OIH

USOIL possible rising in mid-term Oil move slowly as wave 4 and there is last decline. Divergence in MACD support this opinion. Once oil makes new low and MACD divergence still appear, the confirmed buy signal will trigger.

SUB-15 VIX SPELLS A CONTINUATION OF THE BREAK IN PREMIUM SELLINGUgh. In spite of abysmal non-farm payrolls, the week ended with the VIX still in sub-15 territory, meaning that less than 45 DTE premium selling in the broader indices is "off the table" for another week in the absence of something earth-shaking occurring in the markets here. This could come in the form of the most recent "Brexit" referendum poll, which shows the "Brexit" vote moving into a narrow lead over the "Bremain" constituency, albeit with a fairly large number being currently undecided (43% Brexit; 40% Bremain; 17% unwilling to commit to a camp). (GPBUSD is off 100+ pips in early Asian trading; the Euro, largely unfazed).

Aside from broader market instruments, there is nothing popping in the ETF space or in individual underlyings for me to play. My "picky" standards are for an implied volatility rank of 70% plus, a greater than 50% implied volatility, and relatively high options liquidity, and there hasn't been an underlying that meets those criteria in several days.

GDX and GDXJ, however, continue to flirt with an implied volatility rank in the 50-65 range, which could easily have them pop to the forefront here and make them playable in the next several days depending on what happens with gold here (it popped on the poor non-farm's).

And so, I continue to watch for a bit and manage the trades I've got on now. Here's what I'm gandering at:

FXE/EURUSD: With the Euro, I'm looking for price to revisit 1.14+ to get in short via an FXE directional play (so pissed that I missed that spike to EURUSD 1.16), but I want to wait and see how the Brexit uncertainty plays.

TBT/TLT: People just don't want to give up their treasuries here, in spite of the fact that we're quite close to all-time highs in the S&P. In a tightening environment, the general notion is to short treasuries, but if TLT is here at this point in the S&P's trajectory, where's it going to be if the market engages in a modest corrective dip? Higher, so best to wait for TLT to digest the crappy non-farm's for a directional play short or, inversely, a directional play long in the inverse TBT.

VIX/VIX Derivatives: The long vol trade has been disappointing, to say the least, in the short term. Volatility has absolutely caved and contangoized instruments like VXX and UVXY have given up even more. However, there still might be long vol opportunity here, but I'm going to be awfully picky since I already have some long VXX trades on. I'm still looking for the golden sub-12 "moment" in VIX to go long in that instrument with something akin to what I set up in VXX -- a poor man's covered call with the back month far out in time and deep in the money and the front month at the 75% probability out of the money strike. Naturally, we may never get there ... .

Oil: I'm looking for short opportunities if I can get them or, in the alternative, a premium selling play on high implied volatility in one of the oil ETF's (XOP, OIH). It looks sideways or consolidative here, and the implied volatility in the ETF's I ordinarily play isn't enough to bother with yet ... .

/CL-USOIL -- WAIT FOR EMA CROSS + SUPPORT BREAK BEFORE SHORTINGIf you're into oil, my guess is that you're hot to short the stuffing out of this instrument in the vicinity of this $50 level. Me, I'm waiting for a couple of different things to happen. Here's why:

First, oil's been an somewhat of a tear (albeit, sputtering in places) off of the April low of 35.22. Shorting here would be against the trend, which has been bullish. That being said, the upside reward here is somewhat indeterminable, and if you try to do any reading on the subject, there is speculation all over the place as to where price moves from here (e.g., "Saudis don't want >$50 oil, since this brings the spectre of shale piling back into the market"; "Shale is primed to ramp back up on >$50"; "Shorters, feeling the pain on misgauging the 'top,' are bailing here, their egos crushed", etc.).

Secondly, it simply doesn't look like a breakdown is imminent, with the short and long EMA's angling upward, and it could very well flop around in a fairly narrow range (as it is want to do for annoyingly long substantial periods of time).

Third, an OPEC meeting is right around the corner. Although not much is likely to happen during the meeting, the fact that "nothing happened" may actually move the markets, since the Saudis are likely to continue to embrace the status quo (which is basically that they will not be the last kids on the block to pump their petro out of the ground and won't agree to anything that makes them the "last kids"). If they don't or if something else comes out of the meeting (which would be an event of miraculous proportion), I certainly don't want to be on the wrong end of things, which is why I'm patiently waiting here.

From purely a charting standpoint, I'm looking for a cross of the 8 and 34 EMA's on the 4H, followed by a break of significant support (which I kind of see at 47-ish) to short on lower time frames (1H or lower) on a retrace to the "slow" EMA or, alternative, an underside test and subsequent rejection of 47 with my eye on taking profit at 43 or, at the very least, peeling some off there and/or moving my stop loss down significantly into profit to allow the trade to run if it appears there's going to be continuation through that level.

As an alternative to trading /CL directly or USOIL, I'm also looking at oil proxies like XOP and OIH for possible bearish assumption option setups (short call verticals or long put verticals) or USO to trade any /CL breakdown should it occur. If I spot any "juicy" option setups in these instruments, I'll be sure to post those separately ... .

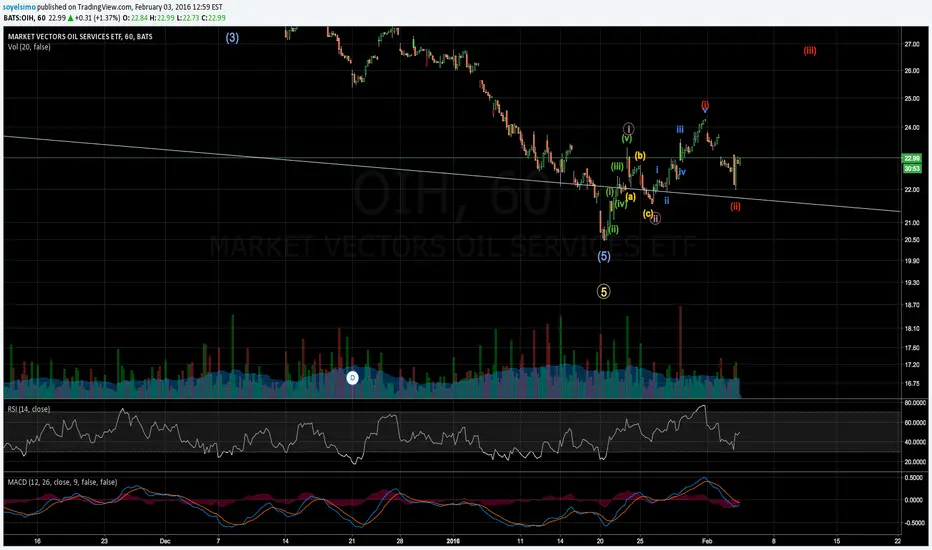

3 of 3 in progress for OIH(iii) wave target's around $26,46 for a 1,618 of (i)

(iv) waves would correct the bullish no under $24,26, should be less if goes to the 0.381 fibbos retracement of (iii) wave

(v) will go to $29,13 again for a 1.618 of (i) that matches the 2.618 fibbo of i (circle wave) what really makes sense...

will see...

Now below $21.56 invalids the analysis.

XOM Exxon Mobil resting buy orders below $81I will be accumulating $XOM Exxon Mobil below $81 as a scale in. Approx $80 down to $78 is a zone that is showing a high probability of at least a significant bounce. Currently XOM is signaling accumulation. It may turn into something more. My strategy is: I'm wrong below $75 and/or scale out some with profit at $85 and move my stop(s) up. This is a risk management strategy.

SLB- Another Bull Channel Building3-5 And here we are today with yet another

energy stock building a Bull channel in green.

What do I need to see to make me get long?

An upside crossover of the green line that's what.

THEN one could place a stop on any break below

the blue line of line of one's choosing. The top blue line

is a tighter stop and IF IF IF an issue is going to go

after breaking out of channel it won't come back-that's

what you want to see anyway after an upside breakout.

As usual this is all strictly for informational and educational purposes only.

Trade at your own risk

$CL_F $USO WTI Crude Oil near trend supprtCrude oil wti futures on approach from above to linear trend line from Dec 1998 to Nov Jan 2009 extended to present. Should see a bounce or stabilization at least. Need to re analyze as condtions in this market are NOT normal. Caution on the long side. Likely short covering. Activity slowing down upon approach. Over night likely to have the move.