Are the bond bulls in control or is it time for a break?Bonds have reached a very important level. For now this seems like a *logical* place for the *anti-reflation* / deflation trade to end, and for the risk on trade to be back. I am more on the disinflationary (very low inflation) camp, however bonds have risen substantially and it might be time to take some profits before the resume lower. I don't think we will have extremely high inflation yet and I don't think we will have the good type of inflation because things are going well. I do expect Oil to go higher and that to cause all sorts of issues and higher prices, but other than that I don't think bonds will get crushed. At least no yet.

The key question for the whole reflation trade is... WIll bonds and USD keep going higher, with only US behemoths rallying or and the rest bleeding or struggling, or could we get a larger shock? Because to me if the USD really breaks out and heads for 96 on the DXY, while bonds also rally... we will eventually see something break. I think we'll soon have a better idea of where things could be heading next so it is better to be patient and take a few select trades that go well with this environment and look technically sound.

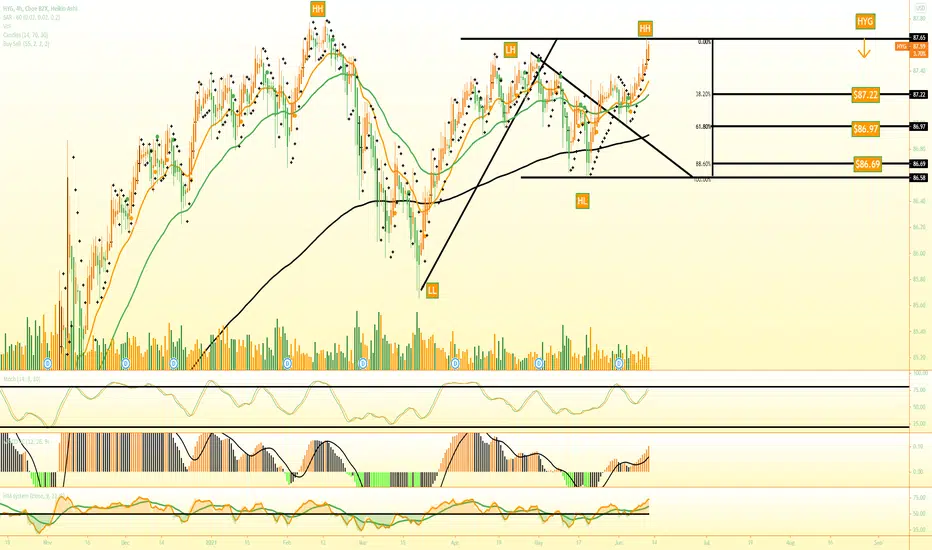

HYG

Credit - HYG ShortIdea for HYG:

- Top of the range, rising wedge.

- Short TP1: 77.

- PT 67.

GLHF

- DPT

SHORT | HYGAMEX:HYG

Possible Scenario: SHORT

Evidence: Price Action

Call options, Strike 86$, 05/28/21 80%POSITION

* This is my idea and could be wrong 100%

Are bonds ready for a bounce?Bond have fallen a lot and quite fast. The sentiment is really stretched and most expect yields to rise more (bonds to fall lower). In my opinion there is quite a decent chance the bond bull market is over given that we had a massive blow off top in March 2020, but this doesn't mean that I don't see a potential bounce here or even bottom. Bonds hit key support, swept the lows before the big move up and are no showing signs of life.

When I see so much debt, when I see slow growth and all the bad things going on around us... I don't think we'll get huge inflation any time soon. To me this is cyclical inflation after a supply shock rather than anything else. Many other yields are decreasing and spreads are the tightest they've been in years, so why would bonds go much lower? The Fed has failed to meet its inflation target for years, but they are going to make it now? We are also post the SLR cliff that could had been the 'sell the rumour buy the news event'

Is high yield signalling a top on SP500?Is high yield debt signalling a top of the SP500?

In the past the market flipped when high yield debt reached these prices.

2021-03-08, Mon. HYG still a wary monitoring!After the US Federal stimulus package re-confirmed passed. Several sectors just strengthen up in place; be it crypto or US Dollar index . At anytime, the tides went South. We need to get out!

2021-02-25, Thu. (HYG) HIGH YIELD CORPORATE BOND ETF (UPDATED)This will be the zoom out version for better picture.

2021-02-23, Tue. High Yield Corporate Bond ETF.The fear of many still remain fresh in every sentiment.

The 2nd Bear Coming

OPENING (IRA): HYG FEBRUARY 19TH 84 SHORT PUT... for a .70 credit.

Notes: The 30 days until expiry weekly isn't very liquid where I want to set up my tent, so going out to the February monthly (59 days until expiry) to collect about twice the monthly dividend in premium instead.

OPENING (IRA): HYG FEBRUARY 19TH 83 SHORT PUT... for a .37/contract credit.

Notes: Selling the strike in the monthly that pays a credit > or = to the monthly dividend, looking to emulate monthly dividends without being in the actual stock. The weeklies, unfortunately, aren't as liquid as I would like, so will sell in the nearest monthly down to 30 days until expiry.

HYG Global view WWe are very close to hit the resistance level 89 by wave (Z) of (WXYXZ) to complete the edge of B.

It can take from couple of weeks to couple of months to hit the level. We expect the downtrend to start by summertime (May-June 2021)

Afterwards the big-big sale of “junk bonds” will undoubtedly start along with deep correction on all the markets which will last till the end of the year 2021

In this case the HYG market might repeat the level of March 2009 - 62

OPENING (IRA): HYG JANUARY 15TH 84 SHORT PUT... for a .37/contract credit.

Notes: Parking a little bit of idle capital in HYG in the expiry nearest 30 days in the strike that pays at or greater than the monthly dividend. Fine with getting assigned, selling call against if that happens. Will otherwise run through expiry/expiring worthless.

OPENING (IRA): HYG JANUARY 8TH 85 SHORT PUT... for a .42/contract credit.

Notes: Selling the strike nearest 30 days that pays at or slightly greater than the monthly dividend to park buying power in short duration in lieu of just letting buying power sit idle. I'm fine with taking assignment, selling call against, so will run these to expiry, particularly given the credit received.

OPENING (IRA): HYG DECEMBER 31ST 84.5 SHORT PUT... for a .35/contract credit.

Notes: Selling the strike nearest 30 days 'til expiry that pays a credit that exceeds the monthly dividend.

High Yield / 30-Yr Bonds ~~ HYG/TLTInteresting leading indicator.

HYG = RISK ON

TLT = Risk OFF

Signals risk off when money moves from High Yield into Fixed Income asset class.

OPENING (IRA): HYG DECEMBER 24TH 84 SHORT PUT... for a .38 credit.

Notes: Here, selling the strike nearest 30 days that pays an amount approximately equal to or greater than the monthly dividend. (See Post Below). Just looking to park what would otherwise be just idle cash in fairly short duration. I'm okay with getting assigned, but would rather just keep the premium.

OPENING (IRA): HYG DECEMBER 18TH 83 SHORT PUT... for a .36 credit.

Notes: Although implied volatility really blows chunks here (30-day at 11.9%), looking to deploy some capital in an underlying I wouldn't mind acquiring for its dividend (current yield 4.94%). Here, selling in the expiry nearest 30 days 'til expiry for a credit that's approximately equal to the monthly dividend (currently .359). This should generate an annualized return approaching the dividend yield without being in the stock itself.

EDUCATION: SYNTHETIC DIVIDEND GENERATION VIA SHORT PUTI think everyone can generally agree that idle cash sitting in your account doesn't earn you much. Here are a couple of methodologies to deploy that capital to emulate dividend generation without being in the stock itself.

For purposes of this exercise, I've chosen HYG, which is not only options liquid, but also has a decent dividend relative to the broader market. Currently, it's 4.92% annually, and its last monthly dividend was .359/share compared to SPY's annual yield of 1.59% and TLT's 1.57%.

In the past, I've used several different methodologies to generate a yield approaching what the underlying is paying annually, depending on how much capital I wanted to or needed to tie up while waiting for opportunities.

(a) The Once a Month/30 Days 'Til Expiry Option: When the next monthly is 30 days until expiry, sell the option paying greater than or equal to the current monthly dividend. Run it until expiry and allow the option to expire worthless and/or take on shares if in-the-money, and sell call against at the same strike as you sold the put. Manage thereafter as you would any ordinary covered call. This is potentially the least buying power intensive setup if you're just selling one contract per month and will necessarily be of short duration.

(b) The Each and Every Weekly 30 Days 'Til Expiry Option: Each week, in the expiry nearest 30 days until expiry, sell the option paying greater than or equal to the current monthly dividend, again allowing each successive weekly option to expire worthless and/or take on shares if in-the-money, selling call against at the same strike as you sold the put, managing it thereafter as a covered call. Naturally, if you want to do something like this each and every week, doing, for example, one contract per week, you'd be tying up greater buying power and/or notional risk to do so. The upside: your longest duration is going to be 30 days.

(c). The Laddering Out in Successive Monthlies Option: Instead of doing just the next monthly at 30 days until expiry, ladder out 30, 60, and 90 days until expiry, selling the put in each successive monthly expiry for an amount greater than or equal to the current monthly dividend. For example, sell the December 18th 83 for .38; the January 15th 80 for .42; and the February 19th 76 for .38. When the front month expires worthless, consider selling a new back month, again for a credit that is equal to or exceeds the monthly dividend. The downside to this methodology is that it is not only buying power intensive, it ties up buying power for greater duration.

OPENING (IRA): HYG NOVEMBER 20TH 77 SHORT PUT... for a .66/contract credit.

Notes: A starter position in "junk" at the 17 delta in the November cycle. The implied volatility here is quite low -- 15.7% for the 30-day, but I'm looking to eventually swap out my TLT position for something that pays more on a percentage basis. HYG's yield is currently 5.02% with a monthly dividend payment of .341, with the short put premium nearly twice that amount, so I'm fine with just keeping the premium versus actually being in the stock. TLT's yield is currently a paltry 1.62% with a monthly dividend of .18292 as of the last distribution.