How US03M Are Front‑Running the Next Fed Cut The link between bonds and rates

The US03M tracks the yield investors demand to lend to the U.S. government for three months, and this yield moves closely with the Federal Funds Rate set by the Fed.

When the Fed hikes, short‑term Treasury yields usually rise toward the new policy rate, and when markets expect cuts, these same yields start dropping before the official decision.

Why US03M front‑runs the Fed 🕒

US03M is a pure play on near‑term monetary policy, so traders price in where they think the Fed Funds Rate will be over the next quarter, not where it is today.

As a result, sharp declines in US03M while the official Fed rate is still flat often signal that fixed‑income markets are betting on upcoming rate cuts.

Why a 25 bps cut is likely 🎯

With US03M hovering roughly a quarter of a percent under the current effective policy rate area shown on the chart, the bond market is effectively voting for at least a 25 bps reduction at the next meaningful decision.

If the Fed cuts by 25 bps, US03M is already priced for that move, so the bigger reaction will come only if the Fed surprises with either a larger cut or no cut at all, giving traders a clear benchmark for risk positioning.

Fed

GBP/USD: Institutions Accumulate, USD Weakens – Key PullbackMacro Context and USD Index (DXY) – Neutral/Weak USD Bias

The COT report on the Dollar Index shows a configuration that suggests sustained bearish pressure on the USD:

Non-commercial traders are adding both long positions (+6,038) and short positions (+5,474), but the overall structure remains clearly short-dominant (32,207 shorts vs. 16,645 longs).

Commercials significantly increase their USD long exposure (+1,188), though their activity typically reflects hedging rather than a directional view.

Open interest rises sharply, signaling renewed institutional participation on the sell side of USD.

In summary, net pressure remains bearish on the USD, a condition that favors upside continuation in GBP/USD.

COT on the British Pound (GBP) – Clear Improvement in Institutional Sentiment

The GBP report is far more revealing:

Non-commercials aggressively cut long exposure (–19,354) while sharply increasing shorts (+15,403).

However, commercials substantially increase their GBP long exposure (+40,231) while reducing short exposure (+504).

This dynamic is typical of market turning points:

When non-commercials rapidly reduce longs and add shorts, it often represents short-term emotional selling.

Commercials, meanwhile, accumulate heavily, suggesting that current price levels are perceived as attractive value zones.

Interpretation:

GBP is likely entering a structural accumulation phase.

Combined with USD weakness → this supports a moderately bullish medium-term bias on GBP/USD.

Retail Sentiment – Contrarian Confirmation of Potential Upside

Retail short: 56%

Retail long: 44%

Retail positioning is predominantly short → classic contrarian signal → reinforces a bullish scenario for GBP/USD.

Seasonality – December Historically Bullish

December typically shows positive seasonal behavior, especially across the 5-year and 2-year curves.

The 10-year curve is slightly bullish as well; only the 20-year curve is mostly neutral.

Interpretation: December tends to favor accumulation and upward extensions, particularly in the second half of the month.

Price Action & Key Levels

Price recently bounced from the ascending channel highlighted in green.

A strong bullish impulse candle broke previous micro-structure, and the pair is now undergoing a technical pullback.

The blue zone (1.3160–1.3230) represents the major daily demand area that initiated the latest rally.

Primary Scenario (Bullish – Higher Probability):

A retracement toward 1.3240–1.3260 is expected, aligning with a retest of the ascending trendline.

From this region, a bullish continuation toward:

• 1.3420 (first supply zone)

• 1.3550 (intermediate liquidity pocket)

• 1.3600–1.3650 (macro supply and seasonal target)

The daily RSI remains neutral, with no signs of exhaustion, leaving ample room for further upside.

Waiting for an Impulse Ahead of the Fed Decision #USDJPYUSDJPY remains in a steady bullish structure and is holding near local highs amid a strong US dollar and the continued accommodative policy of the Bank of Japan. At the same time, the market is entering a waiting phase ahead of the key event of the week — the Federal Reserve decision, which is expected to sharply increase volatility.

The market is pricing in a 0.25% rate cut by the Fed, but the decisive factor for further direction will be the tone of the press conference. Comments on inflation, economic conditions, and the future path of monetary policy will shape the medium-term outlook.

Technically, the pair is consolidating below the resistance zone near recent highs, while maintaining a bullish structure above key moving averages. There is no sign of aggressive selling pressure at this stage.

Key logic

Before the Fed decision — a high probability of range-bound trading and false moves.

After the decision — a breakout from consolidation and the formation of a directional impulse.

The main focus is on the reaction at the upper boundary of the range and volume behavior

Scenarios

Bullish: breakout above local resistance and impulsive continuation higher after Fed signals.

Corrective: pullback toward the nearest support area while preserving the overall bullish structure.

Bearish scenario is only possible in case of a sharp shift in Fed rhetoric and a breakdown of the current structure.

USDJPY is at a decision point, and today’s Fed meeting will be the key trigger for the next directional move in the pair.

Stop Loss Killers Completed – Bullish Expansion Ahead?After three consecutive Stop-Loss Killers (SLK1, SLK2, SLK3), the market appears to have flushed out remaining buyers and collected liquidity below key lows. This structure often signals the end of a manipulation phase and the beginning of a potential bullish expansion.

With the FOMC rate-cut announcement expected this evening, the market now has both structural and fundamental conditions for an upside move. If the sweep was indeed the final liquidity grab, a rally toward the upper target zone may follow next.

BTC vs. The Fed: The "Neutral Coil" Before the ExplosionDescription: Today represents the collision of a massive macro catalyst (FOMC) and a technically "coiling" market. As professional traders, we do not gamble on the outcome of the speech; we identify the breakout levels that the speech will trigger.

1. The Macro Setup: Priced to Perfection According to the CME FedWatch Tool, the market has priced in an 89.6% probability of a rate cut.

The Trap: When certainty is this high, the "upside" of the news is often limited (priced in), while the downside risk of a "hawkish surprise" is violent. The market is leaning one way, which makes the reaction unpredictable.

2. The Technical Reality: Dead Neutral Replacing complex algorithms with standard, time-tested indicators reveals a market that is holding its breath.

RSI (14): Currently sitting at 48.45. This is effectively 50—dead neutral. Bulls and bears are in perfect equilibrium waiting for a trigger.

Bollinger Bands: Price is chopping directly on the 20 SMA (Middle Band). We are neither overbought nor oversold. We are in "fair value" territory, which is typically where trends go to pause before a volatility expansion.

ADX (Trend Strength): The ADX has dropped to 25, signaling that the previous directional trend has exhausted itself.

3. The Levels to Watch (The Trade) Because the technicals are neutral, we must wait for price to leave this "value zone" to confirm the winner.

Bullish Confirmation: We need a decisive Daily Close above the 0.382 Fib level ($97,600) and the upper resistance knot. Reclaiming this level opens the door to test the $100k psychological barrier.

Bearish Invalidation: If the Fed disappoints, watch the recent swing lows around $84,800. A loss of this support invalidates the recovery and exposes the lower Bollinger Band.

Summary: Do not front-run the Fed. The indicators (RSI 48, ADX 25) are telling us there is no trend right now. Wait for the volatility to break the range, then follow the momentum.

DISCLAIMER: Trading involves significant risk. This analysis is for educational purposes only and is not financial advice. Do your own due diligence.

Gold (XAU) — Short-Term Bearish Pressure Before Bullish ContinuaGold is showing signs of short-term downside pressure. I expect an initial decline into the 4100–4130 zone. However, if the Federal Reserve does not deliver the expected rate cuts and maintains higher levels for longer, there is a real possibility of an extended drop toward the 3940–4000 area before the market stabilizes.

Despite these short-term risks, the medium- and long-term outlook remains bullish. The current structure still reflects a healthy corrective move within a larger upward trend. Once liquidity is cleared below, I expect strong bullish continuation toward the 4600–4700 zone.

Higher-timeframe momentum still favors buyers, and the overall price behavior aligns more with institutional accumulation than with true trend exhaustion.

Drop your asset in the comments + hit the like button and I’ll prepare a custom analysis for you.

Stay patient and trade with precision.

Bitcoin Range Play: 94.2k Gate or 84k MagnetMarket Overview

__________________________________________________________________________________

Price is compressing beneath a dense 92,285–94,213 resistance band into the FOMC, with higher timeframes still tilted down. The tape shows a corrective range: rallies into resistance are being faded while demand sits much lower.

Momentum: Bearish-to-range bias under 94,213 as HTF trend filters (12H/1D) point Down; bounces are tactical and short-lived without confirmation.

Key levels:

- Resistances (HTF): 92,285–94,213 (240–1D confluence), 98,330 (Weekly).

- Supports (HTF): 90,900–91,100 (2H shelf), 89,550 (240 PL), 83,900–84,400 (1D/1H ISPD cluster + D Pivot Low).

Volumes: Normal to moderate overall; noteworthy 1H rejection on very high volume above ~93.5k (bearish context while below resistance).

Multi-timeframe signals: 1D/12H/6H Down, 4H Up tactical, 2H/1H/30m/15m Up tactical; HTF downtrend plus overhead resistance argues for patience or fades until a clean reclaim.

Harvest zones: 77,100 (Cluster A) / 83,700–84,400 (Cluster B) — ideal dip-buy areas for inverse pyramiding, with Cluster B aligned to the Daily Pivot Low.

Risk On / Risk Off Indicator context: NEUTRE VENTE — risk-off regime, confirming the cautious momentum beneath HTF resistance.

Trading Playbook

__________________________________________________________________________________

With HTF down-filters active, adopt a neutral-sell stance below 94,213 and let the FOMC be your catalyst filter.

Global bias: Neutral-sell below 94,213; key invalidation for shorts on a daily close > 94,600 with persistence.

Opportunities:

- Tactical sell: Fade 92,285–94,213 if rejection/weak breadth; target 91.9k/89.55k.

- Breakout buy: Daily close and hold > 94,213 (≥2–3 bars on execution TF) opens 98.33k.

- Dip-buy: 83,700–84,400 cluster only on ≥2H reversal; deeper 77.1k on capitulation with strong signal.

Risk zones / invalidations:

- Break below 89,550 unlocks the magnet toward ~84k cluster; longs invalidated there if no reversal.

- Daily close > 94,600 invalidates the fade and favors 98.33k follow-through.

Macro catalysts (Twitter, Perplexity, news):

- FOMC decision/presser today; tone likely dictates whether 94,213 breaks or 89.55k/84k retests.

- US bank access headlines (OCC letter, PNC spot BTC) are structurally supportive but not overriding HTF resistance yet.

- Hard-asset beta bid (silver > $60) hints at medium-term constructive backdrop if policy is supportive.

Harvest Plan (Inverse Pyramid):

- Palier 1 (12.5%): 77,100 (Cluster A) + reversal ≥2H → entry

- Palier 2 (+12.5%): 74,000–72,500 (-4/-6% below Palier 1) → reinforcement

- TP: 50% at +12–18% from PMP → recycle cash

- Runner: hold if break & hold first R HTF (94,213)

- Invalidation: < HTF Pivot Low or 96h no momentum (D Pivot Low 83,900)

- Hedge (1x): Short first R HTF on rejection + bearish trend → neutralize below R (94,213)

Multi-Timeframe Insights

__________________________________________________________________________________

Timeframes are split: HTF downtrend governs, while lower TFs attempt tactical bounces into stacked resistance.

1D/12H/6H: Downtrend intact beneath 92,285–94,213; failure wicks above ~93.5–94.2k reinforce sell-the-rip; downside magnets remain 89,550 then the ~84k cluster.

4H: Tactical Up but counter to HTF; range structure with supply at 93.5–94.2k and support ~89.6k offers fade entries unless 94,213 is reclaimed decisively.

2H/1H/30m/15m: Up tactical momentum stalls below 94,213; watch 92,285 retests for lower highs. A clean 2H reversal at 89,550 can bounce to 92,285; loss of 89,550 exposes ~84k.

Major confluence: 83,700–84,400 aligns ISPD (1D/1H) with the D Pivot Low — the highest quality demand if tested; 92,285–94,213 is the key supply wall to beat.

Macro & On-Chain Drivers

__________________________________________________________________________________

Into the FOMC, positioning is cautious; structural headlines are improving but flows are not yet decisive.

Macro events: The Fed decision and guidance dominate; a dovish tilt could force a squeeze through 94,213 toward 98.33k, while a hawkish tone favors renewed tests of 89,550/84k. Silver’s surge above $60 underscores hard-asset demand if policy eases.

External Macro Analysis: Broader risk appetite is mixed; elevated implied vol and event risk align with a wait-and-see stance — consistent with our neutral-sell bias until 94,213 is reclaimed.

Bitcoin analysis: Price pinned under 93–97k resistance; several analysts flag limited resistance to ~106k on a confirmed break above ~97k; HTF bull structure intact only while mid-60ks stay unbroken on the really big picture.

On-chain data: ETF net flows modest (7d ~ flat); spot CVD softened; OI lighter; structure fragile unless HTF levels are reclaimed.

Expected impact: Macro/on-chain currently cap upside under resistance; a dovish FOMC could flip the tape to breakout mode, otherwise the path of least resistance is range-backfill into 89.55k and possibly the ~84k cluster.

Key Takeaways

__________________________________________________________________________________

BTC sits in a corrective range beneath 94,213 with HTF down-filters active and event risk front and center.

- Trend: Bearish-to-range while below 94,213; respect the 92,285–94,213 supply until a decisive reclaim.

- Most relevant setup: Fade rejections at 92,285–94,213 with targets to 91.9k/89.55k; switch long only on ≥2H or daily confirmation at ~84k or above 94,213.

- Key macro factor: FOMC decision likely sets direction; dovish break > 94,213 versus hawkish roll back into 89.55k/84k.

Stay disciplined: wait for your signal, then commit — this is a boss fight, not a button mash.

USD/CAD: Will the Great Divergence Break the Greenback?The financial world stands on the precipice of a defining moment for North American currency markets. The USD/CAD pair hovers near 1.3855, ticking nervously as traders count down to a rare double-header of central bank decisions. December 10, 2025, marks a pivotal divergence point where economic pathways between the United States and Canada split sharply. This is not merely a technical adjustment; it is a fundamental collision of monetary policy, geopolitical strategy, and industrial resilience. The outcome will likely dictate the Loonie’s trajectory for the coming year.

Macroeconomics: A Tale of Two Trajectories

The macroeconomic landscape reveals a stark contrast between the two nations. The Federal Reserve prepares to slash interest rates for the third consecutive time, targeting a range of 3.50%-3.75%. Markets price this move at nearly 88% probability. The US labor market displays clear signs of cooling, necessitating easier financing conditions to prevent a recession. Conversely, the Bank of Canada (BoC) stands firm. Canada’s economy defied expectations with a robust 2.6% annualized GDP growth in Q3, crushing earlier forecasts. This resilience compels the BoC to hold rates at 2.25% to prevent reigniting inflation, which remains sticky at 2.2%.

Geostrategy: The Fertilizer Chess Game

Beyond interest rates, a high-stakes geopolitical trade war complicates currency valuation. The US administration’s threat of severe tariffs on Canadian fertilizer imports paradoxically jeopardizes US food security. American farmers rely heavily on Canadian potash, importing over half of Canada’s production. Tariffs here act as a double-edged sword: they aim to punish Canada but simultaneously drive up input costs for the US agricultural sector. This strategic misstep weakens the US Dollar’s purchasing power domestically while forcing the administration to print subsidies, further diluting the currency.

Industry Trends: Agriculture Under Siege

The agricultural industry sits at the epicenter of this financial storm. The promise of $12 billion in aid to US farmers highlights the structural damage already inflicted by trade barriers. This subsidy model creates a vicious cycle of dependency rather than innovation. While Canadian fertilizer producers face tariff headwinds, their product remains essential, granting them significant pricing power. US farmers face a "margin squeeze" that ripples through the broader economy, softening the US economic outlook and diminishing the appeal of the Greenback relative to the resource-backed Loonie.

Management & Leadership: Powell vs. Macklem

Leadership styles at the central banks further amplify market volatility. Fed Chair Jerome Powell operates under intense political pressure and conflicting data, forcing a reactionary "data-dependent" approach. His leadership currently signals caution and retreat. In contrast, BoC Governor Tiff Macklem displays a steady hand, anchoring policy to tangible growth metrics like the recent 180.6K job surge. This stability in Canadian monetary leadership attracts foreign capital seeking predictable returns, creating a natural demand for the Canadian Dollar over the politically volatile USD.

Business Models: Supply Chain Resilience

The trade dispute forces companies to rethink business models. Canadian exporters are diversifying markets beyond the US, strengthening long-term resilience. Meanwhile, US importers face a supply chain crisis, unable to quickly source alternative fertilizer at competitive rates. This rigidity in the US supply chain exposes a critical weakness in the American business model for agriculture. Investors recognize this structural flaw, leading to capital flows that favor the adaptability of the Canadian export sector, thereby supporting the CAD against the USD.

Conclusion: The Loonie’s Rebellion

The confluence of diverging interest rates and self-inflicted US trade wounds creates a perfect storm for USD/CAD bears. The Federal Reserve’s dovish pivot contrasts sharply with the Bank of Canada’s confident hold, widening the yield spread in favor of Canadian assets. Combined with the strategic failure of fertilizer tariffs, fundamental drivers point toward a weaker US Dollar. Traders must watch the 1.3850 level closely; a break below likely signals the start of a prolonged downtrend for the pair. The divergence is real, and the Loonie is ready to rebel.

Gold (XAU/USD) at a CrossroadsGold has been consolidating within a well-defined ascending channel on the 4H timeframe, following a strong rally from late October. Recent price action has formed a clear range between the previous weekly high and low, with intraday swings narrowing, a classic sign of compression before expansion.

As the market awaits today’s Federal Reserve interest rate decision, the technical and macro setups appear to be converging.

On the 4-hour chart, gold continues to respect a broad upward channel, with a midline that has acted as a pivot zone. Current price action is hovering just above the channel midline and near the previous day high (PDH) and previous week low (PWL) levels, suggesting indecision.

Key Zones to Watch:

Support:

4,164–4,170 – Confluence of prior lows, minor Fibonacci zones

4,134 – Structural swing low; loss of this level could signal a deeper correction

4,040–4,050 – Historical demand zone and previous reaction area

Resistance:

4,246–4,265 – PDH / PWH zone; the top of current range

4,381 – Channel upper bound and extended target if bullish continuation resumes

Price has been trapped between ~4,170 and 4,265, forming a sideways structure or distribution phase. This type of price action often precedes large moves, the question is: which direction?

Macro Context – Fed Expected to Cut, But Tone May Be Hawkish

Today’s FOMC meeting is widely expected to deliver a 25 basis point rate cut, marking a potential shift from the high-rate regime of the past 18 months. However, market attention is squarely focused on the tone of the Fed’s forward guidance.

Several Fed officials have recently pushed back on aggressive easing expectations, signaling that even if a cut comes now, the path ahead may not be as dovish as markets hope. This sets the stage for what analysts call a “hawkish cut”, a rate reduction delivered with caution, and paired with messaging that suggests further cuts will be gradual or data-dependent.

Implications for gold:

-A hawkish tone may push U.S. yields and the dollar higher, applying pressure on gold

-A dovish surprise (or less hawkish tone) could boost gold, as it benefits from lower yields and a weaker USD

-The outcome could trigger significant short-term volatility, especially as gold is sitting near key technical levels

Bullish Scenario:

Fed cuts + dovish or neutral tone → yields fall, USD weakens

Gold breaks above 4,265 and

Upside targets: 4,320, 4,381, and possibly 4,400+ into early Q1 2026

Bearish Scenario:

Fed cuts, but tone is hawkish → yields rise, USD strengthens

Gold breaks below 4,164, then 4,134

AUDUSD moves sideways after the RBA holds rates steady

The RBA turned hawkish after holding the rate at 3.60%. The central bank acknowledged that inflation risks have increased despite three rate cuts since Feb, noting that recovering demand and rising wages are making it more difficult to return inflation to the target.

Governor Bullock emphasized that the RBA remains focused on inflation and signaled that, if price pressures persist, the bank may need to take appropriate action.

With policy divergence widening between the Fed and the RBA, the aussie dollar may continue to appreciate against the US dollar.

AUDUSD slightly broke below the ascending channel's lower bound before consolidating within the range of 0.6620–0.6650. The price remains above bullish EMAs, indicating a potential uptrend extension.

If AUDUSD reenters the ascending channel, the price may retest the following resistance at 0.6650.

Conversely, if AUDUSD breaks below EMA21 and the support at 0.6620, the price may retreat toward the next support at 0.6580.

NQ1! — Fed Week: 25,650 Inflection | Tight Decision📊 NQ1! NASDAQ 100 E-MINI FUTURES

December 9, 2025 | by officialjackofalltrades

🟡 CAUTIOUS |Fed Week Special Edition

EXECUTIVE SUMMARY - THE PRE-FED SETUP

Current Price: $25,651.50 | Date: December 9, 2025 | Change: -$48.25 (-0.19%)

The Nasdaq 100 E-mini futures are consolidating in a tight range between 25,000-26,300 as markets brace for tomorrow's Federal Reserve decision. After December E-mini Nasdaq futures rose +0.10% on Tuesday, the index is now sitting in a critical decision zone with massive implications for tech stocks.

The Technical Picture:

Pattern: Range-bound consolidation (4 weeks)

Current Position: Middle of range at 25,650

Resistance: 26,200-26,300 (tested multiple times, rejected)

Support: 24,700-24,900 (solid floor since November)

Key Level: 25,200 (bull/bear line)

The Fundamental Backdrop:

Big Tech was mixed at the close: Amazon booked a modest gain, while Apple, Meta and Microsoft finished slightly in the red. More importantly, These industry titans have consistently outpaced the broader S&P 500, with the S&P 500 Top 10 rising over 600% in total since January 1, 2016.

But here's the tension: AI capex coming from tech companies listed in the S&P 500 is $400 billion or more per year, going forward. The biggest AI company OpenAI has disclosed revenues of just $13 billion for 2025.

The Trade: Long from 25,200-25,600, target 26,500-27,200, stop 24,650. Risk/reward: 1:2.5 .

MARKET CONTEXT - WHAT'S REALLY HAPPENING

The Pre-Fed Paralysis

Stock indexes gave up early gains and settled mixed on Tuesday as bond yields climbed after the Oct JOLTS report showed job openings unexpectedly rose to a 5-month high.

This is classic pre-FOMC behavior : markets waiting for the catalyst before committing.

Investing.com - U.S. stock futures inch down ahead of the start of trading for December, with investors keeping tabs on a possible rate cut.

The AI Valuation Debate

Here's what's creating the consolidation: AI optimism vs. valuation concerns .

BULLISH CAMP:

Nvidia leads the tech sector with a market cap of $4.4 trillion

24/7 Wall St. forecast projects Nvidia revenue rising from $121 billion in 2025 to more than $265 billion by 2030

For the Mag 7 group, total earnings are expected to increase by +12.6% on +9.5% higher revenues in 2025

BEARISH CAMP:

OpenAI may have lost $12 billion in the third quarter of 2025 alone, according to a disclosure by Microsoft

806 Russell 2000 companies (40%) have no earnings or negative earnings

The revenues currently being generated by AI companies are far smaller than the amount of capex being directed at them

My Take: This is why NQ is stuck in range. Bulls see AI growth, bears see bubble. Fed decision tomorrow will tip the scale.

TECHNICAL ANALYSIS - THE RANGE-BOUND BATTLE

Pattern: Consolidation Rectangle (4 Weeks)

Your purple boxes perfectly capture the support/resistance clusters . Let me break down what the chart is telling us:

Key Technical Levels:

🔴 RESISTANCE (Selling Zones):

26,200-26,300: Tested 4 times since November, strong rejection zone

26,500-26,700: If we break above, this is next target

27,000-27,200: Extension target if Fed is dovish

🟢 SUPPORT (Buying Zones):

25,200-25,400: Minor support, current price zone

24,900-25,100: Major support cluster (your bottom purple box)

24,700-24,800: Absolute floor, tested Nov 19

24,300-24,500: Nuclear support if range breaks

Current Position: The Nasdaq 100 Futures price has ranged from 25,657.50 to 25,693.75 today extremely tight range showing indecision.

Technical Indicators:

Moving Averages:

50-day MA: ~25,400 (acting as support)

200-day MA: ~24,200 (long-term uptrend intact)

Golden Cross: Active since October = bullish

Volume:

The current trading volume for Nasdaq 100 Futures is 6,395 very low , typical pre-Fed paralysis.

RSI:

Currently: ~52-55 (neutral)

Not overbought (room to run)

Not oversold (no panic)

MACD:

Flat, coiling for breakout

Waiting for directional catalyst

SCENARIO ANALYSIS - THREE FED OUTCOMES

SCENARIO A: Dovish Cut (55% Probability) - BULLISH

What Happens:

Fed cuts 25bps ✓

Dot plot shows 3-4 more cuts in 2026 ✓

Powell emphasizes "labor market concerns" ✓

Tech gets green light to continue AI spending ✓

Market Reaction:

Immediate: NQ pumps 1.5-2% to 26,000-26,200

Day 1-3: Breakout above 26,300, test 26,700

Week 1-2: Rally to 27,000-27,500

Month 1: Target 27,800-28,200 (+9-10%)

Winners:

Nvidia (NVDA), AMD (AMD), Broadcom (AVGO) lead

Mag 7 outperform

High-growth tech rallies hard

Trade Setup:

Enter: Current 25,650 OR breakout above 26,300

Add: On pullback to 26,000 after breakout

Target: 27,500 (+7.2%)

Stop: 25,100 (-2.1%)

Risk/Reward: 1:3.4

SCENARIO B: Hawkish Cut (35% Probability) - CHOPPY

What Happens:

Fed cuts 25bps ✓

BUT dot plot shows only 1-2 cuts in 2026 ❌

Powell says "inflation still concerning" ❌

Tech valuations questioned ❌

Market Reaction:

Immediate: NQ drops 1-1.5% to 25,200-25,400

Day 1: Volatility, test 24,900 support

Week 1-2: Choppy recovery to 25,800-26,000

Month 1: Grind back to 26,200-26,500 (+2-3%)

Losers:

High-valuation AI stocks hit hard

Stocks with high capex vs. revenue scrutinized

Small caps underperform

Trade Setup:

DO NOT chase before Fed

Buy: Dip to 24,900-25,100 (support)

Target: 26,000-26,300 (+5-6% from dip)

Stop: 24,650 (-2%)

Risk/Reward: 1:2.5

SCENARIO C: No Cut OR Very Hawkish (10% Probability) - BEARISH

What Happens:

Fed HOLDS at 3.75-4% ❌

OR cuts but says "this is the last one" ❌

Powell cites AI bubble concerns ❌

Tech sell-off accelerates ❌

Market Reaction:

Immediate: NQ crashes 2-3% to 24,700-25,000

Day 1: VIX spikes, panic selling

Week 1-2: Test 24,300-24,500

Month 1: Bottom around 23,800-24,200 (-7-8%)

Trade Setup:

Exit ALL longs immediately

Wait for capitulation

Buy: 24,000-24,300 (major support)

Target: Recovery to 25,500-26,000 (+6-8%)

High stress, high reward

THE TRADE SETUP - PROFESSIONAL EXECUTION

🟢 PRIMARY LONG SETUP: BUY NQ1!

Entry Strategy (Scale In):

Option A: Conservative (Wait for Dip):

25,000-25,200 (IF hawkish dip)

24,800-25,000 (IF deeper dip to support)

Best for: Risk-averse traders

Stop Loss: 24,650 (HARD STOP)

Below 24,650 = range break on daily

Below this = technical structure invalidated

Max loss from 25,650 entry:

Take Profit Targets:

TP1: 26,200-26,500

Range breakout + resistance retest

Action: Take 40% profit, move stop to 25,200

Gain: +2.1-3.3% | Risk/Reward: 1:2

TP2: 27,000-27,500

Momentum continuation post-Fed

Technical indicators show Strong Buy signal

TP3: 27,800-28,200

Full breakout, AI optimism returns

Long-term forecast shows potential to $28,452

Entry Confirmation Checklist:

Before entering, CHECK:

✅ Price holding above 25,200 (bull/bear line)

✅ Volume spike on bounce (15K+ contracts on 4H)

✅ Fed announces 25bps cut (as expected)

✅ Powell's tone dovish or neutral (not hawkish)

✅ Mag 7 stocks holding up (NVDA, MSFT, AAPL)

✅ VIX below 16 (fear contained)

WAIT FOR 4/6 BEFORE FULL POSITION

Use Micro E-minis (MNQ) for Better Sizing:

MNQ = $2/point (vs NQ $20/point)

Same moves, 1/10th capital

Better for risk management

Fed Day Protocol (December 10):

2:00 PM ET - Fed Statement:

Tighten stops to 25,100 before announcement

READ statement immediately

Ignore first 5 minutes (algo chaos)

2:30 PM ET - Powell Press Conference:

WATCH LIVE - tone matters more than words

Dovish = add to position on dip

Hawkish = cut 50%, tight stops

5. Emergency Exits:

❌ Daily close below 24,650 = EXIT ALL

❌ VIX spikes above 22 = EXIT 50%

❌ Fed announces NO cut = EXIT ALL

❌ Powell says "last cut for 6+ months" = EXIT 50%

❌ Mag 7 stocks crash 3%+ = EXIT 50%

FUNDAMENTAL ANALYSIS - THE AI CONUNDRUM

CATALYST #1: The Magnificent 7 Dominance

Nvidia, Microsoft, and Apple make up 20.7% of the S&P 500 and 43.6% of the Vanguard Information Technology ETF.

This concentration means:

NQ lives or dies by Mag 7 performance

Fed policy directly impacts these valuations

Any weakness cascades fast

Current Status:

Nvidia: $4.37T market cap

Apple: $4.20T market cap

Microsoft: $4T+ market cap

CATALYST #2: The AI Spending Paradox

Here's the $400 billion question :

AI capex from S&P 500 tech companies is $400 billion or more per year. The biggest AI company OpenAI has disclosed revenues of just $13 billion for 2025.

The Math Doesn't Add Up:

Spending: $400B/year

Revenue: $13B/year

Gap: $387B/year of unprofitable spending

"Can the 10 AI companies generate enough revenue to justify the capex?"

says Torsten Sløk, chief economist at Apollo Global Management.

BUT: Nvidia revenue projected to rise from $121B in 2025 to $265B by 2030 revenue IS growing, just not fast enough yet.

CATALYST #3: Earnings Growth Remains Strong

Mag 7 earnings expected to increase +12.6% on +9.5% higher revenues in 2025.

Excluding the Mag 7, total earnings for remaining S&P 500 companies expected to grow +8.7% in 2025.

Translation: Even without AI hype, earnings are solid.

CATALYST #4: Fed Policy is CRITICAL

With U.S. 10-year Treasury yields hovering just above 4% and the Fed set to decide on a widely expected rate cut, growth stocks remain sensitive to even small changes in rate expectations.

Why This Matters:

Lower rates = higher valuations for growth

Higher rates = multiple compression

Tech has highest duration risk

RISK FACTORS - THE BEAR CASE

RISK #1: AI Bubble Concerns

Nvidia's Jensen Huang says he doesn't believe we're in an AI bubble. Amazon's Jeff Bezos says we probably are in one. OpenAI's Sam Altman has invoked a bubble, adding, "I do think some investors are likely to lose a lot of money".

Even AI leaders are split!

RISK #2: Valuation Stretched

OpenAI may have lost $12 billion in Q3 2025 alone, yet is valued at $500 billion by VCs.

If valuations reset, NQ drops 15-20%.

RISK #3: Concentration Risk

Since October 2022, roughly 75% of gains in S&P 500 have come from just seven stocks.

If Mag 7 stumbles, entire index falls .

RISK #4: Technical Breakdown

Break below 24,650 = target 23,800-24,200 (-6-7%)

THE BOTTOM LINE

Here's what I KNOW on December 9, 2025:

✅ Fed expected to cut 25bps tomorrow

✅ NQ technical indicators show Strong Buy

✅ Mag 7 earnings growing +12.6% in 2025

✅ NQ in consolidation range 25,000-26,300

✅ Support at 24,900 has held 4 times

✅ Your purple boxes show clear support/resistance

Here's what I DON'T know:

Will Powell be dovish or hawkish?

How many 2026 cuts will dot plot show?

Will AI bubble concerns accelerate?

But here's the MATH:

Risk: 25,650 → 24,650

Reward: 25,650 → 27,500

Extended: 25,650 → 28,200

The Play:

Small position NOW 25,650

IF hawkish dip to 24,900-25,100

IF dovish → ADD on breakout above 26,300

Stop 24,650

Target 27,500, then 28,200

Position accordingly.

Follow officialjackofalltrades for institutional-grade futures analysis, Fed-day strategies, and professional risk management.

Drop a 📊 if you're trading NQ through the Fed decision.

Drop a 🎯 if this analysis helped your setup.

Drop a 💰 if you're ready for 27,500+ breakout.

Disclaimer: This is not financial advice. This post is for educational and informational purposes only. Always do your own research and manage your own risk.

XAUUSD Set for Surge? Safe-Haven Demand and Fed Cut Bets AlignHey Traders,

In today’s session we are monitoring XAUUSD for a potential buying opportunity around the 4,200 zone. Gold remains in a strong uptrend, and the current correction is bringing price back toward the key 4,200 support–resistance area, which could offer a favorable entry.

Fundamentally, GOLD should continue to benefit from the ongoing weakening of the U.S. Dollar, driven by expectations of a 25bps rate cut. As we head into Wednesday’s FOMC, markets are likely to keep front-running the event, which typically pressures the dollar lower.

Just be cautious—if we see too much front-running, the classic “buy the rumor, sell the fact” reaction could hit once the decision is officially announced.

Additionally, rising geopolitical tensions between Venezuela and the United States are increasing safe-haven demand, which further supports upside for Gold.

Trade safe,

Joe.

Bitcoin Pre‑FOMC: 92.3k Reclaim or 84k Reload__________________________________________________________________________________

Market Overview

__________________________________________________________________________________

Bitcoin remains in a controlled range beneath 92,285–94,213, with sellers defending overhead supply while buyers cluster around the mid-to-high 80Ks. Momentum is two‑sided but tilts cautious as macro risk remains event‑driven into the Fed.

Momentum: Range with a bearish tilt under 92,285; rallies fade at HTF resistance while 88–84k buys time for consolidation.

Key levels:

- Resistances (4H/1D): 92,285–94,213; 98,330 (weekly underside).

- Supports (4H/1D): 89,258–88,122; 83,871–84,405 (dense cluster with D Pivot Low).

Volumes: Mostly normal on 1–6H with occasional 15m spikes; overall moderate.

Multi-timeframe signals: 12H Down vs 1D Up; 4H attempts up but stalls at 92,3k; net NEUTRAL SELL bias until reclaim.

Harvest zones: 75,700 (Cluster A) / 83,600–84,400 (Cluster B) — ideal dip‑buy areas for inverse pyramiding if a flush prints a ≥2H reversal.

Risk On / Risk Off Indicator context: Neutral sell bias; it confirms the cautious momentum and favors disciplined fades at resistance unless 92,3k is reclaimed.

__________________________________________________________________________________

Trading Playbook

__________________________________________________________________________________

Strategically, treat this as a range with overhead supply; lean patient and reactive, not predictive.

Global bias: NEUTRAL SELL while price is capped below 92,285; invalidation of the cautious stance on a sustained reclaim and hold above 92,285.

Opportunities:

- Buy: 84,0–84,6k cluster only on ≥2H bullish reversal; scale toward 90,2–90,6k, then 92,3–94,2k.

- Breakout: Long on break & retest of 92,3k with breadth; target 94,2k then 98,3k.

- Tactical sell: Fade 92,3–94,2k rejection with weak breadth; manage to 90,4k then 88,3–88,0k.

Risk zones / invalidations: Break and daily/12H hold above 94,6k would invalidate the near‑term short bias; loss of 83,6–83,9k would invalidate the long-at‑84k thesis.

Macro catalysts (Twitter, Perplexity, news):

- FOMC decision and guidance are the near‑term pivot; a dovish tilt could clear 92,3k, a firm tone risks a re‑test of 88k/84k.

- ETF flows slightly negative — a mild headwind to risk‑on.

- External dashboard: Risk On / Risk Off Indicator in sell mode; credit‑sensitive gauges soft, early‑cycle tech mixed — mid‑cycle feel.

Harvest Plan (Inverse Pyramid):

- Palier 1 (12.5%): 75,700 (Cluster A) + reversal ≥2H → entry

- Palier 2 (+12.5%): 72,500–71,200 (-4/-6% below Palier 1) → reinforcement

- TP: 50% at +12–18% from PMP → recycle cash

- Runner: hold if break & hold first R HTF (92,285)

- Invalidation: < HTF Pivot Low (83,900) or 96h no momentum

- Hedge (1x): Short first R HTF on rejection + bearish trend → neutralize below R

__________________________________________________________________________________

Multi-Timeframe Insights

__________________________________________________________________________________

Across frames, the market grinds in a capped range: higher timeframes hold key resistance while midframes lean downtrend, keeping the tape tactical.

12H/6H/2H/30m/15m (Down bias): Price capped below 92,3k with frequent fades; supports at 89,0–88,1k and the 84k cluster attract mean‑reversion bounces.

1D/4H (Up attempt but constrained): Structure can repair if 92,3k breaks and holds; until then, path of least resistance is sideways‑to‑down inside the range.

1H (Mixed): Local supply at 90,9–91,3k acts as a lid; reclaiming this band is often a precursor to testing 92,3k.

__________________________________________________________________________________

Macro & On-Chain Drivers

__________________________________________________________________________________

Macro is event‑driven into the Fed, with mixed risk gauges and soft crypto fund flows tempering trend conviction.

Macro events: Fed decision and press conference in focus; a dovish read supports a 92,3k reclaim while a firm stance risks extending the range or probing 88k/84k. Global yields firmed on ECB tone; gas prices soft aid disinflation.

External Macro Analysis: The Risk On / Risk Off Indicator leans sell; credit‑risk gauges cautious; early‑cycle tech mixed — a mid‑cycle profile that aligns with a neutral‑sell technical bias unless 92,3k flips.

Bitcoin analysis: ETF net outflows are a mild headwind; corporate bids provide dip demand but not trend control. 92k is the ceiling to clear; 88k is pivotal support.

On-chain data: Ownership concentration rising as small holders ebb; whale transfers noted but directional intent unclear; realized volatility remains muted, consistent with “controlled vol.”

Expected impact: Macro/on‑chain context supports a patient, reactive stance — bullish if 92,3k is reclaimed with volume, cautious if 88k breaks toward the 84k cluster.

__________________________________________________________________________________

Key Takeaways

__________________________________________________________________________________

Range with a cautious tilt persists beneath 92,3k as the market awaits the Fed.

- Trend: Neutral to bearish inside 92,285–94,213 resistance; buyers defend 88–84k.

- Best setup: Buy only on confirmed 84k reversal or 92,3k break‑and‑retest; fade weak rejections into 92,3–94,2k.

- Macro: FOMC guidance is the catalyst that can resolve the range and validate or negate the 92,3k reclaim.

Stay patient and surgical — in this Tarkov‑style map, the best loot is in defended zones, not in blind pushes.

USDCAD plunges as BOC vs Fed divergence grows! Can it continue?USDCAD has broken sharply lower following Canada's surprise jobs blowout on Friday, with the pair now pricing in a divergence: the Bank of Canada is expected to hold rates Wednesday, while the Fed is expected to cut.

Canada added 54,000 jobs in November, and the unemployment rate plunged to 6.5%, taking a BOC cut off the table. Meanwhile, the Fed is 90% priced to cut by 25bps on Wednesday, narrowing the rate differential and weakening the US dollar against the loonie.

Key drivers

Canada jobs report beat expectations with +54k positions (vs expected loss), unemployment fell to 6.5% from 6.9% — three straight months of gains totalling 181k jobs.

BOC decision this week virtually certain to hold at 2.25% after cutting in October and signalling the easing cycle is likely over.

Fed FOMC decision on Wednesday priced in at 90% odds for a 25bps cut to 3.75–4%, the third consecutive cut driven by cooling US labour and dovish Fed commentary.

Technical: USDCAD corrected to 50% Fibonacci (1.4140–60) of the 1.4790–1.3543 impulse leg and is now breaking down in a potential head and shoulders pattern with neckline at 1.3543.

Downside targets: 1.3370–1.3396 (61.8% extension + 50% retracement confluence), 1.3068 (61.8% retracement), and 1.2895 (100% extension full measured move).

Risk scenario: Neckline hold above 1.3543 could see bounce back toward 1.36 or 1.43, but below 1.4140, the path of least resistance is lower.

Are you trading the USDCAD breakdown? Share your head and shoulders setups in the comments and follow for more central bank divergence and technical trade ideas.

This content is not directed to residents of the EU or UK. Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Stop!Loss|Market View: GOLD🙌 Stop!Loss team welcomes you❗️

In this post, we're going to talk about the near-term outlook for GOLD ☝️

Potential trade setup:

🔔Entry level: 4167.192

💰TP: 3900.356

⛔️SL: 4370.061

"Market View" - a brief analysis of trading instruments, covering the most important aspects of the FOREX market.

👇 In the comments 👇 you can type the trading instrument you'd like to analyze, and we'll talk about it in our next posts.

💬 Description: After breaking out of the accumulation in a symmetrical triangle, gold prices formed an accumulation near the 4200 level, indicating the emergence of a potential limit seller who, after breaking out of the accumulation, will sell the instrument to those willing to buy at the breakout. Against this backdrop, a downward movement is likely expected, and given the potential volatility this week, two scenarios are being considered.

Thanks for your support 🚀

Profits for all ✅

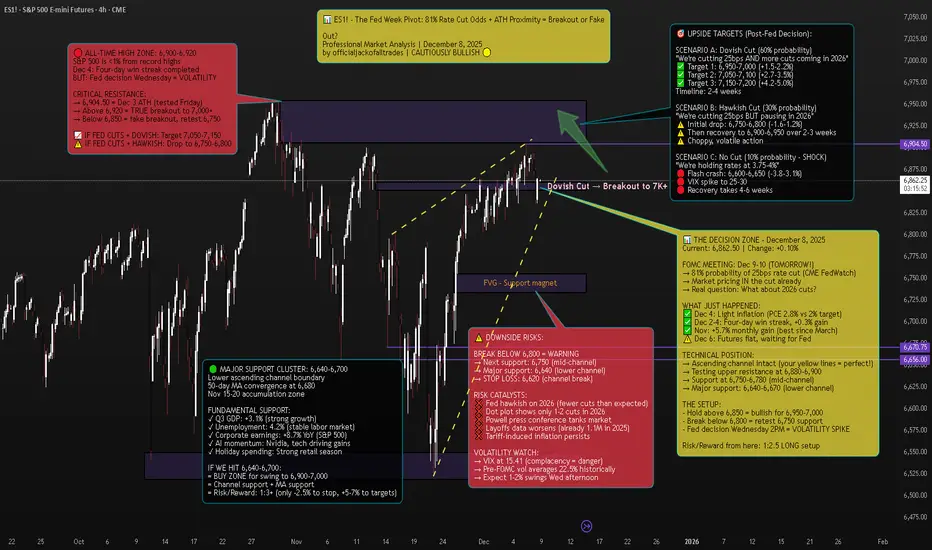

ES1! S&P 500 E-mini Futures - The Fed Week Pivot📈 Executive Summary - The Setup

Current Price: 6,862.50 | Date: December 8, 2025 | Change: +6.75 (+0.10%)

The S&P 500 E-mini futures are sitting less than 1% from all-time highs on the eve of the Federal Reserve's most anticipated meeting of 2025. After a four-day win streak that added 0.3% to the index, markets are now in a classic consolidation pattern at resistance, waiting for Wednesday's 2PM ET catalyst.

The Technical Picture:

Pattern: Ascending channel (intact since November)

Current Position: Testing upper resistance at 6,880-6,900

ATH: 6,904.50 (December 3) - 0.6% away

Support: 6,750-6,780 (mid-channel), 6,640-6,670 (lower channel)

The Fundamental Backdrop:

FedWatch shows a near-90% probability the FOMC will cut the target range for the federal funds rate by another 25 basis points. But here's what markets are REALLY pricing: not just the cut itself (that's a given), but Powell's guidance on 2026.

Minutes from the October meeting showed "many" FOMC members saying no more cuts are needed at least in 2025. Yet the market now indicates an 80% likelihood of a December rate cut, following dovish statements from NY Fed President John Williams and Fed Governor Christopher Waller.

The Trade: This is a tactical long from 6,850-6,870 targeting 6,950-7,050, with stop at 6,820. Risk/reward: 1:2.5.

But the real opportunity? Buying any Fed-induced dip to 6,750-6,800 for a swing to 7,000+.

🔎 Market Context - What's REALLY Happening

The Pre-Fed Calm

US stock futures stall as traders wait for the Fed meeting, with the S&P 500 just below record highs. This is textbook behavior: The indexes have quietly stitched together consistent gains. The Dow and Nasdaq scored back-to-back positive weeks; the S&P 500 added another 0.3% and now sits only a touch from record territory.

S&P 500 futures (ES) traded around 6,880-6,885, roughly 0.1% higher by 6:00-7:30 a.m. ET on Monday.

But don't mistake the calm for weakness. Even after November's wobble, dip-buyers came back as shutdown fears faded and AI jitters cooled.

The Fed's Dilemma

The Federal Reserve is in an impossible position:

Argument FOR cutting:

Concerns about a softening labor market

Employers cut more than 1.1 million jobs through November, the most since 2020 and a 54% increase from the same period a year ago

Job growth remains too low to keep up with labor supply growth and a rising unemployment rate

Argument AGAINST cutting:

Latest inflation scorecard, the Fed's preferred PCE index, is running at 2.8 percent a year, close to its 2 percent goal but not quite there

The annualized inflation rate grew to 3% in September from 2.9% in August and 2.7% in July

Officials expressing skepticism about the need for an additional cut that markets had been widely anticipating, with "many" saying that no more cuts are needed at least in 2025

The Missing Data Problem:

Here's something CRITICAL that most traders don't know: The U.S. central bank will have to make its decision without some key government data. Hiring data for November and the latest inflation number have been delayed until mid-December, after the Fed's meeting, because of the U.S. government shutdown.

The meeting minutes indicated the decision-making was complicated by a lack of government data during the 44-day federal government shutdown. Powell himself compared this to "driving in the fog".

Translation: The Fed is making a $28 TRILLION (SPY market cap) decision BLIND.

The Internal FOMC War

"It's difficult to recall a time when the Federal Open Market Committee has been so evenly divided about the need for additional rate cuts than the upcoming December meeting," Michael Pearce, chief U.S. economist at Oxford Economics, said.

Jerome Powell faces a credibility issue as he tries to satisfy hawks and doves on the most divided Fed in recent memory.

The October meeting vote was 10-2, but the 10-2 vote was not indicative of how split officials were at an institution not generally known for dissent. The minutes revealed multiple camps:

Some favored cutting

Some supported cutting but could have supported holding

Several were against cutting

For December, Mericle expects at least two dissents in favor of no rate cut as well as one in favor of a larger rate cut.

📊 Technical Analysis - The Ascending Channel At Decision Point

The Pattern: Ascending Channel (Bullish Structure)

Your chart annotation is PERFECT. The yellow dashed ascending channel captures the exact structure driving ES1! since the November bottom.

Channel Characteristics:

Lower Support: 6,640 (tested Nov 15, Nov 29) → 6,670 (current)

Upper Resistance: 6,850 (Nov 25) → 6,900 (Dec 3-6) → 6,920 (projected)

Angle: ~25° (strong bull trend)

Tests: 6 touches (3 upper, 3 lower) = highly reliable pattern

Current Position: We're at the UPPER boundary of the channel, testing 6,880-6,900 resistance.

Key Technical Levels:

🔴 RESISTANCE (Selling pressure zones):

6,880-6,900: Current test, upper channel boundary

6,904.50: All-time high from December 3

6,920-6,950: True breakout zone (if we clear ATH)

7,000: Psychological milestone

🟢 SUPPORT (Buying interest zones):

6,850: Immediate support, bull/bear line

6,800-6,820: Minor support cluster + FVG

6,750-6,780: Mid-channel support + 23.6% Fib

6,700-6,720: 38.2% Fib retracement

6,640-6,670: Major support (lower channel + 50-day MA + November accumulation)

Technical Indicators:

Moving Averages:

50-day MA: ~6,680 (rising, bullish)

200-day MA: ~6,450 (rising, bullish)

Golden Cross: Active since mid-November = long-term bullish

RSI (Relative Strength Index):

Current: 58-60 (neutral/slightly bullish)

Not overbought (room to run to 70+)

Not oversold (not panic selling)

Interpretation: Healthy consolidation before next leg

Volume Analysis:

Declining volume into Fed decision = normal pre-FOMC behavior

Stock volatility averages around 22.5% in the month preceding rate cuts, compared with roughly 15% during normal periods

Expect volume spike Wednesday 2PM-4PM (100K+ contracts)

VIX (Fear Index):

VIX at 15.41, down -0.37 (-2.34%)

This is LOW = market complacency

Pre-FOMC, VIX typically rises to 18-22

IF VIX spikes to 20+ Wednesday = sell signal

🎯 Scenario Analysis - Three Possible Outcomes

SCENARIO A: Dovish Cut (60% Probability) - BULLISH

What Happens:

Fed cuts 25bps to 3.50-3.75% range ✓

Dot plot shows 3-4 more cuts in 2026 ✓

Powell says "labor market concerns outweigh inflation" ✓

Balance sheet runoff stops as planned (December 1) ✓

Market Reaction:

Immediate: ES pumps 1-1.5% to 6,930-6,950

Day 1-3: Consolidation at 6,920-6,950

Week 1-2: Breakout to 7,050-7,100

Month 1: Target 7,150-7,200 (+4.2%)

Sector Leaders:

Small caps (Russell 2000) +2-3%

Tech (Nasdaq) +1.5-2%

Financials +1-1.5%

Trade Setup:

Enter: ANY dip to 6,850-6,870 before Fed

Add: On breakout above 6,910 with volume

Target: 7,050 (+2.7%), 7,150 (+4.2%)

Stop: 6,820 (-0.6%)

Risk/Reward: 1:4

SCENARIO B: Hawkish Cut (30% Probability) - NEUTRAL/CHOPPY

What Happens:

Fed cuts 25bps to 3.50-3.75% range ✓

BUT dot plot shows only 1-2 cuts in 2026 ❌

Powell says "we're near neutral, will pause to assess" ❌

Market had priced in 3-4 cuts for 2026 = DISAPPOINTMENT

Market Reaction:

Immediate: ES drops 0.8-1.2% to 6,790-6,820

Day 1: Volatility, chop between 6,780-6,850

Week 1-2: Dip-buying brings it back to 6,870-6,900

Month 1: Grind back to 6,950-7,000 (+1.3%)

Sector Rotation:

Small caps (Russell 2000) -1.5-2%

Tech holds up better (mega-caps)

Defensives (utilities, staples) outperform

Trade Setup:

DO NOT chase before Fed (risk of -1.2% drop)

Buy: Dip to 6,750-6,800 (mid-channel support)

Target: 6,900-6,950 (+2-3% from dip entry)

Stop: 6,720 (-1%)

Risk/Reward: 1:2

SCENARIO C: No Cut OR Very Hawkish (10% Probability) - BEARISH

What Happens:

Fed HOLDS at 3.75-4% range (SHOCK) ❌

OR cuts but says "this is the last one for 6+ months" ❌

Powell cites inflation persistence, tariff risks ❌

Market has 90% priced in for cut = PANIC

Market Reaction:

Immediate: ES flash crashes 2-3% to 6,650-6,750

Day 1: Volatility, VIX spikes to 25-30

Week 1-2: Bounce attempt to 6,750-6,800 fails

Month 1: Retest 6,600, then recovery to 6,800-6,850

Sector Carnage:

Small caps (Russell 2000) -3-4%

Tech -2-3%

Everything bleeds

Trade Setup:

Exit ALL longs immediately on no-cut announcement

Wait for VIX to spike above 25

Buy: Capitulation at 6,600-6,650 (lower channel)

Target: Recovery to 6,850-6,900 (+3-4%)

Risk/Reward: 1:3 (but high stress)

🎯 THE TRADE SETUP - Professional Execution Plan

🟢 PRIMARY LONG SETUP: BUY ES1!

Entry Strategy (Scale In):

Option A: Conservative (Wait for Fed)

50% at 6,750-6,780 (IF hawkish cut dips)

50% at 6,720-6,750 (IF deeper dip)

Best for: Risk-averse traders

Option B: Tactical (Enter Now)

40% at 6,860-6,870 (current - small position)

30% at 6,820-6,840 (IF pre-Fed dip)

30% at 6,750-6,780 (IF post-Fed dip)

Best for: Experienced traders comfortable with volatility

Stop Loss: 6,620 (HARD STOP)

Below 6,620 = channel break on daily close

Below this = technical structure invalidated

Max loss from 6,862 entry: -3.5%

Take Profit Targets:

TP1: 6,950-7,000 (Probability: 70%)

Initial breakout above ATH

Psychological 7,000 level

Action: Take 40% profit, move stop to 6,850

Gain: +1.3-2.0% | Risk/Reward: 1:2

TP2: 7,050-7,100 (Probability: 50%)

Momentum continuation

Channel projection

Action: Take 30% profit, trail stop to 6,920

Gain: +2.7-3.5% | Risk/Reward: 1:3

TP3: 7,150-7,200 (Probability: 30%)

Full breakout extension

TradingView puts it, with a potential breakout in S&P 500 futures above the 6,900 area

Action: Take 20% profit, let 10% ride

Gain: +4.2-4.9% | Risk/Reward: 1:4

Entry Confirmation Checklist:

Before entering, CHECK:

✅ Price holding above 6,850 (bull/bear line)

✅ Volume spike on bounce (80K+ contracts on 15min)

✅ RSI crosses above 60 (momentum shift)

✅ VIX drops below 16 (fear subsiding)

✅ Fed announces 25bps cut (as expected)

✅ Powell's tone is dovish or neutral (not hawkish)

WAIT FOR 4/6 BEFORE FULL POSITION

Fed Day Volatility Protocol:

December 10, 2PM ET - Fed Announcement:

1:45 PM: Tighten stops to 6,830 (before announcement)

2:00 PM: Fed statement released - READ IMMEDIATELY

2:00-2:05 PM: Algorithmic reaction (ignore, volatile)

2:05-2:30 PM: Human digestion of statement

2:30 PM: Powell press conference begins - WATCH LIVE

2:30-3:15 PM: Powell Q&A determines direction

3:15-4:00 PM: Final positioning for overnight

IF DOVISH: Add to position on dip to 6,900

IF HAWKISH: Cut 50%, trail rest tight at 6,820

Weekly Monitoring:

Check EVERY DAY:

Fed speakers: Any 2026 guidance changes

Economic data: Jobs (Dec 16), CPI (Dec 18)

Technical levels: Is channel intact?

VIX: Spikes above 20 = warning

Volume: Declining = weak trend

Emergency Exit Conditions:

❌ Daily close below 6,620 = EXIT ALL (channel break)

❌ VIX spikes above 25 = EXIT 50%, tight stop on rest

❌ Fed announces NO cut (10% scenario) = EXIT ALL immediately

❌ Powell says "this is the last cut for 2026" = EXIT 50%

❌ ES gaps down >1.5% overnight = reassess, likely exit

📊 Fundamental Analysis - Why This Matters

CATALYST #1: The Fed's Impossible Position

Federal Reserve policymakers are expected to cut interest rates at this week's meeting despite inflation remaining above their target amid concerns about a softening labor market.

This is the classic Fed dual mandate dilemma:

Mandate #1: Maximum employment (FAILING - 1.1M layoffs in 2025)

Mandate #2: Stable prices (FAILING - inflation at 2.8% vs 2% target)

They can't fix both. So they have to choose.

David Mericle, chief U.S. economist at Goldman Sachs notes job growth remains too low to keep up with labor supply growth and a rising unemployment rate.

My take: The Fed will prioritize employment over inflation. That's dovish = bullish for stocks.

CATALYST #2: Corporate Earnings Remain Strong

Despite all the macro noise, corporate profits are SOLID:

S&P 500 earnings: +8.7% YoY

Tech sector leading: +12-15% earnings growth

AI spending driving margins higher

Q4 guidance mostly positive

Carvana (CVNA) stock rose 8% before the bell on Monday following news on Friday that it will join the S&P 500 as part of the index's quarterly rebalancing.

Translation: Fundamentals support higher prices, Fed just needs to cooperate.

CATALYST #3: Seasonal Tailwinds

Could spark a "year-end melt-up", as TradingView puts it, with a potential breakout in S&P 500 futures above the 6,900 area.

December-January has positive seasonality:

Holiday spending strong

Tax-loss selling done (Nov-early Dec)

January effect (fresh capital inflows)

Pension/401k rebalancing (buy equities)

Historically, S&P 500 averages +1.3% in December and +1.1% in January.

CATALYST #4: Institutional Positioning

Bloomberg's interviews with 39 investment managers show that most are still planning for a risk-on 2026, citing expectations of continued AI-driven productivity and earnings growth.

But here's the key: Asset managers such as EFG Asset Management and BNP Paribas Asset Management caution that with 2025 already a strong year, they are reluctant to increase equity exposure into thin year-end liquidity, preferring instead to wait for better entry points in early 2026.

Translation: Institutions are WAITING to buy. Any Fed-induced dip to 6,750-6,800 will be AGGRESSIVELY bought.

⚠️ Risk Factors - The Bear Case

RISK #1: Hawkish Powell Tanks Market

Feroli noted that the firm is anticipating at least two dissents in favor of no rate cut as well as one in favor of a larger rate cut.

If Powell leans hawkish to appease the dissenting hawks, market could drop 1-2%.

RISK #2: Tariff-Induced Inflation

Minutes mentioned Trump's tariff policies in forecasts they provided in early September, projecting higher inflation and unemployment, slower growth and a lower federal funds ratel.

If inflation accelerates in 2026 due to tariffs, Fed might have to HIKE again = very bearish.

RISK #3: Labor Market Deterioration

Employers cut more than 1.1 million jobs through November, the most since 2020 and a 54% increase from the same period a year ago.

If this accelerates, could trigger recession fears.

RISK #4: Technical Breakdown

Break below 6,620 = channel invalidated → target 6,500-6,550 (-4.5-5.2%)

🔥 The Bottom Line

Here's what I KNOW on December 8, 2025:

✅ 81% probability of 25bps cut Wednesday

✅ S&P 500 less than 1% from ATH

✅ Your ascending channel is PERFECT technical structure

✅ 39 investment managers planning risk-on 2026

✅ Corporate earnings strong (+8.7% YoY)

✅ Seasonal tailwinds (December +1.3% avg)

✅ Support at 6,750-6,800 = institutional buy zone

Here's what I DON'T know:

Will Powell be dovish or hawkish?

How many 2026 cuts will dot plot show?

Will Q&A reveal recession concerns?

But here's what the MATH says:

Risk: 6,862 → 6,620 = -3.5% (if channel breaks)

Reward: 6,862 → 7,050 = +2.7% (base case)

Extended: 6,862 → 7,150 = +4.2% (bull case)

Risk/Reward: 1:2.5 minimum

The Play:

Small position NOW at 6,860-6,870 (20-30% of intended size)

IF hawkish dip to 6,750-6,800 → ADD 50-70%

IF dovish → ADD on breakout above 6,910

Stop at 6,620 (non-negotiable)

Target 7,050, then 7,150

This is a PROBABILITY game. 60% dovish, 30% hawkish, 10% shock. Position accordingly.

📍 Follow officialjackofalltrades for institutional-grade technical analysis, professional risk management, and trades backed by data.

Drop a 📊 if you're trading the Fed decision.

Drop a 🎯 if this helped your ES1! analysis.

Drop a 💰 if you're ready for 7,000+ SPX.

German Industrial Production Surges, but the Euro Remains UnderToday's Industrial Production s.a. (MoM) data for October surprised to the upside, showing a strong increase of 1.8%, compared to expectations of -0.4% and a previous reading of 1.1%. This marks one of the strongest monthly performances of the year, indicating renewed stabilization in Europe's largest economy.

The indicator, released by the Statistisches Bundesamt Deutschland, is a key measure of the health of the manufacturing and mining sectors-core drivers of the German economy. Typically, higher industrial production is considered positive for the euro, signaling better growth prospects within the Eurozone.

Market Reaction - A Brief Spike Followed by Reversal

Immediately after the release, the euro jumped approximately 20 pips against the US dollar. However, the move was short-lived. During the European morning session, the USD regained all losses and strengthened further, pushing EUR/USD back toward 1.1650, with continued bearish momentum on the single currency.

This price action suggests that investors remain unconvinced that a single positive data point is enough to change the broader negative outlook for the Eurozone.

Geopolitical Pressure and Investor Sentiment

Market sentiment today was influenced not only by economic indicators but also by political commentary. Recent criticism of the European Union by Elon Musk and Donald Trump-including claims that the EU should "return to nation-states"-has added to investor caution regarding European assets.

Although such remarks do not directly affect short-term indicators, they contribute to a broader environment of skepticism toward the Eurozone's long-term stability.

World-Signals Outlook for EURUSD

According to World-Signals, the euro is likely to remain under pressure in the coming days. Expectations of a Federal Reserve interest rate cut toward the end of the year are currently viewed by markets as a supportive factor for the US dollar, signaling continued resilience in the American economy.

Given this backdrop, a move in EURUSD toward 1.1700 appears unlikely in the near term. Instead, USD strength is expected to dominate, with potential for the pair to test lower levels if negative sentiment toward the Eurozone persists.

BTC Range Play: ISPD Cluster Holds, Eyes on FOMCMarket Overview

__________________________________________________________________________________

Bitcoin is consolidating just above a tightly packed multi-timeframe demand cluster, with price boxed between well-defined supports and the 92k–92.5k ceiling as the market waits for the FOMC catalyst.

Momentum: Neutral with a slight bullish tilt while 89,100–89,400 holds; sellers continue to defend 92,000–92,500.

Key levels:

- Resistances (HTF): 91,000–91,400; 92,000–92,500; 99,000–100,000

- Supports (HTF): 89,100–89,400 (multi‑TF cluster); 87,800–88,200 (pivot low); 86,000

Volumes: Moderate on intraday and HTF; no sustained extremes.

Multi-timeframe signals: 1D/12H neutral; 6H/4H/2H lean neutral‑buy at the ISPD floors; LTFs remain choppy under 91k.

Harvest zones: 89,400 (Cluster A) / 89,100–89,300 (Cluster B) — ideal dip‑buy zones for inverse pyramiding with confirmation.

Risk On / Risk Off Indicator context: Sell bias (risk‑off) dominates; it contradicts the mild buy tilt at support and argues for patience into FOMC.

Trading Playbook

__________________________________________________________________________________

The dominant structure is a range with demand control at 89.1k–89.4k and supply at 91k–92.5k; adopt a reactive stance, buying confirmed reversals at the floor and fading clean rejections at HTF resistance.

Global bias: Neutral‑buy above 89,100–89,400; invalidation on a sustained break below 87,800.

Opportunities:

- Buy the dip: 2H+ bullish reversal at 89,100–89,400; partial size, add only on confirmation.

- Breakout buy: Close and hold above 92,500 opens 95k–100k; enter on retest that holds.

- Tactical sell: Fade rejection at 91,000–91,400 (or 92,000–92,500) only with bearish candle + weak volume.

Risk zones / invalidations: A daily/12H close below 87,800 would invalidate the neutral‑buy and expose 86,000; failure to follow through within 48–72h after entry also invalidates.

Macro catalysts (Twitter, Perplexity, news): FOMC with a widely expected 25 bps cut; JOLTS/CPI and Powell’s tone to steer liquidity; gold firm and USD/yields steady keep risk sensitivity elevated.

Harvest Plan (Inverse Pyramid):

- Palier 1 (12.5%): 89,400 (Cluster A) + reversal ≥2H → entry

- Palier 2 (+12.5%): 85,800–84,000 (-4/-6% below Palier 1) → reinforcement

- TP: 50% at +12–18% from PMP → recycle cash

- Runner: hold if break & hold first R HTF (91,400)

- Invalidation: < HTF Pivot Low (87,800) or 96h no momentum

- Hedge (1x): Short first R HTF on rejection (91,400) + bearish trend → neutralize below R

Multi-Timeframe Insights

__________________________________________________________________________________

Across TFs, price is coiling above a dense demand cluster while capped by layered supply into 92k–92.5k.

1D/12H: Sideways/neutral under 92k–92.5k; structure constructive above 87,800 with a clean pivot low; a decisive close above 92,500 is needed to unlock 95k–100k.

6H/4H/2H: Compression above 89,100–89,400 ISPD floors; repeated defenses signal high‑quality demand, but upside needs volume through 91,000–91,400 to avoid another lower high.

1H/30m/15m: Noisy mean‑reversion inside 89,250–91,000; intraday reversals work best when aligned with ≥2H signals. Confluence at the ISPD floors is the edge; macro risk is the main divergence.

Macro & On-Chain Drivers

__________________________________________________________________________________

Macro risk dominates into the FOMC while the external risk regime tilts risk‑off; that keeps Bitcoin’s range intact until a decisive post‑Fed move.

Macro events: Markets largely price a 25 bps cut; Powell’s guidance on path/duration is key. CPI/JOLTS add event risk; gold is firm and USD/yields steady, keeping risk assets sensitive.

External Macro Analysis: Risk On / Risk Off Indicator = sell regime with late‑cycle tone; speculative appetite and credit show stress while semis/small caps are conflicted. This supports a cautious technical bias until confluence improves.

Bitcoin analysis: Bounce from 86–87k reclaimed 90k; 87,800–88,200 is the HTF pivot low; 91k–92.5k caps. Structural resumption needs sustained strength toward 99k–100k. ETF daily inflow positive, but 7‑day average muted.

On-chain data: Demand modest; capital momentum slightly positive; 96–106k quantile remains pivotal for trend resumption; holding the ISPD cluster stabilizes, a breakdown opens an air pocket.

Expected impact: Risk‑off macro tempers upside until post‑FOMC; a supportive Powell could unlock a push through 92.5k, while a hawkish surprise risks losing the 89k cluster.

Key Takeaways

__________________________________________________________________________________

BTC is range‑bound into FOMC, with demand clustered at 89.1k–89.4k and supply stacked at 91k–92.5k.

The overall trend is neutral with a mild buy bias above the ISPD floors. The most relevant setup is buying a confirmed 2H+ reversal at 89.1k–89.4k, then adding only as 91k–91.4k breaks on volume. A risk‑off macro regime into FOMC argues for patience and hard invalidations. Stay nimble and let the post‑Fed move define the next leg; harvest volatility, don’t chase it.

EUR/USD Is Walking Into a Trap: Liquidity Sweep is coming!Price Action & Structure

The current structure shows a corrective rally unfolding within an ascending channel (green dashed lines).

Price action is printing higher highs without fresh momentum, a typical sign of “distribution during a pullback.”

The market is now trading in the upper half of the channel, approaching a daily premium zone just below 1.1700–1.1750.

Daily RSI sits around 60–65, which aligns with an extended pullback, not the beginning of a true bullish trend.

COT Analysis

EUR Futures (CME)

Large speculators are increasing shorts more aggressively than longs → bearish reading on the euro.

Commercials

Commercial traders are adding longs while reducing shorts.

→ This is classic hedging behavior during extended bullish corrections.

USD Index COT

Non-Commercial:

Positioning shows speculators are covering USD longs, but not turning bullish on the euro.

This suggests a temporary squeeze, not a structural trend reversal.

Retail Sentiment

70% SHORT EUR/USD

30% LONG

Retail traders are heavily short and consistently squeezed during upside moves.

This is a classic setup for a fake bullish rally into premium zones, after which larger players typically reverse price.

EUR/USD Seasonality (December)

December is statistically bullish, with average performance between +0.8% and +1.4%.

Seasonal curves show a rise into mid/late December, followed by:

→ a pullback near month-end

→ a bearish setup after January 3rd (typical early-year USD strength)

Thus, the current rally aligns perfectly with seasonality:

December rally → distribution → January drop.

Conclusion

EUR/USD is completing a structural bullish pullback, not forming a new bullish trend.

The move toward 1.1700–1.1750 looks like:

✔️ a liquidity grab

✔️ seasonal pump

✔️ exhaustion before reversal

Bank of Japan Losing Credibility. USDJPY eyes breakout. Continued or large scale QE, capped yields and reluctance to normalise (or being forced back in to easing during a downturn) would anchor Japanese yields far below peers encouraging capital outflows and undermining confidence in the currency.

A shrinking and ageing population chronic fiscal deficits very high public debt and history of trade deficits in recent years represent structural headwinds that can justify a weaker Yen if investors start to question long-run debt sustainability.

With a wide and persistent rate gap, leveraged global players can keep borrowing Yen to buy higher yield assets abroad.

If markets begin to doubt the BOJ's ability to manage the government bond market without either monetisation or financial repression, investors may demand a steep currency discount rather than high nominal yields, instead of typical "higher rates, Stronger FX" reaction.

Global risk: If the dollar regains or maintains "only game in town" safe-haven status in a world of repeated shocks - while the Yen loses it's traditional safe haven status because of Japan's Macro position - USDJPY can behave more like a one way-risk trade than a mean reverting pair.

Gold Eyes 4,207 Rebound as USD Softens & Venezuela Tensions RiseHey Traders, in today’s trading session we are monitoring XAUUSD for a potential buying opportunity around the 4,207 zone. Gold continues to trade within a broader uptrend, and the current pullback is bringing price into a key support–resistance confluence aligned with the ascending trend structure.

Fundamentals:

The US Dollar remains under pressure, with markets increasingly leaning toward a dovish shift from the Federal Reserve, reinforcing gold’s classic negative correlation with the USD. A softer Dollar environment typically boosts demand for metals, and this week’s macro flow continues to point in that direction.

At the same time, geopolitical tensions between the U.S. and Venezuela are escalating, increasing global uncertainty and driving markets toward safe-haven assets. Gold is already reflecting this risk premium, and any further escalation could accelerate flows into XAU.

Next Step:

We’re watching price reaction closely around 4,207 for a potential continuation of the broader bullish structure.

Trade safe,

Joe.

XAUUSD | Broke Symmetrical Triangle pattern --> Bullish BiasMacro:

- Gold prices advanced this week as renewed demand for hedges and expectations for Fed rate cuts offset still‑elevated US yields. Persistent geopolitical risks and concerns about the global growth outlook continued to underpin safe‑haven interest in gold.

- This week’s gains were supported by softer US data, including weaker private payroll indicators, which strengthened expectations that the Fed will deliver a rate cut at its upcoming meeting. These developments have weighed on the dollar at times, helping gold prices hold near recent highs, even as benchmark US Treasury yields hover around 4.10% rather than falling decisively. Structural drivers also remain in place, with investors and central banks maintaining exposure to gold as a hedge against policy missteps and inflation surprises.

- Gold prices may stay supported if upcoming US inflation data and Fed communication confirm a path toward easier policy and a softer dollar. Any downside surprise in inflation or a more dovish‑than‑expected Fed stance would likely reinforce that narrative. At the same time, a hawkish shift or stronger‑than‑expected data could prompt a temporary pullback. Gold may also react sharply to any escalation in geopolitical tensions or negative growth surprises that tighten financial conditions, as both factors tend to boost safe-haven demand and influence real-yield expectations.

Technical:

- XAUUSD broke the Symmetrical Triangle pattern and rose toward the resistance at 4245 before consolidating within a tight range of 4200-4245. The price is above EMA21, indicating an upward momentum remains.

- If XAUUSD breaches above 4245, the price may surge and retest the ATH area at around 4365.

- Conversely, closing below 4200 may prompt a further correction toward EMA21 area.

Analysis by: Dat Tong, Senior Financial Markets Strategist at Exness

DXY at a KEY “Decision Point” on the Supply ZoneAfter an extended bullish duration, the DXY is now challenging a technically critical “Supply Zone” (100.150 – 100.600). Further away from key levels, both pump and dump up and down, momentum oscillators on all time frames give us mixed signals of exhaustion from buyers and that we are near to making a big decision in the direction of our market.

A comprehensive technical look that includes the broader structures and multi-month macroeconomic supply-demand analysis.

TECHNICAL OUTLOOK

Critical Resistance (Purple Zone): We are currently sitting right inside that 100.150 – 100.600 corridor. This is a level we know well—it’s packed with strong selling pressure and smart money order blocks. Think of this zone as a huge mental hurdle for the bulls; trying to go "Long" here without seeing a clean, high-volume breakout is just asking for trouble with a bad risk/reward setup.

Trend Structure: That ascending yellow trendline connecting the lows since September has been holding the price up so far. But look closer—the space between the price and this trend support is squeezing tight (Compression). This usually tells us one thing: volatility is kicking in and a big move is brewing.

Negative Divergence (RSI) : Here’s the warning sign. While the daily chart is trying to make new highs or just hanging on at resistance, the RSI is losing steam and making lower highs. This "Bearish Divergence" is a classic signal that the trend is running on fumes.

Momentum (MACD) : The MACD histogram is fading out, which confirms the bulls are getting tired. It hints that profit-taking—and the sellers taking over—is likely just around the corner.

MACROECONOMIC AND FUNDAMENTAL DYNAMICS