MSTR mNAV indicatorTrack and compute MicroStrategy's mNAV (EV divided by BTC reserve value) over time. - compute method: www.strategy.com - data source: www.strategy.comPine Script® indicatorby ballcatcUpdated 19

Global Market Scanner [Armi Goldman]Concept This indicator is designed to provide a comprehensive "Bird's Eye View" of the global financial economy. Instead of focusing on a single chart, this dashboard allows traders to monitor capital rotation across every major asset class simultaneously. By tracking the Money Flux (daily percentage change) of these markets, users can instantly identify if the market environment is "Risk-On" (flowing into assets) or "Risk-Off" (fleeing to cash/bonds). Features The dashboard displays a real-time table in the top-right corner tracking 9 key sectors: US M2 Money Supply: The broad measure of liquidity availability. US Dollar (DXY): The global currency baseline. Global Stocks (VT): World equities performance. Crypto Market: Total cryptocurrency market capitalization. Commodities: Gold, Silver, and Crude Oil (WTI). Real Estate: Vanguard Real Estate ETF (VNQ). Bonds: US Aggregate Bond Market. How it Works The script utilizes request.security() to fetch data from multiple asset classes regardless of the chart you are currently viewing. Flux Calculation: The "Flux" column calculates the daily percentage change (Close - Open) / Open. This reveals the immediate direction of capital flow for the current session. M2 Trend: For the Money Supply, the script calculates a 30-day rate of change to determine if the Fed is effectively "Inflating" (adding liquidity) or "Tightening" (removing liquidity). Status Logic: The status column uses conditional logic to assign readable labels (e.g., "INFLOW" vs "OUTFLOW" or "STRONGER" vs "WEAKER") based on the positive or negative value of the Flux. How to Use Risk-On Signal: If Stocks, Crypto, and Real Estate show green "INFLOW" status while the Dollar (DXY) is red, capital is deploying into risk assets. Flight to Safety: If Gold and Bonds are green while Equities are red, investors may be hedging against fear. Cash is King: If DXY is strong (Green) and almost all other assets are red, liquidity is drying up and moving into Cash. Liquidity Watch: Monitor the US M2 Supply. A simplified view is that when M2 is "Inflating," it provides a long-term tailwind for asset prices. Tickers Used Liquidity: ECONOMICS:USM2 Currency: TVC:DXY Equities: AMEX:VT (Total World Stock ETF) Real Estate: AMEX:VNQ (Vanguard Real Estate) Bonds: AMEX:AGG Commodities: TVC:GOLD, TVC:SILVER, TVC:USOIL Crypto: CRYPTOCAP:TOTAL Disclaimer This tool is for informational purposes only and does not constitute financial advice.Pine Script® indicatorby armigoldman2212

Crypto Market Pulse: Dom vs Vol AnalyzerConcept & Methodology The core logic of this indicator is based on the "Money Flow" theory. It aggregates data from multiple sources (CRYPTOCAP:TOTAL, BTC.D, BINANCE:BTCUSDT) to provide a comprehensive market overview in a single panel. Key Calculations: Total Market Cap & Volume: Fetches real-time data to determine the overall health of the market. Inverse Dominance Logic: Unlike standard indicators, this script applies inverse color coding to Bitcoin Dominance (BTC.D). When BTC Dominance drops, it is colored Green (indicating liquidity flowing into Altcoins). When BTC Dominance rises, it is colored Red (indicating risk for Altcoins). Volume Delta: Compares the current timeframe's volume against the previous candle to calculate the percentage change, highlighting sudden liquidity injections. █ Features Real-time Dashboard: Displays Cap, Volume, BTC Price, and BTC Dominance. Altcoin-Focus Coloring: Automatically interprets data to favor Altcoin traders (Green Signals = Good for Alts). Dynamic Alerts: Volume Surge Alert: Triggers when volume exceeds a user-defined threshold (default +50%), signaling potential breakout activity. Dominance Drop Alert: Triggers when BTC Dominance falls significantly, signaling the start of potential Altcoin movement. █ How to Use Look for Confluence: The ideal "Altseason" signal is when the Total Cap is Green (Market up) AND BTC Dominance is Green (Dominance down). This indicates money is moving from BTC to Alts. Volume Confirmation: Use the Volume row to confirm the strength of the move. A price rise without volume is often a fakeout. Customization: You can adjust the table position and text size from the settings menu to fit your screen setup. Pine Script® indicatorby THF847

TraderForge - Genesis xMA - EMAs + Daily SMAsA clean, powerful multi-MA system designed for momentum and trend clarity on any symbol and any timeframe. Intraday Momentum: • EMA 9, 13, and 21 form a responsive ribbon that reveals direction, pullbacks, and acceleration zones. Higher-Timeframe Trend Structure: • Daily (or any HTF you choose) SMA 20 / 50 / 200 projected on your chart act as long-range “trend rails,” giving you instant awareness of bullish/bearish bias, mean-reversion zones, and key swing levels. Fully Editable: • Change all EMA/SMA lengths • Select any higher timeframe (default: Daily) • Turn each group on/off from the settings panel Simple. Fast. Visual. Perfect for scalping, day trading, or swing analysis. TraderForge — Simple indicators. Powerful results.Pine Script® indicatorby TraderForge4

TraderForge - 15-min Candle StrategyThis indicator automatically identifies the first 15-minute candle of each trading session and projects its high and low across the entire regular trading day. The result is a clear intraday structure level that helps traders visualize opening strength, early volatility, and potential breakout or rejection zones. Using the same projection engine found in the TraderForge Genesis ATR 1.5 system, the lines extend dynamically based on the chart’s timeframe, ensuring perfect alignment on any intraday interval. Features • Plots the 15-minute High and 15-minute Low for the current session • Automatic session detection and value locking • Clean forward projection for the entire market day • Optional labels for quick identification • Works on any intraday timeframe (1m, 5m, 15m, etc.) • No repainting, no drift, no multi-session clutter Ideal for traders who rely on early-session structure, liquidity mapping, or opening range breakout (ORB) concepts. TraderForge – Simple indicators. Powerful results. P.S.: Now only works for 15-minute candles, working on an agnostic version to be released soon. Pine Script® indicatorby TraderForgeUpdated 5

TraderForge - Genesis PDH/PDLThe Genesis PDH/PDL indicator plots the Previous Day High (PDH) and Previous Day Low (PDL) using a clean daily-session engine that locks values at the start of each new trading day. These levels are key markers for liquidity sweeps, breakout zones, reversals, and intraday trend confirmation. How It Works • Pulls yesterday’s high and low directly from the completed Daily candle. • Locks both values the moment a new day begins. • Projects each level across the entire current session for clear intraday reference. • Labels appear only on today’s session, keeping your chart uncluttered. Features • Accurate, non-repainting PDH and PDL. • Automatic day detection and session-wide projection. • Clean, minimal visual styling consistent with the Genesis indicator family. • Optional labels with PDH (black text) and PDL (white text). • Works seamlessly across all intraday timeframes. TraderForge – Simple indicators. Powerful results.Pine Script® indicatorby TraderForge5

SOFR - IORB Spread (pct pts & bps)Tracks short-term funding conditions by measuring the spread between the Secured Overnight Financing Rate (SOFR) and the Fed’s Interest on Reserve Balances (IORB). When SOFR persistently trades above IORB, it signals cash scarcity and stress in overnight funding markets. This indicator is best used as a risk-regime and plumbing health check, not as a directional trading signal. Calm readings allow trends to persist; sustained spikes often precede periods of volatility and forced deleveraging.Pine Script® indicatorby TheRealJSmith2

EMA (Dynamic Labels)📈 EMA Dynamic Labels - Multi-Timeframe Moving Averages A clean and efficient indicator displaying multiple Exponential and Simple Moving Averages with dynamic labels that follow price action in real-time. ✨ FEATURES: 📊 7 Moving Averages: - EMA 13, 25, 32 (short-term trend) - MA 100 (medium-term reference) - SMMA 200 (long-term trend) - MA 300 (major support/resistance) - 4H EMA 200 (multi-timeframe perspective) 🏷️ Dynamic Labels: Automatically positioned labels that update on the latest candle, making it easy to identify each moving average ⚙️ Fully Customizable: - Toggle any MA on/off individually - Adjust all periods to fit your strategy - Global source selection (close, open, hl2, etc.) - Control label display and offset 🎨 Color-Coded: Each MA has a distinct color for quick visual identification ⚡ Optimized Performance: Efficient code that calculates only what's needed 🎯 BEST FOR: - Trend following strategies - Support/resistance identification - Multi-timeframe analysis - Clean chart visualization 💡 PRO TIP: Use the 4H EMA 200 on lower timeframes to align with higher timeframe trends for better trade entries. 🚀 HOW TO USE: 1. Add to your chart 2. Customize periods and colors in settings 3. Toggle MAs on/off based on your trading style 4. Use labels for quick reference without cluttering your chart Perfect for day traders, swing traders, and position traders who rely on moving averages for their decision-making process. 💪Pine Script® indicatorby vektorxbt3

Open Interest RSI [BackQuant]Open Interest RSI A multi-venue open interest oscillator that aggregates OI across major derivatives exchanges, converts it to coin or USD terms, and runs an RSI-style engine on that aggregated OI so you can track positioning pressure, crowding, and mean reversion in leverage flows, not just in price. What this is This tool is an RSI built on top of aggregated open interest instead of price. It pulls futures OI from several major exchanges, converts it into a unified unit (COIN or USD), sums it into a single synthetic OI candle, then applies RSI and smoothing to that combined series. You can then render that Open Interest RSI in different visual modes: Clean line or colored line for classic oscillator-style reads. Column-style oscillator for impulse and compression views. Flag mode that fills between OI RSI and its EMA for trend/mean reversion blends. See: Heatmap mode that paints the panel based on OI RSI extremes, ideal for scanning. See: On top of that it includes: Aggregated OI source selection (Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit). Choice of OI units (COIN or USD). Reference lines and OB/OS zones. Extreme highlighting for either trend or mean reversion. A vertical OI RSI meter that acts as a quick strength gauge. Aggregated open interest source Under the hood, the indicator builds a synthetic open interest candle by: Looping over a list of supported exchanges: Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit. Looping over multiple contract suffixes (such as USDT.P, USD.P, USDC.P, USD.PM) to capture different contract types on each venue. Requesting OI candles from each venue + contract combination for the same underlying symbol. Converting each OI stream into a common unit: In COIN mode, everything is normalized into coin-denominated OI. In USD mode, coin OI is multiplied by price to approximate notional OI. Summing up open, high, low and close of OI across venues into a single aggregated OI candle. If no valid OI is available for the current symbol across all sources, the script throws a clear runtime error so you know you are on an unsupported market. This gives you a single, exchange-agnostic open interest curve instead of being tied to one venue. That aggregated OI is then passed into the RSI logic. How the OI RSI is calculated The RSI side is straightforward, but it is applied to the aggregated OI close: Compute a base RSI of aggregated OI using the Calculation Period . Apply a simple moving average of length Smoothing Period (SMA) to reduce noise in the raw OI RSI. Optionally apply an EMA on top of the smoothed OI RSI as a moving average signal line. Key parameters: Calculation Period – base RSI length for OI. Smoothing Period (SMA) – extra smoothing on the RSI value. EMA Period – EMA length on the smoothed OI RSI. The result is: oi_rsi – raw RSI of aggregated OI. oi_rsi_s – SMA-smoothed OI RSI. ma – EMA of the smoothed OI RSI. Thresholds and extremes You control three core thresholds: Mid Point – central reference level, typically 50. Extreme Upper Threshold – high-level OI RSI edge (for example 80). Extreme Lower Threshold – low-level OI RSI edge (for example 20). These thresholds are used for: Reference lines or OB/OS zone fills. Heatmap gradient bounds. Background highlighting of extremes. The Extreme Highlighting mode controls how extremes are interpreted: None – do nothing special in extreme regions. Mean-Rev – background turns red on high OI RSI and green on low OI RSI, framing extremes as contrarian zones. Trend – background turns green on high OI RSI and red on low OI RSI, framing extremes as participation zones aligned with the prevailing move. Reference lines and OB/OS zones You can choose: None – clean plotting without guides. Basic Reference Lines – mid, upper and lower thresholds as simple gray horizontals. OB/OS Levels – filled zones between: Upper OB: from the upper threshold to 100, colored with the short/overbought color. Lower OS: from 0 to the lower threshold, colored with the long/oversold color. These guides help visually anchor the OI RSI within "normal" versus "extreme" regions. Plotting modes The Plotting Type input controls how OI RSI is drawn. All modes share the same underlying OI and RSI logic, but emphasise different aspects of the signal. 1) Line mode This is the classic oscillator representation: Plots the smoothed OI RSI as a simple line using RSI Line Color and RSI Line Width . Optionally plots the EMA overlay on the same panel. Works well when you want standard RSI-style signals on leverage flows: crosses of the midline, divergences versus price, and so on. 2) Colored Line mode In this mode: The OI RSI is plotted as a line, but its color is dynamic. If the smoothed OI RSI is above the mid point, it uses the Long/OB Color . If it is below the mid point, it uses the Short/OS Color . This creates an instant visual regime switch between "bullish positioning pressure" and "bearish positioning pressure", while retaining the feel of a traditional RSI line. 3) Oscillator mode Oscillator mode renders OI RSI as vertical columns around the mid level: The smoothed OI RSI is plotted as columns using plot.style_columns . The histogram base is fixed at 50, so bars extend above and below the mid line. Bar color is dynamic, using long or short colors depending on which side of the mid point the value sits. This representation makes impulse and compression in OI flows more obvious. It is especially useful when you want to focus on how quickly OI RSI is expanding or contracting around its neutral level. See: 4) Flag mode Flag mode turns OI RSI and its EMA into a two-line band with a filled area between them: The smoothed OI RSI and its EMA are both plotted. A fill is drawn between them. The fill color flips between the long color and the short color depending on whether OI RSI is above or below its EMA. Black outlines are added to both lines to make the band clear against any background. This creates a "flag" style region where: Green fills show OI RSI leading its EMA, suggesting positive positioning momentum. Red fills show OI RSI trailing below its EMA, suggesting negative positioning momentum. Crossovers of the two lines can be read as shifts in OI momentum regime. Flag mode is useful if you want a more structural view that combines both the level and slope behaviour of OI RSI. See: 5) Heatmap mode Heatmap mode recasts OI RSI as a single-row gradient instead of a line: A single row at level 1 is plotted using column style. The color is pulled from a gradient between the lower and upper thresholds: Near the lower threshold it approaches the short/oversold color and near the upper threshold it approaches the long/overbought color. The EMA overlay and reference lines are disabled in this mode to keep the panel clean. This is a very compact way to track OI RSI state at a glance, especially when stacking it alongside other indicators. See: OI RSI vertical meter Beyond the main plot, the script can draw a small "thermometer" table showing the current OI RSI position from 0 to 100: The meter is a two-column table with a configurable number of rows. Row colors form an inverted gradient: red at the top (100) and green at the bottom (0). The script clamps OI RSI between 0 and 100 and maps it to a row index. An arrow marker "▶" is drawn next to the row corresponding to the current OI RSI value. 0 and 100 labels are printed at the ends of the scale for orientation. You control: Show OI RSI Meter – turn the meter on or off. OI RSI Blocks – number of vertical blocks (granularity). OI RSI Meter Position – panel anchor (top/bottom, left/center/right). The meter is particularly helpful if you keep the main plot in a small panel but still want an intuitive strength gauge. How to read it as a market pressure gauge Because this is an RSI built on aggregated open interest, its extremes and regimes speak to positioning pressure rather than price alone: High OI RSI (near or above the upper threshold) indicates that open interest has been increasing aggressively relative to its recent history. This often coincides with crowded leverage and a buildup of directional pressure. Low OI RSI (near or below the lower threshold) indicates aggressive de-leveraging or closing of positions, often associated with flushes, forced unwinds or post-liquidation clean-ups. Values around the mid point indicate more balanced positioning flows. You can combine this with price action: Price up with rising OI RSI suggests fresh leverage joining the move, a more persistent trend. Price up with falling OI RSI suggests shorts covering or longs taking profit, more fragile upside. Price down with rising OI RSI suggests aggressive new shorts or levered selling. Price down with falling OI RSI suggests de-leveraging and potential exhaustion of the move. Trading applications Trend confirmation on leverage flows Use OI RSI to confirm or question a price trend: In an uptrend, rising OI RSI with values above the mid point indicates supportive leverage flows. In an uptrend, repeated failures to lift OI RSI above mid point or persistent weakness suggest less committed participation. In a downtrend, strong OI RSI on the downside points to aggressive shorting. Mean reversion in positioning Use thresholds and the Mean-Rev highlight mode: When OI RSI spends extended time above the upper threshold, the crowd is extended on one side. That can set up squeeze risk in the opposite direction. When OI RSI has been pinned low, it suggests heavy de-leveraging. Once price stabilises, a re-risking phase is often not far away. Background colours in Mean-Rev mode help visually identify these periods. Regime mapping with plotting modes Different plotting modes give different perspectives: Heatmap mode for dashboard-style use where you just need to know "hot", "neutral" or "cold" on OI flows at a glance. Oscillator mode for short term impulses and compression reads around the mid line. See: Flag mode for blending level and trend of OI RSI into a single banded visual. See: Settings overview RSI group Plotting Type – None, Line, Colored Line, Oscillator, Flag, Heatmap. Calculation Period – base RSI length for OI. Smoothing Period (SMA) – smoothing on RSI. Moving Average group Show EMA – toggle EMA overlay (not used in heatmap). EMA Period – length of EMA on OI RSI. EMA Color – colour of EMA line. Thresholds group Mid Point – central reference. Extreme Upper Threshold and Extreme Lower Threshold – OB/OS thresholds. Select Reference Lines – none, basic lines or OB/OS zone fills. Extreme Highlighting – None, Mean-Rev, Trend. Extra Plotting and UI RSI Line Color and RSI Line Width . Long/OB Color and Short/OS Color . Show OI RSI Meter , OI RSI Blocks , OI RSI Meter Position . Open Interest Source OI Units – COIN or USD. Exchange toggles: Binance, Bybit, OKX, Bitget, Kraken, HTX, Deribit. Notes This is a positioning and pressure tool, not a complete system. It: Models aggregated futures open interest across multiple centralized exchanges. Transforms that OI into an RSI-style oscillator for better comparability across regimes. Offers several visual modes to match different workflows, from detailed analysis to compact dashboards. Use it to understand how leverage and positioning are evolving behind the price, to gauge when the crowd is stretched, and to decide whether to lean with or against that pressure. Attach it to your existing signals, not in place of them. Also, please check out @NoveltyTrade for the OI Aggregation logic & pulling the data source! Here is the original script: Pine Script® indicatorby BackQuantUpdated 464

Candle RangeCandle Range Displays the total range of each candle (high – low) in pips or ticks. The value appears in the status line and updates as you hover over candles. No bars, labels, or chart clutter — just a clean numeric view of candle volatility. Customize text color and decimal precision. Works for Forex, indices, commodities, and other markets.Pine Script® indicatorby simonyap118Updated 9

BuLLzEyE_MNQ FVG/IFVG SystemFVG Boxes These are the main trading zones. The indicator automatically detects Fair Value Gaps and draws boxes on your chart: • GREEN boxes = Bullish FVG (potential buy zone) • RED boxes = Bearish FVG (potential sell zone) • YELLOW boxes = IFVG (Inverse FVG - filled gaps that now act as support/resistance) • GRAY boxes = Mitigated FVG (gap has been filled) • WHITE dashed line = 50% level (optimal entry point within the FVG) Session Boxes Session boxes show you the high/low range of each major trading session. This helps identify where liquidity sits: • PURPLE = Asia Session (6:00 PM - 3:00 AM ET) • BLUE = London Session (3:00 AM - 12:00 PM ET) • ORANGE = New York Session (9:30 AM - 4:00 PM ET) • TEAL = Sydney Session (5:00 PM - 2:00 AM ET) • LIME GREEN = Kill Zone / London-NY Overlap (8:00 AM - 11:00 AM ET) - BEST TRADING TIME Entry Signals • GREEN triangle pointing UP = Long entry signal at a Bullish FVG (not 100% reliable) • RED triangle pointing DOWN = Short entry signal at a Bearish FVG (not 100% reliable) Liquidity Sweeps • RED X with 'SWEEP' = Previous Day High (PDH) was swept • GREEN X with 'SWEEP' = Previous Day Low (PDL) was swept • Dotted lines = PDH (red) and PDL (green) levels Information Tables HTF Bias Table (Top Right): Shows whether the higher timeframe (default 15m) is bullish or bearish, the number of active FVGs, and whether you're in the trading session. Risk Calculator Table (Bottom Right): Shows your risk amount and calculates how many contracts you can trade for different stop loss sizes (5pt, 10pt, 15pt). How It Works What is a Fair Value Gap? A Fair Value Gap (FVG) is a 3-candle pattern where aggressive buying or selling creates a price void. Specifically, it's when the wick of the first candle doesn't overlap with the wick of the third candle, leaving a gap in between. Price tends to return to these gaps to 'rebalance' before continuing in the original direction. What is an Inverse FVG? When an FVG gets filled (price returns and closes through the gap), it becomes an Inverse FVG (IFVG). These zones flip their polarity - a filled Bullish FVG becomes resistance, and a filled Bearish FVG becomes support. The indicator automatically converts mitigated FVGs to yellow IFVG boxes. The 50% Entry Level The dashed white line in each FVG represents the 50% level (also called Consequent Encroachment). This is considered the optimal entry point - it's the middle of the imbalance where price is most likely to react. Suggested Trading Strategy 1. Check HTF Bias (top right table) - only trade in that direction 2. Wait for a liquidity sweep (SWEEP label appears) 3. Look for an FVG to form AFTER the sweep 4. Enter when price returns to the 50% level (dashed line) 5. Place stop loss below/above the FVG (add 2 ticks buffer) 6. Take profit at 1:2 or 1:3 risk-to-reward ratio Settings Explained FVG Settings • Min FVG Size: Minimum gap size in points to be considered valid (default: 2.0) • Max FVG Age: How many bars until an FVG is removed from chart (default: 50) • Show 50% Entry Level: Toggle the dashed entry line on/off Session Settings • Show Session Boxes: Toggle all session boxes on/off • Max Sessions to Show: How many historical sessions to display (default: 5) • Individual Session Toggles: Turn each session (Asia/London/NY/Sydney/Kill Zone) on or off Risk Calculator Settings • Account Size: Your trading account balance • Risk Per Trade: Percentage of account to risk per trade (default: 0.5%) • Tick Value/Size: Contract specifications for MNQ ($0.50 per tick, 0.25 point tick size) Tips for Best Results 1. Trade during the Kill Zone (8:00-11:00 AM ET) for best volatility and liquidity 2. Always align trades with HTF bias - don't fight the trend 3. Wait for liquidity sweeps before entering - this confirms smart money activity 4. Use the 50% level for entries - it offers the best risk-to-reward 5. Watch for IFVG zones as additional confluence for entries 6. Use the risk calculator to size positions properly - never risk more than you can afford 7. Session boxes help identify where stops are clustered - sweeps of these levels often precede reversals Available Alerts • New FVG Formed (Bullish or Bearish) • Price Touching 50% Entry Level • FVG Mitigated (gap filled) • Long Entry Signal • Short Entry Signal • PDH/PDL Liquidity Sweep ───────────────────────────────────── Created by BullyTrading Designed for MNQ Prop Firm Trading Pine Script® indicatorby Bully566

AOT Red Storm V25 Adaptive EditionOverview AOT Red Storm V25 is an invite-only, institutional-style trend suite designed for intraday and swing traders. It does not try to predict exact tops or bottoms. Instead, it focuses on: Multi-timeframe trend alignment Smart 8-minute internal timeframe for cleaner structure Adaptive support/resistance zones Volatility and volume-based risk filtering A compact HUD to summarize market state in one glance Core Components This script is not a simple mashup of public indicators. It integrates several classic building blocks into a single, coherent decision framework: Adaptive Supertrend Core: Supertrend is calculated on an internal 8-minute timeframe (for intraday charts up to 60m), which we found offers a better balance between noise and structure for crypto futures. WaveTrend Tactical Radar: WaveTrend is only used for exit timing and risk-off zones (overheat / exhaustion), not as a standalone entry trigger. It works together with the trend core and cooldown logic. Dual-Layer Support & Resistance: Local SR zones are drawn on the current chart for execution precision, while 30m-level zones track higher-timeframe liquidity and turning areas. Trendlines & Structural BOS: Automatic trendlines and BOS (Break of Structure) are derived from pivot points, to visualize trend continuation vs. potential reversals. Volatility & Volume Risk Filter: Abnormal range bars and daily volume completion are monitored to help traders avoid chasing dangerous moves. AI-style HUD Panel: The on-chart HUD summarizes trend, momentum, volatility, and volume completion into a compact dashboard so traders don’t need to open multiple indicators. How it works in practice The 8-minute engine drives the main trend color and entry markers. Local & 30m SR zones provide execution context and profit-taking areas. WaveTrend helps identify when to reduce risk or take partial profits during extended moves. The HUD acts as a “mission control” view to keep the trader aligned with the dominant state of the market. Intended Use For traders who already understand risk management and position sizing. As a decision support tool, not as an auto-trading holy grail. Best used on BTC/ETH futures from 1m–30m charts. What it is NOT It is not a guaranteed-profit system. It is not an AI that predicts the future. It does not replace your own risk control or psychology. Risk Notice Trading and investing involve risk. Historical behavior of any logic or visual structure does not guarantee future results. This script is for informational and educational purposes only and does not constitute financial advice. 概览 AOT Red Storm V25 是一套面向实盘交易员的“机构级趋势可视化套件”,采用封闭源码 + 邀请制。 它不是在“预测行情”,而是帮助你: 对齐多周期趋势结构 用 8 分钟内部周期做更干净的趋势骨架 叠加本地 + 30m 双重支撑阻力 利用波动率和成交量过滤危险行情 用一个 HUD 面板把核心信息集中展示 核心模块 8m SuperTrend 趋势骨架:内部固定使用 8 分钟周期来做趋势与结构识别,减少噪音。 WaveTrend 战术雷达:只用于辅助止盈/减仓,而不是单独进场信号。 本地 + 30m 支撑阻力区:当前周期做精确执行,30m 负责定位大级别流动性区域。 自动趋势线 + BOS:用结构高低点标记 HH/LL / BOS,辅助趋势延续与反转识别。 波动 & 量能风控:用异常大K / 当日量能进度,提示极端风险。 AI 风格 HUD 面板:把趋势、动能、波动率、量能等压缩在一个信息面板中。 适用人群 有一定交易经验,重视风控与执行纪律的交易员; 用作决策辅助,而不是“闭眼跟随”的圣杯系统; 建议用于 BTC/ETH 永续 1–30m 等周期。 不是什么 不保证稳定盈利; 不预测未来; 不替代你的仓位管理与心理建设。Pine Script® indicatorby AOT-AI-AOYINUpdated 6

One Point Global Net Liquidity The "Fuel" Behind the MarketMost traders look at price action, but price is often just a reflection of the money supply available in the system. This indicator tracks Global Net Liquidity—the actual amount of fiat currency available to flow into risk assets like Crypto and Equities. Unlike standard "Money Supply" (M2) charts, this indicator focuses on Central Bank Balance Sheets, which is a more direct proxy for "Quantitative Easing" (QE) and "Quantitative Tightening" (QT). How It Works (The Formula) This script aggregates the balance sheets of the "Big 4" Central Banks, which represent ~90% of global liquidity. It automatically converts all values to USD Trillions for a standardized view. {Global Liquidity} = {US Net Liquidity} + {ECB} + {PBoC} + {BoJ} 1. US Net Liquidity (The "Trader's" Formula) We do not just use the Fed's Total Assets. We subtract the money that is "stuck" outside the private economy: (+) Fed Balance Sheet: Total Assets. (-) TGA (Treasury General Account): The government's checking account. When this goes up, liquidity is drained from markets. (-) RRP (Reverse Repo): Money parked by banks at the Fed overnight. When this goes up, liquidity is removed from the system. 2. Global Additions ECB (Eurozone): Converted to USD. PBoC (China): Converted to USD. BoJ (Japan): Converted to USD. How to Use This Indicator This indicator is designed as an Overlay on the main chart (using the Left Scale). Correlation: Generally, when the Orange Line (Liquidity) trends up, Bitcoin and the S&P 500 trend up. When Central Banks tighten (line down), risk assets struggle. The "Divergence" Signal (Alpha): Bullish: If Price makes a Lower Low but Liquidity makes a Higher Low, it often signals seller exhaustion and a potential bottom. Bearish: If Price makes a New High but Liquidity fails to follow (or drops), the rally may be unsupported and prone to a reversal. Settings Scale: This indicator is pinned to the Scale Left to allow it to overlay price action without distortion. Data: Uses daily data from ECONOMICS and FRED feeds.Pine Script® indicatorby junosats1114

Fabio-Style Order Flow SystemFabio-Style Order Flow System — LVN • Delta • Big Trades • FVG • Order Blocks • Liquidity • Volume Profile This indicator brings together all major components of Fabio Valentino’s order-flow strategy in one unified tool. It visualizes where smart money is active, where inefficiencies form, and where price is likely to react next. 🔍 FEATURES 1. Order Flow & Delta Smoothed delta to show true market imbalance Background color shifts to bullish/bearish delta dominance Alerts for delta spikes & order-flow flips 2. Big Trade Detection Highlights Big Buy and Big Sell prints (relative to average volume) Helps identify institutional aggression on both sides 3. Low Volume Nodes (LVNs) Automatically detects low-volume zones Flags retests of LVNs for high-probability reactions Uses dynamic volume thresholds for accuracy 4. Volume Profile (Lightweight) Bucket-based intrabar profile across user-defined lookback Highlights volume distribution without heavy TradingView CPU load Auto-scales bucket density & transparency 5. Fair Value Gaps (FVGs) Detects both bullish & bearish three-bar imbalances Marks gaps visually using colored boxes Updates dynamically with a user-set lookback 6. Order Blocks (OBs) Identifies valid displacement bars and their origin OB Plots clean, minimalist rectangles around key OB zones Uses ATR-based impulse filtering 7. Liquidity Grabs Detects wick-based liquidity sweeps Highlights both equal high/low and stop-run type wicks Useful for spotting reversals & trap setups 8. Strategy Dashboard Shows real-time order flow state Displays delta strength, big trades, LVNs, and last directional impulse Auto-positions in all corners 🎯 PERFECT FOR Traders who use: Order Flow Smart Money Concepts (SMC) ICT / FVG / Liquidity models Market Structure + Volume Fabio Valentino-style analysis ⚙️ PERFORMANCE All elements optimized Uses automatic box-clearing to avoid array overload Works on all timeframes & markets (crypto, FX, indices, stocks)Pine Script® indicatorby SaaETH274

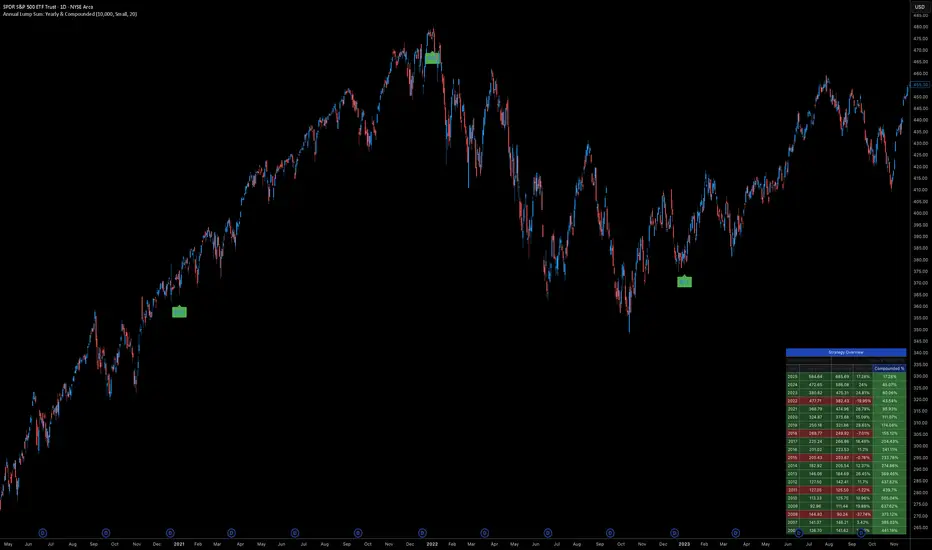

Annual Lump Sum: Yearly & CompoundedAnnual Lump Sum Investment Analyzer (Yearly vs. Compounded) Overview This Pine Script indicator simulates a disciplined "Lump Sum" investing strategy. It calculates the performance of buying a fixed dollar amount (e.g., $10,000) on the very first trading day of every year and holding it indefinitely. Unlike standard backtesters that only show a total percentage, this tool breaks down performance by "Vintage" (the year of purchase), allowing you to see which specific years contributed most to your wealth. Key Features Automated Execution: Automatically detects the first trading bar of every new year to simulate a buy. Dual-Yield Analysis: The table provides two distinct ways to view returns: Yearly %: How the market performed specifically during that calendar year (Jan 1 to Dec 31). Compounded %: The total return of that specific year's investment from the moment it was bought until today. Live Updates: For the current year, the "End Price" and "Yields" update in real-time with market movements. Portfolio Summary: Displays your Total Invested Capital vs. Total Current Value at the top of the table. Table Column Breakdown The dashboard in the bottom-right corner displays the following: Year: The vintage year of the investment. Buy Price: The price of the asset on the first trading day of that year. End Price: The price on the last trading day of that year (or the current price if the year is still active). Yearly %: The isolated performance of that specific calendar year. (Green = The market ended the year higher than it started). Compounded %: The "Diamond Hands" return. This shows how much that specific $10,000 tranche is up (or down) right now relative to the current price. How to Use Add the script to your chart. Crucial: Set your chart timeframe to Daily (D). This ensures the script correctly identifies the first trading day of the year. Open the Settings (Inputs) to adjust: Annual Investment Amount: Default is $10,000. Table Size: Adjust text size (Tiny, Small, Normal, Large). Max Rows: Limit how many historical years are shown to keep the chart clean. Use Case This tool is perfect for investors who want to visualize the power of long-term holding. It allows you to see that even if a specific year had a bad "Yearly Yield" (e.g., buying in 2008), the "Compounded Yield" might still be massive today due to time in the market.Pine Script® indicatorby oojeson9

Vacs - Trade Support Panel 📈 Multi-Function Trade Support Panel (MACD + CVPE + MTF Bias) This is a comprehensive Pine Script indicator designed to provide **multi-timeframe (MTF) bias** and **cumulative volume analysis** alongside standard **Moving Average Convergence Divergence (MACD)**, primarily intended as a **support panel** for confirming signals generated by other trading indicators and strategies. 🛠️ Included Modules and Functionality This panel combines three powerful analysis tools into a single, unified view, all with customizable input controls for visibility and calculation: 1. **MACD (Moving Average Convergence Divergence) Module** Function: Calculates and plots the standard MACD line, Signal line, and Histogram. *Key Feature: Supports an **MTF mode**, allowing you to calculate the MACD based on a higher timeframe (e.g., 4H on a 1H chart) to identify broader momentum shifts. Controls : Separate toggles for the MACD Line, Signal Line, and Histogram plots, along with standard length inputs (Fast EMA, Slow EMA, Signal Length). 2. **CVPE (Cumulative Volume & Position Engine) Module** Function: Provides deeper insight into market pressure by analyzing the cumulative delta/volume flow. CVD (Cumulative Volume Delta):** Tracks the running sum of buying or selling pressure, indicating the direction of order flow and potential accumulation/distribution. Position Bias: Calculates the rate of change (slope) of the CVD, normalized by volatility, to show the immediate strength and conviction of buyers versus sellers. Purpose: Helps identify divergences and confirm the conviction behind price moves. Controls: A master toggle to enable/disable the entire CVPE engine and customizable smoothing methods/lengths. 3. **MTF Bias Panel (Dashboard) Function: Provides a weighted, holistic score for the market bias across **four custom timeframes** (e.g., 1H, 4H, Daily, Weekly). Calculation: The total bias score is derived by combining the directional signals from the MACD Histogram and the CVD Slope (Position Bias) for each selected timeframe, weighted according to user preference. Purpose: Offers a quick, top-down view of the market structure and helps traders align their entries/exits with the larger trend direction. Controls: Master toggle to show/hide the panel, independent weight adjustments for each of the four timeframes, and customizable component weights (MACD vs. CVD) for scoring. 💡 Recommended Use This panel is designed to serve as a **critical confirmation tool** for any existing strategy: 1. **Trend Confirmation:** Use the **MTF Bias Panel** to confirm that the higher timeframes align with your trade direction before entering a signal generated by your primary indicator. 2. **Momentum Confirmation:** Use the **MACD** and **CVPE** modules to confirm that momentum is strong and order flow supports the anticipated move. Look for rising MACD Histograms and increasing Position Bias (CVD slope) in the direction of your trade. 3. **Divergence Spotting:** CVPE is excellent for identifying cumulative volume divergences against price, signaling potential reversals or exhaustion. By providing multiple layers of analysis from different perspectives (momentum, order flow, and multi-timeframe), this indicator significantly reduces noise and helps traders take only the highest-conviction setups. Would you like me to write a short, punchy title or tagline for this description?Pine Script® indicatorby cdssvg4

Symbol Magnifier & MTF Clock# Symbol Magnifier & MTF Clock Shows your symbol, price, and countdown timers for multiple timeframes on one chart. ## What It Does **Symbol Display:** - Big, easy-to-read symbol and price - Shows time left until current candle closes - Green for bullish, red for bearish - Put it anywhere on your chart **Multi-Timeframe Clock:** - Track up to 6 timeframes at once: D1, H4, H1, M30, M15, M5 - See exactly when each candle will close - Turns orange/red in the last 5 minutes as a warning - Choose which timeframes to show ## Why Use It? Never miss important candle closes across multiple timeframes. Perfect if you trade using multiple timeframe analysis or need to time your entries better. ## Settings - Move displays to any corner - Change text size - Pick your colors - Show only the timeframes you care about That's it. Simple timing tool for multi-timeframe traders.Pine Script® indicatorby UnsolutionNFX4

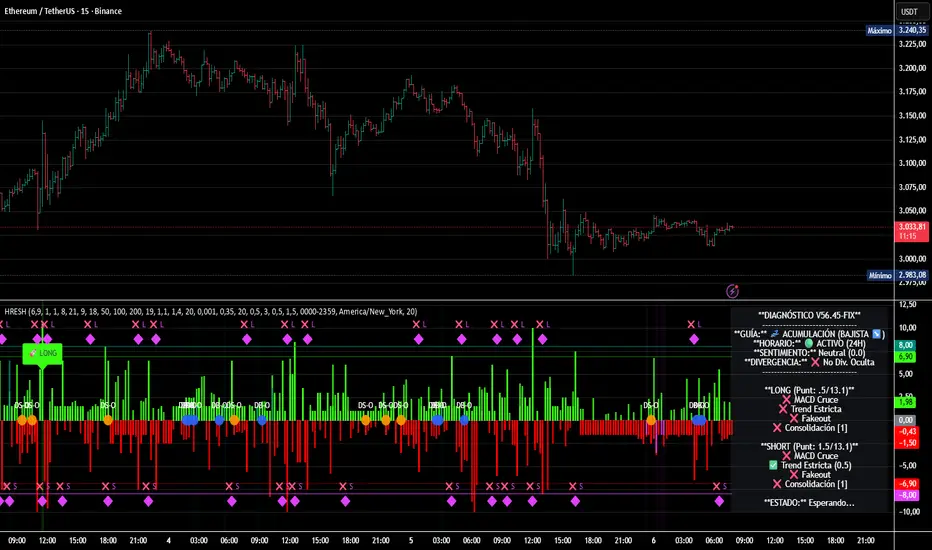

HRESH Pro Dashboard 🦅 HRESH (The Beast) — BTC Specialized System V56.45 This is the fully unlocked, 24-hour version of the HRESH System. It has been mathematically tuned and calibrated specifically for Bitcoin volatility. 🛑 CRITICAL RULES FOR USE (PLEASE READ): 1. STRICT ASSET SELECTION: BTC (Bitcoin): This is the primary asset for this indicator. ETH (Ethereum): Allowed ONLY on the 15-Minute timeframe. ❌ DO NOT USE on other assets (Forex, Altcoins, Stocks). The internal logic is unique to BTC/ETH structure. 2. TIMEFRAME STRATEGY: ⏱️ 1 MINUTE (Daily Operations): Use this for intraday scalping. ⏱️ 15 MINUTES (Sniper Mode): Use this for Swing Trading. Expect only 1 or 2 high-precision signals PER MONTH. This mode requires extreme patience. ❌ OTHER TIMEFRAMES: Do not operate. The calculations will be incorrect. 🌍 TRADING SESSIONS & VOLUME: While this version functions 24 hours a day, I strongly advise AGAINST trading during low-volume hours (such as late Asian session or weekends). ✅ RECOMMENDED: London & New York Sessions. ⚠️ HIGH RISK: Trading off-hours increases the risk of market manipulation and fakeouts. 🔴🔴🔴 RISK DISCLAIMER & WARNING 🔴🔴🔴 YOU ARE RESPONSIBLE FOR YOUR CAPITAL. This indicator is a powerful analytical tool, but it does not guarantee profits. MARKET RISK: Trading cryptocurrency involves substantial risk of loss and is not suitable for every investor. NO FINANCIAL ADVICE: Always manage your risk properly. If you trade outside the recommended hours or assets, you accept 100% of the risk. Trade wisely and respect the algorithm. By Lendrush MargaryanPine Script® indicatorby lendrush12

HRESHEnglish 🔴 IMPORTANT NOTICE This indicator is an advanced trading support tool. It helps you spot opportunities and improve your analysis, but it DOES NOT guarantee results nor replace your personal judgment. • 🔴 Every trade remains your sole responsibility. • 🔴 Risk is always present: the indicator does not eliminate it, only helps manage it. • 🔴 Risk increases when trading on very short timeframes (1 minute), outside the recommended London and New York sessions, or during weekends, where liquidity and signal accuracy may decrease. • 🔴 It is not recommended to trade other assets or use timeframes different from those specified. EAGLE EYE PRO V71.2 RENTAL This indicator is built to deliver clear signals and a professional dashboard, specially optimized for BTC. 🔑 Key highlights: • 🔴 Exclusively optimized for BTC. • 🔴 Recommended timeframe: 15 minutes, providing cleaner and more reliable signals. • 🔴 Adventurous mode: 1 minute, but with higher risk due to extreme volatility. • No time restrictions: it works at any moment of the day. • 🔴 Best accuracy: trade during the London and New York sessions. Pine Script® indicatorby lendrush11

SMC Pre-Trade Checklist (Mozzys)Here is a **clean, professional description** you can use when publishing your TradingView script. It clearly explains what the indicator does and why traders use it—perfect for the public library. --- # **📌 Script Description (for Publishing)** **SMC Pre-Trade Checklist (Compact Edition)** This indicator provides a **smart, compact on-chart checklist** designed for traders who use **Smart Money Concepts (SMC)**. Instead of guessing or rushing entries, the checklist helps you confirm the essential SMC conditions *before* taking a trade. The checklist displays as a **small 3-column panel** in the corner of your chart, making it easy to scan without covering price action. All items are controlled through indicator settings, where you can tick each condition as you validate it in your analysis. --- ## **🔥 What This Tool Helps You Do** This script helps you stay disciplined by verifying the core components of an SMC setup: ### **1. Higher-Timeframe (HTF) Bias** * Market direction clarity * Premium vs. discount zones * HTF POIs and liquidity targets ### **2. Liquidity Conditions** * Liquidity sweeps * Liquidity-based take-profit targets ### **3. Market Structure** * BOS/CHOCH confirmation * Displacement * Clean pullback into POI ### **4. Entry Validation** * Quality POI * LTF confirmation * Logical SL/TP and RR ### **5. Risk Management** * Correct position sizing * Avoiding high-impact news * Spread/volatility conditions ### **6. Trader Discipline** * Trade matches your model * No revenge or emotional trading --- ## **🎯 Why Traders Love This** Most losses come from **breaking rules**, not market randomness. This checklist forces consistency, clarity, and patience—especially in fast environments like FX, indices, and crypto. * Prevents emotional entries * Reduces impulsive trades * Keeps you aligned with your SMC plan * Works with any strategy or SMC style * Clean, minimal, non-intrusive layout --- ## **📌 Features** * Compact 3-column layout * Customizable from the indicator settings * Works on all timeframes and assets * Zero chart clutter * Perfect for rule-based traders --- ## **🚀 Who This Indicator Is For** * SMC traders * ICT-style traders * Liquidity-based traders * Anyone who wants more discipline & consistency * Backtesters who want structured trade evaluation -- Pine Script® indicatorby Mozzy1234527

Auto Seasonality Scanner by Novatrix CapitalThe Auto Seasonality Scanner analyzes historical daily price data to identify recurring seasonal patterns in the market. It highlights periods over the last 10 years where certain price movements have historically occurred. This indicator is designed for the DAILY (1D) timeframe only. Key Features: Visualizes historical entry and exit points for Long and Short patterns using vertical lines. Option to exclude specific years (e.g., 2020) from the analysis. Optional filter by US election cycles. Calculates average returns, win rates, trade lengths, and number of trades for each pattern. Displays results in a customizable table with color-coded Long and Short patterns. This tool is for educational and informational purposes only. It provides a visual guide to potential recurring seasonal trends and does not constitute financial advice or trading recommendations.Pine Script® indicatorby NovatrixCapitalUpdated 336

COT Index & Positions by Novatrix CapitalThis indicator visualizes the positioning of the two main groups from the CFTC COT reports: Commercials and Retail (Non-Reportables / Small Traders). Each group is displayed in two ways: Index (0–100) – normalized net positions to identify bullish or bearish extremes (standard cycle: 26 weeks, optionally 52 weeks). Raw Net Positions – actual long minus short positions. Color coding on the chart: Commercial Index: Blue Commercial Positions: Blue Retail Index: Red Retail Positions: Red Additional features: Reference lines for neutral, overbought, and oversold levels. Helps traders analyze market sentiment and the positioning of major participant groups. Important notice: Since COT data is published only once per week and the COT Index is built on cyclical multi-week analysis, the indicator is intended to be used exclusively on the weekly timeframe. The selected cycle length (typically 26 weeks, optionally 52 weeks) determines how net positions are compared and normalized, and can influence how quickly extreme zones appear in the index lines.Pine Script® indicatorby NovatrixCapital3

AMS Adaptive Supertrend Lite – ORB + VWAP 1.0AMS Adaptive Supertrend Lite – ORB + VWAP This indicator focuses on providing a clean read of trend, structure, and opening range context without unnecessary complexity. It’s designed for traders who prefer straightforward visual tools that support their own decision-making process. Consider this a small multi-tool for your basic ORB needs. Included: -Supertrend A simple ATR-based Supertrend for directional context. You can edit colors, line width, ATR settings, etc. No signals or automation, just a clear trend reference. -EMAs Optional fast and slow EMAs for structural context. Useful for gauging short-term momentum and slope. -VWAP A standard session VWAP. You can style it however you like (solid, dashed, colored) in the Style tab. -Opening Range (ORB) Configurable ORB band including: ORB duration (in minutes) Optional RTH-only logic Adjustable session window Choice of timeframe used to build the ORB Automatic hiding on higher timeframes (optional) The ORB high/low are built on the selected lower timeframe and then displayed on the active chart. -HTF Bias Shading (Optional) A simple background tint based on EMA structure on a higher timeframe. Meant to give gentle context, not trading signals. Alerts Two alerts are included: Supertrend flipping bullish Supertrend flipping bearish These are notifications, not calls to action. Intended Use This is a visual tool for traders who want clear structure and context on their chart. It does not provide entries, exits, strategies, or automated logic. Disclaimer This script is for educational and informational purposes only. It is not financial advice, and no performance is guaranteed. Always test tools for yourself and use proper risk management.Pine Script® indicatorby AtmosMarketSuite7