Liquidity in Trading: The Basics You Must Understand👉 If you can’t identify liquidity, you become the liquidity.

It's not an indicator, It's not a pattern. It's not a theory.

It's how the markets actually move.

Every trader has seen it happen: you take a position at the “obvious” level, only to get stopped out by a quick wick — and then the market runs exactly where you expected. That wasn’t bad luck. That was liquidity.

In this post, you’ll learn few main forms of liquidity that move markets and how to avoid being stop hunted and actually use such a phenomena for your advantage.

Don't be a liquidity

Price doesn’t move randomly inside ranges. It hunts liquidity at the edges.

• Retail trap: Traders pile orders right at the range high/low.

• Smart money: Hunt's edges of range before starting the move.

Wait for the sweep of those levels. The stop runs happen first, the real move comes after.

⚠️ If a pivot level gets tapped multiple times, it's on purpose. Smart money are creating illusion of strong support / Resistance.

Les informed traders trades patterns like : Double bottom, Double top and they put the stop losses above the range - This creates a Liquidity cluster which smart money needs to execute their orders. They will come for it before the real move happen.

How to enter continuation

Even in strong trends, price doesn’t move in straight lines.

• Consolidation → Expansion: Liquidity builds during pullbacks or sideways pauses, then gets released in a sharp move.

• Retracement → Expansion: don’t chase the first pullback. Wait for at least 50% pullbacks. Not earlier. Best setup is when it has all like the one below.

Double top as liquidity, range, 50% pullback , stop hunt

• Double tops and Triple tops are engendered liquidity if you see it expect price go thru that levels

The win isn’t catching the exact bottom. It’s catching a clean entry with strong Trend continuation - low timeframe reversal and with right timeframe allignements.

So here is again GBPUSD example where we had the weekly range, stop hunt to 50% of the swing.

After stop hunt occurs you wait for. H4 OB being created in other words engulf of last bulky down candle and clean close above. Then you can enter with SL below the stop hunted lows, not only that traders was liquidated there but also another group of traders entered shorts and they will be now liquidated above that double top and its your target.

Importance of key level

Even when smart money moves price to the highs where it seems there is not key level always look left price mostly stop just right above or below the key level. Ranges for some time makes false move in the direction which sucks traders in to to a trade and then they hit key level and go that direction.

If the move is not going from key level it's a trap. We can use many types of levels, but here is a tip for the forex Whole, quarter, half levels are strong. If your order block, supply / demand occurs or classic support occurs around that level it will have higher probability and its not because of psychological level. It's because these levels are what institutions are trading.

Stop hunts are not your enemy — unless you ignore it. The market makers hunts liquidity before it moves. By starting thinking about the markets this was way you will recognize and will be able to visualize future movements.

Summary

Big challenge is waiting patiently for the stop hunt to happen. And yes sometimes price moves without a stop hunt and you will miss a move. But it's always better not to be in a trade you want to be than being In trade you dont want to be.

Shift from being the exit liquidity to being the trader who patiently waits, confirms, and executes with precision.

🩸 Spot the trap. 🩸 Wait for the sweep. 🩸 Trade with intention.

Dont trust me and fact check this on your chart for your confidence. It's only way to start to see markets differently.

David Perk aka Dave FX Hunter

X-indicator

Commodity Futures Trading in the Global Market1. Historical Evolution of Commodity Futures Trading

Ancient Trading Roots

Commodity trading dates back thousands of years, with evidence from Mesopotamia and Ancient Greece showing contracts for the future delivery of crops.

In Japan during the 17th century, rice futures were traded at the Dojima Rice Exchange, one of the earliest organized futures markets.

The Chicago Board of Trade (CBOT)

Established in 1848, CBOT standardized forward contracts into formal futures contracts.

Grain farmers in the U.S. Midwest needed to protect themselves against unpredictable prices, while buyers wanted stable supply at predictable rates.

Futures contracts solved this by locking in future delivery prices, reducing uncertainty.

Expansion to Other Commodities

After grains, futures expanded to include livestock, metals, energy, and eventually financial instruments like currencies and interest rates.

By the late 20th century, futures markets had become central not just to commodities but also to global finance.

2. Fundamentals of Commodity Futures

What is a Futures Contract?

A futures contract is a standardized agreement to buy or sell a commodity at a specific price on a future date, traded on an organized exchange.

Key features:

Standardization – Each contract specifies quantity, quality, and delivery terms.

Margin and Leverage – Traders post margin (collateral) to participate, giving them leverage.

Clearinghouses – Ensure counterparty risk is minimized.

Expiration & Settlement – Contracts either settle physically (delivery of the commodity) or financially (cash-settled).

Types of Commodities Traded

Agricultural Commodities – Wheat, corn, soybeans, coffee, sugar, cotton.

Energy Commodities – Crude oil, natural gas, gasoline, heating oil.

Metals – Gold, silver, copper, aluminum, platinum.

Soft Commodities – Cocoa, rubber, palm oil.

3. Key Participants in Global Commodity Futures

1. Hedgers

Farmers, miners, oil producers, airlines, and manufacturers use futures to protect against price volatility.

Example: An airline buys jet fuel futures to lock in prices and protect against oil price spikes.

2. Speculators

Traders who take positions based on price expectations, seeking profits rather than delivery.

Provide liquidity to the market but also increase volatility.

3. Arbitrageurs

Exploit price discrepancies across markets or between spot and futures prices.

Help align prices globally.

4. Institutional Investors

Hedge funds, mutual funds, pension funds use commodity futures for diversification and inflation hedging.

5. Market Makers & Brokers

Facilitate transactions, ensuring continuous liquidity.

4. Global Commodity Futures Exchanges

United States

Chicago Mercantile Exchange (CME Group) – World’s largest futures exchange, trading agricultural, energy, metals, and financial futures.

New York Mercantile Exchange (NYMEX) – Key hub for energy futures like crude oil and natural gas.

Intercontinental Exchange (ICE) – Specializes in energy and soft commodities like coffee, cocoa, and sugar.

Europe

London Metal Exchange (LME) – Benchmark for industrial metals like copper, aluminum, and nickel.

Euronext – Trades agricultural and financial futures in Europe.

Asia

Shanghai Futures Exchange (SHFE) – Major player in metals, energy, and chemicals.

Multi Commodity Exchange of India (MCX) – Leading Indian commodity exchange.

Tokyo Commodity Exchange (TOCOM) – Focuses on energy, metals, and rubber.

Singapore Exchange (SGX) – Emerging hub for global commodities, especially Asian benchmarks.

5. Mechanics of Commodity Futures Trading

1. Opening a Position

Long position (buy futures) if expecting prices to rise.

Short position (sell futures) if expecting prices to fall.

2. Margin System

Initial margin: Upfront collateral to open a position.

Maintenance margin: Minimum balance required.

Daily mark-to-market adjusts accounts based on price movements.

3. Settlement Methods

Physical delivery: Actual exchange of the commodity.

Cash settlement: Price difference settled in cash, common for financial futures.

4. Price Discovery

Futures markets reflect expectations of supply and demand.

Example: Rising oil futures may signal geopolitical risks or expected shortages.

6. Importance of Commodity Futures in the Global Economy

1. Risk Management

Producers and consumers hedge against adverse price swings.

2. Price Discovery

Futures prices act as benchmarks for global trade.

Example: Brent crude futures influence oil prices worldwide.

3. Market Liquidity

Continuous trading provides deep liquidity, enabling efficient transactions.

4. Economic Indicators

Futures prices offer insights into future economic trends (e.g., rising copper prices suggest industrial growth).

7. Challenges and Criticisms

1. Speculative Excess

Excessive speculation can cause price bubbles, hurting real producers and consumers.

Example: 2008 oil price surge partly attributed to speculative trading.

2. Volatility & Market Shocks

Futures markets can amplify volatility, especially during geopolitical or weather-related events.

3. Market Manipulation

Large players can influence prices (e.g., "cornering the market").

4. Regulatory Concerns

Need for global harmonization as futures markets are interconnected.

8. Regulation of Global Commodity Futures

United States

Commodity Futures Trading Commission (CFTC) oversees futures and options markets.

Europe

European Securities and Markets Authority (ESMA) sets regulations under MiFID II.

Asia

Each country has its regulator: SEBI (India), CSRC (China), FSA (Japan).

Global Cooperation

IOSCO (International Organization of Securities Commissions) works on harmonizing standards.

9. Technological Transformation in Commodity Futures

Electronic Trading

Transition from open-outcry trading floors to electronic platforms like CME Globex.

Algorithmic & High-Frequency Trading (HFT)

Now dominate volumes, enabling faster price discovery but raising flash crash risks.

Blockchain & Smart Contracts

Potential to streamline settlement, reduce fraud, and improve transparency.

10. Case Studies

Oil Futures (NYMEX WTI & ICE Brent)

Key benchmarks for global crude oil pricing.

The 2020 COVID-19 crisis saw WTI futures turn negative, highlighting the complexities of storage and physical delivery.

Gold Futures (COMEX)

A hedge against inflation and financial instability.

Demand spikes during geopolitical crises or economic uncertainty.

Agricultural Futures (Chicago Board of Trade)

Corn, wheat, and soybean futures directly impact global food prices.

Conclusion

Commodity futures trading is more than just speculation—it is the nervous system of the global economy. From farmers securing prices for their harvest to airlines hedging jet fuel, and from speculators driving liquidity to regulators ensuring stability, futures markets are indispensable.

They provide transparency, risk management, and global price discovery. Yet they also bring challenges of volatility, speculation, and regulatory complexity.

Looking ahead, technological innovation, sustainability concerns, and the rise of emerging markets will reshape global commodity futures trading. Its importance will only grow as commodities remain the backbone of human survival, industrialization, and energy security.

Exchange-Traded Funds (ETFs) & Index TradingPart I: Understanding Exchange-Traded Funds (ETFs)

1. What are ETFs?

An Exchange-Traded Fund (ETF) is an investment vehicle that holds a basket of assets—such as stocks, bonds, commodities, or currencies—and trades on stock exchanges like a single stock.

Structure: ETFs are designed to track the performance of an underlying index, sector, commodity, or strategy.

Trading: Unlike mutual funds (which are priced once a day), ETFs trade continuously throughout the trading day, with prices fluctuating based on supply and demand.

Flexibility: ETFs can be bought and sold just like stocks, enabling short-selling, margin trading, and intraday strategies.

In essence, ETFs combine the diversification of mutual funds with the flexibility of stocks.

2. History and Evolution of ETFs

The first ETF, SPDR S&P 500 ETF Trust (SPY), was launched in 1993 in the United States. It aimed to track the S&P 500 Index, giving investors exposure to the 500 largest U.S. companies in a single instrument.

Since then, the ETF industry has exploded globally:

1990s: Launch of broad-market ETFs (SPY, QQQ).

2000s: Expansion into sector-based and international ETFs.

2010s: Rise of smart beta and thematic ETFs (e.g., clean energy, robotics, AI).

2020s: Growth in actively managed ETFs, ESG-focused ETFs, and crypto ETFs (like Bitcoin futures ETFs).

Today, ETFs account for trillions of dollars in global assets under management (AUM), making them one of the fastest-growing investment products.

3. Types of ETFs

ETFs come in different forms to suit various investor needs:

Equity ETFs – Track stock indices like S&P 500, Nifty 50, Nasdaq-100.

Bond ETFs – Provide exposure to government, corporate, or municipal bonds.

Commodity ETFs – Track commodities like gold, silver, or oil.

Currency ETFs – Track currency movements (e.g., U.S. Dollar Index ETF).

Sector & Industry ETFs – Focus on sectors like technology, healthcare, or banking.

International & Regional ETFs – Give exposure to markets like China, Europe, or emerging markets.

Inverse & Leveraged ETFs – Provide magnified or opposite returns of an index (used for short-term trading).

Thematic ETFs – Target specific investment themes (renewable energy, AI, blockchain).

Actively Managed ETFs – Managed by fund managers who actively pick securities.

4. How ETFs Work (Mechanics)

ETFs use a creation and redemption mechanism to keep their market price close to the net asset value (NAV).

Authorized Participants (APs): Large institutions that create or redeem ETF shares.

Creation: APs deliver a basket of securities to the ETF provider in exchange for new ETF shares.

Redemption: APs return ETF shares and receive the underlying securities.

This arbitrage mechanism ensures that ETF prices remain close to the value of their underlying assets.

5. Advantages of ETFs

Diversification – Exposure to hundreds of securities in one trade.

Liquidity – Trade throughout the day on exchanges.

Cost Efficiency – Lower expense ratios compared to mutual funds.

Transparency – Daily disclosure of holdings.

Flexibility – Options, margin trading, and short-selling available.

Tax Efficiency – Creation/redemption process reduces taxable distributions.

6. Disadvantages of ETFs

Trading Costs – Brokerage fees and bid-ask spreads can add up.

Tracking Error – ETFs may not perfectly track their underlying index.

Overtrading Risk – Intraday liquidity may encourage speculative behavior.

Leverage & Inverse ETFs Risks – Can lead to significant losses if misunderstood.

Concentration in Popular Sectors – Certain thematic ETFs may be too niche or volatile.

Part II: Index Trading

1. What is an Index?

An index is a statistical measure representing the performance of a group of securities. Examples:

S&P 500 (USA): 500 largest U.S. companies.

Nifty 50 (India): 50 largest companies listed on NSE.

Dow Jones Industrial Average: 30 U.S. blue-chip companies.

Indices serve as benchmarks to measure market or sector performance.

2. What is Index Trading?

Index trading refers to trading financial products based on stock market indices rather than individual stocks.

Investors trade:

Index Futures – Contracts based on future value of an index.

Index Options – Options contracts linked to indices.

ETFs & Index Funds – Indirect way to trade indices.

CFDs (Contracts for Difference): Widely used in global markets.

3. Why Trade Indices?

Diversification – Exposure to entire markets or sectors.

Hedging – Protect portfolios from market downturns.

Speculation – Bet on broad market movements.

Benchmarking – Compare portfolio performance against indices.

4. Popular Global Indices

USA: S&P 500, Nasdaq-100, Dow Jones.

India: Nifty 50, Sensex, Bank Nifty.

Europe: FTSE 100 (UK), DAX 40 (Germany), CAC 40 (France).

Asia: Nikkei 225 (Japan), Hang Seng (Hong Kong), Shanghai Composite (China).

5. Strategies in Index Trading

Buy-and-Hold Strategy: Long-term investment in index ETFs.

Swing Trading: Trading short-to-medium-term index price movements.

Hedging: Using index futures to hedge stock portfolios.

Arbitrage: Exploiting mispricing between futures, ETFs, and underlying stocks.

Sector Rotation: Moving investments between indices/sectors depending on the economic cycle.

Options Strategies: Using index options for spreads, straddles, or covered calls.

Part III: ETFs vs. Index Funds vs. Index Trading

ETFs – Trade on exchanges, intraday pricing, lower costs.

Index Funds – Mutual funds tracking indices, priced once daily.

Index Trading (Futures/Options) – Derivatives-based, high leverage, short-term focus.

Example:

Long-term investor → Index Fund or ETF.

Active trader → Index futures, options, or leveraged ETFs.

Part IV: Risks in ETFs & Index Trading

Market Risk – Both ETFs and indices reflect market movements.

Liquidity Risk – Low-volume ETFs may have wide spreads.

Tracking Error – ETFs may deviate from index returns.

Leverage Risk – Amplified losses in leveraged ETFs/futures.

Currency Risk – International ETFs affected by forex fluctuations.

Concentration Risk – Indices may be dominated by a few large companies (e.g., FAANG in S&P 500).

Part V: ETFs & Index Trading in India

India has seen tremendous growth in ETFs and index trading:

Popular ETFs: Nippon India ETF Nifty BeES, SBI ETF Nifty Bank, ICICI Prudential Nifty Next 50 ETF.

Gold ETFs: Widely used as an alternative to physical gold.

Sector ETFs: Banking, IT, PSU ETFs gaining traction.

Index Futures/Options: Nifty 50 and Bank Nifty derivatives dominate NSE trading volumes.

Government and institutional investors (like EPFO) also allocate large sums to ETFs, boosting the industry further.

Part VI: Future of ETFs & Index Trading

Rise of Thematic & ESG ETFs – Growth in socially responsible investing.

Active ETFs – Managers offering active strategies via ETFs.

Crypto ETFs – Bitcoin and Ethereum ETFs expanding.

Tokenization & Blockchain ETFs – Future of transparent, decentralized ETF structures.

AI-driven Index Construction – Smart beta indices built using machine learning.

Conclusion

Exchange-Traded Funds (ETFs) and Index Trading have reshaped the way investors approach financial markets. They offer simplicity, diversification, transparency, and cost-effectiveness, making them ideal for both beginners and professionals.

ETFs provide access to a wide range of assets, from equities and bonds to commodities and currencies.

Index trading allows traders to speculate, hedge, or invest in entire markets rather than individual stocks.

Together, they represent the future of investing: efficient, scalable, and adaptable to changing global market trends.

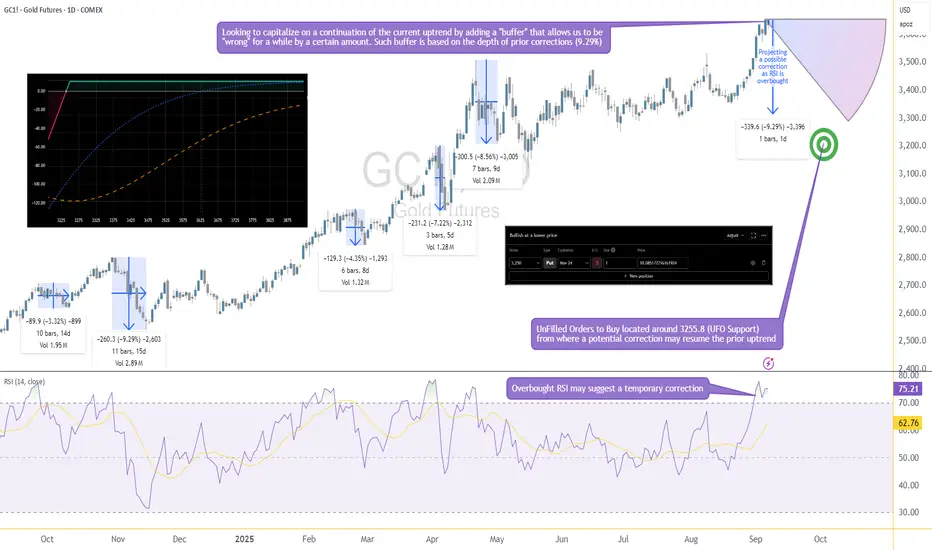

Options Blueprint Series [Basic]: Gold Income or Bargain Entry?The Setup: A Pullback with a Plan

Gold has been riding a strong bullish wave, yet momentum indicators suggest it's time for a breather. RSI is now overbought, and if history repeats, we could see a healthy correction of up to 9.29%, in line with prior pullbacks. This projects price near 3255, where we also find a cluster of UnFilled Orders (UFOs) acting as a potentially relevant support. It’s a key price area where buyers may step in again.

Rather than try to perfectly time the correction or the bottom, we’re applying a more forgiving approach: selling a PUT far below current price—generating income while leaving room to be wrong by over 375 points.

This is not a hedge. This is a standalone income strategy that accepts risk but frames it intelligently using technical context and options structure.

The Strategy: Selling the 3250 PUT on GC

We're using a simple but powerful strategy—selling a naked PUT—which can generate income or result in ownership of Gold at a deep discount if price dips.

Underlying Asset: GCZ2025 – using Gold Futures Options (Nov 24 2025 Expiration)

Strategy: Sell 1x 3250 PUT

Premium Collected: 10.09 points ≈ $1,009

Breakeven Price: 3240

Max Profit: $1,009 (if Gold stays above 3250 until expiration)

Max Risk: Unlimited below breakeven

There are two possible outcomes here:

Gold stays above 3250 → we keep the full premium.

Gold drops below 3250 → we get assigned and become long GC at 3250. From there, we’re exposed to downside risk in Gold, with a breakeven at 3240.

The position benefits from time decay and stable to rising prices, but it does carry the full downside exposure of long Gold futures if the trade moves against us.

We want to be very clear here—this is a naked trade with undefined risk. That doesn’t make it reckless if done with sizing discipline and technical alignment, but it’s not a beginner-friendly strategy.

Gold Contract Specs

Understanding the size and risk of what you're trading is critical—especially with naked options.

✅ GC – Gold Futures (Full Size)

Symbol: GC

Contract Size: 100 troy ounces

Tick Size: 0.10 = $10

Point Value: 1 point = $100

Initial Margin (as of Sep 2025): ~$15,000 per contract (subject to change)

Underlying for the Option: GC Futures

✅ MGC – Micro Gold Futures

Symbol: MGC

Contract Size: 10 troy ounces

Tick Size: 0.10 = $1

Point Value: 1 point = $10

Initial Margin: ~$1,500 per contract (subject to change)

Why does this matter?

Because if GC collapses below 3250 and you're assigned long, you’ll be exposed to full-size futures. That’s $100 per point of movement. A 50-point drop? That's $5,000 in unrealized loss.

That’s where MGC becomes your best ally. Micro Gold futures offer a scalable way to hedge. If price begins moving down or breaks below the support zone, one could short MGC against the Short GC 3250 PUT to cap further losses or rebalance directional exposure with reduced size and margin impact.

The Technical Confluence: Where Structure Meets Strategy

The 3250 strike isn’t just a random number—it’s calculated. Historical RSI-based corrections in Gold have shown recent worse-case scenarios around 9.29%, and projecting that from recent highs lands us precisely near the 3255 zone. This level also aligns with a clear UFO support, where institutional buyers have likely left behind unfilled orders.

That confluence—statistical retracement, technical indicator, and order flow support—gives the 3250 strike an interesting probability structure. Selling a Put beneath it means we are placing our bet below the “floor” and getting paid while we wait.

If Gold never corrects that far, we profit.

If it does, we might get long near a historically meaningful level.

There’s no need to catch the top. There’s no need to nail the bottom.

Just structure the trade where the odds are already potentially skewed in your favor.

Trade Plan: Reward, Risk & Realism

This trade isn’t about precision entry or leveraged glory—it’s about risk-defined logic with a cash-flow twist. Here's the full breakdown:

🧠 Trade Parameters

Strategy: Sell 1x Gold Futures 3250 PUT Options

Premium Collected: 10.09 points = $1,009

Point Value (GC): $100/point

Breakeven Price: 3240 (3250 – 10)

Expiration: Nov 24, 2025

🟩 If Gold Stays Above 3250

You keep the full premium → $1,009 profit

🟥 If Gold Falls Below 3250

You may be assigned 1 GC contra<ct long at 3250

Unrealized losses begin below breakeven (3240)

Losses can be significant if Gold falls aggressively

⚠️ Reward-to-Risk?

Reward is capped at $1,009

Risk is unlimited below breakeven

The trade only makes sense if you're prepared to own Gold, or hedge dynamically via MGC or using any other technique

This isn’t a “set-and-forget” income play—it’s a calculated entry into a structured exposure with a fallback plan.

Risk Management: No Margin for Error

Selling naked options isn’t “free money.” It’s responsibility wrapped in premium. Here's what must be considered:

❗ Undefined Risk

When you sell a naked PUT, you're exposed to the full downside. If Gold drops $100 below your strike, that’s a $10,000 loss. Don’t sell naked options unless you’re ready—and capitalized—to buy the underlying or actively hedge it.

🔄 Use MGC to Hedge

If Gold breaks below 3250, using Micro Gold Futures (MGC) offers a surgical way to hedge risk without overleveraging. A simple short MGC can offset GC losses proportionally, depending on how aggressive the move becomes.

🧮 Precision Matters

Avoid entering trades too early or too large.

Place an “invalidation” point: if price violates the support zone with conviction, reduce or hedge exposure.

Never sell premium just because it’s “high”—sell where structure backs the trade.

📊 Discipline Trumps Direction

This strategy is valid only if risk is respected. The market doesn’t owe anyone consistency—but a structured, risk-controlled approach keeps you in the game long enough to see it.

When charting futures, the data provided could be delayed. Traders working with the ticker symbols discussed in this idea may prefer to use CME Group real-time data plan on TradingView: www.tradingview.com - This consideration is particularly important for shorter-term traders, whereas it may be less critical for those focused on longer-term trading strategies.

General Disclaimer:

The trade ideas presented herein are solely for illustrative purposes forming a part of a case study intended to demonstrate key principles in risk management within the context of the specific market scenarios discussed. These ideas are not to be interpreted as investment recommendations or financial advice. They do not endorse or promote any specific trading strategies, financial products, or services. The information provided is based on data believed to be reliable; however, its accuracy or completeness cannot be guaranteed. Trading in financial markets involves risks, including the potential loss of principal. Each individual should conduct their own research and consult with professional financial advisors before making any investment decisions. The author or publisher of this content bears no responsibility for any actions taken based on the information provided or for any resultant financial or other losses.

Global Hard Commodity Trading1. Understanding Hard Commodities

Hard commodities are natural resources that must be mined, extracted, or produced through industrial processes. They are different from soft commodities, which include agricultural products like wheat, coffee, or cotton.

Examples of Hard Commodities:

Energy Commodities

Crude Oil (Brent, WTI)

Natural Gas

Coal

Uranium

Metals

Precious Metals: Gold, Silver, Platinum, Palladium

Base Metals: Copper, Aluminum, Zinc, Nickel, Lead, Tin

Rare Earth Elements (used in electronics, EVs, clean tech)

Characteristics of Hard Commodities:

Limited in supply, extracted from earth.

Prices are volatile, influenced by global demand and supply shocks.

Traded both physically and financially.

Often priced in US dollars, making them linked to global currency fluctuations.

Hard commodities are critical for energy, manufacturing, construction, defense, and technology sectors, making them a barometer of global economic health.

2. Evolution of Global Hard Commodity Trading

Commodity trading is not new—it dates back thousands of years when civilizations bartered metals, salt, and oil. However, the modern commodity trading system began in the 19th and 20th centuries with the rise of commodity exchanges like the Chicago Mercantile Exchange (CME) and the London Metal Exchange (LME).

Historical Milestones:

19th century: Industrial revolution created huge demand for coal, iron, and copper.

1900s: Oil became the world’s most important energy commodity.

1970s oil shocks: Highlighted the geopolitical importance of commodities.

2000s commodity super-cycle: Rapid demand from China and India fueled a massive rise in metal and energy prices.

Today: Hard commodities are not just traded physically but also heavily speculated on global futures markets.

3. Key Players in Hard Commodity Trading

Trading hard commodities involves a diverse range of participants:

Producers:

Oil companies (ExxonMobil, Saudi Aramco, BP)

Mining giants (Rio Tinto, BHP, Glencore)

Consumers:

Manufacturing companies, refineries, power plants, automakers, construction firms.

Traders & Intermediaries:

Global commodity trading houses like Vitol, Trafigura, Glencore, Gunvor.

These firms buy commodities from producers and sell them to consumers worldwide, often handling logistics, shipping, and financing.

Financial Institutions:

Investment banks (Goldman Sachs, JPMorgan, Morgan Stanley) actively trade in commodity derivatives.

Speculators & Investors:

Hedge funds, mutual funds, and retail traders participate in futures and ETFs for profit.

Governments & Regulators:

OPEC, IEA, WTO, and national regulators influence prices and rules.

4. Major Hard Commodity Markets

4.1 Energy Commodities

Crude Oil: Most traded commodity globally. Benchmarks: Brent (North Sea), WTI (US), Dubai/Oman.

Natural Gas: Key for heating, power generation, and industrial use. LNG (liquefied natural gas) has made gas a global trade.

Coal: Despite clean energy trends, coal still accounts for a major share of electricity generation in Asia.

Uranium: Fuels nuclear energy.

4.2 Metals

Gold & Silver: Precious metals for investment and jewelry. Also safe-haven assets during crises.

Copper: Known as “Dr. Copper” because it signals global economic health—widely used in construction and electronics.

Aluminum, Nickel, Zinc: Critical for cars, infrastructure, and batteries.

Rare Earths: Essential for EVs, wind turbines, semiconductors.

5. How Hard Commodities are Traded

5.1 Physical Trading

This involves the actual movement of goods—oil tankers, copper shipments, coal cargoes. Large trading houses dominate this space, dealing with storage, shipping, and financing.

5.2 Financial Trading

Financial markets allow traders to speculate, hedge, or invest without handling physical goods.

Futures Contracts (CME, LME, ICE)

Options & Swaps

Exchange-Traded Funds (ETFs) linked to commodities

Over-the-Counter (OTC) Derivatives

For example, an airline may hedge jet fuel prices through futures to lock in costs.

6. Price Drivers in Hard Commodity Trading

Hard commodity prices are influenced by a mix of economic, political, and natural factors:

Supply & Demand:

Strong global growth → higher demand for oil, metals.

Supply disruptions (strikes, wars, sanctions) → price spikes.

Geopolitics:

Middle East tensions → oil shocks.

Trade wars → disrupt commodity flows.

Currency Movements:

Most commodities priced in USD. A strong dollar makes them expensive for other countries.

Speculation & Investor Flows:

Hedge funds and ETFs influence short-term price swings.

Technological & Environmental Factors:

EV demand boosts lithium, cobalt, nickel.

Green energy transition reducing coal demand.

Natural Events:

Hurricanes disrupting oil production.

Mining accidents reducing metal supply.

7. Risks in Hard Commodity Trading

Price Volatility: Sharp swings make profits uncertain.

Political Risk: Sanctions, wars, and nationalization.

Credit Risk: Default by counterparties.

Logistics Risk: Shipping delays, storage costs.

Regulatory Risk: Changing government rules.

Environmental Risk: Climate policies reducing fossil fuel demand.

Traders use hedging strategies and risk management tools to minimize exposure.

8. Global Trade Hubs & Exchanges

London Metal Exchange (LME): Key center for base metals.

New York Mercantile Exchange (NYMEX): Crude oil, natural gas.

Intercontinental Exchange (ICE): Brent crude, energy futures.

Shanghai Futures Exchange (SHFE): China’s growing influence.

Dubai Mercantile Exchange (DME): Oil contracts for Middle East & Asia.

Physical hubs include Rotterdam (oil), Singapore (oil & LNG), Shanghai (metals), Dubai (gold).

9. Role of Technology in Hard Commodity Trading

Technology is transforming commodity trading:

AI & Algorithms for price forecasting.

Blockchain for trade finance and supply chain transparency.

Big Data & IoT to track shipments and consumption trends.

Digital platforms replacing traditional paper-based contracts.

10. Future of Hard Commodity Trading

Energy Transition:

Demand for oil may peak in coming decades.

Growth in renewables and metals like lithium, cobalt, nickel.

Green Commodities:

Carbon credits becoming tradable assets.

ESG (Environmental, Social, Governance) shaping investment choices.

China & India’s Role:

Asia will remain the biggest consumer of hard commodities.

Geopolitical Fragmentation:

Sanctions, supply chain shifts, and regional alliances may create “commodity blocs.”

Digitalization:

More algorithm-driven and blockchain-powered commodity trading.

Conclusion

Global hard commodity trading is more than just an economic activity—it is the heartbeat of the world economy. Energy, metals, and minerals not only determine industrial growth but also shape geopolitics, financial markets, and future technologies.

While the industry faces challenges of volatility, climate change, and regulatory shifts, it is also evolving rapidly with digitalization, green energy, and new demand sources.

For traders, investors, and policymakers alike, understanding hard commodity markets is essential—not just to profit, but also to anticipate global economic and political shifts.

Carry Trade in the Global Market1. What is a Carry Trade?

A carry trade is a financial strategy where investors:

Borrow or fund positions in a currency with low interest rates (funding currency).

Use those funds to buy a currency or asset with a higher interest rate (target currency or investment).

Earn the difference between the two rates (the interest rate spread), while also being exposed to currency fluctuations.

Example (Simplified):

Suppose the Japanese yen has a 0.1% interest rate, and the Australian dollar (AUD) has a 5% interest rate.

A trader borrows ¥100 million (Japanese yen) at near-zero cost and converts it into AUD.

The funds are invested in Australian bonds yielding 5%.

Annual return ≈ 4.9% (before considering currency fluctuations).

If the AUD appreciates against the yen during this time, the trader earns both the interest rate differential + capital gains. If AUD depreciates, the trade may turn into a loss.

2. The Mechanics of Carry Trade

Carry trade is not as simple as just switching between two currencies. It involves global capital flows, leverage, interest rate cycles, and risk management.

Step-by-Step Process:

Identify funding currency: Typically one with low or negative interest rates (JPY, CHF, or USD in certain cycles).

Borrow or short-sell this currency.

Buy high-yielding currency assets: Such as government bonds, corporate debt, or equities in emerging markets.

Earn interest spread daily (known as the rollover in forex markets).

Monitor exchange rates since even small currency fluctuations can offset interest gains.

Why It Works:

Differences in monetary policies across central banks create yield gaps.

Investors with large capital seek to exploit these spreads.

Global liquidity cycles and risk appetite drive the demand for carry trades.

3. Historical Importance of Carry Trade

Carry trades have been a cornerstone of currency markets, shaping global financial cycles:

1990s – Japanese Yen Carry Trade

Japan maintained near-zero interest rates after its asset bubble burst in the early 1990s.

Investors borrowed cheap yen and invested in higher-yielding assets abroad (Australia, New Zealand, emerging markets).

This caused yen weakness and strong capital inflows into emerging markets.

2000s – Dollar and Euro Carry Trades

Before the 2008 financial crisis, investors borrowed in low-yielding USD and JPY to invest in high-yielding currencies like the Brazilian Real, Turkish Lira, and South African Rand.

Commodity booms amplified returns, making the carry trade highly profitable.

2008 Global Financial Crisis

Carry trades collapsed as risk aversion spiked.

Investors unwound positions, leading to a surge in yen (JPY) and Swiss franc (CHF).

This showed how carry trade unwind can cause global market turbulence.

2010s – Post-Crisis QE Era

Ultra-low rates in the US, Japan, and Europe sustained carry trade strategies.

Emerging markets benefited from capital inflows but became vulnerable to sudden outflows when US Fed hinted at tightening (2013 “Taper Tantrum”).

2020s – Pandemic & Beyond

Global central banks slashed rates during COVID-19, reviving conditions for carry trades.

However, the 2022–23 inflation surge and rate hikes by the Fed created volatility, making carry trades riskier.

4. Global Carry Trade Currencies

Funding Currencies (Low Yield):

Japanese Yen (JPY): Classic funding currency due to decades of near-zero rates.

Swiss Franc (CHF): Safe-haven status and low yields.

Euro (EUR): Used in periods of ECB ultra-loose policy.

US Dollar (USD): At times of near-zero Fed rates.

Target Currencies (High Yield):

Australian Dollar (AUD) & New Zealand Dollar (NZD): Stable economies with higher yields.

Emerging Market Currencies: Brazilian Real (BRL), Turkish Lira (TRY), Indian Rupee (INR), South African Rand (ZAR).

Commodity Exporters: Higher rates often accompany higher commodity cycles.

5. Drivers of Carry Trade Activity

Carry trades thrive when global financial conditions are supportive.

Interest Rate Differentials – Larger gaps = higher carry.

Global Liquidity – Abundant capital seeks higher yields.

Risk Appetite – Investors pursue carry trades in “risk-on” environments.

Monetary Policy Divergence – When one central bank keeps rates low while others tighten.

Volatility Levels – Low volatility encourages carry trades; high volatility kills them.

6. Risks of Carry Trade

Carry trades may look attractive, but they are highly risky.

Currency Risk – A sudden depreciation of the high-yielding currency can wipe out gains.

Interest Rate Shifts – If the funding currency raises rates or target currency cuts rates, the carry spread shrinks.

Liquidity Risk – In crises, traders rush to unwind, leading to sharp reversals.

Geopolitical Risk – Wars, political instability, or sanctions can collapse carry trades.

Leverage Risk – Carry trades are often leveraged, magnifying both profits and losses.

7. The Role of Central Banks

Central banks indirectly shape carry trades through:

Rate setting policies (zero-rate or tightening cycles).

Forward guidance that signals future moves.

Quantitative easing (QE) that floods markets with liquidity.

Capital controls in emerging markets that try to manage inflows/outflows.

8. Case Studies in Carry Trades

The Yen Carry Trade (2000–2007)

Massive inflows into risky assets globally.

Unwinding during 2008 caused yen to spike 30%, triggering global asset sell-offs.

The Turkish Lira (TRY)

High rates attracted carry trades.

But political instability and inflation led to currency crashes, wiping out investors.

Brazil and South Africa

During commodity booms, high-yield currencies like BRL and ZAR became popular targets.

However, they were also prone to volatility from commodity cycles.

9. Carry Trade in Modern Markets

Today, carry trades are more complex and algorithm-driven. Hedge funds, banks, and institutional investors run quantitative carry trade strategies across forex, bonds, and derivatives.

Tools Used:

FX swaps & forwards

Options for hedging

ETFs & leveraged funds tracking carry trade strategies

Example – G10 Carry Index

Some financial institutions track “carry indices” that measure returns from long high-yield currencies and short low-yield currencies.

10. Advantages of Carry Trade

Predictable Income – Earn from interest rate differentials.

Scalability – Works in global FX markets with high liquidity.

Diversification – Access to multiple asset classes.

Potential for Leverage – High returns if managed correctly.

Conclusion

Carry trade is one of the most fascinating and impactful strategies in the global financial system. By exploiting interest rate differentials across countries, it provides traders with a potential source of profit. However, history has shown that the carry trade is a double-edged sword: highly rewarding in stable times, but brutally punishing during crises.

Understanding its mechanics, historical patterns, risks, and modern applications is essential for any trader, investor, or policymaker. The carry trade is more than just a strategy — it is a barometer of global risk appetite, liquidity, and monetary policy divergence.

For those who master it with discipline and risk management, the carry trade remains a powerful tool in navigating global markets.

Real Estate Market Trading (Global Property Investments)Chapter 1: The Evolution of Global Real Estate

1.1 From Land Ownership to Investment Vehicles

Historically, real estate was limited to direct ownership—buying a plot of land or a house. Over time, as capital markets developed, new vehicles like real estate funds, REITs, and securitized mortgages emerged, democratizing access to property investments.

Pre-20th Century: Land was tied to agriculture and feudal wealth.

Post-WWII Era: Rapid urbanization and industrialization led to housing booms worldwide.

1980s–2000s: Financial innovation enabled securitization of mortgages and global property funds.

2008 Crisis: Highlighted risks of over-leveraged real estate trading (subprime mortgage collapse).

2020s: Rise of proptech, tokenization, and cross-border property investments via digital platforms.

1.2 The Shift to Globalization

Earlier, real estate was local in nature. Today, with international capital mobility, investors in Singapore can own shares of an office building in New York or a luxury resort in Dubai. Sovereign wealth funds, pension funds, and hedge funds now treat real estate as a core part of global portfolios.

Chapter 2: Types of Global Property Investments

2.1 Direct Real Estate Investments

Residential Properties: Apartments, villas, and multi-family housing.

Commercial Properties: Office towers, co-working spaces, retail malls.

Industrial Properties: Warehouses, logistics hubs, data centers.

Hospitality & Tourism: Hotels, resorts, serviced apartments.

Specialty Real Estate: Senior housing, student accommodation, hospitals.

2.2 Indirect Investments

REITs (Real Estate Investment Trusts): Publicly traded companies that own income-generating property.

Property Funds & ETFs: Diversified funds that invest in global or regional properties.

Private Equity Real Estate: Institutional funds targeting high-value projects.

Securitized Real Estate Products: Mortgage-backed securities (MBS).

2.3 New Age Investments

Fractional Ownership: Platforms enabling small-ticket investments in high-value properties.

Tokenized Real Estate: Blockchain-based ownership shares, allowing cross-border property trading.

Green Real Estate Funds: Focus on sustainable buildings and energy-efficient assets.

Chapter 3: Key Drivers of the Global Real Estate Market

3.1 Economic Growth & Income Levels

A strong economy boosts demand for housing, office spaces, and retail outlets. Conversely, recessions often lead to property price corrections.

3.2 Interest Rates & Monetary Policy

Real estate is heavily credit-dependent. When interest rates are low, borrowing is cheaper, encouraging investments. Rising rates often dampen demand and lower valuations.

3.3 Demographics & Urbanization

Young populations drive housing demand.

Aging populations create demand for healthcare and senior housing.

Rapid urban migration boosts infrastructure and property markets in developing nations.

3.4 Technology & Infrastructure

Digital transformation (proptech, AI-driven valuations, blockchain).

Smart cities with IoT-based energy-efficient buildings.

Infrastructure like airports, metros, and highways pushing property values higher.

3.5 Globalization of Capital

Cross-border investments have increased, with Asia-Pacific, Middle East, and European investors pouring capital into North American and emerging-market properties.

3.6 Geopolitical & Environmental Factors

Wars, sanctions, and political instability impact property flows.

Climate change increases demand for resilient, green buildings.

Government housing policies and tax incentives drive local markets.

Chapter 4: Global Real Estate Market Segments

4.1 Residential Real Estate

The backbone of real estate, influenced by population growth, income levels, and mortgage availability. Trends include:

Affordable housing demand in emerging markets.

Luxury housing in global hubs like London, Dubai, and New York.

Vacation homes and short-term rental platforms (Airbnb model).

4.2 Commercial Real Estate (CRE)

Includes offices, malls, and business parks. Post-pandemic trends show:

Hybrid work models reducing demand for traditional office space.

E-commerce boosting logistics and warehousing investments.

Retail shifting from malls to experiential centers.

4.3 Industrial Real Estate

A rising star due to global supply chain realignment:

Warehouses and cold storage facilities.

Data centers (digital economy backbone).

Renewable energy sites (solar and wind farms).

4.4 Hospitality & Tourism Properties

Tourism recovery post-COVID has reignited hotel investments. Countries like UAE, Thailand, and Maldives remain hotspots.

Chapter 5: Real Estate Trading Mechanisms

5.1 Traditional Trading

Direct purchase and sale of land or property.

Long holding periods with rental income.

5.2 Listed Market Trading

Buying and selling REITs, property ETFs, and securitized debt instruments on stock exchanges.

High liquidity compared to physical property.

5.3 Digital & Tokenized Trading

Blockchain enables fractional trading of global assets. For example, an investor in India can purchase a $100 token representing part ownership of a Manhattan office tower.

Chapter 6: Global Hotspots for Property Investment

6.1 North America

United States: Largest REIT market; strong demand in tech hubs like Austin, Miami, and San Francisco.

Canada: Rising immigration boosting residential demand in Toronto and Vancouver.

6.2 Europe

UK: London remains a luxury real estate hub.

Germany: Berlin attracting investors due to stable rental yields.

Spain & Portugal: Tourism-driven real estate and golden visa programs.

6.3 Asia-Pacific

China: Slowdown due to debt-laden developers, but still massive market.

India: Affordable housing, commercial hubs (Bengaluru, Hyderabad), and REITs gaining traction.

Singapore & Hong Kong: Financial hubs attracting global property capital.

6.4 Middle East

UAE (Dubai, Abu Dhabi): Tax-free status, global expat community, and luxury real estate boom.

Saudi Arabia: Vision 2030 fueling mega infrastructure projects.

6.5 Emerging Markets

Africa (Nigeria, Kenya, South Africa): Urbanization and infrastructure push.

Latin America (Brazil, Mexico): Tourism and housing demand.

Chapter 7: Risks in Global Property Trading

7.1 Market Risks

Price volatility due to economic cycles.

Oversupply in certain regions leading to price corrections.

7.2 Financial Risks

Rising interest rates increasing borrowing costs.

Currency fluctuations impacting cross-border investors.

7.3 Political & Regulatory Risks

Changes in property laws, taxes, or ownership rights.

Political instability reducing foreign investment appetite.

7.4 Environmental & Climate Risks

Properties in flood-prone or disaster-prone zones losing value.

Higher costs of compliance with green regulations.

Chapter 8: Future of Global Property Investments

8.1 Technology Transformation

AI for predictive property valuations.

Metaverse real estate and digital land ownership.

Smart contracts automating property transactions.

8.2 Green & Sustainable Real Estate

Global shift toward ESG investing is pushing developers to build carbon-neutral buildings. Green bonds tied to real estate are gaining momentum.

8.3 Institutional Dominance

Pension funds, sovereign funds, and insurance companies will continue to dominate large-scale global property deals.

8.4 Democratization via Tokenization

Retail investors gaining access to billion-dollar properties through blockchain-powered fractional ownership.

Chapter 9: Strategies for Investors

Diversification – Spread across geographies and property types.

Long-Term Vision – Real estate rewards patience.

Leverage Smartly – Avoid overexposure to debt.

Follow Macro Trends – Urbanization, interest rates, and technology adoption.

Risk Mitigation – Use insurance, hedging, and local partnerships.

Conclusion

Real estate market trading and global property investments represent one of the most dynamic and resilient avenues of wealth creation. While challenges exist—such as rising rates, geopolitical uncertainty, and climate risks—the fundamental demand for land and property is eternal. The shift toward digital ownership, sustainability, and cross-border capital flows ensures that the real estate sector will continue to evolve as a global marketplace.

For investors, success lies in combining local insights with global perspectives, diversifying portfolios, embracing technology, and staying agile to adapt to changing market conditions.

In many ways, real estate is no longer just about “location, location, location”—it’s about innovation, globalization, and sustainability.

Shaping Global Trade & Currencies1. Historical Evolution of Trade & Currencies

1.1 Early Trade Systems

Ancient civilizations engaged in barter-based trade, exchanging goods like grains, spices, and metals.

The Silk Road connected Asia, the Middle East, and Europe, becoming one of the earliest global trade routes.

Precious metals such as gold and silver became the first universally accepted currencies for trade.

1.2 Emergence of Modern Currencies

With the rise of kingdoms and empires, coins and paper money replaced barter.

Colonialism reshaped trade routes, with European powers dominating maritime trade.

The gold standard (19th century) linked currencies to gold, bringing stability to global exchange.

1.3 Bretton Woods System

After World War II, the 1944 Bretton Woods Agreement established the US dollar as the anchor currency, pegged to gold.

Institutions like the International Monetary Fund (IMF) and World Bank were created to stabilize trade and finance.

The system collapsed in 1971 when the US abandoned the gold standard, leading to today’s system of floating exchange rates.

2. The Dynamics of Global Trade

2.1 Drivers of Global Trade

Comparative advantage: Countries trade based on their strengths (e.g., oil-rich Middle East, tech-driven US, manufacturing hub China).

Global supply chains: Modern production spans multiple countries (e.g., iPhones designed in the US, assembled in China, components from Japan, Korea).

Technology: Digital platforms, container shipping, and logistics efficiency made cross-border trade faster and cheaper.

Trade liberalization: Free trade agreements (FTAs), regional blocs like EU, NAFTA, ASEAN, and the role of the WTO facilitated tariff reduction.

2.2 Trade Balances & Deficits

Countries with trade surpluses (exports > imports) accumulate foreign reserves (e.g., China, Germany).

Trade deficits (imports > exports) often weaken currencies (e.g., US, India at times).

Persistent imbalances create currency tensions and trade wars.

2.3 Role of Multinational Corporations

MNCs control global supply chains, influence trade volumes, and hedge against currency risks.

Companies like Apple, Toyota, and Amazon shape currency demand through cross-border transactions.

3. The Role of Currencies in Global Trade

3.1 Currency as a Medium of Exchange

Trade requires settlement in common units of value—currencies like USD, Euro, Yen, Yuan.

The US Dollar dominates, accounting for ~60% of global reserves and ~80% of trade invoicing.

3.2 Exchange Rate Systems

Fixed Exchange Rates – pegged to another currency (e.g., Hong Kong Dollar to USD).

Floating Exchange Rates – determined by supply-demand in forex markets (e.g., Euro, Yen).

Managed Exchange Rates – central banks intervene to stabilize value (e.g., Indian Rupee, Chinese Yuan).

3.3 Impact of Currency Fluctuations on Trade

A strong currency makes exports expensive but imports cheaper.

A weak currency boosts exports but makes imports costlier.

Example: Japan often benefits from a weaker Yen, aiding its export-driven economy.

4. Key Institutions Shaping Trade & Currencies

4.1 International Monetary Fund (IMF)

Provides financial stability and currency support.

Monitors exchange rate policies and prevents currency manipulation.

4.2 World Trade Organization (WTO)

Regulates global trade rules.

Resolves trade disputes between nations.

4.3 World Bank

Provides development financing to support trade infrastructure.

Helps emerging economies integrate into global trade.

4.4 Central Banks

Influence currency values via interest rates, monetary policies, and interventions.

Examples: US Federal Reserve, European Central Bank, Reserve Bank of India.

4.5 Regional Trade Blocs

EU (single market, Eurozone).

ASEAN, NAFTA/USMCA.

African Continental Free Trade Agreement (AfCFTA).

5. Geopolitics & Trade-Currency Relations

5.1 Currency Wars

Nations sometimes deliberately devalue currencies to gain export advantage.

Example: China accused of “currency manipulation” by the US.

5.2 Trade Wars

Tariffs, sanctions, and restrictions reshape global flows.

Example: US-China trade war disrupted supply chains and currency stability.

5.3 Sanctions & Currency Power

Dominance of USD allows the US to enforce sanctions by restricting access to its financial system.

Russia, Iran, and others explore alternative settlement systems to bypass USD dominance.

6. Technology & the Future of Trade and Currencies

6.1 Digital Trade

E-commerce and digital platforms enable small businesses to participate globally.

Services trade (software, fintech, education) grows faster than goods trade.

6.2 Fintech & Payments

SWIFT, blockchain, and digital payment networks revolutionize settlements.

Cryptocurrencies like Bitcoin challenge traditional currency systems.

Central Bank Digital Currencies (CBDCs) are emerging as official digital currencies (China’s e-CNY, India’s Digital Rupee).

6.3 Automation & AI

AI-powered logistics and predictive analytics optimize global supply chains.

Digital platforms reduce transaction costs and improve cross-border efficiency.

7. Risks & Challenges in Trade & Currencies

7.1 Exchange Rate Volatility

Currency swings create uncertainty for exporters and importers.

Companies hedge risks via futures, forwards, and options.

7.2 Protectionism

Rise of nationalism and tariffs disrupt free trade principles.

Example: Brexit altered EU-UK trade dynamics.

7.3 Global Inequality

Developed nations often dominate trade benefits, leaving poorer economies vulnerable.

Currency crises in emerging markets (Argentina, Turkey, Sri Lanka) highlight fragility.

7.4 Climate Change & Sustainability

Green trade policies and carbon taxes affect global competitiveness.

Currency values may shift as nations transition to renewable energy.

8. Case Studies

8.1 US Dollar Dominance

Despite challenges, USD remains the global reserve currency.

Stability of US institutions, deep financial markets, and global trust sustain its dominance.

8.2 China’s Yuan Strategy

China pushes Yuan internationalization through Belt & Road projects, trade invoicing, and currency swaps.

Inclusion of Yuan in IMF’s Special Drawing Rights (SDR) basket strengthened its global role.

8.3 Eurozone & Euro

Euro became the second-most traded currency.

But crises like Greece’s debt problems revealed structural weaknesses.

8.4 Emerging Markets

India, Brazil, and others promote local currency trade settlements.

Reduces reliance on USD and improves currency stability.

9. The Future of Global Trade & Currencies

9.1 Multipolar Currency World

Rise of Yuan, Euro, and digital currencies may reduce US dollar dominance.

Regional blocs may settle trade in local currencies.

9.2 Digital Transformation

CBDCs and blockchain-based trade finance could replace traditional banking channels.

Smart contracts may automate trade settlements.

9.3 Sustainable Trade

Carbon-neutral policies, green financing, and ESG compliance will reshape trade.

Currencies of nations leading in green technology may gain strength.

9.4 Resilient Supply Chains

Post-COVID-19, countries diversify supply chains to reduce dependency on one region (e.g., China+1 strategy).

Trade and currency flows adapt to new production hubs (Vietnam, India, Mexico).

Conclusion

Global trade and currencies are inseparable forces driving the world economy. Trade enables nations to leverage comparative advantages, while currencies facilitate exchange and measure competitiveness. Over centuries, from barter to digital currencies, both systems evolved alongside geopolitics, technology, and institutional frameworks.

Today, challenges like protectionism, exchange rate volatility, and sustainability shape the future. At the same time, opportunities such as digital transformation, multipolar currencies, and green trade create new pathways.

Ultimately, the shaping of global trade and currencies reflects a balance between cooperation and competition, tradition and innovation, stability and disruption. The future will likely witness a hybrid world—where digital currencies coexist with traditional systems, regional trade complements global flows, and sustainability becomes a defining factor.

Global trade and currencies, therefore, are not just economic concepts but also mirrors of human progress, resilience, and interconnected destiny.

Impact of Rising US Treasury Yields on Global EquitiesPart 1: Understanding US Treasury Yields

1.1 What Are US Treasury Yields?

US Treasuries are debt securities issued by the US government to finance its operations. They come in different maturities—short-term bills (up to 1 year), medium-term notes (2–10 years), and long-term bonds (20–30 years). The yield on these securities represents the return an investor earns by holding them until maturity.

Yields move inversely to bond prices. When investors sell Treasuries, prices fall and yields rise. Conversely, when demand is high, yields drop.

1.2 Why Are US Treasuries Called “Risk-Free”?

The US government is considered the safest borrower in the world, backed by its ability to tax and print dollars. Thus, Treasuries are seen as risk-free assets in terms of default. This status makes them the benchmark against which global borrowing costs, equity valuations, and investment decisions are calibrated.

1.3 Drivers of Rising Treasury Yields

US Treasury yields rise due to:

Federal Reserve policy (interest rate hikes, balance sheet reductions).

Inflation expectations (higher inflation erodes bond value, pushing yields up).

Economic growth outlook (strong growth boosts demand for capital, raising yields).

Government borrowing (higher fiscal deficits increase supply of Treasuries, pressuring yields higher).

Part 2: Link Between Treasury Yields and Global Equities

2.1 The Discount Rate Effect

Equity valuations are based on the present value of future cash flows. When Treasury yields rise, the discount rate (the rate used to calculate present value) increases. This reduces the attractiveness of equities, especially growth stocks with earnings expected far into the future.

2.2 Opportunity Cost of Capital

Investors compare expected equity returns with risk-free Treasury yields. If yields rise significantly, the relative appeal of equities declines, causing fund flows to shift from stocks to bonds.

2.3 Cost of Borrowing for Corporates

Higher yields mean higher borrowing costs globally. For companies dependent on debt, rising yields squeeze margins and reduce profitability, pressuring stock prices.

2.4 Risk Sentiment and Volatility

Sharp increases in yields often spark volatility. Equity markets prefer stable interest rates. Sudden upward movements in yields are interpreted as signals of tightening liquidity or higher inflation risks, both of which unsettle investors.

Part 3: Historical Case Studies

3.1 The 2013 “Taper Tantrum”

In 2013, when the Federal Reserve hinted at tapering bond purchases, US Treasury yields surged. Emerging markets experienced massive capital outflows, and their stock markets plunged. This episode underscored the global sensitivity to US yields.

3.2 The 2018 Yield Spike

In 2018, the 10-year US Treasury yield touched 3.25%, triggering global equity sell-offs. Investors worried about higher discount rates and slowing global liquidity. Technology and high-growth sectors were hit hardest.

3.3 The 2022 Bond Rout

The Fed’s aggressive rate hikes in 2022 pushed the 10-year yield above 4%. Global equities, including the S&P 500, Europe’s Stoxx 600, and Asian indices, fell into bear markets. The pain was widespread—ranging from US tech giants to emerging-market stocks.

Part 4: Sector-Wise Impact of Rising Yields

4.1 Growth vs. Value Stocks

Growth stocks (e.g., technology, biotech) are most sensitive. Their long-duration cash flows are heavily discounted when yields rise.

Value stocks (e.g., banks, industrials, energy) often fare better. Banks, in particular, benefit from higher interest rates via improved net interest margins.

4.2 Banking & Financials

Higher yields typically boost profitability for banks and insurers, as they can lend at higher rates. Global financial stocks often outperform during rising-yield phases.

4.3 Real Estate & Utilities

These sectors are bond proxies—investors buy them for stable dividends. When Treasury yields rise, their relative appeal diminishes, leading to underperformance.

4.4 Commodities & Energy

Commodities often benefit indirectly if yields rise due to stronger growth expectations. However, if yields rise because of inflation and monetary tightening, commodities may face demand destruction risks.

Part 5: Geographic Sensitivities

5.1 United States

US equities are most directly impacted. The Nasdaq (tech-heavy) suffers more than the Dow Jones (value-oriented).

5.2 Europe

European equities track US yields closely. Higher yields in the US can lead to stronger dollar, pressuring European exporters. Additionally, Europe’s bond yields often rise in sympathy, tightening financial conditions.

5.3 Emerging Markets

Emerging markets are the most vulnerable. Rising US yields trigger:

Capital outflows (investors shift to safer US assets).

Currency depreciation (raising import costs and inflation).

Stock market sell-offs (especially in countries reliant on foreign capital).

For example, India, Brazil, and Turkey often see sharp corrections when US yields spike.

5.4 Asia (Japan, China)

Japan: Rising US yields weaken the yen (as investors chase dollar returns), which can help Japanese exporters but hurt domestic equities tied to imports.

China: Sensitive due to capital flows and trade dynamics. Rising US yields often pressure Chinese equities, especially during growth slowdowns.

Part 6: Currency & Global Equity Interplay

Rising US yields usually strengthen the US dollar. A stronger dollar reduces profits of US multinationals, pressures commodity prices, and creates headwinds for emerging-market equities. For global investors, currency-adjusted returns from foreign equities decline when the dollar is strong, further reducing equity allocations abroad.

Part 7: Broader Macroeconomic Implications

7.1 Liquidity Tightening

Higher yields reduce global liquidity. Central banks in other countries often follow the Fed to prevent capital flight, tightening financial conditions worldwide.

7.2 Inflation & Growth Trade-Off

Rising yields often reflect inflationary pressures. Central banks respond with rate hikes, slowing global growth. Equity markets suffer as both margins and valuations come under pressure.

7.3 Safe-Haven Flows

Paradoxically, in times of global turmoil, US Treasuries attract safe-haven flows, lowering yields again. But during inflationary cycles, this dynamic weakens, making equities more vulnerable.

Part 8: Coping Strategies for Investors

8.1 Diversification

Investors hedge against rising yields by diversifying into value stocks, commodities, and sectors benefiting from higher rates (like banks).

8.2 Global Allocation

Allocating across geographies can help. For instance, some Asian and European stocks may perform better depending on currency moves and domestic cycles.

8.3 Use of Derivatives

Investors use interest-rate futures, options, and currency hedges to manage risks from rising yields.

8.4 Tactical Shifts

Moving from growth to value, reducing exposure to high-duration equities, and increasing allocation to inflation-hedged assets are common strategies.

Part 9: Future Outlook

The long-term trajectory of US Treasury yields depends on:

US fiscal deficits and borrowing needs.

Federal Reserve policy normalization.

Global inflation cycles.

Geopolitical shifts in demand for US Treasuries (e.g., de-dollarization trends).

For global equities, this means heightened sensitivity to yield cycles. Investors must closely monitor not only the direction but also the pace of yield movements. Gradual increases may be absorbed, but sharp spikes usually destabilize global equities.

Conclusion

The relationship between US Treasury yields and global equities is one of the most powerful forces in financial markets. Rising yields act as a tightening mechanism, reducing equity valuations, increasing corporate borrowing costs, triggering capital outflows from emerging markets, and strengthening the US dollar. The effects vary across sectors and geographies—hurting growth stocks, real estate, and emerging markets, while benefiting banks and certain value-oriented sectors.

History shows that equity markets can tolerate moderate, steady increases in yields, particularly when driven by strong growth. However, rapid spikes often cause global turbulence. For investors, understanding these dynamics and positioning portfolios accordingly is crucial.

In essence, rising US Treasury yields are not just an American story—they are a global story, shaping equity performance from Wall Street to Mumbai, from Frankfurt to Tokyo.

Major Global Stock Exchanges1. The Concept of a Stock Exchange

A stock exchange is an organized marketplace where securities such as stocks, bonds, derivatives, and exchange-traded funds (ETFs) are bought and sold. Exchanges are critical for:

Capital Formation: Companies raise funds for growth by issuing shares.

Liquidity: Investors can buy or sell securities quickly.

Price Discovery: Supply and demand set fair market prices.

Transparency & Regulation: Exchanges ensure fair trading practices.

Economic Indicators: Indexes like the S&P 500 or Nikkei 225 reflect economic health.

The global network of stock exchanges creates an interconnected system where money flows seamlessly across borders, influencing trade, investment, and growth.

2. Major Global Stock Exchanges by Region

A. North America

1. New York Stock Exchange (NYSE) – USA

Founded: 1792 (Buttonwood Agreement).

Market Capitalization: Over $30 trillion (2025 est.), making it the world’s largest exchange.

Trading Mechanism: Hybrid system – both electronic and floor-based trading.

Famous Index: Dow Jones Industrial Average (DJIA).

The NYSE is synonymous with Wall Street and represents global capitalism. Home to giants like Apple, Microsoft, and JPMorgan Chase, it attracts global investors. The NYSE’s prestige often means companies choose it over others for IPOs, despite higher listing requirements.

2. NASDAQ – USA

Founded: 1971.

Market Capitalization: Approx. $25 trillion.

Specialty: First electronic exchange, known for tech-heavy listings.

Famous Index: NASDAQ Composite, NASDAQ-100.

NASDAQ revolutionized trading with full automation. Today, it’s the home of global technology leaders such as Alphabet, Amazon, Tesla, and Meta. Its growth is tied to the tech boom, and its influence extends worldwide in shaping technology valuations.

3. Toronto Stock Exchange (TSX) – Canada

Founded: 1852.

Market Capitalization: Around $3.5 trillion.

Specialty: Strong focus on energy, mining, and natural resources.

Canada’s TSX is crucial for global commodities and resource-based industries. It provides capital to firms in oil, gold, and base metals, making it a hub for resource-dependent economies.

B. Europe

4. London Stock Exchange (LSE) – UK

Founded: 1801.

Market Capitalization: Approx. $4 trillion.

Famous Index: FTSE 100.

Historically, the LSE was the world’s most important exchange before the rise of the NYSE. Today, despite Brexit challenges, it remains a global financial center, attracting listings from Europe, Africa, and Asia. It also owns Borsa Italiana and is a hub for international debt securities.

5. Euronext – Pan-European

Founded: 2000 (merger of Amsterdam, Brussels, and Paris exchanges).

Market Capitalization: Approx. $7 trillion.

Famous Index: Euronext 100.

Euronext is Europe’s largest stock exchange, spanning multiple countries including France, the Netherlands, Belgium, Ireland, Italy, and Portugal. Its integrated platform enhances cross-border trading and investment opportunities.

6. Deutsche Börse (Frankfurt Stock Exchange) – Germany

Founded: 1585.

Market Capitalization: Over $2.5 trillion.

Famous Index: DAX 40.

Located in Frankfurt, Germany’s financial hub, Deutsche Börse is vital for Europe’s largest economy. It specializes in advanced trading systems and derivatives via Eurex.

7. SIX Swiss Exchange – Switzerland

Founded: 1850s.

Market Capitalization: Approx. $2 trillion.

Specialty: Banking and pharmaceuticals (Nestlé, Roche, Novartis).

The Swiss Exchange benefits from Switzerland’s strong banking tradition and reputation for stability. It attracts international investors seeking security.

C. Asia-Pacific

8. Tokyo Stock Exchange (TSE) – Japan

Founded: 1878.

Market Capitalization: Over $6 trillion.

Famous Index: Nikkei 225, TOPIX.

TSE is Asia’s largest stock exchange. Japan’s economy and corporate sector (Toyota, Sony, SoftBank) rely heavily on its capital markets. The TSE’s reforms in governance and technology have improved global investor confidence.

9. Shanghai Stock Exchange (SSE) – China

Founded: 1990 (modern re-establishment).

Market Capitalization: Over $7 trillion.

Famous Index: SSE Composite.

The SSE is China’s largest exchange, playing a central role in financing its massive economy. It lists state-owned enterprises (SOEs) and large banks. While it is not fully open to foreign investors, schemes like Stock Connect have increased global participation.

10. Shenzhen Stock Exchange (SZSE) – China

Founded: 1990.

Market Capitalization: Over $5 trillion.

Specialty: Innovative and fast-growing tech companies.

Famous Index: ChiNext.

Often compared to NASDAQ, the SZSE specializes in smaller, high-growth firms. It plays a critical role in China’s startup ecosystem.

11. Hong Kong Stock Exchange (HKEX) – Hong Kong

Founded: 1891.

Market Capitalization: Around $5 trillion.

Famous Index: Hang Seng Index.

HKEX is a gateway for global investors into China. Many Chinese firms, including Alibaba and Tencent, are listed here. Despite political tensions, HKEX remains influential due to its global connectivity.

12. Bombay Stock Exchange (BSE) – India

Founded: 1875 (Asia’s oldest).

Market Capitalization: Over $4 trillion.

Famous Index: Sensex 30.

The BSE is Asia’s first exchange and remains a vital part of India’s fast-growing economy. It has deep liquidity, electronic systems, and diverse listings.

13. National Stock Exchange (NSE) – India

Founded: 1992.

Market Capitalization: Over $4.5 trillion.

Famous Index: Nifty 50.

NSE revolutionized Indian trading by introducing electronic systems. Today, it is larger than BSE in trading volume and derivatives, making it India’s most important exchange.

14. Australian Securities Exchange (ASX) – Australia

Founded: 1987 (merger of state exchanges).

Market Capitalization: Around $2 trillion.

Specialty: Mining, energy, finance.

The ASX plays a regional role, particularly in commodities and finance, while also experimenting with blockchain-based settlement systems.

D. Middle East & Emerging Markets

15. Saudi Stock Exchange (Tadawul) – Saudi Arabia

Founded: 2007 (modern structure).

Market Capitalization: Approx. $3 trillion.

Famous Listing: Saudi Aramco (world’s largest IPO).

Tadawul is the largest exchange in the Middle East, central to Vision 2030 reforms aimed at diversifying the Saudi economy.

16. Johannesburg Stock Exchange (JSE) – South Africa

Founded: 1887.

Market Capitalization: Around $1 trillion.

The JSE dominates Africa, serving mining and resource companies. It connects African economies with global investors.

17. B3 (Brasil Bolsa Balcão) – Brazil

Founded: 1890, merged into B3 in 2017.

Market Capitalization: Approx. $1.2 trillion.

B3 is Latin America’s largest exchange, crucial for Brazil’s energy, agriculture, and financial sectors.

3. Comparative Importance of Global Stock Exchanges

Largest by Market Cap: NYSE, NASDAQ, SSE, TSE, Euronext.

Tech-Focused: NASDAQ, SZSE, NSE.

Commodities-Driven: TSX, JSE, ASX.

Regional Leaders: Tadawul (Middle East), JSE (Africa), B3 (Latin America).

Exchanges compete globally for IPOs and liquidity. Companies often cross-list (e.g., Alibaba on NYSE and HKEX) to access multiple investor bases.

4. The Future of Stock Exchanges

Digital Transformation: Blockchain and AI are reshaping settlement and fraud detection.

Globalization vs Fragmentation: While some exchanges integrate, geopolitical tensions may cause fragmentation.

Sustainability: ESG-focused investing is influencing exchange policies.

Retail Investor Boom: Platforms like Robinhood and Zerodha are increasing participation.

Competition from Private Markets: Startups may prefer private funding over IPOs.

Conclusion

Global stock exchanges are more than marketplaces—they are economic nerve centers. Each exchange has unique strengths: NYSE’s prestige, NASDAQ’s tech dominance, LSE’s international reach, TSE’s resilience, SSE’s link to China’s growth, and NSE’s role in emerging markets. Together, they form an interconnected web driving global finance.

In the future, exchanges will adapt to technology, regulation, and shifting capital flows, but their fundamental purpose—channeling capital into productive use—will remain unchanged.

Master TradingView Like a Pro – Tools, Alerts, and Hidden Gems!Are you really using everything TradingView has to offer?