFs adjust only at market open.

This lag is a profitable window.

5. Risks In Time Zone Arbitrage

While lucrative, the strategy carries risks:

A. Unexpected News Before Market Open

Markets can reverse due to:

Overnight geopolitical events

Emergency press conferences

Central bank surprises

These can eliminate expected gaps.

B. Currency Volatility

When arbitraging international assets, currency swings can cut or reverse profits.

C. Liquidity Risks

After-hours markets often have:

Low volume

Wider spreads

High slippage

This makes execution tricky.

D. Overcrowding of Trades

Institutions and algorithms aggressively exploit these inefficiencies. When too many traders take the same position, the arbitrage window closes quickly.

6. Why Time Zone Arbitrage Still Exists Today

Despite globalization, arbitrage opportunities persist because:

Not all markets operate 24/7.

Retail sentiment spreads slower than institutional news.

Economic data releases are timed for specific countries.

Policy decisions occur during local business hours.

ETFs allow price discovery even when cash markets are shut.

These structural features ensure that time zone arbitrage will continue to remain relevant.

7. Conclusion

Global market time zone arbitrage is a sophisticated trading strategy that leverages asynchronous market hours, delayed price adjustments, and global sentiment flows. While technology has reduced many inefficiencies, markets still respond locally to global news at different times, and liquidity remains uneven across sessions. By understanding how information travels from Asia to Europe to the U.S. and back again, traders can identify profitable windows where prices have not fully adjusted.

However, success in time zone arbitrage requires speed, precision, risk management, and a deep understanding of global macroeconomics. For well-prepared traders, it remains a valuable tool for capturing short-term profits in an interconnected yet time-segmented financial world.

Foundations of Success in the Global Market1. Deep Understanding of Global Market Dynamics

Every global expansion begins with a profound understanding of how markets operate across regions. This includes analyzing demand patterns, competition, consumer behavior, regulatory environments, and geopolitical factors. Markets do not follow identical cycles; a product highly successful in one geography may fail in another due to cultural, economic, or regulatory differences.

Companies that succeed globally invest extensively in market research, scenario planning, and trend forecasts. They pay attention to currency fluctuations, trade policies, tariffs, inflation trends, and global supply chains. Furthermore, understanding demographic dividends—such as Asia’s young workforce or Europe’s aging population—helps shape long-term strategies. A sophisticated grasp of these global dynamics allows organizations to remain resilient during disruptions such as recessions, political conflicts, or inflationary periods.

2. Strong Value Proposition and Differentiation

To compete successfully in global markets, companies must offer a differentiated value proposition. Whether it is unique technology, superior customer service, competitive pricing, or exceptional product quality, differentiation forms the foundation of brand strength.

Global leaders like Apple, Toyota, and Unilever win because they combine innovation with consistent value across markets. Their products may be localized, but their core strengths—design, reliability, or trust—remain intact. Differentiation also requires understanding local competitors. In many emerging markets, domestic companies understand consumer needs better and compete aggressively on price. A global company must therefore offer something that local players cannot easily replicate.

3. Innovation and Technological Capability

Technology is the engine of global competitiveness. The world’s leading companies invest heavily in research, digital processes, AI, automation, analytics, and cutting-edge product development. Technology allows companies to scale faster, optimize costs, and improve quality.

In the global market, the rapid adoption of cloud infrastructure, digital payments, IoT, and AI-driven decision-making has become a baseline expectation. Businesses that fail to innovate eventually lose relevance, even if they previously dominated their sector.

Moreover, technology enhances global coordination. Modern supply chains rely on real-time data, tracking, forecasting, and predictive analytics. This allows companies to manage disruptions—such as shipping delays or raw material shortages—more efficiently.

4. Cultural Intelligence and Localization

Cultural understanding is one of the strongest predictors of global success. Brands that ignore cultural nuances risk alienating their target markets. Localization does not simply mean translating language—it involves adapting product features, packaging, branding, payment options, and customer experience.

For instance, global food chains modify menus to reflect local tastes. Tech companies adjust user interfaces to reflect regional preferences. Fashion brands adapt collections to climate and cultural attire norms.

Cultural intelligence also extends to building local teams. Companies that empower regional leadership often perform better because they understand local realities. Culturally intelligent companies build diverse teams, foster inclusive practices, and ensure global collaboration.

5. Financial Strength and Risk Management

Success in the global market demands strong financial planning and robust risk management. Global companies face currency volatility, geopolitical risks, regulatory changes, and tax complexities. Proper risk management includes:

Hedging currency exposure

Diversifying revenue streams

Maintaining strong cash flows

Building geographically diverse supply chains

Conducting country-risk assessments

Financial resilience also requires disciplined capital allocation—investing in high-growth regions, avoiding unprofitable expansions, and balancing short-term profits with long-term strategy.

6. Operational Excellence and Supply Chain Mastery

Operational efficiency is critical when competing in multiple markets with varying logistics infrastructures and regulatory rules. Efficient supply chain management ensures cost reduction, faster delivery, and higher customer satisfaction.

Successful global companies build flexible supply chains that can adapt to disruptions like pandemics, geopolitical tensions, or natural disasters. They diversify manufacturing locations, establish strong vendor partnerships, and invest in digital supply chain tools to improve transparency and predictive capability.

Operational excellence also includes sustainable manufacturing, lean processes, automation, and quality control across all facilities.

7. Strong Leadership and Strategic Vision

Leadership defines whether a company can successfully navigate global complexity. Visionary leaders create strategic pathways, inspire innovation, and balance global integration with local autonomy.

Successful leaders think long-term—they understand that global scale is not achieved overnight. They anticipate changes in technology, consumer behavior, and geopolitical environments. Building a global brand requires clarity of purpose, adaptability, resilience, and the ability to make decisive yet data-driven decisions.

8. Agility and Speed of Execution

The speed at which a company adapts to market changes often determines its global competitiveness. Markets evolve rapidly—trends emerge, technologies shift, and consumer expectations rise.

Agile companies respond quickly to new competitors, regulatory changes, and economic events. They make fast decisions, accelerate product development, and revise strategies based on real-time data. Agility also implies the willingness to pivot—entering new segments, adjusting pricing, or redesigning supply chains when needed.

9. Strong Branding and Trustworthiness

Global success demands a powerful, credible brand. Trust is a universal currency; companies that maintain consistent quality, honesty, and transparency build stronger customer loyalty.

Brand trust is built through:

Quality products

Ethical practices

Strong customer support

Responsible marketing

Sustainability initiatives

In today’s world, customers expect companies to demonstrate environmental responsibility and social commitment. Brands that embody these values enjoy stronger global appeal.

10. Compliance, Governance, and Ethical Standards

Operating globally requires adherence to a complex web of regulations—trade laws, data privacy rules, labor laws, environmental regulations, and industry-specific standards. Non-compliance can cause financial penalties, reputational damage, or even shutdowns.

Successful global companies maintain strong governance systems, auditing procedures, and internal controls. Ethical behaviour is equally important. Companies committed to fairness, transparency, and responsible business gain long-term goodwill and sustainable growth.

Conclusion

The foundations of success in the global market are multidimensional. Businesses must master global dynamics, innovate continuously, and adapt quickly. Cultural intelligence, operational excellence, risk management, and strong leadership form the core building blocks. While the global market is highly competitive, companies that combine vision, agility, and strategic discipline can build enduring international success. In a world where change is constant, the true winners will be those who innovate faster, understand customers better, and maintain the highest standards of excellence everywhere they operate.

Global Market Risks1. Macroeconomic Risks

a. Inflation and Interest Rate Volatility

Inflation is one of the most significant global risks. When inflation rises, central banks respond by increasing interest rates, which affects borrowing costs, consumer spending, corporate profitability, and international capital flows.

High inflation erodes purchasing power, disrupts business planning, and raises input costs. Meanwhile, sudden interest rate hikes can trigger equity market corrections, real estate slowdowns, and capital outflows from emerging markets. Even a minor shift in policy by the U.S. Federal Reserve or European Central Bank can ripple through global markets.

b. Economic Slowdowns and Recessions

Recessions in major economies like the U.S., China, and the EU create worldwide ripples. Sluggish demand reduces exports, commodity consumption, foreign investments, and corporate earnings. For emerging economies dependent on global trade, a slowdown in developed markets can lead to unemployment, fiscal pressure, and currency instability.

2. Geopolitical Risks

a. Wars, Conflicts, and Political Tensions

Geopolitical tensions—whether in Eastern Europe, the Middle East, or the Indo-Pacific—lead to supply chain disruptions, commodity price volatility, and investor uncertainty. Wars or sanctions can affect energy markets, shipping routes, and cross-border financing. Any conflict involving major nations increases volatility across equities, bonds, and commodity markets.

b. Trade Wars and Tariffs

Rising protectionism can severely impact global trade flows. Trade wars between economic giants like the U.S. and China create uncertainty for global manufacturers, exporters, and consumers. Tariffs raise the cost of goods, reduce competitiveness, and distort global supply chains.

c. Political Instability

Governments facing elections, regime changes, policy uncertainty, or civil unrest create unpredictable market conditions. Investors tend to withdraw capital from politically unstable regions, weakening currencies and stock markets.

3. Currency and Exchange Rate Risks

In global markets, currency movements are one of the most immediate risk factors. Exchange rate fluctuations can affect:

Export competitiveness

Import costs

Foreign debt repayments

Profit margins for multinational companies

Emerging markets are especially vulnerable. A strong U.S. dollar often leads to capital outflows, weakening local currencies and making dollar-denominated debt more expensive. Sudden devaluations can trigger financial crises, as seen in past Asian, Latin American, and Turkish market events.

4. Financial Market Risks

a. Stock Market Volatility

Global equity markets are influenced by economic data, corporate earnings, geopolitical news, and investor sentiment. High-frequency trading, derivatives, and speculation can amplify volatility. Market bubbles—often driven by excessive liquidity—can burst suddenly, leading to massive wealth destruction.

b. Bond Market Risk

Government and corporate bond markets face interest rate, credit, and liquidity risks. Rising rates reduce bond prices, while weaker economies increase default risk. Sovereign debt crises (like those seen in Greece or Argentina) can threaten the entire global financial system.

c. Banking System Risk

Banking failures or liquidity shortages can spread quickly across borders. The global financial system is interconnected, and stress in one region can impact banks worldwide through money markets, cross-border loans, and derivatives exposure.

5. Commodity Market Risks

a. Energy Prices

Oil and natural gas prices are influenced by geopolitics, OPEC decisions, supply disruptions, and global demand. Sharp swings impact inflation, transportation, manufacturing costs, and country finances—especially for oil-dependent economies.

b. Agricultural Commodities

Climate change, extreme weather, export restrictions, and global supply chain issues affect food prices. Food inflation can trigger political instability and global humanitarian risks.

c. Metals and Minerals

Industrial and precious metals are affected by mining output, geopolitical tensions, green-energy demand, and currency strength. For nations dependent on metal exports, price declines pose fiscal and economic threats.

6. Supply Chain and Logistics Risks

Global supply chains became highly vulnerable after the pandemic. Key risks include:

Shipping delays

Port congestion

Container shortages

Dependence on single-country manufacturing

Labour strikes

Trade restrictions

Disruptions lead to higher production costs, longer delivery times, inventory shortages, and reduced global trade efficiency. Critical industries—such as semiconductors, pharmaceuticals, and electronics—are especially exposed.

7. Technological and Cybersecurity Risks

In a world dependent on digital infrastructure, cyber risks are among the most dangerous. Cyberattacks can disrupt:

Banks and payment systems

Stock exchanges

Government operations

Energy grids

Corporate networks

Data theft, ransomware, and hacking incidents create financial losses, reputational damage, and operational outages. As AI and automation expand, cyber vulnerabilities become even more critical.

8. ESG and Climate Change Risks

a. Extreme Weather and Climate Events

Floods, droughts, hurricanes, and wildfires disrupt agriculture, infrastructure, and global supply chains. They raise insurance costs and reduce productivity. Climate risks also shift commodity markets, increase inflation, and strain government budgets.

b. Energy Transition Risks

As countries transition to renewable energy, fossil fuel industries face structural decline. Companies that fail to adapt can suffer large losses or collapse. Investors are also exposed to sudden regulatory changes like carbon taxes or bans on polluting technologies.

c. ESG-Driven Regulatory Risks

Businesses must comply with stricter environmental, social, and governance (ESG) rules. Non-compliance may lead to fines, supply chain disruption, or loss of investor support.

9. Global Debt Risks

Rising global debt—household, corporate, and government—creates major vulnerabilities. High debt levels reduce resilience during shocks. When rates rise, debt servicing becomes costlier, increasing the risk of defaults. Some countries face unsustainable debt burdens, threatening global financial stability.

10. Black Swan and Systemic Risks

Black swan events—rare and unpredictable shocks—can completely reshape markets. Examples include:

Pandemics

Natural disasters

Financial collapses

Major technological failures

Sudden geopolitical crises

Systemic risks occur when failures in one sector spread widely, as seen in the 2008 crisis. Today’s interconnected digital-financial world makes systemic risk more threatening than ever.

Conclusion

Global markets face a wide spectrum of risks—economic, geopolitical, financial, technological, environmental, and systemic. Because global economies are closely linked, shocks in one region often spread rapidly across continents. Managing these risks requires diversification, strong policy frameworks, technological resilience, and timely strategic decisions. Understanding these risks is the first step for investors, businesses, and governments to stay prepared in an increasingly uncertain world.

MiCA Phase 2: Europe’s New Trading RulesRegulation has always been one of the biggest factors shaping market structure.

With MiCA Phase 2 coming into effect in 2026, the European crypto landscape is about to transform more than at any point in the last decade.

While MiCA Phase 1 focused mainly on stablecoins and basic crypto service providers, Phase 2 introduces a deep, structural regulatory framework for:

trading platforms

crypto brokers

custodial services

risk disclosures

transparency standards

From the perspective of industry participants — including firms analyzed in the Taurus Acquisition market segment — the shift is clear: Europe is moving toward a more transparent, predictable, and institution-ready crypto environment.

1. What MiCA Phase 2 Means for Traders

1. Mandatory Client Asset Segregation

Platforms and brokers will be required to separate client funds from company reserves.

For traders, this means:

stronger protection against counterparty failure

clearer accounting of where assets are held

reduced systemic risk during market volatility

This is a core topic often highlighted in market commentary surrounding institutional-grade providers, including those discussed in the Taurus Acquisition space.

2. Full Transparency of Fees and Execution Models

Under MiCA Phase 2, crypto platforms must present:

spreads

commissions

execution rules

liquidity routes

all additional costs

No hidden fees, no complex pricing structures.

For retail traders, this transparency makes comparison easier.

For brokers, it sets a clear bar: execution must be both fair and openly documented.

3. Detailed Risk Disclosures

Products with leverage, derivatives, margin exposure or elevated volatility must come with standardized, easy-to-understand disclosures.

That includes:

clear risk rating

market volatility indicators

liquidation risk

liquidity mechanics

MiCA forbids overly promotional language, forcing the market to focus on education, not aggressive marketing.

2. What Changes for Brokers and Platforms in 2026

1. Higher Licensing Requirements

Brokers serving EU clients will need:

stronger AML/KYC frameworks

defined internal controls

cybersecurity standards

capital adequacy requirements

external audits

This creates a structural filter that elevates the entire market’s professionalism — an important shift aligned with many operational practices associated with companies evaluated within the Taurus Acquisition market category.

2. Compulsory Incident Disclosure

Brokers must report:

system outages

execution disruptions

major liquidity issues

technical failures

In practice, this means traders gain more visibility into how infrastructure behaves during high-volatility periods.

3. Stricter Rules for High-Risk Products

MiCA Phase 2 may limit:

extreme leverage

non-transparent synthetic instruments

high-risk derivative structures

The goal is not to restrict trading, but to ensure users understand risk properly — something institutions have been requesting for years.

3. Who Benefits From MiCA Phase 2?

✔ Retail Traders

stronger asset protection

better pricing transparency

easier verification of licensed brokers

clearer risk communication

This reduces the probability of encountering underregulated platforms that were common in earlier market cycles.

✔ Compliant Brokers

Firms that already operate with clear standards — including those often evaluated for institutional processes such as Taurus Acquisition — benefit from an environment where transparency is mandatory and low-quality competitors fade out.

✔ Institutional Investors

MiCA lays the groundwork for institutional adoption by making Europe one of the safest regulated crypto environments in the world.

4. Who May Be Challenged by MiCA?

❌ Unregulated Brokers

MiCA Phase 2 will force many operators without proper infrastructure to exit the EU market.

❌ Platforms with Hidden Fees

Spread manipulation or unclear execution paths are no longer acceptable.

❌ Firms Unable to Meet Licensing Standards

Capital requirements and risk controls may push out underdeveloped businesses.

5. What Should Traders Do Before 2026?

verify whether their platform is MiCA-ready

check licensing status

review the platform’s execution policy

analyze transparency of spreads and fees

evaluate risk tools and disclosures

This preparation ensures smooth adaptation when MiCA Phase 2 becomes active.

MiCA Phase 2 introduces a new era for European crypto markets:

transparent pricing

stronger asset protection

clearer risk communication

higher operational standards

From a broader industry viewpoint — including case studies and operational comparisons seen around Taurus Acquisition — 2026 represents a shift toward institutional-grade market structure.

For traders, the outcome is a more stable, organized, and predictable environment.

For brokers, it is a test of operational maturity and regulatory readiness.

Major Economic Inflation Alert in the Global Market1. Understanding the Nature of the Current Inflation Alert