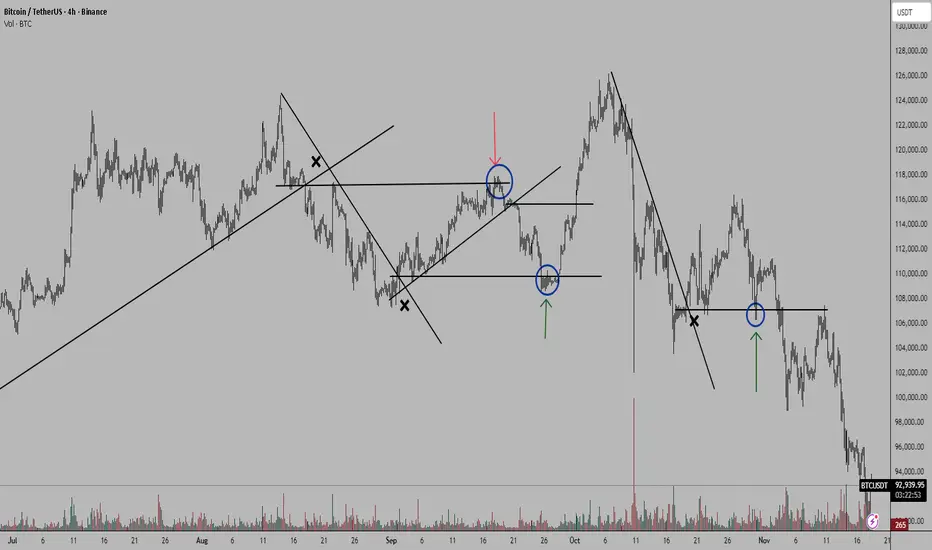

Why Liquidity Is the Real King of Crypto ?🧨 The $1.1 Trillion Lesson: Why Liquidity Is the Real King of Crypto 🧨

A deep dive into how macro headlines and liquidity shifts shape every chart you trade.

Hello Traders 🐺

In this idea, I want to take you on a journey through one of the most brutal and eye-opening moments in crypto history — a $1.1 trillion wipeout in just 42 days.

But this isn’t just about the numbers. It’s about the lesson behind the crash.

Because if you truly understand what caused this — you’ll unlock a superpower most traders never develop:

Reading liquidity like a pro.

So stick with me till the end — because this is more than a chart.

It’s a masterclass in macro awareness.

And it all comes down to one brutal truth:

📈 The Setup: Euphoria at $4.3 Trillion

It was October 2025.

Crypto was booming.

Altcoins were flying.

Influencers were screaming “new ATHs.”

And the total market cap hit a jaw-dropping $4.3 trillion.

Everyone thought the bull run had no brakes.

But then came the headline that changed everything...

🗞️ The Shock: “TRUMP ANNOUNCES 100% TARIFF ON CHINA”

This wasn’t just politics.

It was a liquidity shock.

Global markets flinched.

Risk assets trembled.

And crypto?

It got hit harder than anyone expected.

Why?

Because tariffs = tension = uncertainty = capital flight.

And when capital flees, liquidity dries up.

And when liquidity dries up…

💥 The Fallout: Largest Liquidation Event in Crypto History

Billions wiped in hours.

Leverage nuked.

Altcoins collapsed.

And the total market cap began its brutal descent — erasing over $1.1 trillion in just 42 days.

Let that sink in.

$1.1 trillion.

Gone.

Not because of a chart pattern.

Not because of RSI.

Not because of your favorite altcoin’s roadmap.

But because of liquidity.

📢 The Bounce: “America Will Be #1 in Crypto”

A bold statement from Trump gave the market a short-lived bounce.

But sentiment was already broken.

And without real liquidity support, the bounce was just a trap.

A classic dead-cat.

Because words don’t move markets — money does.

📉 The Aftermath: Crypto Erases $1.1T

From peak to trough, the market bled.

And here’s the lesson:

It wasn’t technicals.

It wasn’t fundamentals.

It was macro.

It was policy.

It was liquidity.

💡 What Can We Learn From This?

✅ Macro headlines move markets faster than any chart pattern

✅ Political shocks = volatility spikes

✅ Liquidity is king — and when it dries up, even the strongest coins fall

✅ Your edge as a trader is not just in TA — it’s in understanding the invisible forces behind price

🎯 Why This Post Matters

This isn’t just a recap.

It’s a wake-up call.

Because most traders are blind to macro.

They chase candles.

They follow influencers.

But they ignore the one thing that truly drives the market:

Liquidity.

If you understand this — you stop reacting.

You start anticipating.

You stop getting liquidated.

You start positioning early.

That’s why this post matters.

Because it teaches you the $1.1 trillion lesson —

A lesson paid for by millions of traders who didn’t see it coming.

🐺 Final Words

If you found this helpful, follow for more deep dives.

Because the next trillion-dollar move might already be loading…

And when it hits, you’ll want to be on the right side of liquidity.

🐺 Discipline is rarely enjoyable, but almost always profitable 🐺

🐺 KIU_COIN 🐺

Chart Patterns

The Support Zone That Refused To Be IgnoredSome chart zones whisper. This one practically waved its arms.

Price slid right into a hefty support area on the higher timeframe… and suddenly started behaving like it had forgotten how to move lower. Classic clue.

Zoom in, and the daily chart shows price squeezing itself into a falling wedge — the market’s equivalent of someone pacing in a hallway, unsure whether to sit down or sprint. Sellers kept trying to push prices lower, but each attempt had less conviction than the last.

When you stack those two pieces together — a big support zone from the monthly chart and a daily pattern running out of room — things start to get interesting. Not predictive, just… interesting.

A breakout above the wedge (around 0.0065030) would basically say, “Alright, I’m done compressing.”

A stop tucked below the lower support range (roughly 0.0063330) keeps the scenario clean.

And a structural projection toward 0.0067695 gives the idea a tidy endpoint if momentum decides to stretch its legs.

Of course, leverage cuts both ways, and traders working with the standard or micro contracts often choose size based on how much room they want between entry and invalidation. When traders choose between the standard and micro versions of this market, it usually comes down to scale. The bigger contract represents 12,500,000 units of the underlying with a $6.25 tick, while the micro mirrors the behavior at 1,250,000 units with a $1.25 tick. Estimated margins also differ — roughly $2,800 for the larger contract and about $280 for the micro. Same chart logic, just two very different footprints on the account.

The real takeaway? When a major zone teams up with a compression pattern, it’s usually worth paying attention. Maybe it leads to a beautiful breakout. Maybe it fizzles. But structurally, this is one of those “save the screenshot” moments.

And whatever the outcome, risk management keeps the whole thing sensible — size smartly, define failure points, and let the chart prove itself instead of assuming it will.

Want More Depth?

If you’d like to go deeper into the building blocks of trading, check out our From Mystery to Mastery trilogy, three cornerstone articles that complement this one:

🔗 From Mystery to Mastery: Trading Essentials

🔗 From Mystery to Mastery: Futures Explained

🔗 From Mystery to Mastery: Options Explained

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Capitalize on fear in reversalsRichard W. Schabacker and Bob Volman are two investors separated by time and methodology. Yet they share one essential thing: both understand the market as a profoundly psychological phenomenon. Influenced by them, I try to trade with maximum simplicity and overwhelming logic.

Today I’m going to share with you one of the most ingenious methods I’ve ever discovered for exploiting high-probability reversals.

Psychological factor: Loss aversion

The pain of a loss is far more intense than the pleasure of an equivalent gain. According to Prospect Theory, developed by Daniel Kahneman and Amos Tversky in 1979, losses psychologically weigh roughly twice as much (or more) as equivalent gains. This causes people to become risk-averse when they are in profit but much more willing to take risks to avoid a certain loss.

In Figure 1 you can see a graphic representation of that pain and loss. Using trendlines, we observe sellers suddenly trapped by aggressive buying pressure.

Figure 1

BTCUSDT (30-minute)

Many of these sellers were undoubtedly stopped out quickly, but I assure you the majority — slaves to the cognitive bias known as loss aversion — will hold their positions hoping for a recovery.

The deeper the losses go, the greater their attachment to the position becomes, along with their desperation. Under that pressure, most of those unfortunate bears will only wish for one thing: a chance to get out of the market at breakeven.

In Figure 2, observe what happens when price returns to the zone where those sellers were originally trapped.

Figure 2

BTCUSDT (30-minute)

In the bullish signals of Figure 2 we can see the confluence of several factors:

Trapped sellers closing their short positions the moment price reaches breakeven, turning into buying pressure (and living to fight another day).

Profitable shorts who were riding the previous downtrend taking profits or closing positions after a deep pullback caused by buying strength, now near potential support zones.

New buyers entering because they see support near the low created by the previous bearish leg (especially if the downtrend has reversed into a range or accumulation phase).

In Figure 3 you can see two examples of groups of buyers who got trapped while expecting continuation of the uptrend. After two deep corrections, most of them only wanted to return to their entry price to escape unscathed.

As soon as price returns to that entry zone, those long positions turn into selling pressure.

Figure 3

BTCUSDT (30-minute)

Figure 4 shows more of the same: desperate bulls and a lot of pain.

Figure 4

USOIL (Daily)

Additional ideas

-Remember: the deeper the pullback, the greater the suffering of the trapped traders. We need them to panic so that, the moment price reaches their entry zone, they close without thinking twice — thereby validating and reinforcing our own positions. (Fibonacci retracements of 0.50, 0.618 and 0.786 are extremely useful for measuring the optimal depth of a pullback)

-Reversal patterns are also essential for our reversal entries because they significantly increase our win rate.

-We must be especially careful when trading against moves with very strong momentum. (characterized by near-vertical price action and disproportionately large candles)

Although I will soon go deeper into the management of this method, I recommend reading the article What nobody ever taught you about risk management ( El Especulador magazine, issue 01). You can also read the chapter titled The Probability Principle in Bob Volman’s book Forex Price Action Scalping .

If you enjoyed this article and want me to expand further on this and other topics, stay close.

We won’t be the ones getting trapped.

How to build a Healthy Trading MindsetMany traders underestimate how much psychology shapes their results. This guide outlines the foundations of a strong trading mindset that supports consistent and disciplined decision-making.

1. Understand That Emotional Discipline Is a Skill

Trading naturally triggers emotions such as fear, frustration, greed, and impatience. These reactions are not weaknesses; they are human. What separates consistent traders from inconsistent ones is their ability to recognize emotions without acting on them.

A resilient mindset comes from training, not talent.

2. Create Distance Between Yourself and Your Trades

Do not tie your self-worth to the outcome of a single position. A loss does not mean you failed, and a win does not mean you are skilled. When traders begin to link identity to results, they make impulsive decisions.

Use phrases like “this trade” instead of “my trade” to remove ownership bias.

3. Focus on Process, Not Profit

Most traders sabotage themselves by obsessing over the end result. The market does not reward effort; it rewards alignment with probability.

Instead of thinking “How much can I make?”, think “Did I execute according to my plan?”

Your trading plan should define your entries, exits, risk, and market conditions. Follow it even when it feels uncomfortable.

4. Accept Uncertainty as Part of the Game

No setup is guaranteed. Every trade, no matter how perfect, carries uncertainty. Accepting this prevents you from forcing control where none exists.

When you fully accept uncertainty, you no longer fear it.

5. Build Consistency Through Routine

A stable routine reduces mental noise. Examples include:

• Reviewing your plan before each session

• Limiting how many markets you monitor

• Taking breaks after high-stress situations

• Logging your trades with honest notes

When your routine is consistent, your decisions become consistent.

6. Use Losses as Data, Not Drama

A loss is not a personal attack from the market. It is information.

Ask: “What does this loss teach me about my system or my mindset?”

If you can extract value from losses, they become opportunities instead of obstacles.

7. Master Patience

Most trading errors come from acting too soon, not too late. Patience means waiting for your setup without deviation.

If you need to be in a trade at all times, it is no longer trading; it is compulsion.

8. Protect Your Mental Capital

Mental capital is as important as financial capital. Overtrading, revenge trading, and excessive chart time drain your cognitive energy.

Stop trading when you notice fatigue, frustration, or impulsiveness. A clear mind is an advantage.

9. Develop Long-Term Thinking

Think in terms of series, not individual outcomes. A single win or loss means little. What matters is the overall direction of your equity curve.

Professional traders think in months and years. Amateurs think in minutes.

Conclusion

A powerful trading mindset is built through consistency, self-awareness, and emotional control. By focusing on process and discipline rather than short-term results, you create a stable internal environment that supports longevity in the markets.

Crypto Cycle: The Arrogance and The Irony — A Must ReadThe Cycle That Changed Everything

This cycle — which really started in October 2023 — broke every pattern from previous crypto bull runs.

Crypto was created as a rebellion:

Freedom from banks.

An anti-system technology.

Privacy.

Self-sovereignty.

A way for normal people to create wealth without permission.

And yet… somehow the exact people crypto was trying to escape have taken control of it.

Retail investors used to love the idea of owning their finances. No more banks telling them what to do. No more gatekeepers.

Until they arrived.

1 — The Arrogance

The rich run the world — that’s nothing new.

But crypto annoyed them. A lot.

Because crypto allowed ordinary people to do what Wall Street hates most:

Make money without giving the rich a cut.

So what did institutions do?

Simple:

“If you can’t kill it… own it.”

They stopped fighting crypto, took over the market, bought the exchanges, injected billions, partnered with the stablecoin printers, and unleashed industrial-scale manipulation.

The old days of making x10 or x100 on leverage?

Gone.

Retail got liquidated again… and again… and again.

Bitcoin pumped 3 times by billionaires (just look at the three green boxes on the chart).

Retail got excited — then destroyed.

Rinse and repeat.

Eventually, retail gave up.

They moved into gold, silver, or even plain USD — just to stop losing money.

Meanwhile institutions kept pumping Bitcoin and Ethereum artificially, hoping to lure back fresh meat…

but nobody came.

2 — The Irony

Then came October 11, 2025 — the day the curtain fell.

In a dry, illiquid market, Binance did their usual liquidation-hunting game, backed by newly-printed billions from Tether:

2 billion minted one day, 2 billion the next.

They pushed Bitcoin to $126,000.

Then the crash hit.

They chased longs so hard that, in a market with no liquidity, the entire altcoin market collapsed.

Some coins literally went to zero.

Binance had to halt trading.

The liquidation chain couldn’t be stopped.

Some market makers lost everything.

And now they’re furious.

Binance got exposed.

The pump-and-dump machine is broken.

And if they continue, they risk criminal investigations and lawsuits from every direction.

Suddenly BlackRock, Saylor, and friends had a problem:

Their favorite manipulation partner was knocked out.

And that’s when reality hit:

Institutions had pushed Bitcoin so high — without retail — that they found themselves holding billions in assets…

…with nobody left to buy their bags.

Old-time Bitcoin holders realized BTC was compromised and began to sell.

Bitcoin maxis rekt the institutions.

The billionaires who bought at $120k got destroyed by the exact people they planned to destroy.

Karma doesn’t miss.

Even Eric Trump started selling — too late.

Bitcoin fell under $89k, and there were no buyers left.

3 — The Lesson

Institutions need to understand one thing:

Crypto is not for institutions.

The tech? Sure.

The coins? No.

Crypto without retail is like a vampire trying to drink its own blood.

Pointless and self-destructive.

And retail won’t return for “fractional Trump coin” or corporate-approved BTC.

Retail wants:

x10, x100, x1000.

That means one thing:

ALTSEASON.

If institutions want liquidity to exit, they must engineer an altseason and share some profits.

Because without retail, they’re stuck in their expensive echo chamber holding overpriced bags that nobody wants.

And if they do create an altseason?

Retail will dump on them harder than ever — watching TradingView and influencers, selling every rally right back into the institutions’ faces.

Wall Street, stick to Wall Street.

Leave crypto to the crypto degenerates.

It’s a wild jungle, and you were never prepared.

#CryptoCycle #BitcoinCrash #AltseasonWhen #CryptoHumor #MarketManipulation #InstitutionsRekt #BinanceDrama #RetailVsWhales #CryptoReality #KarmaInCrypto #CryptoStory #PattayaCryptoDegens

Equity Market Indices (S&P 500, Nasdaq, DAX, Nikkei)1. S&P 500 Index — The Global Benchmark

The Standard & Poor’s 500 Index, commonly known as the S&P 500, is one of the world’s most followed equity indices. It tracks 500 of the largest publicly listed companies in the United States. Unlike the Dow Jones Industrial Average, which uses price weighting, the S&P 500 uses free-float market capitalization weighting, making it a more accurate representation of the U.S. equity market.

Structure and Components

The index spans all major U.S. sectors, including technology, financials, healthcare, consumer discretionary, and energy. Mega-cap companies like Apple, Microsoft, Amazon, and Alphabet often dominate the index due to their large market capitalizations.

Economic Significance

The S&P 500 accounts for over 80% of U.S. total market value, making it a barometer for overall U.S. corporate health. Movements in the index reflect:

Corporate earnings trends

Investor sentiment

Monetary policy expectations

Global macroeconomic factors

Investment and Trading Use

Investors use the S&P 500 for:

Benchmarking fund performance

ETF and index fund investing (e.g., SPY, VOO)

Futures and options trading

Analysts often interpret a rising S&P 500 as a sign of economic expansion, while prolonged declines may indicate recession concerns.

2. Nasdaq Composite & Nasdaq-100 — Tech-Heavy Growth Indicators

The Nasdaq Composite is one of the most technology-heavy indices in the world, tracking over 3,000 stocks listed on the Nasdaq exchange. The more popular trading index, however, is the Nasdaq-100, which includes the top 100 non-financial companies on Nasdaq.

Technology Dominance

The Nasdaq is dominated by:

Technology

Internet services

Biotechnology

Semiconductor companies

Major names include Apple, Microsoft, Nvidia, Meta, and Tesla.

Characteristics and Sensitivity

Because it is tech-heavy, the Nasdaq tends to be:

More volatile than the S&P 500

Highly sensitive to interest rate changes

Influenced strongly by innovation trends, earnings expectations, and regulatory actions

Growth stocks, which dominate the Nasdaq, typically outperform during low-interest-rate environments when borrowing is cheaper and future earnings are more valuable.

Use for Traders

Traders often use the Nasdaq as a sentiment gauge for:

Tech sector strength

Risk appetite in markets

Momentum-driven trading strategies

Nasdaq futures (NQ) and ETFs like QQQ are among the most actively traded instruments globally.

3. DAX (Germany) — Europe’s Industrial Power Index

The DAX (Deutscher Aktienindex) is Germany’s leading stock index, representing 40 blue-chip companies listed on the Frankfurt Stock Exchange. Unlike other indices, the DAX is a performance index, meaning dividends are reinvested, resulting in slightly higher long-term returns.

Composition

The DAX includes major industrial, automotive, chemical, and financial giants such as:

Siemens

Volkswagen

Mercedes-Benz

Bayer

Allianz

SAP

Role in Europe

Germany is Europe’s largest economy, so the DAX essentially acts as a proxy for the health of the Eurozone economy. It reflects:

Manufacturing output

Export competitiveness

Global demand for automobiles and engineering

Euro currency movements

Key Drivers

The DAX is influenced by:

European Central Bank (ECB) policies

Eurozone inflation and GDP

Geopolitical relations with the U.S. & China

Energy prices (Europe is energy-dependent)

During periods of higher global industrial activity, the DAX typically performs strongly due to Germany’s export-led economy.

4. Nikkei 225 — Japan’s Economic Indicator

The Nikkei 225, Japan’s best-known stock index, tracks 225 top companies on the Tokyo Stock Exchange. Unlike most major indices, the Nikkei is price-weighted, similar to the Dow Jones, meaning higher-priced stocks have greater influence regardless of company size.

Sector Mix

Japan’s market includes a mix of:

Automotive companies (Toyota, Honda, Nissan)

Consumer electronics (Sony, Panasonic)

Industrial manufacturers (Fanuc, Hitachi)

Financial institutions

Economic Importance

The Nikkei reflects Japan’s:

Export competitiveness (especially to the U.S. and China)

Yen strength or weakness

Domestic consumption trends

Bank of Japan (BOJ) monetary policy

Japan's prolonged period of low interest rates and deflation has historically shaped the Nikkei’s long-term performance.

Yen Relationship

The Nikkei tends to rise when the Japanese yen weakens, because a weaker yen boosts export revenues. It often behaves inversely to USD/JPY currency movements.

5. How Traders Use These Indices

Market Sentiment Indicators

Each index provides insight into different segments:

S&P 500: overall U.S. economy

Nasdaq: tech and growth sentiment

DAX: European industrial strength

Nikkei: Asian economic trends

Sector Rotation

Investors analyze relative performance to gauge:

Growth vs. value cycles

Domestic vs. international capital flows

Risk-on vs. risk-off behavior

Hedging & Diversification

Indices are widely used for:

Portfolio diversification

Hedging through futures/options

ETF investing across regions

Correlation Behavior

S&P 500 and Nasdaq have high correlation

DAX moves closely with global manufacturing trends

Nikkei correlates strongly with currency markets

Understanding these correlations helps global traders manage risk and time their entries.

6. Global Impact of Index Movements

Because these are major world indices, movements can influence:

Commodity prices (oil, gold)

Currency valuations (USD, EUR, JPY)

Bond markets

Emerging market flows

For example:

A strong S&P 500 often attracts global capital into the U.S.

Weak DAX performance can signal European recession fears

A rising Nikkei can lift Asian equity sentiment

Conclusion

Equity market indices like the S&P 500, Nasdaq, DAX, and Nikkei 225 are more than just collections of stock prices. They are critical indicators of economic health, investor behavior, and global financial stability. Each index reflects the structure of its economy—U.S. technology leadership for Nasdaq, diversified large caps for the S&P 500, industrial might for the DAX, and export-driven growth for the Nikkei. Together, they form the backbone of global equity analysis and remain essential tools for traders, investors, and policymakers worldwide.

Gold & Safe-Haven Asset Trading1. Why Gold Is Considered a Safe-Haven Asset

Gold is perceived as a safe-haven for several reasons:

1.1 Intrinsic Value

Gold is a physical asset with limited supply. It cannot be printed like fiat currency, and mining output grows slowly over time. This scarcity gives gold long-term value stability.

1.2 Universal Acceptance

Gold is accepted globally as a store of value by governments, central banks, banks, institutions, and retail investors. It is one of the few assets that retain value regardless of the political or economic system in place.

1.3 Hedge Against Inflation & Currency Depreciation

When inflation rises or a currency weakens—especially the USD—gold prices tend to increase. This is because investors shift capital into assets that preserve purchasing power.

1.4 Geopolitical Crisis Shield

During wars, conflicts, sanctions, or major political uncertainty, gold attracts strong demand. Institutions rotate out of risk assets like equities and into safer stores of value.

1.5 Negative Real-Yield Environment

When real interest rates (interest rate minus inflation) fall or turn negative, the opportunity cost of holding non-yielding gold decreases, making it more attractive.

2. What Are Safe-Haven Assets?

Safe-haven assets are those that retain or increase value during times of market volatility, economic crisis, or geopolitical stress. The key safe-haven categories include:

Gold

US Dollar (USD)

US Treasury bonds

Japanese Yen (JPY)

Swiss Franc (CHF)

Silver and other precious metals

Sometimes: utilities, consumer staples, defensive stocks

Gold remains the most universal and liquid among them.

3. Key Drivers of Gold Prices

To trade gold effectively, traders must understand the main price drivers:

3.1 US Dollar Index (DXY)

Gold is priced in USD globally.

A stronger USD → gold becomes expensive for holders of other currencies → gold falls

A weaker USD → gold becomes cheaper globally → gold rises

This inverse relationship is one of the strongest correlations in global markets.

3.2 Interest Rates (Especially US Treasury Yields)

Gold does not pay interest. When yields rise, gold becomes less attractive.

Rising yields → bearish for gold

Falling yields → bullish for gold

Real yields matter more than nominal yields.

3.3 Inflation

Gold is a traditional inflation hedge.

Higher inflation → gold demand increases → gold prices rise

Low/deflation → gold weakens

3.4 Geopolitical & Financial Risks

Gold spikes during:

wars

banking system stress

sovereign debt crises

market meltdowns

oil price shocks

trade wars

currency crises

Gold thrives when uncertainty rises.

3.5 Central Bank Gold Purchases

Many central banks buy gold to diversify reserves away from the USD.

Large purchases by China, India, Russia, and emerging markets support gold prices.

3.6 ETF Flows

Gold-backed ETFs (like SPDR Gold Trust – GLD) influence prices through physical purchasing.

4. Gold Trading Instruments

4.1 Spot Gold (XAU/USD)

The most traded instrument in gold markets.

XAU/USD represents gold priced in U.S. dollars.

4.2 Gold Futures (COMEX)

Highly liquid and used by institutional investors and hedgers.

4.3 Gold ETFs (GLD, IAU)

Useful for passive investors or those who want gold exposure without physical storage.

4.4 Gold Mining Stocks

Companies like Barrick Gold, Newmont etc.

Mining stocks are leveraged plays on gold prices.

4.5 Physical Gold (Bars, Coins)

Used mostly for long-term wealth preservation.

5. Safe-Haven Flow Dynamics

Understanding how capital flows during crises is key.

5.1 Risk-Off Environment

When market fear rises:

Equities fall

Bond yields drop

USD and gold rise

Gold attracts capital as a non-correlated asset.

5.2 Risk-On Environment

When markets recover:

Equities rise

USD strengthens

Gold often consolidates or corrects

Safe-haven demand decreases.

6. Trading Strategies for Gold & Safe-Haven Assets

6.1 Trend Following Strategy

Since gold often moves in strong directional trends:

Use moving averages (50/200 EMA)

Buy when price is above key MAs and forming higher highs

Sell when price breaks below MAs with strong volume

6.2 Breakout Strategy

Gold reacts strongly to breakouts from:

price consolidation zones

triangle patterns

wedge patterns

horizontal ranges

A breakout with high volume can signal a strong move.

6.3 Mean Reversion (Contrarian) Strategy

Gold frequently retraces after sharp moves.

Indicators:

RSI (overbought/oversold)

Bollinger bands

Price divergence

Use cautiously during trending markets.

6.4 Macro-Based Trading

Use fundamental triggers:

Fed interest rate decisions

CPI inflation releases

NFP jobs report

Geopolitical events

Central bank speeches

These can cause rapid volatility in gold.

6.5 Safe-Haven Correlation Trading

You can trade gold relative to:

DXY movements

US 10-year yield changes

JPY or CHF moves

VIX index spikes

When volatility rises, gold usually rallies.

7. Gold in Portfolio Diversification

Gold is one of the best hedges against:

inflation

currency weakness

economic slowdowns

stock market crashes

Historically, gold has low correlation with equities, making it ideal for diversification.

Portfolio strategies:

5–10% gold allocation for stability

15–20% during high inflation periods

Use gold to hedge global macro risks

8. Risks in Gold Trading

Despite being a safe-haven, gold trading carries risks:

8.1 High Volatility

Gold can move sharply around:

CPI

NFP

Fed meetings

geopolitical headlines

8.2 Interest Rate Shocks

An unexpected spike in yields can cause large downside in gold.

8.3 USD Strength

A strong, sudden USD rally can drag gold lower.

8.4 False Breakouts

Gold sees many fake breakouts due to liquidity-driven algorithmic trading.

8.5 Over-leveraging

Leverage in futures or CFDs can magnify losses during volatile phases.

9. Long-Term Outlook for Gold

Over decades, gold generally trends upward due to:

global inflation

rising debt levels

currency debasement

central bank gold accumulation

geopolitical risks

The long-term picture remains bullish, but short-term volatility is normal.

Conclusion

Gold and other safe-haven assets play a critical role in global financial markets, serving as stabilizers during periods of uncertainty and volatility. Gold remains the most trusted safe-haven due to its intrinsic value, global acceptance, and strong historical performance during crises. Understanding the correlations between gold, interest rates, USD, inflation, and market sentiment enables traders to anticipate market movements and trade profitably. Whether using technical setups, macro analysis, or multi-asset safe-haven flows, gold trading offers opportunities for both short-term traders and long-term investors. However, managing risk, avoiding over-leverage, and monitoring global macro signals are essential for success in gold markets.

Crude Oil Market (WTI, Brent) & OPEC+ Decisions1. Understanding WTI and Brent Crude

WTI Crude Oil

West Texas Intermediate (WTI) is a high-quality, light, and sweet crude oil primarily sourced from fields in the United States, especially Texas. Its low sulfur content makes it easier to refine into gasoline and diesel, which are in high demand in the North American market. WTI is traded on the New York Mercantile Exchange (NYMEX) and considered a benchmark for U.S. crude prices.

Brent Crude Oil

Brent is sourced from oil fields in the North Sea, spanning the UK and Norway. It is slightly heavier than WTI but still considered a light, sweet crude. Brent is traded on the Intercontinental Exchange (ICE) and acts as the global benchmark for two-thirds of internationally traded crude oil.

Why Two Benchmarks?

The existence of both benchmarks reflects regional differences in production, shipping costs, refining requirements, and market access. Generally:

WTI represents U.S. supply-demand dynamics.

Brent reflects international conditions across Europe, Asia, and Africa.

The price spread between the two (WTI–Brent spread) often indicates logistical constraints, geopolitical tensions, or shifts in global demand.

2. Factors Influencing Crude Oil Prices

Crude oil markets are volatile due to the interplay of multiple economic, geopolitical, and market-driven factors.

a. Global Supply & Demand

Oil demand is affected by:

Economic growth rates

Industrial output

Transportation needs

Seasonal factors (winter heating demand, summer driving season)

Supply depends on:

Production levels in OPEC and non-OPEC countries

U.S. shale output

Production outages or upgrades

Infrastructure constraints

b. Geopolitical Events

Conflicts in the Middle East, sanctions on major producers like Iran, instability in Venezuela, and maritime disruptions (e.g., Strait of Hormuz tensions) significantly move oil prices.

c. Currency Movements

Oil is priced in U.S. dollars.

When the USD strengthens, oil becomes expensive for foreign buyers → demand decreases → prices fall.

When the USD weakens, oil prices tend to rise.

d. Inventories & Storage

Weekly U.S. crude inventory data, especially from the EIA (Energy Information Administration), provides insights into near-term supply-demand balances.

e. Energy Transition Policies

Shift toward renewable energy, environmental policies, and long-term decarbonization targets influence investment, production, and expectations of future oil use.

3. Role of OPEC and OPEC+

What is OPEC?

The Organization of the Petroleum Exporting Countries (OPEC) was founded in 1960 to coordinate and unify petroleum policies of major producing countries. Key members include Saudi Arabia, Iraq, Iran, Kuwait, and UAE.

OPEC+ Formation

In 2016, OPEC expanded to include major non-OPEC producers such as Russia, Mexico, Kazakhstan, and others, forming OPEC+.

This group controls around 40% of global oil production and 80% of known reserves, making their decisions highly influential.

4. OPEC+ Production Decisions

a. Production Cuts

When demand falls (e.g., during pandemics or recessions), OPEC+ often cuts production to support prices.

Cuts reduce global supply → tighter market → higher prices.

b. Production Increases

During times of strong demand, OPEC+ increases output to maintain market stability.

Higher supply → pressure on prices → prevents overheating of global inflation.

c. Voluntary vs. Mandated Cuts

Sometimes individual countries choose voluntary cuts to stabilize the market.

Saudi Arabia often leads with additional voluntary cuts beyond the group agreement.

5. How OPEC+ Decisions Influence WTI and Brent

Market Expectations

Before meetings, traders speculate on whether OPEC+ will:

Cut supply

Maintain quotas

Increase production

Even rumors can create dramatic price swings.

Outcomes of Meetings

A formal announcement of cuts usually triggers:

Brent prices increasing more sharply, as it is more globally sensitive

WTI moving upward, though influenced by U.S. shale reactions

On the contrary, increases in output often lead to a pullback in both benchmarks.

Long-term Impact

Persistent cuts support a long-term bullish trend.

Persistent increases (or cheating on quotas by some members) lead to bearishness.

6. U.S. Shale Oil and the WTI–Brent Spread

One of the biggest changes in oil markets over the past decade is the rise of U.S. shale production.

Shale oil is flexible and responds quickly to price changes:

When prices rise → shale producers increase drilling

When prices fall → production slows

Because shale is mostly priced off WTI, higher U.S. output often widens the WTI–Brent spread.

Logistics Constraints

Pipeline bottlenecks in the U.S. midcontinent region can cause WTI prices to fall below Brent due to oversupply.

7. The Financialization of Oil Markets

Crude oil is not just a physical commodity—it's also a major financial asset.

Investors trade oil futures, options, ETFs, and swaps, influencing price movements.

Key players include:

Hedge funds

Banks

Producers hedging future output

Airlines hedging jet fuel costs

This financial activity creates liquidity but also increases volatility.

8. OPEC+, Price Stability, and Global Economics

Inflation Management

Crude oil is a major driver of fuel prices, transportation costs, and overall inflation.

Sharp increases in oil prices often:

Push inflation higher

Increase the chances of central bank rate hikes

Slow down economic growth

OPEC+ often aims to maintain price ranges that balance producer revenues with global economic stability.

Revenue Dependence

Many OPEC+ members rely heavily on oil revenue to fund government budgets.

Low prices strain fiscal systems; high prices improve surpluses.

9. Future of Crude Oil Markets

Short to Medium Term

Demand is expected to remain strong in developing economies.

Geopolitical risks will continue to play a major role in volatility.

Long Term

Energy transition policies and global decarbonization will gradually reshape demand patterns.

However, oil will likely remain a major energy source for decades due to:

Transportation needs

Industrial petrochemicals

Aviation fuel

Limited large-scale alternatives in some sectors

OPEC+ is expected to maintain a central role in managing supply and stabilizing prices during this transition.

Conclusion

The crude oil market, anchored by the benchmarks WTI and Brent, plays a central role in global economic activity. Price movements are influenced by production levels, geopolitical events, inventory data, currency dynamics, and financial market behavior. Among all players, OPEC+ remains the most influential force in shaping supply trends and managing market stability. Their production decisions can trigger global inflation shifts, currency volatility, and economic fluctuations. As the world gradually moves toward cleaner energy sources, the balance between demand, supply, and policy-driven cuts will define the future of oil markets for years to come.

US Dollar Index (DXY) Movements1. What the DXY Represents

The US Dollar Index was introduced in 1973 after the collapse of the Bretton Woods system. It represents a geometric weighted average of the USD compared with six major currencies:

Euro (EUR) – 57.6%

Japanese Yen (JPY) – 13.6%

British Pound (GBP) – 11.9%

Canadian Dollar (CAD) – 9.1%

Swedish Krona (SEK) – 4.2%

Swiss Franc (CHF) – 3.6%

Since the euro replaced multiple European currencies, its weight became dominant. Because of this, the DXY is heavily influenced by USD/EUR movements.

A rising DXY indicates a stronger dollar relative to the basket; a falling DXY shows a weakening dollar.

2. Why DXY Movements Matter

DXY movements are crucial because the USD is the world’s leading reserve currency. Approximately:

60%+ of global forex reserves are held in USD

40%+ of global trade invoicing uses USD

Most commodities—oil, gold, metals—are priced in USD

Therefore, changes in the DXY have wide-reaching consequences:

Influence commodity prices

Affect emerging market currencies

Impact global liquidity

Alter trade competitiveness

Drive foreign investment flows

Because of its influence, DXY is often considered a barometer of global risk sentiment.

3. Key Drivers of DXY Movements

A. Federal Reserve Interest Rate Policy

The most important driver of DXY is US interest rates, controlled by the Federal Reserve.

Higher US interest rates → attract foreign investment → stronger USD → DXY rises

Lower US interest rates → reduce yield advantage → weaker USD → DXY falls

Why? Because investors chase higher returns on US Treasury bonds, leading to greater demand for USD.

B. Economic Data

Key US economic indicators influence the dollar’s strength:

Non-Farm Payrolls (NFP)

Inflation (CPI, PCE)

GDP growth

Unemployment rate

Retail sales

Strong data makes the USD more attractive; weak data pressures the dollar.

C. Risk Sentiment (Risk-On vs. Risk-Off)

During risk-off times (geopolitical tensions, crises), global investors rush to the safety of the USD → DXY rises.

During risk-on periods (market optimism), investors move to risk assets → DXY weakens.

The USD acts as a safe-haven currency.

D. Global Monetary Policy Divergence

DXY rises when:

The Federal Reserve is more hawkish than the ECB, BOJ, or BOE.

US yields are significantly higher than global peers.

DXY falls when:

Other central banks become more hawkish than the Fed.

Interest rate differentials shrink.

E. Commodity Prices

Because commodities are priced in USD:

Higher commodity prices may weaken USD as import costs rise.

Lower commodity prices can strengthen USD.

Oil has a particularly strong relationship.

F. Geopolitical Events

Events that influence DXY include:

Trade wars (especially US-China)

Middle East conflicts

Elections in major economies

Sanctions and global instability

Uncertainty boosts USD demand.

4. How to Interpret DXY Movements

A. DXY Bullish Trends

When the index is rising, it signals:

Increased confidence in the US economy

Higher US interest rates or expectations of hikes

Flight to safety during global instability

Stronger demand for US assets (Treasuries, equities)

A strong dollar typically leads to:

Lower commodity prices (gold, oil)

Pressure on emerging markets

Weaker currencies in developing nations

B. DXY Bearish Trends

A falling DXY suggests:

Fed is expected to cut rates

Weakening US economic indicators

Rising confidence in global markets (risk-on)

Strong performance of the euro or other major currencies

A weak dollar results in:

Higher commodity prices

Support for emerging market currencies

More competitive US exports

5. Impact of DXY on Global Markets

A. Commodities

Because commodities trade in USD:

When DXY rises → commodities fall

(Because they become more expensive in other currencies)

When DXY falls → commodities rise

Gold has a particularly strong inverse relationship with DXY.

B. Forex Markets

The DXY affects forex pairs:

EUR/USD – inverse relationship

USD/JPY, USD/CHF, USD/CAD – generally move with DXY direction

Traders often use DXY for confirmation of forex signals.

C. Equity Markets

A strong USD:

Hurts US multinational corporations (expensive exports)

Strengthens economies that import US goods cheaply

A weak USD:

Boosts US stock earnings (foreign revenues worth more in USD)

Supports global liquidity flows

D. Emerging Markets

EM countries with USD-denominated debt are directly affected:

Strong DXY → EM currencies fall → debt servicing becomes expensive

Weak DXY → EM markets recover

Countries like India, Brazil, Turkey, and South Africa watch DXY closely.

6. DXY in Trading and Technical Analysis

Traders use the index for:

Trend confirmation

Anticipating commodity or forex moves

Identifying global risk sentiment shifts

Common technical indicators applied to DXY:

Moving averages (50-day, 200-day)

RSI (overbought/oversold signals)

MACD (trend momentum changes)

Fibonacci retracements (medium-term corrections)

Support/resistance zones

A break above long-term resistance is often seen as a sign of USD strength globally.

7. Limitations of the DXY

Even though DXY is widely used, it has limitations:

Overweight Euro – 57.6% makes it euro-centric

Ignores key trading partners like China, Mexico, India

Outdated composition (last changed in 1999)

For broader USD strength measurement, many analysts prefer the Trade-Weighted US Dollar Index by the Federal Reserve.

8. Long-Term DXY Patterns

Historically, DXY has gone through cycles:

1980s: Extremely strong USD due to high interest rates

1990s: Moderate decline during globalization

2000s: Major weakness post-dot-com crash

2008-2020: Dollar strengthened again due to safe-haven flows

2020-2022: Pandemic uncertainty pushed DXY higher

2023 onward: Movements linked to inflation battles and Fed policy shifts

DXY cycles often correlate with US economic performance and global uncertainties.

Conclusion

The US Dollar Index (DXY) is a vital measure of the USD’s global strength. Its movements reflect underlying economic conditions, central bank policies, geopolitical events, and investor sentiment. A rising DXY usually signals risk aversion, stronger US yields, and weakness in commodity and emerging markets. A falling DXY often supports global liquidity, raises commodity prices, and weakens the dollar’s dominance temporarily.

Understanding DXY movements helps traders, investors, and analysts interpret global market dynamics, anticipate forex trends, and position themselves effectively in equities, commodities, and bonds.

Inflation & CPI Trends Across Major Economies1. What Inflation and CPI Represent

Inflation represents the rate at which the general level of prices increases over time. It shows how much the purchasing power of money declines—meaning the same amount of money buys fewer goods and services. The Consumer Price Index (CPI) is one of the most widely used indicators to measure inflation. CPI tracks the price changes of a "basket" of essential goods and services such as food, housing, healthcare, education, transportation, energy, and other everyday items.

Most central banks aim to keep inflation around 2%, believing this level balances economic growth and price stability. Too little inflation risks deflation, while too much inflation destroys purchasing power and can destabilize an economy.

2. United States – Inflation Led by Services and Wages

The U.S. has experienced significant inflationary fluctuations in recent years. After rising sharply due to pandemic-related supply disruptions, labor shortages, and aggressive fiscal stimulus, inflation began to cool. However, the U.S. economy also faced persistent services inflation, driven by rising wages, rent growth, and strong consumer spending.

The Federal Reserve uses the CPI and its preferred measure, the PCE index, to assess inflation pressure. To control inflation, the Fed raised interest rates aggressively. Cooling inflation in the U.S. is heavily influenced by:

Stabilization of supply chains

Declines in energy prices

Slower wage growth

Softening consumer demand

Still, services and housing costs often remain elevated, making full normalization slower. The U.S. inflation trend has major global implications because of the dollar’s role in global trade and finance.

3. Eurozone – Energy Prices and Weak Growth Dynamics

Inflation in the Eurozone has been heavily affected by energy price shocks, particularly due to geopolitical tensions and disruption of natural gas supply. When energy prices surged, CPI reached decades-high levels. As energy prices normalized, inflation cooled significantly.

However, inflation dynamics in Europe differ from the U.S. because of:

Weak GDP growth

Higher dependence on imported energy

Slower wage gains

Fragmented labor markets across member countries

While headline inflation eased, core inflation—which excludes volatile items like food and energy—sometimes remained elevated. The European Central Bank (ECB) aims for a 2% target, but must balance inflation control with the region’s fragile economic growth, making policy decisions more challenging.

4. United Kingdom – Stubbornly High Inflation Pressures

The UK experienced one of the highest inflation rates among developed economies due to a combination of factors:

Brexit-induced supply chain disruptions

Declines in labor supply

High food and energy prices

Strong services inflation

The Bank of England faced a difficult environment: inflation stayed high even as economic growth weakened. Food inflation and rising rents were particularly sticky. Although inflation eventually began easing, services inflation and wage pressures remained key challenges. The UK’s unique mix of structural and cyclical inflation forces continues to make inflation management more difficult compared with the U.S. or Eurozone.

5. Japan – Moving From Deflation to Inflation

Japan historically struggled with deflationary pressures for decades. However, global supply chain disruptions, higher import prices, and a weaker yen pushed Japan’s inflation upward more recently. Japanese inflation trends differ from the West:

Price rises are often driven by cost-push rather than demand-pull factors

Wage growth tends to be modest

Consumer behavior is highly price-sensitive

Firms are reluctant to raise prices

The Bank of Japan maintained ultra-loose monetary policy longer than other central banks due to its long deflation history. Inflation rising closer to the BOJ’s target was seen as a structural shift, but sustainability remains uncertain. Japan’s inflation is typically lower and more fragile than Western economies.

6. China – Low Inflation and Risk of Deflation

Unlike the West, China’s inflation trends have been very subdued. Several factors contribute to China’s low CPI:

Weak domestic demand

Property market slowdown

Falling producer prices

Slow wages growth

Consumers increasing savings rather than spending

At times, China even faces deflationary pressures, especially in the manufacturing sector. China’s CPI is heavily influenced by food prices, particularly pork, which can cause short-term volatility but not persistent inflation. The People’s Bank of China typically uses supportive monetary policy, contrasting sharply with the tightening cycles in Western countries.

China’s low inflation is a sign of economic softness rather than stability, impacting global trade demand and commodity markets.

7. India – Balancing Growth and Inflation

India's inflation trends often revolve around food, fuel, and commodity prices, which make CPI more volatile compared with advanced economies. Seasonal factors, monsoon quality, and global oil prices heavily influence inflation in India. Food inflation—especially vegetables, cereals, and pulses—plays a significant role.

The Reserve Bank of India targets a 4% inflation midpoint. Despite fluctuations, India often manages inflation reasonably due to:

Strong supply-side interventions

Government food subsidies

A diversified economy

A growing services sector

However, persistent food shocks and high global oil prices can challenge India’s inflation stability.

8. Emerging Markets – More Volatility, Higher CPI Pressures

Emerging markets such as Brazil, Turkey, South Africa, and Indonesia often face higher and more volatile inflation due to:

Exchange rate fluctuations

High dependence on imported fuel and food

Political instability

Limited monetary policy credibility

Lower household income buffers

Turkey has experienced hyperinflation-like conditions at times due to unorthodox monetary policy, while Brazil and others use very high interest rates to stabilize inflation.

Inflation management in emerging markets is fundamentally more complex, with structural challenges and external shocks playing a larger role.

9. Global Trends – What Unites and What Differentiates

Several global inflation themes have emerged:

Common Factors Across Economies

Supply chain disruptions

Energy and commodity price volatility

Labor market shifts

Climate-related food supply issues

Geopolitical tensions

Key Differences

Advanced economies face wage-driven services inflation.

China and Japan face weak demand and deflation risks.

Emerging markets face currency-driven inflation shocks.

Central banks globally aim for price stability but must balance inflation control with economic growth. Fiscal policies, demographics, globalization trends, and technological innovation also shape long-term inflation trajectories.

Conclusion

Inflation and CPI trends across major economies are shaped by a mix of global and domestic forces. While the U.S. and Europe focus on cooling services inflation, Japan and China deal with the opposite challenge: ensuring demand is strong enough to prevent deflation. Emerging markets juggle inflation volatility due to external shocks. Understanding these regional differences is essential for investors, businesses, and policymakers to navigate an interconnected global economic landscape.

Global Interest Rate Trends (Fed, ECB, BOJ, BOE)1. Why interest-rates matter

A central bank’s policy (or “policy rate”, the rate at which it lends to or charges on banks) is one of the most important levers in its monetary-policy toolkit. By raising interest rates, a central bank can make borrowing more expensive, slow spending, dampen demand and thus help reduce inflation. By lowering rates, it can stimulate borrowing, spending and investment — supporting growth when the economy is weak.

Because economies are open and interlinked, the interest-rate decisions of one major central bank can ripple through global financial markets via currency, capital‐flows, trade, investment and inflation expectations.

Given the inflation surge in many economies during 2021-23 (linked to supply-chain disruptions, pandemic responses, energy-price shocks, etc.) many central banks shifted gears sharply. Let’s examine what happened region by region.

2. The U.S. – Fed

What happened

The Fed’s main policy mechanism is the federal funds rate (overnight rate banks charge one another).

In response to rising inflation, the Fed embarked on a large rate-hiking cycle during 2022 and early 2023. For example: the target rose to around 4.25-4.50% in December 2022.

More recently (2024-25) the Fed has begun to move into a more cautious stance: holding rates steady, signalling possible cuts, and factoring in weaker labour markets and inflation which is easing.

Why

High inflation meant the Fed needed to tighten policy: raising rates reduces demand and helps bring inflation back toward target.

But raising rates has costs: increased borrowing costs, pressure on consumers and firms, risk of economic slowdown. The Fed must balance inflation control with growth and employment (its dual mandate).

Because inflation has declined from its peaks, and growth has shown signs of moderation, the Fed is increasingly considering when (and how fast) to ease rates rather than only focusing on further hikes.

Implications

The U.S. rate path matters globally: when the Fed raises rates, it raises global funding costs and strengthens the dollar, which can hurt emerging markets or trade partners.

Markets now watch closely for Fed signals on cuts, because a transition from hiking to easing is meaningful for all asset classes (bonds, equities, currencies).

As of late-2025 the Fed’s policy rate is around 4.00%.

3. The Euro-area – ECB

What happened

The ECB’s policy rate (e.g., deposit facility rate) peaked after the inflation surge (in 2023) and then began to be trimmed. For example, one report says the ECB initiated rate cuts in June 2024 after holding rates steady for some time.

As of 2025 the ECB’s rate is about 2.15% (per one data table) though that may slightly lag current decisions.

Why

The Euro-zone economy has been weaker relative to the U.S., with inflation pressures starting to ease and growth concerns creeping in (including from the war in Ukraine, energy shocks, supply disruptions) – so the ECB had both inflation to worry about and growth softness.

Once inflation began to come down, the ECB felt able to begin easing earlier than some peers. However, it emphasised that rates would remain “sufficiently restrictive” for as long as needed.

Implications

Because the ECB began cuts ahead of some other major central banks (e.g., the Fed) it has driven a divergence in interest-rate policy between Europe and the U.S.

That divergence has implications for the euro-dollar exchange rate, export competitiveness in Europe, and how capital flows respond to the relative attractiveness of the euro-zone vs. the U.S.

Lower rates in the euro-zone can help support growth and relieve borrowing costs, but if the divergence becomes too large it could put pressure on the euro and import inflation.

4. The United Kingdom – BoE

What happened

The BoE’s Bank Rate famously rose during the inflation wave; for example, the Bank Rate reached 5.25% around August 2023.

More recently the rate has been brought down somewhat — for instance, it was cut to around 4.00% by November 2025.

Why

The UK experienced high inflation in the post-pandemic period, driven by energy/commodity shocks, supply constraints, labour constraints etc. So the BoE tightened aggressively.

As inflation began to moderate and growth concerns grew (especially with the UK’s unique mix of domestic and external shocks), the BoE shifted toward modest rate cuts or rate holds — trying to tread a fine line between inflation control and growth support.

Implications

The UK being a smaller, open economy relative to the U.S. means that rate decisions can influence the pound, capital flows (especially into London financial markets), and how UK growth holds up in a global slowdown.

For borrowers in the UK (mortgages, consumer debt) the cost of borrowing tends to follow Bank Rate closely, so higher rates have had visible impacts on households and firms.

The BoE’s choices also take into account not only inflation but also the strength of domestic sectors (financial services, housing, exports), the currency, and global spill-overs.

5. Japan – BoJ

What happened

For many years Japan had ultra-low to negative interest rates, as the BoJ battled deflation and weak growth.

In March 2024, the BoJ ended its negative interest-rate policy (NIRP) and raised its overnight rate from around -0.1% to 0-0.1% (its first rate hike in 17 years).

This marks a shift toward “normalising” policy (though rates remain very low compared to other advanced economies).

Why

Japan’s economy had long struggled with deflation or very low inflation, so the BoJ kept policy ultra-accommodative for a long time.

With inflation rising globally and domestically, and the yen weakening significantly, the BoJ signalled a move to exit the ultra-low/negative rate regime.

But Japan still faces structural challenges: high public debt, demographic headwinds, modest growth, which means the BoJ remains cautious.

Implications

Japan’s policy shift matters globally because Japanese investors and financial institutions are major players in global capital markets; changes in Japanese rates/currency affect cross-border flows.

A “last major central bank” to normalise means the phase of ultralow or negative rates worldwide is ending — which has implications for bond yields, global risk premiums, and asset valuations.

For Japan’s economy, the move suggests the BoJ is increasingly confident about inflation reaching target, but any further hikes will depend on sustained domestic wage/inflation momentum.

6. The overall trend & divergence

Broad trend

Following the inflation shock of 2021-22, most major central banks moved into tightening mode: raising policy rates aggressively.

With inflation now easing (though unevenly) and growth risks increasing (especially in Europe and Japan), many central banks are either pausing on hikes or beginning to ease (cut rates).

However, the timing, pace, and magnitude of both tightening and easing differ significantly among the major central banks, creating policy divergence.

Divergence: Why it matters

When one major central bank cuts while another holds or hikes, it affects relative interest-rates, which influence currency values, international capital flows, and trade competitiveness.

For example: the ECB started cutting while the Fed held rates higher for longer — meaning euro-zone borrowing costs fell relative to the U.S., impacting bond yields, equity valuations, and currency markets.

Divergence also complicates global financial conditions: for borrowers, savers, and investors across borders, the landscape becomes more complex.

Risks

Inflation rebound risk: If a central bank cuts too early, inflation might rebound, forcing another hiking cycle — which hurts credibility and causes turbulence.

Growth slowdown risk: If rates remain high too long, growth could falter or a recession could arrive. Central banks are balancing this carefully.

Spill-overs and coordination: Because global markets are integrated, policy decisions in one region spill into others (via currencies, capital flows, commodity prices). For example, U.S. policy is often referenced by other central banks.

7. What this means for you (and for India/global economy)

For borrowers (businesses, households) higher policy rates mean higher interest costs for loans/mortgages; if rates begin to fall, borrowing becomes cheaper.

For savers/investors: higher rates typically make saving more attractive (though other factors like inflation matter), and bond yields rise; lower rates reduce yields and push investors toward riskier assets.

For emerging markets (including India): the global interest-rate environment matters a lot. If the Fed is high or hiking, capital tends to flow to the U.S., currencies of emerging markets can weaken, cost of external borrowing rises. If global rates ease, that can ease conditions for emerging markets.

In trade and currency: if your country’s interest rates diverge from those of major economies, it can affect exports/imports, exchange rates, inflation (via import costs) and competitiveness.

For inflation and growth in your country: since global commodity/energy prices, supply chains, and global demand all influence domestic inflation and growth, central-bank policy abroad matters to you indirectly.

8. Summary & takeaway

In short:

After the pandemic, global inflation surged; central banks responded by raising policy rates.

The U.S. Fed raised quickly and to relatively high levels; the ECB and BoE also raised but faced additional growth/headwind concerns. Japan stayed ultra-low for much longer.

Now (2024/25) many central banks are shifting toward pausing or cutting rates as inflation eases and growth slows — but the timing and extent differ across countries.

These differences (divergences) matter globally: they affect currencies, capital flows, trade and financial markets.

For individuals, businesses and policymakers, keeping an eye on these major central-bank paths helps anticipate borrowing costs, investment yields, exchange‐rate risks and macroeconomic conditions.

Market Condition, Trading Conditions and StrategiesHere are some important terms for traders to understand.

Market Condition refers to the overall long-term trend, where we are in the CYCLE of the Stock Market.

Trading Conditions are identified and traded by using the day over day and week over week trends and trendline patterns within that Cycle.

Strategies relate to a specific trading style based on the current Market Condition and the Trading Condition(s) within that particular Market Condition.

The Market is in a Moderately Uptrending Market Condition at this time. Trading conditions vary from sideways trends to Velocity runs, to minor corrections.

The market is choppy and sideways. Volatile markets have huge white and black candles that change abruptly from one day to the next based upon WHO IS CONTROLLING price.

In the sideways trend we’re experiencing now, different market participants are taking different actions:

Professional Traders are mostly trading to the upside.

There are also smaller funds managers with less than $3 billion in assets under management, aka Retail Side Asset Managers.

There are fewer retail investors and retail traders are mostly sidelined right now since they are worried.

There is some minor Dark Pool rotation to lower inventories of specific stocks in the NASDAQ 100 index, which impacts the QQQ ETF.

Understanding the dynamics of the Stock Market helps you trade with confidence, making decisions based on real market conditions instead of retail news—which is always late and often drives manipulative activity.

Liquidity Basics: Equal Highs/Lows, Inefficiencies & POIsPrice doesn’t move randomly, it is always attracted towards liquidity.

Every wick, breakout, and fake-out tells a story of orders being filled.

If you can read where those orders are hiding, you stop trading noise and start trading intention.

Equal Highs & Lows — The Obvious Targets

Retail traders love to mark equal highs and lows as “strong support/resistance.”

Smart money sees them as fuel.

Above equal highs = cluster of buy stops.

Below equal lows = cluster of sell stops.

When price reaches them, it’s a collection of accumulated liquidity as a main driver behind that move.

Inefficiencies — Fair Value Gaps

Also known as Fair Value Gaps (FVGs) or imbalances, these occur when price moves too quickly, leaving unfilled orders behind.

Price often revisits these zones later to rebalance.

Spot them between large candles with no overlap, they often mark where institutions filled partial orders.

Points of Interest (POIs)

POIs are areas where liquidity and inefficiency converge , the zones of intent.

Look for:

Liquidity sweep of equal highs/lows

Return to imbalance or order block

Shift in market structure

That’s where high-probability setups occur.

Note:

Stop chasing every candle.

Start mapping why price moves.

Equal highs and inefficiencies are magnets, with proper plan and confluence this can represent your strong side of trading.

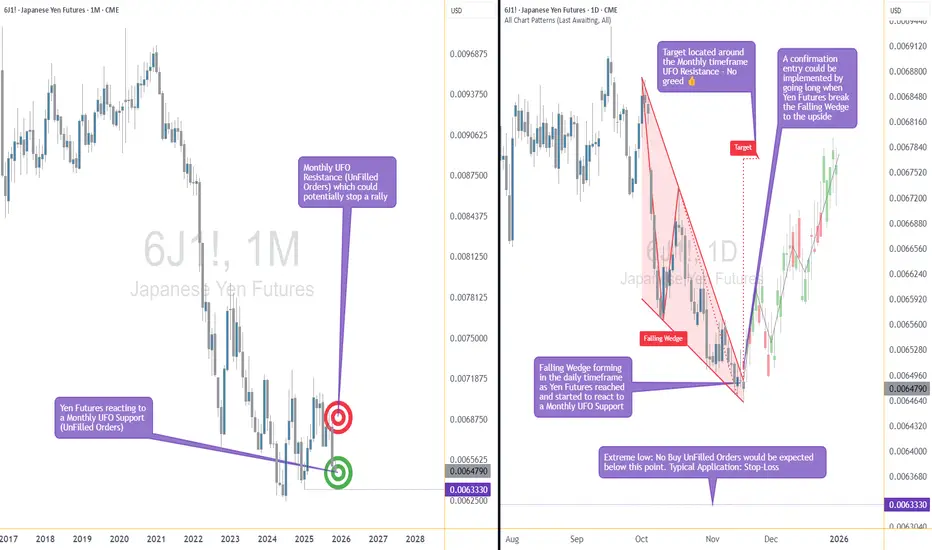

A High-Impact Support Zone Meets a Breakout StructureIntroduction

Markets occasionally compress into areas where structure, momentum, and historical buying pressure align with surprising precision. When that compression occurs at a major higher-timeframe floor, traders often pay closer attention—not because the future is predictable, but because the chart reveals a location where price behavior typically becomes informative.

The current case study centers on a market pressing into a high-impact support zone visible on the monthly chart, while the daily chart displays a falling wedge pattern that has gradually narrowed the range of movement. This combination often highlights moments where the auction process is nearing a decision point. The purpose here is to dissect that confluence using multi-timeframe structure, pattern logic, and broad order-flow principles—strictly for educational exploration.

Higher-Timeframe Structure (Monthly)

The monthly chart shows price approaching a well-defined support area between 0.0065425 and 0.0063330, a region that has acted in the past as a base for significant reactions. These areas often develop because markets rarely absorb all buy interest in a single pass; pockets of unfilled orders may remain, leading to renewed reactions when price returns.

This type of zone does not guarantee a reversal. However, historically, when price reaches such levels, traders tend to monitor whether selling pressure slows or becomes less efficient. In this case, the structure suggests a recurring willingness from buyers to engage at these prices, forming a foundation that has held multiple swings.

The presence of a clear, higher-frame resistance at 0.0067530 anchors the broader range. When price rotates between such boundaries, the monthly context often acts as a roadmap: major support below, major resistance above, and room in between for tactical case-study exploration.

Lower-Timeframe Structure (Daily)

Shifting to the daily chart, price action has carved a falling wedge, a pattern often associated with decelerating downside movement. In wedges, sellers continue to push price lower, but with diminishing strength, as each successive low becomes less effective.

This type of compression structure can provide early evidence that the auction is maturing. Traders studying such patterns often watch for:

tightening of the range,

shorter waves into new lows,

initial signs that buyers are defending intraday attempts to drive price lower.

The daily wedge in this case sits directly on top of the monthly support zone—an alignment that strengthens its analytical relevance. The upper boundary of the wedge sits near 0.0065030, and a break above that line is often interpreted as price escaping the compression phase.

Multi-Timeframe Confluence

Multi-timeframe confluence arises when higher-frame structure provides the background bias and lower-frame patterns offer the tactical trigger. In this case:

The monthly chart signals a historically responsive support zone.

The daily chart shows structural compression and slowing downside momentum.

The interaction between them creates a scenario where educational case studies tend to focus on breakout behavior, as the daily timeframe may provide the first evidence that higher-frame buyers are engaging.

This confluence does not imply certainty. It simply highlights a location where structure tends to become more informative, and where traders often study the transition from absorption to response.

Order-Flow Logic (Non-Tool-Specific)

From an order-flow perspective, strong support zones typically develop where prior buying activity left behind unfilled interest. When price returns to that region, two things often happen:

Sellers begin to encounter difficulty driving price lower, as remaining buy orders absorb their activity.

Compression patterns form, as the market oscillates in a tightening range while participants test whether enough liquidity remains to cause a directional shift.

A breakout of the daily wedge represents a potential change in the auction dynamic. While sellers are still active inside the wedge, a breakout suggests their pressure may have become insufficient to continue the sequence of lower highs and lower lows. Traders studying market transitions often use such moments as part of hypothetical scenarios to understand how imbalances evolve.

Forward-Looking Trade Idea (Illustrative Only)

For educational purposes, here is how a structured case study could frame a potential opportunity using the discussed charts:

Entry: A hypothetical entry could be placed above the falling wedge, around 0.0065030, once buyers demonstrate the ability to break outside the compression structure.

Stop-Loss: A logical invalidation area in this case study would be at or below the monthly support, around 0.0063330, where failure would indicate the higher-timeframe zone did not hold.

Target: A purely structural wedge projection would suggest a target near 0.0067695, aligning closely with the broader resistance region on the monthly chart.

These price points yield a reward-to-risk profile that is measurable and logically linked to structure, though not guaranteed. This case study exists solely to illustrate how support-resistance relationships and pattern logic can be combined into a coherent, rules-based plan, not as an actionable idea for trading.

Yen Futures Contract Context

The larger (6J) and micro-sized (MJY) versions of this futures market follow the same underlying price but differ in exposure and margin scale. The standard contract generally carries a greater notional value and therefore translates each price movement into a larger monetary change. The micro contract mirrors the same structure at a reduced size, allowing traders to adjust position scaling more precisely when navigating major zones or breakout structures such as the one discussed in this case study:

6J equals 12,500,000 Japanese Yen per contract, making it suitable for larger, institutional players. (1 Tick = 0.0000005 per JPY increment = $6.25. Required Margin = $2,800)

MJY equals 1,250,000 Japanese Yen per contract, making it suitable for larger, institutional players. (1 Tick = 0.000001 per JPY increment = $1.25. Required Margin = $280)

Understanding margin requirements is essential—these products are leveraged instruments, and small price changes can result in large percentage gains or losses.

Risk Management Considerations

Strong support zones can attract interest, but risk management remains the foundation of any structured approach. Traders studying these transitions typically:

size positions relative to the distance between entry and invalidation,

maintain clear exit criteria when structure fails,

avoid adjusting stops unless the market has invalidated the original reasons for the plan,

adapt to new information without anchoring to prior expectations.

These principles emphasize the importance of accepting uncertainty. Even at major support zones, markets can remain volatile, and scenarios may unfold differently than anticipated.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Price moves in a very specific way...In this short video I go through a bit of lower timeframe price action on the ETH futures chart.

Yeah, it is pretty straight forward and is just another example of price moving in terms of liquidity, efficiency, and fair value on a fractal nature.

R2F Trading

Bitcoin: What Historical Drawdown in a Bear Market?Since its all-time high at $126,000 reached on October 6, Bitcoin has been following a series of corrective sessions. This pullback raises a key question: is it merely a consolidation within a bull market, or the beginning of a true bear market?

First, if the cycle really ended on Monday, October 6, this would still align with the classic 4-year timing cycle, with a duration that fits within the multi-criteria average (see my correspondence table below) of previous cycles.

At this stage, the downtrend is not confirmed, as key supports — notably the weekly Ichimoku cloud — have not been broken. This level marks the decisive boundary between a standard cycle correction and a deeper reversal.