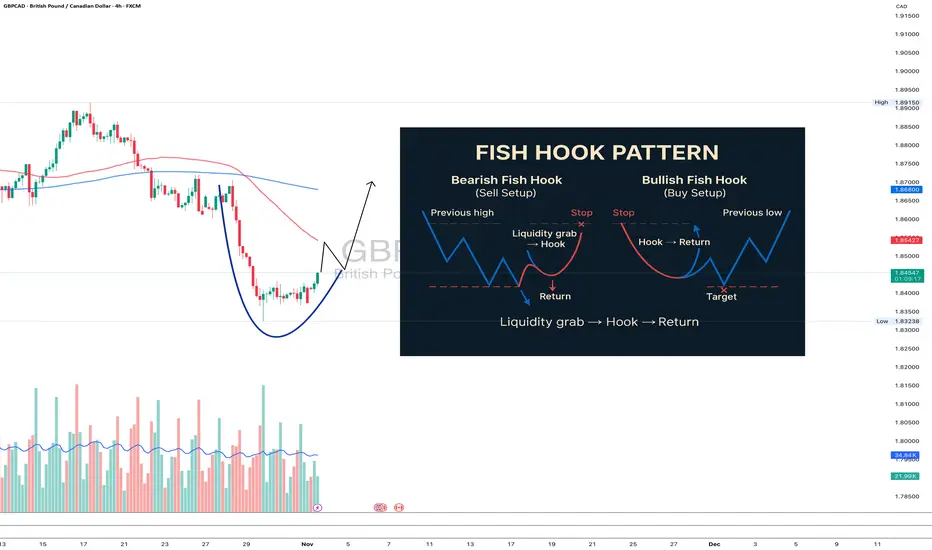

Fish Hook Pattern: the setup that catches liquidity, not tradersThere’s one pattern that never gets enough attention in textbooks, yet it’s one of the purest reflections of smart money logic - the Fish Hook.

It looks simple: price breaks out, triggers stops, traps breakout traders, and snaps back just as fast. But the psychology behind it is what makes it truly powerful.

When the market consolidates under a level, stop orders start to pile up. Big money knows that liquidity sits there - waiting to be taken. They push the price beyond the level, trigger the stops, and absorb liquidity. The breakout traders think they’ve caught momentum, but in reality, they’ve just become the exit liquidity.

Then comes the reversal - fast, decisive, emotional. That sharp return to the range is the “hook.”

If price breaks a key high or low and immediately rejects it - without structure, without a clean retest - you’re watching a Fish Hook in action.

The entry comes on the retest of that level from the opposite side. The stop goes right beyond the “hook’s tip.” Targets? The opposite edge of the range or the next liquidity pool.

The beauty of the Fish Hook lies in its simplicity. It’s not an indicator or a signal. It’s the behavior of money - watching how capital manipulates emotion.

When you start to see it often, you realize the market isn’t random. It’s intentional.

Trading becomes less about chasing candles and more about reading footprints. Fish Hook setups happen daily across pairs, stocks, and crypto and once you train your eye, you’ll never unsee them.

If your stops keep getting hit before the move - congratulations, you just met the Fish Hook from the wrong side.

Chart Patterns

AVOID LOSSES - BE SMART - LIVE ANALYSIS AVOID LOSSES - BE SMART - LIVE ANALYSIS

FRGNT

Be smart — avoid needless and pointless losses.

Anyone can trade, but what truly defines your return is your level of professionalism.

Use the facts to your advantage and build your bias using multiple sources of information. Build your confluence from correlating pairs, not just the pair you’re looking to trade.

Remember — GBPUSD, EURUSD, and AUDUSD are correlating.

So if you believe a trade is ready on one pair, but not showing the same readiness on the others, ask yourself: does this make sense?

Am I acting in line with a professional trader’s mindset?

Use the facts. Trade with logic. Think like a professional.

🔍 Analysis Approach:

I’m applying Smart Money Concepts, focusing on:

Identifying Points of Interest on the Higher Time Frames (HTFs) 🕰️

Using those POIs to define a clear trading range 📐

Refining those zones on Lower Time Frames (LTFs) 🔎

Waiting for a Break of Structure (BoS) for confirmation ✅

This method allows me to stay precise, disciplined, and aligned with the market narrative, rather than chasing price.

💡 My Motto:

"Capital management, discipline, and consistency in your trading edge."

A positive risk-to-reward ratio, paired with a high win rate, is the backbone of any solid trading plan 📈🔐

⚠️ Losses?

They’re part of the mathematical game of trading 🎲

They don’t define you — they’re necessary, they happen, and we move forward 📊➡️

🙏 I appreciate you taking the time to review my Daily Forecast.

Stay sharp, stay consistent, and protect your capital

— FRNGT 🚀

Global Payments RevolutionizedThe Transformation of Money Movement in the Modern Era

The global payments industry has undergone a remarkable transformation in recent decades. Once dominated by cash, checks, and manual bank transfers, today’s payment systems have evolved into fast, secure, and borderless networks driven by innovation, technology, and globalization. The shift from traditional to digital transactions has redefined how individuals, businesses, and governments interact financially. This revolution has not only simplified commerce but also expanded financial inclusion, improved transparency, and accelerated economic growth across the world.

1. The Historical Context of Global Payments

For centuries, global trade relied heavily on physical currency and paper-based systems. International trade payments involved cumbersome processes such as letters of credit, telegraphic transfers, and intermediary banks, often taking days or even weeks to complete. These systems were expensive, slow, and prone to fraud and error. As globalization intensified in the late 20th century, the need for more efficient, standardized, and secure payment systems became evident.

The introduction of credit cards, electronic fund transfers (EFT), and the SWIFT (Society for Worldwide Interbank Financial Telecommunication) network in the 1970s marked the first wave of modernization. SWIFT allowed banks to communicate securely about international payments, while card networks like Visa and Mastercard made cross-border consumer transactions simpler. However, true transformation came with the rise of the internet and digital technologies in the 21st century.

2. Digital Transformation and Fintech Disruption

The emergence of financial technology (fintech) startups in the 2000s redefined the payments ecosystem. Traditional banks faced competition from nimble, tech-driven firms offering faster, cheaper, and user-friendly payment solutions. Companies like PayPal, Stripe, and Square introduced digital payment systems that allowed seamless online transactions, transforming e-commerce globally.

Mobile payment platforms, such as Apple Pay, Google Pay, and Samsung Pay, enabled consumers to make purchases with just a tap of their smartphones. Peer-to-peer (P2P) transfer apps like Venmo, Cash App, and Revolut made splitting bills or sending money internationally almost instant.

Fintech innovation has also driven down transaction costs and improved accessibility. Through digital wallets, even unbanked populations in developing regions can participate in the global economy. For example, M-Pesa in Kenya revolutionized financial inclusion by enabling millions to send, receive, and save money via mobile phones without traditional bank accounts.

3. Rise of Real-Time Payment Systems

One of the most significant advances in modern payments has been the adoption of real-time payment (RTP) systems. Unlike traditional bank transfers that may take days, RTP enables instant fund settlement, 24/7. Countries like the U.K. (with Faster Payments), India (with UPI – Unified Payments Interface), and Brazil (with Pix) have set global benchmarks for efficient domestic payment systems.

India’s UPI, launched in 2016, has become a global model for digital transactions. It allows users to transfer money instantly across different banks using a mobile device, supporting billions of monthly transactions. The success of such systems has inspired other nations to modernize their infrastructure, leading to initiatives like the European Union’s SEPA Instant and the U.S. FedNow system.

These innovations have also enhanced cross-border payment efficiency, allowing businesses to settle invoices, pay suppliers, and manage global operations with unprecedented speed.

4. Blockchain and Cryptocurrency: The Next Frontier

The emergence of blockchain technology and cryptocurrencies such as Bitcoin, Ethereum, and stablecoins has redefined the meaning of global payments. Blockchain’s decentralized ledger allows transactions to be verified and recorded without intermediaries, reducing costs and increasing transparency.

Cryptocurrencies enable near-instant cross-border transfers, bypassing traditional banking channels that often charge high fees. Stablecoins, digital tokens pegged to fiat currencies, provide the stability needed for practical payment use.

Moreover, central bank digital currencies (CBDCs) are being developed globally as a government-backed alternative to private cryptocurrencies. China’s Digital Yuan, the European Union’s Digital Euro, and India’s Digital Rupee are examples of how national monetary authorities are embracing blockchain to modernize payment systems. These initiatives could further enhance financial inclusion and make international payments more secure and efficient.

5. E-commerce and the Rise of Global Payment Gateways

The global e-commerce boom has accelerated the demand for seamless international payment solutions. Platforms like PayPal, Stripe, and Adyen have made it possible for businesses to accept payments in multiple currencies while complying with local regulations.

Additionally, buy-now-pay-later (BNPL) services such as Klarna and Afterpay have transformed consumer behavior by allowing flexible payments without traditional credit cards. These digital solutions have expanded global consumer bases for businesses, enabling cross-border trade like never before.

In parallel, marketplaces such as Amazon, Alibaba, and Shopify have integrated payment gateways into their platforms, ensuring that sellers and buyers worldwide can transact effortlessly.

6. Security, Regulation, and Trust

With the expansion of digital payments comes the challenge of cybersecurity and regulatory compliance. Fraud, data breaches, and money laundering risks have increased, prompting governments and financial institutions to strengthen digital identity verification, encryption, and anti-money laundering (AML) measures.

Frameworks like PSD2 (Payment Services Directive 2) in Europe mandate strong customer authentication and promote open banking. Open banking allows third-party developers to build financial services around consumer data, further promoting innovation while maintaining security standards.

Consumer trust remains crucial, and innovations such as biometric authentication, tokenization, and AI-based fraud detection have made digital payments safer than ever.

7. Financial Inclusion and Socioeconomic Impact

One of the most profound impacts of the payment revolution is the expansion of financial inclusion. Digital payment platforms have brought millions of people—especially in Africa, Asia, and Latin America—into the formal financial system.

For small businesses and entrepreneurs, access to digital payments means access to credit, savings, and investment opportunities. Governments are also using digital payment infrastructure to deliver subsidies, pensions, and social welfare programs directly to citizens, reducing corruption and inefficiency.

The democratization of payments has empowered women, rural communities, and informal workers by giving them control over their finances, thus contributing to overall economic development.

8. The Future of Global Payments

The next decade of payments will likely focus on interoperability, sustainability, and AI-driven automation. Efforts are underway to connect domestic real-time systems globally through initiatives like the Bank for International Settlements (BIS) Project Nexus, which aims to create seamless cross-border payment corridors.

Artificial Intelligence and machine learning will continue to optimize fraud detection, customer experience, and transaction processing. Meanwhile, sustainability is gaining importance—digital payments reduce the carbon footprint associated with cash production and transportation.

Moreover, embedded finance, where payment capabilities are integrated directly into apps, vehicles, or devices, will make payments invisible and frictionless. For instance, electric vehicles might automatically pay for charging, or smart refrigerators could reorder groceries autonomously.

9. Challenges Ahead

Despite rapid progress, challenges persist. Many developing countries still face digital infrastructure gaps, internet connectivity issues, and limited financial literacy. Additionally, regulatory differences between countries complicate global payment interoperability.

There is also an ongoing debate about privacy and surveillance in digital payments, especially concerning CBDCs and data sharing. Balancing innovation, efficiency, and individual rights will be crucial as global payments continue to evolve.

10. Conclusion

The revolution in global payments represents far more than technological advancement—it symbolizes a transformation in how humanity exchanges value. From the days of barter and coins to instant digital transfers and decentralized currencies, payment systems have continuously adapted to the needs of global commerce and society.

Today’s payment revolution is breaking down economic barriers, fostering inclusion, and enabling a truly connected global economy. As technology continues to evolve—powered by blockchain, artificial intelligence, and open banking—the future of global payments promises to be faster, more inclusive, and more intelligent than ever before.

In essence, money is no longer just a medium of exchange—it has become a dynamic, digital ecosystem driving the next phase of global economic growth.

Startups Reshaping the Global Market1. The Startup Revolution: A Global Phenomenon

The startup ecosystem has evolved from being a niche community to a global economic force. Fueled by venture capital, digital connectivity, and technological progress, startups have transformed every sector—from finance and healthcare to transportation and energy. In many ways, they embody the spirit of the 21st-century economy: fast-moving, borderless, and data-driven.

Countries like the United States, India, Israel, China, and the United Kingdom have become major startup hubs, each contributing to the rise of global innovation. India, for instance, has over 100 unicorns (startups valued at over $1 billion), making it the third-largest startup ecosystem in the world. Similarly, regions in Africa, Latin America, and Southeast Asia are now producing startups that serve both local and international markets, contributing to inclusive global growth.

2. Technology as the Great Equalizer

One of the key factors enabling startups to reshape the global market is technology. The digital revolution has drastically lowered entry barriers for new businesses. Cloud computing, artificial intelligence (AI), blockchain, and the Internet of Things (IoT) have provided startups with tools to compete with global corporations without massive capital investments.

For example, fintech startups such as Revolut, Paytm, and Stripe have democratized financial services, enabling millions of unbanked or underserved people to access digital payments, loans, and investments. Similarly, Zoom and Slack revolutionized communication, empowering remote work and global collaboration.

These technological innovations not only improve efficiency but also reshape industries—blurring geographical boundaries and redefining what is possible in business and commerce.

3. Disruption Across Industries

Startups have introduced disruption as a permanent feature of global markets. They challenge established business models and force incumbents to innovate.

In transportation, companies like Uber, Lyft, and Grab transformed mobility through app-based ride-hailing, reshaping how people commute and think about car ownership.

In hospitality, Airbnb created a new asset-light model where ordinary homeowners could become hospitality providers, shaking up the hotel industry.

In retail, Shopify, Shein, and Temu have empowered small businesses and direct-to-consumer models, altering how brands reach global audiences.

In health tech, startups such as Practo, Teladoc, and Cure.ai have revolutionized telemedicine, diagnostics, and data-driven healthcare delivery.

This wave of disruption has compelled traditional players to adapt or perish. Giants like General Motors, Walmart, and even banks have been forced to adopt startup-like agility, investing heavily in innovation to remain competitive.

4. The Power of Data and AI

Artificial intelligence and data analytics have become the lifeblood of modern startups. With access to vast amounts of consumer data, startups can personalize experiences, predict trends, and automate processes.

For instance, Netflix and Spotify use algorithms to curate personalized entertainment experiences, reshaping how people consume content. Similarly, Bytedance (TikTok) leveraged AI-powered recommendation engines to redefine the global social media landscape.

Startups are not just using AI as a tool—they are shaping the ethics, regulation, and practical applications of AI across industries. Their innovations are influencing everything from healthcare diagnosis and logistics optimization to environmental monitoring and autonomous vehicles.

5. Globalization Through Digital Platforms

The internet has erased traditional boundaries, allowing startups to scale globally within months. Digital-first businesses such as Amazon, Alibaba, and Shopee have shown how online marketplaces can integrate suppliers, manufacturers, and consumers across continents.

Cloud-based services, digital payments, and e-commerce platforms have enabled startups in small nations to sell products and services globally. For example, a small design startup in Estonia or a fintech app in Nigeria can reach users in North America or Asia thanks to digital distribution and mobile technology.

This borderless expansion has also diversified global trade. Instead of being dominated by multinational giants, the digital economy now includes countless smaller, agile startups that serve specialized niches with global reach.

6. Sustainability and Social Impact Startups

In an era of environmental awareness and social responsibility, startups are also leading the charge toward sustainability. They are developing solutions that address climate change, waste management, renewable energy, and social inclusion.

Startups like Tesla, Beyond Meat, and Ola Electric have demonstrated how innovation can align profitability with sustainability. Similarly, Too Good To Go and Olio are tackling food waste through technology-driven community sharing models.

These startups represent a shift in global capitalism—from profit maximization to purpose-driven entrepreneurship. Investors, governments, and consumers now prioritize businesses that combine growth with environmental and social impact, reshaping the moral fabric of global markets.

7. Venture Capital and the Funding Ecosystem

Behind every successful startup lies an ecosystem of investors, incubators, and accelerators. Venture capital (VC) has played a critical role in nurturing innovation and scaling new ideas.

Global VC investments reached record highs in the 2020s, with firms like Sequoia Capital, SoftBank, and Andreessen Horowitz funding disruptive startups across continents. Beyond capital, these investors provide mentorship, networks, and strategic guidance.

Interestingly, new funding models such as crowdfunding and angel syndicates have democratized entrepreneurship. Today, even small investors can participate in early-stage funding, fostering a culture of innovation beyond traditional financial centers.

8. Startups and the Future of Work

Startups have redefined the workplace itself. They popularized flexible work cultures, remote operations, and gig-based employment. Platforms like Upwork, Fiverr, and Toptal have enabled millions of freelancers worldwide to participate in the digital economy.

The COVID-19 pandemic accelerated this trend, and startups were the first to adapt. They introduced tools and platforms that made remote work efficient and scalable. The result is a new global labor market—one that values skills over geography and innovation over hierarchy.

9. Challenges Facing Global Startups

Despite their success, startups face numerous challenges. Many struggle with scalability, regulatory compliance, and competition from well-funded incumbents. The global economic slowdown, fluctuating valuations, and rising interest rates have also made fundraising more difficult.

Moreover, startups that grow too fast without solid business fundamentals risk collapse—as seen in the cases of WeWork and FTX. Cybersecurity threats, data privacy issues, and talent retention further complicate the global expansion of startups.

Still, these challenges often fuel innovation. Startups continually evolve, learning from failures and adopting more sustainable growth models.

10. The Future: A Startup-Driven Global Economy

The influence of startups on the global market is only expected to grow. As emerging technologies such as quantum computing, biotech, and Web3 evolve, startups will continue to lead their commercialization. Governments are also recognizing the importance of fostering startup ecosystems, offering tax benefits, innovation grants, and infrastructure support.

In the coming decade, we can expect startups to drive the next wave of global economic transformation—creating smarter cities, cleaner energy systems, inclusive financial networks, and personalized digital services.

Conclusion

Startups are no longer the underdogs of the economy—they are its architects. Through relentless innovation, digital empowerment, and global collaboration, they are reshaping industries, societies, and the world economy itself.

From the smallest local app to the next global unicorn, startups symbolize the power of ideas in motion. As they continue to challenge the status quo and expand their reach, the global market will increasingly reflect their dynamism, creativity, and vision. In essence, the future of global trade and commerce is being written—not in boardrooms—but in the innovation labs, co-working spaces, and digital platforms of startups across the world.

Venture capital’s impact on the global trade marketHow VC affects global trade: the mechanisms

Financing innovation that changes traded goods and services.

VC funds back high-growth firms that commercialize new technologies — cloud computing, advanced manufacturing, fintech, biotech, logistics automation, and more. When those firms scale, they create new tradable goods and services (SaaS, precision-manufactured components, platform-enabled logistics). This changes the composition of trade: more intangible flows (software, data services, algorithms) and more niche high-value physical goods replace or complement traditional commodity exports.

Accelerating cross-border platformization.

Many VC-backed companies are platforms (marketplaces, payment networks, cloud providers) whose value increases rapidly with scale and cross-border adoption. Platforms reduce transaction costs for international trade — matching buyers and sellers, enabling payments, providing reputational signals, and coordinating logistics. As platforms spread, they lower entry barriers for SMEs to sell abroad, boosting smaller-scale cross-border commerce and diversifying trade flows.

Transforming supply chains and logistics.

VC funds startups that digitize procurement, inventory, freight matching, customs compliance, and last-mile delivery. Innovations such as real-time tracking, AI-driven demand forecasting, and digital freight marketplaces make supply chains more responsive and efficient, enabling just-in-time and cross-border manufacturing models that wouldn’t be feasible earlier. This increases the volume and complexity of trade while reducing friction and cost.

Enabling services trade and digital exports.

VC concentrates in sectors with low marginal-cost reproduction (software, digital media, professional services delivered online). This encourages countries and firms to export services rather than only goods. Digital exports scale quickly and change balance-of-trade dynamics: countries with strong VC ecosystems often become net exporters of digital services, platform access, and intellectual property.

Shifting where value is captured.

VC incentives — fast growth, winner-take-most dynamics — tend to cluster value capture into a handful of global hubs (Silicon Valley, Shenzhen, Berlin, Bengaluru). This concentration affects trade patterns: components and raw inputs might be sourced globally, but design, IP, and high-margin services concentrate in VC hubs, shifting where trade-related revenue accrues.

Mobilizing global capital and cross-border investment.

VC syndicates, limited partners, and crossover investors operate internationally. Cross-border VC flows channel capital into emerging markets, enabling local firms to scale for export and import substitution. Conversely, outbound VC by multinationals can seed ecosystems abroad that later integrate into global production networks.

Regional patterns and asymmetries

VC’s trade effects are uneven. Advanced economies with deep VC ecosystems tend to export high-value services, software, and specialized capital goods, while importing raw materials and standardized manufactured goods. Emerging markets often receive VC that helps them move up the value chain (e.g., fintech in Africa enabling cross-border remittances, or manufacturing startups in Southeast Asia adding localized tech to global supply chains). However, the scale and type of VC differ: early-stage consumer apps proliferate in populous markets, while deep-tech VC concentrates where research and IP protection exist.

Risks, distortions, and unintended consequences

Concentration and monopoly power.

VC’s “go big fast” model favors market concentration. Dominant platforms can extract rents, distort trade by locking sellers into their ecosystems, and raise barriers for competitors from other countries.

Short-termism and fragility.

Chasing growth sometimes prioritizes market share over sustainable trade relationships or resilient supply chains. VC-backed firms that expand rapidly but lack stable unit economics can fail, disrupting cross-border networks they had come to enable.

Uneven benefits and inequality.

Regions without VC access may be relegated to low-value segments of global value chains. Even within countries, VC-backed growth can widen gaps between digitally integrated exporters and traditional exporters.

Regulatory arbitrage and data flows.

VC-backed platforms often operate across jurisdictions with differing data, privacy, and competition rules. This can create regulatory tensions that affect trade in digital services and cross-border data transfers.

Overreliance on external capital.

Countries that depend on foreign VC inflows for digital export growth may be vulnerable to cyclical capital flows. A sudden retrenchment in global VC can stall export-oriented startups and compress trade.

Policy implications and responses

Invest in complementary assets.

Governments wanting to maximize trade benefits from VC should strengthen research institutions, IP frameworks, digital infrastructure, and skills training. These make local startups more likely to scale into export-capable firms.

Support inclusive access to VC and alternatives.

Programs to broaden investor access (local LPs, public co-investment, blended finance) can reduce regional disparities and keep value capture local. Supporting later-stage finance domestically helps startups mature without forced early exits.

Regulate to preserve competition and resilience.

Antitrust and data-governance policies should balance innovation incentives with prevention of monopolistic platform dominance that can distort trade. Similarly, policies encouraging supply-chain diversification and transparency improve resilience against startup failures.

Promote standards and cross-border agreements.

Trade agreements and harmonized digital regulations (data portability, e-invoicing, digital ID) reduce friction for VC-enabled cross-border services and platforms.

Mitigate risks of capital volatility.

Macroprudential tools, sovereign wealth participation in funds, or public venture vehicles can dampen boom-bust cycles that otherwise cascade into trade disruptions.

Conclusion

Venture capital significantly reconfigures global trade by financing innovations that change what is traded, how trade is organized, and who captures its value. Its power to accelerate platformization, digitization, and supply-chain optimization brings opportunities for growth, diversification, and inclusion — but it also concentrates value, introduces fragility, and can amplify inequalities without careful policy design. For countries and firms, the goal should be to harness VC’s dynamism while building institutions, regulations, and financing structures that spread benefits, preserve competition, and shore up the resilience of the global trade networks VC helps create.

Shipping, Freight, and Logistics in World Trade1. The Importance of Shipping in Global Trade

Shipping is the lifeline of international trade. Around 90% of world trade by volume is transported by sea, making maritime transport the most cost-effective and energy-efficient mode for moving large quantities of goods over long distances. Without global shipping, the modern economy would collapse—no country could sustain its industries or consumer demand without importing raw materials, energy, and manufactured products.

The shipping industry supports the global supply chain, linking developing nations that supply raw materials with developed economies that manufacture and consume finished goods. For instance, crude oil from the Middle East is transported to refineries in Asia and Europe, while electronics from East Asia are shipped to markets in North America and Africa. This interdependence underscores shipping’s role as the engine of globalization.

2. Understanding Freight in International Trade

Freight refers to the transportation of goods in bulk by various modes—sea, air, rail, or road. Freight services determine how products move from one point to another and how efficiently they reach their destinations. Freight is typically divided into three main categories:

Sea Freight – Used for large and heavy shipments, ideal for commodities such as oil, coal, grain, machinery, and vehicles. Containerization has revolutionized sea freight, enabling efficient and secure movement.

Air Freight – Offers the fastest mode of delivery, mainly for perishable or high-value items like electronics, pharmaceuticals, and luxury goods.

Land Freight (Rail and Road) – Connects ports to inland cities and neighboring countries, playing a vital role in regional trade and last-mile delivery.

Freight costs significantly affect product pricing and competitiveness in the global market. Efficient freight management reduces transportation costs and delivery times, making products more affordable and accessible.

3. The Role of Logistics in World Trade

Logistics refers to the planning, coordination, and management of the movement and storage of goods throughout the supply chain—from production to the final customer. It is the strategic process that integrates shipping and freight into a seamless operation.

Key elements of logistics include:

Transportation Management – Selecting the best mode of transport and optimizing routes.

Warehousing – Storing goods safely before they are distributed or sold.

Inventory Management – Ensuring supply meets demand without overstocking.

Customs Clearance – Handling documentation and compliance with international trade regulations.

Last-Mile Delivery – Delivering goods from distribution centers to consumers.

Modern logistics rely heavily on technology, including GPS tracking, warehouse automation, and data analytics, which provide real-time visibility and improve decision-making.

4. Evolution of Global Shipping and Logistics

The modern logistics industry has come a long way since the days of wooden ships and manual cargo handling. The container revolution in the 1950s, introduced by Malcolm McLean, transformed global trade. Standardized containers allowed goods to be loaded, shipped, and unloaded efficiently across ships, trains, and trucks, drastically reducing costs and time.

The digital revolution of the 21st century further enhanced logistics efficiency. Artificial intelligence, blockchain, and Internet of Things (IoT) technologies now streamline supply chains, track shipments in real time, and reduce human error. E-commerce giants like Amazon and Alibaba have set new standards in global logistics, emphasizing speed, reliability, and transparency.

5. Major Global Shipping Routes

World trade depends on critical maritime routes that connect producers and consumers. Some of the most vital shipping routes include:

The Suez Canal (Egypt): Links Europe and Asia via the Mediterranean and Red Seas.

The Panama Canal (Central America): Connects the Atlantic and Pacific Oceans, crucial for trade between the Americas and Asia.

The Strait of Malacca (Southeast Asia): One of the busiest routes connecting the Indian and Pacific Oceans.

The English Channel and Gibraltar Strait: Important for European trade.

Disruptions in these routes—such as the Suez Canal blockage in 2021—can cause massive delays and losses across global supply chains, showing how fragile yet essential maritime networks are.

6. Key Players in Global Shipping and Logistics

Several major companies dominate international shipping and logistics:

Shipping Lines: Maersk, MSC, CMA CGM, and COSCO handle millions of containers annually.

Freight Forwarders: DHL, FedEx, and Kuehne+Nagel provide end-to-end logistics solutions.

Port Operators: DP World, PSA International, and Hutchison Ports manage the world’s busiest ports.

Ports such as Shanghai, Singapore, Rotterdam, and Dubai’s Jebel Ali are global trade hubs, facilitating the import and export of goods worldwide.

7. Challenges Facing the Shipping and Logistics Industry

Despite its importance, the global shipping and logistics industry faces several challenges:

Supply Chain Disruptions: Events like the COVID-19 pandemic, wars, or natural disasters expose vulnerabilities in global supply chains.

Rising Fuel Costs: Shipping is heavily dependent on oil, and fluctuations in fuel prices directly affect freight rates.

Environmental Regulations: Pressure to reduce carbon emissions has forced the industry to invest in cleaner fuels and green technologies.

Port Congestion: Overcrowded ports lead to delays and increased costs, especially during peak trade periods.

Geopolitical Tensions: Trade wars and sanctions can reroute or restrict global shipping flows.

8. Green and Sustainable Shipping

Sustainability has become a key priority for the maritime industry. The International Maritime Organization (IMO) has set targets to reduce carbon emissions by 50% by 2050. Innovations such as LNG-powered ships, wind-assisted propulsion, and electric container vessels are being developed. Companies are also investing in carbon offset programs and exploring hydrogen fuel as a cleaner alternative.

Green logistics also focus on reducing waste, optimizing routes, and using eco-friendly packaging materials, contributing to a more sustainable global trade ecosystem.

9. The Future of Global Logistics

The future of logistics lies in automation, digitalization, and resilience. Emerging technologies are reshaping the industry:

Artificial Intelligence (AI): Enhances demand forecasting and route optimization.

Blockchain: Provides secure and transparent documentation for international transactions.

Autonomous Ships and Drones: Expected to revolutionize cargo transport and delivery.

Smart Ports: Use IoT sensors and data analytics to streamline operations.

Moreover, the rise of regional trade agreements and nearshoring (relocating production closer to consumers) is redefining supply chains to reduce risks and costs.

10. Conclusion

Shipping, freight, and logistics are the invisible engines powering world trade. They connect nations, support industries, and ensure that goods flow seamlessly across borders. As globalization deepens and technology advances, the logistics sector continues to evolve, balancing efficiency, sustainability, and resilience.

However, the challenges of environmental impact, geopolitical instability, and supply chain vulnerabilities demand innovation and cooperation. The future of global trade depends on a smarter, greener, and more adaptive logistics network—one capable of sustaining the demands of an interconnected world while protecting the planet for generations to come.

Successful Forex Trading1. Understanding the Forex Market

The forex market operates 24 hours a day, five days a week, across major financial centers like London, New York, Tokyo, and Sydney. Currencies are traded in pairs such as EUR/USD, GBP/JPY, or USD/INR, where one currency is bought while the other is sold.

Forex prices fluctuate due to various factors—economic indicators, geopolitical events, interest rate changes, and global demand for currencies. A successful trader understands that the forex market is influenced by both technical and fundamental dynamics.

2. The Foundation: Education and Knowledge

Knowledge is the backbone of successful forex trading. Before risking money, traders must learn how the market works, understand price action, and study trading tools. Beginners should grasp basic concepts such as:

Pips and lots: The smallest unit of price movement and standard trade size.

Leverage and margin: Borrowed capital that amplifies both profits and losses.

Bid-ask spread: The difference between the buying and selling price.

Stop-loss and take-profit: Tools to manage risk and lock in gains.

Reading books, taking courses, and following reliable market news sources like Bloomberg or Reuters can help traders stay informed. Continuous learning is vital, as market conditions and trading technologies evolve rapidly.

3. Developing a Solid Trading Strategy

A well-defined trading strategy is what separates successful traders from impulsive gamblers. Strategies can be short-term (scalping, day trading) or long-term (swing trading, position trading). Some of the popular trading strategies include:

Trend following – Identifying and trading in the direction of the market’s momentum.

Breakout trading – Entering trades when price moves beyond key resistance or support levels.

Range trading – Buying at support and selling at resistance during sideways markets.

News trading – Capitalizing on price volatility during major economic releases.

A successful trader tests strategies through backtesting (using historical data) and demo trading (using virtual money). This builds confidence before risking real funds.

4. Mastering Technical Analysis

Technical analysis helps traders forecast future price movements based on historical data. It involves studying charts, patterns, and indicators. Commonly used tools include:

Moving Averages (MA): To identify trends and smooth price fluctuations.

Relative Strength Index (RSI): To detect overbought or oversold market conditions.

Fibonacci Retracements: To identify potential reversal levels.

Candlestick Patterns: To reveal market sentiment through price behavior.

Technical analysis is most effective when combined with risk management and market psychology, rather than used in isolation.

5. Importance of Fundamental Analysis

While technical analysis focuses on charts, fundamental analysis examines the economic and political forces behind currency movements. Key indicators include:

Interest rates – Currencies with higher interest rates tend to attract more investors.

Inflation and GDP data – Indicate economic health and purchasing power.

Employment reports – Such as U.S. Non-Farm Payrolls, which can cause sharp volatility.

Geopolitical stability – Political crises can weaken a nation’s currency.

Successful traders often blend both technical and fundamental analysis to make informed trading decisions.

6. Risk Management: Protecting Capital

No matter how skilled a trader is, losses are inevitable. The key is to control risk so one bad trade doesn’t wipe out the account. Effective risk management includes:

Position sizing – Risking only 1–2% of trading capital per trade.

Stop-loss orders – Automatically closing trades at a predetermined loss level.

Diversification – Avoiding concentration in a single currency pair.

Avoiding over-leverage – High leverage amplifies both gains and losses.

Successful forex traders focus more on capital preservation than on quick profits. As the saying goes, “Take care of your losses, and profits will take care of themselves.”

7. The Psychology of Trading

Emotions are a trader’s biggest enemy. Fear and greed often lead to irrational decisions, like exiting trades too early or chasing losing positions. To succeed, traders must cultivate:

Discipline: Stick to the trading plan and rules consistently.

Patience: Wait for high-probability setups rather than forcing trades.

Confidence: Trust in analysis and avoid self-doubt after losses.

Emotional control: Accept losses as part of the process.

Maintaining a trading journal helps track performance, recognize emotional triggers, and improve over time.

8. Using Technology and Trading Tools

In today’s digital era, technology plays a massive role in forex trading success. Platforms like MetaTrader 4/5, cTrader, or TradingView offer real-time data, charting tools, and automated trading options.

Successful traders also use:

Economic calendars to track important news events.

Algorithmic trading systems for consistent execution.

VPS hosting to reduce latency for automated strategies.

Staying updated with fintech innovations gives traders a competitive edge in execution speed and market insight.

9. Continuous Improvement and Adaptation

The forex market is dynamic—strategies that worked yesterday may not work tomorrow. Therefore, traders must constantly adapt. Successful forex traders regularly:

Review past trades to learn from mistakes.

Refine strategies based on changing volatility or trends.

Stay updated on global economic developments.

Seek mentorship or community support to exchange insights.

Flexibility and adaptability ensure that traders survive both bullish and bearish cycles.

10. Building Long-Term Success

Successful forex trading is not about overnight riches—it’s about consistency, patience, and growth. The most successful traders:

Focus on steady returns rather than big wins.

Maintain discipline in both winning and losing streaks.

Keep records of all trades for analysis.

Continue to learn, adapt, and evolve with the market.

They treat trading as a business, not a hobby—an enterprise requiring planning, analysis, and emotional balance.

Conclusion

Success in forex trading is a journey that combines knowledge, discipline, strategy, and self-control. It’s not about predicting every market move but about managing risks and maximizing opportunities. A trader who focuses on education, follows a tested strategy, controls emotions, and practices sound risk management can thrive in the volatile world of forex.

The essence of successful forex trading lies in one rule: “Trade smart, not hard.” With persistence, patience, and proper planning, anyone can achieve consistent profitability and long-term success in the global forex market.

Forex Trading Secrets: The Hidden Keys of the Currency Market 1. Understanding the Core Mechanics of Forex

Before diving into strategies, it’s crucial to grasp how Forex truly works. Currencies trade in pairs, such as EUR/USD or USD/JPY, where one currency is bought while the other is sold. The movement of these pairs is driven by supply and demand, interest rate differentials, economic strength, and global political events.

Professional traders understand that the Forex market is not random — it responds to global economic forces and liquidity flows. The key secret is recognizing that Forex is a relative market — success depends not on whether a single economy is strong or weak, but how one performs relative to another.

2. The Power of Institutional Footprints

Retail traders often forget that big banks and institutions control 80% of Forex volume. These institutions move markets through large orders and sophisticated algorithms. They use tactics like stop-hunting, liquidity grabbing, and false breakouts to trap smaller traders.

A smart trader learns to read institutional footprints — areas where price repeatedly reverses or consolidates are often zones where large players enter positions. Watching for liquidity pools near major support and resistance levels can reveal where “smart money” is accumulating or distributing.

3. Mastering Technical Analysis — But With Simplicity

Most traders clutter their charts with too many indicators. Successful Forex traders rely on price action — the pure movement of price — rather than indicator overload.

Candlestick patterns, trendlines, and moving averages remain powerful tools when used wisely. The secret is to use confluence, or the alignment of multiple signals, before taking a trade. For example, if a bullish engulfing pattern appears at a long-term support zone along with an oversold RSI, that’s a higher-probability trade setup.

In short, simplicity beats complexity. The best traders use clear, minimal charts and focus on market structure, not prediction.

4. The Role of Fundamental Forces

Forex is heavily influenced by macroeconomic data such as inflation, GDP growth, interest rates, and employment figures. Central banks — especially the Federal Reserve, ECB, Bank of Japan, and Bank of England — play a dominant role in shaping currency direction.

The “secret” is to trade fundamental momentum, not news headlines. For instance, if the U.S. economy shows consistent strength and the Fed is hiking interest rates, the U.S. dollar tends to appreciate for months — not just during the news release.

Smart traders don’t chase volatility; they position themselves with the macro trend and ride long-term moves based on global monetary cycles.

5. The Secret of Risk Management

Risk management is perhaps the most guarded secret of professional trading. The best traders don’t win every trade; they protect capital so they can stay in the game.

Here are core risk rules:

Never risk more than 1–2% of your account on a single trade.

Always use a stop-loss to cap potential losses.

Calculate your risk-to-reward ratio — aim for at least 1:2, meaning you risk $1 to make $2.

Avoid overleveraging; high leverage can destroy an account quickly.

Remember: Forex success isn’t about being right all the time — it’s about making more on winners than you lose on losers.

6. Psychological Discipline — The Real Edge

Even with perfect analysis, traders often fail due to emotional trading. Fear, greed, and impatience are the true enemies of profit.

Winning traders cultivate discipline and emotional control. They follow their trading plan strictly, never revenge trade after losses, and avoid overconfidence after wins.

Keeping a trading journal is a secret weapon for developing discipline — it helps identify emotional patterns, bad habits, and areas for improvement.

In Forex, your mindset determines your success more than your strategy. As the saying goes, “Trading is 10% strategy and 90% psychology.”

7. The Power of Trading Plans and Backtesting

Every professional trader operates with a clear trading plan — a blueprint defining when to enter, exit, and manage trades. This plan includes:

Entry conditions (technical or fundamental signals)

Exit rules (take profit and stop loss)

Risk parameters

Market conditions to avoid (e.g., major news events)

Before going live, experts backtest their strategies using historical data to assess profitability. This process filters out weak setups and builds confidence. The secret here is consistency — following one well-tested method instead of jumping between strategies after every loss.

8. Liquidity Timing and Session Secrets

The Forex market operates across three main sessions: Asian, European, and U.S. Each has unique volatility and behavior.

The Asian session is typically slower and range-bound.

The London session brings high liquidity and strong trends.

The New York session overlaps with London, creating the most volatile moves of the day.

Seasoned traders know that the London-New York overlap (about 12:30 PM to 3:30 PM IST) offers the best opportunities for strong, sustained moves. Additionally, institutional traders often enter or exit positions around session opens — understanding these patterns can greatly improve timing.

9. Avoiding the Common Retail Traps

Most retail traders fail due to predictable mistakes:

Overtrading and using high leverage

Ignoring stop-losses

Trading during low-liquidity hours

Following social media “gurus” or random signals

Lacking patience for long-term growth

The secret is to trade like a business, not a lottery. Treat capital as inventory, risk as cost, and profits as sustainable growth. Focus on consistency, not overnight success.

10. Continuous Learning and Adaptation

The final secret of Forex mastery is lifelong learning. The market evolves as economies, technology, and monetary policies change. Even the best traders constantly adapt their systems.

Follow economic news, study macroeconomic trends, and refine strategies through experience. Many professionals also use algorithmic tools or AI-driven indicators to enhance precision — but they still rely on human judgment for execution.

The best traders stay students of the market forever. They don’t seek shortcuts; they seek understanding.

Conclusion: The Real Secret Behind Forex Success

In truth, there are no “magic” Forex secrets — only disciplined principles practiced consistently. Success comes from combining technical clarity, macro awareness, emotional discipline, and risk control.

The world’s top traders don’t predict the market — they react intelligently to what it shows. They know when to trade, when to wait, and when to walk away.

The real secret is patience and mastery of self. Once you control your emotions, respect risk, and understand market behavior, the Forex market becomes not a mystery — but a mirror reflecting your own discipline and intelligence.

In the end, Forex trading is not about beating the market — it’s about mastering yourself within it.

Spotting Inefficiencies in an Efficient MarketMarket Efficiency Theory;

Core Idea: Stock prices already include and reflect all available information.

Implication: It is very difficult (if not impossible) to consistently outperform the market because prices adjust quickly when new information appears.

Note: Markets are not perfectly efficient all the time — they can become inefficient in the short term due to emotions, news, or sudden events.

⚙️ Three Forms of Efficiency

Weak Form Efficiency

All past market prices and data are already reflected in current prices.

Therefore, technical analysis (chart patterns, trends) is useless because it can’t predict future prices.

Semi-Strong Form Efficiency

All public information (both technical and fundamental) is reflected in prices.

This means fundamental analysis (using financial statements, news, etc.) is also useless for gaining an edge.

Strong Form Efficiency

All information, including insider or private information, is already priced in.

So, no one can consistently outperform the market — not even insiders.

💡 Why Inefficiencies Exist

Markets aren’t perfectly efficient because human behavior and emotions often cause mispricing:

Investor emotions — Fear and greed can drive irrational buying or selling.

Market sentiment extremes — Overconfidence or panic can push prices too far.

Short-term behavioral mistakes — Herd mentality or cognitive biases lead to temporary inefficiencies.

🔍 Finding Inefficiencies

Although hard, traders can sometimes find and exploit short-lived inefficiencies:

Market sentiment indicators like VIX (volatility index) or put/call ratios signal extremes.

Seasonal trading strategies such as “Sell in May” patterns or year-end rallies.

Time arbitrage — taking advantage of short-term market overreactions.

Exploiting short squeezes when traders betting against a stock are forced to buy back.

⚠️ Difficult Markets for Traders

Some markets are naturally harder to trade efficiently:

Forex market: Highly competitive with huge volumes and professional players.

Commodities market: Often volatile and erratic due to unpredictable factors like weather, geopolitics, or demand shocks.

Conclusion:

Is it possible to find inefficiencies in the markets?

The markets are probably to a certain degree efficient, but we believe you can make good and consistent returns by using the right approach – which is to use empirical and quantified data for short-term strategies and by using common sense. Moreover, we believe the best place to start is in the stock market.

The markets are somewhat inefficient because of human folly. This is unlikely to change, which is good for the rational trader and investor. So the correct answer about inefficiencies is this: Yes, it’s possible to find inefficiencies in the markets.

Effects of Currency Wars on Forex MarketsIntroduction

Currency wars—also known as competitive devaluations—occur when countries deliberately devalue their currencies to gain trade advantages, stimulate exports, and support domestic economic growth. The term “currency war” was popularized in 2010 by Brazil’s Finance Minister Guido Mantega, who warned of nations engaging in deliberate exchange rate manipulation. In the modern forex (foreign exchange) market, where over $7 trillion is traded daily, the implications of such actions are vast and deeply interconnected with global economic stability.

This essay explores the origins, mechanisms, and multifaceted effects of currency wars on forex markets, examining both short-term and long-term consequences for traders, investors, and national economies.

1. Understanding Currency Wars

A currency war takes place when a country intentionally lowers the value of its currency relative to others to make its exports cheaper and imports costlier. The logic is straightforward: a weaker currency helps boost exports by making goods more affordable to foreign buyers, which can support domestic industries and job creation. However, it simultaneously raises import prices, which can lead to inflationary pressures.

Currency wars can emerge through monetary policy tools, such as:

Quantitative easing (QE): Central banks inject liquidity into the economy by purchasing government bonds, indirectly weakening the currency.

Interest rate cuts: Lowering interest rates makes the currency less attractive to foreign investors seeking higher yields, reducing demand.

Foreign exchange interventions: Direct buying or selling of foreign currencies to influence exchange rates.

While such policies can serve domestic goals, they often have international repercussions—triggering countermeasures from other nations and volatility in forex markets.

2. Historical Context of Currency Wars

Currency wars are not new phenomena. Understanding their history helps illustrate how they shape forex market dynamics:

1930s: The Great Depression Era

Many countries, including the U.S. and Britain, abandoned the gold standard and devalued their currencies to promote exports. This led to competitive devaluations, trade barriers, and worsened global economic conditions.

1980s: The Plaza Accord (1985)

In response to a strong U.S. dollar that was hurting American exports, major economies (U.S., Japan, Germany, France, and the U.K.) agreed to coordinate currency interventions to weaken the dollar.

Post-2008 Financial Crisis:

With the global financial meltdown, central banks worldwide adopted aggressive monetary easing policies. The U.S. Federal Reserve’s quantitative easing led to accusations of a “new currency war,” as emerging markets faced unwanted capital inflows and exchange rate appreciation.

These historical examples show how currency manipulation can trigger chain reactions in forex markets and global trade balances.

3. Mechanisms Through Which Currency Wars Affect Forex Markets

Currency wars impact forex markets through multiple transmission channels:

a. Exchange Rate Volatility

When countries engage in competitive devaluations, exchange rates fluctuate dramatically. For instance, if Japan devalues the yen through monetary easing, the U.S. dollar may appreciate, prompting other countries to adjust policies in response. This constant tug-of-war leads to instability in forex markets, affecting traders’ confidence and investment planning.

b. Capital Flows and Investor Behavior

Investors seek safe havens when volatility rises. During currency wars, capital often flows into stable currencies such as the U.S. dollar (USD), Swiss franc (CHF), or Japanese yen (JPY). This movement can distort global capital distribution, cause currency misalignments, and even impact emerging markets through capital flight.

c. Trade Balances

A nation’s trade balance is directly influenced by exchange rate movements. While a weaker currency may boost exports, if multiple countries devalue simultaneously, the competitive advantage disappears, leading to a “race to the bottom.” This disrupts global trade dynamics and can reduce overall demand for goods and services.

d. Inflationary and Deflationary Pressures

Currency devaluation raises the price of imported goods, leading to inflation. Conversely, countries facing appreciation (due to other nations’ devaluation) may experience deflationary pressures. Forex markets adjust accordingly, pricing in expectations of future central bank actions to control inflation or deflation.

4. Short-Term Effects on Forex Trading

In the short term, currency wars create fertile ground for traders seeking profit opportunities, but they also heighten risks.

a. Increased Market Volatility

Forex traders often witness sharp intraday moves during periods of competitive devaluation. For example, central bank announcements or interventions can cause sudden spikes in currency pairs, such as USD/JPY or EUR/USD, leading to both profit opportunities and losses for leveraged traders.

b. Speculative Positioning

Speculators in forex markets often take advantage of anticipated devaluations. If the market expects the euro to weaken due to the European Central Bank’s dovish stance, traders may short the EUR/USD pair. Such speculative flows can accelerate the very devaluation that policymakers seek to manage.

c. Safe-Haven Demand

During currency wars, uncertainty drives investors toward stable assets—gold, U.S. Treasury bonds, and safe-haven currencies like the CHF or JPY. This shifts forex demand patterns and alters global capital distribution temporarily.

5. Long-Term Effects on Forex Markets

While short-term volatility defines immediate reactions, long-term effects reshape global economic relationships and trading patterns.

a. Shifts in Currency Valuations

Prolonged currency wars may lead to sustained undervaluation or overvaluation of certain currencies. Persistent intervention by central banks (e.g., China’s managed yuan policy) can distort true market equilibrium, leading to imbalances that eventually correct violently.

b. Structural Changes in Forex Market Dynamics

Currency wars can encourage nations to diversify away from traditional reserve currencies. For instance, emerging economies may reduce reliance on the U.S. dollar and increase holdings in other currencies or commodities (like gold). This diversification affects long-term forex flows and liquidity distribution.

c. Impact on Global Confidence

Persistent currency manipulation undermines faith in fair trade and stable exchange rate mechanisms. Traders and multinational corporations face higher hedging costs to protect against unpredictable currency swings, making long-term contracts and investments riskier.

d. The Rise of Regional Currencies

As global currency tensions rise, regional trade blocs often move toward establishing independent payment systems or regional currencies to reduce exposure to forex volatility. The European Union’s euro and proposed BRICS currency are prime examples.

6. Case Studies of Currency Wars and Their Forex Impact

a. Japan’s Yen Devaluation (2012–2013)

Under “Abenomics,” Japan implemented massive quantitative easing to fight deflation and stimulate growth. The yen weakened sharply, boosting exports but triggering retaliatory rhetoric from other economies. The USD/JPY pair saw unprecedented volatility, attracting global forex traders and speculative capital inflows.

b. China’s Yuan Policy (2015–2019)

China’s central bank allowed a sudden yuan devaluation in 2015, sending shockwaves through forex markets. The move was seen as an attempt to boost exports amid slowing growth. The USD/CNY surged, global markets sold off, and emerging currencies weakened, reflecting how one nation’s policy can ripple across global forex systems.

c. U.S. Dollar Strength Post-QE (2014–2018)

When the Federal Reserve began tapering its QE program and raising interest rates, the dollar strengthened significantly. This created global capital outflows from emerging markets, which had previously benefited from U.S. liquidity. Forex markets saw heavy pressure on emerging currencies like the Indian rupee (INR), Turkish lira (TRY), and Brazilian real (BRL).

7. Implications for Traders and Investors

Currency wars reshape trading strategies, risk management, and portfolio allocation:

Hedging Becomes Crucial: Businesses and investors use derivatives—like forward contracts and options—to protect against currency risk.

Shift Toward Short-Term Trading: Increased volatility encourages short-term speculative trading rather than long-term investing.

Greater Dependence on Central Bank Guidance: Traders closely monitor policy statements, interest rate decisions, and quantitative easing announcements for cues on currency direction.

Diversification Across Currencies: Investors spread risk across multiple currency pairs to hedge against sudden policy shocks.

8. Policy and Regulatory Consequences

Central banks and international bodies often step in to prevent prolonged currency wars. The International Monetary Fund (IMF) and World Trade Organization (WTO) advocate for coordinated monetary policies to maintain global stability. Unchecked currency devaluations can lead to retaliatory tariffs, protectionism, and a breakdown of cooperative trade relations.

For instance, during the 2010–2013 currency tensions, the G20 nations agreed to refrain from “competitive devaluations,” emphasizing that monetary policies should focus on domestic stability rather than exchange rate manipulation. However, adherence remains inconsistent, especially during economic downturns.

9. Emerging Technologies and Currency Wars

In recent years, digital currencies and fintech have introduced new dimensions to currency competition. Central Bank Digital Currencies (CBDCs), like China’s digital yuan, could shift global forex dynamics by reducing dependency on traditional payment networks dominated by the U.S. dollar.

Moreover, cryptocurrencies like Bitcoin offer an alternative asset class immune to direct government manipulation, though their volatility makes them less suitable for trade settlements. As digital currencies grow, they could potentially neutralize some of the destabilizing effects of traditional currency wars.

10. The Future of Currency Wars and Forex Markets

As globalization deepens and economies become more interdependent, the consequences of currency wars grow more complex. Future conflicts may not involve overt devaluations but subtle forms of monetary manipulation—like prolonged negative interest rates or unconventional liquidity injections.

Traders and policymakers must adapt to an environment where monetary policy divergence, digital innovation, and geopolitical competition define forex market trends. Collaborative frameworks between major economies will be essential to prevent destructive cycles of devaluation that could undermine global economic recovery.

Conclusion

Currency wars are powerful forces that shape the global forex landscape, influencing everything from short-term market volatility to long-term investment flows. While devaluation can serve as a tool for economic recovery, uncoordinated competitive policies can trigger instability, inflation, and loss of global trust.

For forex traders, currency wars present both opportunities and risks—volatile price movements can yield profits but demand vigilant risk management. For policymakers, the challenge lies in balancing national interests with global stability.

In the interconnected world of modern finance, no currency moves in isolation. A single policy decision in Washington, Tokyo, or Beijing can reverberate across markets worldwide—reminding us that in a currency war, there are rarely true victors, only shifting tides in the global economic battlefield.

Reserves and Their Role in Controlling InflationIntroduction

Inflation — the sustained rise in the general price level of goods and services — is a central concern for every economy. When prices rise too quickly, purchasing power declines, savings lose value, and economic uncertainty increases. To manage inflation, policymakers and central banks rely on several tools, and reserves play a crucial role among them.

Reserves, in an economic and financial sense, refer to the assets or holdings that a central bank or a nation keeps to stabilize its currency, support the banking system, and influence liquidity in the economy. They are the backbone of monetary policy — providing a safety net during crises and a lever to control inflationary or deflationary pressures.

This article explores what reserves are, the types of reserves, how they interact with the broader economy, and most importantly, how they are used as instruments to control inflation.

1. Understanding Reserves

1.1 Definition

Reserves are the portion of assets that financial institutions or nations hold and do not actively circulate in the economy. They are typically kept in the form of:

Foreign exchange reserves (foreign currencies, gold, IMF Special Drawing Rights)

Bank reserves (funds held by commercial banks with the central bank)

Strategic reserves (such as oil or commodities held by governments for stability)

Monetary reserves (central bank’s holdings that back the issuance of currency)

In the context of inflation control, foreign exchange reserves and bank reserves are most relevant.

2. Types of Reserves and Their Economic Importance

2.1 Bank Reserves

Bank reserves refer to the cash or deposits that commercial banks hold with the central bank. These reserves are essential for meeting withdrawal demands, ensuring liquidity, and adhering to regulatory requirements.

Required Reserves: The minimum percentage of deposits that banks must hold and not lend out, set by the central bank.

Excess Reserves: Any reserves that banks hold beyond the required minimum.

2.2 Foreign Exchange Reserves

Foreign exchange reserves are assets held by a central bank in foreign currencies. These reserves include:

U.S. dollars, euros, or yen

Gold holdings

IMF’s Special Drawing Rights (SDRs)

These reserves help stabilize a nation’s currency and manage exchange rate volatility, both of which directly affect inflation levels.

2.3 Strategic Reserves

Governments often maintain reserves of essential commodities like crude oil, food grains, and fertilizers. These strategic reserves protect the economy from supply shocks, which could lead to cost-push inflation if shortages occur.

3. How Reserves Influence Inflation

Reserves act as a monetary control mechanism. By adjusting reserve requirements, managing liquidity, and using foreign reserves strategically, a central bank can control money supply — the key driver of inflation.

3.1 The Link Between Money Supply and Inflation

According to the Quantity Theory of Money, expressed as:

MV = PQ

Where:

M = Money supply

V = Velocity of money

P = Price level

Q = Output

If money supply (M) increases faster than economic output (Q), prices (P) rise — leading to inflation.

Hence, controlling money supply via reserves becomes a vital anti-inflationary tool.

4. Mechanisms: How Reserves Help Control Inflation

4.1 Reserve Requirement Ratio (RRR)

The reserve requirement is the percentage of deposits that banks must hold with the central bank and cannot lend.

When inflation is high, central banks increase the reserve ratio, reducing banks’ capacity to lend.

→ This decreases money supply and dampens spending, cooling inflation.

When inflation is low or the economy is slowing, the ratio is reduced to encourage lending and spending.

For example, if the Reserve Bank of India (RBI) raises the Cash Reserve Ratio (CRR), commercial banks have less liquidity to issue new loans, thereby reducing credit growth and inflationary pressure.

4.2 Open Market Operations (OMO)

Central banks use reserves to buy or sell government securities:

Selling securities → absorbs liquidity → reduces money supply → controls inflation.

Buying securities → injects liquidity → increases money supply → combats deflation.

Thus, OMOs are a dynamic way of using reserves to regulate inflation without drastic policy shifts.

4.3 Managing Foreign Exchange Reserves

Foreign reserves can indirectly control inflation through exchange rate management:

When a currency depreciates, import prices rise, increasing inflation (imported inflation).

Central banks can use foreign reserves to buy their own currency, strengthening it and reducing inflationary pressure.

Conversely, when inflation is low, the central bank may allow the currency to weaken slightly to boost exports and growth.

4.4 Sterilization Policy

When a country experiences large foreign capital inflows, it increases domestic money supply and may fuel inflation.

To counter this, central banks conduct sterilization — selling government securities to absorb the excess liquidity created by foreign inflows.

4.5 Interest Rate Adjustments Using Reserves

Reserves influence interbank liquidity, which affects interest rates.

When reserves are high, liquidity is ample, and short-term rates fall — boosting spending.

To control inflation, the central bank may reduce liquidity (through higher CRR or OMO sales), pushing up rates and discouraging borrowing.

5. Case Studies: Reserves in Action

5.1 India – Reserve Bank of India (RBI)

The RBI actively uses CRR and Statutory Liquidity Ratio (SLR) to control inflation.

For instance:

During the 2010–2011 period, when inflation crossed 9%, RBI raised CRR to restrict liquidity.

Conversely, in 2020 (pandemic period), RBI reduced CRR from 4% to 3% to ease liquidity and support economic recovery.

Additionally, RBI manages over $650 billion in forex reserves, which it uses to stabilize the rupee and prevent imported inflation caused by a depreciating currency.

5.2 United States – Federal Reserve System

The U.S. Federal Reserve influences inflation through reserve balances and open market operations.

During high inflation (e.g., post-2021 pandemic period), the Fed reduced excess reserves in the banking system through Quantitative Tightening (QT) — selling bonds and raising interest rates to control money supply.

5.3 China – People’s Bank of China (PBOC)

China maintains one of the world’s largest foreign exchange reserves (over $3 trillion).

It uses these reserves to:

Stabilize the yuan’s exchange rate

Control import-export price volatility

Manage inflation driven by currency movements

6. Relationship Between Reserves and Exchange Rate Stability

Exchange rate stability is directly linked to inflation control.

A strong domestic currency reduces the cost of imported goods and keeps inflation low.

A weak currency, on the other hand, makes imports expensive, triggering inflation.

By holding substantial forex reserves, central banks can intervene in currency markets — buying or selling domestic currency to maintain a stable exchange rate and prevent inflationary shocks.

7. The Role of Gold and Commodity Reserves

Gold reserves historically backed national currencies and still act as a hedge against inflation.

When inflation rises globally and fiat currencies lose value, central banks often increase gold reserves to preserve asset value and stability.

Similarly, commodity reserves like oil and grains help governments buffer supply-side shocks, which are a major cause of inflation spikes (e.g., oil crises or food shortages).

8. Challenges and Limitations

While reserves are powerful tools, their use in inflation control faces several challenges:

8.1 Limited Effectiveness in Supply-Side Inflation

Reserves can control demand-pull inflation (caused by excessive spending) but are less effective against cost-push inflation (caused by supply shocks like oil price hikes).

8.2 Risk of Over-tightening

Excessive tightening through high reserve requirements or OMO sales can stifle credit growth and economic expansion, leading to recession.

8.3 Foreign Exchange Volatility

Using forex reserves for inflation control via currency stabilization can deplete reserves quickly if global market pressures persist.

8.4 Sterilization Cost

Sterilization operations (offsetting capital inflows) can be expensive and may strain central bank balance sheets.

9. Coordinated Use of Reserves and Other Tools

For effective inflation management, reserves are used in conjunction with:

Interest rate policy

Fiscal discipline

Supply-side reforms

Targeted liquidity management

A well-coordinated monetary-fiscal framework ensures that reserves act as a stabilizing force rather than a reactive one.

10. Future Outlook: Reserves and Inflation in the Global Economy

In today’s interconnected world, inflation control is not just a domestic concern.

Global commodity prices, exchange rate fluctuations, and capital flows can all influence inflation levels.

As digital currencies, blockchain-based payment systems, and cross-border trade evolve, the composition and management of reserves will also transform.

Central banks may diversify away from traditional reserves like the U.S. dollar and hold multi-currency baskets, digital assets, or even climate-linked reserves to ensure sustainable control of inflation.

Conclusion

Reserves — whether held by central banks, governments, or financial institutions — form the foundation of monetary stability. They serve as both a defensive shield and an active instrument in combating inflation.

By managing bank reserves, foreign exchange holdings, and strategic commodities, policymakers can influence liquidity, exchange rates, and overall price stability.

However, the effectiveness of reserves depends on timely policy coordination, global conditions, and domestic fiscal discipline.

In essence, reserves are not merely a pile of assets — they are a reflection of a nation’s economic strength, policy credibility, and capacity to maintain price stability. Through prudent reserve management, central banks can ensure sustainable growth while keeping inflation under control — achieving the delicate balance every economy strives for.

Fundamental Analysis and Technical Analysis in the Forex Market1. Understanding the Forex Market

Before diving into the analytical methods, it’s important to grasp the nature of the forex (foreign exchange) market. Forex trading involves the simultaneous buying of one currency and selling of another — for example, buying the EUR/USD means buying euros while selling U.S. dollars.

Unlike stock markets that focus on individual companies, forex prices reflect macroeconomic conditions and the relative strength of nations’ economies. Therefore, both economic fundamentals and market psychology play vital roles in determining currency values.

2. What Is Fundamental Analysis in Forex?

2.1 Definition and Core Idea

Fundamental analysis in the forex market focuses on evaluating a country’s economic, financial, and political factors to determine the intrinsic value of its currency. It seeks to answer the question: “Is a currency undervalued or overvalued compared to another?”

Just as stock analysts study company balance sheets, forex traders study national balance sheets — economic growth rates, employment levels, inflation, trade balances, and monetary policies. These elements influence the demand and supply for currencies and ultimately drive long-term exchange rate trends.

3. Key Components of Fundamental Analysis

3.1 Economic Indicators

Economic indicators provide measurable data about an economy’s performance. Forex traders pay close attention to these releases because they directly impact currency strength.

Gross Domestic Product (GDP): A strong GDP growth rate indicates a healthy economy, attracting foreign investment and strengthening the currency.

Inflation Data (CPI, PPI): Central banks adjust interest rates based on inflation trends. Rising inflation often leads to higher rates, boosting currency value.

Employment Reports: Data like the U.S. Non-Farm Payroll (NFP) report shows labor market health. Higher employment typically signals economic expansion.

Retail Sales and Consumer Confidence: These reflect domestic demand and overall economic optimism.