Will the AI frenzy drive US indices to new record highs again?

Despite the US government shutdown risk and elevated valuation concerns, US equities continued their upward rally, driven primarily by strength in AI-related stocks.

OpenAI’s valuation has surged to USD 500 billion, a sharp jump from the USD 300 billion valuation in an earlier SoftBank-led funding round earlier this year. This makes OpenAI the most valuable startup in the world, surpassing SpaceX.

Citigroup (C) raised its forecast for global AI spending, projecting USD 490 billion by 2026 (up from USD 420 billion) and cumulative hyperscaler investments by Amazon (AMZN), Microsoft (MSFT), and others to reach USD 2.8 trillion by 2029, up from the previous USD 2.3 trillion estimate.

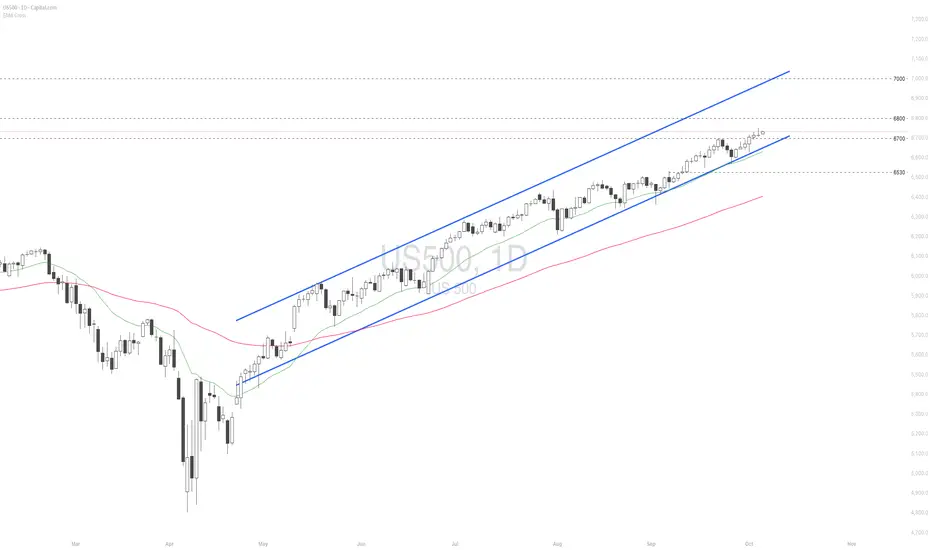

US500 extended its rally to a new record high, maintaining a solid uptrend within the ascending channel. The diverging bullish EMAs point to the potential continuation of bullish momentum. If US500 breaches above the psychological resistance at 6800, the index may gain upward momentum toward the next psychological resistance at 7000. Conversely, if US500 breaks below the support at 6700, the index could retreat toward 6530.

Fed

USD/CHF Bulls Eye 0.8080 – But Is a Trap Coming First?🔹 COT (Commitment of Traders)

USD Index: Non-commercial longs increased (+1,541), shorts decreased (-1,009). → Speculators turning more bullish on the Dollar.

CHF Futures: Non-commercial longs rose (+1,992), shorts declined (-1,030). → Speculators also turning more bullish on the Swiss Franc.

📌 Combined Result: Strength on both USD and CHF, but the imbalance favors the Dollar.

🔹 FX Sentiment (retail positioning)

74% long USD/CHF vs 26% short.

📌 Retail is heavily long → contrarian signal → risk of a downside correction, even though the macro setup still favors USD.

🔹 Seasonality

October is historically bearish for USD/CHF (average -0.01 to -0.02 over the last 10–20 years).

November tends to be neutral, while December is again weak.

📌 Seasonal bias → contradicts Dollar strength, adding short-term downside risk.

🔹 Price Action

Price consolidating around 0.7980, after a recovery from the BPR (Balanced Price Range).

Structure suggests possible continuation higher toward the 0.8050–0.8080 supply zone.

RSI neutral, with room for further upside.

A break below 0.7940 would invalidate the bullish scenario and expose downside toward 0.7900.

CADJPY Set for October Crash? Institutions Bet Big on Yen 📊 Multi-Factor Analysis – CADJPY

COT Data

JPY: Net long positions are strongly increasing → Non-Commercial long +14.7K, Commercial long +12K. Institutional flows favor the Yen, confirming a bullish bias on JPY.

CAD: Heavy liquidation → Commercial longs -49K, shorts -59K, Non-Commercial longs decreasing (-2.9K). Net positioning shows bearish sentiment on CAD, with a clear prevalence of short exposure among speculators.

👉 Interpretation: Institutional flows point toward a strong JPY and weak CAD → bearish bias on CADJPY.

Seasonality

CAD: Historically weak in October (negative averages in 20Y and 15Y, worsening in 5Y and 2Y).

JPY: Historically strong in October, especially on short-term frames (5Y and 2Y very bullish).

👉 Interpretation: Seasonality supports a bearish scenario on CADJPY during October.

Retail Sentiment

90% Long vs 10% Short on CADJPY.

👉 Extreme retail long positioning = contrarian bearish signal → potential for further downside pressure.

Technical Analysis

CADJPY broke below the descending trendline.

Currently trading inside the weekly demand zone (105–106), acting as short-term support.

RSI oversold → likely technical bounce toward 106.8–107.2 (supply + trendline) before continuation lower.

Primary structure remains bearish, with medium-term targets at 104.80–105.00.

EUR/GBP Rejected at 0.8760 - Is a Pullback to 0.8660 Next?🔹 COT (Commitment of Traders)

GBP Futures: Non-commercial longs increased (+3,704) while shorts decreased (-912) → speculators are turning more bullish on the Pound. Commercials slightly increased shorts (-1,853) but remain largely neutral.

Euro Futures: Non-commercial longs decreased (-789) while shorts increased (+2,625) → signaling bearish pressure on the Euro.

📌 Combined Result: Clear imbalance in favor of GBP, with stronger net positioning compared to the Euro.

🔹 FX Sentiment (retail positioning)

EUR/GBP: 87% short vs 13% long.

📌 Extremely skewed retail positioning → contrarian signal → short-term upside potential for EUR/GBP, but macro context still favors GBP strength.

🔹 Seasonality

September and October show a historically neutral to slightly bearish bias over 15–20 years.

November–December tend to favor the Euro with seasonal rebounds.

📌 In the short term, there is no strong seasonal support for an EUR/GBP rally.

🔹 Price Action

Strong rejection from the 0.8740–0.8760 supply zone, with consolidation below resistance.

Possible retracement toward demand area 0.8660–0.8680, aligning with the dynamic trendline.

RSI is neutral, no major divergences, but momentum is cooling.

Structure remains bullish only above 0.8760; otherwise, risk of reversal toward 0.8620–0.8600.

EUR/USD Rejected Hard at 1.19 COT (Commitment of Traders)

Euro FX: Non-commercials slightly reduced longs (-789) but increased shorts significantly (+2,625). Commercials added both longs (+4,978) and shorts (+3,375), signaling hedging but with a defensive bias. → Net positioning remains positive on the Euro, but short pressure is increasing.

USD Index: Non-commercial longs rose (+1,541), while shorts decreased (-1,009). → USD strengthened by large speculators.

📌 Interpretation: Imbalance in favor of the Dollar, with the market turning more cautious on the Euro.

FX Sentiment

55% short EUR/USD vs 45% long.

📌 Retail is slightly skewed short → often contrarian → could support limited upside, but not extreme.

Seasonality

September is historically weak for EUR/USD (-0.01/-0.012 over 5–10 years).

October is also negative, while November–December historically show rebounds.

📌 Short-term seasonal bias (September–October) remains bearish.

Price Action

Strong rejection from the 1.1850–1.1900 supply zone.

Currently testing the 1.1740 area.

Bearish structure with probable downside targets at demand zones:

1.1650 → first key level.

1.1550 → deeper bearish extension if USD strength persists.

Only a stable recovery above 1.1820 would invalidate the bearish scenario.

Trading Outlook

Main Bias: Bearish in the short term (Sep–Oct), supported by COT (USD strength), negative seasonality, and technical rejection.

Contrarian Risk: Slight retail shorts could trigger minor rebounds, but overall setup favors selling rallies.

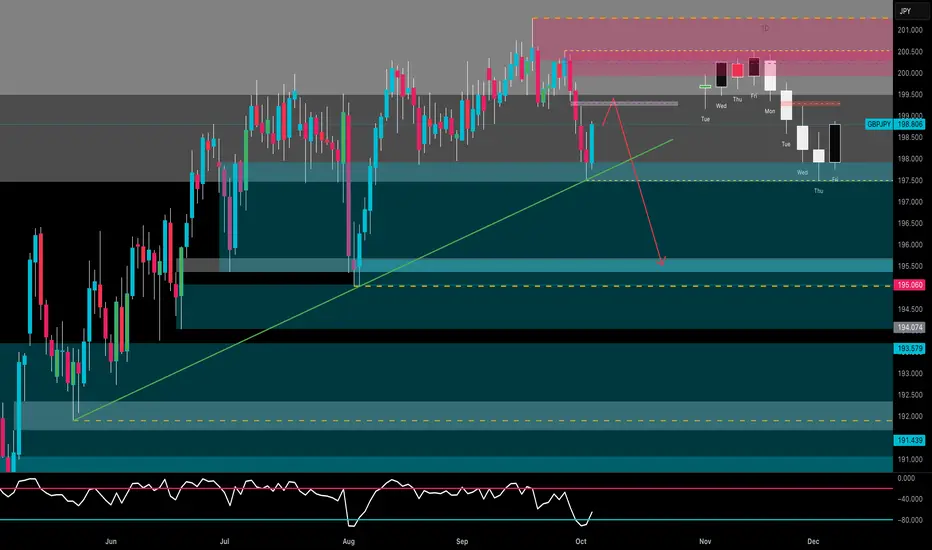

GBP/JPY Bears Back in Control – Is 195.50 the Next Target?🔹 COT (Commitment of Traders)

GBP Futures: Non-commercial longs increased (+3,704) while shorts decreased (-912) → speculators are turning more bullish on the Pound.

JPY Futures: Non-commercial longs sharply increased (+14,727) while shorts declined (-3,362) → strong bullish momentum returning to the Yen.

📌 Combined interpretation: Opposite momentum — both GBP and JPY show long accumulation, but the strength is significantly higher on the Yen, suggesting potential short-term weakness for GBP/JPY.

🔹 FX Sentiment (retail positioning)

59% short vs 41% long.

📌 Retail slightly skewed short → moderate contrarian signal, but not extreme. A short-term bounce is possible, though the broader macro picture remains fragile for GBP.

🔹 Seasonality

October is historically bullish for GBP/JPY on a 5–10 year average (+1.8% to +2.4%).

However, 15–20 year data show a more neutral to slightly negative bias, reflecting volatility rather than stable direction.

📌 Overall, a neutral-to-bullish seasonal bias, but vulnerable to a technical correction after the strong rallies seen in August–September.

🔹 Price Action

Strong rejection from the 200.50–201.00 supply zone with consecutive bearish daily closes.

Current dynamic support sits around 197.00–196.50, aligned with the ascending trendline.

RSI remains neutral and far from oversold → room for further downside.

Possible pullback toward 199.00–199.50 before a new bearish leg.

Main downside targets: 195.50, then 194.00 as an extended target.

🔹 Trading Outlook

Main Bias: Short-term bearish, with JPY strength (COT) and a corrective structure following the 201.00 top.

Contrarian Risk: Slight retail short bias could trigger a minor bounce before continuation lower.

Key Levels:

Resistance: 199.50 / 200.50

Support: 197.00 / 195.50 / 194.00

🎯 Outlook: Expect a pullback toward 199.00 before another bearish move toward 195.50. Daily structure remains bearish as long as 200.50 holds.

Why I have USD/JPY Falling Below 139.5 On My Bingo CardUSD/JPY traders have been treated (or perhaps burned) from two months of choppy trade, reversals and false breakouts. Yet price action clues and developments from the Fed and BOJ have allowed me to revisit my original thesis of a lower USD/JPY. I now have a break below 139.50 on my bingo card.

Matt Simpson, Market Analyst at City Index.

FICO and the FedNow that NYSE:UNH has started to pick up due to the shares acquired by many large names, we need to turn our attention to companies not yet in the news cycle. One of these companies is NYSE:FICO , which handles credit worthiness scores. But why, in a time where home buyers and consumers are being crushed at every turn, would a credit solutions agency be a good buy? The answer is because it is forward looking, and we are looking toward a time of, more likely than not, lower interest rates.

First let’s look at the charts...

As you can see, from the all-time high, FICO is at a 40% discount. So, we are following the universal rule of buying low. Now all we must do is sell high. Based on Powell's speech at Jackson Hole, we can see that the Fed is gearing up to cut interest rates. You can also see this is the case with the amount of debt-buying taking place in the bond market...

So, the problem is not IF they'll cut rates, but WHEN and by how much. In agreement with what most people see coming, expect the next meeting to lead to a 25 bps drop in the $FRED:FEDFUNDS. When this happens, you can also expect the credit agencies to blast off onto the horizon. (Written before Sep 16-17 meeting)

Before we get to the exit plan, we do have some housekeeping. It should be noted that FICO, in the practical sense, is no longer a monopoly. Equifax has been approved for its rating system by the government, so this trade does not come without risk. The good news is that as rates get lowered we can expect more people to take on more debt (because it is cheaper), which will boost the demand for FICO's rating abilities. We should aim for a timeframe before the next earnings call to get out of this trade, but the usual target of 3 to 6 months remains as the timeframe for holding this position. A longer period can be justified based off any unusual performance. The price target will be set at $2,000.

EURUSD BULLSA lot of traders are anticipating sell direction, most have already sold at around 1.17700 zone. For me I still hold a bullish bias due to:

1. Although technical analysis leaves room to catch sells the pair still maintains an uptrend. Therefore, based on recent events claiming a US government shut down, conflicting views on rate cuts from Fed officials and NFP Lining up on Friday creating a risk on mood, I find it wise to sell towards NfP. Any lower than expected will confirm the bulls further and focus can shift to 1.192000 and later 1.20000. But higher than expected will mean that the Fed will keep interest rates steady and a reversal will be confirmed.

Exness: Japanese Yen Hawkish Shift Intertwined with Fed Rate CutExness: Japanese Yen Hawkish Shift Intertwined with Fed Rate Cut Expectations: What Lies Ahead?

The signals from the Bank of Japan's policy meeting on September 18-19 mark a potential turning point. Although the decision was made to keep the policy interest rate at 0.5% with a 7-2 vote, the internal details revealed growing hawkish pressure. Policy board members Hajime Takata and Naoki Tamura voted against maintaining the interest rate, advocating for an immediate 25 basis point hike to 0.75%. This is the first dissenting vote since Governor Kazuo Ueda took office, clearly indicating a growing call for tighter policy within the central bank.

Even more surprisingly, the Bank of Japan simultaneously announced that it would begin preparations to sell its holdings of exchange-traded funds (ETFs) and Japanese Real Estate Investment Trusts (J-REITs). Although the planned pace of sales is relatively modest, this is seen as a substantive step towards policy normalization, with its signaling significance far outweighing its actual market impact.

The "Summary of Opinions" from the September meeting, just released today (September 30), provides decisive evidence of this hawkish shift. The document shows that there was a serious and in-depth debate within the policy board on the "possibility of a near-term rate hike." Several members believed that the conditions for another rate hike were maturing, with one opinion explicitly stating, "Given that it has been more than six months since the last rate hike, perhaps it is time to consider raising the policy interest rate again." Even Asahi Noguchi, a deliberation committee member usually considered dovish, stated in a speech on September 29 that the necessity of adjusting the policy interest rate is "greater than ever."

This series of signals quickly reshaped market expectations. Currently, market pricing reflects that the probability of the Bank of Japan raising rates by 25 basis points at its next meeting on October 29-30 has surged to about 60%.

In stark contrast to the Bank of Japan's increasingly firm stance, the Federal Reserve is on a clear path of easing, primarily driven by concerns about a cooling US labor market. Key inflation data released last week on September 26 further solidified this expectation.

Data shows that the Federal Reserve's most favored inflation indicator, the core Personal Consumption Expenditures (PCE) (Chart 1) price index for August, increased by 2.9% year-on-year, remaining consistent with July and fully meeting market expectations. This "as expected" report is widely interpreted by the market as "non-threatening" inflation, suggesting it will not hinder the Federal Reserve's interest rate cuts and instead bolsters investor confidence in future rate reductions.

The Tug-of-War Between Inflation and Growth

The fierce debate within the Bank of Japan between hawks and doves stems from the contradictory signals sent by Japan's domestic economic data. On the one hand, persistently above-target inflation provides a reason for raising interest rates; on the other hand, recent signs of slowing growth call for the central bank to remain cautious. This tug-of-war between inflation and growth makes the Bank of Japan's decision-making path full of uncertainty.

Inflation Outlook: The Hawks' Confidence

Hawkish officials who support interest rate hikes primarily base their arguments on persistent inflationary pressures in Japan. The national core Consumer Price Index (CPI) (Chart 2) for August, released on September 18th, rose by 2.7% year-on-year. Although this is a slowdown from July's 3.1%, it marks the 29th consecutive month that this data has been above the Bank of Japan's 2% target.

What is even more noteworthy is that the "Core-Core CPI", which excludes fresh food and energy and is regarded by the Bank of Japan as a measure of underlying inflation trends, remained stubbornly high at 3.3% in August. This persistent underlying price pressure is the core argument for hawkish members who believe the inflation target has been "largely achieved." In addition, the Tokyo core CPI for September (released on September 25), which is a leading indicator for national inflation, remained stable at 2.5% year-on-year, further indicating that inflationary pressures are not rapidly dissipating.

Growth Outlook: Dovish Concerns

However, just when the hawkish arguments seemed fully substantiated, the latest series of economic activity data released this week cast a shadow over the outlook, providing strong support for a dovish, cautious stance.

Data released on September 29th and 30th showed that preliminary industrial output for August decreased by 1.2% month-on-month (Chart 3), significantly worse than the market expectation of -0.8% and also weaker than the previous figure of -0.4%. This indicates that production activities are contracting in manufacturing, a crucial pillar of the Japanese economy, possibly due to the negative impact of US tariff policies and a slowdown in global demand.

At the same time, retail sales data for August, a key indicator of domestic demand, was also disappointing.

This data unexpectedly fell by 1.1% year-on-year, a significant departure from market expectations of a 1.0% increase; it even saw a substantial 1.6% month-on-month decrease. This clearly indicates that Japanese household consumption power is being eroded, and domestic demand is beginning to show weakness, against a backdrop of inflation consistently higher than wage growth.

In addition, the preliminary Manufacturing Purchasing Managers' Index (PMI) (Chart 4) for September fell to 48.4, marking the fastest contraction in six months and further confirming the downward pressure on the economy.

From a technical perspective, USD/JPY is at a critical crossroads. Recent price movements show a fierce struggle between bulls and bears around important technical levels, reflecting fundamental uncertainties. USD/JPY failed to reach the key 150.00 level, then fell back below 149.00 and the EMA21. The price is still fluctuating within the 148.00-149.00 range, indicating possible consolidation. If it stays below 149.00, the price may consolidate further within the 148.00-149.00 range. Conversely, if it returns above the EMA21 and 149.00, it may retest the key 150.00 level.

Integrating the above fundamental and technical analysis, a core conclusion can be drawn: the previous one-sided short-yen trading environment has ended. The market is entering a new phase that is more balanced but potentially significantly more volatile.

The movement of USD/JPY is no longer dominated by a single factor, but depends on the interplay between the hawkish potential of the Bank of Japan and the dovish reality of the Federal Reserve. The short-term direction of the exchange rate will be determined by which central bank's actions (or inactions) surprise the market more.

The future path will be largely determined by two key economic data releases scheduled for this week:

Japan Tankan Survey (October 1): Can this report give the Bank of Japan's hawks enough confidence to act in October?

US Non-Farm Payrolls (October 3): Will this data confirm the weakening of the US labor market, thereby "paving the way" for the Federal Reserve's rate cut path?

The outcome of these two events will likely determine whether USD/JPY breaks key support and tests lower levels, or whether it can hold its ground here and gather strength to challenge the strong resistance area of 150 again.

In any case, what is certain is that the era of one-sided yen depreciation is over, and a new phase full of strategic reassessment and uncertainty has arrived.

By: Eric Chia, Financial Market Strategist at Exness

SPY MONEY PRINTER GO BRRR|LONG|

✅SPY with the FED lowering rates, liquidity injections perspective fuel risk assets. Price has broken out above the key level, signaling bullish order flow. SMC outlook suggests momentum could push into new all-time highs as money printer effects unfold. Time Frame 1H.

LONG🚀

✅Like and subscribe to never miss a new idea!✅

BTC Tests Range Highs Below 120k: Wait for Confirmation __________________________________________________________________________________

Market Overview

__________________________________________________________________________________

BTC is back at the top of its range, pressing 116.8k–117.97k just beneath the 120k barrier. Higher timeframes (12H/1D) lean bullish, while mid-TFs still push back — confirmation is key before chasing strength.

Momentum: 📈 Cautiously bullish; above 115.2k, a clean close >117.97k would likely unlock 120k.

Key levels: Resistances: 116.8k–117.97k; 120k; 124.3k. Supports: 115.2k; 114k; 112.4k–111.1k.

Volumes: Very high on 6H→30m (mostly under resistance), normal on 1D.

Multi-timeframe signals: 1D/12H Up; 6H/4H/2H Down; 1H/30m/15m Up.

Risk On / Risk Off Indicator context: NEUTRE VENTE — slight risk-off, contradicting daily momentum.

__________________________________________________________________________________

Trading Playbook

__________________________________________________________________________________

With range highs overhead, stay constructive but disciplined: lean cautiously bullish while 115.2k holds and wait for confirmed breaks to avoid traps.

Global bias: Cautious bullish while 115.2k holds; major invalidation on a 1D close <114k.

Opportunities:

• Pullback buy if 115.2k holds, then confirm >116.8k.

• Breakout long on 1D close >117.97k; add if 120k flips to support.

• Tactical sell on rejection at 116.8k–117.97k toward 115.2k then 114k.

Risk zones / invalidations: Loss of 115.2k opens 114k/112.4k; a 1D close >120.6k invalidates top-shorts.

Macro catalysts: Fed −25 bps (supports risk), potential US data timing shifts (ISM/NFP) that can cluster volatility, and positive BTC spot ETF flows (Day +$430M) reinforcing dips.

Action plan: Entry >117.97k (≥2 closes + retest) / Stop <115.8k / TP1 120k, TP2 122.5k, TP3 124.3k / R:R ~1.8–2.5.

__________________________________________________________________________________

Multi-Timeframe Insights

__________________________________________________________________________________

Higher timeframes point up, but mid-TF supply still caps price near the range highs; intraday strength needs follow-through to avoid bull traps.

1D/12H: Holding above 115.2k preserves upside bias; convert 117.97k to open 120k then 124.3k.

6H/4H/2H: Seller pressure below 116.8k–117.5k; beware fake breaks without volume follow-through.

1H/30m/15m: Impulsive bounce is constructive, but requires break/hold (≥2 bars) to confirm trend continuation.

__________________________________________________________________________________

Macro & On-Chain Drivers

__________________________________________________________________________________

A supportive macro backdrop and improving flows help, but timing risks keep volatility elevated around resistance.

Macro events: Fed easing (−25 bps) underpins risk appetite; shifting ISM/NFP timing may concentrate moves around data windows.

Bitcoin analysis: 114k–115.2k defended; highest quarterly close; weekly ETF inflows turned positive.

On-chain data: STH cost basis ~111k; ETF inflows resumed; recent deleveraging cleans positioning.

Expected impact: Slight bullish tilt if 115.2k holds and 117.97k flips to support; otherwise risk of 114k/112.4k retests.

__________________________________________________________________________________

Key Takeaways

__________________________________________________________________________________

BTC is pressing range highs with active supply below 120k. The cleaner long is a confirmed breakout >117.97k with 120k turning into support; otherwise, fading rejections back into 115.2k remains valid. Macro support (−25 bps + positive ETF flows) helps, but confirmation at resistance matters most. Stay patient and execute only on validated signals.

Long EUR/USD on USD Weakness Amid Government ShutdownShort-term trade idea:

Entry: 1.1740–1.1750

Target: 1.1820

Time Horizon: 1–3 days

The ongoing U.S. government shutdown adds downside risk to the dollar, particularly amid softening data and weakening labor market sentiment. Delays in key releases like jobless claims and nonfarm payrolls reduce policy visibility for the Fed and support market expectations for rate cuts in the coming months. Broader risk-off sentiment and pressure on U.S. equities also weigh on the dollar.

Meanwhile, the ECB's decision to keep rates on hold confirms a "wait-and-see" approach, which was already priced in. More importantly, there was no dovish surprise. The ECB is not signaling imminent cuts. With eurozone inflation expected to remain firm, rate cut expectations should stay contained, helping to keep the euro supported. This opens the door for EUR/USD to grind higher, with 1.1800–1.1820 as a short-term target.

Risks:

Rapid resolution of the U.S. government shutdown

Strong upside surprise in U.S. ISM or ADP data

Hawkish Fed rhetoric pushing back against market dovishness

Bitcoin capped below 115k: plan and invalidations__________________________________________________________________________________

Market Overview

__________________________________________________________________________________

BTC is staging a controlled recovery above 111k while stalling beneath a heavy 113.8k–116k supply zone ahead of the 117.97k pivot. The backdrop is constructive, but intraday timeframes still show profit-taking.

Momentum: Bullish 📈 on 1D/12H, with active consolidation on 2H–6H after the 114.6k–114.8k rejection.

Key levels:

• Resistances (HTF): 114.8k–116k (1D/12H), 117.97k (1D), 124.3k (W).

• Supports (HTF): 112.4k–111.5k (12H), 110.4k (pivot), 109.3k (6H).

Volumes: Normal on 1D, very high intraday on the 114.6k–114.8k fade, moderate on 6H.

Multi-timeframe signals: 1D/12H Up; 2H/4H/6H Down (pullback within HTF trend); 1H/30m/15m tactical rebounds at 112.6k–112.9k. Elevated offer-side volumes argue for clear validations before breakout.

Risk On / Risk Off Indicator: NEUTRAL BUY → mild risk-on bias, aligned with HTF momentum; occasional intraday spikes to STRONG BUY, but not persistent.

__________________________________________________________________________________

Trading Playbook

__________________________________________________________________________________

Context: HTF trend is bullish; favor disciplined dip-buys at supports with confirmation, be cautious below 114.8k–116k.

Global bias: Moderately bullish while > 111k; primary invalidation below 110.4k (structure loss).

Opportunities:

• Buy-the-dip: Buy 112.7k–112.2k on reversal signal; target 114.6k then 115.3k/117.0k.

• Breakout: Buy break & hold > 114.8k (30m–1H) aiming for 117.97k.

• Tactical sell: Fade clean rejection at 114.6k–115.3k (wick + volume) toward 113.7k then 112.9k.

Risk zones / invalidations: A firm break < 112.2k reopens 111.5k–110.4k; a 1D close > 118k invalidates tactical shorts.

Macro catalysts (Twitter, Perplexity, news):

• Fed: initial 25 bp cut and gradual easing path → gentle risk-on.

• Softer USD, gold at highs, oil lower (OPEC+) → supportive tailwind for BTC.

• US shutdown risk + CPI/ISM/NFP week → elevated volatility near key levels.

Action plan:

• Entry: 112.7k–112.2k (candle reversal + intraday momentum rebuild).

• Stop: below 111.8k (aggressive) or below 110.4k (conservative).

• TP: 114.6k (TP1) / 115.3k (TP2) / 117.0k (TP3).

• R/R guide: ~1.8R (tight stop) up to ~2.5–3R (wide stop) depending on execution/trailing.

__________________________________________________________________________________

Multi-Timeframe Insights

__________________________________________________________________________________

Overall HTF is bullish, MTF is breathing, and LTF is rebounding at demand.

1D/12H: Bullish structure above 111k–112k; compression below 114.8k–116k. A daily close > 114k strengthens odds for 117.97k.

6H/4H/2H: Orderly pullback after 109k→114k impulse; buyer pivot 112.4k–111.9k; sustained upside needs > 113.8k then > 114.6k.

1H/30m/15m: Tactical bid active at 112.6k–112.9k; very high offer-side volumes → wait for confirmations, avoid late chases under 114.8k.

Confluences/divergences: Strong confluence 112.4k–111.5k; recent intraday divergences suggest shallow but jumpy pullbacks.

__________________________________________________________________________________

Macro & On-Chain Drivers

__________________________________________________________________________________

Macro is mildly supportive (more dovish Fed, softer USD), while on-chain and ETF signals are positive but uneven.

Macro events: Fed started easing (−25 bp) with a cautious tone; USD softer, gold at highs, oil lower (OPEC+); US shutdown risk and CPI/ISM/NFP in focus.

Bitcoin analysis: ETF inflows turned positive on the day but 7D trend is fragile → tactical support to dip-buys; technical structure reclaimed with firm BTC dominance.

On-chain data: STH cost basis near ~111k is pivotal; LTH realized sizable profits; derivatives deleveraging and elevated put skew → respect downside shock risk.

Expected impact: Supportive yet not euphoric, fitting a “buy dips” approach while 110.4k holds; above 114.8k, macro could help extend toward 117.97k.

__________________________________________________________________________________

Key Takeaways

__________________________________________________________________________________

BTC is recovering above 111k but sellers defend 114.8k–116k.

- Overall trend: Constructively bullish on HTF, with a breathing MTF.

- Best setup: Disciplined buy at 112.7k–112.2k with confirmations; extend if break & hold > 114.8k toward 117.97k.

- Key macro: Gradual Fed easing + softer USD provide a tailwind.

Stay selective: demand confirmations at offers and watch 110.4k as the key line in the sand.

Bitcoin - Bitcoin Left Behind the Stock Market!?Bitcoin is in its descending channel on the four-hour timeframe, between the EMA50 and EMA200. In case of an upward correction towards the specified supply zone, it is possible to sell Bitcoin with a better risk-reward.

It should be noted that there is a possibility of heavy fluctuations and shadows due to the movement of whales in the market and compliance with capital management in the cryptocurrency market will be more important. If the downward trend continues, we can buy in the demand range.

A group of U.S. lawmakers has called on the Securities and Exchange Commission (SEC) to enforce an executive order issued by President Donald Trump that opens the door for cryptocurrency investments within the $12.5 trillion 401(k) retirement fund market. Signed in August, the order authorizes 401(k) plans to offer cryptocurrencies as a new investment option.

Members of the House Financial Services Committee, in a formal letter, praised the order for its potential to help Americans boost their retirement savings. They urged the SEC to work with the Department of Labor to update existing rules and guidelines, with the aim of enabling millions of Americans to gain access to such investment opportunities for their retirement.

The letter further stated: “We also ask the SEC to review the bipartisan bills currently advancing in the 119th Congress regarding accredited investors. We hope these measures will allow the 90 million Americans who are currently excluded from alternative investments to secure a more dignified and comfortable retirement.”

Meanwhile, the Senate Finance Committee announced that it will hold a hearing this week on the issue of digital asset taxation, as industry stakeholders continue to press for greater clarity in federal regulations.

According to Committee Chairman Mike Crapo, the session—titled “Examining the Taxation of Digital Assets”—is scheduled for October 1. The official notice confirmed that Lawrence Zlatkin, Vice President of Tax at Coinbase, and Jason Somensatto, Policy Director at Coin Center, will testify at the hearing.

The committee had earlier invited public comments on how existing tax laws should apply to digital assets and whether new legislative frameworks are needed. The upcoming session is expected to draw heavily on the recommendations of the White House Digital Asset Working Group, which urged lawmakers to recognize cryptocurrencies as a distinct asset class and establish tailored tax rules separate from those applied to commodities and securities.

From a market perspective, liquidation heatmaps in the futures market highlight clusters of leveraged positions at key levels. When the price fell between $114,000 and $112,000, a wave of long liquidations occurred simultaneously, leading to heavy wipeouts and accelerating the downward momentum.

Risk pockets remain around the $117,000 level, making both sides of the market vulnerable to liquidity-driven volatility. Without strong demand at these levels, fragility persists, increasing the likelihood of another sharp downward move.

NAS100 - Stock Market Awaits Employment Data!The index is above the EMA200 and EMA50 on the four-hour time frame and is in its long-term ascending channel. If the upward momentum decreases, we can expect a correction to the demand range and buy Nasdaq in that range with an appropriate reward for the risk.

According to reports released over the weekend, UBS stated that there is a 93% probability of the U.S. economy entering a recession this year. This figure implicitly suggests that the country may already be in recession, though some analysts remain skeptical of such a direct conclusion. UBS’s projection is based on indicators such as personal income, consumption, industrial production, and employment.

The bank warned that the U.S. economy has reached “historically troubling levels,” though no outright collapse has yet occurred. Analysts at UBS described the economy as “weak, soft, and fragile,” while noting that a definitive declaration of recession has not been made.

In the United States, an official declaration of recession is the responsibility of the Business Cycle Dating Committee at the National Bureau of Economic Research (NBER), which typically makes such calls with a lag of 6 to 18 months after the recession has started. Their assessment relies on revised data covering GDP, employment, income, sales, and production, and they generally avoid premature decisions.

In the meantime, policymakers and markets tend to act on real-time indicators such as GDP estimates, jobs data, yield curve signals, and credit spreads. In practice, traders react more strongly to price movements than to formal definitions of recession.

Separately, Michael Feroli, chief U.S. economist at J.P. Morgan, dismissed Fed board member Steven Miran’s call for cutting rates to 2.5% or lower. The bank has maintained its forecast for gradual 25-basis-point cuts, targeting a range of 3.25% to 3.5% by early next year.

A potential Supreme Court case involving Fed board member Lisa Cook has also emerged as a “wild card,” since a ruling against her could undermine the positions of other members as well. J.P. Morgan has warned that politicization of the Federal Reserve would leave the institution more vulnerable to pressure from a Trump administration on monetary policy.

The U.S. dollar remained relatively strong this week, as investors continued to parse the Fed’s less-dovish stance. While the latest dot plot showed policymakers aligned with the market on two additional rate cuts this year, the median dot for 2026 pointed to only one more 25-basis-point reduction. By contrast, markets still expect as many as three cuts next year.

However, following Chair Jerome Powell’s cautious tone on Tuesday—emphasizing that the Fed must continue balancing the competing risks of elevated inflation and a weakening labor market—investors scaled back some of their bets.

Inflation risks remain significant. The OECD highlighted this week that the full effects of tariff hikes are still unfolding. What supports Powell’s cautious approach is that, despite signs of labor market weakness, the Fed’s own forecasts remain relatively optimistic, with economic activity showing resilience. The Atlanta Fed’s GDPNow model projects 3.3% growth for Q3.

Although last week’s inflation data failed to dampen market optimism for rate cuts—and equities continued their rally—the focus in the coming week will shift back to labor market conditions.

The week begins Monday with pending home sales data. On Tuesday, the JOLTS job openings report and the consumer confidence index will be released. Wednesday brings private-sector employment data from ADP, followed by the ISM Manufacturing PMI. On Thursday, weekly jobless claims will be published as usual.

All of these releases will build up to Friday’s critical nonfarm payrolls (NFP) report, widely seen as the market’s ultimate test.Investors will closely monitor whether recent labor market weakness persists, and whether the Fed can move another step toward a rate cut at the October meeting. Finally, the ISM Services Index will provide a more comprehensive picture of U.S. economic health.

Ahead of the jobs data, traders may also take note of remarks from several Fed officials, including Vice Chair Jefferson, New York Fed President Williams, Atlanta Fed President Bostic, Chicago Fed President Goolsbee, and Dallas Fed President Logan. The ADP and NFP releases on Wednesday will likely provide the first snapshot of September labor market performance.

The DOW, Gold, and Morgan StanleyAs it turns out, the stock market that appears to be the gift that keeps giving, is actually giving nothing. In reality, when we measure the value of the DOW with real money (Gold) rather than fiat inflationary currency, the markets are crashing down so fast it'll make your head spin. The $NYSE:DOW/TVC:GOLD shows us that what appears to be one of the greatest bull markets in the history of the entire exchange, is actually just one giant melt up fueled by monetary expansion and inflationary action.

Morgan Stanley NYSE:MS recent came out and shared their new edit to their famous 60/40 portfolio arrangement. In this edit, they entertained the idea that inflation was simply not friendly to the client's holdings and that they should actually diversify their positions. Originally, the 60/40 portfolio consisted of 60% equities, and 40% bonds. However, they presume that the future will not bring a passive environment to the boring 40% bonds because, like anyone with two eyes and a brain, they believe that higher inflation lies ahead. Their solution? Get this, to buy Gold . Who would of thought of something so genius? The profound idea that a placeholder of value would hold value and protect you from inflation could only possibly be developed in such a megabank super titan with trillions in AUM. All sarcasm aside though, it might not be exactly obvious to most what this means for gold and bonds.

Firstly for bonds, most of which are held in treasuries, we can expect some sort of retail selloff only to be bought back up again by the Fed. So nothing news worthy there. However for our precious gleaming metal, we can expect a continuing bull run as money leaves the debt market and enters into precious metals (again namely gold). We should also be inclined to believe that this should help gold mining companies and give them a nice increase in their stock values over time. Next, we shouldn't expect to much of a move from this in the stock market except the usual volatility and seasonal shifts.

Lastly, from this admission from the boys at Morgan Stanley, we can also expect continuing inflation despite what the numbers released by the Fed say. No, the cost of living will not lower. No, the Fed will not raise rates to curb inflation. No, the numbers are never real and never will be. But this does mean that we know what's coming and how to protect ourselves.

Here are the possible plays to consider

Gold: GOLD (USD/OZ)

Stocks: NYSE:NEM , $B, NYSE:EGO , AMEX:EQX , NYSE:AEM

ETF: GDX, GDXJ

Tokyo Core CPI remains unchanged, US PCE Index ticks higherThe Japanese yen has stabilized on Friday. In the North American session, US/JPY is trading at 149.61, down 0.11% on the day. The yen has taken a beating over the past two days, falling 1.5%.

Tokyo Core CPI held steady in September at 2.5% y/y. This matched the downwardly revised August reading and was lower than the market estimate of 2.8%. Tokyo Core CPI excluding food and energy dropped to 2.5%, down sharply from 3.0% in August. Food inflation remains high but eased to 6.9% in September from 7.4% in August.

The Bank of Japan will include this data in the mix when it meets next on October 29-30. Aside from inflation, BoJ policymakers will be looking at the impact of US tariffs on the economy.

The US PCE Price Index, which is the Federal Reserve's preferred inflation indicator, ticked higher in August. Annualized, PCE rose to 2.7%, up from 2.6% in July and in line with the consensus. Monthly, PCE gained 0.3%, up from 0.2% in July and matching the consensus.

With inflation largely under control, the Federal Reserve's priority has shifted to the US labor market. The last two nonfarm payrolls reports showed marginal job growth and missed expectations, raising concerns that the labor market is quickly losing steam. If next week's nonfarm payroll report is soft, it could cement an October rate cut.

USDJPY is testing support at 149.75. Next, there is support at 149.62

There is resistance at 149.89 and 150.02

Dollar Index Holds Firm on Fed CautionFundamental approach:

- DXY edged higher this week amid firmer US data and cautious Fed rhetoric that tempered aggressive easing bets. Risk sentiment was mixed, with markets awaiting core PCE for policy cues, supporting the dollar on rate differentials and data resilience.

- Stronger jobless claims and an upgraded Q2 GDP print underpinned the greenback, while Fed speakers highlighted divisions over the pace of additional cuts, limiting the index's downside.

- DXY could stabilize or firm if core PCE surprises, while a soft print may rekindle cut expectations and weigh on the dollar.

Technical approach:

- DXY broke the descending trendline and retested the key resistance at around 98.60. The index is around EMA21, and it is awaiting an apparent breakout to determine the upcoming trend.

- If DXY breaks above EMA21 and key resistance at 98.60, the index may retest the following resistance at 100.

- On the contrary, failing to close above 98.60 may lead the index to retest EMA78 or the following support at around 97.15.

Analysis by: Dat Tong, Senior Financial Markets Strategist at Exness

SNB holds interest rates, US GDP revised higher, Swissy slips The Swiss franc is sharply lower on Thursday. In the North American session, USD/CHF is trading at 0.8013, up 0.78% on the day.

The Swiss National Bank held its benchmark rate at zero earlier today. The decision was widely expected. The Swiss franc has fallen sharply today but that is more likely due to the surprising strong US GDP release, rather than the SNB rate cut.

The SNB statement noted that inflation had remained virtually the same in the second quarter and the inflation outlook called for little change. However, members expressed concern about the slowdown in global economic growth and the uncertainty over US tariffs.

The statement said that the Swiss economy had been affected by the US tariffs, dampening the export sector. In particular, the machinery and watchmaking industries had been hit, but the impact on the services sector had been limited.

Switzerland has been hit with massive tariffs of 39% on Swiss goods, and the statement warned that the economic outllook for the country remains "uncertain".

Third-estimate GDP climbed to 3.8% in the second quarter, a strong improvement from the 3.3% gain in the second estimate. This was above the consensus of 3.3%. The gain was driven by stronger consumer spending and a sharp decline in US imports.

The tariffs continue to create uncertainty and could dampen consumer spending as the price of imports rise. There are concerns that GDP will fall significantly in the second half of the year.

The Federal Reserve signaled at last week's meeting that it planned to cut rates twice more before the end of the year, but today's strong GDP data lowers the pressure on the Fed to ease policy. The markets have priced in an October rate cut at 88%, according to CME's FedWatch.

BTC | 111k holds: tactical long bias, eyes on 113.1k__________________________________________________________________________________

Market Overview

__________________________________________________________________________________

BTC is consolidating above 111,040, trapped in a tight range with a higher‑timeframe bullish bias, while intraday remains pressured below 113,129. The 111k area acts as the market’s key pivot. 🔁

Momentum: Range with bullish tilt 📈 — higher TFs positive (1D/12H), intraday needs a reclaim above 113,129.

Key levels:

• Resistances (TF): 113,129–114,384 (240/1D, immediate ceiling), 117,900 (1D, upper cap).

• Supports (TF): 111,040 (240/1D, major pivot), 110,440 (intraday), 107,255 (1D).

Volumes: Normal on daily; moderate on 4H/30m downside pushes — no standalone catalyst.

Multi-timeframe signals: 1D/12H/6H bullish, 4H/2H/1H mixed-to-bearish below 113,129; a reclaim/hold > 113,129 opens 114,384.

Risk On / Risk Off Indicator: NEUTRAL BUY (stronger on 15m) — confirms the range‑bullish bias and favors buy‑the‑dip above 111k.

__________________________________________________________________________________

Trading Playbook

__________________________________________________________________________________

Strategic stance: higher‑timeframe uptrend, prefer tactical longs above 111,040. 🎯

Global bias: NEUTRAL BUY while 111,040 holds; key invalidation on a close below 111,040 (align TF to your horizon).

Opportunities:

• Defensive long: bullish reaction confirmed above 111,040; add on break/hold > 112,300 then > 113,129.

• Breakout long: close and hold > 113,129 (30m/15m ≥ 2 bars) to target 114,384.

• Tactical sell: clean rejection at 112.9k–113.1k with selling volume, target a pullback to 111,040 (reduced size vs HTF filter).

Risk zones / invalidations:

• A confirmed loss of 111,040 → increases risk toward 110,440 then 107,255.

• Reclaim & hold > 113,129 → negates intraday pressure and unlocks 114,384.

Macro catalysts:

• Fed: -25 bps cut with dovish guidance — medium‑term risk support, validates buy‑the‑dip.

• Dollar (DXY): bounce risk — near‑term headwind, argues for staged entries.

• ETF flows: recent modest inflows, neutral‑to‑slightly constructive — not a trigger but doesn’t cap the technical upside.

Action plan:

• Entry: 111,300–111,500 on re‑acceptance/HL confirmation (15m/30m); add if holding > 112,300 then > 113,129.

• Stop: 110,850 (below swing & S1).

• TP1: 112,950; TP2: 113,129–113,300; TP3: 114,300–114,400.

• R/R: ≈ 2.0–2.5x depending on execution and adds.

__________________________________________________________________________________

Multi-Timeframe Insights

__________________________________________________________________________________

Overall, higher timeframes lean bullish while lower timeframes remain pressured until 113,129 is reclaimed. 🧭

1D/12H/6H: Bullish bias while holding 111,040; clearing 113,129 then 114,384 would enable compression toward 117,900.

4H/2H/1H/30m/15m: Intraday pressure below 113,129, moderate volume on sell pushes; dip‑buys near 111,040 remain preferred as long as the pivot holds.

Key divergences: HTF Up vs LTF Down → favors “buy the dip” at support, confirmed by volume and reclaim of prior caps (112,300 → 113,129).

__________________________________________________________________________________

Macro & On-Chain Drivers

__________________________________________________________________________________

Macro backdrop is modestly supportive (dovish Fed), but a dollar bounce could cap near‑term rallies; ETF flows are constructive but not decisive. ⚖️

Macro events: Fed -25 bps and still‑dovish dot plot support risk; a technical DXY bounce remains a short‑term counterweight.

Bitcoin analysis: Defending ~111k near the 100D; gradual recovery toward the 50D plausible if 113,129/114,384 are reclaimed; institutional/ETF tone mildly positive.

On-chain data: Not provided — technicals and flows drive the lens.

Expected impact: Macro is broadly risk‑friendly, but execution should be paced under resistance; prefer staged entries above 111k.

__________________________________________________________________________________

Key Takeaways

__________________________________________________________________________________

BTC is ranging above 111,040 with a higher‑timeframe bullish bias and intraday headwinds below 113,129.

- Trend: bullish in HTF, neutral/paused intraday until 113,129 is reclaimed.

- Setup: buy the dip above 111,040, then add on breakout > 113,129 toward 114,384.

- Macro: Dovish Fed supports the case, while a firm DXY can slow upside.

Stay nimble: watch 111,040 defense and the 113,129 reclaim to trigger the next leg.

Fed Cut Hopes & Geopolitical Risks Fuel Gold Rally📊 Market View

Gold is holding its bullish tone, trading firmly above 3750 USD/oz and refreshing daily highs in the European session. Investor sentiment is being lifted by rising expectations that the Federal Reserve will continue rate cuts into year-end, lowering borrowing costs and strengthening demand for non-yielding assets like gold. Meanwhile, geopolitical risks keep safe-haven flows alive, further reinforcing gold’s momentum.

🔎 Technical Analysis (H1/H4)

Price structure remains bullish above 3750, supported by trendline dynamics.

Buy liquidity zones identified at 3742–3740 (major demand) and 3757–3755 (scalp entry).

Key short-term resistance sits around 3778, with extended liquidity targets towards 3813–3815.

A rejection from the 3813–3815 sell zone could trigger pullbacks into demand areas.

🔑 Key Levels

Resistance: 3778 ➡️ 3813–3815

Support / Buy Zones: 3757–3755 ➡️ 3742–3740

📈 Scenarios & Trading Plan

✅ BUY ZONE (Main Setup): 3742–3740

SL: 3735

TP: 3748 ➡️ 3752 ➡️ 3756 ➡️ 3760 ➡️ 3770 ➡️ 3780 ➡️ …

✅ BUY SCALP (Aggressive Entry): 3757–3755

SL: 3750

TP: 3762 ➡️ 3766 ➡️ 3780 ➡️ …

✅ SELL ZONE (Liquidity Trap): 3813–3815

SL: 3820

TP: 3810 ➡️ 3805 ➡️ 3800 ➡️ 3795 ➡️ 3790 ➡️ 3780 ➡️ …

⚠️ Risk Management Notes

Watch for fake breakouts near 3813–3815 — liquidity sweeps are common before reversal.

Prioritize long entries on confirmed pullbacks, avoid chasing price in the middle range.

Keep position sizing modest as volatility could spike on Fed commentary or geopolitical updates.

✅ Summary

Gold remains in a strong bullish phase, fueled by Fed rate cut expectations and geopolitical tensions. Strategy: buy dips at 3757–3755 or 3742–3740, targeting 3770–3780, while watching for short-term rejection at 3813–3815 for potential sells.

📢 Follow MMFLOW TRADING for live intraday updates, liquidity-based trading setups, and high-probability strategies on XAUUSD.

$SPY / $SPX Scenarios — Thursday, Sept 25, 2025🔮 AMEX:SPY / SP:SPX Scenarios — Thursday, Sept 25, 2025 🔮

🌍 Market-Moving Headlines

📉 Data-heavy morning: Multiple macro releases hit at 8:30 AM, setting tone across bonds, USD, and equities.

💬 Fed chorus: Packed lineup of Fed speakers keeps policy narrative in focus.

💻 Tech + rates tension: AMEX:XLK flows remain sensitive to bond yield direction post-FOMC.

🛢️ Energy lens: Oil volatility continues to act as an inflation wildcard.

📊 Key Data & Events (ET)

⏰ 🚩 8:30 AM — Initial Jobless Claims (weekly)

⏰ 🚩 8:30 AM — GDP (Q2, third estimate)

⏰ 🚩 8:30 AM — Durable Goods Orders (Aug)

⏰ 10:00 AM — Existing Home Sales (Aug)

🗣️ Fed Speakers:

• 8:20 AM — Austan Goolsbee (Chicago Fed)

• 9:00 AM — John Williams (NY Fed) & Jeff Schmid (Kansas City Fed)

• 10:00 AM — Michelle Bowman (Fed Vice Chair for Supervision)

• 1:00 PM — Michael Barr (Fed Gov.)

• 1:40 PM — Lorie Logan (Dallas Fed)

• 3:30 PM — Mary Daly (San Francisco Fed)

⚠️ Disclaimer: Educational/informational only — not financial advice.

📌 #trading #stockmarket #SPY #SPX #GDP #joblessclaims #durablegoods #housing #Fed #Powell #Dollar #bonds #megacaps