Global Hard Commodity Trading1. What Are Hard Commodities?

Hard commodities are natural resources categorized into three primary segments:

(a) Energy Commodities

Crude oil (Brent, WTI)

Natural gas (LNG, Henry Hub)

Coal

Uranium

These are central to power generation, transportation, and industrial operations.

(b) Metal Commodities

Precious metals: Gold, silver, platinum

Base metals: Copper, aluminum, zinc, lead, nickel, tin

Steelmaking inputs: Iron ore, coking coal

These metals are required for manufacturing, construction, electronics, automobiles, renewable energy systems, and more.

(c) Minerals & Industrial Raw Materials

Lithium

Cobalt

Rare earth elements

Phosphate and potash (fertilizers)

These minerals increasingly power modern, technology-driven industries like batteries, EVs, semiconductors, and clean energy.

2. Importance of Hard Commodity Trading in the Global Economy

(a) Foundation of Industrial Growth

Hard commodities are essential for infrastructure—roads, bridges, buildings, railways, ports—all require metals and minerals. Energy commodities fuel industries and transportation.

(b) Economic Interdependence

Countries with rich natural resources export them to countries lacking these assets.

Examples:

Middle East → Oil to Europe and Asia

Australia → Iron ore to China

Chile → Copper to global markets

This creates a network of global interdependence.

(c) Price Discovery and Transparency

Trading on global exchanges—like NYMEX, ICE, LME, CME, MCX—helps determine a fair market price. Producers, consumers, and investors rely on these prices for contracts and budgeting.

(d) Risk Management

Hedgers—including miners, oil producers, and manufacturers—use commodity derivatives to lock in prices and protect themselves from volatility.

3. Where Hard Commodities Are Traded?

(a) Physical Markets

Actual physical goods are bought, shipped, stored, and delivered.

Large physical traders include:

Glencore

Trafigura

Vitol

Cargill

Gunvor

These companies handle logistics, shipping, storage, and distribution.

(b) Futures & Derivatives Markets

Exchanges such as:

NYMEX (New York Mercantile Exchange) – Oil, natural gas

ICE (Intercontinental Exchange) – Brent crude, coal

LME (London Metal Exchange) – Copper, aluminum, zinc

CME Group – Metals, energy contracts

SHFE (Shanghai Futures Exchange) – China-based metals

Futures markets allow:

Speculators to profit from price movements

Hedgers to protect against adverse price fluctuations

4. Key Factors Influencing Global Hard Commodity Prices

1. Supply and Demand Dynamics

Industrial growth increases metal and energy demand.

Mining disruptions, strikes, or geopolitical issues affect supply.

2. Geopolitical Tensions

War, sanctions, and political instability can reduce supply or disrupt shipping routes.

Example: Middle East tensions often raise crude prices.

3. Global Economic Health

Recessions typically reduce demand for metals and energy.

Boom periods—like China’s industrialization—boost demand.

4. Currency Movements

Most commodities are priced in USD.

A strong dollar usually lowers commodity prices; a weak dollar increases them.

5. Technological Changes

EVs have increased demand for lithium, nickel, cobalt, and rare earths.

Renewable energy affects demand for oil and coal.

6. Weather Conditions

Weather impacts mining, shipping, and energy usage.

Cold winters raise natural gas demand, while storms disrupt oil production.

5. Major Players in Global Hard Commodity Trading

(a) Producing Countries

Oil: Saudi Arabia, Iraq, Russia, US

Coal: Australia, Indonesia, China

Metals: Chile (copper), Peru (silver), DRC (cobalt)

(b) Consuming Countries

China: World’s largest consumer of metals and energy

India: Growing demand for crude oil, coal, and steel resources

US and EU: High consumption of energy and industrial metals

(c) Commodity Trading Companies

They act as middlemen, coordinating logistics and finance:

Glencore: Metals & minerals

Vitol & Trafigura: Oil & energy trades

BHP, Rio Tinto, Vale: Mining giants

(d) Financial Institutions

Banks, hedge funds, and asset managers trade futures for investment and speculation.

6. The Process of Hard Commodity Trading

Step 1: Extraction and Production

Oil is drilled, metals are mined, and minerals are refined.

Step 2: Transportation

Commodities are transported through:

Ships (VLCC for crude oil)

Pipelines (natural gas, petroleum)

Railways and trucks (coal, metals)

Step 3: Storage

Stored in:

Tank farms (oil)

Warehouses (metals)

Silos (raw materials)

Step 4: Trading

Producers sell commodities through:

Long-term contracts

Spot markets

Futures markets

Step 5: Use in Industrial Processes

Refineries convert crude into usable fuels.

Manufacturers use metals in electronics, cars, machinery, and infrastructure.

7. Challenges in Global Hard Commodity Trading

1. Price Volatility

Commodities face large price swings due to geopolitical events or economic cycles.

2. Logistics & Infrastructure Constraints

Limited shipping capacity, port congestion, or poor transport systems can delay trade.

3. Environmental Regulations

Countries are shifting toward cleaner energy, reducing demand for fossil fuels.

4. Resource Nationalism

Governments may restrict exports, raise royalties, or nationalize mining assets.

5. Climate Change

Extreme weather disrupts production and transportation.

8. Future Trends in Hard Commodity Trading

(a) Energy Transition

Shift to renewable energy will change demand patterns:

Reduced demand for oil and coal

Increased demand for lithium, copper, nickel, and rare earths

(b) Digitalization of Commodity Markets

Blockchain, AI, and smart contracts are improving transparency and efficiency.

(c) Rise of Critical Minerals

Minerals like lithium, cobalt, and rare earths are becoming strategically important.

(d) Decentralized Trading Platforms

Technological platforms allow smaller players to trade without intermediaries.

(e) Sustainability and ESG Focus

Investors increasingly prefer sustainably sourced commodities, changing how mines operate.

Conclusion

Global hard commodity trading is a complex, interconnected system involving physical supply chains, financial markets, geopolitical influences, and technological advancements. These commodities power industries, sustain economic growth, and shape international relations. As the world transitions toward cleaner energy and more advanced technologies, the demand structure for hard commodities will evolve, creating new opportunities and challenges. Understanding these dynamics allows businesses, investors, and policymakers to make better strategic decisions in an increasingly competitive global landscape.

Chart Patterns

Spot forex trading — practical “secrets”1. Trade the market you see, not the story you tell

One of the most costly “secrets” is simply this: markets don’t care about your narrative. Human brains love stories (inflation, wars, central banks) and those stories can be useful, but your priority must be price action and confirmed structure. If price breaks a key level and confirms with follow-through, act. If your view relies entirely on a neat story without price confirmation, you’re speculating, not trading.

2. Make risk management your system’s backbone

Successful traders manage risk first, edge second. A few principles:

Risk a fixed small percent of capital per trade (commonly 0.5–2%). This prevents one loss from wiping your gains.

Define stop loss and maximum acceptable daily drawdown before entering.

Use position sizing math (risk per trade / distance to stop) to determine lots. This is mechanical and removes emotion.

Never average down into a losing position unless you have a documented, statistically tested scaling plan and the trade still fits your edge.

3. The spread and slippage are your invisible costs

Spreads, commissions and slippage silently erode profitability. Avoid trading pairs with wide spreads or during low-liquidity hours. Be mindful of news events that widen spreads and cause slippage. Using limit orders where sensible can reduce market impact, but they come with the risk of not getting filled.

4. Know when liquidity favors you

Forex liquidity follows a daily rhythm: London and New York sessions see the most volume and narrowest spreads. Volatility is higher at market overlaps (London/New York). Trade when your strategy thrives — if you’re a breakout trader, trade during high-liquidity hours; if you prefer quiet mean-reversion, consider quieter times but watch for thin-market spikes.

5. Use timeframes intentionally — multi-timeframe confirmation

A “secret” repeatedly practiced by pros: align multiple timeframes. Identify the primary bias on a higher timeframe (daily/4H), then refine entries on a lower timeframe (1H/15m). This reduces random noise and improves odds. Don’t confuse confirmation with paralysis — you still need execution rules.

6. Focus on a handful of pairs

Mastery beats variety. Pick 3–6 currency pairs and learn their quirks: baseline volatility, reaction to economic releases, correlation to other assets (e.g., USD/JPY sensitivity to risk sentiment). Specialization lets you anticipate typical behavior and manage trades more skillfully.

7. Correlation awareness avoids accidental overexposure

Many currency pairs move together. Holding multiple correlated positions doubles risk without you noticing. Monitor correlations and limit portfolio-level exposure to avoid being leveraged into a single macro move.

8. Trade the event, not the headline

Economic releases are traded in two stages: initial fast move (often noisy and driven by order flow) and the follow-through as market participants digest the new information. If you trade news, have rules about whether you fade the initial spike, chase momentum, or wait for the post-news structure. Rushing in during the chaotic first seconds is a common way to get stopped out.

9. Execution matters: order types and placement

Limit orders can capture better prices and reduce spread costs — use them for entries and scaling.

Stop orders protect capital; place them beyond logical structural levels, not at obvious spots where they’re likely to be hunted.

Virtual stops (mental stops) are dangerous; write your stops in the platform and accept fills.

10. Keep a rigorous trading journal

Record entry/exit, stop size, reasoning, timeframe, emotions, and post-trade thoughts. Over weeks and months, the journal reveals systematic errors (overtrading, revenge trading, entering too early). The journal is the only honest performance feedback loop — analyze it weekly.

11. Have a clear, tested edge

An “edge” might be: specific breakout behavior after a London open, mean reversion after RSI extremes on 1H for EURUSD, or trading divergence with volume confirmation. Backtest carefully, but beware overfitting. Simpler rules that generalize are better than complex rules that only worked historically.

12. Use position scaling and pyramiding conservatively

Scaling in (adding to winners) can be more effective than averaging losers. Add small increments as the trade proves correct and widen stops appropriately. Pyramiding increases position when evidence supports it; averaging into a losing trade destroys capital.

13. Understand carry, swaps, and overnight exposure

Holding spot forex overnight can incur swap/rollover credits or charges depending on interest rate differentials. For short-term traders this is minor; for swing traders it matters. Include swap costs in your plan when holding for days.

14. Manage psychology like a trader, not a gambler

Common mental traps: FOMO (chasing a missed move), revenge trading (immediately trying to recoup a loss), and overconfidence after a streak. Predefine a daily trade limit and a rule to stop after N consecutive losses. Mindfulness, routines, and small rituals before trading can stabilize decision-making.

15. Build a repeatable routine and playbook

Have a morning checklist: review economic calendar, market internals, correlated asset moves (equities, bonds, commodities), overnight price action, and your watchlist levels. A consistent routine reduces impulsive trades and protects capital.

16. Use technology — but avoid overreliance

Algos and EAs can execute consistently, but remember they inherit your assumptions. Backtest on out-of-sample data and forward paper-trade before going live. Latency, slippage, and broker behavior differ from backtest assumptions.

17. Respect market structure — support/resistance, trend, range

Trade with the structure: buy pullbacks in a clean uptrend; sell rallies in a downtrend; trade ranges only when price respects levels repeatedly. Recognize when structure is shifting (higher highs/lows breakdown) and adapt.

18. Continual learning vs. strategy churn

Many traders hurt themselves by switching strategies too often. Test a new idea on a small size or in a demo account and apply only if it shows consistent edge. Maintain a learning log and implement improvements incrementally.

Final secret: small consistent edges compound

You don’t need to be right all the time. If your average win is larger than your average loss and you manage trade frequency and risk, compounding will work in your favor. Shrink risk, increase discipline, and keep trading costs low — that combination, repeated, is the truest “secret” in spot forex.

Derivatives Trading in Emerging Markets1. Understanding Derivatives

A derivative is a financial instrument whose value is derived from the price of an underlying asset. The underlying can be stocks, bonds, commodities, interest rates, exchange rates, or market indices. The most common types of derivatives include forwards, futures, options, and swaps.

Forwards are customized contracts traded over the counter (OTC), where two parties agree to buy or sell an asset at a future date at a predetermined price.

Futures are standardized contracts traded on exchanges, reducing counterparty risk through clearing houses.

Options give the holder the right, but not the obligation, to buy or sell an asset at a specified price within a certain period.

Swaps involve the exchange of cash flows or financial instruments between two parties, often to manage exposure to interest rates or currencies.

Derivatives are used for hedging, speculation, and arbitrage, making them vital tools for both risk management and profit generation.

2. Growth of Derivatives in Emerging Markets

Emerging markets such as India, China, Brazil, South Africa, and Indonesia have witnessed rapid growth in derivatives trading over the past two decades. Initially, their financial systems were dominated by cash or spot markets. However, the volatility in exchange rates, commodity prices, and interest rates created demand for instruments that could mitigate these risks.

India’s derivatives market, for example, began in 2000 with index futures on the NSE (National Stock Exchange). Today, it is one of the largest derivatives markets globally in terms of contract volumes.

China launched commodity futures exchanges in the 1990s and gradually introduced financial derivatives, although its government maintains strict control to prevent speculation-driven instability.

Brazil’s BM&FBOVESPA (now B3) is another major hub, offering derivatives on interest rates, currencies, and commodities.

This expansion reflects both the globalization of finance and the increasing sophistication of local investors and institutions.

3. Role and Importance in Emerging Markets

a. Risk Management

Derivatives are crucial for hedging against uncertainties in currency rates, interest rates, and commodity prices. For instance, exporters in India use currency futures to protect themselves from exchange rate fluctuations, while farmers in Brazil hedge their crop prices through commodity futures.

By allowing investors and companies to transfer risk to those willing to bear it, derivatives enhance financial stability.

b. Price Discovery

Futures and options markets help in determining the expected future price of an asset based on market sentiment. For example, futures prices of crude oil or gold on Indian exchanges provide valuable information to producers, traders, and policymakers about expected market conditions.

c. Market Liquidity and Efficiency

Derivatives attract speculators who add liquidity to the market. This increased participation tightens bid-ask spreads and improves overall price efficiency. Furthermore, arbitrage between spot and derivatives markets ensures prices remain aligned, reducing distortions.

d. Financial Deepening

A vibrant derivatives market signals financial maturity. It encourages institutional participation, supports innovation, and contributes to the development of related sectors such as clearing and settlement systems, credit rating agencies, and risk management firms.

4. Challenges Faced by Emerging Markets

While the benefits are clear, emerging markets face several structural and operational challenges in developing robust derivatives markets.

a. Regulatory and Legal Framework

In many countries, the regulatory environment is still evolving. Over-regulation can stifle innovation, while weak supervision can lead to excessive speculation and financial crises. For instance, in some Asian markets, derivatives trading was temporarily banned after being linked to market volatility.

Emerging markets need transparent, consistent, and globally aligned regulations to build investor confidence and attract international participation.

b. Limited Market Depth and Participation

Retail participation in derivatives is often low due to limited awareness and the perception of high risk. Institutional investors, such as pension funds and insurance companies, may face restrictions on using derivatives. As a result, markets may be dominated by a few large players, reducing competition and liquidity.

c. Counterparty and Credit Risk

In OTC derivatives markets, the risk that one party may default on its obligation remains significant. The lack of centralized clearing mechanisms in some markets exacerbates this problem. Developing central counterparty (CCP) systems and improving risk management practices are vital.

d. Infrastructure and Technology

Efficient trading, clearing, and settlement require advanced infrastructure. Some emerging markets still face technological constraints, slow transaction processing, or inadequate risk monitoring systems, limiting the scalability of derivatives trading.

e. Market Manipulation and Speculation

Because derivatives offer high leverage, they can be used for speculative purposes, sometimes leading to market manipulation or bubbles. Regulatory oversight and investor education are essential to prevent misuse.

f. Low Financial Literacy

Many investors in emerging markets lack a full understanding of derivatives. Without proper knowledge, they may engage in speculative trading or misuse derivatives, leading to losses and erosion of trust in the system.

5. Case Studies

India

India’s derivatives market is among the most developed in the emerging world. The NSE and BSE offer a wide range of products, including equity futures and options, currency derivatives, and commodity contracts. The Securities and Exchange Board of India (SEBI) plays a crucial role in regulating the market, ensuring transparency and risk management. India’s introduction of interest rate futures and index options has enhanced hedging opportunities for institutional and retail investors alike.

China

China’s derivatives market has grown rapidly but remains tightly controlled by regulators to avoid excessive speculation. The Shanghai Futures Exchange and Dalian Commodity Exchange are major platforms. China’s government uses derivatives strategically to stabilize commodity and currency markets, reflecting a cautious but steady approach to liberalization.

Brazil

Brazil’s derivatives market, integrated through B3 Exchange, is known for innovation in interest rate and currency products. It supports both domestic and international investors and serves as a model of how derivatives can aid monetary policy and risk management in volatile economies.

6. Future Prospects

The future of derivatives trading in emerging markets is promising, driven by technological innovation, financial integration, and policy reforms.

Digital transformation and algorithmic trading will enhance liquidity and efficiency.

Blockchain and smart contracts could make derivatives trading more transparent and secure.

Cross-border trading and integration with global exchanges will deepen market access.

ESG-linked derivatives may emerge, allowing investors to hedge environmental and sustainability risks.

However, to realize this potential, emerging markets must invest in education, infrastructure, and governance. Collaboration with global institutions such as the International Monetary Fund (IMF) and the World Bank can also provide technical assistance and policy guidance.

7. Conclusion

Derivatives trading has evolved from a sophisticated financial tool to a vital pillar of modern emerging economies. It helps manage risks, enhances liquidity, and strengthens the resilience of financial systems. However, the path to maturity is complex—emerging markets must balance innovation with regulation, speculation with stability, and access with responsibility.

As these economies continue to integrate into the global financial system, the expansion of derivatives markets will play a key role in supporting sustainable growth, attracting foreign investment, and providing the foundation for a more resilient global economy. With prudent regulation, improved market infrastructure, and growing investor sophistication, the future of derivatives trading in emerging markets is both dynamic and promising.

Forward and Future Forex Trading1. Understanding Forex Derivatives

A derivative is a financial contract whose value is derived from the performance of an underlying asset—in this case, a currency pair. In forex trading, derivatives such as forwards, futures, options, and swaps are used to hedge currency risks or to speculate on currency price movements. The purpose is to manage exchange rate volatility that can impact trade, investment returns, or the cost of imported and exported goods.

2. What is a Forward Forex Contract?

A forward contract in forex is a customized agreement between two parties to exchange a specific amount of one currency for another at a predetermined rate (known as the forward rate) on a specified future date.

For example, suppose an Indian importer expects to pay $1 million to a U.S. supplier in three months. If the current USD/INR rate is ₹83, and the importer fears that the rupee may depreciate to ₹85, they can enter into a forward contract with a bank to buy $1 million at ₹83.50 after three months. Regardless of the market rate at that time, the importer will pay ₹83.50 per dollar, thus avoiding potential losses from exchange rate volatility.

Key Characteristics of Forward Contracts:

Customization: The contract size, maturity date, and exchange rate are negotiated between the buyer and seller.

No Exchange Trading: Forwards are traded over-the-counter (OTC), typically between banks, corporations, or financial institutions.

Settlement: The exchange of currencies occurs on the agreed future date.

No Initial Margin: Usually, no upfront margin is required; settlement happens only at maturity.

3. What is a Forex Futures Contract?

A forex futures contract is a standardized agreement to buy or sell a specific amount of currency at a future date and a predetermined rate. Unlike forwards, futures are traded on regulated exchanges such as the Chicago Mercantile Exchange (CME) or Intercontinental Exchange (ICE).

For instance, a trader may buy a Euro FX Futures contract to purchase euros and sell U.S. dollars at a fixed exchange rate three months from now. These contracts are marked to market daily, meaning profits and losses are settled at the end of each trading day.

Key Characteristics of Futures Contracts:

Standardization: Futures have fixed contract sizes, maturity dates, and settlement procedures.

Exchange-Traded: Traded on organized exchanges under regulatory supervision.

Daily Settlement: Open positions are marked to market daily, and margin adjustments are made accordingly.

Margins and Clearing Houses: Traders deposit an initial margin and maintain a variation margin to cover potential losses. Clearing houses guarantee the trade, reducing counterparty risk.

4. Forward vs. Future Forex Contracts – Key Differences

Feature Forward Contract Futures Contract

Trading Venue Over-the-counter (OTC) Organized exchanges (e.g., CME)

Customization Fully customizable Standardized

Counterparty Risk Higher (no clearing house) Lower (clearing house guarantees)

Liquidity Lower Higher

Margin Requirement Usually none Required (initial and variation)

Settlement At maturity Daily mark-to-market

Flexibility High Limited due to standardization

Use Case Hedging by corporations Speculation and hedging by traders

In essence, forwards are tailored instruments suited for businesses with specific needs, while futures cater more to traders and investors who prefer liquidity, transparency, and regulatory oversight.

5. Purpose and Applications

A. Hedging

Corporations use forwards and futures to hedge foreign exchange exposure from imports, exports, loans, or investments.

Example: An Indian IT firm expecting USD inflows may sell dollars forward to lock in the current exchange rate and protect against rupee appreciation.

B. Speculation

Traders and investors use futures to profit from expected currency movements.

Example: A trader expecting the euro to strengthen may buy euro futures contracts.

C. Arbitrage

Arbitrageurs exploit differences in currency prices between spot, forward, and futures markets to earn risk-free profits.

Example: Covered interest arbitrage ensures alignment between interest rates and forward premiums.

D. Portfolio Diversification

Forex futures allow institutional investors to gain exposure to foreign currencies, balancing risk in their investment portfolios.

6. Advantages of Forward and Future Forex Contracts

Forwards:

Tailored contracts that meet exact needs.

Useful for long-term hedging.

No upfront margin or daily cash flow requirement.

Futures:

Highly liquid and easily tradable.

Reduced counterparty risk due to clearing houses.

Transparent pricing and regulated environment.

Ideal for short-term trading or speculation.

7. Disadvantages and Risks

Forwards:

High counterparty risk.

Illiquid—difficult to exit before maturity.

No daily marking to market; losses can accumulate unnoticed.

Futures:

Less flexibility due to standardization.

Requires margin deposits, tying up capital.

Daily settlement can create cash flow challenges.

Speculative positions can amplify losses.

8. Market Participants

The key participants in forward and future forex trading include:

Commercial Banks – act as counterparties in forward contracts.

Corporations – hedge foreign exchange risk.

Hedge Funds & Institutional Investors – speculate using futures.

Central Banks – use forwards/futures for currency stabilization.

Retail Traders – participate in exchange-traded futures for short-term gains.

9. Real-World Examples

Forward Example:

A Japanese exporter expecting $5 million from a U.S. buyer in six months locks in the JPY/USD forward rate to avoid yen appreciation losses.

Futures Example:

A currency trader on CME buys British Pound futures anticipating a rise in GBP against USD. If GBP strengthens, the trader profits as the futures contract gains value.

10. Global Forex Forward and Futures Markets

The forward market is vast, largely dominated by interbank transactions. According to the Bank for International Settlements (BIS), forwards account for over $1 trillion in daily turnover globally.

The futures market, while smaller, is growing rapidly due to transparency and accessibility. Leading exchanges like CME, Euronext, and SGX offer a wide range of currency futures, including EUR/USD, GBP/USD, USD/JPY, and emerging market pairs such as USD/INR.

Conclusion

Both forward and future forex trading play critical roles in the international financial system. Forwards provide flexibility and customization, making them ideal for corporations seeking to hedge long-term currency risks. Futures, on the other hand, offer liquidity, transparency, and regulatory safety, making them attractive for traders and investors.

In today’s volatile global economy, where exchange rates can fluctuate due to geopolitical tensions, monetary policies, or economic shocks, these instruments are indispensable tools for managing currency exposure and optimizing financial strategies. The choice between forwards and futures ultimately depends on the trader’s objectives, risk appetite, and the nature of their exposure. Together, they ensure that global trade and investment can proceed with reduced uncertainty and enhanced financial stability.

Pharma Stocks in the World Market1. Overview of the Global Pharmaceutical Industry

The global pharmaceutical market is vast and dynamic, valued at over $1.5 trillion as of the mid-2020s. It encompasses traditional drug manufacturers, biotechnology firms, and healthcare innovators. The industry’s growth is driven by several long-term trends such as population aging, chronic disease prevalence, technological innovation, and rising healthcare spending in both developed and emerging economies.

Pharmaceutical companies can broadly be divided into two categories:

Innovator or Research-Based Companies: These firms invest heavily in research and development (R&D) to create new drugs. Examples include Pfizer, Merck, Johnson & Johnson, Roche, Novartis, AstraZeneca, and Eli Lilly.

Generic Drug Manufacturers: These companies produce lower-cost versions of branded drugs after patents expire. Examples include Teva Pharmaceutical, Sun Pharma, Dr. Reddy’s Laboratories, and Cipla.

Both segments are essential to global healthcare, but their business models and profit margins differ significantly.

2. Factors Driving the Growth of Pharma Stocks

a. Aging Population and Chronic Diseases:

As populations age, particularly in developed nations, the prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders rises sharply. This creates a steady and long-term demand for pharmaceuticals, making the sector relatively resilient to economic downturns.

b. Technological Advancements:

Innovations in biotechnology, genomics, and artificial intelligence have transformed drug discovery and personalized medicine. New treatments such as gene therapies, immunotherapies, and mRNA vaccines have expanded the scope of healthcare and boosted investor confidence in the sector.

c. Rising Global Healthcare Expenditure:

Governments and private sectors worldwide are increasing their spending on healthcare infrastructure and medication access. Emerging markets such as India, China, and Brazil are witnessing rapid pharmaceutical market expansion due to improving income levels and healthcare awareness.

d. Regulatory Support and Fast-Track Approvals:

Regulatory bodies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have adopted fast-track processes for breakthrough drugs and pandemic-related treatments. These initiatives accelerate innovation and market entry for critical therapies.

e. Pandemic Influence:

The COVID-19 pandemic profoundly impacted global pharma stocks, showcasing the industry’s vital role. Companies like Pfizer, Moderna, and AstraZeneca gained global prominence for developing vaccines, resulting in unprecedented revenue growth and investor interest.

3. Key Players in the Global Pharma Market

Several multinational corporations dominate the pharmaceutical sector:

Pfizer Inc. (U.S.) – Known for its vaccine leadership and a diversified portfolio across cardiovascular, oncology, and rare diseases.

Johnson & Johnson (U.S.) – A healthcare conglomerate engaged in pharmaceuticals, medical devices, and consumer health products.

Roche Holding (Switzerland) – A leader in oncology and diagnostics, with a focus on precision medicine.

Novartis (Switzerland) – Known for its strong research orientation and biologics pipeline.

AstraZeneca (U.K.) – A major player in oncology and respiratory drugs with a rapidly expanding vaccine business.

Eli Lilly (U.S.) – Recently recognized for its breakthroughs in diabetes and obesity treatments.

Sanofi (France) – A key European player in vaccines and specialty care.

Gilead Sciences (U.S.) – Specializes in antiviral drugs for HIV, hepatitis, and COVID-19.

Bristol Myers Squibb (U.S.) – Known for its innovative cancer immunotherapy products.

GlaxoSmithKline (U.K.) – Focused on vaccines, respiratory, and infectious disease segments.

These companies collectively account for a large share of global pharma revenues and are heavily represented in major stock indices like the S&P 500 Healthcare Index and the MSCI World Health Care Index.

4. Market Trends and Developments

a. Biotechnology and mRNA Revolution:

The success of mRNA vaccines during the COVID-19 pandemic opened new possibilities for treatments against cancers, genetic disorders, and autoimmune diseases. Biotech firms such as Moderna and BioNTech are now among the most-watched stocks globally.

b. Mergers and Acquisitions (M&A):

Consolidation is a key strategy in the pharma sector. Large companies frequently acquire smaller biotech firms to strengthen their drug pipelines and reduce research risks. Examples include Pfizer’s acquisition of Seagen and Amgen’s acquisition of Horizon Therapeutics.

c. Digital Health and AI Integration:

Artificial intelligence is revolutionizing drug discovery, clinical trials, and patient monitoring. Companies integrating AI in R&D—such as Roche and Novartis—are expected to gain a competitive edge.

d. Focus on Rare Diseases:

Pharma firms are increasingly investing in treatments for rare or “orphan” diseases, which often enjoy premium pricing and extended patent protections.

e. Sustainability and ESG Practices:

Investors are emphasizing environmental, social, and governance (ESG) standards. Pharmaceutical firms are being evaluated not only for profits but also for ethical practices, drug pricing transparency, and environmental impact.

5. Risks and Challenges

Despite strong growth potential, pharma stocks face several challenges:

a. Regulatory Hurdles:

Drug development is a long, complex, and costly process. Regulatory delays or denials can significantly impact a company’s valuation and investor sentiment.

b. Patent Expiry and Generic Competition:

When blockbuster drugs lose patent protection, generic manufacturers flood the market with cheaper alternatives, eroding profits.

c. Pricing Pressure:

Governments and insurers worldwide are tightening controls over drug pricing to ensure affordability, especially in the U.S. and Europe.

d. Research and Development Costs:

Developing a single new drug can cost over $2 billion and take more than a decade. Failure in clinical trials can lead to heavy financial losses.

e. Political and Ethical Issues:

Pharma companies often face public scrutiny over drug accessibility, pricing controversies, and intellectual property disputes.

6. Regional Insights

United States:

The U.S. leads the world pharmaceutical market, accounting for nearly 40% of global sales. It has a robust ecosystem of biotech startups, large-cap pharma firms, and supportive venture capital funding. The NASDAQ Biotechnology Index (NBI) and S&P Pharmaceuticals Select Industry Index track many of these leading firms.

Europe:

Switzerland, Germany, the U.K., and France are home to some of the world’s most respected pharmaceutical giants. European firms emphasize innovation in biotechnology, vaccines, and specialty care.

Asia-Pacific:

Countries like India and China have emerged as major manufacturing hubs. India is the world’s largest supplier of generic medicines, while China has rapidly advanced in biologics and contract manufacturing.

Emerging Markets:

Latin America, Africa, and Southeast Asia are witnessing growing demand for affordable healthcare solutions, creating new markets for both branded and generic drugs.

7. Investment Outlook for Pharma Stocks

Pharma stocks are often viewed as defensive investments, meaning they perform relatively well during economic downturns because healthcare demand remains stable. The sector also offers long-term growth potential due to innovation and demographic trends.

Investors typically evaluate pharma companies based on:

R&D pipeline strength

Regulatory approvals and patents

Revenue diversification

Cash flow stability

Dividend history

Exchange-traded funds (ETFs) such as the iShares U.S. Pharmaceuticals ETF (IHE) or SPDR S&P Biotech ETF (XBI) provide diversified exposure to the sector.

8. Future Prospects

The next decade promises significant transformation in the pharmaceutical landscape. Personalized medicine, AI-driven research, digital therapeutics, and global vaccine innovation will reshape how treatments are developed and delivered. Furthermore, the integration of genomics and data analytics will allow for more targeted therapies, reducing side effects and improving patient outcomes.

Pharma companies that can combine innovation, scalability, and ethical responsibility are likely to outperform. Meanwhile, investors seeking stability and long-term value will continue to view pharma stocks as an essential part of diversified portfolios.

Conclusion

Pharma stocks represent a cornerstone of the global market, balancing innovation-driven growth with defensive stability. The industry’s influence extends far beyond financial returns—it underpins human health, economic resilience, and technological progress. Despite regulatory, ethical, and pricing challenges, the sector’s future remains bright, driven by scientific advancements, aging populations, and the ongoing pursuit of better health for all. As global healthcare evolves, pharmaceutical companies will continue to play a central role in shaping the world economy and investment landscape.

Scalping in the World Market1. Understanding Scalping

Scalping is a short-term trading strategy that focuses on exploiting tiny price gaps created by order flows, liquidity imbalances, or temporary market inefficiencies. Unlike swing traders or investors who hold positions for days, weeks, or months, scalpers hold positions for seconds to minutes. The key principle behind scalping is that smaller price movements occur more frequently than larger ones, offering more trading opportunities.

In global markets—such as forex, commodities, equities, and indices—scalpers rely on high liquidity and tight spreads to enter and exit positions quickly. They typically use leverage to magnify gains, as the profit per trade is minimal.

2. Core Principles of Scalping

Scalping operates on several fundamental principles:

Speed: Since market prices can change within milliseconds, speed in execution is essential. Scalpers use advanced trading platforms, direct market access (DMA), and low-latency connections.

Volume: Scalpers make many small trades daily. Each trade might aim for profits as low as 0.05%–0.3%, but hundreds of trades can compound into meaningful returns.

Liquidity: High liquidity ensures that scalpers can enter and exit positions without significant slippage. Major currency pairs like EUR/USD or large-cap stocks like Apple, Microsoft, or Tesla are popular among scalpers.

Risk Control: Because profits per trade are small, losses must be minimized. Scalpers often set tight stop-losses and focus on maintaining a high win rate (above 70%).

3. Types of Scalping Strategies

There are multiple approaches to scalping in the world market, each tailored to different instruments and trader preferences:

a. Market-Making Scalping

Traders act as market makers, placing both buy and sell limit orders around the current price. They profit from the bid-ask spread if both orders are filled. This method requires deep understanding of order book dynamics and access to direct liquidity pools.

b. Momentum Scalping

This strategy relies on identifying short-term trends and trading in the direction of momentum. Scalpers jump into trades when a breakout occurs and exit as soon as momentum slows. It is common in volatile assets like cryptocurrencies and tech stocks.

c. Range Scalping

Scalpers exploit sideways market movements by repeatedly buying at support and selling at resistance. This works well in stable, low-volatility sessions when prices oscillate within a predictable band.

d. News-Based Scalping

Scalpers react to breaking news, such as economic data releases or earnings announcements. Fast reactions to volatility spikes can yield quick profits—but require excellent reflexes and execution systems.

e. Algorithmic Scalping

Automated systems or trading bots are programmed to execute thousands of micro-trades per second based on pre-set parameters. Algorithmic scalping dominates modern global markets due to its speed and efficiency.

4. Scalping Across Global Markets

Scalping takes different forms depending on the market environment and asset class:

a. Forex Market

The foreign exchange market is ideal for scalping due to 24-hour trading, high liquidity, and minimal transaction costs. Popular pairs include EUR/USD, GBP/USD, and USD/JPY. Forex scalpers rely heavily on technical indicators like moving averages, Bollinger Bands, and RSI to time entries and exits.

b. Stock Market

In equity markets, scalping focuses on high-volume, blue-chip stocks. Traders monitor order books, market depth, and volume patterns. Scalpers often use Level II quotes to anticipate short-term price changes.

c. Commodities and Futures

Gold, crude oil, and index futures are popular instruments for scalping because they offer high liquidity and continuous price movement. Traders use tick charts and DOM (Depth of Market) data to detect micro-trends.

d. Cryptocurrency Market

The 24/7 nature and volatility of crypto markets make them attractive for scalping. Bitcoin (BTC), Ethereum (ETH), and Solana (SOL) often move several percent daily, offering frequent micro opportunities. However, spreads and fees can be higher compared to forex.

5. Tools and Techniques Used in Scalping

Successful scalpers rely on advanced tools and precise analysis:

Charting Software: Real-time charting with one-minute, tick, or volume-based time frames.

Indicators: Moving Average Convergence Divergence (MACD), Relative Strength Index (RSI), VWAP (Volume Weighted Average Price), and Stochastic Oscillator.

Order Flow Analysis: Observing the order book, time and sales data, and bid-ask imbalances to anticipate short-term direction.

Hotkeys and Automation: Speedy order entry and exits are crucial, often executed using hotkeys or algorithmic scripts.

Broker and Platform: Low-latency brokers with ECN (Electronic Communication Network) access and minimal spreads are preferred.

6. Advantages of Scalping

Frequent Opportunities: Since prices fluctuate constantly, there are continuous trading chances.

Limited Exposure: Positions are held briefly, reducing exposure to large market swings or news shocks.

Compounding Gains: Small consistent profits accumulate over time, building meaningful returns.

Adaptability: Scalping strategies can be applied to multiple asset classes globally.

7. Disadvantages and Risks of Scalping

Despite its appeal, scalping is challenging and not suitable for every trader:

High Transaction Costs: Frequent trades lead to higher commissions and fees that can erode profits.

Stress and Concentration: The need for quick decisions and constant monitoring can be mentally exhausting.

Execution Slippage: Delays in order execution can turn profitable trades into losses.

Broker Restrictions: Some brokers discourage or prohibit scalping due to the high server load and short holding times.

Small Margin of Error: One large loss can wipe out profits from dozens of successful trades.

8. Psychology of a Scalper

Scalping demands a specific mindset. Scalpers must remain calm, disciplined, and unemotional even under intense market pressure. They focus on process over outcome, knowing that statistical consistency matters more than any single trade. Impulsiveness or revenge trading can quickly destroy a scalper’s capital.

Good scalpers often have backgrounds in mathematics, data analysis, or programming, allowing them to develop or optimize trading systems that enhance precision and risk control.

9. Risk Management in Scalping

Effective risk management is crucial. Typical techniques include:

Tight Stop-Loss Orders: To prevent large drawdowns, stops are set just a few ticks away.

Position Sizing: Scalpers limit exposure per trade to a small portion of their capital.

Daily Loss Limits: Many professionals stop trading after hitting a predefined loss cap.

Avoiding Overtrading: Not every price movement is an opportunity; discipline is key.

10. The Future of Scalping in the Global Market

As global markets become increasingly digitalized, scalping is evolving rapidly. The rise of high-frequency trading (HFT), AI-driven algorithms, and machine learning models has made manual scalping less dominant but still viable for specialized traders.

Technological advances such as low-latency networks, colocation near exchange servers, and quantitative analysis tools give professional scalpers a competitive edge. However, regulators worldwide are introducing tighter rules to ensure market fairness, which affects the way scalping is conducted—especially in equity and futures markets.

Conclusion

Scalping plays a vital role in the global financial ecosystem by enhancing liquidity, narrowing spreads, and maintaining market efficiency. It attracts traders who thrive on speed, precision, and discipline. While it offers the potential for consistent profit, it demands exceptional skill, emotional control, and access to cutting-edge technology.

In essence, scalping is not just about quick profits—it is a test of reflexes, discipline, and strategy in a world where milliseconds can determine success or failure. As automation and AI reshape global trading, scalping continues to be both an art and a science, symbolizing the ultimate pursuit of efficiency in the financial markets.

The Role of the Metals Market in Global Trade1. Historical Background and Evolution of the Metals Market

Metals have played a pivotal role in the evolution of human societies. Ancient civilizations like Egypt, Mesopotamia, and the Indus Valley used copper, bronze, and gold for tools, ornaments, and trade. The discovery of iron marked the beginning of the Iron Age, revolutionizing warfare, agriculture, and construction. As maritime trade expanded during the Renaissance, gold and silver became the foundation of global commerce, with countries competing for control over mineral-rich territories.

The Industrial Revolution in the 18th and 19th centuries marked a turning point. The demand for coal, iron, and later steel surged as nations built railways, ships, and factories. This era established metals as a driving force behind industrial power. In the 20th century, aluminum, copper, and nickel became essential for the automotive, electrical, and aerospace industries. Today, the digital revolution and green transition have added new dimensions to the metals trade, with lithium, cobalt, and rare earth elements at the forefront.

2. Classification of Metals in Global Trade

Metals can broadly be classified into precious metals, base metals, and ferrous metals:

Precious metals such as gold, silver, and platinum are valued for their rarity, monetary use, and investment appeal. They often act as safe-haven assets during economic uncertainty.

Base metals like copper, aluminum, zinc, and nickel are essential industrial inputs used in construction, manufacturing, and electronics.

Ferrous metals, primarily iron and steel, form the backbone of global infrastructure, machinery, and transportation.

Each category plays a distinct role in trade flows and economic development, influencing everything from industrial output to currency stability.

3. Key Players in the Global Metals Market

The global metals trade is dominated by a few major producers and consumers:

China is the largest consumer and producer of most base metals, particularly steel and aluminum. Its rapid industrialization has made it a major influencer of global metal prices.

Australia, Brazil, and Chile are leading exporters of iron ore, copper, and other minerals, contributing significantly to global supply.

The United States, Russia, and Canada play key roles in producing precious metals and industrial metals like nickel and palladium.

Africa, particularly countries like South Africa and the Democratic Republic of Congo (DRC), is rich in gold, platinum, and cobalt resources.

These nations’ trade relationships often reflect their comparative advantages in metal production and processing, forming the foundation for global supply chains.

4. Metals as Strategic and Economic Assets

Metals are not just industrial materials—they are strategic assets that influence national security and economic resilience. Nations stockpile metals like copper, nickel, and rare earth elements to secure industrial supply chains and mitigate geopolitical risks. For example:

Rare earth metals are crucial for producing high-tech devices, defense equipment, and renewable energy systems. China’s dominance in this sector gives it significant geopolitical leverage.

Oil-to-metal transitions, driven by green energy goals, have increased the demand for metals like lithium and cobalt used in electric vehicle (EV) batteries and renewable technologies.

Consequently, control over metal reserves has become a modern form of strategic power, shaping trade alliances and economic policies.

5. Pricing and Market Dynamics

Metal prices are determined by supply-demand fundamentals, economic cycles, and speculative activities. Major commodities exchanges like the London Metal Exchange (LME), Chicago Mercantile Exchange (CME), and Shanghai Futures Exchange (SHFE) facilitate global pricing and hedging.

Factors influencing metal prices include:

Economic growth: Rising industrial activity boosts metal demand and prices.

Technological innovation: New manufacturing technologies alter consumption patterns (e.g., lightweight aluminum replacing steel).

Geopolitical tensions: Trade restrictions or sanctions can disrupt supply chains.

Environmental policies: Carbon regulations and sustainability goals affect mining and production costs.

Investment flows: Metals also serve as speculative assets, influenced by currency strength, inflation, and interest rates.

Thus, metal prices often act as economic indicators, reflecting global industrial health and investor sentiment.

6. The Role of Metals in Industrialization and Infrastructure Development

Metals are indispensable to industrialization. Steel underpins infrastructure — bridges, railways, and skyscrapers — while copper powers electrical networks and communication systems. Aluminum enables lightweight transportation and aerospace manufacturing, and nickel and cobalt are key in renewable energy storage.

Developing economies rely heavily on metal imports to build infrastructure and manufacturing capacity. For instance, India’s expanding urbanization and infrastructure development drive strong demand for iron and aluminum. Conversely, developed economies export technology and capital to resource-rich nations in exchange for raw materials, fostering interdependence in global trade.

7. Environmental and Sustainability Challenges

Mining and metal production are energy-intensive processes that contribute significantly to carbon emissions and ecological degradation. The global push toward sustainability has forced the metals industry to adopt cleaner technologies and recycling practices.

Recycling metals reduces energy consumption by up to 95% compared to primary production.

Circular economy models are being promoted to minimize waste and maximize resource efficiency.

ESG (Environmental, Social, and Governance) frameworks now influence investment in mining and metal companies, driving greener operations.

Additionally, the transition to renewable energy and electric vehicles has paradoxically increased demand for certain metals like lithium and copper, creating new sustainability dilemmas related to mining practices.

8. Trade Policies and Market Regulation

Governments play a crucial role in shaping metal trade through tariffs, export restrictions, and subsidies. For example:

The U.S.–China trade tensions have led to tariffs on aluminum and steel.

Indonesia has imposed export bans on nickel ore to encourage domestic processing.

The European Union’s Carbon Border Adjustment Mechanism (CBAM) aims to penalize imports of carbon-intensive metals, pushing producers toward cleaner production.

These policies influence global trade patterns, encouraging nations to diversify sources and invest in local refining capacities.

9. The Future of the Global Metals Market

The metals market is undergoing a structural transformation. The shift toward green technologies, digitalization, and geopolitical realignments will reshape global demand and supply chains.

Key trends include:

Rising demand for battery metals (lithium, cobalt, nickel) due to electric vehicle growth.

Technological advances in mining, such as automation and AI, enhancing efficiency.

Increased recycling and circular economy initiatives.

Geopolitical competition over strategic metals, especially between the U.S., China, and the EU.

Digital metal trading platforms improving transparency and liquidity.

These developments indicate that the future metals market will be more sustainable, technologically advanced, and geopolitically complex.

10. Conclusion

The metals market remains a cornerstone of global trade, connecting economies through resource flows and industrial demand. Metals shape not only the physical world—through construction, manufacturing, and technology—but also the geopolitical and economic landscape. As nations strive for cleaner growth, technological advancement, and strategic security, metals will continue to hold immense importance. From traditional iron and copper to modern lithium and rare earths, metals are the silent engines driving the global economy forward. Their trade will increasingly define the balance between growth, sustainability, and geopolitical influence in the 21st century.

ESG Investing and Sustainable Finance1. Understanding ESG Investing

ESG stands for Environmental, Social, and Governance — the three key pillars used to evaluate the sustainability and ethical impact of an investment.

Environmental (E):

This pillar examines how a company manages its environmental responsibilities. Factors include carbon emissions, energy efficiency, waste management, pollution control, renewable energy use, and climate change mitigation strategies.

Example: Companies that reduce greenhouse gas emissions or invest in renewable energy are seen as environmentally responsible.

Importance: Investors assess environmental performance to gauge how well a company can manage climate-related risks and comply with emerging environmental regulations.

Social (S):

This component focuses on how a company interacts with people — employees, customers, suppliers, and communities. It includes labor practices, employee welfare, diversity and inclusion, human rights, product safety, and community engagement.

Example: Firms that promote gender equality, maintain fair wages, or engage in ethical supply chains demonstrate strong social values.

Importance: Socially responsible companies tend to attract loyal customers, maintain a motivated workforce, and avoid reputational risks.

Governance (G):

Governance deals with corporate leadership, internal controls, and shareholder rights. It assesses board diversity, executive pay, ethical business conduct, transparency, and anti-corruption policies.

Example: Companies with independent boards, fair executive compensation, and transparent reporting systems score high in governance.

Importance: Good governance reduces the likelihood of fraud, mismanagement, and unethical behavior — ensuring long-term stability.

In ESG investing, these three dimensions help investors identify organizations that are not only financially sound but also sustainable and ethical in their operations.

2. The Rise of ESG Investing

ESG investing has evolved from a niche concept to a global mainstream movement. Several factors have contributed to this shift:

Investor Awareness:

Modern investors, particularly millennials and Gen Z, are increasingly motivated by values. They prefer to invest in companies that align with their ethical and environmental beliefs.

Regulatory Push:

Governments and international bodies are promoting ESG standards. For example, the European Union introduced the Sustainable Finance Disclosure Regulation (SFDR), and India’s Business Responsibility and Sustainability Report (BRSR) mandates ESG disclosures for top-listed companies.

Corporate Accountability:

Global corporations are under growing pressure to adopt ESG frameworks, not only to attract investors but also to secure long-term sustainability and brand credibility.

Risk Management:

ESG factors are now recognized as essential to identifying long-term risks such as environmental disasters, regulatory changes, or social unrest that could affect business performance.

According to data from the Global Sustainable Investment Alliance (GSIA), ESG-related investments surpassed $35 trillion globally by 2023, representing about one-third of all professionally managed assets.

3. The Concept of Sustainable Finance

While ESG investing focuses on evaluating company performance using sustainability metrics, sustainable finance refers to the broader financial system that supports sustainable development.

Sustainable finance integrates environmental, social, and governance considerations into all aspects of financial decision-making — including banking, insurance, and capital markets. It aims to channel capital toward projects and companies that contribute positively to society and the planet.

Key components of sustainable finance include:

Green Finance:

This focuses on funding environmentally friendly projects — such as renewable energy, energy-efficient infrastructure, sustainable agriculture, or water conservation.

Example: Green bonds are debt instruments used to finance environmental projects.

Social Finance:

This supports initiatives that improve social well-being — such as affordable housing, education, healthcare, or employment generation.

Climate Finance:

A subcategory of sustainable finance, it targets investments that mitigate or adapt to climate change. This includes funding clean technologies and climate-resilient infrastructure.

Impact Investing:

This approach seeks measurable positive social and environmental outcomes alongside financial returns. Investors directly fund projects or enterprises that deliver tangible societal benefits.

4. Interconnection Between ESG Investing and Sustainable Finance

ESG investing is a subset of sustainable finance. While ESG focuses on assessing companies through sustainability metrics, sustainable finance provides the financial infrastructure — such as green bonds, sustainability-linked loans, and climate funds — to support those ESG-driven companies and initiatives.

In other words:

ESG provides the criteria for evaluation.

Sustainable finance provides the capital for transformation.

Together, they form a comprehensive ecosystem where financial decisions contribute to a greener, fairer, and more transparent global economy.

5. Benefits of ESG Investing and Sustainable Finance

Long-Term Value Creation:

ESG-aligned companies tend to perform better in the long run due to better risk management, innovation, and adaptability.

Lower Risk Exposure:

Firms adhering to ESG standards are less likely to face regulatory fines, lawsuits, or reputational damage.

Improved Access to Capital:

Sustainable companies attract more investors, as many institutional funds now mandate ESG compliance.

Enhanced Reputation and Brand Loyalty:

Consumers increasingly support ethical and eco-conscious brands, boosting market share.

Positive Societal Impact:

Capital is directed toward solving global issues like climate change, poverty, and inequality, leading to inclusive growth.

6. Challenges in ESG and Sustainable Finance

Despite its growth, ESG investing faces several obstacles:

Lack of Standardization:

Different rating agencies use varying ESG criteria, leading to inconsistent evaluations of the same company.

Greenwashing:

Some companies falsely claim to be sustainable to attract investors — a practice known as “greenwashing.”

Data Limitations:

Reliable and comparable ESG data is scarce, especially in emerging markets.

Short-Term Market Pressures:

Investors often prioritize quarterly profits over long-term sustainability goals.

High Implementation Costs:

Transitioning to sustainable practices can be expensive, particularly for small and medium enterprises (SMEs).

7. Global and Indian Perspective

Globally, regions like Europe and North America lead in ESG adoption, with institutional investors such as BlackRock and Vanguard emphasizing sustainability mandates. The United Nations Principles for Responsible Investment (UN PRI) and the Paris Agreement have further driven ESG integration into the financial system.

In India, ESG and sustainable finance are gaining momentum:

SEBI (Securities and Exchange Board of India) has made ESG reporting mandatory for the top 1,000 listed companies under the BRSR framework.

The Reserve Bank of India (RBI) has initiated policies supporting green and social financing.

Indian banks like SBI and HDFC are issuing green bonds to finance renewable energy and social projects.

This marks a clear shift in India’s investment culture — aligning financial growth with sustainability.

8. The Future of ESG and Sustainable Finance

The future of finance lies in sustainability-driven innovation. Artificial intelligence, big data, and blockchain are being used to enhance ESG data transparency and traceability. Governments are introducing carbon pricing, taxonomy regulations, and sustainability-linked incentives to encourage responsible investing.

As climate risks and social inequalities intensify, ESG and sustainable finance will continue to evolve — not as alternatives but as the new standard of global financial practice.

Conclusion

ESG investing and sustainable finance represent more than just financial trends — they are part of a paradigm shift in how societies view growth and prosperity. They align economic success with social well-being and environmental preservation. By integrating sustainability into financial systems, investors and institutions are not only securing returns but also shaping a resilient, equitable, and sustainable future for generations to come.

In essence, profit and purpose are no longer opposites — they are partners in the global mission toward sustainable development.

Fractal Dimension VisualizedThere are plenty of times where fractals are mentioned across TA, from indicators like FRAMA, Williams Fractals, concepts like Elliott waves - all the way to my own way of breaking cycles through Fibonacci Channels. Pretty much most of them are about self-similar behavior of the market which is often invisible to unweponized eye.

In this piece I’m going to the core - fractal dimension . Don’t fixate on numbers! Instead, visualize the scaling process: how structures fills space as you zoom in and out.

Regular Dimensions

The most fundamental question is: How many copies (N) do we get with each magnification (R).

Line (1D): A line has only one length. If I magnify length by a factor R, the number of smaller copies that fit is N=R. (Double the length → 2 copies; in general N = R^1.)

Square (2D): Magnify side length by R: the big square splits into a grid of R x R old squares, so N=R^2.

Cube (3D): Magnify edge length by R: the big cube contains R x R x R small cubes, so N=R^3.

So in D dimensions, when you scale length by R, the count of self-similar copies is N = R^D

Hence, we can extract dimension: D = log N / log R

This is the similarity dimension formula when the object breaks into N exact copies, each scaled by 1/R in length.

Application to Fractals

Sierpinski Triangle

We actually start with a solid 2D equilateral triangle. Then we remove the central upside-down triangle to leave three smaller solid triangles. Now we repeat that step inside every remaining triangle, forever. As this process continues, any patch of solid area that survives will eventually be removed, so the total area shrinks toward zero while the number of pieces explodes. The limit is the Sierpiński triangle: not “just lines,” but a fractal set with no area and a non-integer dimension between 1 and 2

At each step you get N=3 copies, each scaled by 1/2 (so R=2).

D = log 3 / log 2 = 1.5850

How to work out D in practice

Identify the scaling length: by what factor R must you magnify so the large figure looks like a collage of smaller identical copies?

Count those copies N.

Plug into D = log N / log R.

This is highly important for perceiving scaling laws not just for self-similar shapes but also other patterns.

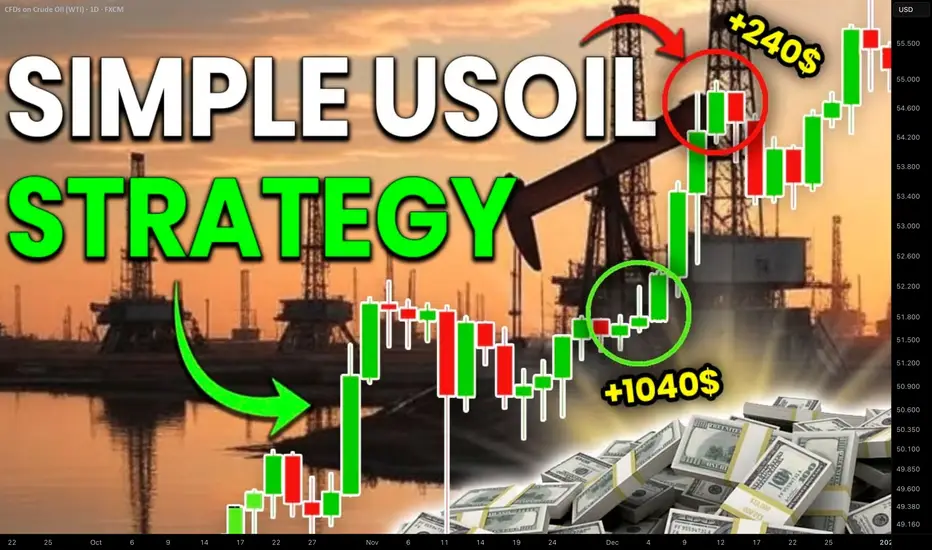

How to Trade Crude Oil with Smart Money Concepts SMC Explained

Smart Money Concepts is one of the most reliable techniques for trading WTI Crude Oil.

In this article, I will teach you a profitable SMC strategy for analysing and trading USOIL futures and CFD.

This simple strategy is based on an important event every SMC trader should know - a break of structure BoS.

In a bullish trend, the best break of structure will be based on a violation and a candle close above a current higher high.

It will signify a highly probable bullish continuation and provides a great opportunity to buy

Though you can spot a bullish break of structure on any time frame, the most reliable one is a daily.

After a formation of a new high, I suggest waiting for a short term intraday correctional movement.

With a high probability, the market will retest a recently broken structure and smart money will manipulate the market, pushing the price below that, making buyers close their positions.

Once the market starts retracing, analyze an hourly time frame. The price will need to establish an i ntraday minor bearish trend.

In this bearish trend, 2 trend lines should connect lower highs and lower lows composing an expanding, parallel or contracting channel - a bullish flag pattern.

Your best signal will be a breakout of a resistance line of the flag and a violation of the level of the last lower high - a bullish change of character of a liquidity grab.

It will confirm a completion of a correction.

Buy the market on a retest of the level of the last higher low, it will be your best entry.

Set your stop loss at least below a trend line and aim at the next strong daily resistance.

That will be a perfect model for trading break of structure on WTI Crude Oil.

We spotted such a setup in my trading academy on one of the live streams with my students.

WTI Crude Oil was trading in an uptrend on a daily time frame.

A bullish violation of the last Higher High and a candle close above that confirmed a Break of Structure BoS.

The price started a correctional movement then, and we spotted a bullish flag pattern on an hourly time frame.

The market completed a correction after grabbing a liquidity below a broken structure.

A bullish movement started then, and the price violated a resistance line of the flag and the level of the last lower high.

These 2 breakouts confirmed a completion of a correction and a resumption of a bullish trend.

We opened a buy position immediately on a retest of a broken level of the last lower high.

Stop loss was below a trend line, take profit was based on the closest key daily resistance.

And the price went straight to the target.

Break of Structure BoS will be useful for analysis, forecasting and trading WTI Crude Oil.

Combining that with top-down analysis and lower time frames confirmations will provide accurate signals and profitable trading setups.

Integrate a price model that I shared in your strategy, and good luck to you trading USOIL!

❤️Please, support my work with like, thank you!❤️

I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

"Trading is a lonely journey, but the most rewarding""Trading is a lonely journey."

I had heard that saying a long time ago, but only when I stepped onto this path did I truly understand what it meant. On the first day I placed a trade, I thought everything was simple , just a few clicks, a few flickering green and red numbers, and I could make money. But the deeper I went, the more I realized that behind the screen was a cold, silent world where I was the only one facing myself.

No one understands the feeling of watching your account evaporate in just a few seconds. Nor can anyone share the tiny joy of a winning trade, because most outsiders only see the results — not the sleepless nights, not the heartbeats racing with every moving candle. Gradually, I learned to stay quiet : no more bragging about profits, no more complaining about losses. Trading taught me that emotions are the cruelest enemy.

There are days I stare at the chart until my eyes ache, my head spinning from those merciless price waves. I ask myself, “Am I really going in the right direction? Is trading even meant for me?” But then, in silence, I open my laptop again - analyze, take notes, place orders, as if it’s a habit I can’t let go of. Every loss hurts, but it also makes me stronger . I’ve learned to accept being wrong, to be disciplined, and to live with loneliness.

Trading isn’t just a battle with the market, it’s a battle with your own ego . It’s lonely, yes, but not meaningless. In that silence, I can hear my own thoughts more clearly ,my limits, and my desire to rise beyond them. Maybe only those who have walked this path can truly understand: behind every click lies countless emotions, unseen scars that only traders carry.

Trading is a lonely journey — but it’s also one of the most valuable journeys of all.

Try harder my friend! ;)

ANFIBO_

Sanctions and Their Role in the Global Market1. Understanding Sanctions

Sanctions are restrictions placed by one country or a group of countries on another nation or entity to enforce international laws or influence political or economic decisions. They are often used as alternatives to military intervention, serving as diplomatic or economic pressure tools. Sanctions can be applied for various reasons — to punish aggression, prevent nuclear proliferation, counter terrorism, or respond to human rights violations.

The key players in imposing sanctions are major economic and political blocs such as the United Nations (UN), the European Union (EU), and powerful individual nations like the United States. The U.S., for instance, uses the Office of Foreign Assets Control (OFAC) to design and enforce sanctions globally.

2. Types of Sanctions

Sanctions come in several forms, each targeting different aspects of an economy or government operation. The most common types include:

Economic Sanctions:

These restrict trade and financial transactions. Examples include import and export bans, restrictions on investments, or freezing of assets. Economic sanctions are intended to weaken a nation’s economic stability.

Trade Sanctions:

Trade restrictions can prevent the export of critical goods like oil, technology, or weapons. For instance, sanctions on Iran’s oil exports have significantly limited its main source of revenue.

Financial Sanctions:

These target banking systems, financial institutions, and access to international payment systems like SWIFT. Russia, for example, faced severe financial isolation after its 2022 invasion of Ukraine.

Travel and Visa Sanctions:

These restrict the movement of political leaders, business executives, or individuals associated with illicit activities.

Military Sanctions:

These include arms embargoes that prevent the sale or supply of weapons and military technology.

Sectoral Sanctions:

These are targeted at specific sectors, such as defense, energy, or finance, to maximize economic pressure while minimizing collateral damage.

3. Objectives of Sanctions

The main goal of sanctions is to influence the behavior of governments or organizations without direct conflict. Their objectives include:

Deterring Aggression:

Sanctions can discourage military invasions or aggressive policies by raising the economic costs of conflict.

Promoting Human Rights:

Countries imposing sanctions often aim to pressure regimes accused of human rights abuses to change their policies or release political prisoners.

Preventing Nuclear Proliferation:

Sanctions against nations like North Korea and Iran are designed to stop the development of nuclear weapons programs.

Countering Terrorism:

Sanctions can block financial channels and assets used by terrorist groups.

Maintaining Global Stability:

Sanctions can be part of a coordinated global response to maintain international peace and uphold the rules-based order.

4. Mechanisms and Enforcement

Sanctions are typically implemented through laws, executive orders, or international agreements. Enforcement mechanisms include:

Asset Freezes: Preventing access to money or property held in foreign accounts.

Export Controls: Blocking the sale of critical goods, technology, or services.

Financial Restrictions: Limiting a country's access to international capital markets or payment systems.

Secondary Sanctions: Penalizing third-party countries or companies that do business with the sanctioned nation.

Monitoring compliance is crucial. Organizations such as the Financial Action Task Force (FATF) help track illegal financial activities and ensure that sanctions are effectively enforced.

5. Impact on the Global Market

The effects of sanctions ripple through the global economy, influencing trade balances, currency values, and market confidence. The impact varies based on the size and integration of the targeted country into the global market.

a. Trade and Supply Chains

Sanctions often disrupt global supply chains. For instance, sanctions on Russia and Iran have affected oil and gas supplies, driving up energy prices worldwide. Similarly, export restrictions on high-tech goods to China have reshaped global semiconductor and electronics markets.

b. Energy Markets

Energy is one of the most affected sectors. Russia’s sanctions after the Ukraine conflict caused global oil and gas price surges, forcing Europe to seek alternative energy suppliers. The Organization of the Petroleum Exporting Countries (OPEC) also faces indirect pressure when sanctions alter global energy supply and demand dynamics.

c. Financial Markets

Financial sanctions can restrict global capital flow. When large economies face sanctions, investors often move funds to safer markets, affecting currency exchange rates and global liquidity. For example, the freezing of Russian foreign reserves shook confidence in the global financial system and led to a rethinking of foreign reserve management by other nations.

d. Currency and Inflation

Countries under sanctions often experience currency depreciation due to restricted foreign investment and reduced exports. This leads to inflation and reduced purchasing power. Conversely, global markets can see inflation spikes when critical exports like oil or metals are restricted.

e. Global Business and Investment